Cell Culture Media Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

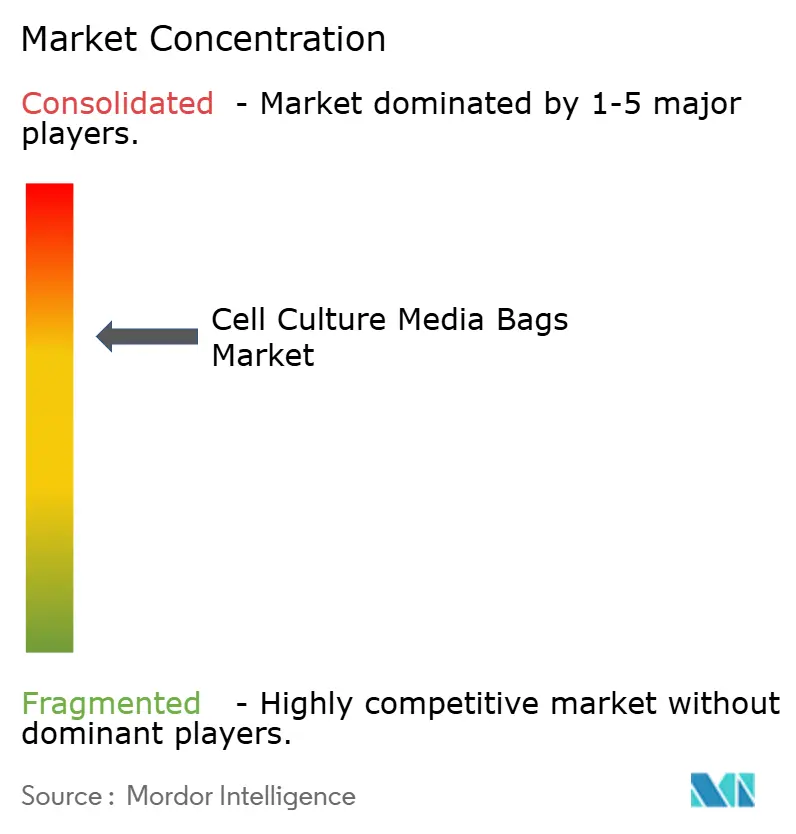

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cell Culture Media Bags Market Analysis by Mordor Intelligence

The cell culture media bags market size in 2026 is estimated at USD 1.71 billion, growing from 2025 value of USD 1.58 billion with 2031 projections showing USD 2.51 billion, growing at 8.05% CAGR over 2026-2031. Robust demand is tied to accelerating single-use bioprocessing adoption, expanding monoclonal antibody (mAB) pipelines, and renewed capacity investment by vaccine CDMOs. Intensifying focus on contamination-free operations, shorter changeovers, and sustainability credentials positions single-use media bags as a preferred alternative to stainless-steel vessels. Fluoropolymer innovations that lower leachable risk, coupled with vertical integration moves by major suppliers, create added momentum. At the same time, supply-chain vulnerability in premium-grade polymers and stricter regulatory oversight on extractables present countervailing pressures.

Key Report Takeaways

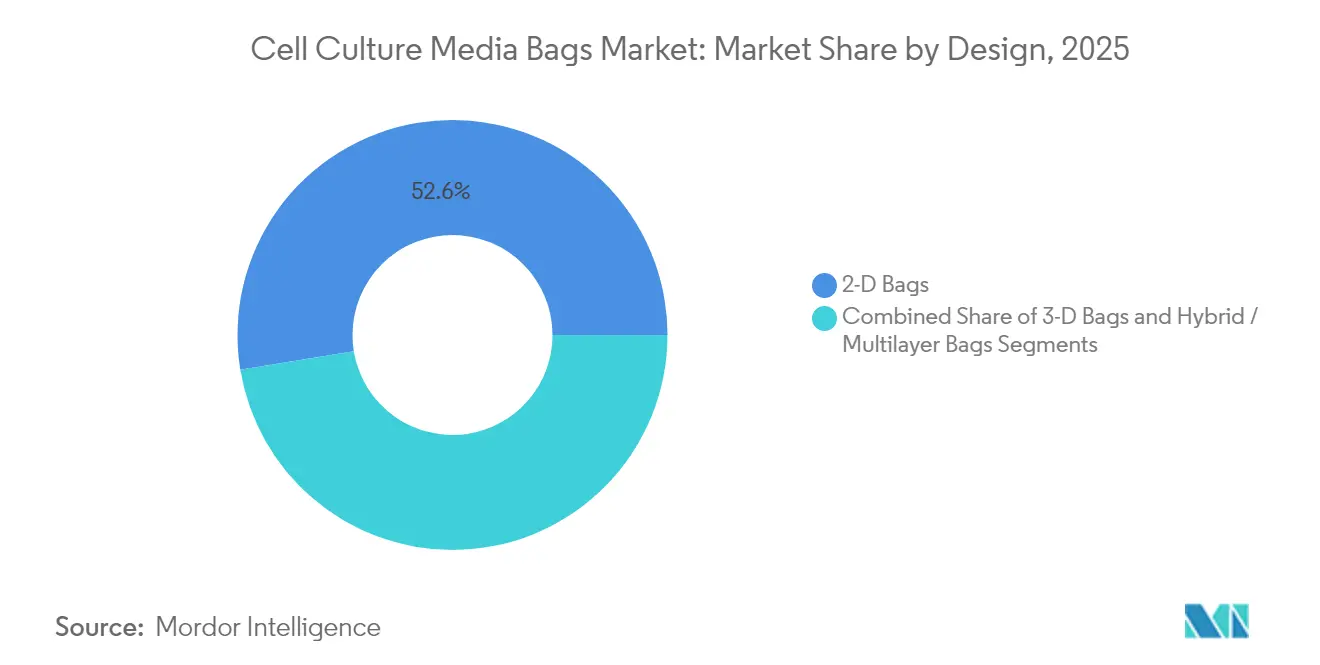

- By design, 2-D bags led with 52.58% of the cell culture media bags market share in 2025, while 3-D bags are forecast to expand at a 10.05% CAGR to 2031.

- By material, EVA captured 35.06% revenue share in 2025; fluorinated polymers such as PVDF are projected to grow at a 10.41% CAGR through 2031.

- By capacity volume, the 50–500 L segment accounted for 39.05% of the cell culture media bags market size in 2025; volumes above 500 L are set to rise at an 11.02% CAGR.

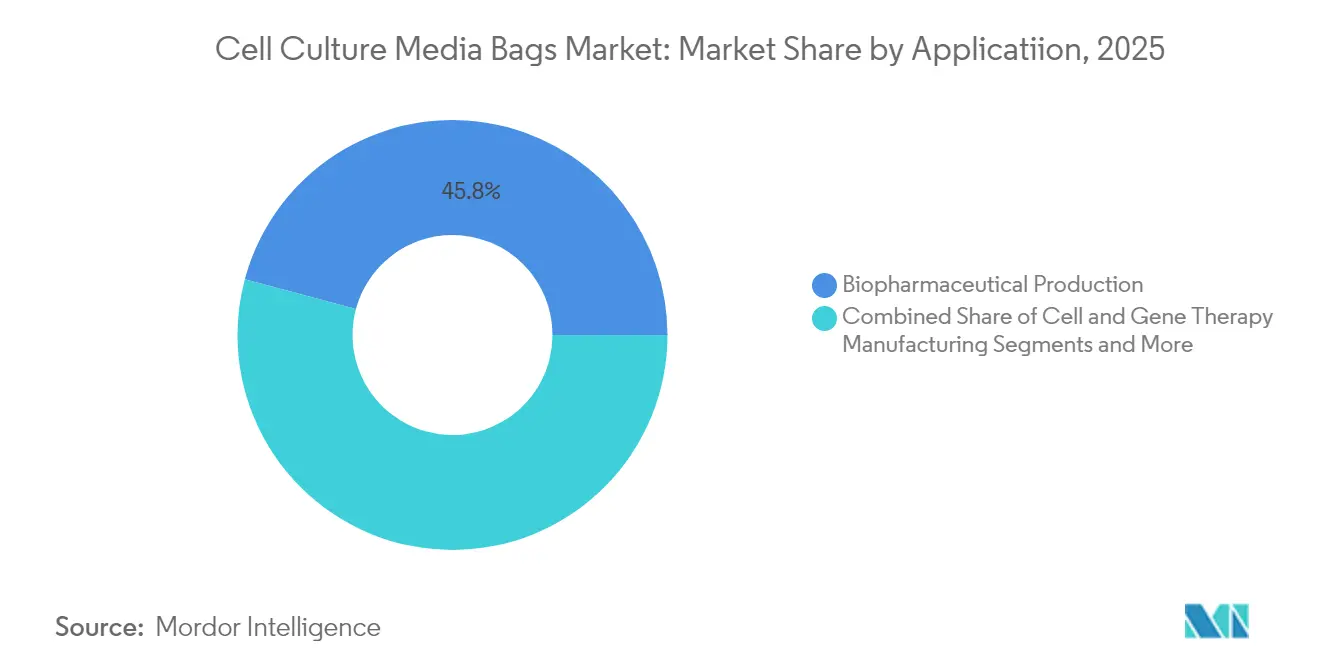

- By application, biopharmaceutical production held a 45.83% share of the cell culture media bags market size in 2025, whereas cell and gene therapy manufacturing is advancing at a 11.98% CAGR.

- By end user, pharmaceutical and biotechnology firms commanded 54.02% share in 2025; CDMOs/CROs exhibit the fastest growth at a 9.76% CAGR.

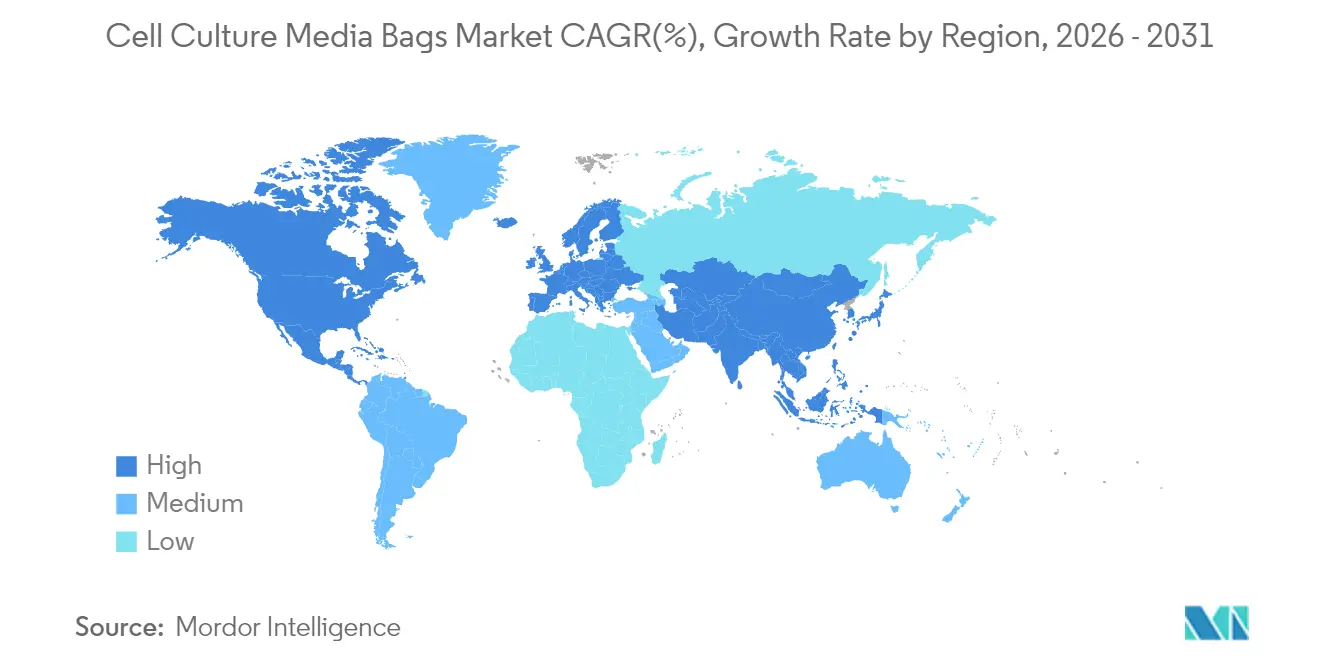

- By geography, North America controlled 38.62% of 2025 revenues, while Asia-Pacific is the quickest riser with an 11.36% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Culture Media Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Biopharma and mAB Production Pipelines | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Rapid Adoption of Single-Use Bioprocessing Systems | +2.1% | Global, led by North America, expanding in APAC | Short term (≤ 2 years) |

| Rising Stem-Cell & Regenerative-Medicine Clinical Trials | +1.2% | North America & EU core, emerging in APAC | Long term (≥ 4 years) |

| Capacity Build-Out of Vaccine CDMOs Post-COVID-19 | +0.9% | Global, with focus on APAC and emerging markets | Medium term (2-4 years) |

| Shift Toward High-Density Perfusion Micro-Bioreactors | +1.4% | North America & EU, technology transfer to APAC | Medium term (2-4 years) |

| Scope-3 Decarbonisation Mandates Favouring Lightweight Polymer Bags | +0.7% | EU-led, expanding to North America and multinational corporations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Biopharma and mAB Production Pipelines

Monoclonal antibody capacity additions such as Fujifilm Diosynth’s USD 1.6 billion Denmark expansion underscore the scale of demand for large-volume cell culture media bags market solutions. Higher-titer processes lengthen culture duration and increase protein concentration, requiring durable bag films that resist extractable buildup. Antibody-drug conjugate manufacturing further elevates contamination control needs, reinforcing the shift to pre-sterilised single-use assemblies. Geographic diversification of clinical trials into China and India is creating regional sourcing opportunities that still comply with FDA and EMA expectations.

Rapid Adoption of Single-Use Bioprocessing Systems

Changeover times that drop from weeks to 48 hours and lower cleaning requirements make single-use systems highly attractive for multiproduct CDMOs.[1]Boyd Biomedical, “Single-Use Systems Cut Changeover to 48 Hours,” BioProcess International, bioprocessintl.com Life-cycle assessments reveal smaller overall environmental footprints compared with stainless steel, dispelling myths about disposables. Cell and gene therapy producers regard single use as mandatory to mitigate cross-contamination between autologous batches, lifting demand for bespoke bag geometries compatible with perfusion and intensified processes.

Rising Stem-Cell & Regenerative-Medicine Clinical Trials

Clinical programs such as Mass General Brigham’s Parkinson’s trial rely on ultra-low-leachable fluoropolymer bags to preserve sensitive stem-cell phenotypes.[2]Mass General Brigham, “Clinical trial tests novel stem-cell treatment for Parkinson's disease,” Science Daily, sciencedaily.com As research settings scale toward commercial volumes, suppliers offering consistent bag performance from <5 L to 50 L gain an advantage. Stringent biocompatibility standards in regenerative medicine reward manufacturers capable of USP <87> and USP <665> compliance.

Capacity Build-Out of Vaccine CDMOs Post-COVID-19

Investments like Resilience’s USD 225 million fill-finish upgrade are expanding viral-vector and mRNA production footprints. These modalities demand bag films that tolerate low pH and solvent contact. Regional localisation in Asia-Pacific tightens lead times and reduces freight-related emissions, further propelling the cell culture media bags market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contamination & Leachable Risk Versus Rigid Vessels | -1.3% | Global, with heightened scrutiny in North America & EU | Short term (≤ 2 years) |

| Bio-Hazardous Waste-Disposal Cost Escalation | -0.8% | Developed markets, spreading to emerging economies | Medium term (2-4 years) |

| Volatility in Premium-Grade EVA & PE Resin Prices | -0.6% | Global, with regional variations in supply access | Short term (≤ 2 years) |

| Geopolitical Polymer-Supply Concentration | -0.4% | Global, with particular impact on Western manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Contamination & Leachable Risk Versus Rigid Vessels

Discovery of cytotoxic compounds such as bDtBPP has placed fresh emphasis on rigorous extractables testing, prompting FDA guidance that redefines acceptable risk thresholds. Transition from USP <88> to USP <87>/<665> raises qualification costs, encouraging suppliers to develop fluoropolymer-lined bags despite higher price points.

Bio-Hazardous Waste-Disposal Cost Escalation

Incineration remains the dominant end-of-life route, yet escalating fees and tightening landfill regulations add operating expenses. Early-stage recycling and pyrolysis pilots offer promise but require capital outlays and regulatory clarity before mainstream adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design: 3-D innovation drives premium adoption

2-D films retained 52.58% of the cell culture media bags market in 2025, reflecting legacy dominance in seed-train and buffer-prep tasks. However, 3-D formats are expanding at a 10.05% CAGR, powered by strong uptake in intensified perfusion and commercial-scale viral-vector suites. The flexible cube geometry improves mixing and mass-transfer rates while conserving floor space, attributes validated through computational fluid dynamics studies. Hybrid multilayer versions that combine EVA core layers with fluoropolymer contact surfaces target high-potency biologics and cell therapy batches, commanding price premiums that elevate revenue growth.

Demand for 3-D bags also rides on integration with automated pallet tanks that simplify logistics between upstream and downstream steps. As mAB facilities standardize on 2,000 L single-use bioreactors, suppliers are aligning 3-D bag designs with g-force limitations of modern rocking platforms. The cell culture media bags market size for 3-D configurations is projected to reach USD 1.01 billion by 2031, underpinning expanded capital investment by extrusion firms. Innovations such as laser-etched port reinforcements and pre-installed sensors reduce operator touches and help CDMOs accelerate turnaround times.

By Material: Fluorinated polymers lead innovation

EVA captured 35.06% revenue in 2025 because of its balance of clarity, weldability, and cost. Even so, fluorinated polymers such as PVDF are registering a 10.41% CAGR, outpacing the cell culture media bags industry average as stem-cell and gene therapy operators insist on ultra-clean contact layers. Regulatory flags over PFAS substance classes create future uncertainty, but interim demand remains high given limited non-fluorinated substitutes with comparable inertness.

Multi-layer structures that sandwich a thin PVDF surface between EVA support webs help manage cost while delivering leachable performance. Supplier R&D is also targeting bio-based tie layers that maintain gas-barrier traits yet improve end-of-life recyclability. The cell culture media bags market size for fluorinated films is set to surpass USD 0.6 billion by 2031 as mature facilities retrofit older suites to meet updated extractables limits. Conversely, PVC usage is tapering because of phthalate migration concerns, accelerating material mix shift toward high-performance alternatives.

By Capacity Volume: Large-scale drives growth

The 50–500 L range accounted for 39.05% of 2025 sales given its central role in clinical supply and pilot runs. Nevertheless, volumes above 500 L are rising at an 11.02% CAGR due to surge investments such as Lonza’s 330,000 L Vacaville site. High-volume demand benefits suppliers offering reinforced handle loops and wider-bore ports capable of rapid media transfer.

Process intensification lets manufacturers achieve >100 × 10^6 cells/mL viable density, which extends bag service life and raises scrutiny of film fatigue performance. The cell culture media bags market share held by >500 L formats is expected to climb to 17.30% by 2031 as scale-out strategies complement traditional scale-up. Suppliers are ensuring consistent mixing performance across bag sizes by preserving aspect ratios and sparger configurations, easing validation burdens for GMP operators.

By Application: Cell & gene therapy accelerates

Biopharmaceutical protein production remained the backbone with 45.83% share in 2025, reflecting entrenched antibody and recombinant protein programmes. The cell & gene therapy segment, however, is growing at 11.98% CAGR on the back of multiple FDA gene-therapy approvals in 2024. Autologous workflows demand small, closed, single-use systems that protect patient-specific batches from cross-talk.

Advanced therapy vectors often involve low pH or solvent steps that challenge conventional bag films, stimulating upgrades to fluoropolymer contact layers. The cell culture media bags market size tied to cell & gene therapy could top USD 0.54 billion by 2031, propelled by more than 1,200 ongoing trials worldwide. Vaccine manufacturing also contributes incremental volume, especially for mRNA platforms that require nuclease-free process contact.

By End User: CDMOs drive market expansion

In-house operations at pharma and biotech companies commanded 54.02% of 2025 demand; yet CDMOs and CROs are surging at 9.76% CAGR as innovators outsource to gain capacity agility. Outsourcers favour turnkey packages that bundle bags, connectors, and pre-validated sterilisation certificates to streamline regulatory filings.

Strategic alliances between bag suppliers and service providers integrate supply security with process-development expertise. The cell culture media bags market size linked to CDMOs is projected to exceed USD 0.9 billion by 2031. Academic labs and diagnostic firms offer steady but smaller growth, benefitting from miniature bag variants that reduce media consumption in high-throughput formats.

Geography Analysis

North America secured 38.62% of global revenue in 2025 thanks to deep clinical pipelines, mature GMP infrastructure, and FDA regulatory leadership. Investments such as Pfizer’s USD 200 million Massachusetts site and Fujifilm’s USD 1.2 billion North Carolina plant reinforce regional scale advantages. Canada and Mexico augment regional supply through niche production and cost-efficient fill-finish capacity. High uptake of cell and gene therapy platforms further boosts sophisticated single-use bag demand, particularly those lined with fluoropolymer contact layers for ultra-low extractables.

Asia-Pacific is the fastest-growing region, advancing at an 11.36% CAGR to 2031 on the back of Chinese and Indian policy support for domestic biologics. China’s regulatory harmonisation with ICH standards favours Western-compliant local media bag production. India’s cost-competitive manufacturing model attracts contract work from global sponsors, while South Korea leverages government incentives to build advanced therapy clusters. Japan transitions legacy stainless-steel suites toward flexible single-use platforms, although validation practices remain conservative. The cell culture media bags market size attributable to Asia-Pacific is projected to overtake Europe by 2028.

Europe maintains solid growth fuelled by German, UK, and French biologics hubs plus EU sustainability mandates that reward low-carbon materials. Circular-economy policies are catalysing R&D into recyclable films and closed-loop take-back schemes. Brexit reshapes supply logistics, but EMA adoption of FDA-aligned extractables guidance simplifies technology transfer. Italy and Spain add capacity for niche vaccines, whereas Eastern Europe remains a smaller yet rising player. Collectively, Europe emphasises carbon footprint disclosure in procurement, spurring adoption of life-cycle-assessed bag portfolios.

Regulatory Landscape

In the United States, products used in human ex vivo tissue and cell culture processing sit within an FDA medical device framework, including classification under 21 CFR 876.5885 for tissue culture media as a Class II device with special controls. This elevates expectations for documented performance and biocompatibility for contact materials used in associated fluid paths. FDA also issued Chemistry, Manufacturing, and Controls (CMC) flexibilities for developing human cellular and gene therapy products (January 2026), reinforcing risk-based justification approaches that influence how sponsors qualify single-use assemblies, including media bags, for smaller-batch and patient-specific manufacturing.

In Europe, EU GMP Annex 1 for sterile medicinal products has been fully applicable since August 25, 2024, formalizing contamination control strategy requirements that tighten expectations for single-use system integrity, sterilization, and supplier qualification in aseptic operations. Standards alignment is also shifting: FDA recognized ISO 10993-1:2025 (sixth edition) as a consensus standard on May 25, 2026, with a transition period running to July 1, 2029. For bag manufacturers, this points toward a risk-management-integrated biological evaluation approach (linked to ISO 14971) rather than relying on legacy test-only packages.

Value Chain Analysis

The value chain starts with upstream feedstocks and compounding of medical-grade polymers, including EVA and LDPE, plus barrier or high-inertness layers used in multilayer constructions. This is followed by film extrusion or casting, conversion into 2-D and 3-D formats through cutting and welding, and then integration of ports and connectors. Sterile assembly uses validated sterilization methods, commonly gamma irradiation, while quality documentation and testing (extractables and leachables data, biocompatibility evaluation, and lot traceability) run alongside production steps because end users incorporate bag packages into GMP filings and change-control processes.

Downstream, distributors and direct OEM supply support biopharma manufacturers, CDMOs and CROs, and advanced-therapy sites that often request preconfigured, closed assemblies. Bottlenecks cluster around constrained sterilization capacity and the availability of specialized resins and films, which has historically stretched lead times during demand spikes. In response, the chain is moving toward vertical integration, multi-sourcing, and longer-term supply agreements. Examples of resilience moves include Cytiva scaling capacity through its June 2025 multi-region investment program, as well as increased in-house production initiatives cited in the market ecosystem (including Nucleus Biologics developing internal bag manufacturing capability to reduce third-party dependency).

Competitive Landscape

The cell culture media bags market demonstrates moderate consolidation, with leading five suppliers accounting for an estimated 55% of 2024 revenue. Danaher’s USD 7.5 billion merger of Cytiva and Pall forms an expansive single-use platform covering media preparation through chromatography. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification unit extends its reach into downstream filtration, reinforcing a vertically integrated offering. Sartorius and Merck KGaA remain strong through differentiated film chemistries and regional manufacturing nodes that shorten lead times.

Technology rivalry centres on reducing leachable profiles without compromising weldability. Patent filings highlight multilayer fluoropolymer-EVA constructions and port designs that maintain integrity during gamma irradiation. Saint-Gobain leverages aerospace-grade polymer know-how to craft high-clarity, high-strength films for perfusion bioreactors. Smaller players such as Single Use Support carve niches in cold-chain bulk drug storage, aided by Novo Holdings’ 2024 majority stake purchase.

Geographic expansion remains a strategic priority. Major suppliers are commissioning extrusion lines in Singapore, Wuxi, and Wuppertal to mitigate freight and tariff risks. Sustainability offerings—including take-back programs and recycled resin blends—are becoming table stakes in EU tenders. Regulatory tightening around PFAS may reorder material hierarchies, giving an edge to companies with alternative high-performance polymers already in pipeline.

Cell Culture Media Bags Industry Leaders

-

ThermoFisher Scientific

-

Sartorius AG

-

Corning Incorporated

-

Danaher

-

Saint- Gobain Performance Plastics

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is widening around compliance-ready, low-extractables solutions and the documentation packages that de-risk qualification for GMP users as standards and guidance tighten. FDA recognition of ISO 10993-1:2025 on May 25, 2026, with transition through July 1, 2029, along with broader extractables and leachables scrutiny in single-use systems, creates room for suppliers that can deliver risk-based biological evaluation, robust E&L datasets, and change-control transparency across EVA and fluoropolymer-contact multilayer designs.

Capacity build-outs in single-use biologics and advanced-therapy manufacturing are also pulling demand for large-volume and customized bag configurations that integrate with automated mixing, filling, and closed transfer. Evidence in-scope includes single-use CDMO and GMP expansions such as Fujifilm Biotechnologies operationalizing a large single-use facility in Teesside, United Kingdom (February 2026), WuXi Biologics completing first GMP production at its MFG17 single-use facility in Shanghai (June 2026), and Bora Biologics expanding US single-use drug substance capacity across two FDA-registered facilities (July 2026). These investments increase the installed base of single-use trains that consume media bags across seed, expansion, and media preparation steps, and they strengthen the case for localized supply nodes and supplier qualification programs aligned with FDA and EU GMP expectations.

Recent Industry Developments

- June 2026: Cytiva completed an expansion of its Logan, Utah site, doubling liquid media production capacity and adding infrastructure such as filling manifolds, mixing tanks, and formulation booths. The added output supports higher-throughput single-use workflows where media preparation and transfer reliability directly influence upstream utilization and campaign turnaround.

- June 2025: Cytiva announced a USD 1.6 billion program to expand capacity for resins, filtration, single-use bags, and media across Europe, Asia-Pacific, and North America. The multi-continent footprint targets supply assurance and shorter lead times for GMP customers as demand rises for closed, contamination-controlled single-use operations.

- May 2024: Novo Holdings acquired a 60% stake in Single Use Support to expand fluid-management capabilities used in advanced-therapy manufacturing. The move strengthens the ecosystem around single-use handling, storage, and logistics, which supports broader adoption of sterile bag-based workflows across cell and gene therapy supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers sterile polymer bags used to store, mix, and transfer cell culture media in lab-scale and biomanufacturing workflows. The market size is measured as revenue generated from the sale of these bags across major end users and regions.

Scope exclusions: We exclude related accessories and hardware, such as tubing manifolds, bag holders, and rigid seed-train vessels, even if they are sold alongside media bags.

Segmentation Overview

-

By Design

- 2-D Bags

- 3-D Bags

- Hybrid / Multilayer Bags

-

By Material

- EVA

- LDPE

- PVC

- Polypropylene

- Fluorinated Polymers (e.g., PVDF)

- Others

-

By Capacity Volume

- <5 L

- 5 – 50 L

- 50 – 500 L

- >500 L

-

By Application

- Biopharmaceutical Production

- Cell & Gene Therapy Manufacturing

- Vaccine Manufacturing

- Stem-Cell & Academic Research

- Others

-

By End User

- Pharmaceutical & Biotechnology Companies

- CDMOs / CROs

- Academic & Research Institutes

- Diagnostic Laboratories

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping how demand is created across bioprocessing and lab workflows, then aligning the product boundary to what is actually purchased as a media bag. We used public sources including the US FDA biologics databases, NIH and other grant databases, USITC and UN Comtrade trade statistics for relevant polymers and lab consumables, OECD health and R&D indicators, and peer-reviewed articles indexed in PubMed that discuss single-use systems and contamination controls.

In parallel, we reviewed company annual reports and investor presentations to understand how product mix is described, how capacity additions are planned, and how quickly single-use systems are being adopted. We also used paid databases for company financials and business intelligence, patent databases, and shipment-level import-export views where applicable, mainly to cross-check timelines, manufacturing footprints, and product positioning. These desk sources are illustrative and not exhaustive, since many other public documents and filings were also used to collect data points and clarify assumptions.

Primary Interviews and Surveys

Primary work focused on suppliers, distributors, and end users, including biopharma manufacturing teams, CDMOs, and research labs. These groups see different parts of the buying process and replacement cycles. We used the interviews to validate typical bag volumes and configurations, the frequency of changeovers, pricing movement by material, and the practical split between 2-D and 3-D use cases across regions, so we could close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 20% | APAC: 49% |

| Mid tier: 50% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 21% | Managers: 43% | Americas: 20% |

Market-Sizing & Forecasting

Our core model starts from a top-down build where bioprocessing activity indicators are converted into an addressable demand pool for media bags, using usage intensity and replacement assumptions. In practice, we link demand to variables such as biologics and vaccine manufacturing scale-up signals, the mix of single-use versus fixed stainless workflows, average bag capacity ranges used for media prep and transfer, changeover frequency tied to contamination risk policies, and ASP differences by polymer type.

We then pressure-test those totals with selective bottom-up approximations, including rolling up representative supplier revenue splits for media bag lines, channel checks on distributor throughput, and sampled ASP times estimated unit volumes for common bag sizes. When gaps appear in bottom-up views, such as private company revenue opacity or bundled billing, we normalize using interview-led splits and apply conservative assumptions that can be rechecked.

For forecasting, we used scenario analysis supported by primary inputs, since adoption speed and capacity plans can shift quickly in biomanufacturing. The forward view is driven by expected biomanufacturing capacity additions, regional investment cycles, and the pace of single-use penetration in new lines. Assumptions are revisited whenever a major expansion or policy change is identified.

Data Validation & Update Cycle

Each build is checked through multiple passes, reviewing inputs, conversions, and resulting totals for odd jumps by region, by use case, and by implied unit economics. We compare outputs with independent signals, such as reported capacity expansions, trade flows for relevant materials, and the direction of pricing and lead times communicated in interviews, then we recontact sources when a variance cannot be explained.

Before sign-off, another analyst reviews the logic, the math, and the reasonableness of key assumptions, so the final number is not dependent on one viewpoint. Reports are refreshed annually, and interim updates are done when material events occur, followed by a final pre-delivery check to ensure clients receive the latest view.

Mordor Intelligence's Cell Culture Media Bags Market Size Compared With Other Published Estimates

Published estimates for this niche often do not line up because the boundary around what counts as a media bag is handled differently, and the assumed price and usage intensity can vary by end user. Timing also plays a role, since some sources anchor their value to different base years or apply different currency and inflation handling.

Capacity expansion announcements and primary channel checks on typical bag consumption per campaign are the evidence points that keep Mordor Intelligence aligned to the real purchasing pool for sterile polymer media bags, while also helping avoid pulling in adjacent single-use containers and accessory assemblies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.71 B (2026) | |

| Trade Journal A | USD 0.40 B (2022) | Uses an older base year and appears to count a narrower set of media storage bags, with limited adjustment for the shift toward larger volume and 3-D formats in biomanufacturing. |

| Industry Publisher B | USD 1.30 B (2025) | Seems to apply broader single-use bag demand signals and a simplified ASP path, which can pull in neighboring bag categories or over-smooth regional price dispersion. |

Across the three figures, the spread is mainly explained by year selection and by how tightly the product boundary is enforced around media bags versus nearby single-use bag categories. By grounding assumptions in repeatable activity signals and rechecking them through interviews, our final number stays traceable to clear drivers that can be updated as capacity plans and pricing change.

Key Questions Answered in the Report

What is the current size of the cell culture media bags market?

The market is valued at USD 1.71 billion in 2026.

How fast is the cell culture media bags market expected to grow?

It is forecast to expand at an 8.05% CAGR, reaching USD 2.51 billion by 2031 (2026-2031).

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region with an 11.36% CAGR through 2031.

Why are 3-D bag designs gaining traction?

They offer improved mixing, smaller footprints, and better compatibility with high-density perfusion cultures.

What material trends dominate the market?

EVA remains most common, while fluorinated polymers such as PVDF are gaining due to lower leachables.

How are sustainability goals influencing procurement?

Scope 3 emission targets push buyers toward lightweight single-use bags and encourage development of recycling programs.

Page last updated on: