Biohazard Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

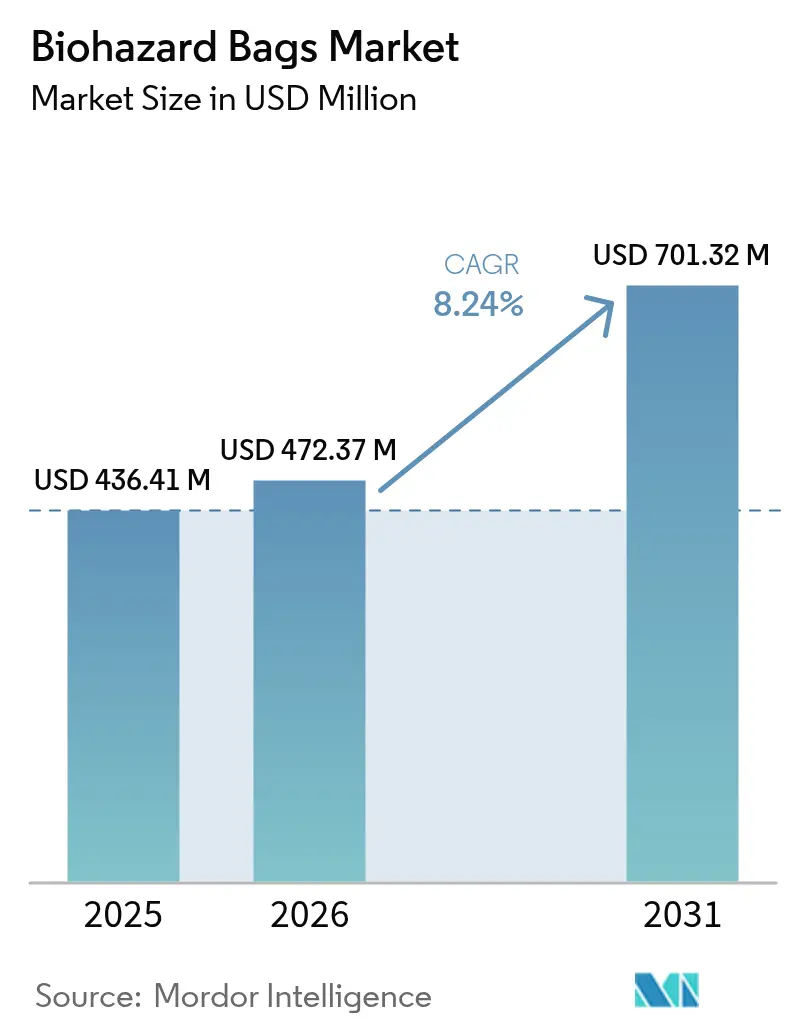

| Market Size (2026) | USD 472.37 Million |

| Market Size (2031) | USD 701.32 Million |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

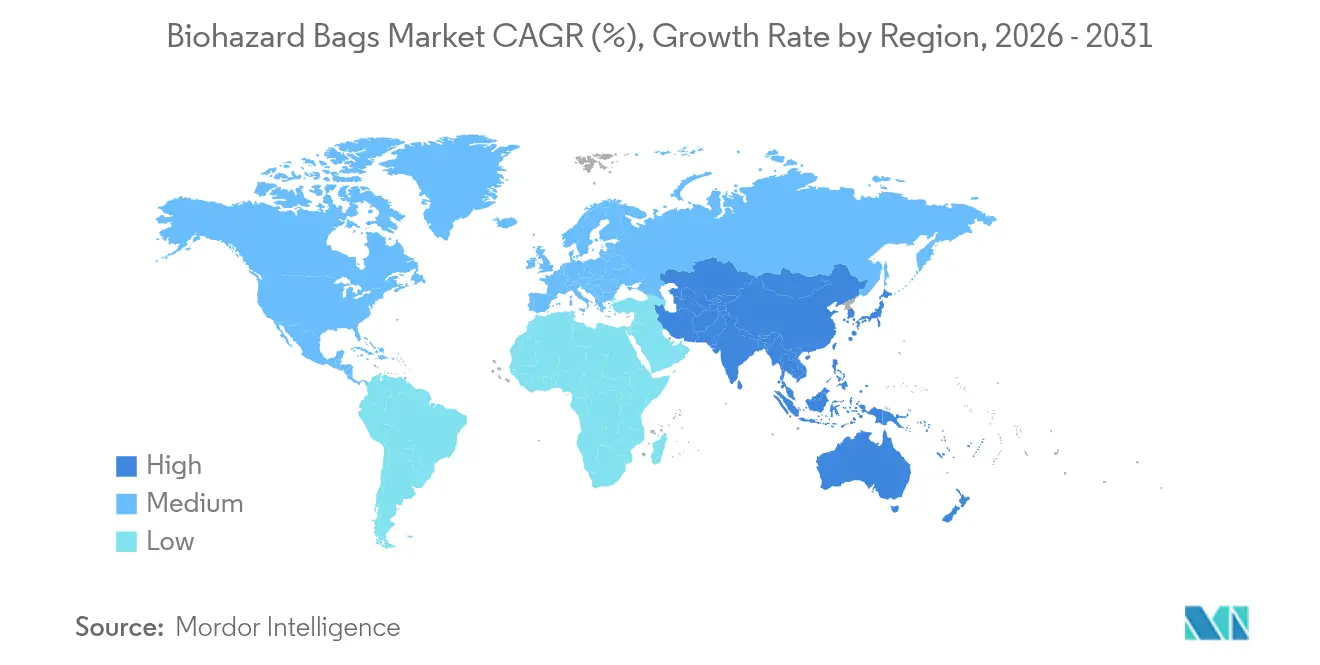

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

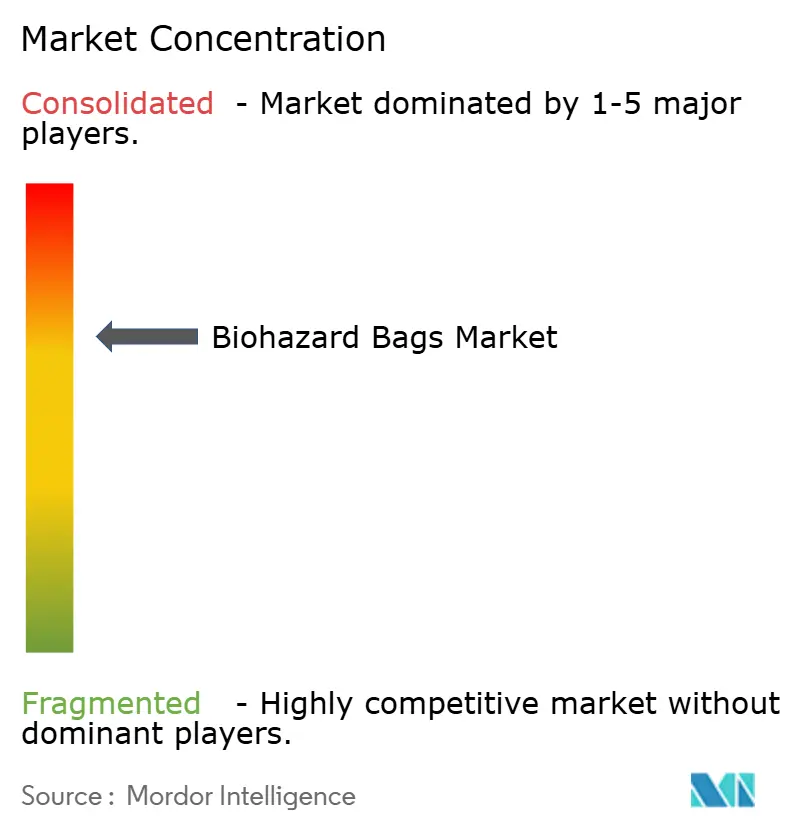

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biohazard Bags Market Analysis by Mordor Intelligence

The biohazard bags market size was valued at USD 436.41 million in 2025 and estimated to grow from USD 472.37 million in 2026 to reach USD 701.32 million by 2031, at a CAGR of 8.24% during the forecast period (2026-2031). Expansion reflects the healthcare sector’s heightened emphasis on infection-control protocols, the post-pandemic rise in single-use consumables and the steady tightening of hazardous-waste regulations. Demand is further underpinned by the volume of biomedical waste, 15% of which is classified as hazardous, and by the spread of standardized compliance rules such as the Hazardous Waste Generator Improvements Rule adopted by 40 states. Hospitals, diagnostic laboratories and pharmaceutical plants continue to scale capacity, and each new facility embeds waste-segregation requirements at the design stage. These combined factors reinforce sustained purchasing of color-coded, puncture-resistant containment products across the biohazard bags market[1]Centers for Disease Control and Prevention, “Healthcare Infection Prevention and Control,” cdc.gov.

Key Report Takeaways

- By product material, low-density polyethylene led with 42.11% revenue share in 2025; polypropylene is projected to expand at a 10.01% CAGR through 2031.

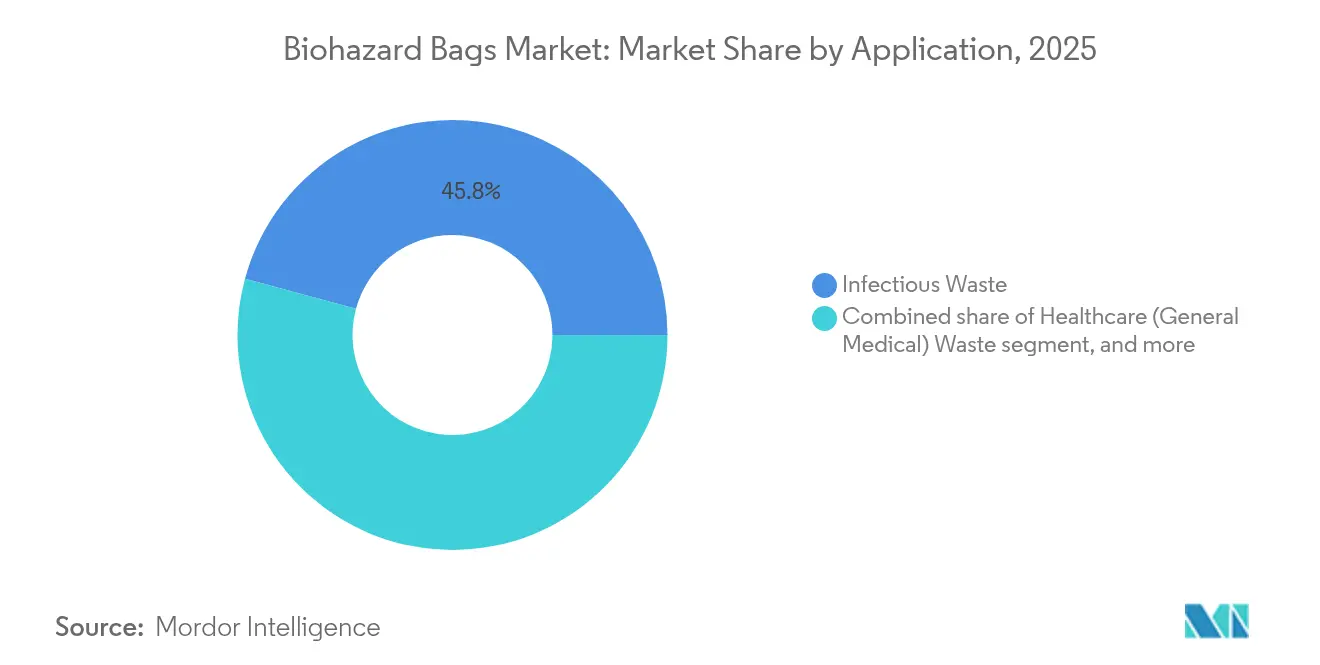

- By application, infectious waste captured 45.78% of the biohazard bags market size in 2025 while healthcare general medical waste records the highest expected CAGR at 9.74% to 2031.

- By end user, hospitals held 55.02% of the biohazard bags market share in 2025, whereas diagnostic laboratories are set to post an 10.92% CAGR during the forecast period.

- By geography, North America accounted for 38.12% revenue share in 2025; Asia-Pacific is forecast to grow the fastest, at 9.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biohazard Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating generation of biomedical waste | +2.1% | Global, concentrated in North America & Europe | Medium term (2 – 4 years) |

| Expansion of global healthcare infrastructure | +1.8% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Stricter regulatory compliance for hazardous waste segregation | +1.6% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rising adoption of single-use medical consumables | +1.4% | Global, led by developed markets | Medium term (2 – 4 years) |

| Growth of pharmaceutical and biologics manufacturing | +1.2% | North America, Europe and emerging Asia-Pacific hubs | Long term (≥ 4 years) |

| Increasing public-health awareness of infection control | +1.0% | Global post-pandemic | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Generation of Biomedical Waste

Healthcare facilities now classify 15% of waste as hazardous, a share that remains elevated after 2020. Intensive care units and emergency departments generate larger volumes of contaminated disposables than before, and the World Health Organization’s guidance on point-of-generation segregation has become a routine benchmark. Hospitals respond by purchasing colour-coded bag systems that align with federal, state and international requirements for traceability, puncture resistance and leak protection. Mandatory staff-training modules on handling procedures further increase reorder frequency, making this factor one of the most durable growth contributors for the biohazard bags market.

Expansion of Global Healthcare Infrastructure

Asia-Pacific governments are commissioning hospitals, outpatient clinics and diagnostic hubs at a pace unmatched elsewhere. These projects embed medical-waste rooms, automated bag-sealers and inspection points into facility blueprints. New plants for biologics and vaccines use containment specifications based on United States and European Union rules, which accelerates demand for thicker-gauge polypropylene and high-density polyethylene bags. Builders and operators also stipulate eco-labels as they move toward sustainable procurement targets set by regional authorities. The long-term investment cycle therefore feeds continuous volume growth across the biohazard bags market.

Stricter Regulatory Compliance for Hazardous Waste Segregation

Forty states now enforce the Hazardous Waste Generator Improvements Rule, and the EPA’s e-Manifest system obliges healthcare providers to document waste from point of origin to disposal. The Management Standards for Hazardous Waste Pharmaceuticals prohibit sewer disposal and direct generators toward compliant containment and incineration. Recent state proposals on sharps handling add further specificity, prompting hospitals to adopt heavy-duty bag formats certified for both tear strength and bar-code tracking. Suppliers able to match these niche requirements gain an advantage in the biohazard bags market.

Rising Adoption of Single-Use Medical Consumables

The FDA re-emphasized single-use device safety guidelines in 2024, discouraging reprocessing of items that contact sterile tissue. Dental clinics and ambulatory centers must now dispose of gloves, gowns and tubing immediately after patient contact, each item classified as regulated medical waste. Proper disposal relies on bags that meet ASTM puncture- and impact-resistance thresholds. Facilities embed disposal policies into daily checklists, translating directly into higher bag consumption per procedure.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of reusable waste containment systems | -0.8% | Global, stronger in sustainability-focused markets | Medium term (2-4 years) |

| Volatility in polyethylene raw material prices | -0.6% | Global, with regional supply-chain variations | Short term (≤ 2 years) |

| Emerging bans on single-use plastics | -0.7% | Europe, North America and select Asia-Pacific jurisdictions | Medium term (2-4 years) |

| High capital requirements for waste-treatment compliance | -0.5% | Global, more pronounced in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Reusable Waste Containment Systems

Large hospitals adopting circular-economy objectives trial bag-less cart systems that integrate solid plastic linings and sealed lids. Firms such as Daniels Health market cassette-style sharps units that can be emptied, sterilized and redeployed. Sustainability committees note lower cradle-to-grave emissions and reduced worker-injury risk compared with double-bag techniques. Initial capital outlay and comprehensive staff retraining limit adoption to major networks, yet the option introduces price sensitivity within the biohazard bags market, particularly for low-value red bags.

Volatility in Polyethylene Raw Material Prices

Surges in naphtha and ethane feedstock costs prompt resin price swings, compressing margins for converters and prompting healthcare buyers to renegotiate contracts. Manufacturers hedge with multi-month inventories, but smaller converters remain exposed to spot-price fluctuations. Some hospitals test alternative materials or request mid-contract price reviews. Meanwhile, supply-chain departments diversify suppliers to reduce disruption risk. Extended volatility therefore delays bulk-purchase decisions and introduces a moderate dampening effect on biohazard bags market growth[2]Environmental Protection Agency, “Hazardous Waste Generator Improvements Rule,” epa.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Material: Polypropylene Gains Ground Despite LDPE Dominance

Low-density polyethylene commanded 42.11% of the biohazard bags market share in 2025, reflecting its proven flexibility and puncture-resistance attributes that satisfy general infectious-waste handling requirements. The material dominates high-throughput hospital settings where cost, availability and automated-sealing compatibility matter most. However, polypropylene continues to outpace all other resins, and the biohazard bags market size for the polypropylene segment is projected to expand at 10.01% CAGR between 2026 and 2031 thanks to its higher chemical-resistance threshold, suitability for chemotherapeutic and pharmaceutical waste and ability to withstand high-temperature autoclave cycles.

The preference landscape is evolving. Specialized cancer centers and biologics plants often specify high-density polyethylene or multilayer co-extruded structures to secure extra leak resistance. A niche group of facilities is also piloting biopolymers derived from polylactic acid or polyhydroxyalkanoate, aiming to lower carbon footprints, yet uptake remains embryonic because healthcare regulators require exhaustive validation before approving bag materials for hazardous waste. Manufacturers are therefore balancing environmental claims with mandatory ASTM and ISO puncture, tear and transmissibility testing, ensuring that innovation continues without undermining the core performance expectations of the biohazard bags market.

By Application: Healthcare General Medical Waste Accelerates Growth

Infectious waste accounted for 45.78% of the biohazard bags market size in 2025, driven by sustained use of disposable drapes, gowns and gloves across surgical suites and intensive-care units. These procedures generate consistent daily volumes that must be removed quickly, making red infectious-waste bags the workhorse of hospital operations. At the same time, the healthcare general medical waste category is forecast to grow the fastest, with 9.74% CAGR through 2031, as outpatient clinics and point-of-care diagnostic sites multiply. These facilities produce a broad mix of partially contaminated items that still require containment but do not always meet the infectious threshold, thereby expanding mid-gauge bag demand.

Chemical and pharmaceutical waste will remain a speciality sub-segment, drawing demand for thicker, yellow or black bags incorporating heavyweight polypropylene to resist aggressive solvents. Other categories, such as pathological waste, hold smaller shares but command premium-priced, vapor-barrier configurations. Regulators continue to refine bag specifications, especially for drug-contaminated disposables, which funnel additional purchase orders toward suppliers adept at application-specific designs within the biohazard bags market.

By End User: Diagnostic Laboratories Drive Fastest Expansion

Hospitals represented more than half of the biohazard bags market size in 2025 at 55.02%, a share reflecting their high patient throughput, complex waste matrices and on-site autoclave facilities. Within hospitals, peri-operative departments and catheterization labs consume the bulk of bags due to constant instrument turnover. Diagnostic laboratories, however, are projected to post the highest growth at 10.92% CAGR through 2031 as molecular-testing volumes climb and decentralized testing formats spread to pharmacies and retail clinics. Each specimen loop, pipette tip and microcentrifuge tube must be disposed of in a compliant liner, driving frequent reorder cycles.

Pharmaceutical manufacturing plants also add incremental demand as they expand batch sizes for biologics and vaccines. These sites require bags that survive chemical-decontamination steps before incineration, favoring multilayer polypropylene or co-extruded substrates. Research institutions and veterinary facilities round out the end-user mix, forming smaller yet steady revenue pools within the broader biohazard bags market.

Geography Analysis

North America retained leadership with a 38.12% revenue share in 2025, anchored by a well-established regulatory network comprising the EPA, OSHA and FDA. Hospitals allocate dedicated compliance budgets to ensure waste-tracking accuracy and purchase bags meeting ASTM D1709 puncture standards. States’ uptake of the Hazardous Waste Generator Improvements Rule harmonizes documentation requirements, further embedding standardized liner use and sustaining demand across the United States and Canada. While growth is slower than in developing regions, replacement cycles, red-bag subsidies for rural clinics and consolidation among waste-management service providers preserve market vibrancy.

Asia-Pacific contributes the most dynamic growth storyline. Government funding for new inpatient beds, oncology centers, dialysis units and vaccine plants is accompanied by mandatory waste-segregation guidelines modeled on United States and European Union directives. As governments implement these rules, procurement teams specify minimum bag thickness, bag color by waste class and traceability features. Local manufacturers ramp production, yet premium imports still dominate high-spec orders, ensuring cross-border supply chains form an integral part of the biohazard bags market. With healthcare expenditure rising alongside urban population growth, Asia-Pacific’s 9.34% CAGR is likely to remain intact this decade.

Europe maintains a significant market position thanks to Green Deal policy incentives and stringent circular-economy objectives. Hospitals are piloting low-carbon or reusable waste systems, yet infection-prevention priorities keep single-use liners firmly in place for high-risk waste streams. Regulatory authorities such as the European Chemicals Agency frequently update guidance on halogenated plastics, prompting manufacturers to adjust formulations. The Middle East and Africa display moderate yet accelerating growth as Gulf states commission teaching hospitals with Western-style waste rooms, while South America records steady improvement as public-sector hospitals upgrade to meet revised waste-handling laws.

Competitive Landscape

The biohazard bags market is moderately consolidated. Waste Management’s USD 7.2 billion purchase of Stericycle in June 2024 produced the largest integrated medical waste company in North America and yielded USD 125 million in annual synergies, boosting cross-selling opportunities for proprietary bag lines positioned alongside haul-off services. The merger accelerates vertical integration, enabling bundled contracts that cover liner supply, pickup, treatment and compliance reporting within a single service agreement.

Traditional bag specialists compete by refining niche products. STERIS introduced Verafit Sterilization Bags with viewing windows that confirm dryness after steam exposure, specifically targeting EU GMP Annex 1 requirements for sterile-manufacturing fill-finish zones[3]STERIS, “Verafit Sterilization Bags and Covers,” steris.com. Smaller converters differentiate through short-run color printing, biodegradable additives and strong customer service for rural or specialty clinics. Meanwhile, sustainability ambitions push manufacturers to research plant-derived resins or to collaborate with chemical recyclers aiming to close the loop on polyethylene waste.

Technology adoption is another differentiator. Smart bag dispensers equipped with RFID tags allow environmental-services teams to track daily liner consumption by department. Data generated helps hospitals refine supply forecasts and minimize stockouts. Players able to integrate digital-tracking options, offer compliant film recipes and document full chain-of-custody continue to capture higher-margin contracts. Consolidation is likely to continue as service providers and bag producers seek scale advantages, especially within international markets where multi-facility health networks demand harmonized supply.

Biohazard Bags Industry Leaders

Thermo Fisher Scientific, Inc.

Inteplast Group (Minigrip)

Transcendia Inc.

SP Bel-Art

Merck KGaA (MilliporeSigma)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Waste Management completed its USD 7.2 billion acquisition of Stericycle, creating the largest integrated medical-waste management company in North America with over USD 125 million in annual synergies.

- March 2024: STERIS launched Verafit Sterilization Bags and Covers featuring patent-pending viewing windows that support EU GMP Annex 1 compliance.

- February 2024: The Environmental Protection Agency finalized updates to the Hazardous Waste Generator Improvements Rule, raising segregation and containment requirements across healthcare facilities.

- January 2024: DuPont announced a strategic partnership with B. Braun Medical that reduced packaging area by 33% and lifted production throughput by 30%.

- December 2024: The FDA issued updated guidance on single-use medical-device reprocessing, reinforcing the requirement for disposal of contaminated devices in regulated medical-waste containers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biohazard bags market as the annual revenue generated from sealed, puncture-resistant polymer bags, primarily LDPE, HDPE, and polypropylene, specifically labeled for collecting, transporting, and disposing of infectious or other biomedical waste across healthcare, laboratory, and pharmaceutical settings worldwide.

Single-use sharps containers, reusable rigid canisters, and broader chemical packaging solutions are outside the present scope.

Segmentation Overview

- By Product Material

- LDPE

- HDPE

- Polypropylene

- Cellophane

- Other Product Materials

- By Application

- Infectious Waste

- Healthcare (General Medical) Waste

- Chemical & Pharmaceutical Waste

- Other Applications

- By End User

- Hospitals

- Diagnostic Laboratories

- Pharmaceutical & Biologics Manufacturing

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Targeted interviews with waste-management officers in hospitals, buyers at diagnostic labs, polymer-resin distributors, and regional regulators in North America, Europe, Asia-Pacific, and the GCC helped validate disposal practices, capacity-utilization norms, and recent price pass-throughs. Follow-up surveys with procurement heads confirmed adoption rates of eco-friendly variants, filling gaps left by desk findings and guiding assumption bounds.

Desk Research

Mordor analysts began with structured searches across open-access authorities such as the World Health Organization, the U.S. OSHA Bloodborne Pathogens Standard, EU Waste Framework Directive dashboards, UN Comtrade trade codes for polymer bag exports, and Ministry of Health biomedical-waste statistics in China, India, and Brazil. These sources clarified regulatory definitions, waste-generation baselines, and regional compliance timelines. Financial filings, investor decks, and product brochures from listed bag manufacturers then anchored typical average selling prices and material mixes, while recall notices and patent filings signaled design trends like autoclave-safe multi-layer films. To enrich numeric rigor, our team tapped paid repositories, including D&B Hoovers for company revenue splits, Dow Jones Factiva for shipment news, and Volza customs data for cross-border bag volumes, to triangulate supply visibility by geography. The sources cited above illustrate key inputs; many additional public and subscription datasets were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A blended top-down, bottom-up model was used. National healthcare-waste generation (kg per inpatient bed and per outpatient visit) was paired with infection-risk fractions to build a demand pool, which was then multiplied by verified bag usage coefficients. Supplier roll-ups and channel checks on ASP × volume provided a bottom-up reasonableness screen, and discrepancies greater than three percent triggered parameter reviews. Key drivers in the model include hospital bed additions, surgical procedure counts, polymer resin price trends, regulatory deadline milestones, bag weight-per-use evolution, and penetration of biodegradable grades. Multivariate regression, supported by ARIMA smoothing for seasonality, projects each driver through 2030, after which scenario analysis adjusts for regulatory shocks.

Data Validation & Update Cycle

Outputs pass three tiers of variance and anomaly checks before senior review. We compare results with independent waste-tracking datasets and material price indices, re-contacting sources when swings exceed preset thresholds. Reports refresh annually, with mid-cycle updates if material policy or supply events arise; a final analyst pass occurs immediately prior to client delivery.

Why Mordor's Biohazard Bags Baseline Stands Out for Decision-Makers

Published estimates often differ because firms select varying material baskets, data vintages, and refresh cadences, creating a confusing range for managers who need one dependable figure.

Key gap drivers include narrower material scope, divergent disposal-rate assumptions, currency conversions, and less-frequent data updates at other publishers, while Mordor Intelligence anchors its base year to primary-validated bag utilization and annually refreshed regulatory checkpoints.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 436.41 million (2025) | Mordor Intelligence | - |

| USD 433.6 million (2025) | Global Consultancy A | Limited primary validation and exclusion of polypropylene sub-segment |

| USD 439.1 million (2024) | Industry Journal B | Conservative infection-waste growth, two-year refresh cycle, desk-only data |

In sum, the disciplined variable selection, timely source re-validation, and transparent assumption log maintained by Mordor Intelligence give users a market baseline that is traceable, balanced, and ready for confident board-level decisions.

Key Questions Answered in the Report

What is the current value of the biohazard bags market?

The market stands at USD 472.37 million in 2026 and is projected to hit USD 701.32 million by 2031.

Which material leads sales within the biohazard bags market?

Low-density polyethylene leads, accounting for 42.11% of revenue in 2025.

Why are diagnostic laboratories the fastest-growing end-user group?

Rising molecular-testing volumes and the spread of decentralized point-of-care diagnostics increase contaminated consumables, which drives 10.92% CAGR for laboratories.

Which region shows the fastest market growth?

Asia-Pacific posts the highest CAGR at 9.34% through 2031, due to major healthcare infrastructure investments and stricter waste-handling regulations.

What sustainability initiatives affect the biohazard bags market?

Hospitals in North America and Europe are piloting reusable container systems and exploring plant-based resins, pushing suppliers to invest in lower-carbon or recyclable product lines.

Page last updated on: