Non-PVC IV Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

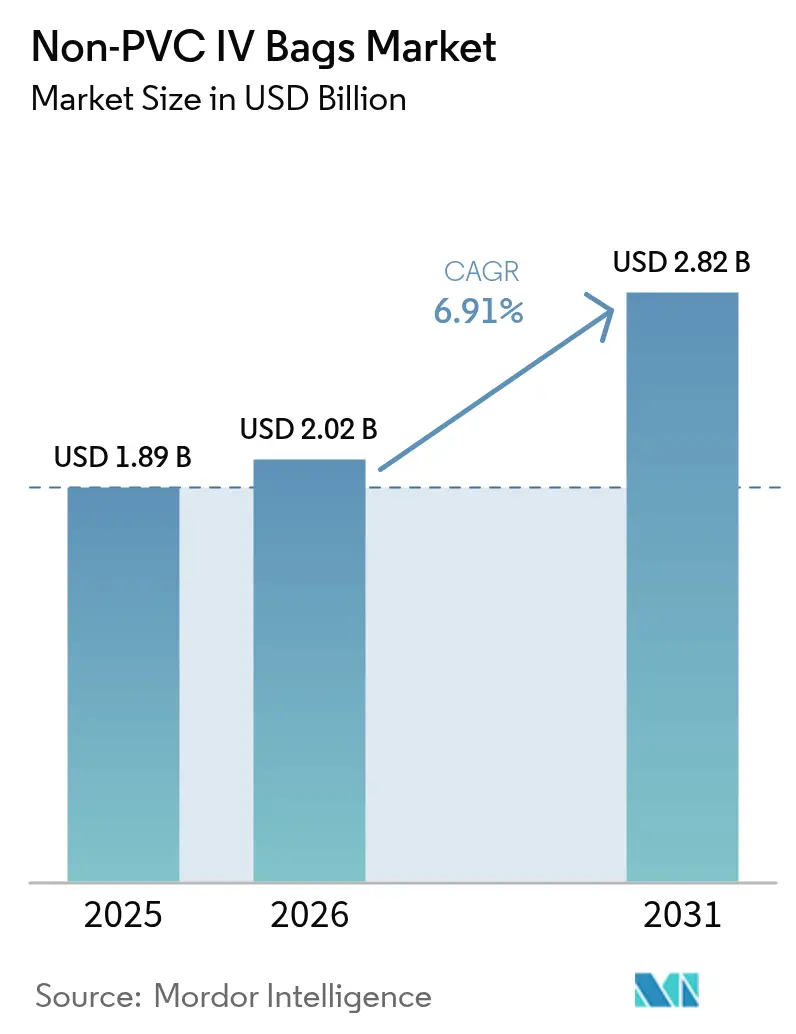

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.82 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

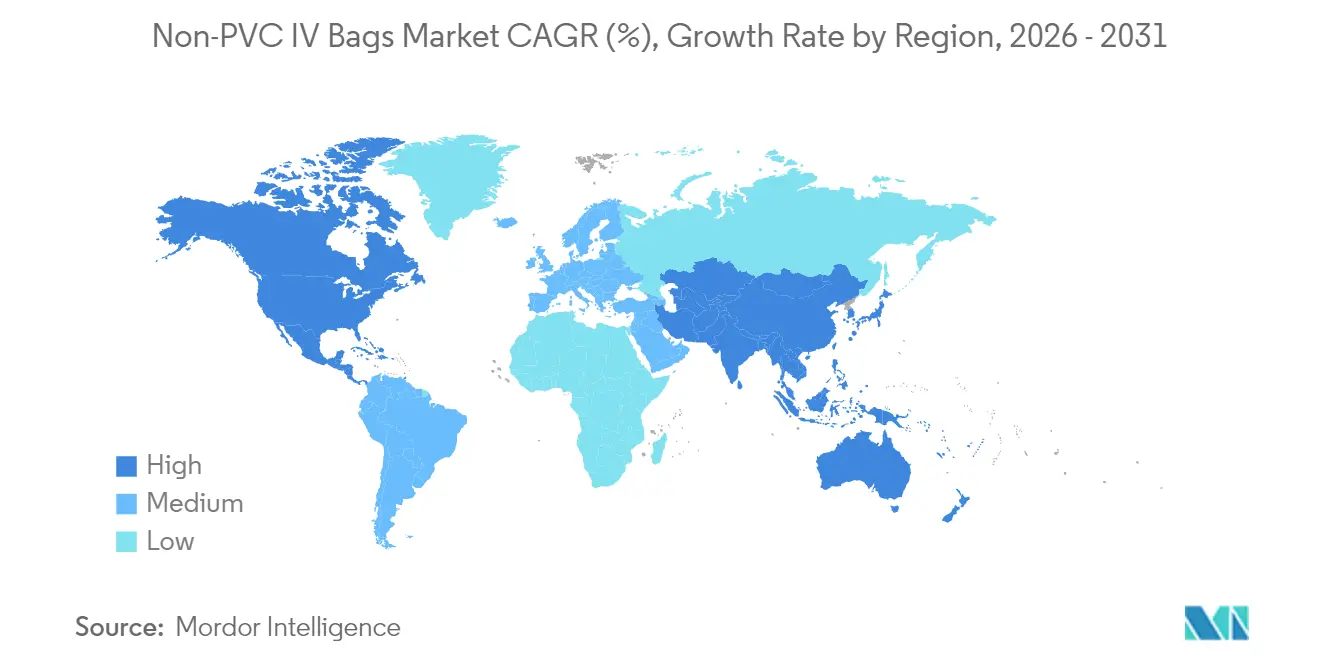

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-PVC IV Bags Market Analysis by Mordor Intelligence

The non-PVC IV bags market size is expected to grow from USD 1.89 billion in 2025 to USD 2.02 billion in 2026 and is forecast to reach USD 2.82 billion by 2031 at 6.91% CAGR over 2026-2031. Regulatory pressure to remove di-ethyl-hexyl phthalate (DEHP) from clinical environments, hospital decarbonisation targets and a steady pipeline of complex biologic infusions are reshaping procurement strategies in North America, Europe and select Asia–Pacific economies. Ethylene Vinyl Acetate (EVA) maintains a volume lead, yet polypropylene’s rapid uptake signals cost-focused buyers are pivoting to lower-priced, recyclable resins. Growth is also supported by smarter drug-delivery formats, with RFID-enabled labels increasingly paired with smart pumps to curb medication errors. Finally, supply-chain shocks in petrochemicals are nudging manufacturers toward biomass-derived EVA that promises lower lifecycle emissions while safeguarding performance.

Key Report Takeaways

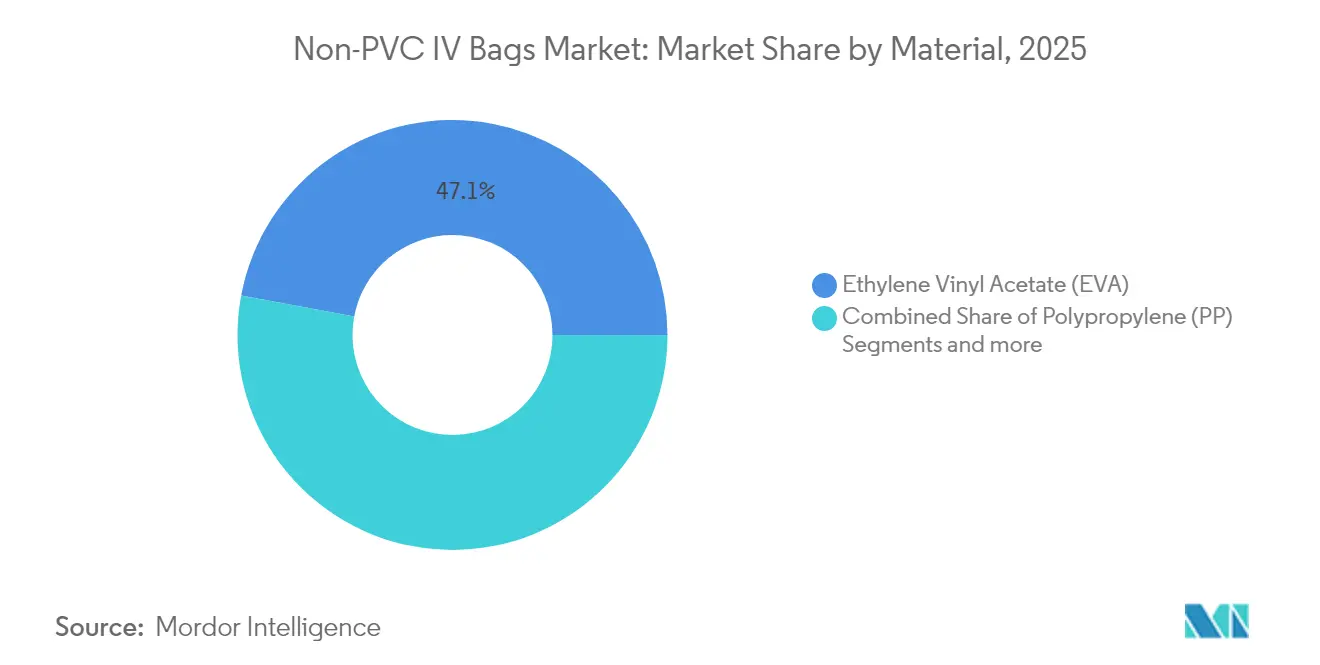

- - By material, EVA captured 47.05% of the non-PVC IV bags market share in 2025.

- - By product type, single-chamber formats held 65.10% of the non-PVC IV bags market size in 2025, while multi-chamber solutions are advancing at a 7.45% CAGR through 2031.

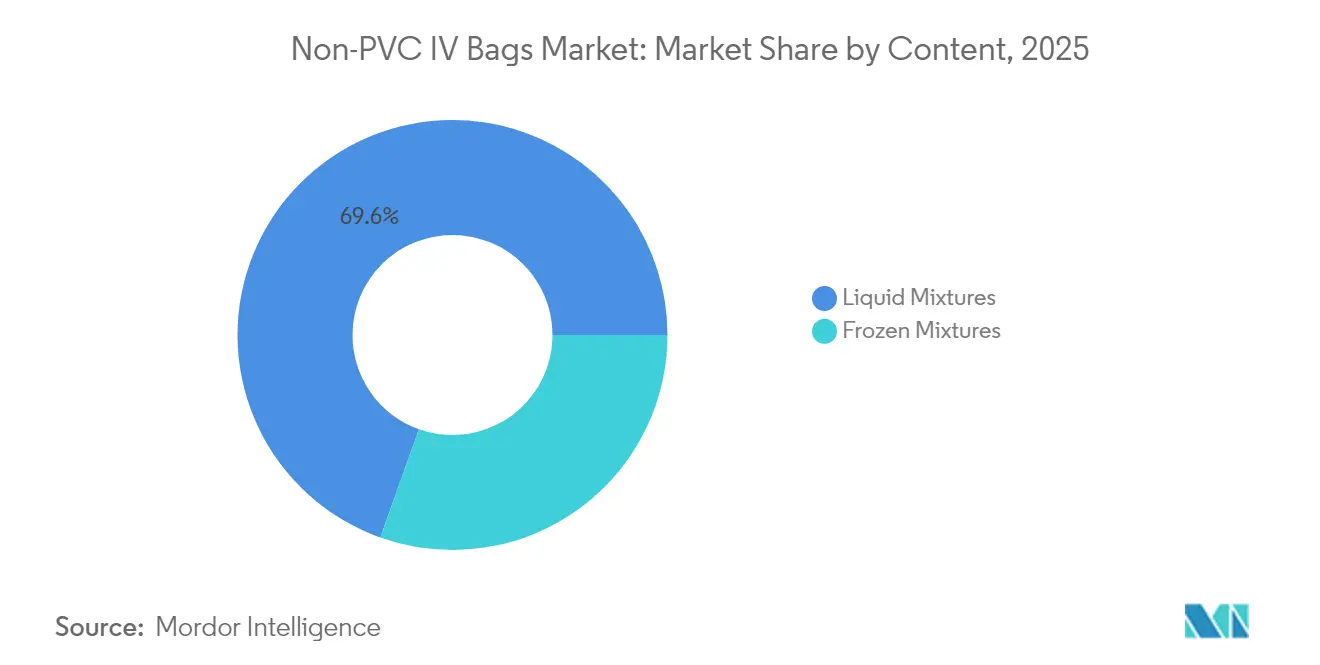

- - By content, liquid mixtures commanded 69.55% share of the non-PVC IV bags market size in 2025.

- - By end-user, hospitals represented 70.85% revenue in 2025 and ambulatory surgical centres are expanding at 7.54% CAGR to 2031.

- - By geography, North America represented 40.85% revenue in 2025 and Asia-Pacific are expanding at 7.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-PVC IV Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining PVC acceptance in mature markets | +1.8% | North America & Europe | Medium term (2-4 years) |

| Rapid biologics & oncology infusion growth | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Rise of home- & ambulatory-care infusion | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Stringent EU REACH / U.S. Prop-65 DEHP bans | +1.0% | North America & Europe | Short term (≤ 2 years) |

| Embedded RFID & e-label innovations | +0.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Hospital decarbonisation procurement targets | +0.6% | Global, strongest in Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining PVC Acceptance in Mature Markets

Procurement teams in large academic hospitals are actively retiring PVC devices as evidence of phthalate toxicity spreads across clinical networks. Cleveland Clinic’s pledge to remove PVC and DEHP from two high-volume supply categories by 2025 has become a bellwether for sustainability benchmarking among US health systems [1]Cleveland Clinic, “PVC and DEHP Elimination Initiative,” clevelandclinic.org. The US FDA’s advisory to minimise DEHP exposure in neonatal and paediatric settings elevated non-PVC alternatives from optional to essential in critical care. Purchasing consortia now evaluate bids against lifecycle risk metrics rather than unit price alone, pushing vendors to deliver compliant solutions at scale [2]Practice Greenhealth, “Safer Materials in Neonatal Care,” practicegreenhealth.org.In the European Union, the REACH Restrictions Roadmap targeting PVC additives gives manufacturers regulatory certainty to retool production lines. As peer institutions publicise progress reports, a network effect is rapidly normalising DEHP-free IV procurement across North America and Western Europe.

Rapid Biologics & Oncology Infusion Growth

The oncology pipeline is driving demand for bags that will not leach plasticisers or compromise biologic potency. Sources projects more than 100 new cancer therapies to debut over the next five years, many requiring non-PVC containers to preserve drug stability. Antibody–drug conjugates alone generated USD 14.9 billion sales in 2024 at a 40% compound growth rate. These high-value therapeutics make price a secondary concern to safety and compatibility, favouring non-PVC formats even in cost-sensitive institutions. Radioligand and personalised therapies need containers with superior chemical inertness; EVA and emerging copolyesters fit this requirement. Investments in dedicated oncology infusion suites ensure hospitals continue to stock premium DEHP-free bags, while home-based chemotherapy services use the same specifications to extend treatment beyond inpatient wards.

Rise of Home- & Ambulatory-Care Infusion

Ambulatory surgical centres (ASCs) treated 3.3 million Medicare beneficiaries in 2022, absorbing USD 6.1 billion in federal spending and validating the shift toward lower-cost outpatient care [3]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services Payment System,” medpac.gov. Longer storage intervals and patient self-administration elevate sterility and barrier requirements, prompting purchasing teams to standardise on non-PVC containers. Interoperability with dose-error-reduction pumps has accelerated adoption of RFID-tagged bags that feed preparation data directly to electronic medical records, mitigating wrong-drug and wrong-dose events. Home infusion providers increasingly embed DEHP-free specifications in tender documents to protect vulnerable, long-term patients. The projected USD 142 billion outlay for global infusion therapy by 2027 will channel a large share toward alternate-site settings, sustaining above-average growth for the non-PVC IV bags market.

Stringent EU REACH / US Prop-65 DEHP Bans

Converging regulations are eliminating the feasibility of region-specific PVC product lines. The European Commission’s Regulation (EU) 2023/2482 forbids DEHP in medical devices from July 2030 unless companies secure authorisation by January 2029. In California, AB 2300 requires manufacturers to brief customers on DEHP-free solutions by July 2025 and update compliance status by January 2028, effectively accelerating R&D timelines. The European Chemicals Agency proposal to expand the Authorisation List may capture 11 additional substitute phthalates, pushing manufacturers toward phthalate-free resins. With major markets now aligned, global suppliers face a single path: scale up non-PVC production or exit high-value regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 15-20% price premium vs. PVC equivalents | -1.4% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Supply-chain reliance on EVA resin imports | -0.9% | Global, concentrated in regions without petrochemical capacity | Medium term (2-4 years) |

| Qualification inertia in low-income countries | -0.7% | Low- and middle-income countries | Long term (≥ 4 years) |

| End-of-life recycling bottlenecks | -0.5% | Global, most acute in regions with advanced waste management | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

15-20% Price Premium vs PVC Equivalents

Even where legislation mandates DEHP removal, procurement managers must reconcile higher unit prices with flat operating budgets. PVC enjoys decades of process optimisation that deliver scale efficiencies; by contrast non-PVC bag lines still carry smaller batch sizes and higher resin costs. Large-volume commodities such as 0.9% saline amplify the absolute cost delta when hospitals purchase millions of units. Some systems postpone conversion until final rule-making deadlines remove low-cost PVC options entirely. Promisingly, Dow-Mitsui Polychemicals introduced biomass-derived EVA in 2024, signalling a route to eventual cost parity as bio-feedstock volumes rise. As environmental, health and disposal costs become line-item charges in value-based tenders, the apparent premium narrows, yet price remains a near-term hurdle in low-resource settings.

Supply-Chain Reliance on EVA Resin Imports

Producers operating outside North America and Northeast Asia depend on imported EVA, exposing them to exchange-rate risk and shipping disruptions. The sector’s experience during recent hurricane-related ethylene outages underscored the fragility of single-source supply for critical care products. Volatile crude oil prices translate almost directly into EVA contracts, undermining multi-year price agreements with hospitals. Governments are beginning to bundle localisation incentives with healthcare tenders, yet a full resin plant requires multi-billion-dollar investment and multi-year permitting. Alternative feedstocks—bio-ethylene or chemically recycled polyethylene—could broaden the supplier base once regulatory approvals are secured, but these remain medium-term prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Cost-Driven Polypropylene Challenge to EVA Leadership

EVA retained 47.05% non-PVC IV bags market share in 2025, benefiting from its flexibility and optical clarity that echo legacy PVC performance while eliminating DEHP. Nonetheless, the polypropylene subsegment is advancing at a 7.32% CAGR to 2031, powered by lower resin prices, better recyclability and simpler sterilisation protocols. The non-PVC IV bags market is witnessing innovation in bio-based EVA grades that match mechanical properties yet cut cradle-to-gate emissions by up to 75%. In cost-constrained public hospitals of emerging Asia, polypropylene’s price advantage is winning tenders even where EVA dominates in premium oncology centres. Regulatory dossiers show both resins meet USP <661.1> extractables limits, leaving procurement teams to trade off flexibility versus cost. Over the forecast horizon, the segment may converge toward a two-horse race unless copolyester ether (COPE) makers unlock mass-production pricing.

EVA suppliers are countering polypropylene’s momentum by highlighting cold-temperature crack resistance and longer sterilisation window. Multi-national resin producers are also investing in closed-loop take-back programs to collect and re-process used bags, creating a circularity narrative attractive to hospital sustainability officers. Where governments assign extended-producer-responsibility fees, these programs could offset EVA’s price premium, extending the resin’s dominance in the non-PVC IV bags market.

By Product: Multi-Chamber Systems Gain Clinical Favour

Single-chamber bags generated 65.10% of the non-PVC IV bags market size in 2025 on the back of broad application in hydration, antibiotics and analgesics. That said, multi-chamber variants are projected to post a 7.45% CAGR through 2031 as parenteral nutrition protocols become more sophisticated. Clinical studies link pre-filled triple-chamber nutrition bags to fewer compounding errors and improved calorie accuracy. Hospitals without 24-hour pharmacy services appreciate room-temperature shelf lives of up to 24 months, reducing wastage. B. Braun’s DUPLEX drug-delivery system, cleared by the US FDA in April 2025, demonstrated a 54% reduction in medication errors, illustrating the safety premium driving adoption.

Nevertheless, a practitioner survey reported in ECRI found that one-third of clinicians had encountered at least one error using multi-chamber parenteral nutrition, spotlighting the need for robust in-service training. Manufacturers are embedding colour-coded activation ports and audible snap indicators to address usability challenges. As hospital pharmacy budgets tighten, cost calculators showing labour savings from ready-to-use bags strengthen the commercial case, supporting double-digit penetration gains within the non-PVC IV bags market.

By Content: Frozen Mixtures Move Beyond Niche Uses

Liquid formulations accounted for 69.55% revenue in 2025 thanks to entrenched practice, ambient distribution chains and rapid turn-round compounding. Frozen mixtures, once limited to isolated oncology preparations, are expanding at a 7.58% CAGR as cold-chain logistics mature. These products safeguard potency of monoclonal antibodies and high-value chemotherapy agents during six-month storage cycles, attractive for tertiary hospitals operating regional drug repositories. Temperature-tracking labels embedded in non-PVC laminate films feed data to cloud dashboards, helping pharmacists maintain Good Distribution Practices and avoid costly discard.

Refrigerated shipping containers equipped with passive phase-change panels now permit cross-continent transfer without dry ice, lowering freight emissions. Although buying managers must amortise freezer capital costs, reduced drug obsolescence and emergency stockpiling benefits often offset the investment. In lower-latitude geographies where ambient heat challenges drug stability, adoption of frozen bags is expected to outpace the global average, lifting share within the non-PVC IV bags market.

By End-User: ASC Expansion Broadens Addressable Volume

Hospitals retained 70.85% consumption in 2025, driven by round-the-clock critical-care demand and high inventory turns. Yet ambulatory surgical centres are forecast to show a 7.54% CAGR into 2031, reflecting payer incentives to migrate day surgeries to lower-cost venues. ASCs value lightweight, puncture-resistant non-PVC bags that integrate seamlessly with compact smart pumps for post-operative analgesia. Medicare’s expanded bundled payments for outpatient joint replacements place a premium on error-free infusion therapy, giving DEHP-free devices a competitive edge.

Specialty clinics dedicated to rheumatology, gastroenterology and immunology represent an emergent user base, deploying infusion suites to administer biologics outside hospital walls. Home-health agencies form the smallest but fastest elongating slice, enabled by courier networks delivering RFID-tagged, stability-certified bags directly to patients. Vendors offering end-to-end cold-chain fulfilment and on-site waste pickup are differentiating themselves as reimbursement models increasingly reward total-cost-of-care savings rather than initial purchase price.

Geography Analysis

North America led with 40.85% of global revenue in 2025 as early DEHP bans and hospital sustainability charters created assured demand for compliant products. Widespread adoption in high-acuity neonatal intensive-care units underpins baseline volume, while state-level legislation such as California’s Toxic-Free Medical Devices Act removes residual PVC products from formularies. Growth now hinges on penetrating smaller community hospitals and Veteran Affairs facilities where budget sensitivity remains significant.

Europe follows as a mature but steadily expanding arena. The delayed EU cut-off date of July 2030 grants institutions ample transition time, enabling orderly retirement of PVC inventories. Procurement frameworks increasingly evaluate carbon-footprint disclosures alongside clinical performance, giving a boost to closed-loop recycling pilots led by Baxter in the United Kingdom. Variations in national reimbursement constrain rapid uptake in Southern Europe, but Nordic and German hospitals continue to set aggressive plastic-reduction benchmarks that ripple across continental group purchasing organisations.

Asia-Pacific is the fastest-growing territory, registering a 7.60% CAGR through 2031. Population-weighted healthcare capacity additions, particularly in China, India and Southeast Asia, are enlarging baseline demand for infusion disposables. Regional governments have announced incentives for domestic clean-room manufacturing plants, attracting joint ventures between global resin suppliers and local contract manufacturers. Meanwhile, fragmented regulatory oversight necessitates country-specific registrations, elongating approval timelines for foreign brands. Companies adept at technology transfer and local-content sourcing stand to capture above-market gains, accelerating broader adoption of the non-PVC IV bags market across the region.

Competitive Landscape

The non-PVC IV bags market features medium concentration, with fewer than 15 global players capable of high-volume medical-grade film extrusion, gamma sterilisation and multi-chamber welding. Barriers include ISO 13485 certification, biocompatibility validation and capital-intensive clean-room facilities. Leading firms emphasise incremental material innovation—such as peroxide-free cross-linking to cut extractables—alongside cost-down programmes to chip away at the enduring EVA premium.

Sustainability credentials are fast emerging as a differentiator. Baxter piloted a take-back scheme at Northwestern Memorial Hospital that diverted 6 tons of IV-bag waste from landfill, illustrating how circularity initiatives can fortify customer loyalty. Patent filings are trending toward smart-label integration and modular port systems; one recent US grant covers a plunger-sealed additive port that extends shelf life without compromising sterility. These innovations speak directly to usability and safety, aligning with hospital metrics tied to reimbursement.

M&A continues to reshape the field. Nordson’s USD 460 million purchase of Atrion in May 2024 secured three FDA-registered plants and a specialised fluid-delivery portfolio, plugging capability gaps in non-PVC bag production. Regional contestants are also gaining ground: several Southeast Asian firms now supply EVA film to domestic assemblers, reducing dependence on imports and creating price competition in mid-tier segments. Overall, supply chain resilience, regulatory agility and ESG performance are likely to dictate share shifts rather than disruptive technology alone.

Non-PVC IV Bags Industry Leaders

B. Braun Medical Inc

Baxter

JW Life Science

RENOLIT SE

Fresenius Kabi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: B. Braun Medical obtained FDA clearance for Piperacillin-Tazobactam in its DEHP-free, PVC-free DUPLEX dual-compartment system, reporting a 54% medication-error reduction.

- September 2024: Avient Corporation expanded healthcare TPU production, debuting NEUSoft grades for IV applications that comply with international medical standards.

- September 2024: Dow-Mitsui Polychemicals commenced commercial sales of biomass-based EVA and LDPE resins with identical mechanical properties to petro-sourced equivalents.

- May 2024: Nordson Corporation finalised its USD 460 million acquisition of Atrion Corporation, adding medical-grade fluid-delivery technologies and three US FDA-registered factories.

Global Non-PVC IV Bags Market Report Scope

As per the scope of the report, non-PVC IV bags are intravenous bags that are made up of non-polyvinyl chloride film. These bags have several advantages such as less pollution, safety, compatibility, lightweight, convenience, and low risk of contamination due to which there is a huge demand for oncology treatment. The Non-PVC IV Bags Market is segmented By Material (Ethylene Vinyl Acetate, Copolyester ether, Polypropylene, and Others), Product (Multi-Chamber, Single Chamber), Content (Liquid Mixture and Frozen Mixture), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Ethylene Vinyl Acetate (EVA) |

| Polypropylene (PP) |

| Copolyester Ether (COPE) |

| Others |

| Single-Chamber Bags |

| Multi-Chamber Bags |

| Liquid Mixtures |

| Frozen Mixtures |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Ethylene Vinyl Acetate (EVA) | |

| Polypropylene (PP) | ||

| Copolyester Ether (COPE) | ||

| Others | ||

| By Product | Single-Chamber Bags | |

| Multi-Chamber Bags | ||

| By Content | Liquid Mixtures | |

| Frozen Mixtures | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the non-PVC IV bags market?

The market is valued at USD 2.02 billion in 2026.

How fast is the non-PVC IV bags market expected to grow?

It is projected to expand at a 6.91% CAGR, reaching USD 2.82 billion by 2031.

Which material currently leads sales of DEHP-free IV containers?

EVA holds 47.05% share, though polypropylene is the fastest-growing alternative.

Why are multi-chamber bags gaining traction?

They simplify parenteral nutrition delivery and demonstrated a 54% error reduction in FDA-cleared systems.

Which region shows the highest growth potential?

Asia-Pacific is forecast to post a 7.60% CAGR through 2031 amid rapid healthcare infrastructure expansion.

What is the main restraint to wider adoption in emerging markets?

A 15-20% price premium over PVC remains a barrier where reimbursement budgets are tight.

Page last updated on: