United States Healthcare Staffing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

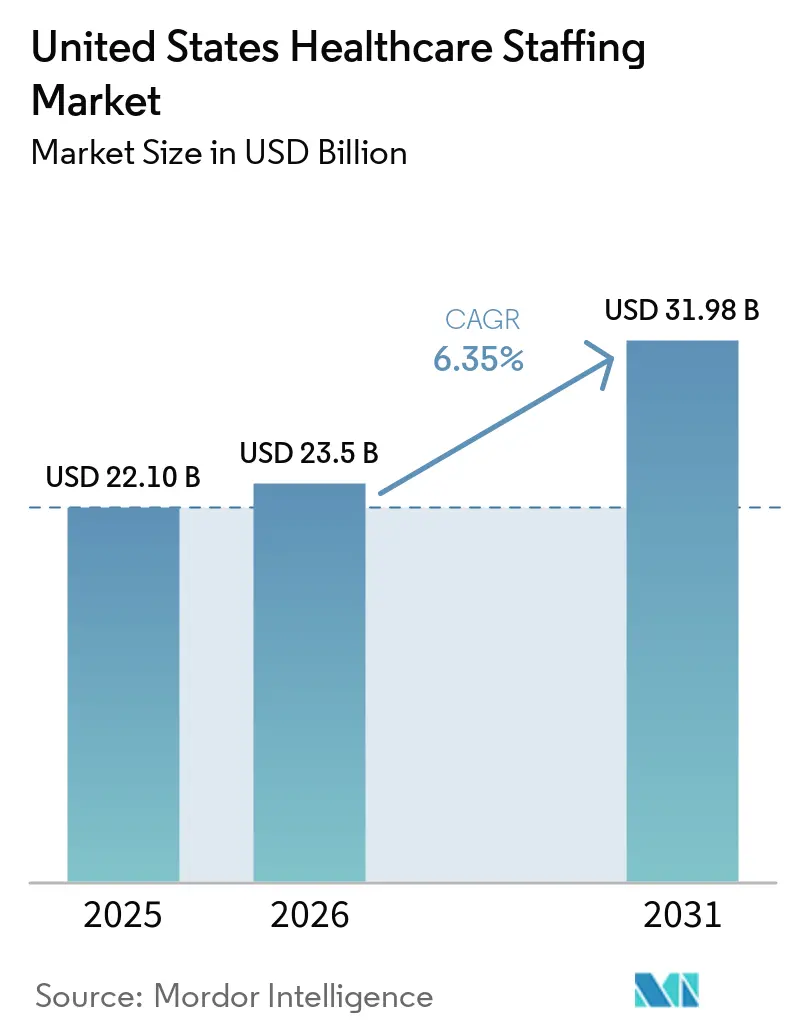

| Base Year Market Size (2025) | USD 22.10 Billion |

| Market Size (2026) | USD 23.5 Billion |

| Market Size (2031) | USD 31.98 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

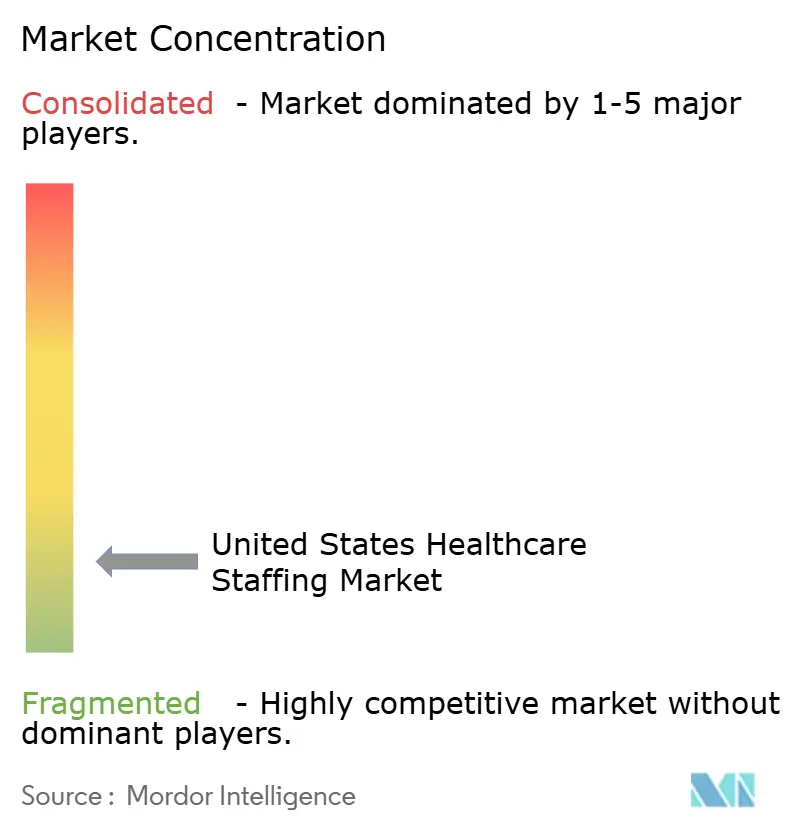

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Healthcare Staffing Market Analysis by Mordor Intelligence

The United States Healthcare Staffing Market size is expected to grow from USD 22.10 billion in 2025 to USD 23.5 billion in 2026 and is forecast to reach USD 31.98 billion by 2031 at 6.35% CAGR over 2026-2031.

The United States (US) healthcare staffing market entered 2026 on a recovery path after post-pandemic normalization reduced travel nurse revenue by 36% between 2022 and 2025 as bill rates moved closer to pre-crisis levels. This phase looks different from the earlier cycle because contingent labor is now built into health system workforce planning, not treated only as an emergency tool. Structural imbalance in labor supply remains in place because demand is shaped by demographics, training bottlenecks, and clinician preferences for more flexible work arrangements. The Bureau of Labor Statistics projects 193,100 registered nurse job openings each year through 2032, while nursing schools turned away 65,766 qualified applicants in 2023 because of faculty shortages and limited clinical placements, which keeps the replacement gap wide across the US healthcare staffing market. Growth is concentrating in locum tenens, home-based care settings, advanced practice provider coverage, and tele-staffing, while hospital margin pressure and tighter reimbursement keep pricing discipline high and favor larger operators with stronger technology and delivery scale in the US healthcare staffing market.

Key Report Takeaways

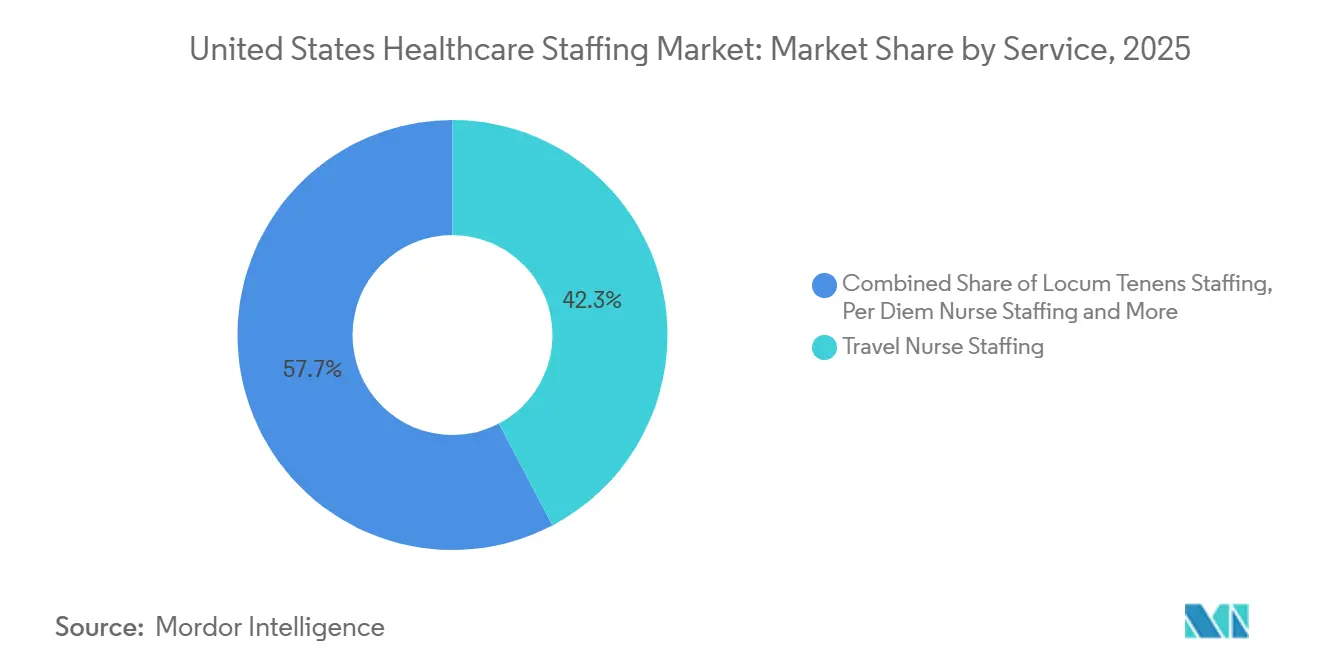

- By service, travel nurse staffing held 42.31% of revenue in 2025, while locum tenens staffing is projected to expand at an 8.38% CAGR through 2031.

- By end user, hospitals held 41.24% of revenue in 2025, while home health, hospice, and PACE organizations are forecast to grow at an 8.52% CAGR through 2031.

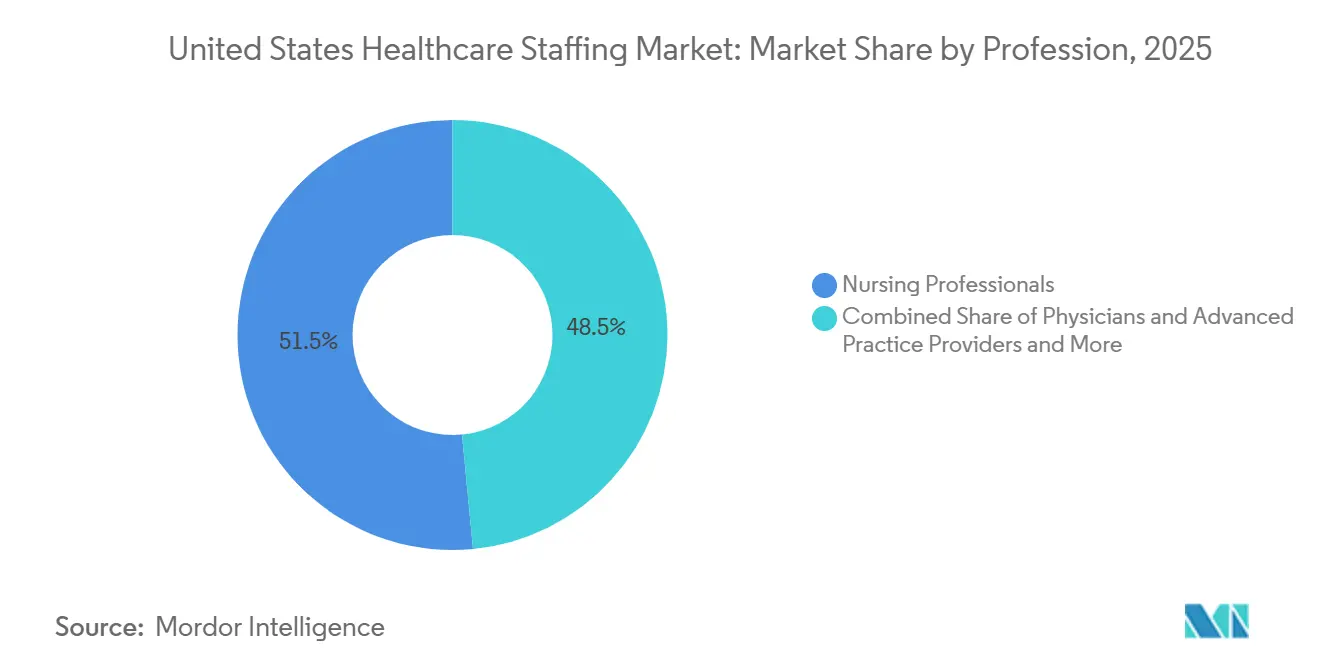

- By profession, nursing professionals accounted for 51.52% of revenue in 2025, while physicians and advanced practice providers are projected to advance at an 8.25% CAGR through 2031.

- By delivery mode, on-site staffing held 60.54% of revenue in 2025, while remote and tele-staffing is projected to grow at an 8.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Healthcare Staffing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population And Chronic Disease Burden | +1.5% | National, concentrated in Southeast (FL, TX, GA) and Southwest (AZ, NV) | Long term (≥ 4 years) |

| Provider Shortages And Burnout-Driven Vacancy Levels | +1.8% | National, acute in rural Midwest, Appalachian, and Mountain West regions | Medium term (2-4 years) |

| Flexible Labor Adoption For Cost And Coverage Management | +1.2% | National, led by Northeast and Pacific Coast integrated health systems | Medium term (2-4 years) |

| Expansion Of Home Health, Outpatient, And Post-Acute Sites Of Care | +1.0% | National, with early gains in FL, TX, OH, PA | Long term (≥ 4 years) |

| Interstate Licensure And Tele-Staffing Accelerating Multi-State Deployment | +0.6% | National, particularly rural Midwest, Mountain West, and newly compliant states | Short term (≤ 2 years) |

| APP-Led Coverage Redesign For Hard-To-Fill Specialties | +0.7% | National, concentrated in primary care shortage areas and rural geographies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic Disease Burden

The aging of the US population is widening the care burden that providers must absorb across acute care, home health, and post-acute settings in the US healthcare staffing market. The population aged 65 and older is expected to reach 23% of the total population by 2050, or 82 million people, and more than half of this group is expected to develop serious disabilities that require paid long-term services. That shift changes the acuity mix because patients are leaving hospitals sooner and entering home-based and post-acute settings with more complex clinical needs. Those care sites usually do not have deep permanent staffing benches, so they rely more heavily on contingent clinicians to absorb higher-complexity caseloads. Chronic disease management also pushes demand toward specialist locum coverage in cardiology, pulmonology, and behavioral health, which supports stronger revenue per placement even when general travel nurse rates remain under pressure.

Provider Shortages and Burnout-Driven Vacancy Levels

Provider burnout continues to feed vacancy levels in the US healthcare staffing market even though some burnout indicators have improved from their recent peaks. The American Medical Association reported a physician burnout rate of 41.9% in 2025, with emergency medicine at 49.8%, showing that stress remains concentrated in hospital-based specialties that are difficult to staff[1]“AMA: Physician Burnout Rates Are Falling, Specialty Gaps Remain,” American Medical Association, ama-assn.org. Nursing trends show a similar split because 75% of nurses reported career satisfaction, yet 58% said they experience burnout most days and only 39% planned to stay in their current jobs over the next 12 months. That means churn, not only total workforce loss, is driving placement demand as clinicians move into travel work, per diem roles, or early retirement. Replacement pressure remains strong enough that temporary staffing demand can stay elevated even when total system headcount looks stable on paper.

Flexible Labor Adoption for Cost and Coverage Management

The US healthcare staffing market is benefiting from a structural shift in labor strategy as health systems move from fixed staffing models toward variable labor pools. Internal float pools, per diem layers, and on-demand marketplaces are now used in sequence before facilities escalate to premium agency channels, which creates a broader and more organized demand stack. ShiftMed reported a USD 15 to USD 30 per hour premium pay gap between local on-demand clinicians and traditional agency-sourced staff across major markets in 2026, which shows why buyers are pushing vendors toward technology-based fulfillment models. Hallmark found that 59% of healthcare leaders viewed technology limits as the main barrier to offering per diem roles, which suggests adoption is constrained more by infrastructure than by clinician interest. Labor still represents around 60% of total hospital operating expenses and labor costs rose 5.6% in 2025, so the pressure is to optimize labor mix rather than simply eliminate contingent staffing from the US healthcare staffing market.

Expansion of Home Health, Outpatient, and Post-Acute Sites of Care

The US healthcare staffing market is also being supported by the steady movement of care away from the inpatient hospital setting. Outpatient revenue increased 16.8% from Q4 2023 to Q4 2025, while inpatient revenue increased 9.0% over the same period, which confirms that care delivery is becoming more decentralized. Ambulatory centers, physician offices, post-acute providers, and home-based care organizations do not carry the same permanent workforce depth as large hospitals, so they rely more heavily on agency labor for continuity. Home health also has to manage high turnover and rising patient complexity, which makes internal capacity building difficult and increases recurring use of contingent clinical staff. At the same time, tighter reimbursement in home health rewards scale, scheduling discipline, and technology-led cost control, which gives larger staffing operators an advantage as the US healthcare staffing market expands into these settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hospital Margin Pressure And Reimbursement Volatility | -1.5% | National, most acute in low-reimbursement rural and safety-net markets | Medium term (2-4 years) |

| Credentialing, Privileging, And Compliance Complexity | -0.7% | National | Short term (≤ 2 years) |

| MSP/VMS Fee Compression And Reduced Vendor Access | -0.5% | National, more acute in Northeast and Midwest health-system-dense regions | Medium term (2-4 years) |

| Visa And Immigration Bottlenecks For Internationally Trained Clinicians | -0.8% | National, concentrated in NY, MA, CA, PA, OH | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hospital Margin Pressure and Reimbursement Volatility

Hospital finances remain the main near-term constraint on the US healthcare staffing market. Median operating margin fell to -0.6% in January 2026 from 1.3% in December 2025, while total expenses kept rising faster than revenue. The American Hospital Association reported that hospital expenses rose 7.5% in 2025, with drug costs up 13.6% and supply costs up 9.9%, which leaves procurement teams looking for labor savings even when staffing is not the original source of cost inflation. Medicare reimbursement covered only 83 cents of every dollar of hospital costs in 2024, which keeps the reimbursement gap structural rather than temporary[2]“Costs of Caring: Challenges Facing America’s Hospitals as They Care for Patients in 2026,” American Hospital Association, aha.org. As a result, clients are consolidating vendors, expanding MSP oversight, and pushing rate compression harder, which narrows room for smaller agencies without proprietary platforms or compliance infrastructure.

Visa and Immigration Bottlenecks for Internationally Trained Clinicians

Visa policy disruption is limiting one of the relief valves that many providers use to close persistent workforce gaps in the US healthcare staffing market. Internationally trained clinicians hold an important role in rural access, primary care, and shortage specialties, so visa delays affect both near-term staffing and longer training pipelines. CBS News reported that a new USD 100,000 H-1B petition fee for workers based outside the United States has made international recruitment materially harder for rural and safety-net hospitals that already operate with very thin margins. KFF also noted that healthcare and social assistance H-1B approvals had been rising, moving from nearly 18,000 in fiscal year 2022 to more than 19,000 in fiscal year 2025, even as approvals in other sectors declined. That interruption pushes more demand back toward domestic agency channels, especially in psychiatry, primary care, and internal medicine where international clinicians have been especially important.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Travel Nursing Anchors Revenue While Locums Reshape Growth Calculus

Travel nurse staffing held 42.31% of revenue in 2025, making it the largest service line in the US healthcare staffing market. Its position remains tied to the segment’s role as the primary flex-labor buffer for acute-care facilities dealing with census swings and difficult specialty coverage. The segment is becoming more specialty-driven than geography-driven because ICU, emergency medicine, and behavioral health roles still command higher bill rates than general medical-surgical assignments. This means travel nursing is retaining strategic importance even after broad post-pandemic rate normalization. At the same time, locum tenens staffing is the fastest-growing service category and is projected to expand at an 8.38% CAGR through 2031, which shows where the sharpest unmet physician and APP gaps are forming.

Locum tenens growth is being reinforced by changing care models rather than only by temporary vacancy spikes. Advanced practice provider use within the locum tenens segment increased by nearly 25% year over year in the first half of 2024 as scope-of-practice expansion and facility redesign moved more coverage responsibility away from physician-only models. Flexible scheduling supports that pattern because 81% of nurses said schedule flexibility would do the most to improve working conditions. Allied healthcare staffing segment is led by imaging, respiratory care, and surgical support roles, while strike staffing, international nurse staffing, and health-plan staffing give larger operators broader revenue diversification across the US healthcare staffing industry. Other service niches can also produce sharp revenue spikes, as shown by AMN Healthcare’s labor disruption events.

By End User: Home Health Acceleration Driven by Care Decentralization

Hospitals accounted for 41.24% of revenue in 2025 and remained the largest end-user group in the US healthcare staffing market. They still need large volumes of contingent labor because inpatient care, emergency operations, surgery, and high-acuity units cannot function with narrow staffing buffers. Even so, the fastest demand expansion is coming from home health, hospice, and PACE organizations, which are projected to grow at an 8.52% CAGR through 2031. That shift reflects the movement of Medicare spending and care delivery toward home- and community-based models, especially for dementia, palliative, and chronic disease management. In this part of the US healthcare staffing market size, agencies are increasingly supplying skilled clinical labor rather than only lower-cost support roles.

The friction in home-based care is not only demand growth, but also the inability of providers to create lasting internal workforce stability. High turnover in frontline home health roles and the rising acuity of patients in the home setting make agency-supplied nurses and allied clinicians critical for continuity. Hospitals are also managing two opposing forces at the same time because compliance requirements create a practical floor for contingent staffing, while weak margins keep procurement teams aggressive in contract negotiations. Ambulatory surgical centers, physician groups, and clinics are adding demand as outpatient procedures increase and physician practices struggle with a 129-day average time-to-fill for permanent physician positions. Long-term care and rehabilitation facilities also support steady agency demand because vacancy and turnover remain elevated in licensed practical nursing roles, and compliance-led minimum staffing expectations make shift-by-shift coverage harder to manage with permanent staff alone. This keeps end-user demand broad even as the growth center moves away from traditional hospital-only buying patterns in the US healthcare staffing market.

By Profession: Nursing Dominance Masks a Structural Attrition Problem

Nursing professionals accounted for 51.52% of revenue in 2025, giving the profession the largest position in the US healthcare staffing market share by workforce type. That scale reflects the basic size of registered nurse and practical nurse demand across hospitals, long-term care, post-acute care, and home-based services. The profession’s weight also means that even modest changes in nurse churn or licensing flow can move total staffing demand materially. Press Ganey reported in 2026 that 1 in 5 early-career nurses is leaving their organizations, which weakens the future permanent workforce by draining the group expected to mature into experienced staff over the next decade. AACN also cited HRSA projections showing a nationwide RN shortage of 78,610 full-time equivalents in 2025, which confirms that the staffing gap is structural rather than short-lived.

Physicians and advanced practice providers are the fastest-growing profession segment and are forecast to advance at an 8.25% CAGR from 2026 to 2031 in the US healthcare staffing market. Their growth reflects APP-led coverage redesign in primary care, behavioral health, and hospitalist models where facilities are redistributing work that had historically sat with physician-only teams. This part of the US healthcare staffing industry is also benefiting from harder-to-fill anesthesia and specialty care needs, where locum use remains a practical answer to skill scarcity. Allied health professionals such as imaging technologists, respiratory therapists, physical therapists, and laboratory staff continue to see demand tied to outpatient growth and specialized service-line expansion. Non-clinical and administrative professionals are also gaining importance because hospitals face billing, claims, and regulatory complexity that the American Hospital Association values at around USD 43 billion each year in claims management costs. The profession mix therefore shows that nursing still dominates current revenue, but faster expansion is spreading into physician, APP, allied, and administrative categories where coverage gaps are harder to solve with conventional hiring.

By Delivery Mode: Tele-Staffing Growth Moderated by In-Person Compliance Requirements

On-site staffing held 60.54% of revenue in 2025, so it remained the dominant delivery mode across the US healthcare staffing market. Acute care, surgery, imaging, and bedside nursing still require physical presence, which limits how far remote coverage can replace traditional staffing. Even so, remote and tele-staffing is the fastest-growing delivery mode and is expected to expand at an 8.83% CAGR through 2031. Growth is being supported by interstate licensure compacts that reduce the time needed to deploy clinicians across state lines. The Interstate Medical Licensure Compact covered 42 states, the District of Columbia, and Guam, and 37.4% of all initial medical licenses were issued through the compact pathway in 2024, up from 31% in 2022.

Tele-staffing is growing because it expands the effective reach of limited clinician supply across many facilities and geographies. It is especially useful for behavioral health, primary care follow-up, specialty consults, and APP-led coverage models where travel time and local shortage conditions slow traditional staffing. At the same time, some Medicare-covered services are moving back toward in-person delivery in 2026, which is increasing demand for on-site locum coverage in specialties that had leaned more heavily on virtual care. The result is not a substitution story where remote staffing simply replaces on-site labor. Instead, remote and on-site models are growing together because compact licensing expands multi-state deployment while clinical rules still protect the need for bedside presence. As more APP compact pathways become operational, tele-staffing capacity should widen further, but the largest revenue base in the US healthcare staffing market will remain tied to in-person clinical delivery for the foreseeable period.

Geography Analysis

The Southeast and broader Sun Belt represent the most concentrated demand cluster within the US healthcare staffing market. Florida, Texas, Georgia, and Arizona are carrying heavier staffing needs because they combine older populations, faster population growth, and continued pressure on provider capacity. That mix raises demand across hospitals, home health, post-acute care, and outpatient settings rather than in one service line alone. The same demographic shift that lifts care demand also raises the need for clinicians comfortable with chronic disease management, senior care, and home-based monitoring, which broadens the opportunity set for agencies with multi-setting coverage capabilities. In practical terms, the US healthcare staffing market size is increasingly influenced by states where patient growth is outpacing the ability of permanent workforce pipelines to respond.

The Northeast absorbs a large share of MSP-managed staffing demand because it has dense networks of academic medical centers, integrated delivery systems, and unionized clinical workforces. Pennsylvania’s activation of the Interstate Medical Licensure Compact, Nurse Licensure Compact, and Physical Therapy Compact in July 2025 reduced physician licensing turnaround from 43 days to 10 days and nurse licensing from 25 business days to 5 business days, which lowers deployment friction for multi-state staffing vendors. Visa disruption is also felt more strongly in this region because New York and Massachusetts accounted for 23% of all healthcare-sector H-1B approvals in fiscal year 2025. That leaves the Northeast exposed to both demand concentration and supply disruption at the same time in the US healthcare staffing market.

The Midwest and Mountain West face a different staffing pattern because the main challenge is rural access, travel distance, and thin specialist coverage rather than only raw workforce volume. Only 10% of US physicians serve 20% of the population in rural and frontier areas, which makes locum tenens and rotating specialty coverage central to care delivery in these markets. Rural critical-access hospitals often depend on locums for a meaningful share of physician shifts, so visa constraints and recruitment delays can lift agency demand even further. New compact activity in states such as Arkansas, where more than one-third of residents live in health professional shortage areas, expands the addressable geography for national staffing networks and tele-enabled deployment models.

Competitive Landscape

The US healthcare staffing market remains fragmented by agency count, but revenue is moving toward larger operators with broader platforms and stronger compliance systems. Competition in 2025 and 2026 is moving away from pure placement volume and toward technology depth, especially in credentialing automation, workforce analytics, shift prediction, and VMS integration. Cross Country Healthcare agreed to be acquired by Knox Lane in an all-cash transaction valued at USD 437 million in May 2026, which shows that scale assets in this market are attracting private capital interest. The same period also showed that regulators view staffing technology platforms as meaningful competitive assets, not just service add-ons, which raises the strategic value of workflow software and data tools. White space remains visible in locum and nurse VMS expansion, where vendors are trying to centralize a sourcing process that is still not fully standardized across the US healthcare staffing market.

Hybrid platform-and-agency models are becoming more important because they combine clinician networks with embedded workforce software. ShiftMed’s March 2026 integration with symplr Smart Square let hospitals route open shifts directly from enterprise scheduling systems into ShiftMed’s clinician network, making the staffing process more embedded in daily operations[3]“ShiftMed Announces Integration with symplr Smart Square to Expand Flexible Staffing for Health Systems,” ShiftMed, shiftmed.com. CHG Healthcare’s Nursesmart launch in 2025 targeted the same direction by bringing vendor management capabilities into nurse staffing workflows. These moves show that competitive advantage is increasingly tied to owning workflow access and fulfillment data, not only recruiter scale.

Mergers and acquisitions continue to reshape competitive positions in the US healthcare staffing market. Elite365 Family of Brands acquired Focus Staff in January 2026 to broaden its national contingent staffing platform across travel nursing and allied health. Smaller independent firms still matter in local niches, rural coverage, and specialty staffing, but they face more pressure when hospital clients want national contracts, deeper credentialing infrastructure, or tighter MSP alignment. This keeps the competitive structure fragmented in appearance, but increasingly consolidated in revenue and bargaining power.

United States Healthcare Staffing Industry Leaders

Aya Healthcare

CHG Healthcare

Jackson Healthcare

Medical Solutions

AMN Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Elite365 Family of Brands, backed by Regal Healthcare Capital Partners, acquired Focus Staff, a Joint Commission-certified travel nursing and allied health staffing provider operating across all 50 states, to expand its national contingent staffing platform.

- January 2026: Adecco acquired Advantis Medical Staffing, a U.S.-based travel nursing and allied health firm, to strengthen its healthcare staffing services in North America and improve its AI-powered recruiting and onboarding platform.

United States Healthcare Staffing Market Report Scope

As per the scope of the report, healthcare staffing refers to the process of recruiting, hiring, and managing healthcare professionals such as doctors, nurses, technicians, and support staff to ensure that healthcare facilities have the appropriate personnel to deliver quality patient care. It involves sourcing qualified staff, scheduling, and maintaining workforce needs to meet the demands of healthcare services.

The segmentation of the United States healthcare staffing market is categorized by service, end user, profession, and delivery mode. By service, it includes travel nurse staffing, per diem nurse staffing, locum tenens staffing, allied healthcare staffing, and other services. By end user, it covers hospitals, ambulatory surgical centers, physician groups and clinics, long-term care and rehabilitation facilities, home health, hospice, and PACE organizations, and other end users. By profession, it comprises nursing professionals, physicians and advanced practice providers, allied health professionals, and non-clinical and administrative professionals. By delivery mode, it is segmented into on-site staffing and remote/tele-staffing. For each segment, the market size and forecast are provided in terms of value (USD).

| Travel Nurse Staffing |

| Per Diem Nurse Staffing |

| Locum Tenens Staffing |

| Allied Healthcare Staffing |

| Other Services |

| Hospitals |

| Ambulatory Surgical Centers |

| Physician Groups and Clinics |

| Long-term Care and Rehabilitation Facilities |

| Home Health, Hospice, and PACE Organizations |

| Other End Users |

| Nursing Professionals |

| Physicians and Advanced Practice Providers |

| Allied Health Professionals |

| Non-clinical and Administrative Professionals |

| On-site Staffing |

| Remote/Tele-staffing |

| By Service | Travel Nurse Staffing |

| Per Diem Nurse Staffing | |

| Locum Tenens Staffing | |

| Allied Healthcare Staffing | |

| Other Services | |

| By End User | Hospitals |

| Ambulatory Surgical Centers | |

| Physician Groups and Clinics | |

| Long-term Care and Rehabilitation Facilities | |

| Home Health, Hospice, and PACE Organizations | |

| Other End Users | |

| By Profession | Nursing Professionals |

| Physicians and Advanced Practice Providers | |

| Allied Health Professionals | |

| Non-clinical and Administrative Professionals | |

| By Delivery Mode | On-site Staffing |

| Remote/Tele-staffing |

Key Questions Answered in the Report

What is driving growth in US healthcare staffing through 2031?

Growth is being supported by structural nurse and physician shortages, broader use of flexible labor models, and faster expansion in locum tenens, home-based care, and tele-staffing. The market is projected to rise from USD 23.50 billion in 2026 to USD 31.98 billion by 2031 at a 6.35% CAGR.

Which service category is largest in US healthcare staffing?

Travel nurse staffing remained the largest service category with a 42.31% revenue share in 2025, reflecting its role as the main flex-labor buffer for acute-care facilities.

Which service category is growing the fastest?

Locum tenens is the fastest-growing service segment, with an expected 8.38% CAGR through 2031, supported by physician shortages and wider APP use.

Which end users are expanding most quickly?

Home health, hospice, and PACE organizations are the fastest-growing end-user group, with an 8.52% CAGR through 2031 as care shifts away from inpatient settings.

Why does nursing still dominate revenue?

Nursing professionals accounted for 51.52% of 2025 revenue because hospitals, post-acute providers, and home-based care settings all depend heavily on registered and practical nurses, while attrition keeps vacancies high.

How important is tele-staffing in future care delivery?

Remote and tele-staffing is forecast to grow at an 8.83% CAGR through 2031, helped by interstate licensure compacts, but on-site staffing still held 60.54% of revenue in 2025 because many clinical roles require physical presence.

Page last updated on: