U.S. Hospital & Healthcare Spending For Filtration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

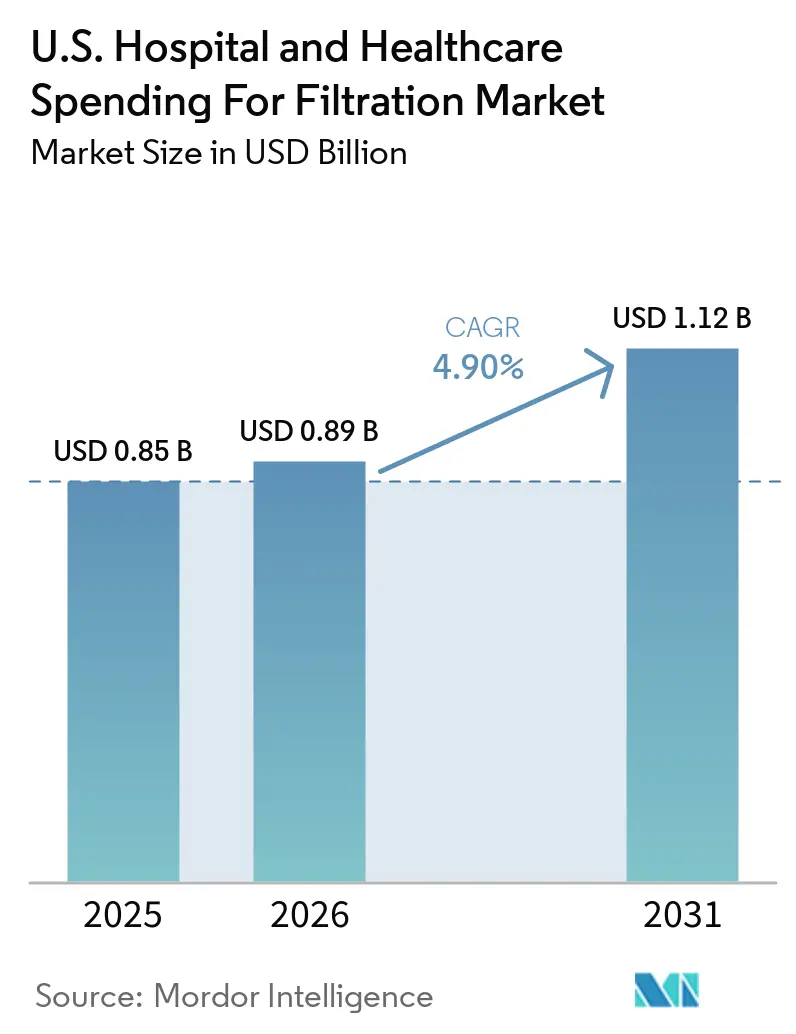

| Base Year Market Size (2025) | USD 0.85 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Hospital & Healthcare Spending For Filtration Market Analysis by Mordor Intelligence

The U.S. Hospital & Healthcare Spending For Filtration Market size was valued at USD 0.85 billion in 2025 and is estimated to grow from USD 0.89 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 4.90% during the forecast period (2026-2031).

In 2025, the ANSI/ASHRAE/ASHE Standard 170 expanded its scope to include a broader range of healthcare spaces, emphasizing both new construction and ongoing retrofit and replacement activities in existing facilities. Water management has become a critical operational requirement, with certified facilities expected to implement policies to minimize risks from Legionella and other pathogens in building water systems. The ANSI/AAMI ST108 introduced clearer standards for sterile-processing water quality, driving demand for validated multi-step filtration pathways in reprocessing areas. This shift reflects the growing emphasis on compliance and operational efficiency in healthcare facilities.

Key Report Takeaways

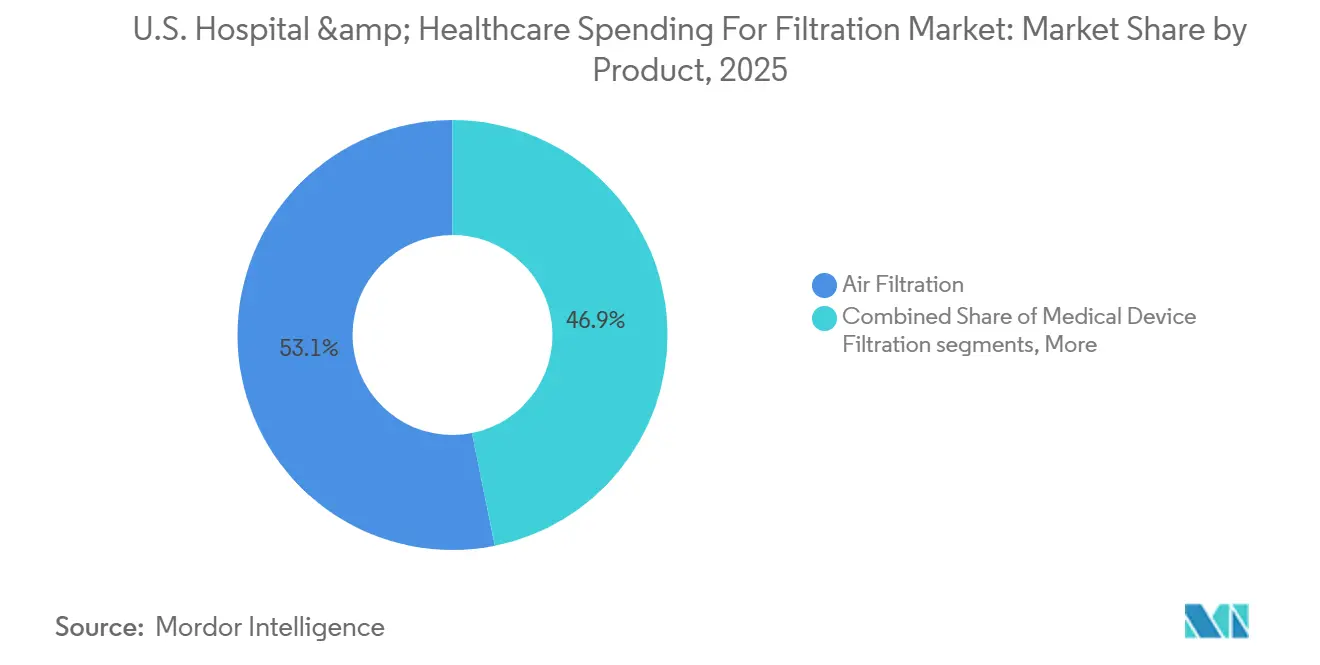

- By product, air filtration held 53.14% of the U.S. hospital & healthcare spending for filtration market share in 2025, while medical device filtration is forecasted to expand at a 6.10% CAGR through 2031.

- By filtration process, HEPA filtration accounted for 44.45% share of the U.S. hospital & healthcare spending for filtration market size in 2025, while reverse osmosis is projected to grow at a 7.40% CAGR through 2031.

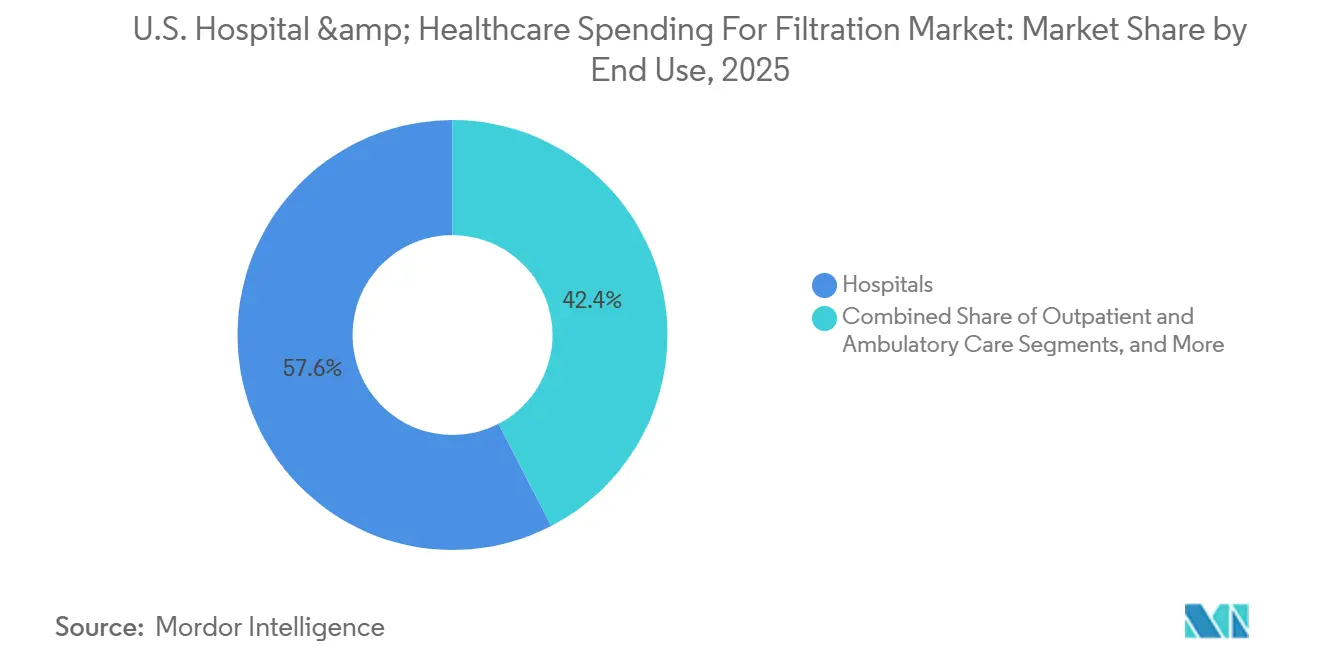

- By end use, hospitals held 57.60% share in 2025, while outpatient and ambulatory care is projected to grow at a 6.45% CAGR through 2031.

- By application area, patient-care air quality represented 34.55% share in 2025, while sterile processing and reprocessing water is expected to grow at a 6.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Hospital & Healthcare Spending For Filtration Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | Impact Timeline |

|---|---|---|---|

| CDC and ASHRAE airflow compliance in critical-care spaces | +1.2% | US-wide, most acute in dense inpatient markets across Northeast and Midwest | Medium term (2-4 years) |

| CMS and Joint Commission water-management enforcement | +0.9% | US-wide, concentrated in Medicare and Medicaid certified acute-care and long-term care | Medium term (2-4 years) |

| Outpatient migration expands filtration points across ASCs and clinics | +1.0% | US-wide, concentrated in Sun Belt and Southeast growth corridors | Short term (≤ 2 years) |

| AAMI ST108 upgrades sterile-processing water loops | +0.7% | US-wide, hospitals with Joint Commission, DNV, or HFAP accreditation | Short term (≤ 2 years) |

| Low-pressure-drop retrofit filters gain priority in margin-stressed hospitals | +0.5% | US-wide, highest impact in under-capitalized regional and rural systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

CDC and ASHRAE Airflow Compliance Reshape Critical-Care Filtration Demand

The 2025 edition of ANSI/ASHRAE/ASHE Standard 170 revised ventilation requirements for healthcare facilities, adding space types aligned with modern care patterns, such as behavioral health and imaging areas.[1]ASHRAE/ASHE, “ANSI/ASHRAE/ASHE Standard 170-2025, Ventilation of Health Care Facilities,” ASHE, ashe.org This impacts the United States hospital filtration market as older hospitals must assess if existing air-handling systems meet compliance standards. Unlike new constructions, these projects often adapt legacy ductwork and mechanical systems. Portable industrial-grade HEPA units, recommended by the CDC, enhance contaminant removal in areas where fixed HVAC systems are insufficient. This creates demand driven by both replacement cycles and supplemental filtration, especially in critical spaces like operating rooms and isolation areas.

CMS and Joint Commission Water-Management Enforcement Drives Sustained Liquid Filtration Investment

CMS mandates that Medicare and Medicaid-certified hospitals, critical access hospitals, and long-term care facilities implement water management policies to mitigate risks from pathogens like Legionella. These policies require ongoing risk assessments, control measures, and monitoring, making water safety a continuous operational priority. The Joint Commission reinforces this focus by emphasizing infection control and environmental care in accreditation processes. This drives consistent demand for point-of-use filters, monitoring tools, and replacement media, ensuring liquid filtration remains a resilient segment even during tighter construction budgets.

Outpatient Migration Multiplies Filtration Nodes Across ASCs and Clinics

The shift to outpatient care is expanding filtration demand across a growing network of smaller care facilities. Ambulatory surgery centers and higher-acuity procedures are driving filtration needs beyond traditional hospital campuses into distributed procedure rooms and support spaces. While individual sites require less filtration capacity, they still demand compliant air handling and water control. This trend increases installation points, service requirements, and recurring replacement activity, favoring vendors offering standardized solutions and scalable maintenance models for outpatient settings.

AAMI ST108 Triggers Capital Cycles in Sterile-Processing Water Infrastructure

ANSI/AAMI ST108 established national standards for water used in medical device processing, providing clearer compliance guidelines for water quality controls. This shift is significant for the United States hospital filtration market as hospitals move toward more verifiable water pathways. Reverse osmosis remains central, but ST108-related decisions now emphasize downstream barriers, monitoring, and system accountability. Procurement is shifting from individual components to comprehensive systems, as seen in the 2024 AmeriWater agreement with Vizient, which expanded access to compliant water solutions. This trend boosts demand for suppliers offering integrated treatment performance and compliance support.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hospital capital rationing and deferred facilities projects | -1.0% | US-wide, strongest in rural and single-hospital markets | Medium term (2-4 years) |

| Maintenance complexity across air, water, steam, and device filtration | -0.6% | US-wide, concentrated in large multi-facility health systems | Long term (≥ 4 years) |

| Specialized media and membrane sourcing volatility | -0.5% | US-wide, sharpest impact in sterile processing and dialysis segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hospital Capital Rationing Extends Filtration Replacement Cycles

Uneven capital access continues to challenge segments of the United States hospital filtration market, despite rising compliance pressures. In 2025, HFMA reported 15 hospital projects exceeding USD 1 billion, reflecting significant investments by major systems.[2]Centers for Disease Control and Prevention, “Part II, Recommendations for Environmental Infection Control in Health-Care Facilities,” CDC, cdc.gov However, smaller facilities face funding shortfalls, with a 2024 ASHE survey showing 79% received less than half of their deferred maintenance funding, and 43% secured only 10%. Budget constraints delay filtration upgrades and extend replacement cycles, slowing project conversions. Vendors now focus on lifecycle savings, energy efficiency, and reduced disruptions to address these challenges.

Maintenance Complexity Across Multi-Modal Filtration Strains Operational Capacity

The United States hospital filtration market spans air systems, water treatment, steam pathways, and medical device processing, each requiring specialized maintenance. Hospitals depend on diverse teams, but these skills are often unavailable simultaneously. A 2024 ASHE survey revealed 64% of hospitals reported increased maintenance staffing needs over three years, while only 27% saw headcount growth.[3]Association for the Advancement of Medical Instrumentation, “ANSI/AAMI ST108:2023, Water for the Processing of Medical Devices,” AAMI, aami.org Significant gaps in HVAC and controls staffing hinder filter maintenance and validation cycles, delaying new program rollouts. This drives demand for managed-service contracts, though staffing shortages continue to slow implementation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Medical Device Filtration Gains as Sterile Processing Standards Tighten

In 2025, air filtration held a 53.14% share, maintaining its lead due to its critical role in hospital ventilation systems across inpatient care, surgeries, and high-risk areas. Hospitals are required to meet stringent air handling standards, with the 2025 Standard 170 update broadening space-level requirements. Liquid filtration followed, driven by potable water safety, dialysis water treatment, and point-of-use controls.

Medical device filtration is projected to grow at a 6.10% CAGR through 2031, making it the fastest-growing segment in the United States hospital filtration market. Growth is linked to ST108 upgrades and increased reprocessing of instruments as procedural volumes shift across care sites. Complex devices now require stricter control over water quality and bioburden during reprocessing. Rising outpatient procedure acuity has increased filtration stages in workflows, pushing demand for validated systems aligned with sterile-processing protocols.

By Filtration Process: Reverse Osmosis Disrupts the Established HEPA-Centric Spend Model

HEPA filtration accounted for 44.45% share in 2025, remaining the largest process category due to its established role in hospital ventilation for high-risk and critical treatment areas. ULPA filtration catered to niche applications requiring tighter containment, while activated carbon and gas-phase systems addressed odor, chemical, and air quality control in specialized areas.

Reverse osmosis is expected to grow at a 7.40% CAGR through 2031, becoming the fastest-growing process segment in the United States hospital filtration market. This growth is driven by dialysis expansion, water safety focus, and the need for reliable sterile-processing water pathways. While reverse osmosis gains attention, it complements rather than replaces HEPA, reflecting increased focus on water-side compliance and budget allocation.

By End Use: Outpatient Growth Redistributes Filtration Spend Across the Care Continuum

Hospitals represented 57.60% of the United States hospital filtration market in 2025, leading due to their extensive ventilation, water, and sterile-processing needs. Acute-care surgical environments drive high filtration intensity, while post-acute and long-term care focus on water management programs. Diagnostic and laboratory sites, though smaller, demand high-value filtration for equipment performance and testing integrity.

Outpatient and ambulatory care is projected to grow at a 6.45% CAGR through 2031, making it the fastest-growing segment in the United States hospital filtration market. This shift reflects the move toward procedure-based care outside inpatient settings, with smaller sites requiring compliant air and water systems. Fragmented demand emphasizes supplier reach, service consistency, and quick installations over equipment scale.

By Application Area: Sterile Processing Water Becomes the Market's Most Dynamic Investment Category

Patient-care air quality held a 34.55% share of the United States hospital filtration market in 2025, driven by HVAC-linked filtration in inpatient rooms, corridors, and critical-care zones. Facility water safety followed, supported by CMS water management expectations, while clinical and diagnostic utilities filtration ensured equipment performance in laboratories and endoscope workflows. Respiratory and infusion protection also contributed through infection control applications.

Sterile processing and reprocessing water is forecast to grow at a 6.80% CAGR through 2031, becoming the most dynamic application area in the United States hospital filtration market. ST108 emphasizes water quality in medical device processing, raising standards for system specifications and maintenance. Investments focus on protecting high-value instruments and ensuring process integrity, driving demand for monitored and validated water treatment pathways.

Geography Analysis

The United States hospital filtration market operates on a national scale, with spending concentrated in regions featuring dense hospital infrastructure, older buildings, and rapid outpatient expansion. The Northeast, including states like Massachusetts, New York, and Pennsylvania, drives significant demand due to its high concentration of academic medical centers, transplant programs, and trauma facilities. Older building stock in this region necessitates air-handling retrofits, housing upgrades, and phased filtration component replacements, ensuring steady demand even when new construction is limited, as retrofits must meet current ASHE ventilation standards.

The Midwest and Mountain West exhibit distinct demand patterns in the United States hospital filtration market. Regional systems in these areas often face tighter capital constraints, leading to a focus on low lifecycle cost upgrades, pressure-drop reduction, and efficiency improvements over full system replacements. According to the 2024 ASHE hospital operations survey, 79% of respondents received less than half of their deferred maintenance funding requests, highlighting the importance of phased retrofits and managed-service support to distribute costs over time in rural and critical-access facilities.

The South, including the Sun Belt and Southeast growth corridors, is emerging as a key region in the United States hospital filtration market. Rapid population growth and outpatient expansion are driving the need for compliant air and water control across new care sites. The market benefits from repeated deployments across ambulatory and mixed-care networks rather than large single-site projects.

Competitive Landscape

In the United States hospital filtration market, top-tier players dominate, while several specialized niches remain fragmented. Key suppliers like Pall Medical, STERIS, Parker Hannifin, Camfil USA, and AAF International maintain strong positions. Hospitals prefer vendors with proven compliance records, established contract channels, and extensive filtration portfolios. Additionally, suppliers offering validation support, replacement planning, and comprehensive documentation are highly valued.

Recent strategic developments indicate how major suppliers are expanding their reach in the United States hospital filtration market. In November 2025, Parker Hannifin announced plans to acquire Filtration Group for USD 9.25 billion. This acquisition adds a business with projected 2025 sales of USD 2 billion, with 85% of revenue derived from aftermarket services. The move strengthens Parker’s presence across life sciences, HVAC/R, and industrial filtration, enhancing its ability to serve hospital clients comprehensively.

Smaller and mid-sized specialists continue to find opportunities in areas requiring focused compliance support or recurring service models. In April 2026, Nephros identified a USD 25 million annual addressable market for point-of-use filtration and related services in the Greater New York region. The broader potential lies in integrating hardware with records, monitoring, validation, and compliance documentation, which are critical during hospital inspections. Suppliers combining filters, services, and documentation are better positioned to protect margins compared to component-only providers in the United States hospital filtration market.

U.S. Hospital & Healthcare Spending For Filtration Industry Leaders

Baxter International Inc.

Pall Medical

Danaher Corporation

Nephros, Inc.

STERIS plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: STERIS invested USD 60 million over two years to establish a sterility assurance manufacturing plant in Mentor, Ohio, consolidating U.S. production into a single center of excellence with operations planned by late 2027.

- April 2026: Nephros strengthened its presence in the Greater New York City market by appointing a regional sales leader and identifying a USD 25 million annual addressable opportunity for point-of-use filtration and related services.

- November 2025: Parker Hannifin acquired Filtration Group for USD 9.25 billion, with the target business reporting expected 2025 sales of USD 2 billion and an 85% aftermarket revenue mix.

- November 2025: Camfil USA launched the AQ13 panel filter, compliant with ASHRAE 241 standards and designed for healthcare facilities and HVAC systems with 4-inch depth limitations during retrofits.

U.S. Hospital & Healthcare Spending For Filtration Market Report Scope

As per the scope of the report, the hospital & healthcare spending for filtration market refers to the capital invested by medical facilities, clinics, and laboratories into air, liquid, and gas filtration systems. Its core purpose is to maintain sterile environments, reduce healthcare-associated infections (HAIs), and ensure regulatory compliance.

The U.S. hospital and healthcare spending for the filtration market is segmented by product, filtration process, end use, and application area. By product, the market includes air filtration, liquid filtration, medical device filtration, and environmental and utility filtration. By filtration process, the market is segmented into HEPA filtration, ULPA filtration, activated carbon and gas-phase filtration, reverse osmosis, ultrafiltration, microfiltration, and endotoxin and final-barrier filtration. By end use, the market is categorized into hospitals, outpatient and ambulatory care, post-acute and long-term care, dialysis and renal care sites, and diagnostic and laboratory sites. By application area, the market is segmented into patient-care air quality, sterile processing and reprocessing water, facility water safety, clinical and diagnostic utilities, and respiratory and infusion protection. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Air Filtration |

| Liquid Filtration |

| Medical Device Filtration |

| Environmental and Utility Filtration |

| HEPA Filtration |

| ULPA Filtration |

| Activated Carbon and Gas-Phase Filtration |

| Reverse Osmosis |

| Ultrafiltration |

| Microfiltration |

| Endotoxin and Final-Barrier Filtration |

| Hospitals |

| Outpatient and Ambulatory Care |

| Post-Acute and Long-Term Care |

| Dialysis and Renal Care Sites |

| Diagnostic and Laboratory Sites |

| Patient-Care Air Quality |

| Sterile Processing and Reprocessing Water |

| Facility Water Safety |

| Clinical and Diagnostic Utilities |

| Respiratory and Infusion Protection |

| By Product | Air Filtration |

| Liquid Filtration | |

| Medical Device Filtration | |

| Environmental and Utility Filtration | |

| By Filtration Process | HEPA Filtration |

| ULPA Filtration | |

| Activated Carbon and Gas-Phase Filtration | |

| Reverse Osmosis | |

| Ultrafiltration | |

| Microfiltration | |

| Endotoxin and Final-Barrier Filtration | |

| By End Use | Hospitals |

| Outpatient and Ambulatory Care | |

| Post-Acute and Long-Term Care | |

| Dialysis and Renal Care Sites | |

| Diagnostic and Laboratory Sites | |

| By Application Area | Patient-Care Air Quality |

| Sterile Processing and Reprocessing Water | |

| Facility Water Safety | |

| Clinical and Diagnostic Utilities | |

| Respiratory and Infusion Protection |

Key Questions Answered in the Report

What is the projected value of the U. S. hospital & healthcare spending for filtration market by 2031?

The U. S. hospital & healthcare spending for filtration market is forecast to reach USD 1.12 billion by 2031, rising from USD 0.88 billion in 2026 at a 4.90% CAGR.

Which product category leads hospital filtration spending in the United States?

Air filtration led product demand with 53.14% share in 2025, supported by the broad use of HVAC-linked filtration across inpatient and surgical spaces.

Which filtration process is growing the fastest in hospitals and healthcare facilities?

Reverse osmosis is the fastest-growing process segment, with a projected 7.40% CAGR through 2031, driven by dialysis and sterile-processing water upgrades.

Why is sterile-processing water becoming more important for healthcare facilities?

ANSI/AAMI ST108 has raised attention on validated water quality for medical device reprocessing, and this is pushing stronger demand for monitored multi-step treatment pathways.

Which end-use setting is expanding fastest for filtration demand?

Outpatient and ambulatory care is expected to grow the fastest at a 6.45% CAGR through 2031, as more procedures move beyond the inpatient hospital setting.

What is the fastest-growing application area in U.S. hospital filtration?

Sterile processing and reprocessing water is the fastest-growing application area, with a projected 6.80% CAGR through 2031, supported by stricter water quality expectations and more complex instrument reprocessing.

Page last updated on: