Healthcare Staffing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

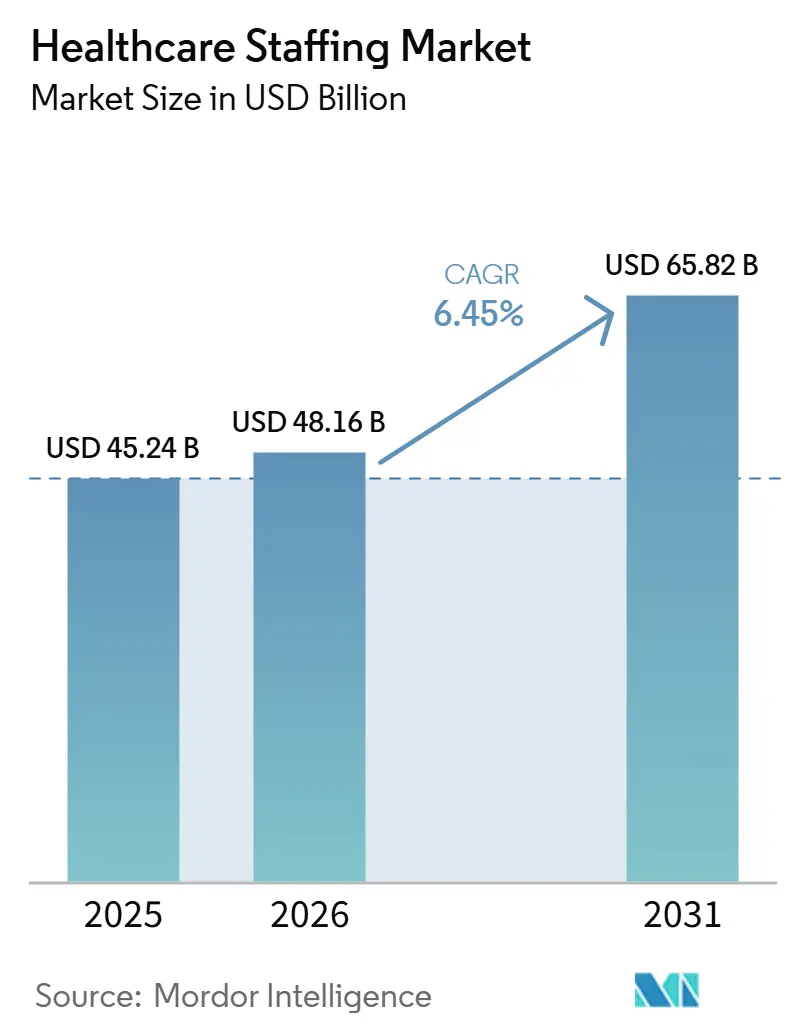

| Market Size (2026) | USD 48.16 Billion |

| Market Size (2031) | USD 65.82 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Staffing Market Analysis by Mordor Intelligence

The healthcare staffing market size is expected to grow from USD 45.24 billion in 2025 to USD 48.16 billion in 2026 and is forecast to reach USD 65.82 billion by 2031 at 6.45% CAGR over 2026-2031. Persistent clinician shortages, regulatory staffing mandates, and the widening adoption of flexible labor models keep demand elevated across clinical and non-clinical roles. Hospitals, home-health agencies, and ambulatory centers now treat contingent labor as a core operational lever, using managed service provider frameworks and AI-enabled scheduling to stabilize coverage and reduce premium labor costs. Demographic shifts, notably the acceleration of the 65-plus population cohort, amplify service volumes while simultaneously shrinking the supply of experienced practitioners exiting the workforce. Technology investments—from predictive workforce analytics to integrated credentialing—lower time-to-fill metrics and deepen vendor differentiation, supporting steady expansion of the healthcare staffing market even as travel-nurse bill rates normalize. Intensifying consolidation among leading agencies signals a maturing competitive environment in which scale and digital capability influence client retention and margin performance.

Key Report Takeaways

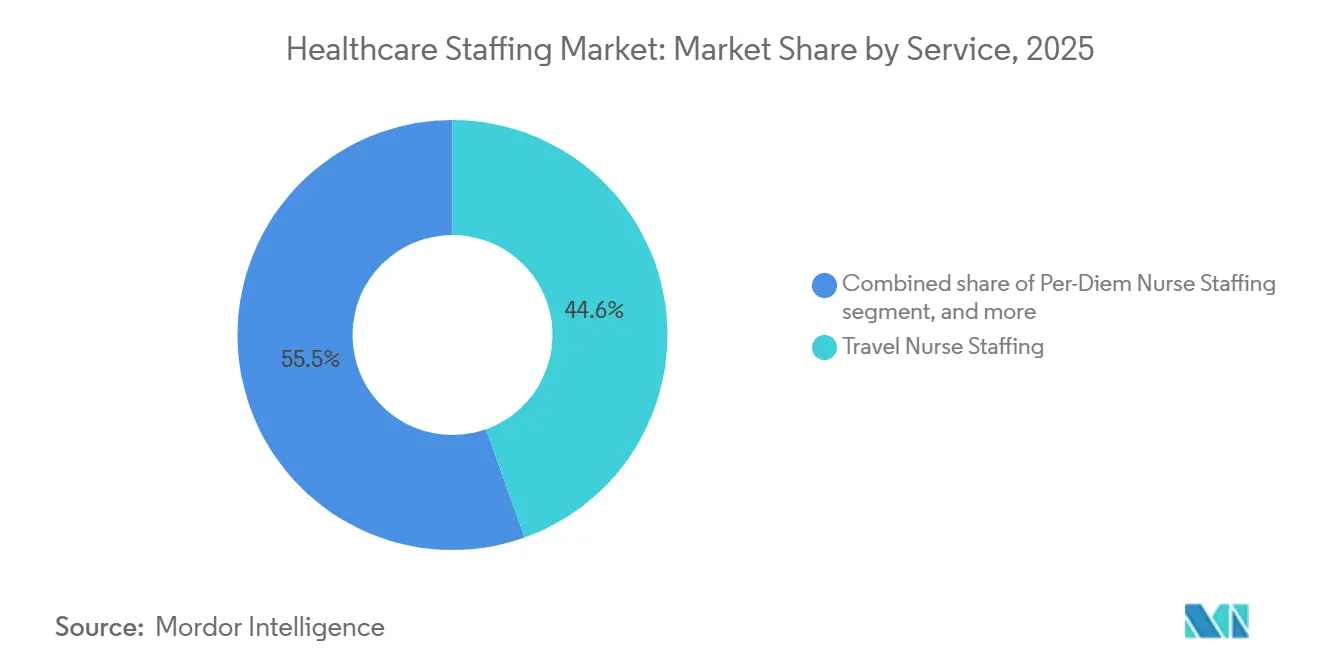

- By service, travel nurse staffing led with 44.55% revenue share in 2025, whereas locum tenens posted the fastest 8.12% CAGR through 2031.

- By end-user, hospitals held 41.88% of the healthcare staffing market share in 2025, while home-health agencies are projected to grow at 9.05% CAGR.

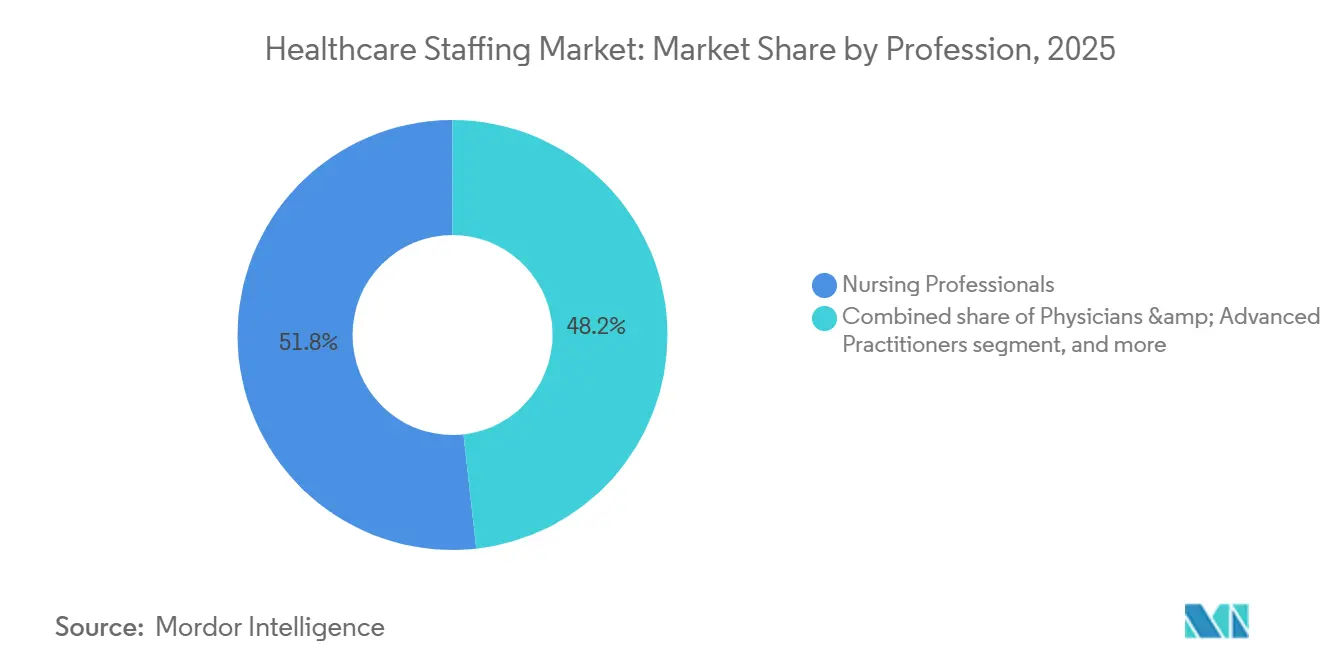

- By profession, nursing commanded 51.76% share of the healthcare staffing market size in 2025; physicians & advanced practitioners will expand 8.34% annually to 2031.

- By delivery mode, on-site models retained 59.72% revenue in 2025, yet remote/tele-staffing is rising at 8.96% CAGR.

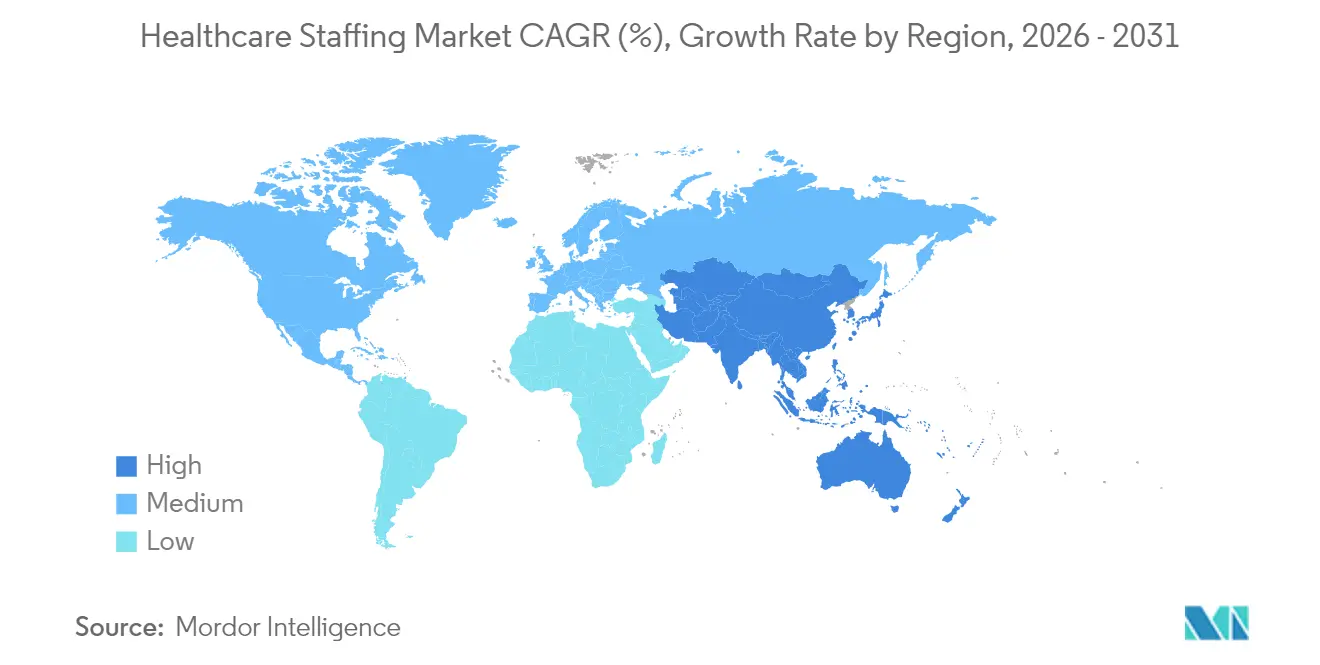

- By geography, North America accounted for 38.10% revenue in 2025; Asia-Pacific is the fastest-growing geography at 7.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Staffing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rising healthcare demand | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Increasing healthcare expenditure worldwide | +1.2% | Global, led by developed markets | Medium term (2-4 years) |

| Growing adoption of temporary staffing models for cost optimization | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Technological advancements in recruitment platforms and workforce analytics | +0.9% | Global, early adoption in North America | Short term (≤ 2 years) |

| Regulatory push for quality care and staffing compliance | +0.7% | North America & Europe | Short-to-medium term (≤ 4 years) |

| Expansion of home healthcare and outpatient services | +1.0% | Global, strongest in North America & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Healthcare Demand

Surging longevity deepens care intensity: the United States will see adults aged 65 and older jump from 62 million to 84 million by 2045, while centenarians worldwide quadruple during the same horizon[1]Partners HealthCare, “Aging Population Implications,” partners.org. Older adults over 85 consume triple the care resources of the 65-74 group, driving continuous requisitions for nurses, therapists, and home-care aides. The Bureau of Labor Statistics projects 1.8 million new healthcare jobs each year to 2035, magnifying the recruitment burden[2]Bureau of Labor Statistics, “Employment Projections 2024-2034,” bls.gov. Rural systems, constrained by declining permanent-hire pipelines, collaborate with staffing firms to maintain service lines, particularly in critical-access hospitals. Retirements inside the clinician workforce intensify the gap, pushing agencies to expand international sourcing and cross-training programs.

Increasing Healthcare Expenditure Worldwide

Healthcare spending’s share of gross domestic product, led by the United States at a projected 19.7% of GDP by 2032, reinforces the resource pool available for outsourced labor even amid cost-containment scrutiny[3]Health Affairs, “National Health Expenditure Projections,” healthaffairs.org. Medicare outlays are rising 7.4% annually, spurring providers to balance revenue capture against escalating wage pressures. In contrast, the World Health Organization notes a decline in average per-capita public health spending after pandemic-era surges, prompting systems to toggle between permanent and contingent staff to ride fiscal cycles[4]World Health Organization, “Global Health Spending 2024 Update,” who.int. Temporary staffing contracts enable administrators to flex supply without locking long-term expense, safeguarding service continuity under budget ceilings.

Growing Adoption of Temporary Staffing Models for Cost Optimization

Eighty-two percent of hospital executives deploy locum tenens to bridge vacancies, with 46% citing revenue protection during recruitment lags. The 2024 federal nursing home staffing rule requiring 3.48 hours per resident immediately lifted demand for shift-based coverage, benefiting digital managed-service platforms that offer real-time roster visibility. Health systems recalibrate from high-cost travel contracts toward local or regional pools, using AI-driven rate benchmarking to contain premium pay while maintaining quality metrics.

Technological Advancements in Recruitment Platforms and Workforce Analytics

Artificial intelligence turbocharges the end-to-end hiring funnel: Incredible Health’s platform cuts nurse-placement time by 25% through predictive matching algorithms. Predictive analytics integrate admission forecasts and acuity trends, enabling proactive requisition posting and reducing overtime outlays. Aya Healthcare’s deployment of AI workforce management underpins its multi-year growth strategy and margin resilience. Generative AI now drafts job descriptions and surfaces passive talent, helping agencies identify niche clinicians in competitive subspecialties.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of qualified healthcare professionals | -1.4% | Global, acute in rural areas | Long term (≥ 4 years) |

| Volatility in hospital budgets and reimbursement rates | -0.8% | North America & EU, regulatory-driven | Medium term (2-4 years) |

| Complex regulatory and credentialing requirements | -0.6% | Global, fragmented across jurisdictions | Short-to-medium term (≤ 4 years) |

| Rising competition and price pressures among staffing agencies | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Qualified Healthcare Professionals

The global deficit could exceed 10 million clinicians by 2030, with the United States alone lacking 195,400 nurses and up to 86,000 physicians in the same window. Education pipelines cannot expand rapidly enough, despite increased nursing school seats. Forty-three US states reported permanent provider closures in rural zones during 2024, underlining maldistribution challenges. International recruitment offers partial relief yet raises ethical questions about draining scarce talent from emerging economies and layers compliance complexity onto agency operations.

Volatility In Hospital Budgets and Reimbursement Rates

Labor already represents 60% of hospital operating costs and rose 22% between 2019 and 2022. Medicare’s 2025 home-health rate cut of 4.067% squeezes margins for agencies whose reimbursement mix skews heavily toward government payers. Providers operating below full census due to staffing caps confront a paradox: latent demand exists, yet cash-flow limitations hinder head-count growth, pushing many facilities to rely on overtime rather than fresh contingent contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Travel Nursing Stabilizes While Locum Tenens Accelerates

Travel nurse staffing retained 44.55% revenue in 2025 despite a correction from the 2022 pandemic peak. The segment declined from USD 42.7 billion to USD 25.6 billion, and average bill rates fell to USD 106.78. Analysts expect the healthcare staffing market size for travel nurses to level near USD 19.18 billion in 2026, signaling a new equilibrium as hospitals emphasize local float pools. Locum tenens, meanwhile, is pacing at 8.12% CAGR, buoyed by enduring physician shortages and flexible scheduling preferences. Nearly 52,000 doctors practiced as locums in 2024, filling emergency, psychiatry, and primary-care gaps. AI-enabled matching speeds credentialing and curbs idle time, strengthening agency economics across both service lines.

Demand for allied health professionals also rises as imaging, laboratory, and rehabilitation volumes expand, aided by broader scope-of-practice regulations. Per-diem nurse pools continue supporting weekend and surge demands where full-time hires would under-utilize capacity. Overall, each service tier now leans on advanced analytics to forecast site-level needs, enhancing utilization and client satisfaction while anchoring long-term growth trajectories inside the healthcare staffing market.

By End-user: Home-Health Agencies Drive Growth Amid Hospital Consolidation

Hospitals retained 41.88% of 2025 revenue, reflecting their status as the largest employer group. Yet federal minimum staffing mandates and reimbursement headwinds push administrators toward cost-efficient roster models, including integrated MSP partnerships. Ambulatory surgery centers expand staffing needs as procedure migration to outpatient settings persists. Skilled-nursing and rehab units confront elevated vacancy rates, with 21% downsizing beds in the past year.

Home-health agencies represent the fastest-growing end-user at 9.05% CAGR to 2031. CMS’s 2025 home-health payment refresh ties reimbursement more tightly to patient acuity, incentivizing agencies with robust nurse and therapist pools. Investment in AI scheduling and remote patient monitoring boosts productivity, attracting private-equity capital targeting roll-up plays. Value-based care penalties on readmissions further propel referral volumes into the home setting, reinforcing the home-health contribution to the healthcare staffing market.

By Profession: Advanced Practitioners Gain Ground as Nursing Remains Dominant

Nursing preserved a 51.76% hold on 2025 revenue, but burnout and demographic pressure continue to squeeze retention. Demand for critical-care, perioperative, and emergency expertise sustains premium differentials. Travel demand has normalized, yet a modest 5% uptick is forecast for 2025 as clinicians seek flexibility and cultural alignment.

Physicians and advanced practitioners show the quickest trajectory at 8.34% CAGR. Regulatory moves expanding nurse-practitioner scope and physician-assistant autonomy underpin this rise. Nurse practitioner employment is forecast to swell 40% by 2033, while physician assistants will advance 28%, supporting expanded mid-level coverage models within the healthcare staffing market. Allied professionals—in imaging, laboratory science, and rehab—also benefit from modality growth, while non-clinical administrative expertise gains value in revenue-cycle, compliance, and IT implementation.

By Delivery Mode: Remote Staffing Transforms Traditional Models

On-site staffing still generated 59.72% revenue in 2025, upheld by regulatory mandates for physical presence in many clinical tasks. However, digital workforce suites now optimize shift alignment, reduce overtime, and enhance retention through transparent scheduling. Hybrid arrangements, blending on-site care with off-site documentation, emerge in large health systems.

Remote/tele-staffing is scaling fastest at 8.96% CAGR. Telehealth adoption and interstate practice compacts broaden the accessible clinician pool, with virtual care firms offering USD 160-plus hourly rates for multi-state-licensed physicians. Remote care coordinators, teleradiologists, and virtual scribes widen service catalogs, embedding remote supply into the core of the healthcare staffing market. Credentialing, cyber-security, and cross-border compliance remain gating issues but are gradually easing with unified licensure and sandbox pilots.

Geography Analysis

North America dominated the healthcare staffing market with 38.10% revenue in 2025. Robust infrastructure, intricate reimbursement frameworks, and entrenched MSP ecosystems sustain consistent contingent labor utilization. The American Hospital Association warns that workforce gaps could near 100,000 critical workers by 2028, a reality steering hospitals toward technology-enabled vendors and pushing further consolidation. Canada and Mexico present incremental opportunities yet require navigation of distinct licensure and bilingual expectations. Market analysts anticipate a 20% contraction in premium travel nursing within the region as systems pivot to permanent hiring and local float pools, yet overall contingent demand remains resilient due to mandate-driven minimum staffing thresholds.

Europe faces a projected deficit of 1.8 million healthcare workers, with physician density as low as 2.4 per 1,000 residents in some member states. The European Commission has earmarked EUR 65 billion for workforce upskilling and mobility programs to blunt the shortage impact. Germany alone may require 500,000 additional nurses by 2030, spurring cross-border recruitment and English-language training incentives. Post-Brexit immigration hurdles complicate UK workforce planning, but the National Health Service continues to rely on international nurses and locum doctors to sustain service levels. Digital credentialing platforms accelerate onboarding yet face fragmented data standards across jurisdictions, tempering the near-term acceleration of the healthcare staffing market size in Europe.

Asia-Pacific is the fastest-growing territory at 7.32% CAGR, propelled by infrastructure investment and rising chronic-disease prevalence. Japan projects a shortage of nearly 1 million health workers by 2040, prompting bilateral agreements to attract Indonesian and Filipino nurses. Australia is easing restrictions on overseas medical recruitment, though ethical considerations arise around talent drain from lower-income neighbors. India’s burgeoning private hospital sector seeks specialized nurses and allied professionals, yet retention is challenged by competitive salaries in Gulf and North American markets. While regulation, licensure variability, and salary differentials temper velocity, demographic momentum positions Asia-Pacific as a crucial growth lever for the healthcare staffing market.

Competitive Landscape

The healthcare staffing market remains moderately fragmented; however, deal activity is accelerating as scale and technology become decisive. Aya Healthcare’s USD 615 million purchase of Cross Country Healthcare forged a powerhouse with expanded AI-driven scheduling and analytics capabilities. AMN Healthcare, with USD 3.1 billion in trailing-twelve-month revenue, is investing in predictive talent suites and language-service adjacencies to diversify revenue streams. ShiftMed’s acquisition of CareerStaff Unlimited created the first end-to-end digital managed service platform dedicated to nursing, highlighting investor appetite for vertically integrated solutions.

Digital innovation is the prime differentiator. Ingenovis Health integrated seven legacy brands onto Bullhorn’s cloud talent hub, compressing credential approval times and enhancing candidate experience. AI matching engines now sift credential repositories, align skill tags, and project retention likelihood, giving early adopters measurable speed and fill-rate advantages. White-space specializations such as infection-control staffing and behavioral-health locums attract niche entrants that leverage narrow clinical focus plus tech-forward engagement. Consolidators simultaneously eye adjacent services—revenue-cycle staff augmentation, telehealth provider rosters, and data-driven workforce consulting—to extend client wallet share and raise switching costs, reshaping competitive boundaries inside the healthcare staffing market.

Healthcare Staffing Industry Leaders

Aya Healthcare

Medical Solutions

AMN Healthcare

CHG Healthcare, Inc.

Cross Country Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Aya Healthcare named Emily Hazen as CEO following founder Alan Braynin’s passing, signaling leadership continuity for the fast-growing platform.

- April 2025: Smartlinx purchased StafferLink, a contingent staffing software managing 2 million shifts and USD 1 billion in spend annually.

- February 2025: CHG Healthcare bought CareerMD to broaden physician recruitment and career-support services.

- January 2025: Ascension Health advanced negotiations to acquire AmSurg for approximately USD 3.9 billion, widening its ambulatory surgery footprint amid an 18.1% rise in volume.

- December 2024: Aya Healthcare closed its USD 615 million acquisition of Cross Country Healthcare at USD 18.61 per share, expanding technology-enabled workforce offerings.

Global Healthcare Staffing Market Report Scope

As per the scope of the report, healthcare staffing is a process of hiring healthcare providers or healthcare professionals for a specific organization as needed. The service providers help healthcare units make staff available without indulging in a long recruitment process. Healthcare staffing is gaining popularity among hospitals, research centers, and clinics. The healthcare staffing market is segmented by service and geography. By service, the market is segmented into travel nurse staffing, per diem nurse staffing, locum tenens staffing, and allied healthcare staffing. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of value (USD).

| Travel Nurse Staffing |

| Per-Diem Nurse Staffing |

| Locum Tenens Staffing |

| Allied Healthcare Staffing |

| Hospitals |

| Ambulatory Surgical Centers |

| Long-term Care & Rehab Facilities |

| Home-Health Agencies |

| Nursing Professionals |

| Physicians & Advanced Practitioners |

| Allied Health Professionals |

| Non-clinical/Administrative |

| On-site Staffing |

| Remote/Tele-staffing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Travel Nurse Staffing | |

| Per-Diem Nurse Staffing | ||

| Locum Tenens Staffing | ||

| Allied Healthcare Staffing | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Long-term Care & Rehab Facilities | ||

| Home-Health Agencies | ||

| By Profession | Nursing Professionals | |

| Physicians & Advanced Practitioners | ||

| Allied Health Professionals | ||

| Non-clinical/Administrative | ||

| By Delivery Mode | On-site Staffing | |

| Remote/Tele-staffing | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the healthcare staffing market?

The market is valued at USD 48.16 billion in 2026 and is projected to reach USD 65.82 billion by 2031 at a 6.45% CAGR.

Which service segment is growing fastest in the healthcare staffing market?

Locum tenens staffing is expanding at an 8.12% CAGR due to physician shortages and flexible coverage preferences.

Why are home-health agencies a key growth area for healthcare staffing firms?

Regulatory incentives promoting aging in place and CMS acuity-based reimbursement boosts have accelerated home-health staffing demand at a 9.05% CAGR.

How is technology reshaping healthcare staffing operations?

AI-enabled platforms streamline candidate matching, forecast staffing needs, and reduce time-to-hire, improving efficiency and margin performance for agencies.

Which region presents the strongest growth outlook for healthcare staffing?

Asia-Pacific leads with a 7.32% CAGR, driven by infrastructure expansion, demographic pressure, and workforce migration initiatives.

What recent consolidation trends are shaping the competitive landscape?

Major deals like Aya Healthcare’s USD 615 million acquisition of Cross Country Healthcare and ShiftMed’s purchase of CareerStaff Unlimited reflect a push toward scale and digital capabilities within the sector.

Page last updated on: