Medical Specialty Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

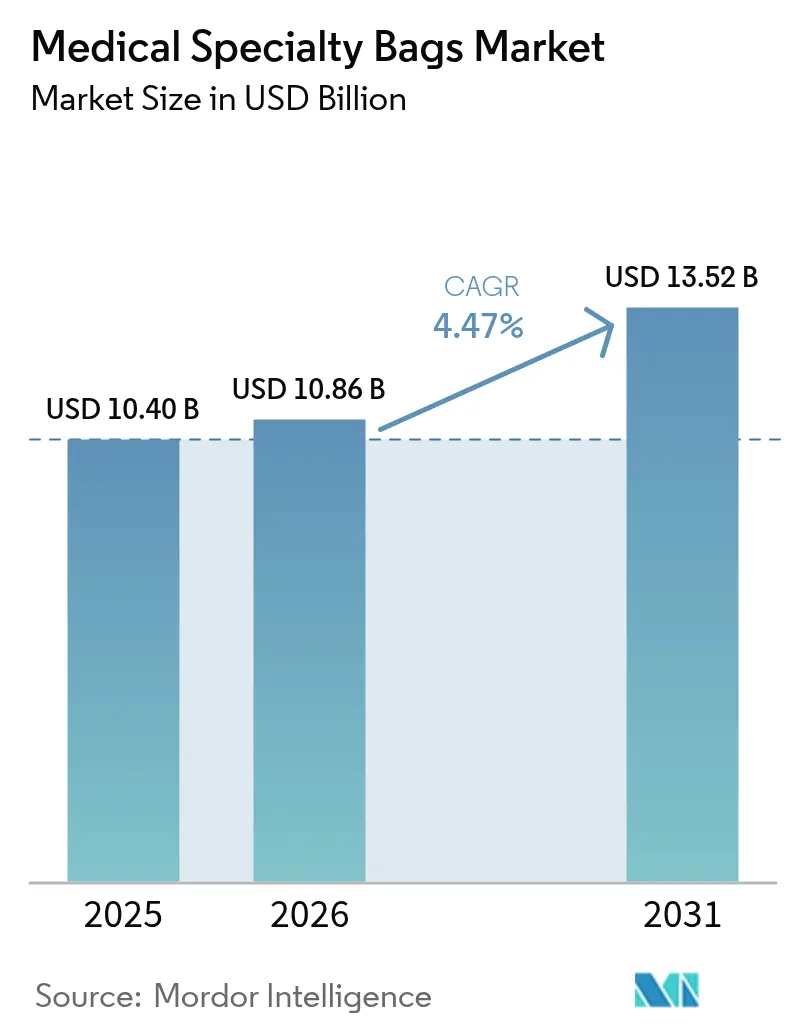

| Market Size (2026) | USD 10.86 Billion |

| Market Size (2031) | USD 13.52 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Specialty Bags Market Analysis by Mordor Intelligence

medical specialty bags market size in 2026 is estimated at USD 10.86 billion, growing from 2025 value of USD 10.40 billion with 2031 projections showing USD 13.52 billion, growing at 4.47% CAGR over 2026-2031. As hospital networks decentralize care and regulators tighten sustainability rules, demand pivots toward lightweight, recyclable pouches and at-home treatment kits. Long-standing suppliers respond through green chemistry investments, while newer entrants concentrate on single-indication products that lessen complication rates. Rising colorectal cancer incidence, wider insurance coverage for home dialysis, and the growth of ambulatory surgical centers collectively reinforce the upward trajectory of the medical specialty bags market. Cost headwinds from resin price swings and extended polymer approval cycles temper, but do not derail, the sector’s expansion.

Key Report Takeaways

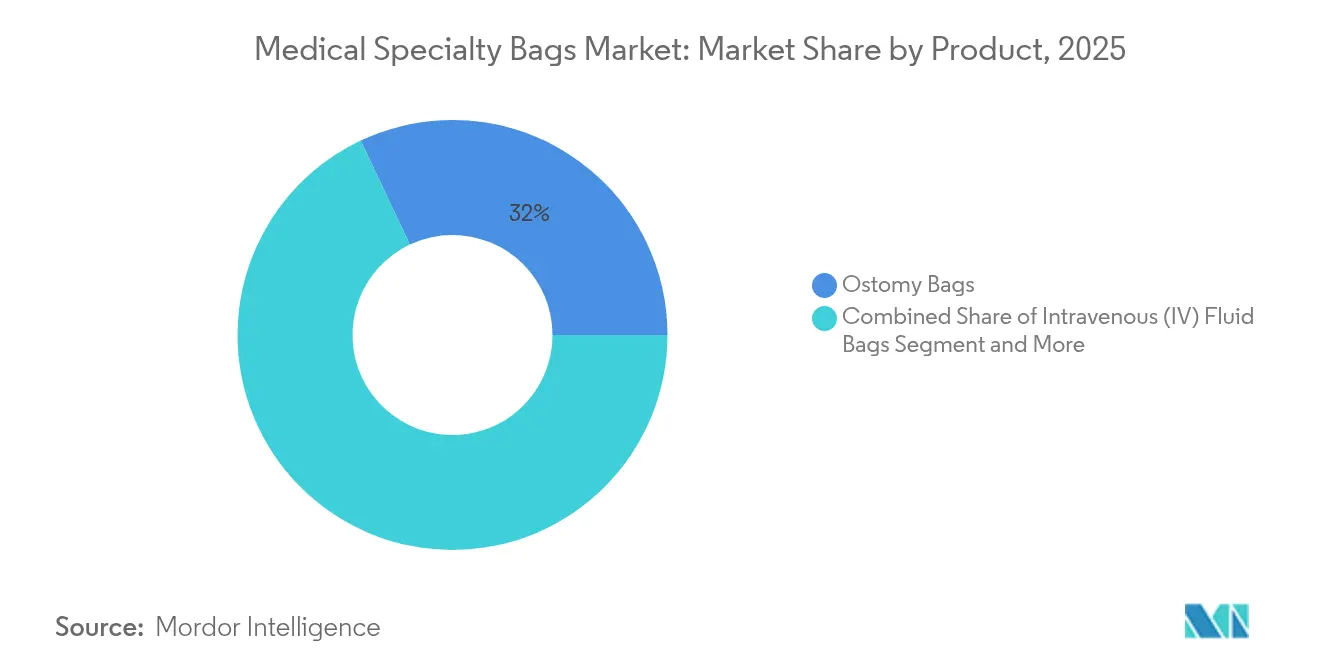

- By product category, ostomy bags held 32.02% of the medical specialty bags market share in 2025; Continuous Ambulatory Peritoneal Dialysis (CAPD) bags are advancing at an 8.23% CAGR through 2031.

- By material, polyvinyl chloride (PVC) accounted for 56.12% of the medical specialty bags market size in 2025, whereas bio-based and compostable polymers are projected to grow at an 11.21% CAGR between 2026-2031.

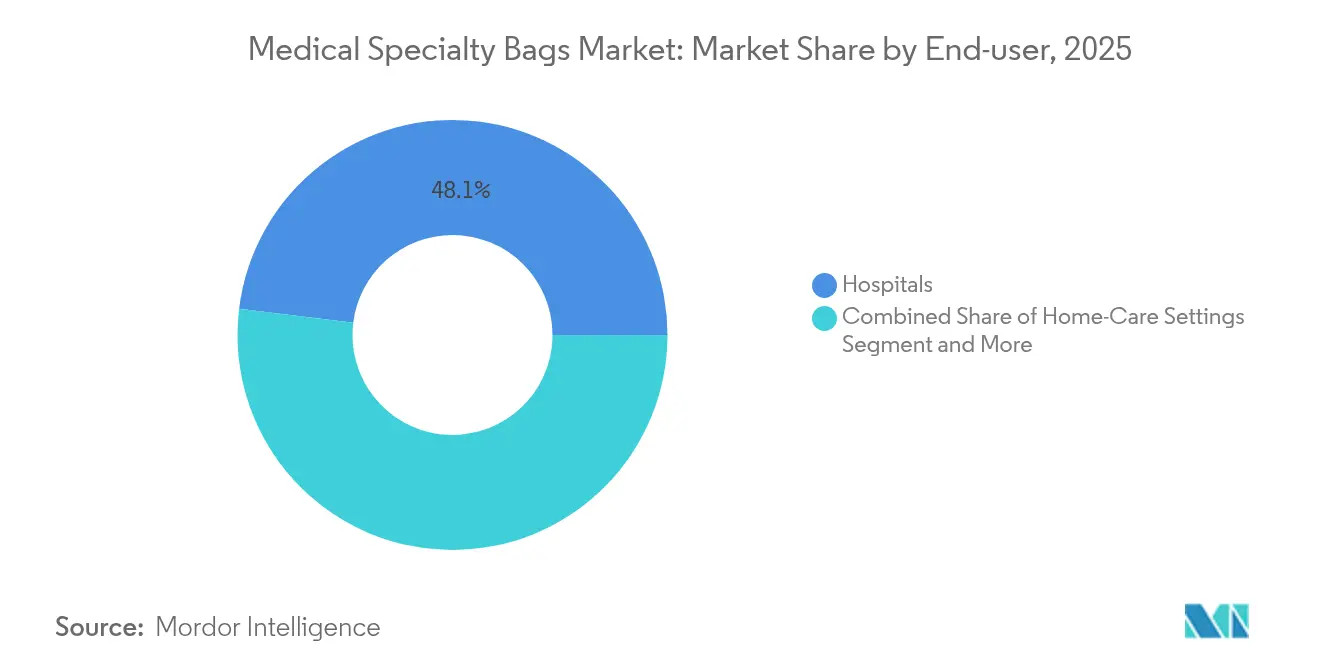

- By end-user, hospitals commanded 48.05% of the medical specialty bags market size in 2025, while the home-care channel is forecast to expand at a 10.12% CAGR over the same period.

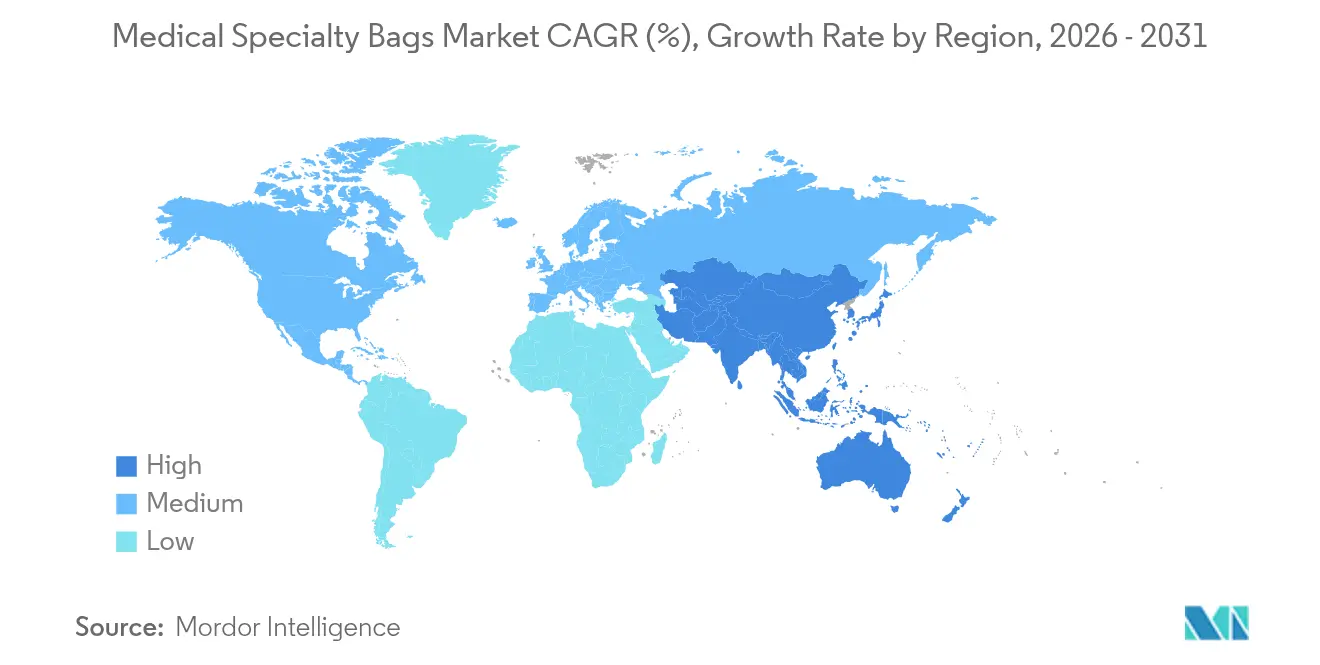

- By geography, North America contributed 35.82% of the medical specialty bags market share in 2025; Asia-Pacific is set to register an 8.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Specialty Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Chronic Diseases & Surgeries | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption Of CAPD For Home Renal Care | +0.8% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| Shift Toward PVC-Free & Recyclable Polymers | +0.6% | Europe & North America leading, global adoption | Long term (≥ 4 years) |

| Expansion Of Ambulatory & Day-Care Centers | +0.7% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| AI-Enabled Production Line Quality Control | +0.3% | Global, led by developed markets | Short term (≤ 2 years) |

| Hospital Demand For RFID-/IoT-Tagged Smart Bags | +0.2% | North America & Europe pilot programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases and Surgical Procedures

Colorectal cancer and inflammatory bowel disease prevalence continues to rise, elevating permanent and temporary stoma creation volumes worldwide. Hospitals standardize pouching systems to lower readmission risks, spurring orders for leak-resistant ostomy kits that improve peristomal skin integrity. Manufacturers add hydrocolloid and silicone coupling layers to boost wear-time and comfort, encouraging patient adherence. Integrated discharge programs train patients in pouch maintenance, further anchoring recurring demand within the medical specialty bags market. These developments sustain baseline growth even when elective procedure rates fluctuate.

Accelerated Uptake of CAPD for Home Renal Therapy

Public payers in Asia-Pacific and Latin America increasingly reimburse home-based dialysis to ease inpatient bed pressure and enhance quality of life. The Carry Life UF platform underscores how precise glucose titration can increase ultrafiltration and sodium removal, helping patients stay in target fluid ranges. Training apps and tele-monitoring keep complication rates low, prompting clinicians to recommend Continuous Ambulatory Peritoneal Dialysis earlier in the treatment journey. Producers of CAPD solution and drainage bags benefit from kit bundling policies, which lock in multi-year supply contracts. Consequently, CAPD continues to be the fastest-growing product line inside the medical specialty bags market.

Transition to PVC-Free and Recyclable Polymers

Healthcare systems in Europe and North America mandate greener product portfolios, driving trials of polyhydroxyalkanoates, polylactic acid, and polybutylene succinate. ConvaTec’s science-based emissions goals illustrate how life-cycle analyses now shape sourcing decisions. Early models show that biodegradable ostomy pouches can keep odor barriers intact while reducing incineration loads. To mitigate sterility risks, firms invest in low-temperature gamma-compatible additives. Regulatory bodies support progress by recognizing ASTM benchmarks for implant-grade lactide resins. As more hospitals issue “PVC-free” tenders, polymer transition programs move from pilot to scale.

Growth of Ambulatory Care Models and Digitalized Bag Solutions

Medicare spent USD 6.1 billion on ambulatory surgical center (ASC) services for 3.3 million fee-for-service beneficiaries in 2024, spotlighting a structural shift out of inpatient theaters[1]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” medpac.gov. ASCs prize pre-filled, bar-coded IV and irrigation bags that streamline room turnover and shrink drug compounding errors. Parallel advances in AI-assisted visual inspection and RFID-tagged supply tracking cut waste during high-volume orthopedic and gastroenterology lists. Device makers integrate near-field communication chips into drainage sets so staff can verify expiration and lot data with a tablet scan. These connected formats differentiate brands in a moderately fragmented medical specialty bags market while supporting real-time inventory analytics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement gaps in emerging economies | -0.4% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Long regulatory approval cycles for novel polymers | -0.3% | Global, strongest in Europe & North America | Medium term (2-4 years) |

| Volatile prices of medical-grade resins | -0.2% | Global supply chain | Short term (≤ 2 years) |

| Rising ESG scrutiny on single-use devices | -0.3% | Europe & North America, spreading worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Gaps in Emerging Economies

While procedure volumes climb, many public insurers in lower-income regions do not reimburse advanced ostomy or CAPD kits in full, forcing patients to self-pay significant portions. Out-of-pocket burdens reduce uptake of premium, skin-friendly materials, dampening revenue potential for global suppliers. Insurance modernization is under way, yet inflationary pressures on health budgets prolong subsidy negotiations. Local distributors often favor low-cost PVC options, stalling adoption of greener polymers. Over time, tiered pricing models and expanded private insurance pools may narrow the gap, but near-term drag on the medical specialty bags market persists.

Extended Regulatory Timelines for Novel Polymers

FDA quality system amendments effective February 2026 align with ISO 13485 but require file updates, site audits, and supplier re-qualification. Biocompatibility submissions now demand granular extractables and leachables data, lengthening lab test cycles. Similar rigor appears in European MDR technical files, adding workload for cross-regional launches. Resin cost spikes and heightened ESG reviews further complicate risk-benefit dossiers, especially for fully compostable materials. Collectively, these factors slow product refresh rates in the medical specialty bags market and elevate compliance costs for smaller producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Ostomy Dominance Meets CAPD Momentum

Ostomy bags remained the largest product line with a 32.02% medical specialty bags market share in 2025 as colorectal cancer surgeries and inflammatory bowel disease resections kept stoma creation steady. Hospitals favor multi-layer barrier films that prolong wear time, lowering peristomal dermatitis incidence and reducing unscheduled clinic visits. Leading OEMs supply closed-end and drainable variants in a wide size range, which drives bulk purchasing under group contracts. Continuous innovation, including 3-D-printed convex baseplates tailored to patient anatomy, improves seal integrity and boosts brand loyalty in the broader medical specialty bags market.

The CAPD bag portfolio, by contrast, posted the fastest expansion at an 8.23% CAGR, reflecting payer incentives for home renal therapies. New low-glucose solutions extend membrane life and widen treatment eligibility for diabetic populations. Ready-to-use twin-compartment bags minimize spiking steps, reducing peritonitis risk during exchanges. Regional manufacturing hubs in India and Vietnam shorten lead times and protect supply continuity during resin shortages. As clinical specialists’ education programs gain traction, CAPD adoption curves mirror insulin pump trends, signaling sustained growth beyond large urban centers.

By Material: PVC Leads Amid Sustainable Shift

PVC secured 56.12% of the medical specialty bags market size in 2025 thanks to established heat-sealing lines and favorable material costs. Phthalate-free grades now dominate new hospital contracts, indicating regulatory caution can coexist with PVC’s mechanical versatility. Nonetheless, institutional green-procurement frameworks push suppliers to disclose additive profiles and end-of-life disposal pathways. Producers respond by launching controlled-incineration buy-back schemes that monetize post-use waste streams, protecting share in the short term.

Bio-based and compostable polymers recorded an 11.21% CAGR, benefiting from hospital climate pledges and surgeon demand for lighter pouches. FDA acceptance of ASTM F2579-18 for lactide copolymers bolsters confidence in long-term material performance. Early-stage trials of polybutylene succinate ostomy wafers show comparable tensile properties versus traditional EVA, positioning eco-grades for wider rollout. Supply chain partners invest in multi-layer co-extrusion lines that merge biodegradable cores with moisture-barrier outer layers to preserve fluid integrity. As carbon accounting standards permeate tenders, the medical specialty bags market embraces a dual-material pathway that balances cost, performance, and sustainability.

By End-user: Hospitals Anchor, Home-Care Accelerates

Hospitals represented 48.05% of total revenue in 2025 as centralized purchasing departments prioritized bulk contracts covering ostomy, drainage, and IV solution bags. Clinical engineering teams favor suppliers with on-site consignment and near-zero back-order records, cementing long-term agreements. Integration of bar-coded medication labels into premix IV bags cuts adverse-drug-event rates, reinforcing hospital preference for turnkey offerings in the medical specialty bags market.

The home-care channel expanded at a 10.12% CAGR as chronic-care models moved dialysis, parenteral nutrition, and wound drainage into residential settings. Tele-coaching apps and sensor-equipped pouches empower patients to track output and spot early warning signs, supporting adherence. National payers reimburse equipment bundles that include starter kits, monthly refill deliveries, and disposal containers, creating predictable recurring revenue for manufacturers. Training content translated into multiple local languages underpins uptake in rural areas, while portable warmers enhance comfort during CAPD exchanges on the move. This convergence of technology, reimbursement, and patient empowerment sustains double-digit growth within the medical specialty bags market.

Geography Analysis

North America held 35.82% of global revenue in 2025, anchored by robust insurance coverage and rapid clearance pathways that speed novel bag introductions. The region’s ASC boom fuels demand for compact anesthesia and drainage sets that fit small procedure rooms, while hurricane-related factory disruptions spotlight the importance of geographic redundancy in IV bag production. Canada’s national strategy to cut single-use plastics accelerates pilot programs for compostable ostomy pouches, and Mexico’s maquiladora corridor supplies low-cost PVC units to both domestic and U.S. facilities, reinforcing cross-border supply resilience.

Asia-Pacific registered the fastest growth at an 8.16% CAGR, propelled by aging populations and expanding universal health coverage. China’s volume-based procurement exerts downward pressure on average selling prices, yet high unit throughput preserves supplier margins. Japanese home-dialysis penetration exceeds 15%, creating early-adopter demand for automated exchange bag sets with RFID chips. India subsidizes stoma care appliances for low-income groups through state insurance schemes, broadening the base of ostomy users. Southeast Asia’s medical device parks attract foreign direct investment, fostering local supply of infusion and drainage bags and cementing the region as a manufacturing pivot in the medical specialty bags market.

Europe remains a steady contributor, with stringent environmental directives pushing conversion from DEHP-plasticized PVC toward recyclable or bio-based films. Hospitals in Germany and the Nordics embed life-cycle metrics into tenders, rewarding vendors with validated carbon-footprint disclosures. France’s reimbursement of home nutrition solutions boosts sales of multilayer EVA/PP bags compatible with compounding automation. The United Kingdom funds pilot studies on smart ostomy pouches that transmit fill-level data to community nurses, reducing unplanned clinic visits. Overall, the continent’s policy mix of sustainability incentives and quality-of-life reimbursement preserves mid-single-digit expansion in the medical specialty bags market.

Regulatory Landscape

Medical specialty bags are regulated as medical devices in major markets, with access driven by quality systems, technical documentation, and sterile barrier and packaging validation. In the United States, the FDA Quality Management System Regulation (QMSR) became effective in February 2026, amending 21 CFR Part 820 to align quality management expectations with ISO 13485:2016, affecting supplier controls, complaint handling, and design-change documentation for bag and set manufacturers.

In Europe, Regulation (EU) 2017/745 (EU MDR) continues to govern conformity assessment and post-market obligations for device manufacturers, including those supplying ostomy, drainage, and infusion-related bag systems. In December 2025, the European Commission published proposal COM(2025) 1023 to simplify and reduce administrative burden under the EU MDR and IVDR, a signal for companies sustaining broad portfolios of niche bag configurations. Across regions, packaging validation remains a key gatekeeper for market access and sterility maintenance, with ISO 11607 serving as a recognized consensus framework for sterile barrier performance and distribution testing, which in turn shapes material changes such as PVC-free transitions and broader use of novel polymers.

Competitive Landscape

The medical specialty bags market features moderate fragmentation in which the top five suppliers collectively account for major revenue. Baxter International leverages an integrated fluid-therapy franchise, booking USD 10.64 billion in global sales during 2024, with growth in parenteral nutrition and infusion systems underpinning bag demand. B. Braun extends market reach by offering pre-mixed heparin sodium infusions that simplify anticoagulation protocols and lower pharmacy compounding workloads. Fresenius Medical Care capitalizes on its dialysis clinic network to bundle CAPD supplies under multi-year agreements, stabilizing unit volumes despite regional reimbursement swings.

Sustainability garners competitive differentiation. ConvaTec doubled R&D spend in H1 2024 to fast-track low-carbon ostomy barrier films and publicly targets net-zero emissions by 2045[3]Convatec Group, “Convatec Interim Results for the Six Months Ended 30 June 2024,” convatecgroup.com. BD’s USD 4.2 billion acquisition of a critical-care product line deepens its infusion therapy stack, augmenting design synergies across IV and drainage portfolios. Start-ups explore biodegradable elastomers for pediatric stoma pouches, while niche firms deploy 3-D printing to customize convexity and improve post-operative skin outcomes. Digitalization remains nascent: only a handful of providers pilot RFID-embedded drain bags, yet early feedback shows 20% inventory reduction, encouraging larger OEMs to follow suit. With FDA quality-system convergence on the horizon, scale players invest in enterprise-level compliance platforms, erecting cost barriers for smaller rivals.

Medical Specialty Bags Industry Leaders

Baxter International Inc.

Fresenius Medical Care AG & Co. KGaA

Coloplast A/S

B. Braun Melsungen AG

ConvaTec Group plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is product redesign that lowers material use while meeting hospital sustainability procurement requirements, without weakening barrier performance. In February 2026, Serres introduced the Serres Sylva surgical suction bag, which the company described as reducing waste by up to 40% versus standard soft suction bags, reinforcing demand for lighter, lower-waste consumables in procedural settings that prioritize fast setup and dependable fluid management.

Supply resilience and regional capacity additions also expand whitespace for suppliers able to maintain delivery of IV solutions and related bag formats, especially as providers push for continuity after disruption events discussed in the industry. In July 2026, Otsuka ICU Medical LLC announced a USD 500 million expansion in Austin, Texas, including a new 500,000-square-foot facility and upgrades to an existing 700,000-square-foot site to advance non-DEHP IV solutions, highlighting where customers are making volume commitments and where competing vendors may need localized manufacturing or dual-sourcing. Related investment in sterile drug-device combination and assembly capabilities further supports opportunities for bag makers and component suppliers positioned for combination-product packaging, kitting, and validated sterile distribution workflows, including PCI Pharma Services announcing infrastructure investment exceeding USD 1 billion in April 2026 across US campuses.

Recent Industry Developments

- July 2026: Otsuka ICU Medical LLC announced a USD 500 million expansion of IV solutions manufacturing in Austin, Texas, including a new 500,000-square-foot facility and upgrades to its existing 700,000-square-foot site. The expansion supports higher-output domestic supply of IV solution bags and aligns with hospital procurement shifts toward non-DEHP formats.

- March 2025: Fresenius Medical Care expanded production of bibag dry bicarbonate concentrate bags for hemodialysis at its factory in Jaguariuna, Brazil, supported by a high-level automated production line. Higher availability of concentrate bag formats helps dialysis providers reduce logistics intensity versus liquid alternatives and strengthens the company’s consumables position tied to its renal care footprint.

- May 2024: Coloplast launched the SenSura Mio in black ostomy bag range in multiple European markets, including Italy, France, Denmark, Norway, and the Netherlands. The launch broadened product choice around discretion and user preference, adding differentiation within ostomy portfolios where comfort, wear-time, and patient confidence influence brand retention.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from medical specialty bags designed for clinical use, where the bags are used to store, collect, transport, or deliver fluids and related materials in care settings.

Scope exclusions: We exclude general purpose packaging bags and non-medical consumer bags, even if similar materials are used.

Segmentation Overview

- By Product

- Intravenous (IV) Fluid Bags

- Ostomy Bags

- Sterile Collection & Drainage Bags

- Continuous Ambulatory Peritoneal Dialysis (CAPD) Bags

- Anesthesia & Resuscitation Bags

- Blood & Blood-Component Transfer Bags

- Others

- By Material

- PVC

- PE & PP

- EVA & Other Copolymers

- Silicone & TPU

- Bio-based / Compostable Polymers

- By End-user

- Hospitals

- Ambulatory & Day-Care Centers

- Home-Care Settings

- Long-term Care Facilities

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the starting model, we first aligned the product scope with widely used clinical categories such as IV fluid bags, ostomy bags, CAPD bags, anesthesia and resuscitation bags, and sterile collection and drainage bags. We then pulled public health and utilization indicators from sources including the World Health Organization, the World Bank, the US Centers for Disease Control and Prevention, and the OECD health statistics series to understand procedure intensity and care-setting mix.

We also reviewed regulatory and material-related signals from sources such as the US FDA device database, the European Commission medical device framework pages, and peer reviewed journals that discuss sterilization, PVC replacement, and barrier film trends. For cross checks, we used company annual reports and investor presentations, plus reputable press and association websites that report on dialysis, ostomy care, and infusion supplies. Paid database subscriptions were used selectively for company financials and intelligence, news and financials screening, patent searches, and import and export shipment-level checks where trade flow could serve as a proxy. This list is not exhaustive, and we referenced many other public sources to collect inputs, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work focused on confirming what hospital procurement, home-care supply, and ambulatory centers actually count as a specialty bag, and on validating price ranges and mix shifts by bag type and material. We interviewed a mix of manufacturers and distributors, along with clinical and procurement roles that influence demand, so that volume drivers and adoption constraints could be checked across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 48% |

| Mid tier: 44% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 17% | Managers: 55% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing used a top-down approach where patient care activity and procedure pools were translated into annual bag demand, then priced using typical selling ranges by bag category and material. In practice, the model uses variables such as dialysis and home infusion adoption, ostomy prevalence and replacement frequency, hospital admissions and surgical volumes, the shift from PVC toward polyolefin or EVA, and the care-setting mix across hospitals and ambulatory centers.

To keep totals realistic, we corroborated the outputs with selective bottom-up approximations, including sampled ASP times volume checks for key bag types and channel feedback on mix splits, and then adjusted for data gaps where smaller local supply is not fully visible. For forecasting, scenario analysis was used because utilization and material substitution do not move in a straight line. Scenario paths were anchored to expert views on reimbursement, infection control priorities, and regional capacity expansion.

Data Validation & Update Cycle

Outputs were checked against independent demand signals, including procedure volumes, care-setting expansion, and material conversion timelines, and then reviewed for step changes that did not align with known conditions. When a country level result looked misaligned with its clinical footprint, assumptions were revisited and, where needed, respondents were re-contacted to confirm pricing, usage rates, or product mapping.

Before sign-off, the model and write-up go through multi-step analyst reviews to keep arithmetic checks, unit consistency, and regional roll-ups aligned. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Medical Specialty Bags Market Size Measured Against Other Published Estimates

Published market numbers for medical specialty bags can differ because the term is used differently across studies, and because some models start from device sales while others start from clinical demand. Differences also appear when forecasts assume rapid material shifts, aggressive home-care growth, or when currency timing is handled inconsistently.

The largest gap drivers usually come from scope and counting rules, especially whether IV fluid bags, CAPD bags, anesthesia and resuscitation bags, and sterile collection and drainage bags are all included under one umbrella, and whether revenues are counted at manufacturer level or further down the channel. Some estimates also report a growth delta rather than a full market value, which makes comparison harder without reconstructing the base. Clear product mapping and price-by-mix checks reduce this spread. This is why the model keeps adjacent packaging categories out and ties totals back to usage and pricing signals, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.86 B (2026) | |

| Trade Journal A | USD 3.77 B (2024) | Uses a narrower definition that emphasizes select specialty bag groups and appears to exclude several high-volume categories, which lowers the total before any growth is applied. |

| Industry Report B | USD 7.80 B (2029) | Presents an incremental growth figure over a period and pairs it with a separate CAGR, so the full market value depends on an assumed starting size and reconciliation of scope and currency timing. |

The table indicates that most of the spread is explained by how the product set is defined and whether the published figure is a full market value or a period growth number. When inputs are tied to care activity, replacement frequency, and realistic price-by-mix ranges, the resulting market value becomes easier to trace and repeat across geographies and years.

Key Questions Answered in the Report

How large is the medical specialty bags market in 2026?

The medical specialty bags market size reached USD 10.86 billion in 2026 and is forecast to continue growing.

Which product category leads sales?

Ostomy bags generated the highest revenue, accounting for a 32.02% share in 2025.

What is the fastest-growing product category?

CAPD bags are expanding at an 8.23% CAGR as payers encourage home renal therapy.

Which region shows the strongest growth?

Asia-Pacific posts the quickest rise, projected at an 8.16% CAGR to 2031, supported by broader healthcare access.

How is sustainability shaping purchasing decisions?

Hospitals increasingly demand PVC-free or recyclable pouches, driving double-digit growth in bio-based polymer volumes.

Who are the key market leaders?

Baxter International, B. Braun, Fresenius Medical Care, BD, and ConvaTec collectively make up the core competitive set.

Page last updated on: