Medical Fluid Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

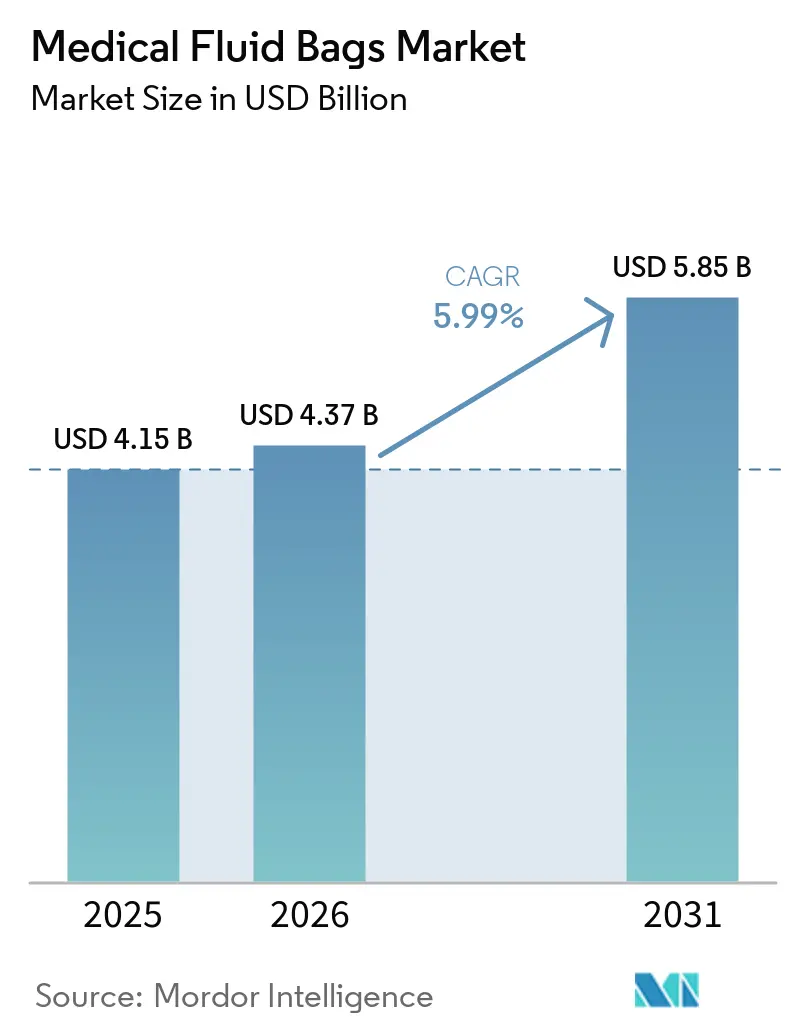

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 5.85 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

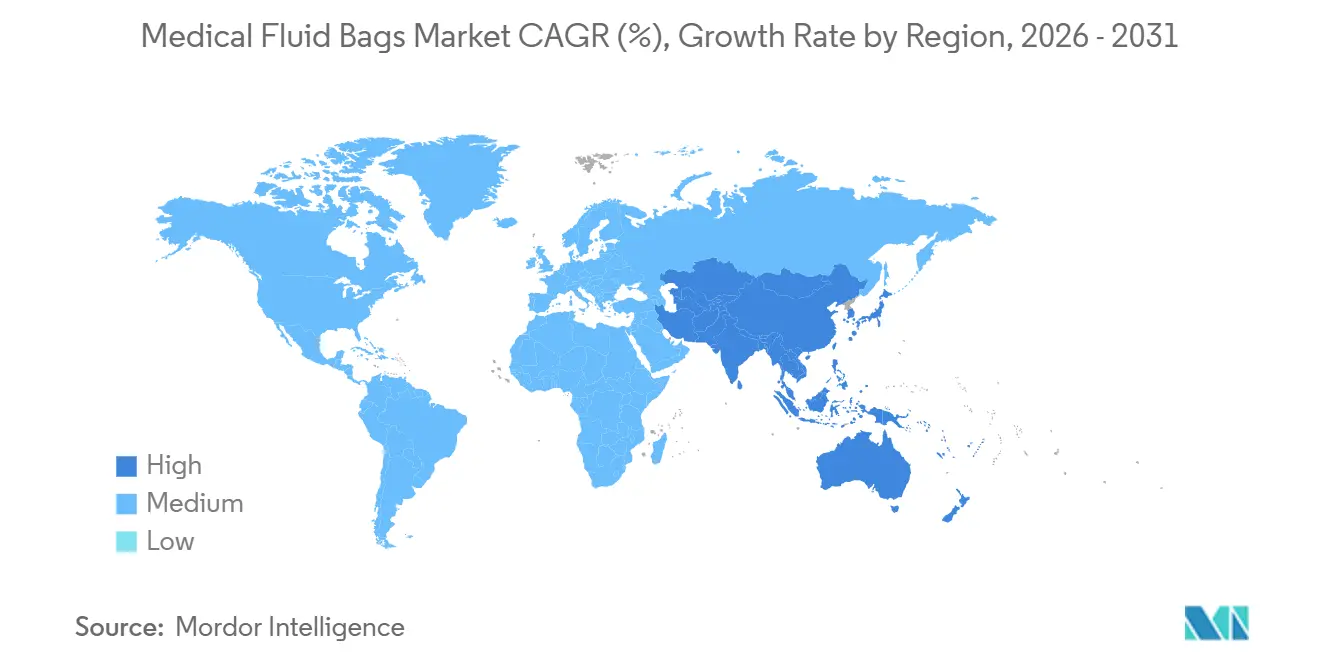

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Fluid Bags Market Analysis by Mordor Intelligence

The Medical Fluid Bags Market size is projected to expand from USD 4.15 billion in 2025 and USD 4.37 billion in 2026 to USD 5.85 billion by 2031, registering a CAGR of 5.99% between 2026 to 2031.

A shift from legacy PVC toward non-PVC and polyolefin multilayer formats is reshaping material choices and capital planning as producers adjust tooling, sealing parameters, and validation strategies. Regulatory scrutiny over sterilization emissions and material chemistries is pushing the medical fluid bags market toward higher compliance spending and selective product retirements that do not meet new thresholds. Procurement teams are moving specifications toward phthalate-free, DEHP-free options, which is reinforcing the premium tier even as unit budgets remain tight in hospitals and home-care networks. Manufacturers are also hardening supply chains for climate and operational shocks, including investment in additional capacity and redundancy in sterilization to reduce line stoppages linked to environmental compliance upgrades. Regional policy signals, such as California’s ban on DEHP in specified devices beginning in 2030 and targeted government grants for onshore production, accelerate replacement cycles and shape near-term bids in the medical fluid bags market. Public funding for IV fluid capacity in Australia following supply disruptions underscores the broader push for regional resilience and diversification in the medical fluid bags market.

Key Report Takeaways

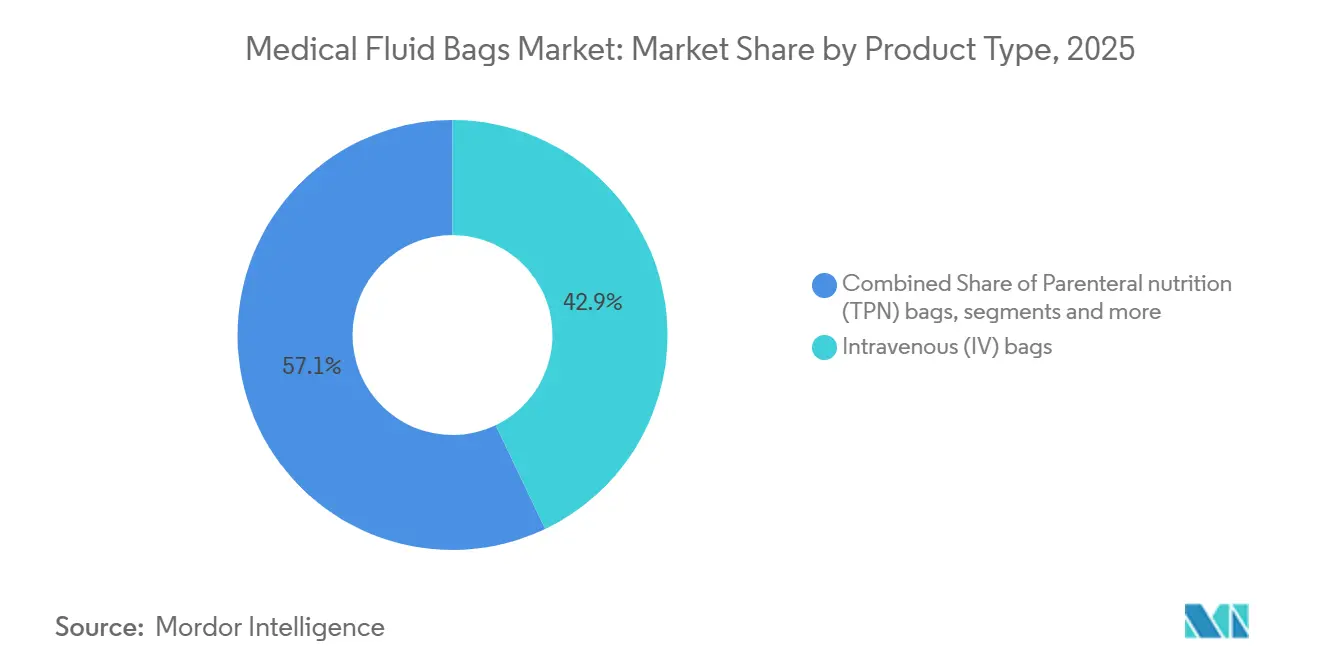

- By product type, intravenous bags led with 42.90% revenue share in 2025, while parenteral nutrition is projected to expand at a 7.34% CAGR through 2031.

- By material, PVC held 46.23% share in 2025, while polyolefin multilayer formats are projected to grow at 8.65% CAGR through 2031.

- By capacity, 500-1,000 ml commanded 42.31% share in 2025, while above-1,000 ml is projected to advance at 7.65% CAGR through 2031.

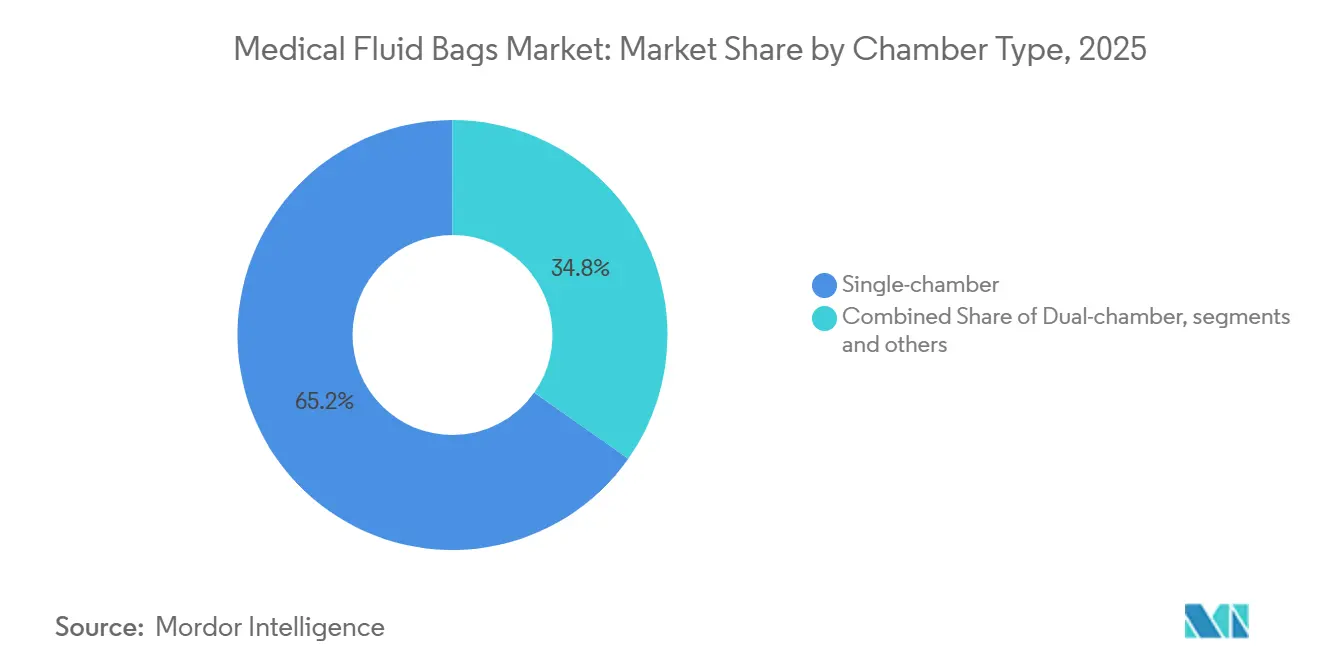

- By chamber type, single-chamber bags accounted for 65.23% share in 2025, while triple and multi-chamber formats are projected to grow at 8.61% CAGR through 2031.

- By end user, hospitals held 55.34% share in 2025, while home healthcare is projected to record a 7.89% CAGR through 2031.

- By geography, North America held 45.34% share in 2025, while Asia-Pacific is projected to expand at 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Fluid Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical volumes and chronic disease burden increasing IV therapy, transfusion and dialysis utilization | +1.8% | Global, with pronounced gains in APAC core, China and India, and spill-over to MEA | Medium term (2-4 years) |

| Expansion of ambulatory surgery and home-care shifting demand to flexible, lightweight bag formats | +1.3% | North America and EU, early adoption in urban APAC corridors | Medium term (2-4 years) |

| Material shift to non-PVC, DEHP-free formats accelerating replacement demand in mature markets | +1.5% | North America, EU core including Germany, France, UK, and regulatory harmonization in Japan | Medium term (2-4 years) |

| Aging population elevating incidence of urinary incontinence and transfusion needs | +1.0% | Japan, South Korea, Western Europe, with rising momentum in China’s 60+ cohort | Long term (≥ 4 years) |

| EPA 2024 EtO sterilizer standards catalyzing retooling and alternative-sterilant ready bag adoption | +0.6% | United States, with indirect influence on Canada and Mexico suppliers | Short term (≤ 2 years) |

| EU REACH and MDR phthalate authorization timeline driving non-PVC conversion programs | +0.7% | European Economic Area and UK, with spill-over into export-dependent Asian manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes and Chronic Disease Burden Increasing IV Therapy, Transfusion and Dialysis Utilization

The medical fluid bags market continues to benefit from the persistent rise in chronic conditions that require controlled fluid therapy, dialysis solutions, and blood component transfusions. Hospitals and outpatient centers depend on reliable IV hydration and electrolyte management during and after procedures, which sustains the baseline for daily bag consumption across care settings. Growth in dialysis and infusion therapy in ambulatory and home environments expands the use cases for standardized bag formats and durable connectors that simplify administration. As care shifts earlier in the recovery pathway, formulary committees and clinical teams are standardizing kits and labeling conventions to reduce administration errors and speed bedside workflows. Reimbursement policy remains a strong determinant of use patterns, and when reimbursement rules favor out-of-hospital care, suppliers that align product design to caregiver ease-of-use tend to gain share within the medical fluid bags market.

Expansion of Ambulatory Surgery and Home-Care Shifting Demand to Flexible, Lightweight Bag Formats

Ambulatory surgery growth drives demand for lightweight, portable, prefilled systems that can integrate into short-stay recovery and safe discharge protocols the same day. Home infusion and long-term care growth favor flexible designs with secure ports, color coding, and clear volume markings that non-clinical caregivers can handle without compromising asepsis. These design preferences lift adoption of formats that enhance tamper evidence and reduce backflow while maintaining compatibility with pumps and gravity sets common in home-care inventory. Device makers that improve clarity of labels and implement intuitive connectors reduce training time and errors for rotating staff and family caregivers. This shift continues to influence capacity choices and chamber configurations as the medical fluid bags market adapts to lower-acuity care settings with different handling and storage constraints.

Material Shift to Non-PVC, DEHP-Free Formats Accelerating Replacement Demand in Mature Markets

A coordinated phase-out of DEHP in specific device categories is accelerating conversions to non-PVC and DEHP-free alternatives in high-income markets, creating a multi-year replacement cycle across formularies and tenders[1]Stoneexpert Team, “DINCH vs DEHP A Cross-Sector Comparison for PVC Manufacturers,” BASTONE Plastics, bastone-plastics.com . Clinical data show much higher DEHP migration into lipid-containing solutions compared with DINCH alternatives, which strengthens the clinical case for non-phthalate systems in neonatal and maternal care units. Cost parity is not yet universal, and DINCH-loaded formulations can require higher loading to match flexibility, which keeps a price premium in some applications even as scale improves. Where hospitals emphasize patient populations sensitive to endocrine-disrupting compounds, procurement often prioritizes polyolefin multilayer structures that avoid plasticizers entirely and satisfy biocompatibility thresholds without additive migration. These dynamics shift capital spending toward co-extrusion capability and new sealing profiles, which in turn demand fresh validation files and sterility assurance evidence in the medical fluid bags market.

Aging Population Elevating Incidence of Urinary Incontinence and Transfusion Needs

An aging demographic increases the prevalence of chronic conditions that necessitate urinary drainage management and routine transfusions during complex procedures. This patient mix favors practical combinations of leg bags for mobility and higher-capacity units for night use, which reduces caregiver interventions and improves patient comfort. Hospitals and long-term care providers adjust inventory toward reliable connectors and high-clarity bag materials that support visual inspection by staff with varying training levels. Blood management also grows more complex as donor pools age, which keeps attention on storage methods and device features that protect cell integrity across shelf life. Together, these needs maintain steady demand in established segments while drawing investment toward product features that meet geriatric care protocols in the medical fluid bags market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex sterile manufacturing, validation and regulatory compliance raising cost and time-to-market | -0.9% | Global, with acute effects in EU under MDR and U.S. under FDA 21 CFR 820 | Medium term (2-4 years) |

| PVC disposal and leachables scrutiny and resin price volatility pressuring margins | -0.6% | North America and EU core markets with expanding attention in select APAC jurisdictions | Medium term (2-4 years) |

| Sterilization capacity constraints during EtO retrofits risk intermittent supply bottlenecks | -0.4% | United States facilities with knock-on effects across global device supply chains | Short term (≤ 2 years) |

| EVA and PP resin supply concentration and tariff exposure elevating input cost risk | -0.3% | Global polyolefin value chain with pressure in import-dependent North America and tariff-exposed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Sterile Manufacturing, Validation and Regulatory Compliance Raising Cost and Time-to-Market

Sterile barrier integrity and process validation expectations add cost and time to new product introductions and line changes, which can delay commercialization. Packaging validations and seal performance qualifications drive repeat testing whenever materials, equipment, or process parameters change, and gaps in documentation or challenge conditions can prompt remediation before release. In parallel, new emission limits for EtO sterilization require capital projects to add controls like permanent total enclosures and continuous monitoring, which diverts budgets from R&D and slows throughput during installation. For multi-site manufacturers, staggered retrofits reduce systemic risk, but local bottlenecks still occur as chambers go offline for upgrades. These realities raise the compliance threshold for smaller firms and favor players with established quality systems and sterilization partnerships in the medical fluid bags market.

PVC Disposal and Leachables Scrutiny and Resin Price Volatility Pressuring Margins

Sustainability programs at hospitals and national health systems are re-evaluating PVC in patient-contact devices because of leachables and end-of-life handling, which strengthens the case for non-PVC lines despite a price premium in many categories. European frameworks that restrict CMR substances above defined thresholds further limit the headroom for DEHP in clinical devices, prompting formulary shifts toward compliant chemistries. Resin markets also add uncertainty, with recycled polypropylene trading at a notable premium to virgin grades, which complicates contracting in segments moving to polyolefin-based bags. Tariff adjustments and logistics frictions inject further variability into landed costs for extrusion-grade resins and specialty additives, which tightens pricing flexibility in hospital bids. Producer price trends indicate mixed pressures along the plastics chain, and that leaves manufacturers balancing input volatility against price-sensitive purchasing teams in the medical fluid bags market[2]: Perc Pineda, “Tariffs and the U.S. Plastics Industry Supply Chain Where Do We Stand,” Plastics Industry Association, plasticsindustry.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TPN Bags Outpace Legacy IV Categories

Intravenous bags commanded 42.90% share in 2025 as the default modality for hydration and electrolyte management across emergency, surgical, and infusion settings in the medical fluid bags market. This foundation keeps line utilization steady while niche categories grow into specialized roles aligned to therapy protocols. Parenteral nutrition bags, supported by standardized multi-chamber formats, are projected to grow at 7.34% CAGR as clinical teams consolidate compounding steps into ready-to-activate designs that cut error risk and preparation time. Hospitals standardize around integrated compartments for lipids, amino acids, and glucose, which also improve distribution efficiency and simplify bedside activation procedures. Blood collection and storage bags remain essential to component processing and inventory management, while dialysis solution and urinary drainage bags align to chronic-care pathways in inpatient and home settings.

The medical fluid bags market reflects procurement preferences that reward validated quality systems and consistent delivery performance, which supports incumbents with global manufacturing and service footprints. Enteral feeding and surgical drainage bags play targeted roles tied to oncology, gastroenterology, and post-surgical care where single-use norms remain non-negotiable. Buyers emphasize labeling clarity, tamper-evident seals, and compatibility with existing pumps and accessories to minimize change-management overhead. Packaging and sterile barrier validations remain a gating factor for product switch-outs, which tempers the speed of change in busy hospital pharmacies. Over the forecast period, the medical fluid bags market will likely see continued adoption of TPN kits that address infection control and cost-to-serve, while legacy IV solutions continue to anchor everyday fluid therapy across care settings.

By Material: Polyolefin Gains Eclipse PVC’s Legacy Grip

PVC, both DEHP-plasticized and DEHP-free variants, held 46.23% share in 2025 due to long clinical familiarity and straightforward seal compatibility in the medical fluid bags market. At the same time, polyolefin multilayer co-extrusions are projected to grow at 8.65% CAGR as hospitals and national bodies emphasize low-extractables profiles and alternatives to phthalates in sensitive populations. California’s ban of DEHP in specified medical devices beginning 2030 intensifies planning for non-PVC lines, with procurement teams pushing earlier conversions in neonatal and maternal care pathways. Clinical data also show far lower migration into lipid-containing solutions when alternative plasticizers or polyolefin substrates are used, which supports long-horizon decisions that prioritize biocompatibility.

Tooling and process transitions from PVC to multilayer PP or PE demand recalibration of extrusion, sealing, and port welding, which raises upfront costs before scale benefits arrive. EVA retains a role where chemical compatibility and clarity are decisive, while elastomeric blends and copolyesters see use in high-stress applications like blood component processing. EU device rules that restrict CMR substances add to the compliance case for non-phthalate formulations within the remaining PVC cohort. Taken together, safety profiles, regulatory direction, and total cost-of-ownership calculations are moving a larger share of the medical fluid bags market toward polyolefin and non-phthalate platforms across routine and specialty applications.

By Capacity: 500-1,000 ml Dominance Faces High-Volume Encroachment

The 500-1,000 ml capacity range captured 42.31% share in 2025, anchored by broad protocol fit for post-operative hydration, chemotherapy support, and general ward use in the medical fluid bags market. These sizes balance dosing precision with manageable wastage profiles for ambulatory and inpatient settings. Above-1,000 ml formats are projected to expand at 7.65% CAGR as home healthcare and long-term care providers prefer longer-duration exchanges that reduce overnight interventions and caregiver burden. In peritoneal dialysis and longer TPN regimens, higher-capacity bags cut the frequency of changeovers and streamline home setup routines for patients and families. These patterns guide plant scheduling toward a wider mix of larger formats and re-usable packaging configurations for bulk shipments into distribution networks.

Inventory control and sterile barrier demands do not diminish for smaller volumes, and neonatal and pediatric protocols keep 250-500 ml formats relevant in centers with high pediatric caseloads. The medical fluid bags market size for larger capacities is projected to scale with home-based therapy penetration and improvements in delivery logistics that guarantee timely residential replenishment. In ambulatory surgery, 250-500 ml options continue to support rapid fluid administration under short observation windows before discharge. Across capacities, packaging validation costs are similar, which leads manufacturers to prioritize high-velocity SKUs where compliance and capital costs are amortized fastest.

By Chamber Type: Single-Chamber Simplicity Versus Multi-Chamber Sophistication

Single-chamber bags accounted for 65.23% share in 2025, reflecting straightforward administration and compatibility with legacy infusion fleets in the medical fluid bags market. These bags remain essential for saline, dextrose, and electrolyte solutions in emergency, med-surg, and step-down units. Triple and multi-chamber formats are projected to grow at 8.61% CAGR as more hospitals adopt pre-configured parenteral nutrition systems that separate components until activation, reducing pharmacy workload and contamination risk. Dual-chamber bags support oncology regimens where agents need separation from diluents until administration, and they fit protocols that require activation at bedside under controlled steps. Incremental material advances, including improved oxygen and moisture barriers, extend shelf stability and support ambient distribution for select formulas.

Validation burdens are higher for multi-chamber designs because each seal and activation feature must demonstrate performance consistency under expected stresses. These requirements reinforce the advantage of suppliers with comprehensive design files and strong post-market surveillance frameworks. Clinical teams value the ability to reduce compounding steps and potential for human error when chambered systems are adopted at scale. As health systems pressure-test labor models, the medical fluid bags market is likely to see sustained movement toward multi-compartment options in nutrition and chemotherapy support where complexity has clear cost and safety implications.

By End User: Hospital Concentration Meets Home Healthcare’s Rapid Gains

Hospitals held 55.34% of end-user demand in 2025, a reflection of surgical volume, ICU needs, and the centralized purchasing power of group procurement arrangements in the medical fluid bags market. Contracting models emphasize firm service levels on delivery reliability and defect thresholds that smaller suppliers struggle to meet, which feeds share stability among large incumbents. Home healthcare is projected to grow at 7.89% CAGR as care shifts continue to favor out-of-hospital settings for stable patients receiving parenteral nutrition, hydration, and antibiotic therapies. This growth places a premium on intuitive labels, tamper-evident features, and ergonomic port designs that non-clinical caregivers can handle safely. Long-term care facilities are adopting standardized kits that consolidate connectors and filters to reduce error risk during staff turnovers.

Ambulatory surgery centers remain a rising channel that values lightweight designs aligned to short-stay recovery and rapid turnover. The medical fluid bags market size in this channel depends on maintaining compatibility with common pumps and gravity sets while limiting inventory sprawl. Blood banks and transfusion centers continue to demand specialized collection and storage bags that fit component processing workflows, centrifugation, and storage standards. As end-user preferences diverge across settings, suppliers that match product features to workflow and staffing realities tend to reinforce positions in competitive accounts.

Geography Analysis

North America held 45.34% share of the medical fluid bags market in 2025, supported by entrenched hospital networks, broad adoption of validated non-PVC lines for sensitive patient groups, and supply-chain initiatives that reduce exposure to single-site risk. States that implement material restrictions and sustainability requirements are nudging hospitals toward phthalate-free options, and California’s device-focused DEHP ban is a visible example guiding procurement calendars. The region faces near-term sterilization retrofit activity as commercial sterilizers install emissions controls, and these projects can create temporary allocation environments that increase the value of multi-site capacity and diversified contract sterilization partnerships. Investment decisions are shaped by the need for supply assurance, which has led to new onshore capacity commitments and targeted government support to reduce import dependence for critical fluids. These elements together reinforce the role of quality systems and delivery performance in contract awards across the medical fluid bags market.

In Europe, MDR enforcement and chemical safety reviews reinforce a gradual pivot away from phthalate-containing PVC toward compliant chemistries and polyolefin multilayers. These regulations often require deeper documentation on extractables and leachables, which favors suppliers with robust testing programs and stability data. Procurement teams also weigh lifecycle environmental impacts in tender scoring, stimulating interest in recyclable substrates or designs with reduced additive loadings. With device-makers updating portfolios to meet evolving expectations, buyers place value on backward compatibility with existing hardware to limit training and capital needs. The overall effect is a steady rationalization of product lines to those that meet European compliance norms and sustainability priorities within the medical fluid bags market.

Asia-Pacific is projected to expand at 8.01% CAGR through 2031 as domestic manufacturing capacity matures and governments support local production to strengthen healthcare resilience. Expanded dialysis use and nutrition therapy in fast-urbanizing centers will continue to influence capacity mixes and product formats. Regional producers are scaling non-PVC lines and applying international quality frameworks to qualify for tenders across public and private channels. Distribution models in large countries remain decisive, and players that match product to regional clinician preferences and logistics requirements can gain quicker traction. The medical fluid bags market in Asia-Pacific also benefits from ongoing investment in hospital infrastructure and the spread of home-care programs in higher-income economies within the region.

Competitive Landscape

The medical fluid bags market features established leaders with validated quality systems and large-scale manufacturing, including longstanding providers of IV solutions and specialty bags. These firms leverage integrated supply chains and multi-continental footprints to protect service levels when a site outage or surge demand requires rapid rebalancing. Procurement strategies at major hospital networks and integrated delivery organizations reward reliable fulfillment and defect control, which sustains incumbent positions in enterprise contracts over multi-year horizons. At the same time, regional specialists continue to grow in niches where customization, small-batch runs, and fast prototyping cycles create differentiation. Capability to validate materials quickly and run short trials for clinical programs can secure entry into national tenders and distributor networks that value responsiveness.

Compliance investments are an increasingly central competitive lever, especially in the United States where EtO NESHAP retrofits require capital outlays and careful scheduling with contract sterilization partners. Packaging and sterile barrier validation under ISO 11607 remains a substantial documentation burden that favors suppliers with strong design histories and rigorous challenge testing programs. Material safety trends reinforce the business case for non-PVC lines and polyolefin multilayers, particularly in regions with explicit restrictions on DEHP and related phthalates in patient-contact devices. Together these drivers maintain a moderate concentration, with room for regionally strong players that meet localized regulatory, logistics, and customer support requirements within the medical fluid bags market.

Selected strategic moves highlight capacity resilience and portfolio advancement in key categories. Public investment to expand IV fluid output in Australia supports regional security of supply and complements private investment to lift annual volumes toward forecast targets. In blood management, approvals for systems that protect red cell integrity under hypoxic storage conditions aim to preserve quality and extend utility for blood establishments, which plays into a larger effort to maximize yield and reduce waste. These actions align with hospital priorities for safety, availability, and traceability, and they reinforce performance criteria that shape formulary and vendor decisions across the medical fluid bags market.

Medical Fluid Bags Industry Leaders

B. Braun Melsungen AG

Baxter International Inc.

Becton, Dickinson and Company (BD)

Fresenius Kabi AG

ICU Medical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hemanext Inc. received 510(k) clearance from the U.S. Food and Drug Administration for expanded indications for its Hemanext ONE System, a first-in-class disposable medical device that removes oxygen from red blood cells and maintains hypoxic storage conditions to preserve cell metabolism and structure, addressing oxidative damage during conventional storage and enabling U.S. blood establishments to process both whole blood-derived and apheresis-derived leukocyte-reduced RBCs in CP2D/AS-3 and ACD-A/AS-3 formulations, with the system already holding CE-mark authorization for commercial distribution in the European Economic Area and the United Kingdom Hemanext.

- March 2025: In a bid to tackle IV fluid shortages that have plagued Australia since early 2023, the Australian government has committed USD 20 million to bolster Baxter Healthcare's production facility in Western Sydney. In a show of confidence, Baxter is matching this investment. With this infusion, Baxter aims to ramp up its local IV fluid production by a minimum of 20 million units, setting its sights on an ambitious target of 80 million units annually by 2027. This strategic move not only seeks to alleviate the domestic shortages but also aims to curtail the nation's reliance on overseas supplies. The urgency of this initiative was underscored by Hurricane Helene's disruption in September 2024, which hit Baxter's North Cove facility in North Carolina and prompted global allocation protocols.

Global Medical Fluid Bags Market Report Scope

As per the report’s scope, medical fluid bags serve as sterile, flexible, and single-use containers. They are crafted to hold, transport, and deliver pharmaceutical solutions, ranging from saline and dextrose to medications and nutrients, straight into a patient's bloodstream. These bags play an essential role in contemporary healthcare, facilitating hydration, medication delivery, and nutritional support. The medical fluid bags is segmented by product type, material, capacity, chamber type, end user, and geography.

Based on product type, the market is segmented into intravenous (IV) bags, parenteral nutrition (TPN) bags, enteral feeding bags, blood collection and storage bags, urinary drainage bags (leg, bedside), dialysis/peritoneal dialysis solution bags, surgical/wound drainage and suction canister liners, and enema/irrigation bags. Based on material, the market is segmented as PVC (DEHP-plasticized; DEHP-free), polyolefin multilayer (PP/PE co-extrusions), EVA (ethylene-vinyl acetate), copolyester ether (COPE), and thermoplastic elastomers (TPU/TPE). Based on capacity, the market is segmented as up to 250 mL, 250–500 mL, 500–1,000 mL, and above 1,000 mL. Based on chamber type, the market is segmented as single-chamber, dual-chamber, and triple / multi-chamber. Based on end user, the market is segmented into hospitals (tertiary/community), ambulatory surgical centers, blood banks/transfusion centers, home healthcare / long-term care, and clinics & physician offices. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Intravenous (IV) bags |

| Parenteral nutrition (TPN) bags |

| Enteral feeding bags |

| Blood collection and storage bags |

| Urinary drainage bags (leg, bedside) |

| Dialysis/peritoneal dialysis solution bags |

| Surgical/wound drainage and suction canister liners |

| Enema/irrigation bags |

| PVC (DEHP-plasticized; DEHP-free) |

| Polyolefin multilayer (PP/PE co-extrusions) |

| EVA (ethylene-vinyl acetate) |

| Copolyester ether (COPE) |

| Thermoplastic elastomers (TPU/TPE) |

| Up to 250 mL |

| 250-500 mL |

| 500-1,000 mL |

| Above 1,000 mL |

| Single-chamber |

| Dual-chamber |

| Triple / Multi-chamber |

| Hospitals (tertiary/community) |

| Ambulatory surgical centers |

| Blood banks / transfusion centers |

| Home healthcare / long-term care |

| Clinics & physician offices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Intravenous (IV) bags | |

| Parenteral nutrition (TPN) bags | ||

| Enteral feeding bags | ||

| Blood collection and storage bags | ||

| Urinary drainage bags (leg, bedside) | ||

| Dialysis/peritoneal dialysis solution bags | ||

| Surgical/wound drainage and suction canister liners | ||

| Enema/irrigation bags | ||

| By Material | PVC (DEHP-plasticized; DEHP-free) | |

| Polyolefin multilayer (PP/PE co-extrusions) | ||

| EVA (ethylene-vinyl acetate) | ||

| Copolyester ether (COPE) | ||

| Thermoplastic elastomers (TPU/TPE) | ||

| By Capacity | Up to 250 mL | |

| 250-500 mL | ||

| 500-1,000 mL | ||

| Above 1,000 mL | ||

| By Chamber Type | Single-chamber | |

| Dual-chamber | ||

| Triple / Multi-chamber | ||

| By End User | Hospitals (tertiary/community) | |

| Ambulatory surgical centers | ||

| Blood banks / transfusion centers | ||

| Home healthcare / long-term care | ||

| Clinics & physician offices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the medical fluid bags market outlook through 2031?

The medical fluid bags market size is projected to reach USD 5.85 billion by 2031, growing at a 5.99% CAGR from 2026 as material shifts, sterilization compliance, and home-care expansion shape demand.

Which product categories are leading growth within the medical fluid bags market?

Intravenous bags held 42.90% share in 2025 while parenteral nutrition bags show faster growth as multi-chamber formats reduce compounding steps and support clinical safety objectives.

How are material trends influencing procurement in the medical fluid bags market?

Conversions to non-PVC and DEHP-free formats are rising in regions with strict chemical safety policies, and polyolefin multilayer films are gaining adoption where low extractables and barrier performance are prioritized.

Which capacity segments are expanding the fastest in the medical fluid bags market?

Above-1,000 ml bags are projected to grow at 7.65% CAGR due to home-care and long-term care use cases that benefit from longer-duration exchanges and fewer changeovers.

What regulatory factors most affect suppliers in the medical fluid bags market?

Emission controls for EtO sterilization in the United States and material restrictions, including DEHP limits in California and Europe, drive capital investments, validation work, and product portfolio updates.

Which end-user segments are shaping design priorities in the medical fluid bags market?

Hospitals remain the largest buyers, while home healthcare shows the fastest growth and pushes design toward ergonomic ports, intuitive labels, and tamper-evident features that support non-clinical caregivers.

Page last updated on: