Disposable Blood Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

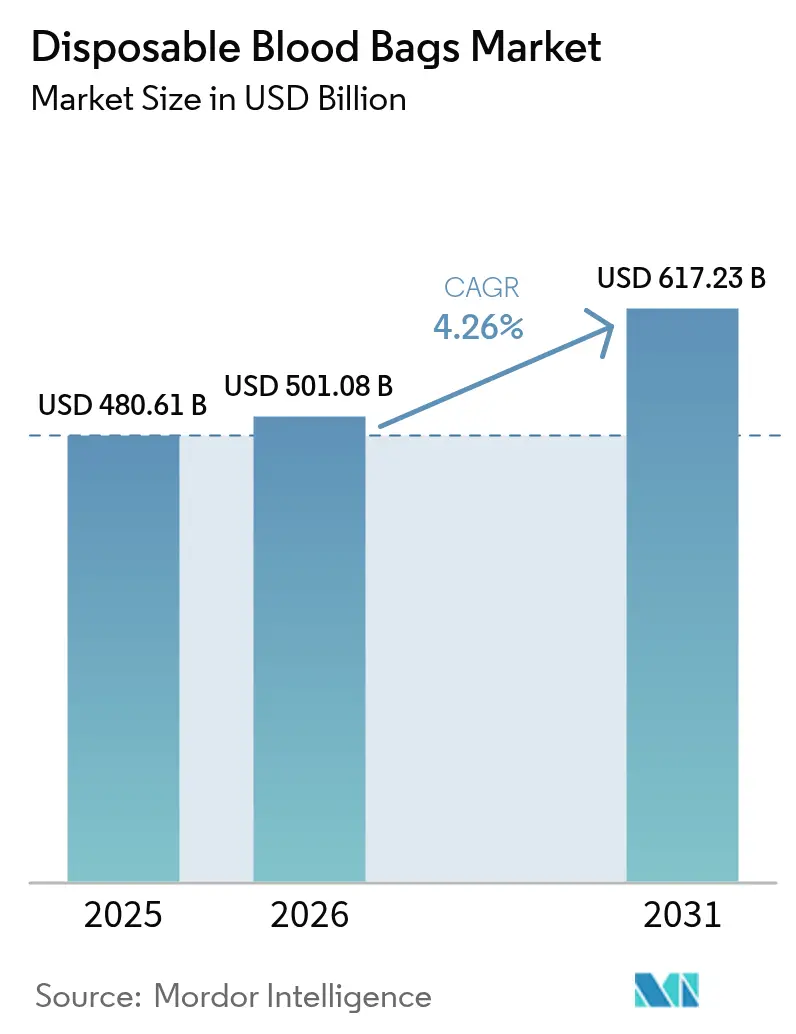

| Market Size (2026) | USD 501.08 Billion |

| Market Size (2031) | USD 617.23 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Blood Bags Market Analysis by Mordor Intelligence

The disposable blood bags market size is expected to grow from USD 480.61 million in 2025 to USD 501.08 million in 2026 and is forecast to reach USD 617.23 million by 2031 at 4.26% CAGR over 2026-2031. A confluence of demographic aging, expanding surgical volumes, and technology-enabled quality controls is strengthening demand for sterile, single-use collection and storage systems. Government programs that digitalize donation networks, coupled with investments in cold-chain logistics and drone delivery, are widening access in lower-income settings. Hospitals are accelerating adoption of pathogen-reduced multi-bag configurations that maximize component yield and minimize contamination risk. Simultaneously, regulatory pressure to eliminate DEHP plasticizer is stimulating rapid material innovation and strategic collaborations among incumbents.

Key Report Takeaways

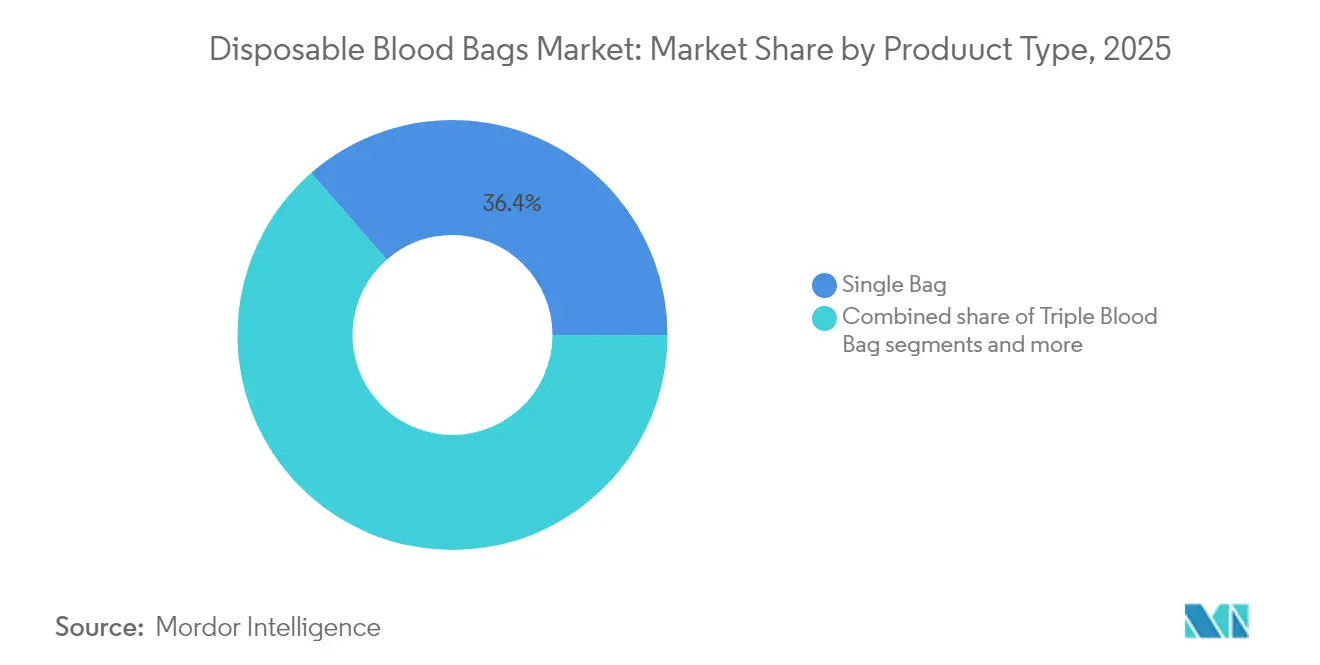

- By product type, single blood bags led with 36.42% of disposable blood bags market share in 2025, while quadruple bags recorded the fastest 4.34% CAGR through 2031.

- By material, PVC DEHP products accounted for 62.54% of the disposable blood bags market size in 2025; PVC DEHP-free alternatives are expanding at a 4.47% CAGR to 2031.

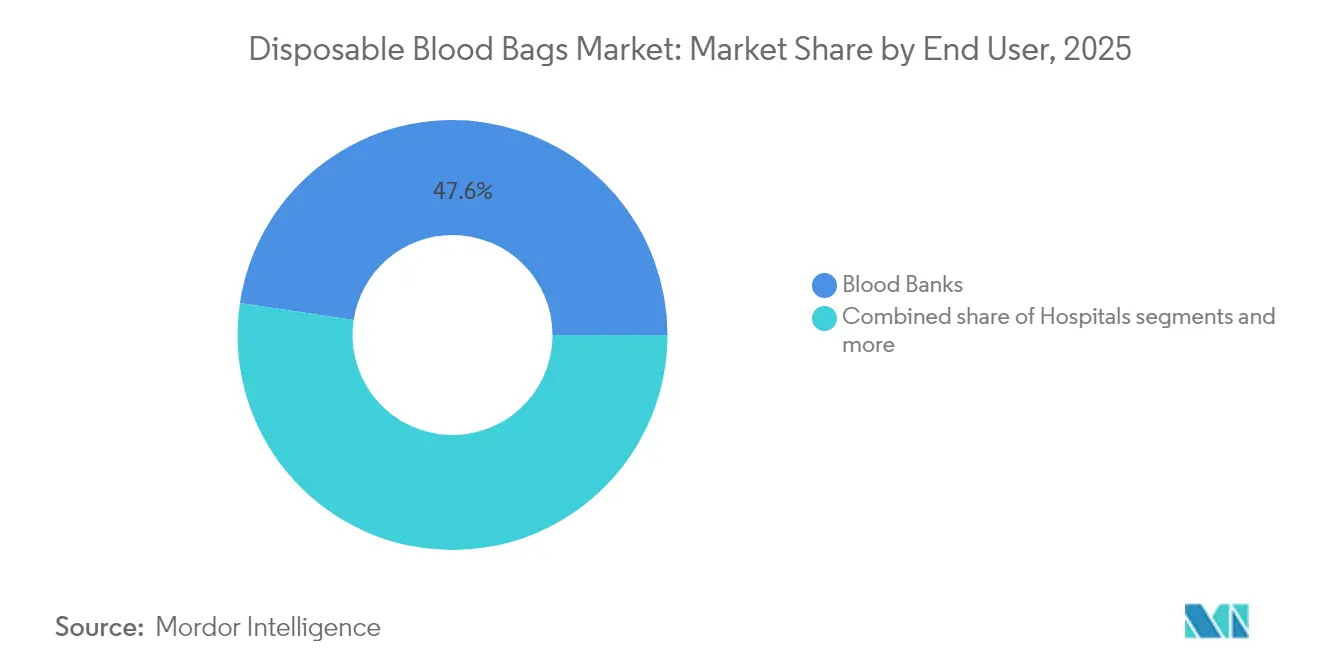

- By end user, blood banks held 47.62% share of the disposable blood bags market size in 2025, whereas hospitals are advancing at a 4.66% CAGR through 2031.

- By application, collection captured 55.14% of the disposable blood bags market size in 2025 and processing is progressing at a 4.78% CAGR through 2031.

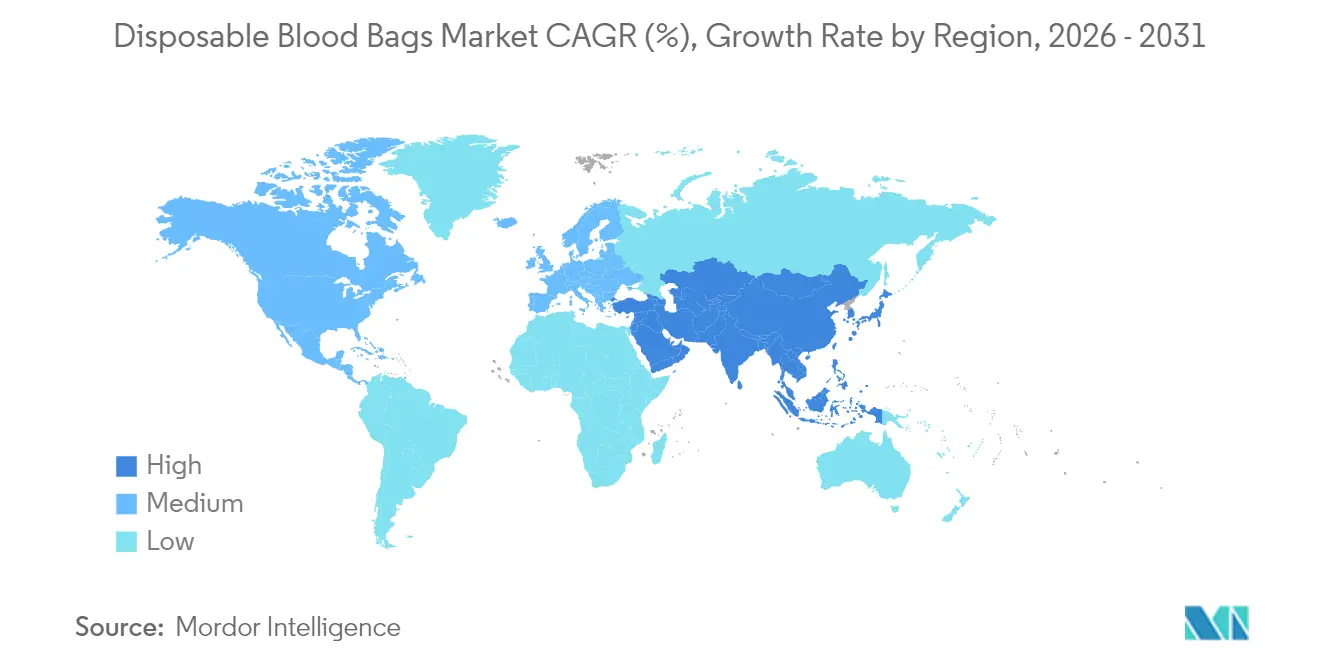

- By geography, North America commanded 38.64% share in 2025; Asia-Pacific is projected to post the quickest 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Disposable Blood Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedures & transfusion rates in aging populations | 1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Increasing prevalence of trauma & chronic diseases requiring blood components | 0.9% | Global, with higher impact in Asia-Pacific & LMICs | Medium term (2-4 years) |

| Government initiatives to improve voluntary donation & cold-chain infrastructure | 0.8% | Asia-Pacific core, spill-over to MEA & Latin America | Medium term (2-4 years) |

| Shift toward single-use infection-controlled products | 0.7% | Global, led by North America & EU regulatory frameworks | Short term (≤ 2 years) |

| Emerging adoption of non-PVC eco-friendly bags | 0.5% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Mobile donation units expanding component therapy in LMICs | 0.4% | LMICs, particularly Sub-Saharan Africa & South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising surgical procedures & transfusion rates in aging populations

The median age of surgical patients climbed from 56 to 59 years between 2008 and 2020, and forecasts indicate a further increase to 61.5 years by 2030. Elderly individuals often present lower preoperative hematocrit, triggering higher transfusion frequency across orthopedic, cardiovascular, and oncologic specialties. Cardiovascular surgery alone consumed 10–15% of all U.S. blood components in 2024, underscoring a durable demand base. Age-linked comorbidities also elevate complications, prompting hospitals to stock greater inventories of pathogen-reduced platelets and leukoreduced red cells. ISO 13485 and FDA quality mandates compel manufacturers to deliver containers that safeguard product potency for this vulnerable cohort. Collectively, these clinical realities reinforce sustained consumption in the disposable blood bags market.

Increasing prevalence of trauma & chronic diseases requiring blood components

Trauma remains a top cause of mortality among working-age adults, driving acute demand for type-specific packed red cells in emergency rooms across Asia-Pacific urban corridors. Chronic conditions such as sickle-cell disease, thalassemia, and certain cancers now necessitate frequent transfusions, with Asia accounting for more than half of global hematologic disease burden[1]Source: World Health Organization, “Guidance on Implementation of a Quality System in Blood Establishments,” iris.who.int . Expanded insurance coverage and economic growth are improving procedure accessibility, thereby elevating transfusion volumes in mid-tier hospitals. Mobile component therapy programs in LMICs enable remote trauma centers to receive platelets within eight minutes via drone dispatch, compressing the traditional 55-minute ground delivery window. As incidence of non-communicable diseases rises, so does the requirement for consistent, contamination-free bag systems that meet 21 CFR Part 640 standards. These dynamics continually amplify growth in the disposable blood bags market.

Government initiatives to improve voluntary donation & cold-chain infrastructure

India’s e-Raktkosh digital platform now coordinates 4,263 licensed blood centers, accelerating stock visibility and donor mobilization[2]Source: Ministry of Health and Family Welfare, “Blood Transfusion Services,” dghs.mohfw.gov.in . The United Kingdom targets 25% domestic plasma self-sufficiency by 2025, pledging to save USD 12.6 million annually through import substitution. National AIDS Control Programme-funded mobile units in India boosted voluntary donation rates from 8.5% to 14.39% within two years. Simultaneously, WHO quality-system guidance steers harmonized accreditation, ensuring that scale-up does not compromise safety. Investments in smart refrigerators and GPS-linked cold boxes curtail waste from temperature excursions, while drone transport pilots demonstrate rapid, cost-efficient logistics that expand reach to under-served regions. Consequently, public policy support is bolstering structural demand across the disposable blood bags market.

Shift toward single-use infection-controlled products

COVID-19 catalyzed a strict infection-prevention culture, propelling hospitals to adopt hermetically sealed, single-use blood bag sets that eliminate cross-contamination risk. The FDA’s 2024 guidance on buffy-coat processing underscores disposable components, reinforcing market adoption. Automated systems such as Terumo’s Reveos reduce manual steps from 26 to 9, minimize touchpoints, and integrate single-use tubing, thereby ensuring sterility and curtailing batch-to-batch variability. Hospitals report fewer transfusion-transmitted infection investigations after transitioning to all-in-one disposable sets that comply with 21 CFR 864.9115 container standards. ISO-aligned quality records further document reduced error rates, validating the tangible clinical and operational benefits that underpin sustained expansion in the disposable blood bags market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining birth rates & autologous transfusion techniques in developed markets | -0.8% | North America & Europe, emerging in East Asia | Long term (≥ 4 years) |

| Stringent regulatory hurdles for new bag materials | -0.6% | Global, with stricter enforcement in North America & EU | Medium term (2-4 years) |

| Supply-chain dependence on medical-grade PVC resin price volatility | -0.5% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Patient Blood Management (PBM) programs reducing transfusion volumes | -0.7% | North America & Europe core, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining birth rates & autologous transfusion techniques in developed markets

Fertility rates in North America and Europe fell below replacement levels, narrowing the obstetric transfusion pool that historically generated stable whole-blood demand. Concurrently, cell-salvage devices reclaim intraoperative blood, allowing orthopedic and cardiac surgeons to return autologous red cells to patients, thus lowering allogeneic usage. Hospitals deploying salvage units recorded 15–30% reductions in donor blood requests during major joint replacements, easing pressure on inventory levels. Although salvage bags still require sterile disposables, volumes are significantly smaller than standard donation sets. Long-term demographic contraction and surgical technology overlap diminish future growth momentum, especially in mature markets of the disposable blood bags industry.

Patient Blood Management (PBM) programs reducing transfusion volumes

Comprehensive PBM rollouts in tertiary centers cut red-cell usage by up to 39%, delivering annual savings exceeding USD 2 million per hospital. National PBM certification launched by The Joint Commission in 2025 standardizes restrictive transfusion thresholds at 7–8 g/dL for stable adults. Improved cross-match-to-transfusion ratios—from 15:1 to 1.5:1—signal heightened efficiency and lower discard rates. While PBM creates operational excellence, it directly suppresses unit demand, placing a moderating effect on CAGR projections in the disposable blood bags market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Component separation drives multi-bag adoption

Single bags retained a 36.42% lead in 2025 as cost-effective whole-blood collection tools for emergent situations and rural drives, anchoring baseline volume in the disposable blood bags market. The disposable blood bags market size for single sets, however, is growing more slowly than multi-chamber configurations as hospitals shift toward component therapy. Quadruple bags, expanding at a 4.34% CAGR, accommodate concurrent preparation of packed red cells, plasma, platelets, and cryoprecipitate, maximizing therapeutic value per donation. Automated Reveos platforms integrate with quadruple kits to standardize yields, delivering 150 plasma ml and ≥3×10⁹ platelets per unit, an advantage over manual processes.

Growing recognition of cost-per-therapy metrics strengthens multi-bag appeal among reimbursement-driven hospitals. Double and triple bags maintain relevance in mid-tier facilities that perform moderate platelet demand yet face budgetary constraints. Penta sets, though niche, support advanced pathogen inactivation and add-on filtration, attracting specialized blood centers. Across all variants, ISO 8363 burst-strength criteria and 21 CFR Part 640 sterility mandates govern design, compelling suppliers to refine barrier properties while curbing plasticizer migration. These evolving clinical and compliance parameters ensure sustained product mix evolution within the disposable blood bags market.

Blood Transfer Bags Segment in Global Disposable Blood Bags Market

The blood transfer bags segment holds the remaining market share and serves as a crucial component in the blood banking and transfusion process. These bags are specifically designed for transporting blood components between collection points and healthcare facilities, ensuring safe and contamination-free transfer of blood products. The segment's growth is supported by the increasing adoption of component separation techniques and the rising need for efficient blood component transportation systems in healthcare settings. The demand is further bolstered by the growing network of blood banks and transfusion centers, particularly in developing regions, along with the increasing emphasis on maintaining proper cold chain management during blood product transportation. This segment is an integral part of the blood transfer bags market within the broader disposable medical bag market.

By Material: DEHP-free transition accelerates safety innovation

PVC DEHP bags dominated with 62.54% market share in 2025, benefiting from entrenched production expertise and proven hemocompatibility. Yet toxicological scrutiny of DEHP’s endocrine disruption has prompted California to legislate a medical-device ban by 2030, albeit exempting blood bags, signaling a progressive regulatory tide. The disposable blood bags market size tied to PVC DEHP-free formulations is advancing 4.47% CAGR as suppliers adopt DINCH plasticizer or EVA copolymers. Studies reveal DINCH bags sustain 24-day red-cell viability with lower hemolysis compared with DEHP-laden controls.

R&D pipelines also explore cyclo-olefin polymers that deliver ultraviolet clarity for visual inspection while resisting lipid adsorption. EU MDR and forthcoming SoHO regulation require exhaustive biocompatibility and post-market surveillance, lengthening approval timelines yet rewarding early movers with compliance credibility. Manufacturers such as Fresenius Kabi are partnering with pathogen-inactivation firms to bundle safety features into new bag lines, differentiating beyond material alone. Material innovation is therefore a central vector in securing competitive advantage across the disposable blood bags market.

By End User: Hospital integration transforms blood management

Blood banks contributed 47.62% revenue in 2025 by aggregating collection, testing, and regional distribution for multi-hospital networks. Nonetheless, hospital demand is climbing at a 4.66% CAGR as point-of-care advanced therapy manufacturing gains regulatory approval. The disposable blood bags industry increasingly serves operating rooms that perform final cryoprecipitate concentration or cell-therapy enrichment bedside, reducing lead times and wastage.

Surgeons integrating PBM algorithms prefer multi-bag systems with integrated leukoreduction to align with restrictive thresholds. Diagnostic centers form a smaller but steady segment, utilizing mini-bags in cross-match labs and chronic disease clinics. Emergency medical services adopt lightweight apheresis-capable kits for disaster response, a niche yet visible sub-market. As hospital laboratories assume broader manufacturing roles, vendor qualification criteria now include performance metrics on in-hospital centrifuge compatibility and closed-system integrity. This deepening clinical integration cements hospital influence over product specifications within the disposable blood bags market.

By Application: Processing innovation enhances blood safety

Collection remained the anchor with 55.14% share in 2025 thanks to ongoing voluntary and replacement donation programs worldwide. Yet processing is charting the quickest 4.78% CAGR as healthcare systems seek to extend shelf life and mitigate pathogen risk. The disposable blood bags market share for processing kits is rising on the back of leukoreduction, buffy-coat fractionation, and pathogen inactivation modules that ship with ready-to-connect tubing and filters.

Transportation and storage retain relevance, especially in military and disaster-relief logistics where ruggedized, EVA-lined bags withstand temperature fluctuation. Automated centrifuge compatibility enhances throughput from 60 to 120 units per hour, reducing labor cost per component by 35% in high-volume centers. FDA guidances finalized in 2024 encourage integrated systems that perform collection, processing, and storage within a sealed loop, eliminating open transfers and lowering bacterial contamination incidence. These technological advances continue to elevate processing applications as a primary growth locus for the disposable blood bags market.

Geography Analysis

North America retained a commanding 38.64% share in 2025, underpinned by robust reimbursement, widespread PBM adoption, and stringent FDA oversight that favors premium, innovative bag systems. California’s forthcoming DEHP device ban has already influenced procurement teams to pilot DINCH and EVA alternatives, accelerating material migration timelines across U.S. hospital groups. Canada’s national science program funds research on pediatric-safe plasticizers, broadening clinical evidence that informs purchasing decisions nationwide.

Asia-Pacific represents the fastest-growing territory with a projected 4.92% CAGR through 2031 as urbanizing populations drive surgical demand and governments invest in digital blood-management infrastructure. Terumo’s USD 15 million localization initiative in Hangzhou illustrates how domestic manufacturing can trim import tariffs and bolster regional supply security. India’s mobile donation units now service remote districts, while drone corridors between regional centers and trauma hubs slash delivery lead times by 85%. These capacity expansions feed sustained momentum in the disposable blood bags market.

Europe exhibits measured growth, sustained by replacement of legacy DEHP stocks and harmonization under the SoHO regulation effective August 2027. The United Kingdom’s domestic plasma initiative seeks 80% albumin self-reliance, spurring investments in advanced collection kits and cold-chain upgrades. South America and the Middle East-Africa region present untapped opportunity where WHO estimates a 102-million-unit annual shortfall. International collaborations aim to introduce compact, solar-powered refrigeration and simplified multi-bag platforms suited for resource-limited environments. Collectively, regional heterogeneity in regulation, infrastructure, and clinical practice shapes a nuanced, yet steadily expanding disposable blood bags market.

Competitive Landscape

The disposable blood bags market shows moderate concentration, with legacy manufacturers leveraging scale, automation, and regulatory track records to preserve positioning. Terumo, Fresenius Kabi, and Haemonetics collectively account for a substantial share, benefiting from vertically integrated resin compounding, in-house extrusion, and global field-service networks. GVS’s USD 67.8 million acquisition of Haemonetics’ whole-blood assets in 2025 broadened its access to U.S. and Mexican manufacturing, signaling active portfolio rationalization among incumbents.

Technology leadership differentiates competitors: Terumo’s Reveos platform integrates optical sensor-based yield algorithms; Fresenius Kabi focuses on non-DEHP materials paired with pathogen inactivation; Haemonetics scales its apheresis line to support high-margin immunotherapy collection. Artificial-intelligence inventory systems deployed by select blood banks optimize expiry rotation, reducing outdates by 20% and indirectly boosting demand for specialized storage bag variants. Emerging Asian suppliers leverage cost efficiencies but face steep ISO 13485 and MDR conformity hurdles, slowing entry into premium markets.

Strategic collaborations are deepening: Sanquin’s ten-year deal to roll out Reveos across 400,000 annual donations streamlines European processing output. Fresenius aligns with Cerus to co-package INTERCEPT pathogen-inactivation sleeves, offering an end-to-end safety bundle attractive to PBM-oriented hospitals. Meanwhile, material innovators partner with petrochemical firms to secure consistent DINCH supply, mitigating resin price volatility. Competitive intensity is poised to heighten as regulatory deadlines on DEHP draw nearer, nudging all players to accelerate eco-friendly transitions within the disposable blood bags market.

Disposable Blood Bags Industry Leaders

Fresenius SE & Co. KGaA

Haemonetics Corporation

MacoPharma

Teleflex Incorporated

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Haemonetics Corporation completed the sale of its whole-blood assets to GVS S.p.A for USD 67.8 million, refocusing on apheresis solutions

- November 2024: Terumo Blood and Cell Technologies announced USD 15 million investment in China localization to manufacture Trima Accel and Spectra Optia systems

Global Disposable Blood Bags Market Report Scope

As per the report's scope, disposable blood bags are disposable bio-medical devices used for collecting, storing, transporting, and transfusion blood and blood components. The disposable blood bags market is segmented by type of bag, end-user, and geography. By type of bag, the market is segmented into blood collection bags (single blood bags, double blood bags, triple blood bags, and quadruple blood bags) and blood transfusion bags. By end users, the market is segmented into blood banks, hospitals, non-government organizations, and other end users. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Single Blood Bag |

| Double Blood Bag |

| Triple Blood Bag |

| Quadruple Blood Bag |

| Penta Blood Bag |

| PVC DEHP |

| PVC DEHP-free |

| Non-PVC (EVA & others) |

| Hospitals |

| Blood Banks |

| Diagnostic Centers |

| Others |

| Collection |

| Transportation / Storage |

| Processing (Leukoreduction, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value, USD million) | Single Blood Bag | |

| Double Blood Bag | ||

| Triple Blood Bag | ||

| Quadruple Blood Bag | ||

| Penta Blood Bag | ||

| By Material (Value, USD million) | PVC DEHP | |

| PVC DEHP-free | ||

| Non-PVC (EVA & others) | ||

| By End User (Value, USD million) | Hospitals | |

| Blood Banks | ||

| Diagnostic Centers | ||

| Others | ||

| By Application (Value) | Collection | |

| Transportation / Storage | ||

| Processing (Leukoreduction, etc.) | ||

| By Geography (Value, USD million) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the disposable blood bags market?

The disposable blood bags market size reached USD 501.08 million in 2026 and is projected to hit USD 617.23 million by 2031.

Which region leads global demand for disposable blood bags?

North America held the largest 38.64% share in 2025, driven by strict FDA regulations and advanced healthcare infrastructure.

Which product segment is expanding the fastest?

Quadruple blood bags are registering the highest 4.34% CAGR thanks to their ability to separate multiple components from a single donation.

Why are DEHP-free materials gaining momentum?

Regulatory scrutiny of DEHP's toxicity and upcoming bans are spurring hospitals to adopt DINCH-plasticized or EVA bags that maintain blood quality without endocrine risks.

How do Patient Blood Management programs affect unit demand?

PBM initiatives have cut red-cell transfusions by up to 39%, prompting hospitals to favor high-efficacy bags that support component therapy with fewer overall units.

What major deal reshaped the competitive landscape recently?

In January 2025, GVS acquired Haemonetics whole-blood assets for USD 67.8 million, expanding its manufacturing footprint in the Americas.

Page last updated on: