Pressure Infusion Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

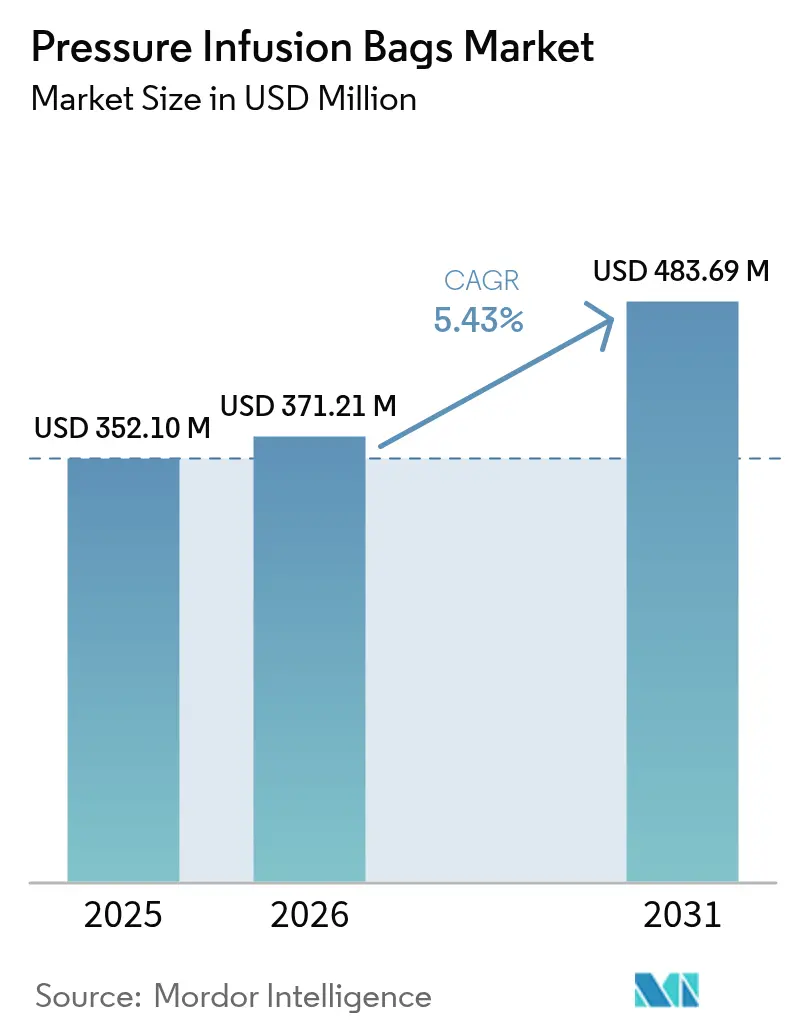

| Market Size (2026) | USD 371.21 Million |

| Market Size (2031) | USD 483.69 Million |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pressure Infusion Bags Market Analysis by Mordor Intelligence

Pressure Infusion Bags market size in 2026 is estimated at USD 371.21 million, growing from 2025 value of USD 352.10 million with 2031 projections showing USD 483.69 million, growing at 5.43% CAGR over 2026-2031.

Rapid fluid resuscitation protocols in emergency medicine, growth in surgical volume, and wider intensive-care adoption continue to pull demand upward. Disposable systems gain momentum as infection-control mandates tighten, while integrated pressure-monitoring valves move from pilot projects to routine procurement. Raw material cost inflation, especially in medical-grade nylon and polyurethane has raised device production costs. However, premium products with AI-enabled flow control are still commanding price resilience in high-acuity settings. Mid-range pressure devices (250-300 mmHg) remain the workhorse of hospital practice, yet demand for higher-pressure bags accelerates alongside evolving trauma guidelines and military medicine requirements.

Key Report Takeaways

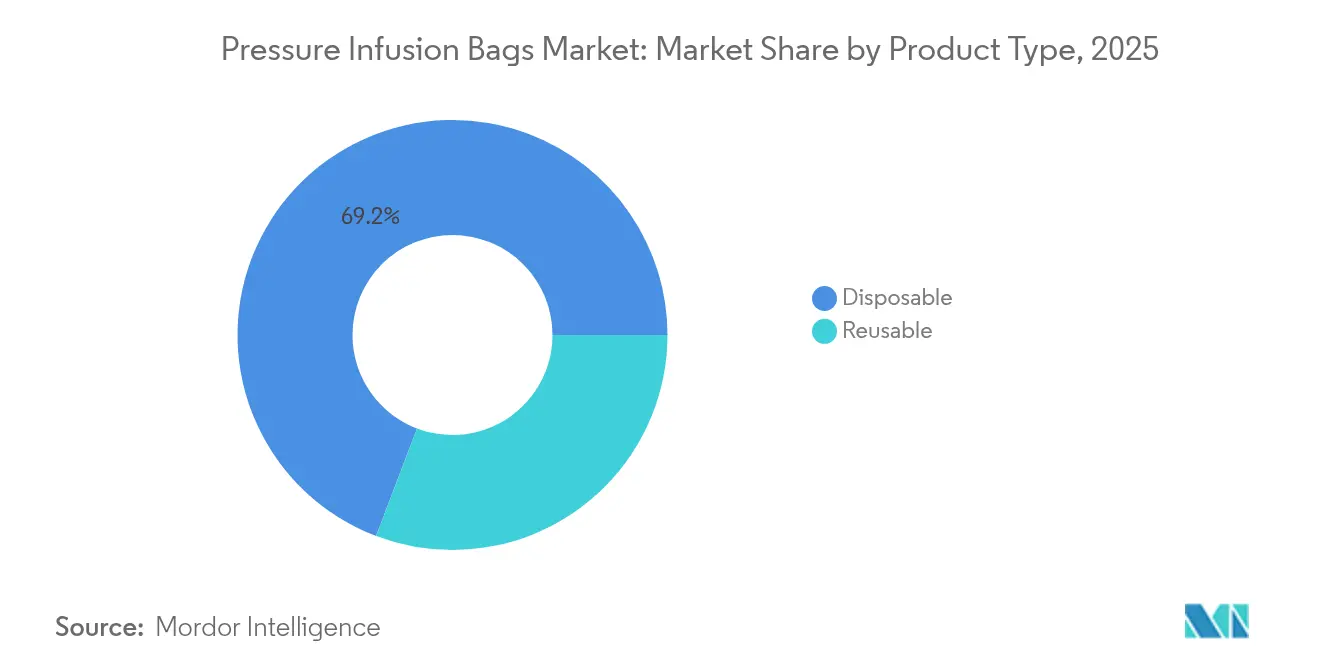

- By product type, disposable bags led with 69.22% of the pressure infusion bags market share in 2025, and it is projected to expand at a 6.08% CAGR through 2031.

- By material, nylon accounted for 43.85% share of the pressure infusion bags market size in 2025; PVC-free alternatives are the fastest-growing group at 6.97% CAGR.

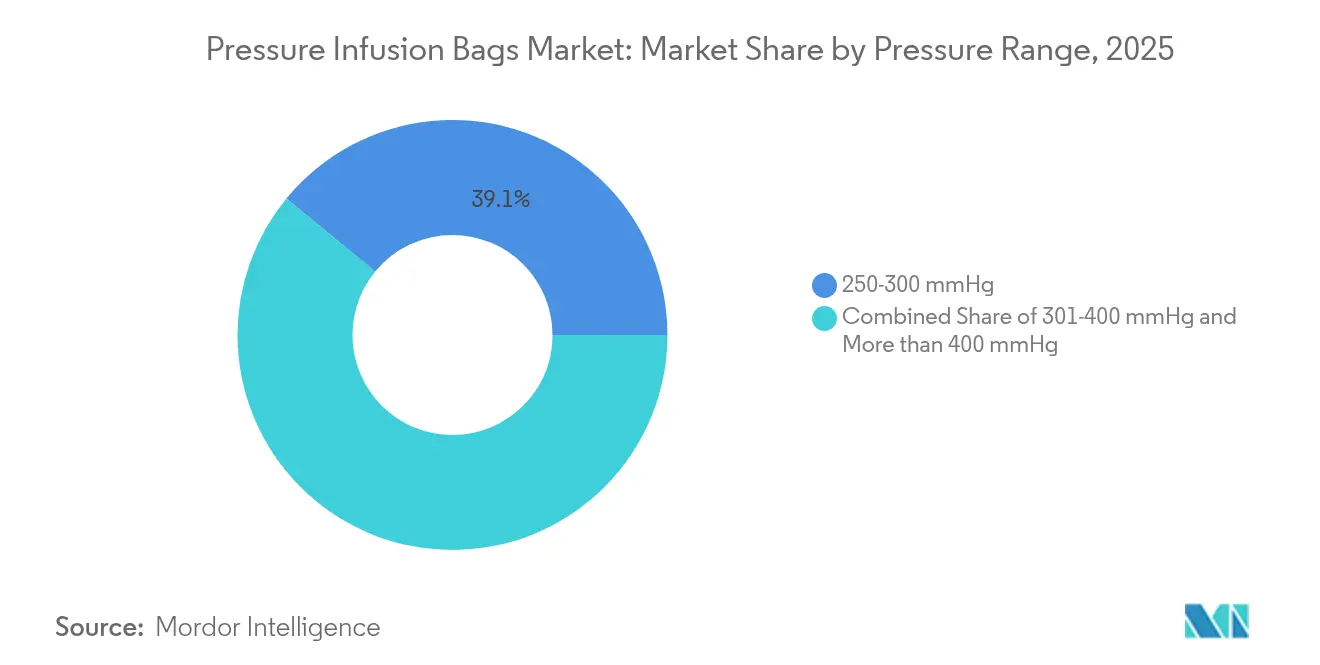

- By pressure range, the 250-300 mmHg segment held a 39.05% share of the pressure infusion bags market in 2025, while 301-400 mmHg systems recorded the highest projected CAGR at 8.21% to 2031.

- By application, blood and drug infusion captured 56.85% revenue share in 2025; rapid fluid resuscitation is advancing at a 7.28% CAGR through 2031.

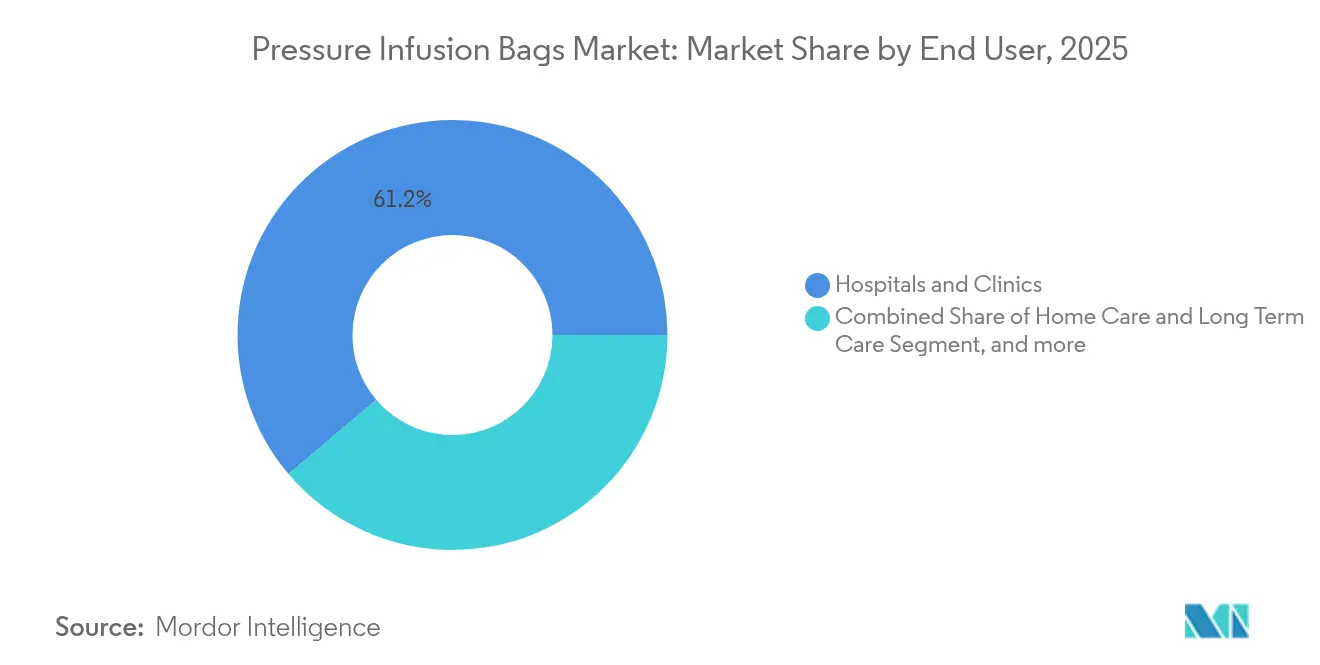

- By end user, hospitals and clinics controlled 61.20% of the pressure infusion bags market size in 2025, whereas ambulatory surgical centers are set to grow at 5.58% CAGR.

- By geography, North America commanded 37.10% revenue in 2025; Asia-Pacific is forecast to post the fastest regional CAGR at 5.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pressure Infusion Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases & trauma cases | +1.2% | Global, strongest in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rapid adoption of disposable bags in OR & ED | +0.9% | North America & EU lead; APAC catching up | Medium term (2-4 years) |

| Expansion of ambulatory/field-care & military medicine | +0.7% | Global, conflict zones and remote healthcare sites | Medium term (2-4 years) |

| Technological shift to integrated pressure-monitoring valves | +0.8% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Sustainability push for PVC-free bag materials | +0.6% | Europe leads; North America and APAC follow | Long term (≥ 4 years) |

| AI-assisted closed-loop infusion systems | +0.5% | Advanced systems in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases & Trauma Cases

Trauma centers increasingly report complex polytrauma presentations requiring rapid, high-volume infusions that favor reliable pressurized delivery systems. Combat casualty care underscores this need: the U.S. Department of Defense’s Golden Hour initiatives highlight pressure-assisted devices capable of continuous operation for two days in austere environments.[1]U.S. Department of Defense, “Golden Hour Extended Support Program,” defense.gov Tactical Combat Casualty Care Guidelines 2024 recommend early intravenous or intraosseous access supported by portable pressure systems for hemorrhagic shock.[2]Tactical Combat Casualty Care Committee, “TCCC Guidelines 2024,” health.mil Parallel demographic shifts, aging populations, and urban mobility–related injuries are boosting unit consumption in civilian emergency departments worldwide.

Rapid Adoption of Disposable Pressure Bags in OR & ED

Hospital infection-control committees widely favor single-use bags after outbreaks linked to inadequately reprocessed reusable cuffs. B. Braun’s DUPLEX platform demonstrated a 54% reduction in medication-error incidence and shaved nearly four minutes off each dose preparation cycle, a benefit amplified during mass-casualty events.[3]B. Braun Medical Inc., “DUPLEX Drug Delivery System,” bbraunusa.com As labor shortages inflate reprocessing costs, disposables offer an attractive total-cost profile, turning once-marginal price premiums into operational savings.

Expansion of Ambulatory/Field-Care & Military Medicine

Home-based infusion therapy already exceeds, with nearly half of the pipeline biologics formulated for infusion delivery. Field-care scenarios from humanitarian disasters to military deployments demand ruggedized, battery-efficient pressure infusion systems capable of accurate flow under extreme temperature and vibration, spurring purpose-built designs validated by the U.S. Army’s Automated Battlefield Trauma System.

Technological Shift to Integrated Pressure-Monitoring Valves

Real-time pressure sensing reduces manual cuff checks, mitigates occlusion risk, and flags infiltration earlier. Clinical trials of inline force-sensor arrays cut alarm response times by over 40 seconds, improving critical-care workflow. Tekscan’s FlexiForce sensors add automatic occlusion detection, allowing staff to intervene before adverse events escalate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled infusion therapists in low-income regions | -0.8% | Sub-Saharan Africa, South Asia, rural providers worldwide | Long term (≥ 4 years) |

| Stringent ISO 8536-8 particulate/pressure compliance costs | -0.6% | Global; highest burden on smaller manufacturers | Medium term (2-4 years) |

| Volatility in medical-grade nylon & PU resin supply chains | -0.5% | Global; acute in single-source regions | Short term (≤ 2 years) |

| Competition from elastomeric & needle-free devices | -0.4% | North America & EU ambulatory care, spreading to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Infusion Therapists in Low-Income Regions

Nepal’s nursing schools report diminished supervision, leaving graduates unprepared for complex infusion protocols, a pattern repeated across several low-resource health systems. Only 31.1% of global practitioners receive formal training on contrast-media allergy management, underscoring a skills gap that limits sophisticated device use.

Stringent ISO 8536-8 Particulate / Pressure Compliance Costs

Updating labs to meet ISO 8536-8’s tighter particulate thresholds pushes testing expenses to 3-5% of device revenues for mid-size manufacturers. The FDA’s recent warning to a leading infusion-pump brand illustrates rising regulatory scrutiny and the hefty corrective-action costs now embedded in go-to-market budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Drive Infection Control Revolution

Disposable bags captured 69.22% of 2025 revenue, anchoring the pressure infusion bags market’s infection-control priority. This share reflects rising legal liability from hospital-acquired infections alongside payor penalties. Under these dynamics, the pressure infusion bags market size for disposables is projected to grow at 6.08% CAGR through 2031, replacing reusable cuffs even in cost-sensitive regions.

Hospitals now measure the hidden costs of sterilization staff time, autoclave maintenance, and litigation against the straightforward economics of one-time-use bags. During multi-casualty drills, emergency departments reported 20% faster turnover when disposables were pre-assembled on trauma carts. Manufacturers are consequently automating production to narrow unit-cost differentials while maintaining quality assurance.

By Material: PVC-Free Innovation Accelerates Sustainability Transition

Nylon held 43.85% revenue in 2025 due to its established biocompatibility and favorable price-performance ratio. Yet PVC-free biopolymers post a 6.97% CAGR, powered by EU directives phasing out DEHP-containing PVC in clinical environments. This momentum positions PVC-free variants as the fastest-growing slice of the pressure infusion bags market.

Sustainability teams at university hospitals increasingly specify bio-polyurethane bags in tenders, citing lifecycle-carbon savings and lower incineration emissions. Suppliers are diversifying feedstocks away from volatile nylon streams, hedging geopolitical risk and stabilizing cost structures while promoting green-label credentials.

By Pressure Range: Mid-Range Systems Capture Emergency Applications

Bags rated 250-300 mmHg secured 39.05% 2025 revenue, aligning with standard blood-bank protocols and routine fluid replacement. Higher-pressure 301-400 mmHg devices, however, register the steepest growth at 8.21% CAGR, mirroring more aggressive trauma-resuscitation algorithms that stipulate rapid, large-volume infusion.

The pressure infusion bags market size attached to mid-range devices remains resilient, yet hospitals are stocking extra 301-400 mmHg units for polytrauma and major obstetric hemorrhage stacks. Pressure-sensor integration reassures clinical teams about over-pressurization risks, driving broader acceptance of these advanced cuffs.

By Application: Blood Infusion Dominates While Resuscitation Accelerates

Blood and drug delivery accounted for 56.85% revenue in 2025, anchoring daily inpatient usage and underpinning the largest slice of the pressure infusion bags market. Rapid fluid resuscitation, however, charts a 7.28% CAGR as military trauma algorithms inform civilian emergency department guidelines.

AI-supported dosing algorithms for neonatal parenteral nutrition from Stanford Medicine further bolster demand for precision-controlled systems. Meanwhile, high-viscosity contrast-media injections remain stable, supported by integrated pressure valves that prevent inadvertent catheter damage under imaging workloads.

By End User: Hospitals Lead While Ambulatory Centers Surge

Hospitals and clinics retained 61.20% 2025 share, capitalizing on multi-departmental consumption. Ambulatory surgery centers, growing at 5.58% CAGR, increasingly purchase compact, portable units that match fast-turnover schedules without compromising safety.

Home-care programs adopt backpack-compatible pressure cuffs, enabling infusion of specialty biologics in community settings. For disaster-response agencies, ruggedized bags rated for temperature extremes provide mission-critical support in field hospitals, reinforcing niche but strategically important demand clusters.

Geography Analysis

North America held 37.10% of 2025 revenue, underpinned by premium reimbursement structures, strong military medical budgets, and rapid adoption of smart infusion technologies. U.S. buyers benefit from bundled payment incentives that reward shorter ICU stays, encouraging investment in devices that reduce infusion-related complications. Canada’s national procurement initiatives are likewise pivoting toward disposable, PVC-free alternatives, aligning with federal environmental targets.

Asia-Pacific logs the fastest regional CAGR at 5.89% through 2031, propelled by hospital-build programs in China and India and by rising surgical volumes in Indonesia, Vietnam, and the Philippines. Multiple Chinese manufacturers have advanced to Class III device certification, enhancing domestic competition and driving export ambitions despite R&D constraints. Regional regulators coordinate under ASEAN Medical Device Directives to ease market entry, although varied reimbursement models still require localized go-to-market strategies.

Europe commands a substantial slice of the pressure infusion bags market, with sustainability and quality directives shaping procurement standards. Germany’s DRG-based hospital financing supports premium purchases that shorten postoperative recovery. France’s eco-design decree accelerates adoption of bio-polymeric bags, while UK hospitals continue to align with EU technical files post-Brexit. The Middle East funds state-of-the-art trauma centers, notably in the UAE and Saudi Arabia, whereas South Africa consolidates regional distribution, supplying neighboring states with pressure infusion kits through existing pharmaceutical channels.

Regulatory Landscape

Pressure infusion bags and associated pressure infusors sit within established medical device regulatory frameworks, with compliance burdens varying by region. In the United States, pressure infusors for IV bags are classified under 21 CFR 880.5420 as Class I devices and are generally 510(k) exempt, which supports market entry while still requiring conformity to applicable general controls and recognized consensus standards for safety and performance.

In Europe, pressure infusion devices are typically regulated under the Medical Device Regulation (EU) 2017/745 using Annex VIII classification rules, often resulting in Class IIa classification for non-invasive channeling devices. The framework places greater weight on technical documentation, clinical evaluation, and post-market obligations. Across geographies, international standards continue to shape design and test requirements, including ISO 1135-5:2025 for single-use transfusion sets intended for use with pressure infusion apparatus, along with the ISO 8536 series that is commonly referenced for infusion equipment performance expectations.

Competitive Landscape

The pressure infusion bags market remains moderately fragmented. Merit Medical Systems, ICU Medical, and B. Braun occupy leading positions, leveraging global distribution and diversified product portfolios. These incumbents actively integrate pressure-monitoring valves and compatibility with smart pumps, differentiating on safety and workflow productivity. Mid-tier specialists such as VBM Medizintechnik and Biegler focus on high-pressure trauma cuffs and niche anesthesiology applications, competing on performance and customization.

Supply-chain volatility has pushed several manufacturers to backward-integrate or dual-source nylon and polyurethane. Patent filings on vented fluid pathways and auto-venting caps have risen sharply since 2023, demonstrating a pivot toward engineering innovations that lower priming times and aerosol generation. Alternative modalities—elastomeric pumps and needle-free pressure systems—chip away at low-acuity wards, motivating bag producers to acquire or partner with developers of hybrid delivery technologies.

Large-scale hospital tenders now include sustainability scoring, compelling vendors to certify PVC-free lines and recyclable packaging. In response, top players invest in green-chemistry R&D while negotiating closed-loop recycling pilots with waste-management firms, aiming to differentiate beyond purely clinical features.

Pressure Infusion Bags Industry Leaders

Merit Medical Systems

ICU Medical Inc.

Tapmedic LLC

SunMed

VBM Medizintechnik GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement whitespace is widening as hospitals tighten infection-control practices and standardize single-use infusion workflows, which continues to support conversion toward disposable pressure bags, a major demand driver highlighted for 2025 in this report. The sustainability shift away from DEHP-containing PVC, reflected in tender specifications and described in the report as accelerating adoption of PVC-free alternatives, also creates room for suppliers offering PVC-free biopolymer lines with validated pressure performance and explicit compatibility statements tied to ISO 8536 series requirements for pressure infusion sets and fluid lines.

Technology-led opportunities center on embedding pressure-monitoring functionality and traceability into pressure-assisted delivery workflows, particularly where facilities are building closed-loop safety processes. As a concrete indicator of activity in higher-acuity infusion upgrades, the December 2024 FDA 510(k) clearance for Belmont Medical Technologies Rapid Infuser RI-2 reinforces continued investment in rapid fluid delivery platforms that need to work with pressure-rated disposables and accessories. Separately, reimbursement pathway changes in outpatient infusion settings, including CMS separate payment eligibility linked to NOPAIN Act implementation effective January 1, 2026 for qualifying ambulatory infusion pumps, support continued budget allocation toward safer, protocolized infusion infrastructure that can pull through compatible pressure infusion consumables.

Recent Industry Developments

- January 2026: InfuSystem announced that CMS added the CADD-Solis ambulatory infusion pump (manufactured by ICU Medical) to the list of qualifying products for separate payment under the NOPAIN Act, effective January 1, 2026. This change enables hospital outpatient departments and ambulatory surgical centers to receive separate Medicare reimbursement when using the device in eligible pain management services, supporting higher utilization of protocol-driven infusion workflows and related accessory consumption.

- June 2025: Washington State University researchers reported development of an e-catheter hub technology aimed at reducing central line-associated bloodstream infections. The advance points to broader innovation focused on infection prevention around infusion access, aligning with continued hospital emphasis on single-use and contamination-reducing consumables across infusion setups.

- December 2024: Belmont Medical Technologies received FDA 510(k) clearance (K242735) for the Rapid Infuser RI-2, a high-capacity fluid delivery system for rapid infusion. The clearance supports the installed base of rapid infusion platforms used in trauma and perioperative care, which in turn sustains demand for compatible pressure-rated disposables and pressure-assisted administration components.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from pressure infusion bags used to rapidly infuse IV fluids by applying external pressure to a fluid bag in acute care and procedural settings. We size the market in value terms across key buying settings and major geographies.

Scope exclusions: We exclude IV fluid bags themselves, infusion pumps, IV sets, and pressure monitoring transducers, unless the revenue is explicitly for the pressure infusion bag device.

Segmentation Overview

- By Product Type

- Reusable

- Disposable

- By Material

- Nylon

- Polyurethane

- Silicone-coated Composites

- PVC-free Biopolymers

- By Pressure Range

- 250-300 mmHg

- 301-400 mmHg

- More than 400 mmHg

- By Application

- Blood & Drug Infusion

- Invasive Pressure Monitoring

- Rapid Fluid Resuscitation

- Contrast-Media Injection

- By End User

- Hospitals & Clinics

- Ambulatory Surgical & Outpatient Centers

- Home Care & Long Term Care

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the real demand pool and the supply landscape before we moved into modeling. We mainly leaned on public health and trade signals that indicate where rapid infusion is used most often, and then linked that to device adoption patterns.

Common sources reviewed include government health statistics and procedure volumes (such as CDC and OECD health data), regulatory and safety communications from agencies such as the US FDA, and peer reviewed clinical literature indexed in PubMed. We also reviewed procurement or utilization notes published by large hospital systems and professional societies, plus company filings and product catalogs to understand typical product configurations and positioning. For added coverage, we used a paid subscription for company financials and news, along with a patent database to track product improvement themes over time. These desk sources are not exhaustive, and we checked additional public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming use frequency in emergency care, surgery, and critical care, and on checking pricing and replacement cycles for reusable versus disposable bags. We spoke with a mix of manufacturers, distributors, and clinical procurement stakeholders across APAC, EMEA, and the Americas so desk assumptions could be corrected and final totals could be triangulated across buyer perspectives.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | APAC: 50% |

| Mid tier: 40% | Functional/Unit leaders: 23% | EMEA: 31% |

| Smaller Players: 22% | Managers: 60% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs demand from procedure and acute-care activity, then converts that activity into expected device usage through penetration and replacement assumptions. For pressure infusion bags, the model is driven by indicators such as emergency and trauma admissions, surgical volumes, ICU bed availability, blood transfusion activity, and the split between disposable and reusable use in hospitals and outpatient facilities.

After setting the demand pool, we checked totals with selective bottom-up approximations, including sampled price points by bag type and pressure range, channel feedback on order frequency, and a supplier mix sanity check by region. Where direct data points were missing for smaller countries, we filled gaps using proxy indicators such as hospital infrastructure and procedure intensity, then normalized results to avoid overstating adoption.

Forecasts were prepared using scenario analysis, supported by expert views on how clinical protocols, procurement constraints, and pricing trends could shift over the next few years. We stress-tested a short list of sensitive assumptions, including ASP movement, disposable versus reusable mix, and procedure growth, to keep the range realistic and repeatable.

Data Validation & Update Cycle

Validation was performed through multiple checks so that no single data point would dominate the outcome. We compared modeled results against independent signals such as regional procedure direction, procurement patterns, and the expected split by end user, then flagged outliers for rework.

Before sign-off, the model goes through stepwise analyst review, including unit consistency checks, currency conversion timing checks, and variance checks across regions and segments. If a key assumption changes, or if a major event affects supply or clinical practice, we re-contact respondents and recalculate the model. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Pressure Infusion Bags Market Size Measured Against Other Published Estimates

Published market sizes for pressure infusion bags often differ because the counted products are not always identical, and the usage logic behind volume assumptions is not always transparent. Differences also show up when one estimate emphasizes a specific care setting, or when a different base year and currency timing is used.

Some estimates broaden scope by adding adjacent infusion accessories or by counting a wider set of clinical indications that are harder to validate consistently. In Mordor Intelligence, only pressure infusion bag device revenues are counted, and the demand pool is anchored to procedure and acute-care activity checks before ASP and mix are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 371.21 M (2026) | |

| Global Consultancy A | USD 388.20 M (2025) | Uses a different base year and forecast frame, and also expands the lens using indication-led buckets, which can inflate implied usage rates beyond what procedure and hospital activity signals support. |

| Industry Publisher B | USD 357.29 M (2025) | Applies a lower starting value tied to a narrower near-term demand view, and is less transparent on how reusable replacement cycles and disposable mix are converted into annual revenue. |

Overall, the spread is explained by year alignment, the way usage is translated from clinical activity, and whether adjacent items are implicitly blended into the total. Our approach keeps the result traceable to clear demand indicators, practical pricing assumptions, and repeatable checks that can be re-run as new information becomes available.

Key Questions Answered in the Report

What is the current size of the pressure infusion bags market?

The market stands at USD 371.21 million in 2026 with a 5.43% CAGR forecast to 2031.

Which product segment dominates the pressure infusion bags market?

Disposable bags lead, capturing 69.22% revenue in 2025 due to stringent infection-control policies.

Which region is expanding fastest?

Asia-Pacific posts the highest CAGR at 5.89% through 2031 on the back of healthcare infrastructure investments.

What material trend is shaping future procurement?

Healthcare providers increasingly specify PVC-free bio-polymers, the fastest-growing material class at 6.97% CAGR.

How are regulatory changes affecting manufacturers?

Tougher ISO 8536-8 particulate and pressure standards raise compliance outlays to as much as 5% of device revenues, favoring scale players.

What technological innovations are influencing buying decisions?

Integrated pressure-monitoring valves and AI-assisted closed-loop control improve safety and efficiency, accelerating replacement of legacy cuffs.

Page last updated on: