Hospital Linen Supply And Management Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

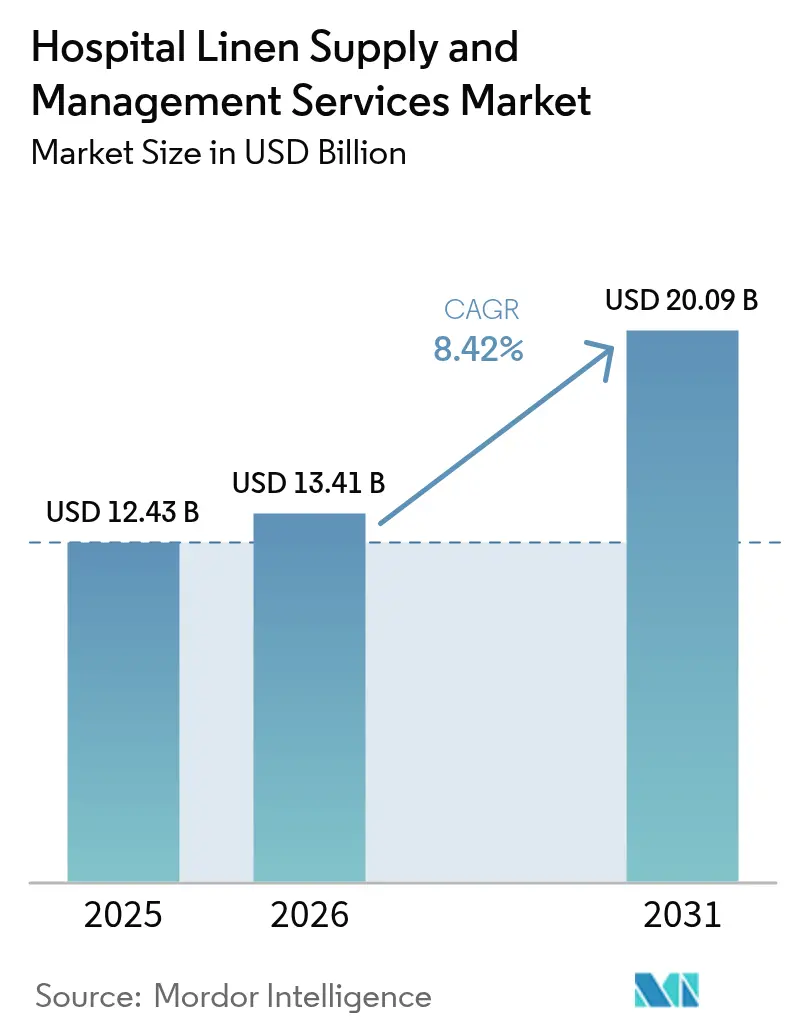

| Market Size (2026) | USD 13.41 Billion |

| Market Size (2031) | USD 20.09 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

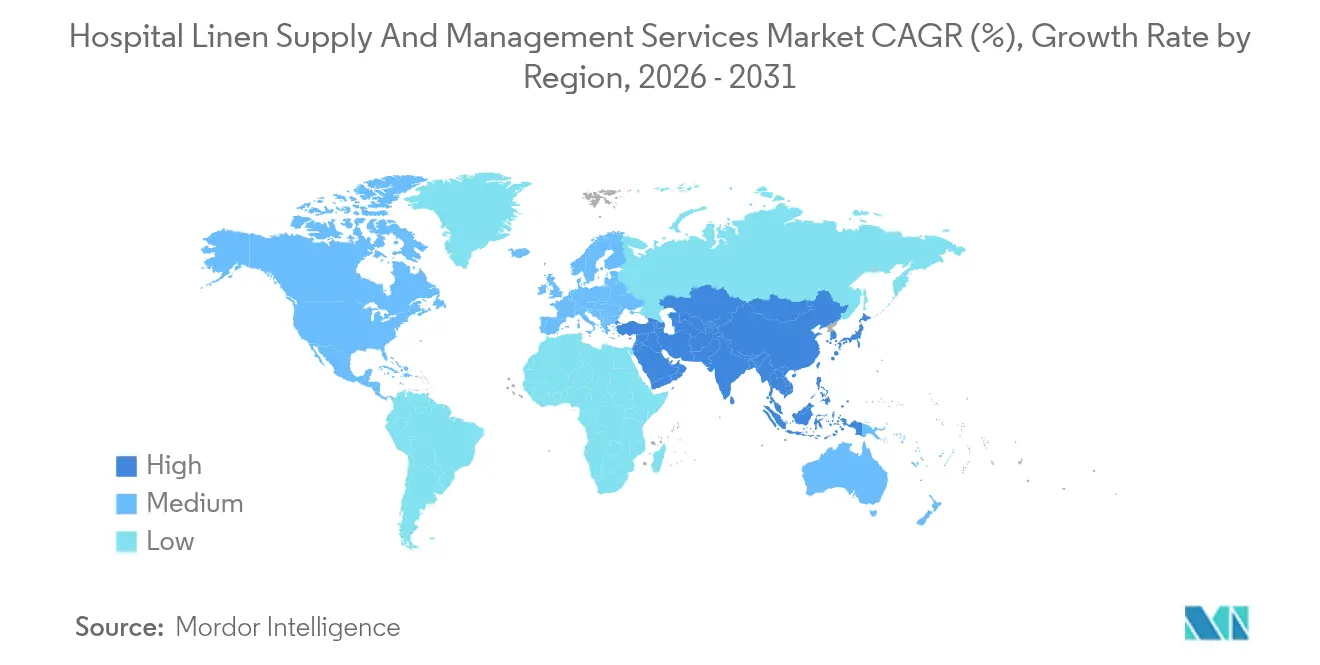

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Linen Supply And Management Services Market Analysis by Mordor Intelligence

The Hospital Linen Supply And Management Services Market size is projected to expand from USD 12.43 billion in 2025 and USD 13.41 billion in 2026 to USD 20.09 billion by 2031, registering a CAGR of 8.42% between 2026 to 2031.

Demand is expanding as aging populations drive higher bed-occupancy, hospitals outsource to avoid multi-million-dollar laundry investments, and regulators tighten infection-control rules. Outsourcing cuts per-kilogram processing costs by 13% in mid-size facilities and frees capital for clinical priorities. RFID tracking delivers a 33% labor savings and a 20% reduction in linen procurement costs, yet adoption lags in over half of North American hospitals, creating a technology arbitrage for early movers.

Key Report Takeaways

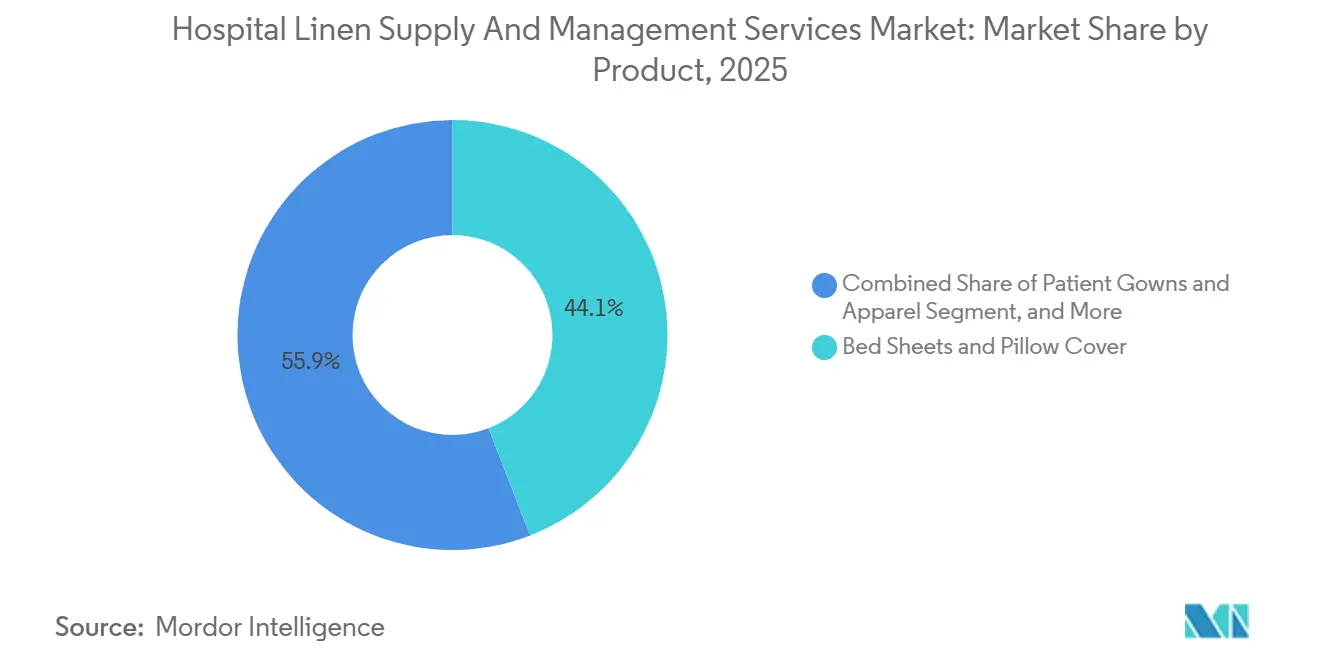

- By product category, bed sheets & pillow covers held 44.12% of the hospital linen supply and management services market share in 2025, while patient gowns & apparel are forecast to expand at a 9.20% CAGR through 2031.

- By material, woven cotton & blends accounted for 72.05% of the hospital linen supply and management services market size in 2025; non-woven disposables are projected to grow at a 9.47% CAGR to 2031.

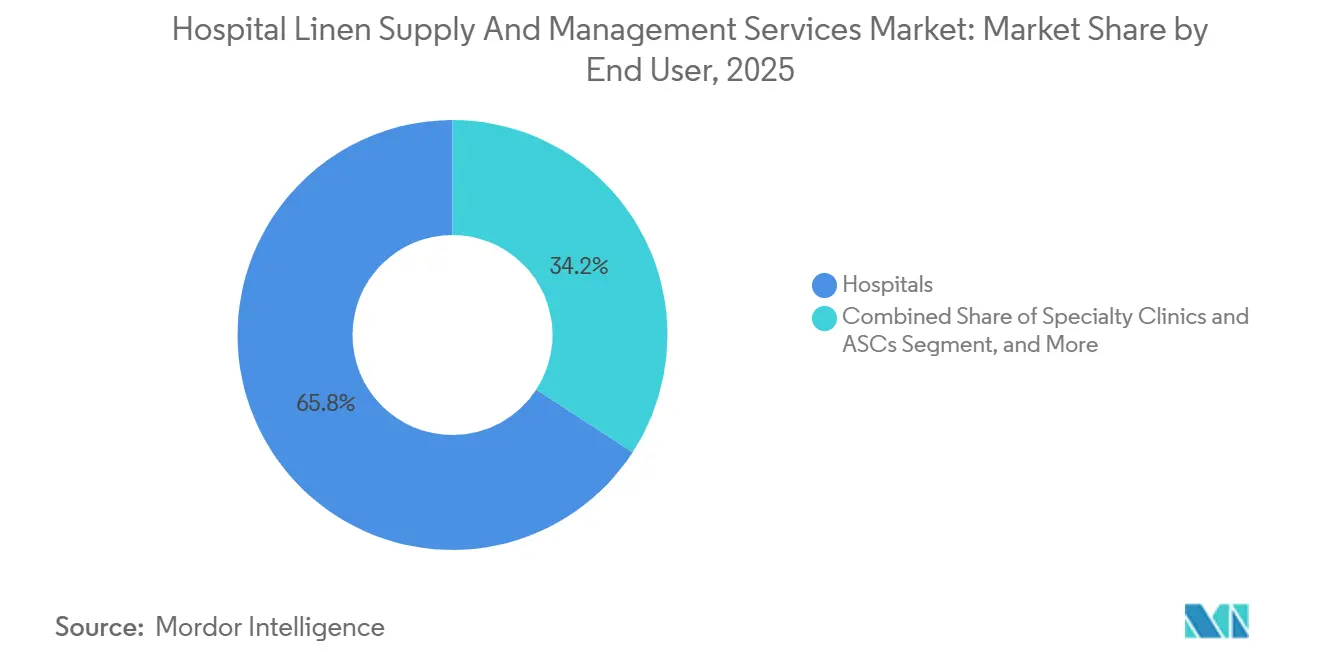

- By end user, hospitals commanded a 65.82% share in 2025, whereas specialty clinics & ASCs record the highest projected CAGR at 10.58% through 2031.

- By geography, North America captured 41.05% revenue in 2025; Asia-Pacific is advancing at a 10.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hospital Linen Supply And Management Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hospitalization Rates Amplified by Aging Population | +1.8% | Global, concentration in North America, Europe, Japan | Long term (≥ 4 years) |

| Stringent Infection Control Regulations Mandating Hygienic Linens | +1.5% | Global, led by North America and EU | Medium term (2-4 years) |

| Cost Optimization Push Driving Outsourcing of Linen Services | +1.3% | Global, rapid in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Expansion of Healthcare Infrastructure in Emerging Economies | +1.2% | Asia-Pacific core, spillover to Middle East & Africa | Long term (≥ 4 years) |

| Adoption of RFID-Enabled Tracking Increasing Service Efficiency | +0.9% | North America, Europe early; APAC following | Short term (≤ 2 years) |

| Circular Economy Initiatives Favoring Reusable Linen Programs | +0.8% | EU-led, growing in North America and select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hospitalization Rates Amplified by Aging Population

The number of people aged 75 and older will rise by 49.9% in the United States by 2037, a cohort that consumes 2.5 times as many inpatient days as younger adults, driving bed occupancy toward 85%.[1]U.S. Health Resources & Services Administration, “Aging Population Projections,” hrsa.gov Each occupied bed produces 9-12 pounds of soiled textiles a day. Longer stays tied to chronic diseases increase linen-change frequency, forcing hospitals either to add on-premises laundries costing USD 2 million per 100 beds or to pivot to HLAC-accredited vendors. China’s 60+ population will exceed 300 million by 2030, mirroring the same demand trajectory. As demographic pressure builds, the hospital linen supply and management services market is poised for structural, volume-driven growth.

Stringent Infection Control Regulations Mandating Hygienic Linens

CDC guidelines require 160 °F for 25 minutes or EPA-registered chemistries during laundering, while the Joint Commission obliges quarterly microbial testing and HLAC accreditation for suppliers.[2]Centers for Disease Control and Prevention, “Laundry: Cleaning and Sanitizing,” cdc.gov These mandates drive capital investment into tunnel washers, ozone injection, and ISO 15797 quality protocols. Antimicrobial textiles infused with copper or silver reduce MRSA and C. difficile transmission by up to 40% and are gaining FDA clearance.[3]U.S. Food & Drug Administration, “Antimicrobial Textiles,” fda.gov Higher up-front linen costs are offset by fewer hospital-acquired infections, aligning economic incentives with regulatory compliance and fueling premium-product demand within the hospital linen supply and management services market.

Cost Optimization Push Driving Outsourcing of Linen Services

A 300-bed Indian hospital cut annual linen expenses by USD 16,800 by outsourcing at USD 0.48 per kilogram, down from USD 0.55 in-house, for a 13% saving. The Texas Medical Center Laundry Co-Op processes 42 million pounds annually for 21 hospitals and saved USD 230,000 in utilities during its first year on a low-temperature peracetic-acid system. Such data confirm that outsourcing unlocks economies of scale, protects margins in value-based reimbursement models, and expands the hospital linen supply and management services market footprint beyond traditional acute-care segments.

Expansion of Healthcare Infrastructure in Emerging Economies

China added 13,000 new hospitals by 2025, and India aims to add 3 million additional beds under Ayushman Bharat. GCC spending will reach USD 159 billion by 2029, adding over 12,000 beds, 69% in Saudi Arabia. New facilities embed long-term linen contracts at the design phase, ensuring multi-year volume visibility for providers operating in the hospital linen supply and management services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Required for On-Premise Laundry Automation | -0.6% | Global, acute in small-to-medium hospitals | Medium term (2-4 years) |

| Fluctuating Cotton Prices Affecting Linen Procurement Costs | -0.5% | Global, import-dependent regions | Short term (≤ 2 years) |

| Shortage of Skilled Laundry Workforce in Urban Hospitals | -0.4% | North America, Europe, emerging APAC metros | Medium term (2-4 years) |

| Environmental Concerns Over Water & Energy Use Prompting Scrutiny | -0.3% | EU-led, spread to water-stressed areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Required for On-Premise Laundry Automation

A 100-bed hospital needs USD 2-3 million for tunnel washers, dryers, and finishing lines, plus 5,000 square feet of utility-heavy space. Sub-500-bed facilities cannot amortize these costs, so outsourced providers scale faster, thereby widening the addressable market for hospital linen supply and management services.

Fluctuating Cotton Prices Affecting Linen Procurement Costs

The Cotlook A-Index fell to USD 0.80 per pound in March 2025, yet tariffs on finished textiles add 10-15%, squeezing laundries locked into multi-year fixed-price contracts. Operators hedge by shifting toward polyester blends or sourcing from domestic mills—strategies that contain risk but may raise sustainability questions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Patient Gowns Propel Premium Growth

Bed Sheets & Pillow Covers delivered 44.12% of 2025 revenue, underpinned by three sheet changes per occupied bed weekly. Patient Gowns & Apparel, however, will grow at 9.20% CAGR, the fastest pace in the hospital linen supply and management services market, as antimicrobial fabrics command premium pricing and hospitals prioritize patient dignity. Surgical Drapes & Wrappers show a structural move toward disposable polypropylene in trauma and cardiac theaters.

Commodity towels and blankets rise mainly with new-bed additions, but the growth edge lies in procedure-specific packs for orthopedic and ophthalmic ASCs that fetch USD 15-25 per kit. Vendors with FDA-cleared antimicrobial portfolios improve margins and enhance stickiness in the hospital linen supply and management services market.

By Material: Disposable Non-Wovens Accelerate

Woven Cotton & Blends owned 72.05% share in 2025 and remains essential for bed and bath linens due to comfort and moisture absorption. Non-Woven Disposables are set to grow 9.47% CAGR as infection-control stakes rise. ASTM-compliant polypropylene drapes offer viral-penetration resistance at a lower per-unit cost and eliminate laundering logistics from OR schedules.

Sustainability pressures moderate disposable adoption in Europe, where landfill levies exceed EUR 100 per ton, steering low-risk procedures back to reusables. Blended polyester-cotton offers price stability amid cotton volatility, though microplastic rules in California and the EU may restrain uptake. These cross-currents shape material strategy within the hospital linen supply and management services market.

By End User: ASCs Outpace Acute-Care Hospitals

Hospitals generated 65.82% revenue in 2025, with large medical centers exceeding 15,000 pounds weekly throughput. Yet specialty clinics & ASCs will log a 10.58% CAGR to 2031 as Medicare channels orthopedic and ophthalmic procedures to outpatient settings.

ASCs need same-day turnaround and procedure-pack customization, a service that niche laundries monetize at higher per-pound rates. Long-term care facilities are shifting from in-house to outsourced laundry amid infection-control mandates, creating a new volume stream in the hospital linen supply and management services market for post-acute products such as incontinence pads and pressure-relief covers.

Geography Analysis

North America accounted for 41.05% of 2025 revenue, driven by mature outsourcing penetration above 60% and strict HLAC compliance. Private-equity deals such as PureStar’s 2026 acquisition of Emerald Textiles consolidate regional operators into multistate networks. Canada’s single-payer system standardizes linen protocols across provinces, while Mexico’s medical-tourism corridor raises quality benchmarks.

Asia-Pacific, forecast at 10.97% CAGR, will become the fastest-growing region as China’s healthcare spending heads for USD 1.8 trillion by 2030 and India deploys 3 million new beds. Centralized laundry hubs near mega-hospitals in Shanghai and Delhi capture scale advantages, accelerating the diffusion of RFID and ozone technologies in the hospital linen supply and management services market.

Europe faces slower unit growth but leads on sustainability mandates. Elis SA’s 440 plants across 29 countries capture multi-country contracts by offering traceable, low-impact wash chemistry. The Middle East & Africa benefits from USD 159 billion in GCC healthcare spending, with Saudi Arabia privatizing 290 hospitals by 2030 and generating greenfield contracts under long-term PPP models. South America’s fragmented provider base outsources linen to mitigate currency shocks and tariff costs, though equipment import duties constrain the pace of modernization.

Competitive Landscape

The hospital linen supply and management services market remains moderately concentrated. Private equity is reshaping ownership: PureStar’s 2026 Emerald Textiles deal created a 12-plant network with three depots, and The Pritzker Organization invested in Crown Health Care Laundry Services to assemble a Southeast U.S. platform. The strategy centers on RFID-enabled traceability, AI-driven predictive maintenance, and low-temperature peracetic-acid chemistry that reduces fabric damage by 30-50%.

White space persists in long-term care and home health bundles. NOVO Health Services purchased EcoBrite Linen in December 2025 to expand into nursing-home outsourcing, where penetration had just topped 20%. Disruptors deploy chipless RFID tags priced below USD 0.01, enabling economic tracking of single-use drapes and widening the competitive moat for innovators within the hospital linen supply and management services market.

Hospital Linen Supply And Management Services Industry Leaders

Unitex Textile Rental Services, Inc.

Emes Textiles Pvt. Ltd

ImageFIRST

Tetsudo Linen Service Co., Ltd

Angelica Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: SSM Health and BJC HealthCare launched St. Louis Healthcare Support Services to process 35 million lbs of linens annually by mid-2025

- January 2024: Mohawk Medbuy Corporation (MMC) sold its Linen Services division to Ecotex Healthcare Linen Service, aimed to sharpen its focus on expanding its national healthcare supply chain services.

Global Hospital Linen Supply And Management Services Market Report Scope

As per the scope of this report, hospital linen supply and management services are professional services that aid in providing and maintaining hospital or healthcare institution linen supplies to ensure optimal hygiene.

The hospital linen supply and management services market is segmented by product, material, end-user, and geography. By product, the market is segmented into bed sheets and pillow covers, blankets, bed covers, and others (bathing and cleaning accessories, patient repositioners, and others). By material, the market is segmented into woven cotton & blends, non-woven disposables, and others. By end-user, the market is segmented into hospitals, specialty clinics & ASCs, and long-term care & rehab centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Bed Sheets & Pillow Cover |

| Patient Gowns & Apparel |

| Towels & Bath Linens |

| Surgical Drapes & Wrappers |

| Blankets |

| Others |

| Woven Cotton & Blends |

| Non-Woven Disposables |

| Others |

| Hospitals | Large Hospitals (>500 beds) |

| Medium Hospitals (100-499 beds) | |

| Small Hospitals (<100 beds) | |

| Specialty Clinics & ASCs | |

| Long-Term Care & Rehab Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Bed Sheets & Pillow Cover | |

| Patient Gowns & Apparel | ||

| Towels & Bath Linens | ||

| Surgical Drapes & Wrappers | ||

| Blankets | ||

| Others | ||

| By Material | Woven Cotton & Blends | |

| Non-Woven Disposables | ||

| Others | ||

| By End User | Hospitals | Large Hospitals (>500 beds) |

| Medium Hospitals (100-499 beds) | ||

| Small Hospitals (<100 beds) | ||

| Specialty Clinics & ASCs | ||

| Long-Term Care & Rehab Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the hospital linen supply and management services market in 2031?

The market is projected to reach USD 20.09 billion by 2031.

Which product segment is expanding fastest?

Patient Gowns & Apparel are forecast to grow at 9.20% CAGR through 2031.

Which region shows the highest growth rate?

Asia-Pacific is advancing at a 10.97% CAGR driven by large-scale hospital construction.

How does RFID improve linen operations?

Deployments cut labor costs by 33% and linen purchases by 20%, with payback in under two years.

Why are hospitals outsourcing linen services?

Outsourcing delivers 13% per-kilogram cost savings and removes the need for multi-million-dollar on-premise laundries.

Page last updated on: