United States Hospital Facilities Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

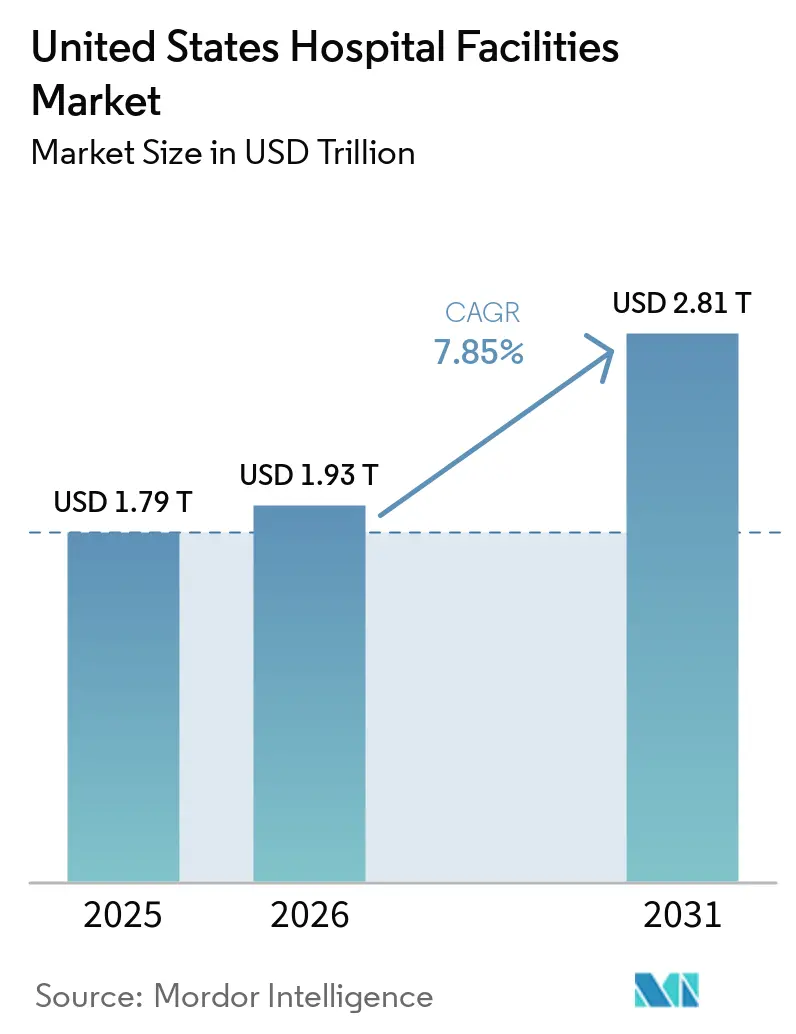

| Base Year Market Size (2025) | USD 1.79 Trillion |

| Market Size (2026) | USD 1.93 Trillion |

| Market Size (2031) | USD 2.81 Trillion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Hospital Facilities Market Analysis by Mordor Intelligence

The United States Hospital Facilities Market size was valued at USD 1.79 trillion in 2025 and is estimated to grow from USD 1.93 trillion in 2026 to reach USD 2.81 trillion by 2031, at a CAGR of 7.85% during the forecast period (2026-2031).

Hospital expenditures grew by 8.9% to USD 1,634.7 billion in 2024, while overall national health expenditure growth was 7.2%, and hospital price growth reached 3.4% in the same year, which shows that hospital care is taking a larger role in overall healthcare spending. Hospital care accounted for nearly one-third of total national health expenditures, and CMS projects hospital spending to reach 6.4% of GDP by 2033 from 5.6% in 2024, which supports a steady expansion path for the United States hospital facilities market. Demand remains firm because the population aged 75 and older is projected to grow by 44% over the next decade, which will sustain higher use of inpatient, emergency, and specialty care services in the United States hospital facilities market. The care burden is also becoming heavier because patients with multiple chronic conditions made up 11% of the population yet accounted for 52% of inpatient admissions, which keeps pressure on capacity, staffing, and service mix in the United States hospital facilities market. At the same time, more than 65% of surgeries now occur in outpatient settings, CMS began removing 285 musculoskeletal procedures from the Inpatient Only List in 2026, and labor represented 56% of total hospital costs, so operators in the United States hospital facilities market are expanding ambulatory footprints while trying to protect margins and maintain facility investment discipline.

Key Report Takeaways

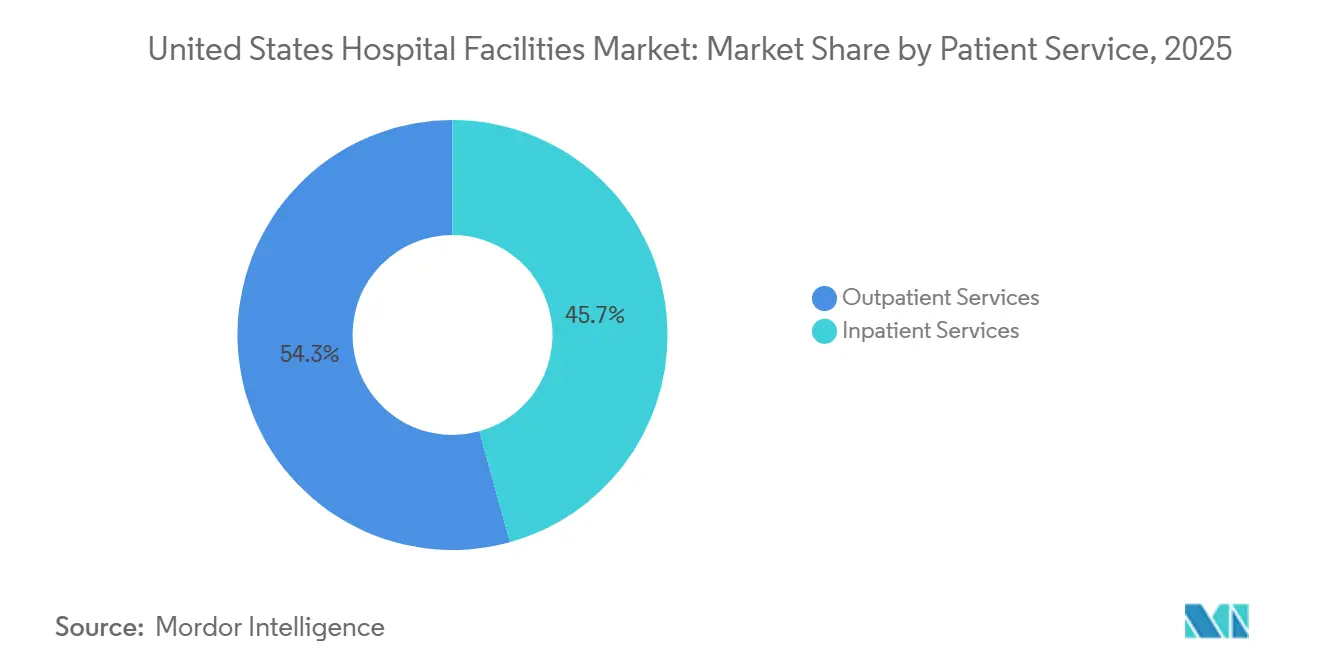

- By patient service, Outpatient Services held 54.31% of revenue in 2025, while the same segment is projected to record the highest CAGR of 8.38% through 2031.

- By facility type, Public and Community Hospitals accounted for 53.24% of revenue in 2025, while State-Owned and Federal Hospitals are forecast to expand at the fastest CAGR of 8.52% through 2031.

- By service type, Acute Care captured 35.52% of revenue in 2025, while Cancer Care is projected to grow at the fastest CAGR of 9.25% through 2031.

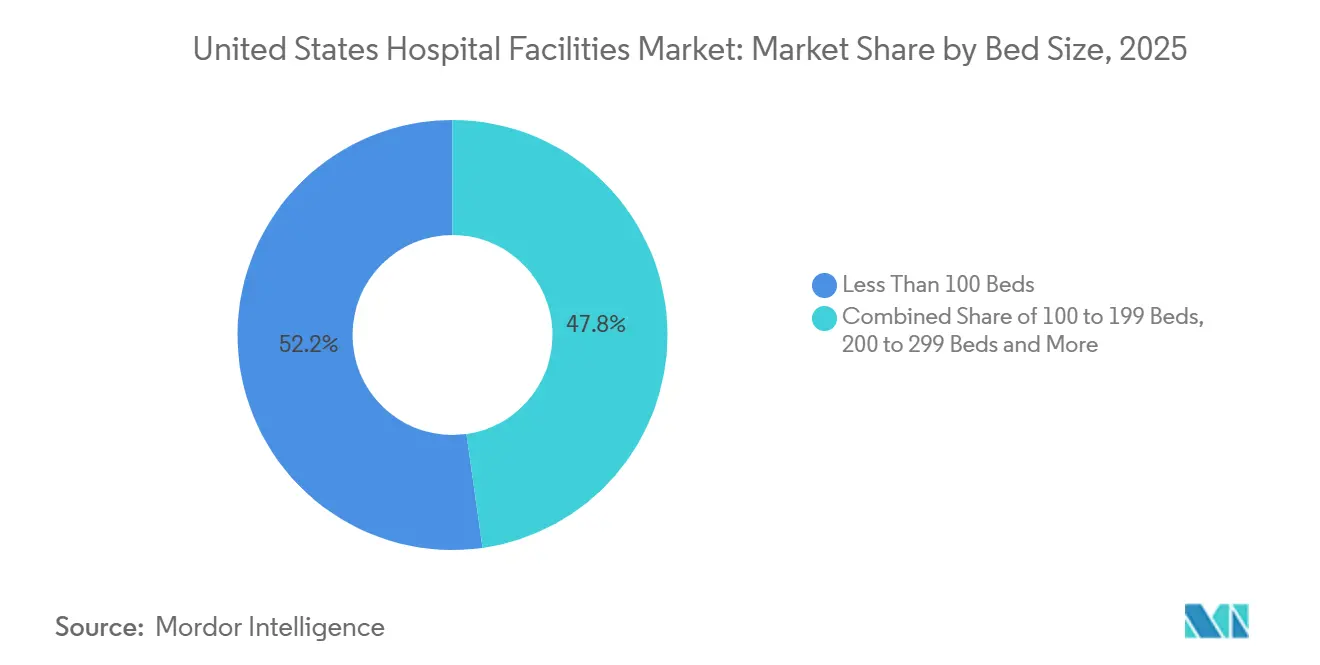

- By bed size, facilities with Less Than 100 Beds represented 52.22% of revenue in 2025, while the 100-to-199 Beds segment is expected to advance at the fastest CAGR of 8.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hospital Facilities Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Outpatient Shift And Same-Day Surgery Mix | +2.0% | Global relevance, strongest in South and West | Short term (≤ 2 years) |

| Hospital System Consolidation, Referral Capture, And Network Density | +1.5% | National, with acceleration in South and Midwest | Medium term (2-4 years) |

| Technology-Enabled Bed And Throughput Optimization | +1.2% | National, with early gains in large urban health systems | Medium term (2-4 years) |

| Aging Population And Chronic Disease Burden | +1.8% | National, with intensity in Southeast and Northeast | Long term (≥ 4 years) |

| Cyber Resilience And Continuity Spending For Connected Care | +0.5% | National | Short term (≤ 2 years) |

| Private-Room Conversion And Infection-Control Retrofits | +0.4% | National, with concentration in Northeast and Midwest academic medical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Outpatient Shift and Same-Day Surgery Mix

The United States hospital facilities market is being reshaped by a steady migration of surgical volume from inpatient campuses to outpatient settings. Research published in December 2025 confirmed that more than 65% of surgeries in the United States now occur in outpatient settings, and inpatient shares for hip and knee replacements fell after the pandemic, which shows that the shift has stayed in place rather than reversing. CMS reinforced this direction in 2026 by lifting total OPPS payments to USD 101.0 billion, up by USD 8.0 billion from 2025, while also starting the removal of 285 mainly musculoskeletal procedures from the Inpatient Only List. This matters because many of the procedures moving out of inpatient care were historically among the more profitable cases for hospital systems. When those procedures leave the main hospital campus, operators need outpatient departments and ambulatory surgery centers to keep referral flows and physician alignment intact. Medicare-certified ambulatory surgery centers reached 12,294 in 2025, and the sector captured 45% of total outpatient surgical volume, which shows that the United States hospital facilities market is not just growing, it is also changing where revenue is earned[1]ASC Data, “Industry Overview August 2025,” ASC Data, ascdata.com.

Hospital System Consolidation, Referral Capture, and Network Density

The United States hospital facilities market continues to favor systems that can control referral pathways across hospitals, clinics, outpatient sites, and surgery centers. The logic behind consolidation has shifted toward care-continuum control, because market leaders need local density and physician connectivity more than simple bed count. HCA Healthcare showed that approach in 2025 by adding nearly 100 outpatient business units and reporting net income of USD 6.8 billion, up 17.8% year over year, while also signaling that more capital remains available for future expansion in 2026 and 2027. Regulatory scrutiny is rising at the same time, as the FTC required Ascension to divest 7 ambulatory surgery centers in June 2026 to complete the AmSurg acquisition, which sets a clear limit on how fast networks can build outpatient scale through deals[2]Federal Trade Commission, “FTC Requires Divestiture of Ambulatory Surgery Centers to Protect Patients from Anticompetitive Effects of Ascension Health AmSurg Deal,” FTC, ftc.gov. The Department of Justice also sued NewYork-Presbyterian in 2026 over contract restrictions that it said raised healthcare costs, which shows that the United States hospital facilities market now faces antitrust pressure not only on mergers but also on payer contracting behavior. As a result, systems that can expand outpatient density and referral capture without relying on large transactions are likely to hold the more durable position.

Technology-Enabled Bed and Throughput Optimization

The United States hospital facilities market is also being supported by technologies that improve patient flow and increase effective capacity inside existing buildings. A 2026 peer-reviewed review of combined Lean and AI implementations found that command-center deployment can create effective capacity gains equal to 30 or more additional beds without physical expansion. These systems improve wait times, length of stay, and dynamic bed allocation, which makes them especially relevant when staffing and capital are tight. This changes the role of technology in the United States hospital facilities market because throughput tools are no longer optional process upgrades. They now support daily operating stability by reducing avoidable delays, limiting diversion risk, and helping hospitals use the beds they already own more effectively. That is especially important for operators trying to handle rising chronic disease burden and higher outpatient handoffs without committing immediately to new towers or large replacement campuses.

Aging Population and Chronic Disease Burden

The United States hospital facilities market has a long demand runway because aging and chronic illness are moving together rather than separately. Claims data covering nearly 81 million covered lives showed in March 2026 that patients with multiple chronic conditions accounted for 52% of inpatient admissions and 35% of emergency department visits, even though they represented only 11% of the population. At the same time, the population aged 75 and older is projected to rise by 44% over the next decade, which keeps the volume outlook firm for hospitals that deliver acute and specialty care. This widens the planning challenge for hospitals because staffing, emergency throughput, medical-surgical demand, and specialty service lines all stay under pressure for a longer period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages In Clinical And Facility Operations | -0.8% | National, most acute in rural and underserved markets | Long term (≥ 4 years) |

| High Capital Intensity And Slow Payback For Facility Expansion | -0.6% | National, with disproportionate strain on mid-tier systems | Medium term (2-4 years) |

| Hospital-Acquired Infection Risk And Sterile Workflow Constraints | -0.3% | National | Medium term (2-4 years) |

| Antitrust Scrutiny On Cross-Market Consolidation | -0.3% | National, concentrated in urban markets with high HHI | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages in Clinical and Facility Operations

Labor scarcity remains the most persistent structural restraint on the United States hospital facilities market. The Association of American Medical Colleges projected a physician shortage of 13,500 to 86,000 by 2036, and NIHCM noted that 31 of 35 physician specialties are expected to face supply gaps, which indicates that capacity expansion will continue to run into clinical staffing limits. Nursing pressure is also rising, and the AHA said the United States Chamber of Commerce expects 42 states to face nursing shortages by 2030. Advertised registered nurse salaries grew 26.6% faster than inflation over the last 4 years, which means revenue growth does not automatically translate into healthier margins for the United States hospital facilities market. Labor already represented 56% of total hospital costs, and the Veterans Health Administration reported a 50% year over year increase in severe occupational staffing shortages in FY2025, which points to continuing operational strain[3]Veterans Affairs Office of Inspector General, “OIG Determination of Veterans Health Administration’s Severe Occupational Staffing Shortages Fiscal Year 2025,” VA OIG, vaoig.gov. This creates a practical limit for facility growth because beds can be licensed and buildings can be opened, but they cannot support clinical volume unless staffing standards are met.

High Capital Intensity and Slow Payback for Facility Expansion

High capital intensity continues to limit how quickly the United States hospital facilities market can add or modernize physical capacity. The AHA reported that total hospital expense rose by 5.1% in 2024, while inflation was 2.9%, which means operating costs still moved faster than the general price environment. The same report said Medicare reimbursed only 83 cents for every USD 1 spent, which leaves a structural funding gap for many operators that depend heavily on public payers. The AHA also found that 94% of healthcare administrators expected to delay equipment upgrades because tariff-related cost increases were raising capital pressure. At the same time, the average age of hospital plant infrastructure rose by more than 10% over the last 2 years, which means deferred maintenance is building up rather than clearing. This slows the pace of large campus projects for mid-tier systems and gives better-capitalized networks a clearer advantage in the United States hospital facilities market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Patient Service: Outpatient Volume Reshaping Hospital Economics

Outpatient Services held 54.31% of the United States hospital facilities market share within the patient service segmentation in 2025, and the United States hospital facilities market size for this segment is projected to grow at a CAGR of 8.38% through 2031. That combination shows that outpatient care is already the larger revenue pool and is still widening its lead. The shift is structural because procedure migration has remained in place after the pandemic rather than reverting to earlier inpatient patterns. More than 65% of surgeries now take place in outpatient settings, which gives hospital systems a strong reason to invest in ambulatory networks and hospital-based outpatient departments. The United States hospital facilities market is therefore seeing service migration within the system rather than simple demand loss, especially when providers own the outpatient site of care.

Hospital-owned outpatient facilities performed 45% of outpatient surgeries in 2025, which shows that integrated systems can still retain a meaningful part of procedural revenue if they control the right assets. CMS also increased OPPS payment rates by 2.6% for 2026 services, which offers some support to hospital-based outpatient departments as they compete with freestanding centers. Inpatient Services still accounted for 45.69% of patient service revenue in 2025, and that base remains important because intensive care, complex surgery, and high-acuity chronic disease management cannot move easily into same-day settings. What changes in the United States hospital facilities market is the inpatient mix, because the remaining cases are increasingly more severe and more resource intensive. This leaves hospitals balancing two priorities at once, protecting high-acuity inpatient capacity while expanding outpatient access fast enough to hold referral relationships.

By Facility Type: Public Systems Holding the Base While Federal Capacity Grows Faster

Public and Community Hospitals commanded 53.24% of revenue in 2025, which makes them the largest facility type in the United States hospital facilities market. Their lead reflects the broad access role they play across urban, suburban, and rural communities. These hospitals absorb large volumes of emergency care, uncompensated care, and medically necessary services that cannot be selected mainly on profit profile. That role gives them a durable place in the United States hospital facilities industry, even when margins are tight and capital budgets are under pressure. Private Hospitals operate a smaller share of the base, but they often run more capital-efficient models and capture a stronger mix of elective and commercially insured procedures.

State-Owned and Federal Hospitals are the fastest-growing facility type, with a CAGR of 8.52% through 2031. This faster expansion signals that public capacity investment is staying active even as many independent operators remain cautious on large projects. The United States hospital facilities industry still requires the same accreditation and licensing standards across public and private ownership models, which means compliance burdens do not fall simply because the owner changes. Public procurement cycles often stretch spending over longer periods, which supports a steadier buildout pattern across the forecast window. As a result, the United States hospital facilities market keeps its revenue base in community hospitals while a faster growth rate develops in publicly backed capacity additions.

By Service Type: Acute Care Remains the Core While Cancer Care Expands Fastest

Acute Care held 35.52% of revenue in 2025, which means it remained the largest service type in the United States hospital facilities market. That position is grounded in emergency medicine, critical care, and general medical-surgical volumes that patients cannot defer for long. Acute services also sit at the center of hospital utilization because they connect emergency departments, inpatient units, imaging, surgery, and discharge planning into one operating flow. Cardiovascular care remained another major revenue contributor because older and multi-morbid patients continue to drive steady demand for high-acuity intervention. This keeps the United States hospital facilities industry anchored in essential care lines even as elective and specialty volumes shift across settings.

Cancer Care is projected to record the fastest CAGR at 9.25% through 2031, reflecting the continued expansion of oncology demand and facility investment. The American Cancer Society estimated 2.1 million new cancer cases in the United States in 2026, which supports longer treatment pathways across diagnostics, infusion, surgery, and follow-up care. Large specialty projects continue to reinforce that shift, including the Dana-Farber and Beth Israel Deaconess cancer hospital project in Boston that moved through formal state review. Pathology, diagnostics, and imaging also benefit as cancer and chronic disease care depend on earlier detection, faster testing, and more complex monitoring. This gives the United States hospital facilities market a service mix where acute care remains the largest base, while oncology creates one of the clearest expansion tracks.

By Bed Size: Small Hospitals Lead the Base While Mid-Sized Facilities Grow Faster

Facilities with Less Than 100 Beds held 52.22% of revenue in 2025, which shows that smaller hospitals still form the broadest physical footprint in the United States hospital facilities market. Their lead reflects the large number of critical access hospitals and other small community facilities that support local healthcare access across dispersed areas. Federal payment designations, including Critical Access Hospital status for facilities with up to 25 inpatient beds and other rural protections, help preserve financial viability in low-density markets. This means small-bed facilities remain essential even when they do not generate the same elective revenue scale as larger urban systems. In practical terms, they keep the United States hospital facilities market connected to rural and isolated populations that would otherwise face longer travel times and delayed treatment.

The 100-to-199 Beds segment is projected to grow at the fastest CAGR of 8.65% through 2031. That pattern suggests mid-sized hospitals are well placed between cost discipline and service breadth, especially in suburban and exurban corridors where population growth is still creating new care demand. These facilities can support emergency care, surgery, diagnostics, and selected specialties without the full capital burden of large academic campuses. By contrast, 200-to-299 Beds and 300 Beds and Above segments remain more tied to metropolitan systems and tertiary care models that need stronger balance sheets and deeper staffing pools. This leaves the United States hospital facilities market with a split structure, where smaller hospitals dominate by count and value share, while mid-sized facilities add capacity at the faster rate.

Geography Analysis

The South remains one of the most active regions in the United States hospital facilities market, supported by population growth, retiree inflows, and ongoing greenfield investment. HCA Florida opened a USD 235 million, 90-bed hospital in Gainesville in 2026, the first full-service hospital in that area in more than 50 years, which shows that operators still see room for new inpatient capacity in selected Southern markets. Orlando Health also announced plans for a new seven-story regional hospital and a 60,000-square-foot medical office building in Viera, Florida, with groundbreaking in June 2026, which points to continuing investment in fast-growing local corridors. Ascension Saint Thomas announced groundbreaking for a USD 148.5 million full-service hospital and health campus in Clarksville, Tennessee, adding inpatient, oncology, cardiology, women’s health, and emergency capabilities in one integrated project. These moves show that the United States hospital facilities market in the South is still adding full-service capacity, not only outpatient clinics, because local demand growth is strong enough to support larger campuses.

The Northeast and Mid-Atlantic continue to stand out for higher spending intensity and a dense concentration of tertiary and academic care. CMS data showed that per capita personal healthcare spending in New England and the Mideast remained 25% and 23% above the national average, which supports more complex case mix and higher-value specialty services. That setting also brings heavier regulatory attention, as the Department of Justice sued NewYork-Presbyterian in 2026 over contract practices that it said raised healthcare costs across New York City. At the same time, formal review activity around large specialty projects such as the Dana-Farber and Beth Israel Deaconess cancer hospital indicates that major investment in advanced care lines remains active in the region.

The Midwest and West show a different pattern in the United States hospital facilities market, with investment focused on selective expansion, replacement capacity, and large branded systems. Cleveland Clinic announced expansion of Avon Hospital and the Richard E. Jacobs Family Health Center in 2025, which supports its regional care network strategy rather than a single-site growth model. Mayo Clinic announced a USD 1.9 billion investment in Arizona in 2026, reinforcing the role of major destination systems in driving facility spending and specialty capacity. Kaiser Permanente broke ground on a new hospital tower at Sunnyside Medical Center in Oregon in April 2026, which shows that the West is still committing capital to long-cycle inpatient infrastructure. These regional moves suggest that growth outside the South is less about volume alone and more about network depth, brand strength, and the ability to support complex care models over time. In that sense, the United States hospital facilities market remains national in scale but highly local in how capacity is added and defended.

Competitive Landscape

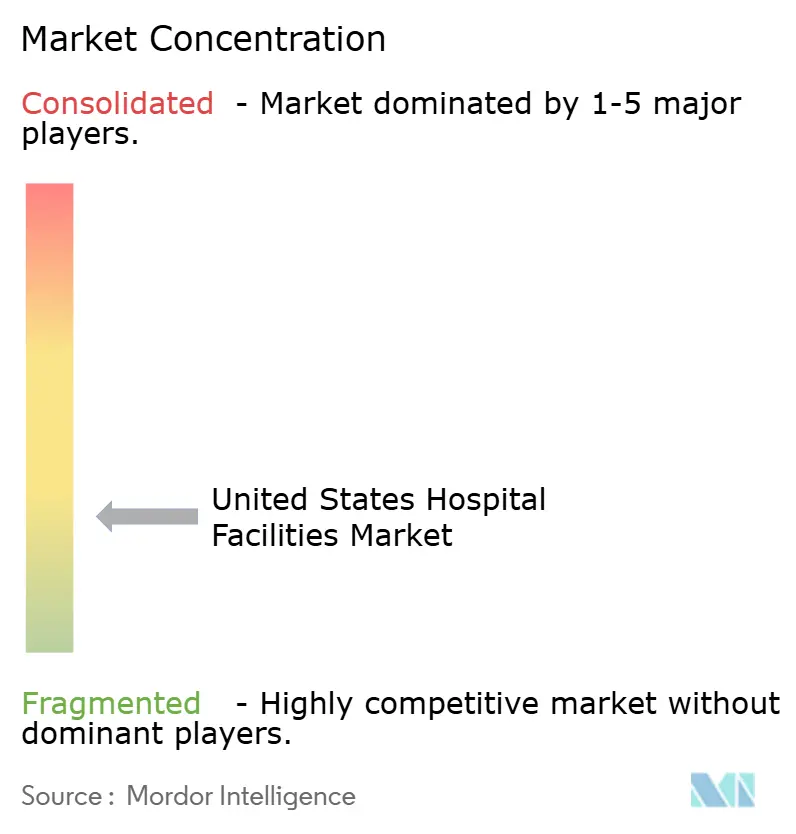

The United States hospital facilities market is fragmented at the regional system level. The Health Care Cost Institute found that 88% of metropolitan areas were highly or very highly concentrated by Herfindahl-Hirschman Index, and 40% of metro markets had hospital spending above the national average, which shows that local bargaining power can be strong even when national share is more dispersed. This gives the United States hospital facilities market a dual structure where local systems can dominate referral patterns in their own areas, even though no single operator controls the country as a whole. Competition therefore depends less on national presence alone and more on local density, specialty depth, payer mix, and physician alignment. Providers that can link inpatient care, outpatient sites, specialty centers, and physician access points into one operating network are better positioned to protect volume and pricing.

Regulators are now a larger part of the competitive equation in the United States hospital facilities market. The FTC required 7 ambulatory surgery center divestitures for the Ascension and AmSurg transaction in June 2026, which shows that outpatient platform building through acquisition will face direct structural limits when concentration concerns rise. The Department of Justice action against NewYork-Presbyterian also shows that hospital systems are being judged not only on merger activity but also on how they write and use commercial contracts. Strategic moves by leading operators still continue, with Mayo Clinic committing USD 1.9 billion in Arizona, Kaiser Permanente building a new tower at Sunnyside, and Ascension Saint Thomas developing an integrated campus in Clarksville. These moves show that large systems are still using targeted capital deployment to strengthen local presence and specialty access.

Technology is becoming another clear source of competitive advantage in the United States hospital facilities market. Peer-reviewed evidence published in 2026 found that Lean and AI command-center models can deliver effective capacity gains equal to 30 or more beds without new construction, which matters for systems that cannot build fast enough to match demand. That gives smaller and mid-tier systems a practical tool to defend throughput and patient access when capital or labor remain constrained. At the same time, operators with stronger balance sheets still hold an edge because they can combine physical expansion, outpatient network growth, and process technology rather than choosing only one of them. This keeps the United States hospital facilities market competitive, but the advantage is moving toward systems that can manage regulation, capital, staffing, and patient flow at the same time.

United States Hospital Facilities Industry Leaders

-

HCA Healthcare, Inc.

-

CommonSpirit Health

-

Ascension Health

-

Tenet Healthcare Corporation

-

Universal Health Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Orlando Health announced plans to build a new seven-story regional hospital and a 60,000-square-foot medical office building on a 40-acre campus in Viera, Florida, breaking ground in June 2026. The investment reflects demand from the rapidly growing Central Space Coast region.

- May 2026: Ascension Saint Thomas announced groundbreaking for a USD 148.5 million full-service hospital and health campus in Clarksville, Tennessee, anchoring a 96-acre integrated campus with oncology, cardiology, women's health, and emergency services. The facility will open with 44 inpatient beds and create approximately 250 jobs.

United States Hospital Facilities Market Report Scope

As per the scope of the report, hospital facilities refer to the physical infrastructure, departments, and amenities that support the delivery of medical care and patient treatment. They ensure a safe, efficient, and comfortable environment for healthcare services.

The segmentation of the United States hospital facilities market is categorized by patient service, facility type, service type, and bed size. By patient service, the market is divided into inpatient services and outpatient services. By facility type, it includes public and community hospitals, private hospitals, and state-owned and federal hospitals. By service type, the segmentation covers acute care, cardiovascular, cancer care, pathology lab, diagnostics, and imaging, obstetrics and gynecology, emergency and trauma care, and other service types. By bed size, the market is segmented into less than 100 beds, 100 to 199 beds, 200 to 299 beds, and 300 beds and above. For each segment, the market size and forecast are provided in terms of value (USD).

| Inpatient Services |

| Outpatient Services |

| Public and Community Hospitals |

| Private Hospitals |

| State-Owned and Federal Hospitals |

| Acute Care |

| Cardiovascular |

| Cancer Care |

| Pathology Lab, Diagnostics, and Imaging |

| Obstetrics and Gynecology |

| Emergency and Trauma Care |

| Other Service Types |

| Less Than 100 Beds |

| 100 to 199 Beds |

| 200 to 299 Beds |

| 300 Beds and Above |

| By Patient Service | Inpatient Services |

| Outpatient Services | |

| By Facility Type | Public and Community Hospitals |

| Private Hospitals | |

| State-Owned and Federal Hospitals | |

| By Service Type | Acute Care |

| Cardiovascular | |

| Cancer Care | |

| Pathology Lab, Diagnostics, and Imaging | |

| Obstetrics and Gynecology | |

| Emergency and Trauma Care | |

| Other Service Types | |

| By Bed Size | Less Than 100 Beds |

| 100 to 199 Beds | |

| 200 to 299 Beds | |

| 300 Beds and Above |

Key Questions Answered in the Report

How large is the United States hospital facilities market in 2026 and 2031?

The United States hospital facilities market is valued at USD 1.93 trillion in 2026 and is forecast to reach USD 2.81 trillion by 2031, growing at a CAGR of 7.85%.

Which patient service category is leading growth through 2031?

Outpatient Services lead with a 54.31% revenue share in 2025 and are also the fastest-growing patient service segment at a CAGR of 8.38% through 2031.

Why is outpatient migration so important for hospital operators?

More than 65% of surgeries now occur in outpatient settings, so hospitals need stronger ambulatory networks to retain referrals, procedure volume, and physician relationships.

Which service line is expanding the fastest in hospitals?

Cancer Care is the fastest-growing service type, with a 9.25% CAGR through 2031, supported by an estimated 2.1 million new cancer cases in the United States in 2026.

What is the biggest operational challenge for hospitals over the next few years?

Labor shortages remain the main operational constraint, as physician and nursing supply gaps are expected to persist while labor already makes up 56% of total hospital costs.

Which regions are seeing notable new facility investments in 2026?

The South is seeing visible greenfield activity, including HCA Florida in Gainesville, Orlando Health in Viera, and Ascension Saint Thomas in Clarksville, while major systems in the Midwest and West are also funding selective expansion projects.

Page last updated on: