IV Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

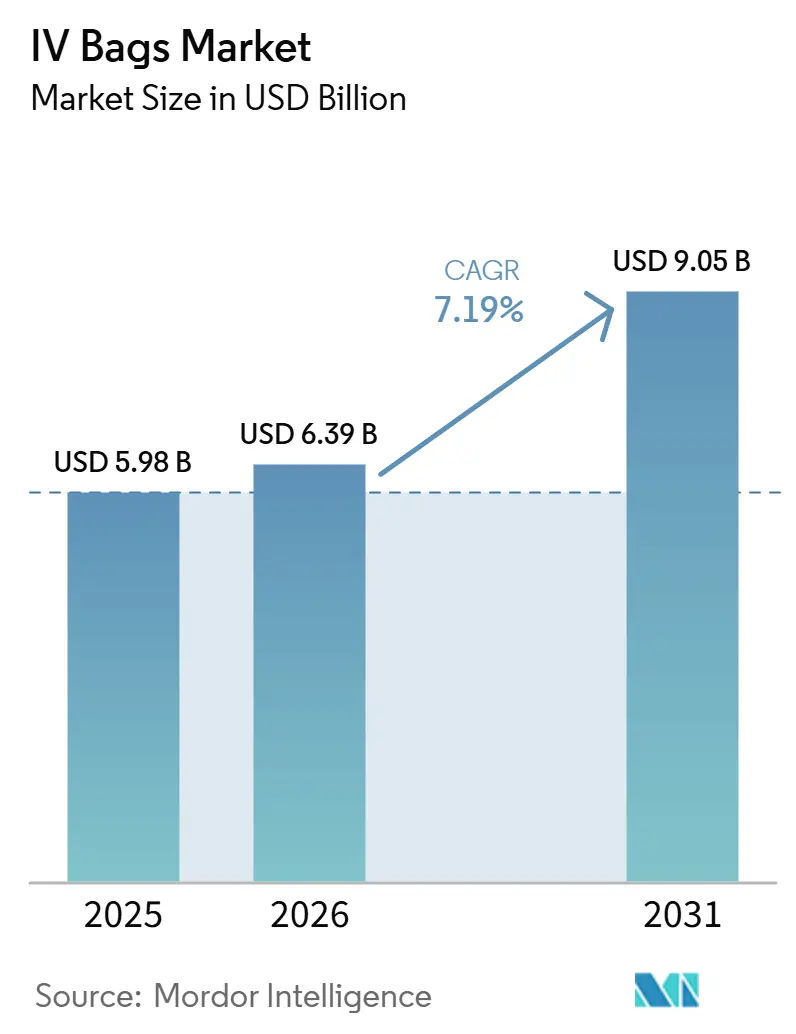

| Market Size (2026) | USD 6.39 Billion |

| Market Size (2031) | USD 9.05 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

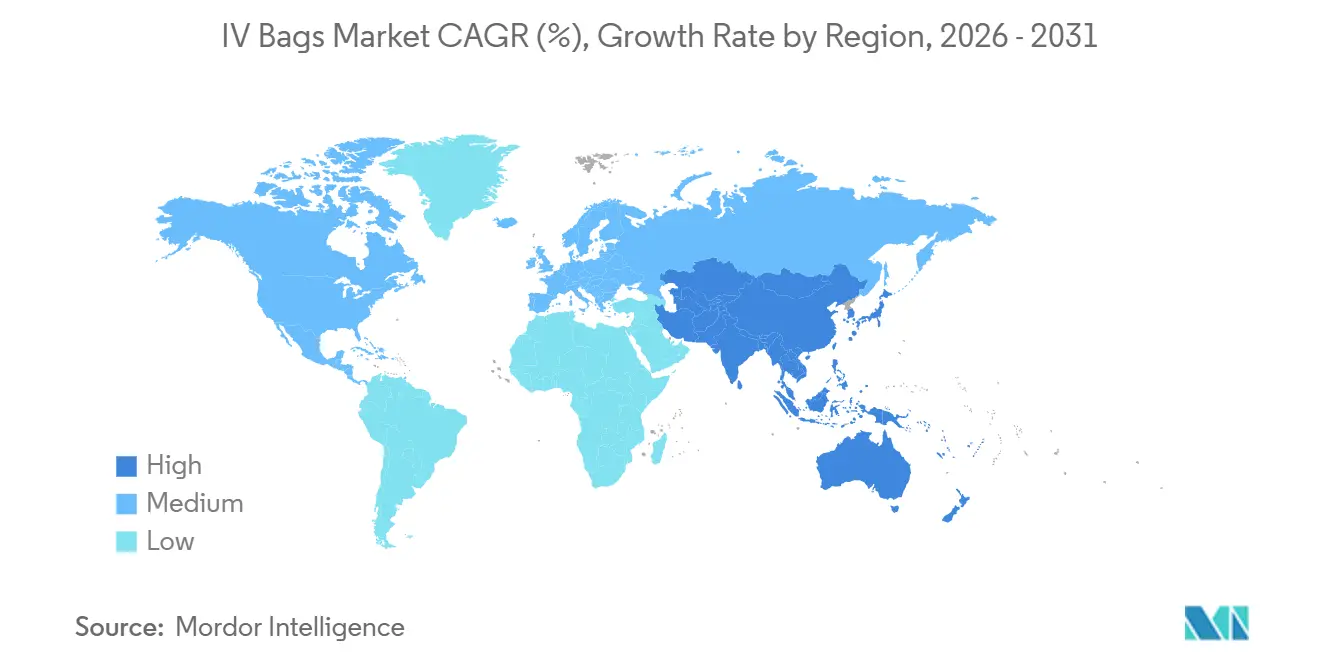

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

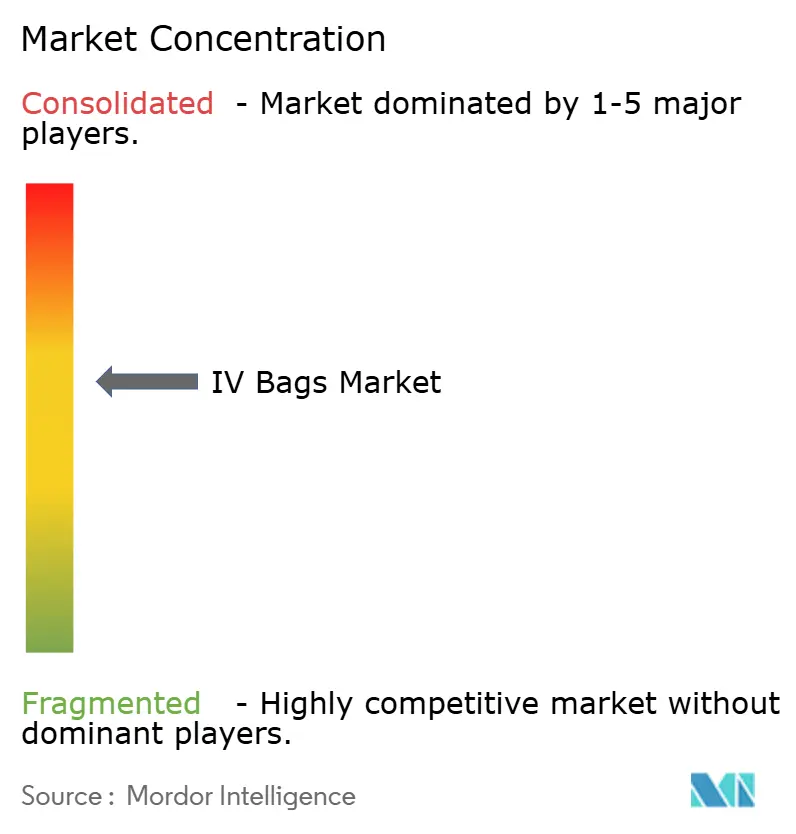

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IV Bags Market Analysis by Mordor Intelligence

The IV Bags Market size is projected to expand from USD 5.98 billion in 2025 and USD 6.39 billion in 2026 to USD 9.05 billion by 2031, registering a CAGR of 7.19% between 2026 to 2031.

Global regulations are tightening, leading manufacturers to pivot from traditional polyvinyl-chloride (PVC) formulations to ethylene-vinyl-acetate (EVA) and polyolefin chemistries. This shift, combined with a swift move towards home-based infusion care, is altering the economic landscape for manufacturers. In Europe and North America, demand for phthalate-free materials is rising, driven by restrictions from the Medical Device Regulation (MDR). Concurrently, in the U.S., an expanded reimbursement for home-infusion therapy is shifting volume away from centralized hospital pharmacies to decentralized specialty providers. To counteract input-price volatility, large integrated suppliers are locking in margins with multi-year resin contracts. In contrast, smaller contract manufacturers grapple with margin compression and face pressures of consolidation. On another front, mandates for RFID-enabled traceability and climate resilience stockpiles are unveiling new revenue opportunities. These rewards are particularly pronounced for suppliers adept at swift configuration changes and maintaining secure data connectivity.

Key Report Takeaways

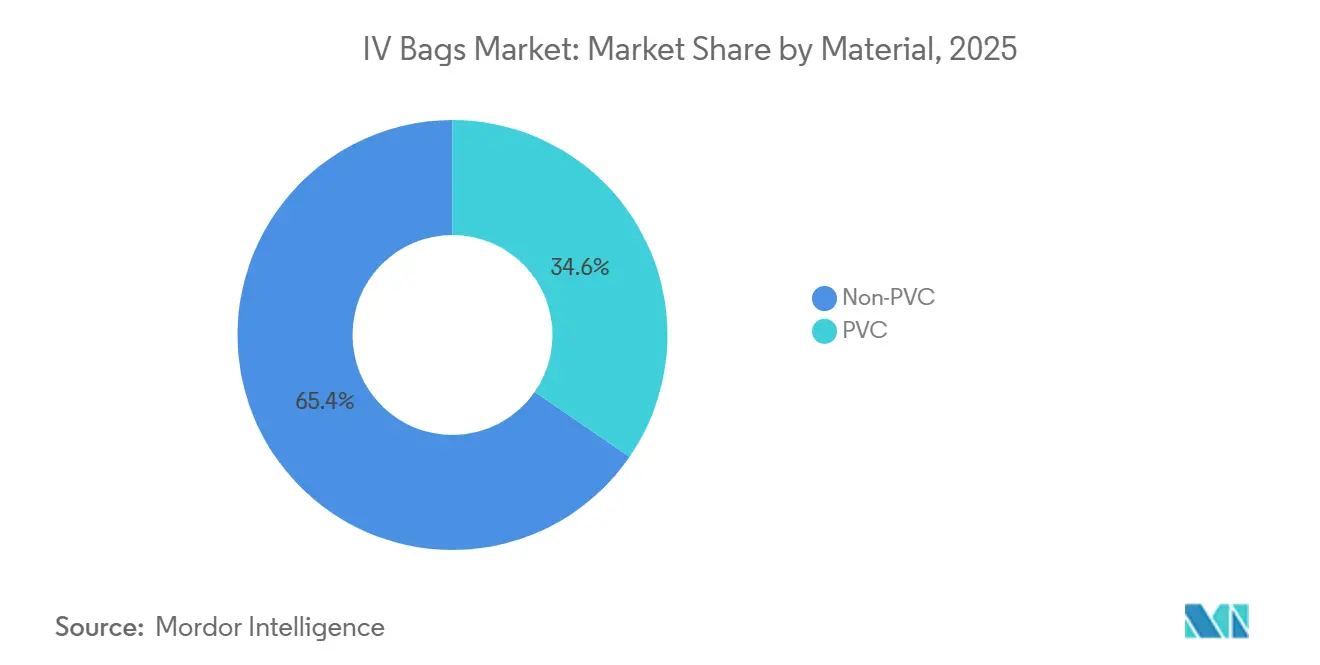

- By material, non-PVC solutions led with 54.60% of IV bags market share in 2025, and ethylene-vinyl-acetate (EVA) variants are forecast to expand at a 10.78% CAGR through 2031.

- By capacity, the 500–1,000 ml tier held 36.45% of the IV bags market size in 2025, whereas containers exceeding 1,000 ml post the quickest 11.05% CAGR to 2031

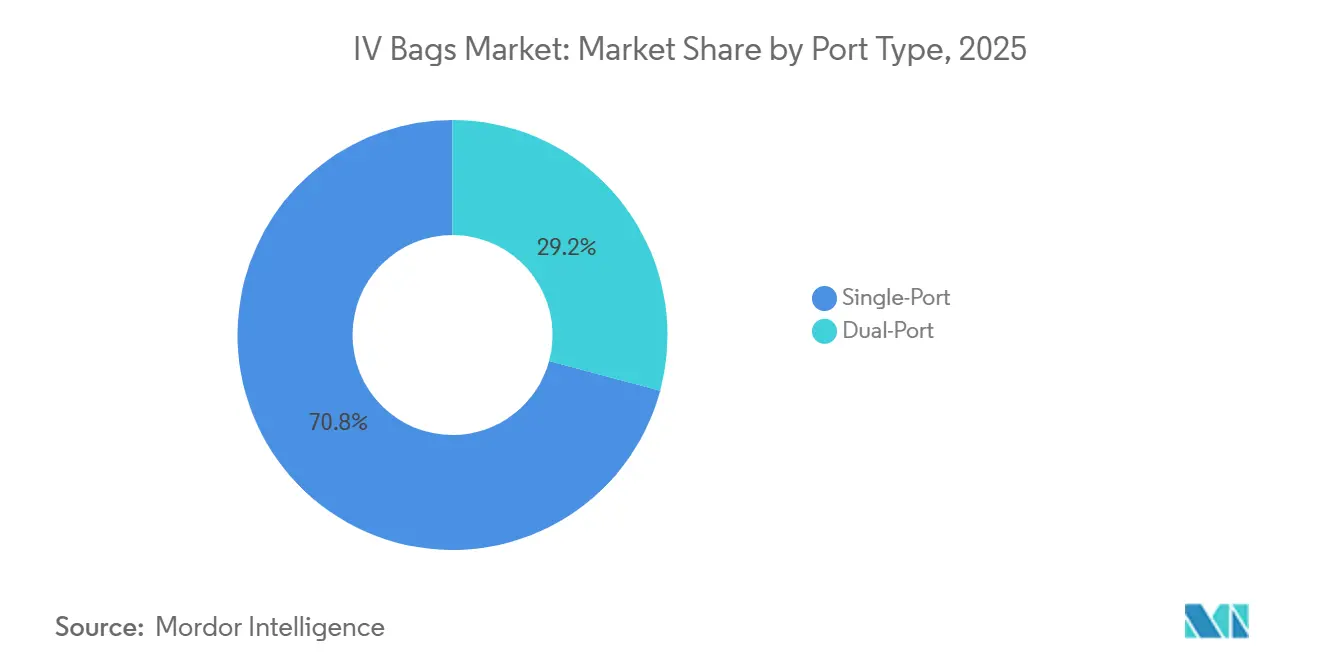

- By port type, single-port bags accounted for 71.00% of 2025 revenue, while dual-port designs are projected to advance at a 9.92% CAGR through 2031.

- By fluid type, crystalloids commanded 70.20% of the IV bags market size in 2025; colloids grow faster at an 11.28% CAGR through 2031.

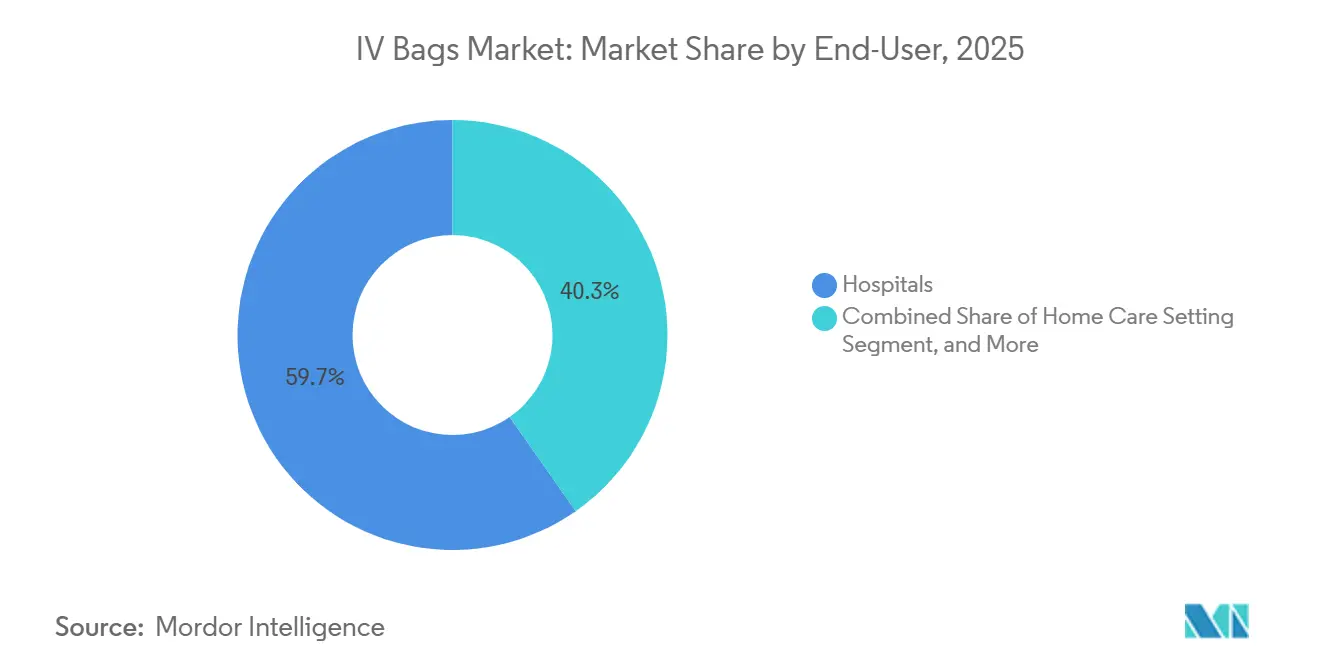

- By end user, hospitals retained 66.35% of the IV bags market share in 2025, whereas home-care settings recorded a 10.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IV Bags Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging Global Population Coupled with Increased Surgical Intervention Volumes | +2.1% | Global; highest intensity in North America and Europe | Long term (≥ 4 years) |

| Shift toward DEHP-free, non-PVC materials | +1.8% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Growth of home-infusion therapy models | +1.6% | North America core; expanding to Europe and urban Asia-Pacific | Medium term (2-4 years) |

| RFID/Unique Device Identification mandates | +1.3% | North America, Europe; pilot activity in Japan | Short term (≤ 2 years) |

| Government climate-resilience stockpiling | +0.9% | North America, Europe, Australia; emerging in GCC | Long term (≥ 4 years) |

| AI-driven demand-forecasting for pharmacies | +0.7% | North America, Western Europe; early uptake in Singapore, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Global Population Coupled with Increased Surgical Intervention Volumes

The increasing prevalence of degenerative musculoskeletal disorders among elderly populations has resulted in a sustained rise in joint replacement procedures worldwide. As life expectancy improves and healthcare systems prioritize mobility restoration and quality of life, the number of hip and knee arthroplasties continues to expand across developed healthcare markets. Consequently, increasing orthopedic surgical volumes directly translate into higher utilization of sterile IV bags, particularly in hospitals and orthopedic specialty centers, thereby strengthening long-term market demand. For instance, according to the OECD in November 2025, the OECD average reached 198 hip replacements and 156 knee replacements per 100,000 population. During the previous decade, hip replacement rates increased by 90 or more procedures per 100,000 population in Lithuania, Slovenia, and Poland, while knee replacement rates increased by 70 or more procedures per 100,000 population in Switzerland, Poland, Germany, and Australia. The report explicitly attributed these increases to aging populations and the growing prevalence of osteoarthritis.

Shift Toward DEHP-Free, Non-PVC Materials

As of May 2024, Europe's MDR mandates that di(2-ethylhexyl) phthalate content in pediatric and neonatal devices be capped at below 0.1% by weight. This regulation effectively pushes manufacturers to transition to non-PVC alternatives. Leading the charge, EVA copolymers emerge as the primary substitute. Their oxygen transmission rate, measured at 23 °C, is below 0.5 cc/100 in²/24 h. This characteristic enables the secure storage of oxygen-sensitive nutritional emulsions, eliminating the need for secondary barrier layers. Meanwhile, the U.S. FDA, in its January 2025 guidance, advocates risk assessments for devices with cumulative phthalate exposure exceeding 0.5 mg/kg/day. This nudge steers manufacturers towards polyolefin blends, especially for long-term infusions. Polyolefins boast a density of 0.90 g/cm³, significantly lighter than PVC's 1.38 g/cm³.[3]U.S. Food and Drug Administration, “Phthalate Alternative Guidance 2025,” fda.gov This density advantage translates to a 26% reduction in shipping weight, a crucial edge for intercontinental shipments from India and China. Suppliers who proactively initiated ISO 10993 biocompatibility testing ahead of the MDR deadline now enjoy a timing advantage of approximately 18 months.

Growth of Home-Infusion Therapy Models

By mid-2025, UnitedHealthcare, following the trend set by commercial insurers, designated home infusion as its preferred care site for chronic regimens lasting over 14 days, contingent on clinical appropriateness criteria. The National Home Infusion Association reported 3.2 million home-infusion days in the U.S. in 2025, a 19% increase from 2024, with anti-infectives accounting for 48% of sessions. There's a growing preference for 250- to 500-milliliter bags, aligning with single-dose antibiotics to minimize waste. While Europe sees only about 8% patient penetration, challenges persist due to hiring bottlenecks for certified home infusion nurses. However, the European Commission’s 2025 digital-health directive aims to standardize tele-supervision, potentially unlocking significant demand.

RFID/UDI Mandates for IV-Bag Traceability

Starting September 2024, U.S. manufacturers must encode GTINs and lot-expiration data on every IV bag, as mandated by the Unique Device Identification (UDI) rule. Hospital pilots showcase the benefits: After switching to RFID-enabled bags, Intermountain Healthcare reduced inventory stockouts by 34% across 24 facilities. EUDAMED, which became operational for IV bags in January 2025, mandates manufacturers to upload device master records within 60 days of their first distribution in the EU, thereby enhancing post-market surveillance. In 2025, ISO/IEC 27001 certification became the standard entry requirement for smart-bag suppliers, with both Fresenius Kabi and B. Braun successfully passing the audit.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile prices of medical-grade polymers | -1.4% | Global; acute pressure in Asia-Pacific and South America | Short term (≤ 2 years) |

| Lengthy medical-device approval backlogs | -1.1% | Europe (EU MDR backlog); secondary impact in North America | Medium term (2-4 years) |

| Bio-based resin supply-chain constraints | -0.6% | Global; most acute in Europe and North America | Long term (≥ 4 years) |

| Cyber-security certification delays | -0.5% | North America and Europe; emerging pressure in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Medical-Grade Polymers

PVC, EVA, and polypropylene resins track crude-oil swings. Limited supplier diversity inflates price amplitude during geopolitical shocks. Smaller manufacturers unable to hedge long-term contracts pass surcharges on, delaying tenders and tempering adoption of premium non-PVC bags.

Lengthy Regulatory Approval Timelines

Each formulation change triggers new 510(k) or MDR filings that can add 12–18 months to market entry, discouraging smaller entrants and slowing innovation cycles. Established players with dedicated regulatory teams hold a structural edge. IV bags must adhere to stringent sterility requirements. Regulatory bodies, such as the FDA, have noted that flexible plastic bags are vulnerable to microscopic punctures, which can result in contamination and necessitate detailed inspections. The packaging (bag) must undergo testing to ensure it does not react with or leach toxins into the solution throughout its shelf life, requiring long-term stability studies (e.g., 12-month studies for Parenteral Nutrition bags).

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Non-PVC Solutions Drive Safety Transformation

Non-PVC formulations captured 65.40% of 2025 revenue and are forecast to log a 7.37% CAGR through 2031. EVA’s chemical inertness makes it ideal for oncology drugs, while polyolefins offer steam-sterilization stability for parenteral nutrition. The IV bags market size attributable to non-PVC lines is estimated at USD 9.05 billion by 2031, reflecting the shift away from PVC due to its plasticizer content. California and Massachusetts have already mandated DEHP-free procurement, and donor-funded green tenders in Africa signal broader global catch-up.

PVC remains entrenched in price-sensitive segments, yet its total-cost advantage erodes once disposal levies and carbon accounting enter the calculus. Mold-replacement cycles after 2027 provide a natural pivot point at which converters are likely to reinvest in future-proof tooling compatible with EVA or PP. This material re-mix raises switching barriers and enlarges profit pools for first movers.

By Capacity: Large-Volume Containers Capture Surgical Demand

Bags sized 251 - 500 ml held a 56.84% share in 2025 as they meet standard peri-operative hydration needs. Containers exceeding 1,000 ml are projected to clock an 8.82% CAGR, fueled by longer organ-transplant and trauma procedures requiring continuous resuscitation.

Micro-volume 0–250 ml bags service pediatrics and niche biologics. Their unit volumes outpace revenue, but emerging closed-system connectors promise margin uplift by bundling safety technology. Across all capacities, RFID tagging expedites expiry tracking and reduces pharmacy spoilage, making digital labeling an implicit tender requirement for hospital procurement teams.

By Port Type: Dual-Port Systems Enable Complex Therapies

Single-port designs accounted for 70.83% of 2025 shipments due to their simplicity and lower price. Dual-port configurations, however, deliver a 7.78% CAGR, enabling simultaneous infusion of drugs and nutritional fluids without line changes. BD’s needle-free SmartSite valve supports repeated access while mitigating needlestick risk, a feature prized in oncology wards with high manipulation frequency.

Port innovation now integrates with smart-pump auto-identification: RFID-enabled ports preload pump libraries, reducing wrong-drug errors by 30% in early-adopter hospitals. As biologic combo-therapies gain traction, multi-manifold bags will emerge, although regulatory verification may slow scale-up beyond tertiary centers. A 2025 Journal of Hospital Infection study found dual-port adoption cut microbial contamination risk by 22%. Nursing inertia remains a hurdle; 58% of respondents in an American Nurses Association survey prefer single-port bags, but the FDA’s 2024 clarification that additive-only ports are not drug-device combos streamlines clearance and supports new entrants.[4]American Society of Clinical Oncology, “Closed-System Transfer Recommendations 2025,” asco.org

By Fluid Type: Crystalloids Dominate, Colloids Accelerate

Crystalloids captured 68.27% revenue in 2025 thanks to broad indications. Normal saline remains a staple, while balanced formulations such as Ringer’s lactate gain surgical favor to avoid hyperchloremic acidosis.

Colloids, especially 5% and 20% human albumin, post an 7.59% CAGR through 2031, driven by critical-care applications and compelling survival data in decompensated cirrhosis. Grifols’ Albutein trial showed improved five-year outcomes, spurring reimbursement across 17 countries. Synthetic starches remain under safety review, prompting hospitals to shift their formularies toward natural colloids. Blood and blood-product bags are exempt from DEHP bans, yet innovation in pathogen reduction extends platelet shelf life. Within crystalloids, balanced solutions such as lactated Ringer’s gained ground after the SMART follow-up demonstrated a 1.8 % absolute reduction in adverse kidney events, nudging critical-care societies to elevate balanced fluids to first-line status.

By End User: Hospitals Lead, Ambulatory Surgical Centers Transforms

Hospitals accounted for 59.71% of the 2025 volume, leveraging group purchasing organizations to negotiate discounts. Nevertheless, home-care channels expand at a 7.60% CAGR as insurers reimburse outpatient infusions to cut bed-day costs. The IV bags market in home settings will be supported by subscription models that bundle disposables and nurse visits.

Ambulatory surgical centers act as a mid-growth niche, requiring rapid-turnover bags that integrate with electronic medication administration records. Veterinary clinics represent an ancillary yet double-digit growth avenue, with scaled-down port gauges tailored to small-animal catheters, reinforcing diversification beyond human medicine.

Geography Analysis

North America accounted for 41.75% of 2025 revenue, totaling USD 2.50 billion. Federal incentives promote domestic sterile-fluid output, while California’s DEHP ban cements material migration toward EVA. The IV bags market in the United States is forecast to reach USD 3.68 billion by 2031. Recent hurricane-sparked shortages led Congress to propose tax credits for redundant manufacturing lines, making geographic diversification a procurement criterion.

Europe displays slower topline expansion yet sharper product sophistication. Germany and France already report non-PVC adoption above 60%, and the United Kingdom trialed a closed-loop polyolefin recycling scheme that cut clinical-plastic emissions by 28%, with a national rollout slated for 2027. MDR compliance costs escalate entry barriers, protecting incumbents endowed with regulatory bandwidth.

Asia-Pacific delivers the fastest 7.90% CAGR. China’s ongoing hospital build-out and India’s expanding surgical volumes underpin unit demand, albeit still skewed toward PVC on price grounds. Australia committed AUD 20 million (USD 13.2 million) to scale Baxter’s Western Sydney plant, bolstering self-reliance and signalling broader regional industrial policy shifts. Medical-tourism hubs like Thailand are upgrading to dual-port EVA systems, aligning with visiting patients' expectations for Western-grade safety. India’s USD 180 million production-linked incentive program spurred Poly Medicure’s USD 65 million expansion to 600 million units by 2027.

South America and the Middle East & Africa each contribute under 12% of revenue but promise pockets of double-digit growth. Brazil’s private hospital chains are standardizing single-use protocols, while Gulf states procure large-volume parenterals for trauma centers aligned with expanding road infrastructure.

Competitive Landscape

The IV bags market is moderately consolidated: the top five vendors command roughly 68% of 2024 revenue. Baxter, Fresenius Kabi, and B. Braun leverage multi-continent production footprints and vertically integrated film extrusion to lock in long-term tenders. Strategy emphasis is shifting from unit capacity to value-adding service ecosystems. Baxter’s Spectrum IQ pump interfaces exclusively with its own bags, driving 97% drug-library compliance within one month of rollout.

Tier-2 players such as ICU Medical and Terumo scale via alliances: the 2024 ICU Medical–Otsuka joint venture will add 25 million units of annual North American output by 2026, diffusing single-source concentration risk. Chinese manufacturers Sichuan Kelun and CSPC challenge incumbents on price in tender markets, accelerating commoditization in PVC but struggling to penetrate non-PVC premium tiers without Western regulatory clearances.

Innovation vectors center on material sustainability and digital integration. Suppliers are patenting bio-based polyolefins and piloting hospital take-back loops to capture resin for closed-loop recycling. Concurrently, RFID-enabled ports feed infusion data into EMRs, enabling predictive maintenance and reducing human error. Dual-chamber drug-device combinations push up approval complexity but promise higher margins and stronger clinical lock-in.

IV Bags Industry Leaders

Baxter international Inc.

B. Braun SE

Fresenius Kabi AG

Otsuka Holdings Co. Ltd

ICU Medical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Australian government committed AUD 20 million to expand Baxter’s Western Sydney plant, lifting capacity to 80 million units by 2027.

- May 2025: ICU Medical and Otsuka Pharmaceutical Factory launched a joint venture to scale IV-solution manufacturing, operations begin Q2 2025.

Global IV Bags Market Report Scope

As per the scope of the report, IV bags are containers used to store a liquid for intravenous administration to patients, suspended from slender poles called IV poles. IV fluids prevent dehydration, maintain blood pressure, or give patients medicines or nutrients.

The IV bags market is segmented by material type, capacity, port type, fluid type, end-user, and geography. By material, the market is segmented into polyethylene, polyvinyl chloride, polypropylene, and other materials. By capacity, the market is segmented into 0-250 ml, 251-500 ml, 501-1000 ml, and >1000 ml. By port type, the market is segmented into single-port and dual-port. By fluid type, the market is segmented into crystelloid, colloids, blood, and blood products, and others. By end-user, the market is segmented into hospitals, clinics, home care settings, ambulatory surgical centers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| PVC | |

| Non-PVC | Polyolefin (PP) |

| Ethylene-Vinyl-Acetate (EVA) | |

| Others |

| 0-250 ml |

| 251-500 ml |

| 501-1,000 ml |

| >1,000 ml |

| Single-Port |

| Dual-Port |

| Crystalloids | Normal Saline (0.9% NaCl) |

| Dextrose Solutions | |

| Ringer’s Lactate | |

| Colloids | Albumin |

| Dextran & Others | |

| Blood & Blood Products | |

| Others |

| Hospitals |

| Clinics |

| Home-Care |

| Ambulatory Surgical Centres |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | PVC | |

| Non-PVC | Polyolefin (PP) | |

| Ethylene-Vinyl-Acetate (EVA) | ||

| Others | ||

| By Capacity | 0-250 ml | |

| 251-500 ml | ||

| 501-1,000 ml | ||

| >1,000 ml | ||

| By Port Type | Single-Port | |

| Dual-Port | ||

| By Fluid Type | Crystalloids | Normal Saline (0.9% NaCl) |

| Dextrose Solutions | ||

| Ringer’s Lactate | ||

| Colloids | Albumin | |

| Dextran & Others | ||

| Blood & Blood Products | ||

| Others | ||

| By End User | Hospitals | |

| Clinics | ||

| Home-Care | ||

| Ambulatory Surgical Centres | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the estimated global value of the IV bags market in 2026 and its projected revenue by 2031?

It is USD 6.39 billion in 2026 and is forecast to rise to USD 9.05 billion by 2031, reflecting a 7.19% CAGR.

Which non-PVC materials are gaining the most traction as DEHP-free alternatives?

Ethylene-vinyl-acetate (EVA) and polyolefin blends lead adoption, together holding 7.37% share in 2025 and expanding at a 10.78% CAGR through 2031.

Which geographic region currently contributes the largest revenue for IV bags?

North America accounts for 41.75% of 2025 turnover, supported by advanced healthcare infrastructure and early regulatory moves on DEHP elimination.

How quickly are home-infusion applications for IV bags expanding?

Home-care settings are logging an 6.26% CAGR to 2031 as payers reimburse at-home intravenous antibiotics, nutrition and immunoglobulin therapy.

When does Californias law require full removal of DEHP from intravenous solution containers?

The Toxic-Free Medical Device Act mandates DEHP-free IV bags no later than 1 January 2030, triggering nationwide material transitions.

Page last updated on: