United States Medical Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

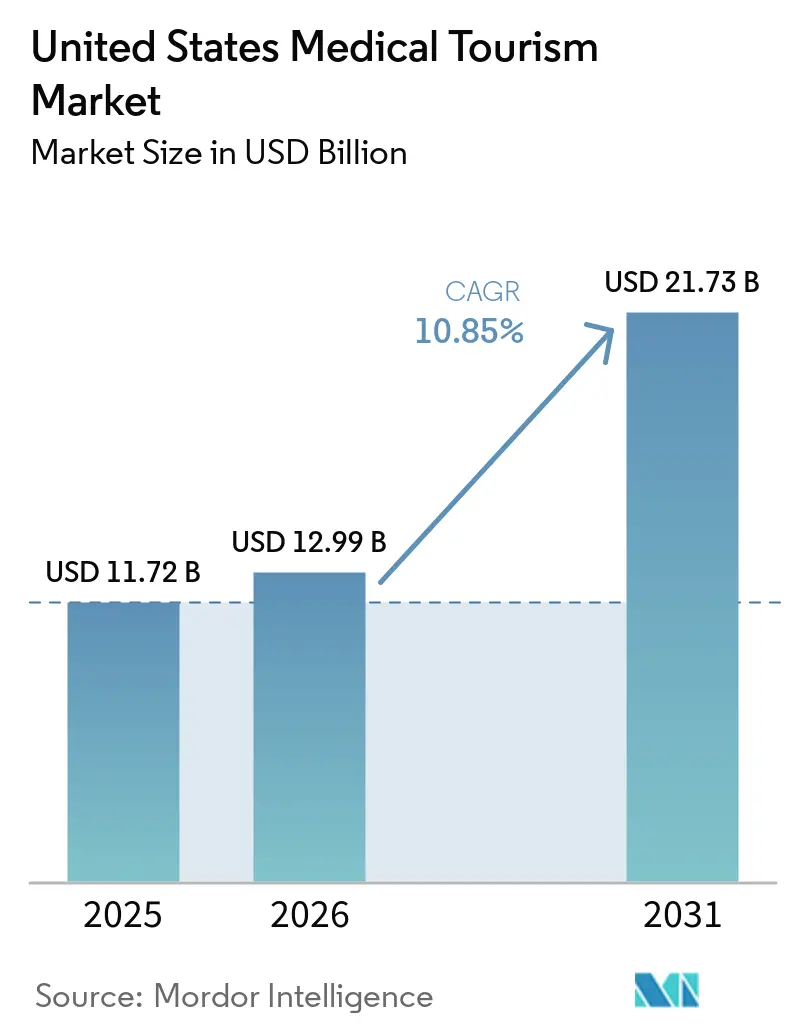

| Base Year Market Size (2025) | USD 11.72 Billion |

| Market Size (2026) | USD 12.99 Billion |

| Market Size (2031) | USD 21.73 Billion |

| Growth Rate (2026 - 2031) | 10.85% CAGR |

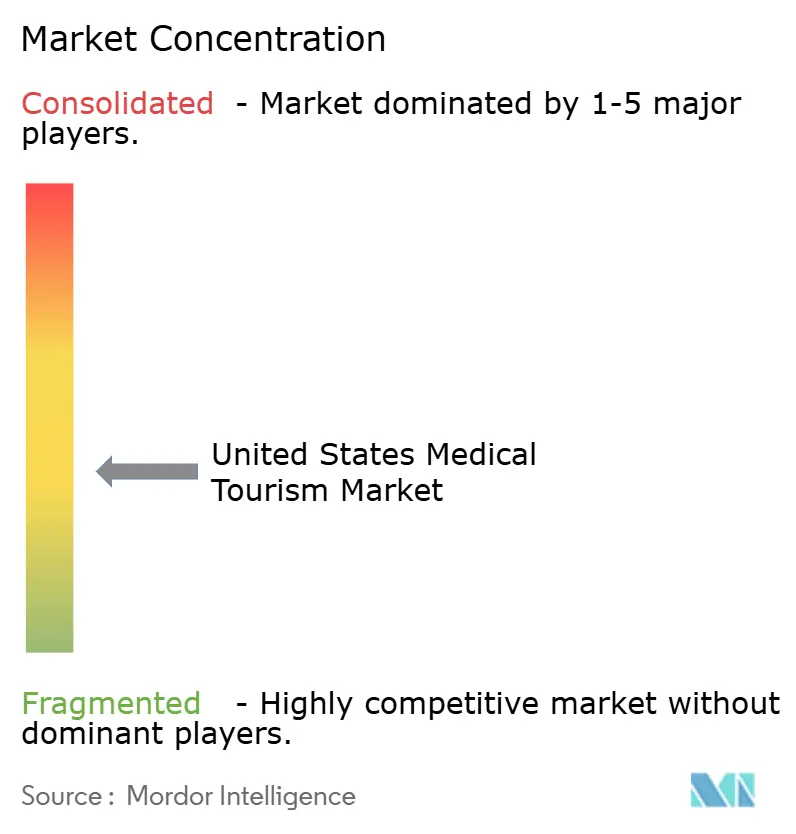

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Medical Tourism Market Analysis by Mordor Intelligence

The United States Medical Tourism Market size is projected to be USD 11.72 billion in 2025, USD 12.99 billion in 2026, and reach USD 21.73 billion by 2031, growing at a CAGR of 10.85% from 2026 to 2031.

The market is being shaped by a split demand pattern in which many U.S. residents leave the country for lower-cost care, while international patients still travel into the country for highly specialized treatment that is difficult to access elsewhere. Domestic affordability pressure remains a central force, with average family premiums reaching USD 26,993 in 2025 and average single deductibles rising to USD 1,886, which keeps self-pay and cross-border options relevant for elective and specialist procedures. Telehealth-enabled second opinions are also changing how patients enter the system, as digital triage now works as an early acquisition channel for both inbound and outbound pathways. Mayo Clinic’s outpatient digital visits rose 17% to 1.2 million in 2025, while Cleveland Clinic reported nearly USD 18 billion in operating revenue for 2025 across a system that spans 3 continents, which shows how scale in digital and physical capacity is reinforcing established brands. Competition in the United States medical tourism market is therefore moderate to high, with premium academic centers defending inbound complexity cases, facilitators competing for price-sensitive outbound demand, and follow-up care gaps plus limited insurance portability still acting as clear brakes on wider adoption.

Key Report Takeaways

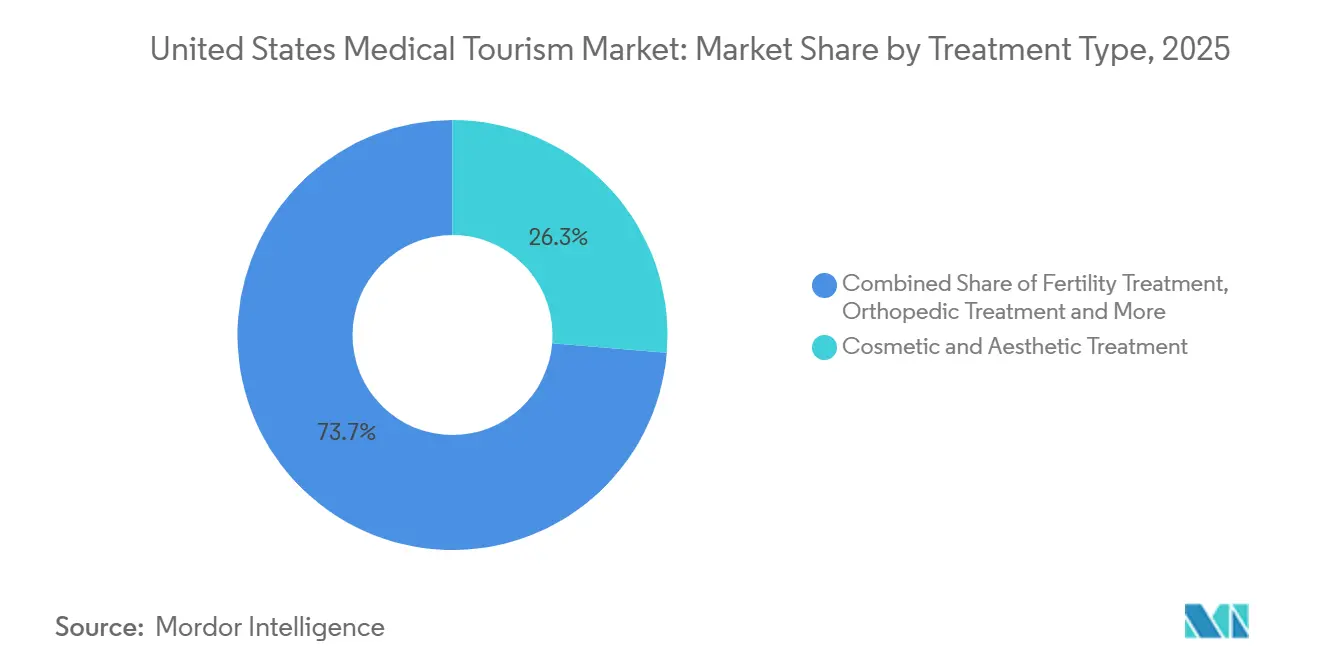

- By treatment type, Cosmetic & Aesthetic Treatment held 26.31% of the United States medical tourism market share in 2025, while Fertility Treatment is projected to expand at a 12.38% CAGR through 2031.

- By service provider, Domestic US Hospitals & Health Systems accounted for 51.24% of the United States medical tourism market size in 2025, while Telehealth Second-Opinion Platforms are forecast to grow at a 13.52% CAGR through 2031.

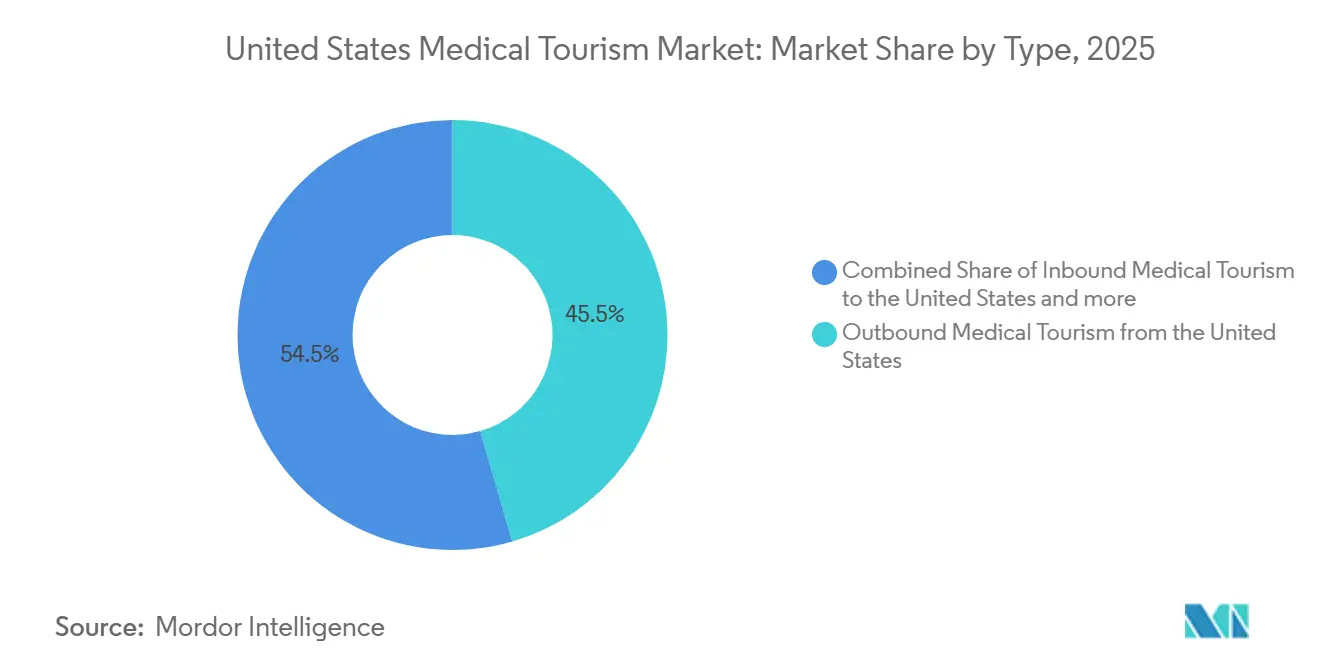

- By type, Outbound Medical Tourism from the United States held 45.52% share in 2025, while Inbound Medical Tourism to the United States is expected to advance at an 11.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Medical Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Domestic Out-of-Pocket Costs And Employer Benefit Gaps | +2.8% | National, with concentration in uninsured and underinsured states, Texas, Florida, Georgia | Short term (≤ 2 years) |

| U.S. Cross-Border Price Arbitrage For Elective Procedures | +2.2% | US-Mexico border corridor, spill-over to Colombia, Costa Rica, and Thailand | Short term (≤ 2 years) to Medium term (2-4 years) |

| Expansion Of Accredited Telehealth-Led Second Opinions | +1.4% | Global, with primary uptake in Middle East, South/East Asia, and Latin America | Medium term (2-4 years) |

| Growth Of Digitally Coordinated Care Navigation And Concierge Models | +1.0% | National (US), with inbound acquisition from Gulf States and Southeast Asia | Medium term (2-4 years) |

| Capacity Shortages And Waiting-Time Spillover Into Private Self-Pay Care | +0.9% | US domestic, with outbound relief to Mexico and Canada | Short term (≤ 2 years) |

| Cross-Border Fertility, Dental, And Aesthetic Demand From U.S. Residents | +1.3% | US outbound to Mexico, Spain, Czech Republic, Greece | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Out-Of-Pocket Costs Accelerate Outbound Flows

Healthcare affordability pressure has moved beyond a policy issue and now directly affects patient behavior inside the United States medical tourism market. Total healthcare costs for an average American family reached USD 35,119 in 2025, and outpatient facility costs rose 8.5% in the same year, which reinforced the financial strain around nonemergency procedures. Employer-sponsored coverage is also leaving many families exposed, since 72% of covered workers faced out-of-pocket maximums above USD 3,000 for single coverage and 21% faced more than USD 6,000. That burden is steering many middle-income patients toward self-pay travel for dental, aesthetic, bariatric, and fertility procedures, especially when benefit plans exclude coverage or require difficult prior approvals. The practical effect is that affordability pressure is not just reducing care access, it is redirecting demand into organized outbound channels and informal cross-border care pathways. This makes cost stress one of the clearest volume drivers in the United States medical tourism market, especially for procedures that patients can delay, compare, and finance on their own.

U.S. Cross-Border Price Arbitrage For Elective Procedures

Price gaps between domestic and foreign treatment remain one of the main commercial engines of the United States medical tourism market. Gastric sleeve gastrectomy costs USD 15,000–25,000 in the United States compared with USD 4,000–6,500 in Mexico, and domestic pre-authorization often takes 3 to 6 months versus 1 to 4 weeks abroad. Mexico also received 1.4 million patients from the United States and Canada by the end of 2024, which reinforced its role as the most important destination in Latin America and one of the largest globally. Baja California alone generates an estimated USD 2 billion annually from medical tourism, and 60% of its 4.5 million annual health-related visitors come from the United States, which shows how deeply integrated this corridor has become. Competitive advantage in this corridor now depends on proximity, bilingual coordination, U.S.-facing logistics, and telehealth support, not only on price. The result is that the U.S.-Mexico route increasingly functions as a cross-border care system with its own referral logic, patient expectations, and repeat-demand patterns.

Expansion Of Accredited Telehealth-Led Second Opinions

Telehealth-led second opinions are becoming a structural part of the United States medical tourism market rather than a supporting service. Telehealth Second-Opinion Platforms are projected to grow at a 13.52% CAGR from 2026 to 2031, and that pace reflects how patients now seek specialist review before they commit to travel. Mayo Clinic’s outpatient digital visits rose 17% to 1.2 million in 2025, which shows that virtual engagement is already operating at meaningful scale inside major academic systems. Cleveland Clinic also tied its virtual second-opinion reach to a broader AI and digital care strategy in its 2025 State of the Clinic update, which supports the use of virtual review as a feeder for later treatment decisions. This means the United States medical tourism market is increasingly rewarding providers that can evaluate, triage, and build trust before any physical encounter happens.

Growth Of Digitally Coordinated Care Navigation And Concierge Models

Digitally coordinated navigation is changing how patients move through the United States medical tourism market. Concierge models are taking on record transfer, provider matching, travel coordination, and post-care communication that many patients previously handled on their own. That role matters because friction between intent and completed treatment is often highest before the procedure, especially when patients compare multiple destinations and providers. Navigation platforms also create a layer of patient data around preferences, conversion, and outcomes, which gives them leverage even when they do not own the clinical asset. As these models mature, competition is shifting from simple referral activity toward the ability to manage the full patient journey with low drop-off and better continuity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Post-Procedure Follow-Up Across Jurisdictions | -1.2% | National (US), particularly in states with limited cross-border care coordination norms | Short term (≤ 2 years) to Medium term (2-4 years) |

| Limited Insurance Reimbursement For Outbound Treatment | -0.9% | National, with higher impact in states with high uninsured rates, Texas, Florida | Short term (≤ 2 years) |

| State-Level Licensing And Malpractice Complexity | -0.6% | National, with concentration in large states requiring in-state licensure for telehealth | Medium term (2-4 years) |

| Provider Trust Issues Around Outcome Transparency And Bundled Pricing | -0.5% | Global (outbound destinations), with heightened sensitivity in fertility and aesthetic segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Post-Procedure Follow-Up Across Jurisdictions

Post-procedure continuity remains one of the clearest operational weaknesses in the United States medical tourism market. Patients who travel abroad for surgery often return to a domestic system where the original provider is outside the legal, clinical, and administrative reach of their local care network. U.S. physicians are not obligated to manage complications from procedures they did not perform, and many patients must arrange specialist follow-up on their own after returning home. This burden falls hardest on patients who traveled for cost reasons without using a structured facilitator or hospital-linked navigation model. The CDC has already stated that outbound treatment planning should include return follow-up care, which shows that the risk is recognized even if it is not consistently managed in practice[1]Centers for Disease Control and Prevention, “Medical Tourism,” Yellow Book: Health Information for International Travel, cdc.gov.

Limited Insurance Reimbursement For Outbound Treatment

Insurance design still limits how far the United States medical tourism market can expand on the outbound side. Many patients who travel abroad do so on a self-pay basis because coverage structures rarely move with them across borders, even when international providers may offer acceptable clinical quality. This creates a split in demand, where higher-income patients are more able to choose premium domestic self-pay or flagship U.S. centers, while lower-income patients carry more risk in cost-driven outbound options. The practical effect is not only lower reimbursed demand, but also uneven quality exposure across income groups and procedure types. Limited portability therefore acts as a structural brake on broader formalization, even while affordability pressure continues to push more patients to look outside the domestic system.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Cosmetic And Dental Demand Anchor Patient Volumes

Cosmetic & Aesthetic Treatment held the largest share at 26.31% in 2025, which made it the leading treatment category in the United States medical tourism market. The American Society of Plastic Surgeons reported 1.6 million cosmetic surgical procedures and 28.5 million minimally invasive treatments in the United States in 2024, with cosmetic surgical volume up 1% and minimally invasive procedures up 3%[2]American Society of Plastic Surgeons, “Interest in Aesthetic Health Remained Consistent Despite Economic Uncertainty in 2024,” ASPS Press Release, plasticsurgery.org. That sustained demand helps explain why outbound travel remains active for price-sensitive body contouring and breast procedures, while inbound demand still exists for patients seeking the safety profile and specialist reputation of U.S. board-certified surgeons. South Korea also drew more U.S. patients in 2025, with arrivals rising 70.4% to 173,000 and more than 62% of foreign patients receiving dermatology treatment, which signals that premium aesthetic care abroad is attracting a distinct U.S. segment.

Dental Treatment remained the second-largest category and the highest-volume outbound procedure group in the United States medical tourism industry. The CDC reported that an estimated 550,000 U.S. patients traveled to Mexico for dental care in 2024, largely because implants and full-mouth restoration are far cheaper there than in the domestic system. Orthopedic and bariatric procedures also hold an important place because patients can compare prices, plan travel, and avoid domestic delays more easily than in emergency care. Fertility Treatment is the fastest-growing category, with the United States medical tourism market size for this segment projected to expand at a 12.38% CAGR through 2031, supported by strong cross-border demand from patients who face high domestic costs and limited coverage. Cancer Treatment remains the anchor of inbound demand because pioneering oncology programs, advanced diagnostic depth, and complex care coordination remain concentrated in major U.S. academic centers. This mix shows that treatment demand in the United States medical tourism market spans both price-led outbound travel and capability-led inbound travel rather than leaning only in one direction.

By Service Provider: Hospital Systems Lead While Digital Platforms Gain Ground

Domestic US Hospitals & Health Systems held 51.24% of the United States medical tourism market size in 2025, which kept them firmly in the lead across the provider landscape. These systems sit at the center of inbound medical travel because they combine specialty reputation, clinical depth, research capability, and branded international patient programs that smaller players cannot easily match. Cleveland Clinic reported nearly USD 18 billion in operating revenue and nearly 16 million patient encounters in 2025, while Mayo Clinic treated patients from more than 140 countries, performed 161,590 surgical cases, and completed 2,065 solid-organ transplants. The United States medical tourism industry therefore continues to rely on large hospital systems as both a destination for inbound care and a benchmark for domestic self-pay decision-making.

Telehealth Second-Opinion Platforms are the fastest-growing provider group, expanding at a 13.52% CAGR between 2026 and 2031, which shows how digital review is moving upstream in the patient journey. In many cases, a virtual specialist review now comes before travel, and sometimes replaces it, especially for diagnosis confirmation and treatment planning. Platforms such as Transcarent and MediPocket USA are increasingly tying second opinions to employer benefit structures, which changes the commercial model from one-off patient acquisition to recurring enterprise revenue. Cross-Border Specialty Hospitals and Medical Tourism Facilitators still serve important roles, but both groups face pressure as digital triage and concierge coordination absorb parts of the referral chain. HCA Healthcare also entered 2026 with a USD 5.5–6 billion approved capital pipeline and added around 100 outpatient business units in 2025, which shows that scale players are still investing heavily in capacity and access infrastructure. This provider structure keeps the United States medical tourism market balanced between hospital-led authority and platform-led accessibility.

By Type: Outbound Volume Leads While Inbound Grows Fastest

Outbound Medical Tourism from the United States held 45.52% share in 2025, which made it the largest type segment in the United States medical tourism market. The main reason is structural cost pressure, since millions of uninsured and underinsured patients see foreign treatment as the only realistic path for many elective or specialist procedures. Mexico remained the dominant destination in this flow, receiving 1.4 million patients from the United States and Canada in 2024 and generating more than USD 2.5 billion in medical tourism revenue. The outbound mix is also broadening beyond dental and bariatric care, as reporting tied to INEGI data indicates that orthopedics, spinal surgery, stem cell therapy, and fertility treatments are taking a larger role in Baja California’s incoming patient profile.

Inbound Medical Tourism to the United States is forecast to grow at an 11.55% CAGR through 2031, making it the fastest-growing type within the United States medical tourism market. This side of the market grows on specialty access rather than price, especially for gene therapy, CAR-T cell therapy, proton beam and carbon ion radiation oncology, multi-organ transplantation, and rare-disease diagnostics. Dana-Farber’s new cancer hospital project and its approved USD 50.5 million proton therapy center add clear capacity for future oncology inflows, while Stanford Medicine opened a new proton therapy facility in April 2026 for pediatric and adult cancer patients. Domestic Self-Pay Medical Travel within the United States remains a meaningful and stable segment because patients still move across states to access lower charges, stronger specialists, or shorter waits. Taken together, these type dynamics show that the United States medical tourism market is expanding through both outward cost arbitrage and inward premium specialization.

Geography Analysis

Inbound Medical Tourism to the United States is projected to grow at 11.55% CAGR through 2031, and that makes the country one of the strongest destinations in the high-complexity end of the United States medical tourism market. Houston, Miami, Boston, New York, and the Mayo Clinic clusters in Rochester, Jacksonville, and Phoenix remain the main receiving hubs because they combine specialist depth, international patient services, and recognizable clinical brands. Mayo Clinic treated patients from more than 140 countries in 2025, completed 161,590 surgical procedures, and lifted outpatient digital visits 17% to 1.2 million, which shows the scale of its inbound reach and pre-travel engagement[3]Mayo Clinic, “Mayo Clinic's 2025 Performance Advances Its Patient-Centered Mission,” Mayo Clinic News Network, newsnetwork.mayoclinic.org. Cleveland Clinic Abu Dhabi also reported a 35% rise in international patient volume in 2024, and its role as a feeder for more complex cases supports the global referral position of the wider Cleveland Clinic network.

Mexico and Latin America form the most mature outbound corridor for U.S. residents and remain central to the United States medical tourism market. Mexico received 1.4 million patients from the United States and Canada in 2024, and Baja California alone generated an estimated USD 2 billion in annual medical tourism revenue, which shows the scale of organized cross-border care. Procedures in Mexico were reported at 36–89% below comparable U.S. prices for surgical categories such as orthopedics, bariatric surgery, cosmetic procedures, and dental restoration, which helps explain the corridor’s staying power. Colombia is also becoming more visible for fertility and specialty care through JCI-accredited hospitals in Bogotá and Medellín, while Baja California continues to market itself through organized congresses and coordinated destination promotion rather than isolated provider outreach. That shift matters because it gives the U.S.-Mexico corridor more institutional support and a more durable patient acquisition model.

Europe and Asia Pacific serve different needs within the United States medical tourism market, rather than competing on the same value proposition. Spain, the Czech Republic, and Greece remain the main European destinations for U.S. fertility travelers, while South Korea is emerging as a strong destination for aesthetic and dermatology procedures. Thailand and India still attract U.S. patients for more acute surgical procedures, which shows that distance is becoming less of a barrier as digital screening and coordination improve. This geographic pattern confirms that the United States medical tourism market no longer revolves around one destination corridor alone, even if Mexico remains the dominant outbound route.

Competitive Landscape

The United States medical tourism market remains structurally split between a concentrated inbound segment and a fragmented outbound segment. On the inbound side, Mayo Clinic, Cleveland Clinic, Johns Hopkins Medicine International, Dana-Farber, and MD Anderson compete mainly on clinical reputation, specialty depth, and the credibility of their international patient programs. Mayo Clinic’s Bold. Forward. Unbound. strategy includes advanced digital tools, new facilities, and the Americas’ first carbon ion therapy program under development in Florida, which shows a long-term effort to deepen its global pull rather than simply defend current volume. Cleveland Clinic is following a similar logic through disciplined global expansion, with Abu Dhabi scaling robotic procedures and its London cancer center moving toward patient care by the end of 2027.

Outbound competition is much more fragmented, and no single facilitator appears to control a large portion of the broader United States medical tourism market. Facilitators, concierge agencies, and destination-country hospital networks compete on bundled pricing, coordination quality, accreditation, and patient trust rather than on brand dominance. This part of the market still has room to formalize because many employer-sponsored plans exclude foreign treatment, yet a growing group of self-insured employers is evaluating structured medical travel for cost control on selected procedures. Better by MTA’s Platinum network expansion in January 2026 illustrated how facilitator ecosystems are trying to move beyond individual self-pay transactions and toward enterprise-ready models with curated quality and payment support. JCI accreditation remains one of the most visible quality signals in this field, especially for U.S. patients who want a recognizable assurance marker when comparing lower-cost foreign options.

Digital patient acquisition is now one of the clearest competitive battlegrounds in the United States medical tourism market. Telehealth second opinions, remote triage, and pre-travel case review are shifting the contest upstream, which benefits institutions with strong clinical content, specialist access, and established trust. Mayo Clinic’s rise in digital visits and Cleveland Clinic’s digital strategy both show that leading providers are not leaving this layer to intermediaries alone. The result is a competitive field where inbound leadership remains relatively concentrated among elite systems, while outbound facilitation is still dispersed and open to platform-led disruption.

United States Medical Tourism Industry Leaders

Cleveland Clinic

Mayo Clinic

Johns Hopkins Medicine International

HCA Healthcare

Mass General Brigham

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Massachusetts Public Health Council approved Dana-Farber Cancer Institute's application to build a USD 50.5 million proton therapy center at its Boston campus, construction begins in spring 2026 with the facility expected to open to patients in late 2027, expanding inbound oncology capacity for the US medical tourism market.

- April 2026: Stanford Health Care and Alameda Health System announced a strategic collaboration to expand specialized care access in California's East Bay at St. Rose Hospital, including leasing and developing medical-surgical bed capacity under Stanford management, a move that expands Stanford's patient referral network for both domestic and international patients.

United States Medical Tourism Market Report Scope

As per the scope of the report, medical tourism refers to the practice of traveling across international borders to obtain medical treatment, healthcare services, or procedures. Patients often seek medical tourism to access affordable, high-quality care, or specialized treatments that may not be available or are more expensive in their home country.

The segmentation for the United States medical tourism market is categorized by treatment type, service provider, and type. By treatment type, it includes dental care, cosmetic and aesthetic procedures, fertility services, orthopedic care, cardiovascular services, ophthalmic care, bariatric services, neurological care, cancer care, and other medical services. By service provider, it covers U.S. hospitals and health systems, specialty hospitals abroad, medical tourism agencies and concierge services, and telehealth second-opinion services. By type, it is segmented into inbound medical tourism to the U.S., outbound medical tourism from the U.S., and domestic self-pay medical travel in the U.S. For each segment, the market size and forecast are provided in terms of value (USD).

| Dental Treatment |

| Cosmetic & Aesthetic Treatment |

| Fertility Treatment |

| Orthopedic Treatment |

| Cardiovascular Treatment |

| Ophthalmic Treatment |

| Bariatric Treatment |

| Neurology Treatment |

| Cancer Treatment |

| Other Treatments |

| Domestic U.S. Hospitals & Health Systems |

| Cross-Border Specialty Hospitals |

| Medical Tourism Facilitators & Concierge Agencies |

| Telehealth Second-Opinion Platforms |

| Inbound Medical Tourism to the United States |

| Outbound Medical Tourism from the United States |

| Domestic Self-Pay Medical Travel within the United States |

| By Treatment Type | Dental Treatment |

| Cosmetic & Aesthetic Treatment | |

| Fertility Treatment | |

| Orthopedic Treatment | |

| Cardiovascular Treatment | |

| Ophthalmic Treatment | |

| Bariatric Treatment | |

| Neurology Treatment | |

| Cancer Treatment | |

| Other Treatments | |

| By Service Provider | Domestic U.S. Hospitals & Health Systems |

| Cross-Border Specialty Hospitals | |

| Medical Tourism Facilitators & Concierge Agencies | |

| Telehealth Second-Opinion Platforms | |

| By Type | Inbound Medical Tourism to the United States |

| Outbound Medical Tourism from the United States | |

| Domestic Self-Pay Medical Travel within the United States |

Key Questions Answered in the Report

What is the 2026 position of the United States medical tourism market?

The United States medical tourism market stands at USD 12.99 billion in 2026 and is forecast to reach USD 21.73 billion by 2031 at a 10.85% CAGR.

Why are U.S. patients traveling abroad for treatment?

The strongest reasons are rising premiums, higher deductibles, and major price gaps for elective procedures, especially dental, aesthetic, bariatric, and fertility care.

Which treatment category leads demand in this space?

Cosmetic & Aesthetic Treatment led with 26.31% share in 2025, while Fertility Treatment is the fastest-growing category with a 12.38% CAGR through 2031.

Which provider group has the strongest position today?

Domestic US Hospitals & Health Systems led with 51.24% share in 2025 because they combine international patient programs, specialty depth, and large-scale clinical infrastructure.

What is driving faster growth in inbound care to the United States?

Growth is being supported by advanced specialty access, including complex oncology, transplant, gene therapy, and proton therapy capacity being added by leading U.S. institutions.

How are telehealth and digital navigation changing patient behavior?

Virtual second opinions and digital navigation are moving patient decisions earlier in the care journey, which helps providers screen cases, build trust, and convert demand before travel occurs.

Page last updated on: