Hospital Outsourcing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

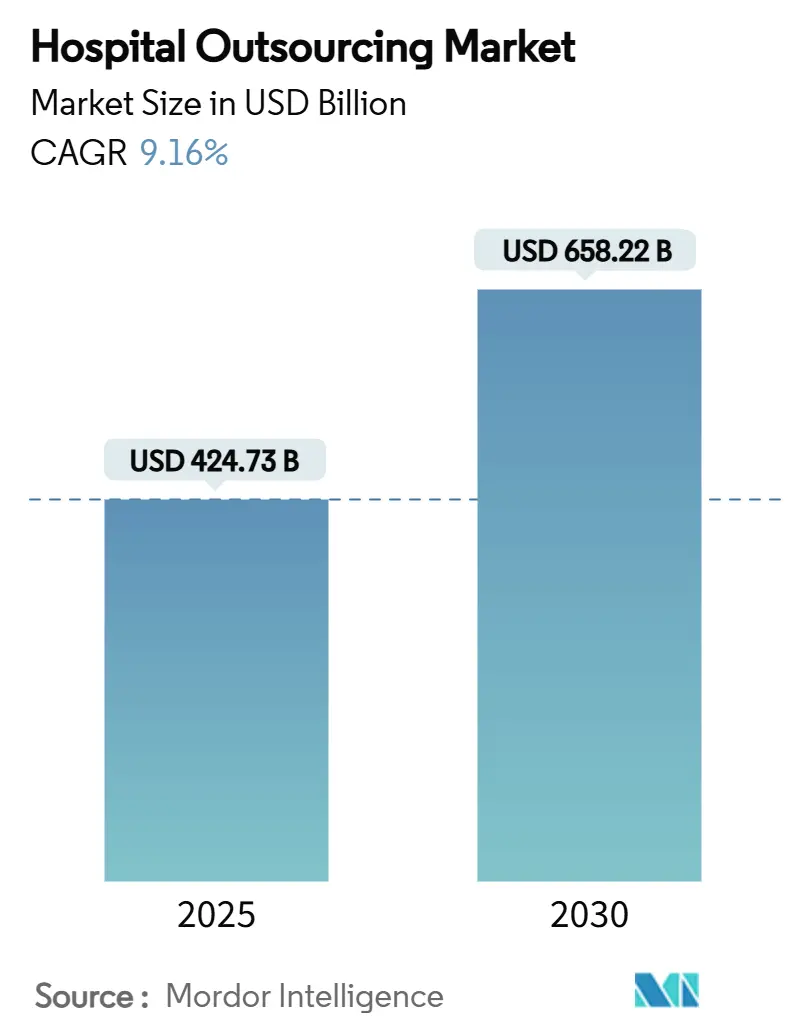

| Market Size (2025) | USD 424.73 Billion |

| Market Size (2030) | USD 658.22 Billion |

| Growth Rate (2025 - 2030) | 9.16% CAGR |

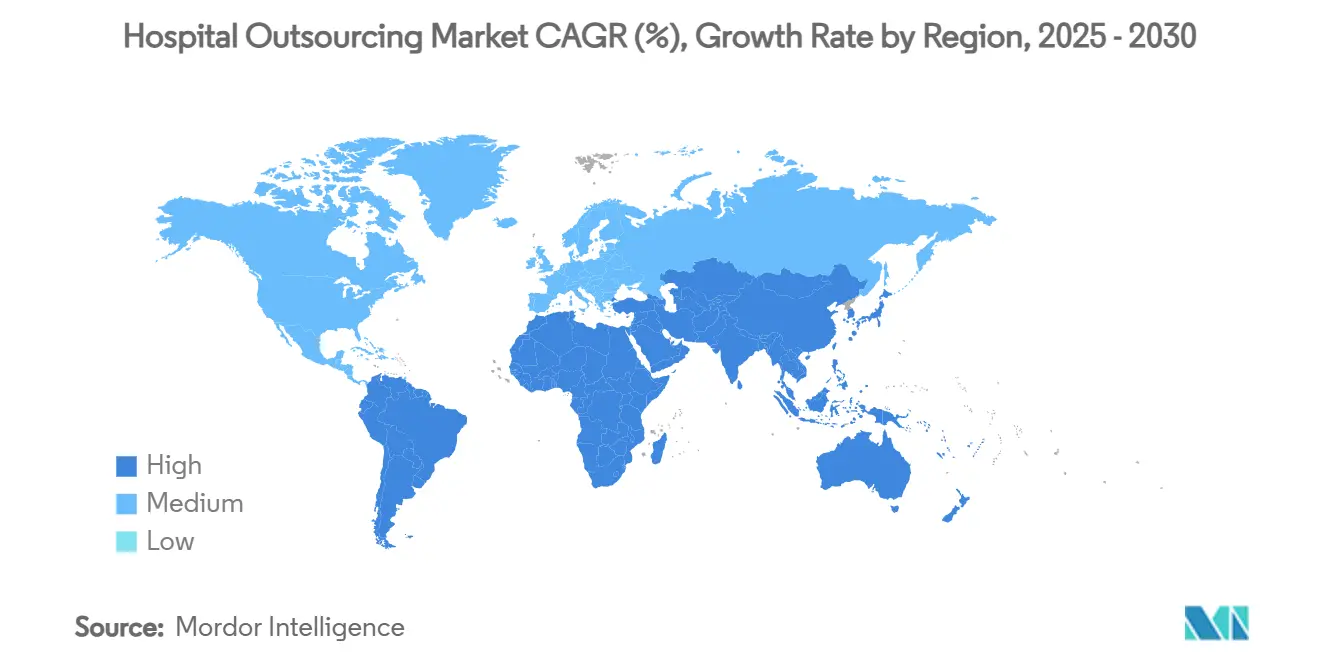

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Outsourcing Market Analysis by Mordor Intelligence

The hospital outsourcing market size stood at USD 424.73 billion in 2025 and is forecast to reach USD 658.22 billion by 2030, advancing at a 9.16% CAGR over the period. Rising operating pressures, global workforce shortages and expanding technology requirements are prompting hospitals to form deep, multi-year partnerships with external specialists. Information-technology (IT) contracts dominate current spend, yet clinical services outsourcing is scaling rapidly as health systems protect core competencies while ensuring access to scarce talent. Tight cybersecurity regulations, value-based-care incentives and artificial-intelligence (AI) automation are accelerating adoption, while inflation-driven wage increases and data-localization mandates temper near-term growth. Intensifying competition among diversified service groups and niche technology vendors is encouraging strategic acquisitions and cross-sector collaborations that embed digital tools directly into daily clinical and administrative workflows.

Key Report Takeaways

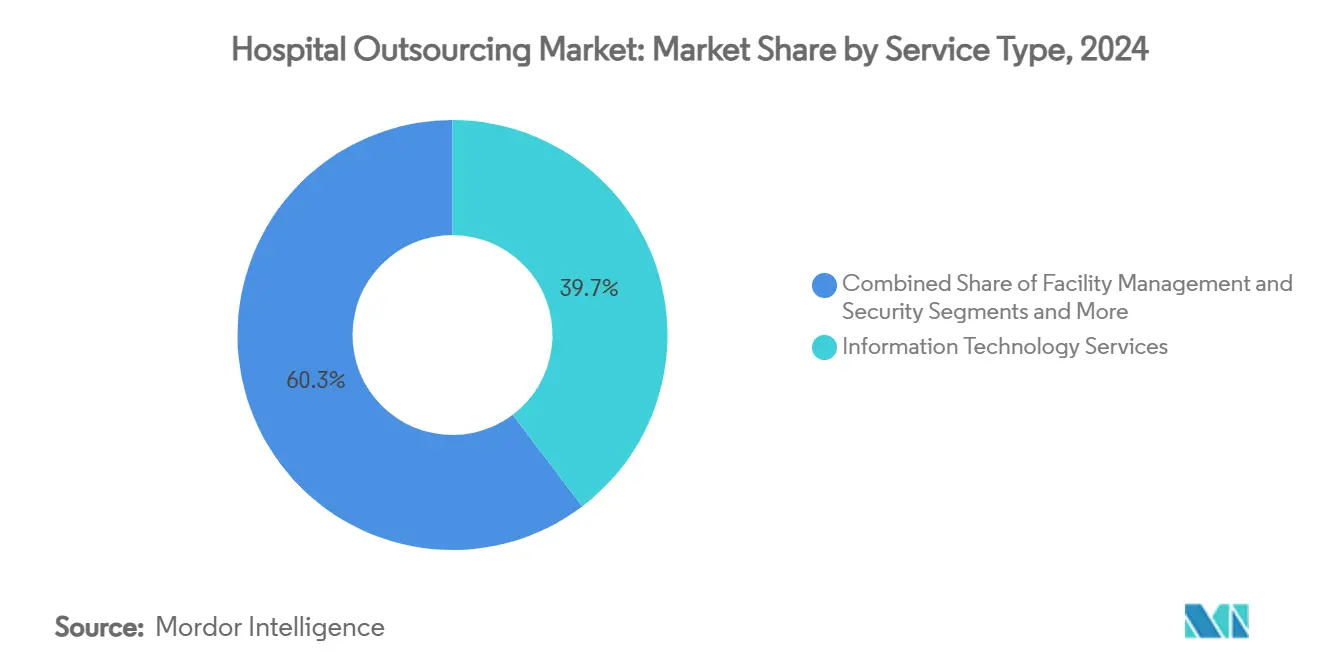

- By service type, IT services captured 39.69% of hospital outsourcing market share in 2024; clinical services are projected to expand at a 13.23% CAGR through 2030.

- By hospital size, large facilities with ≥300 beds held 67.84% of the hospital outsourcing market size in 2024 while small and medium hospitals are growing at a 12.68% CAGR to 2030.

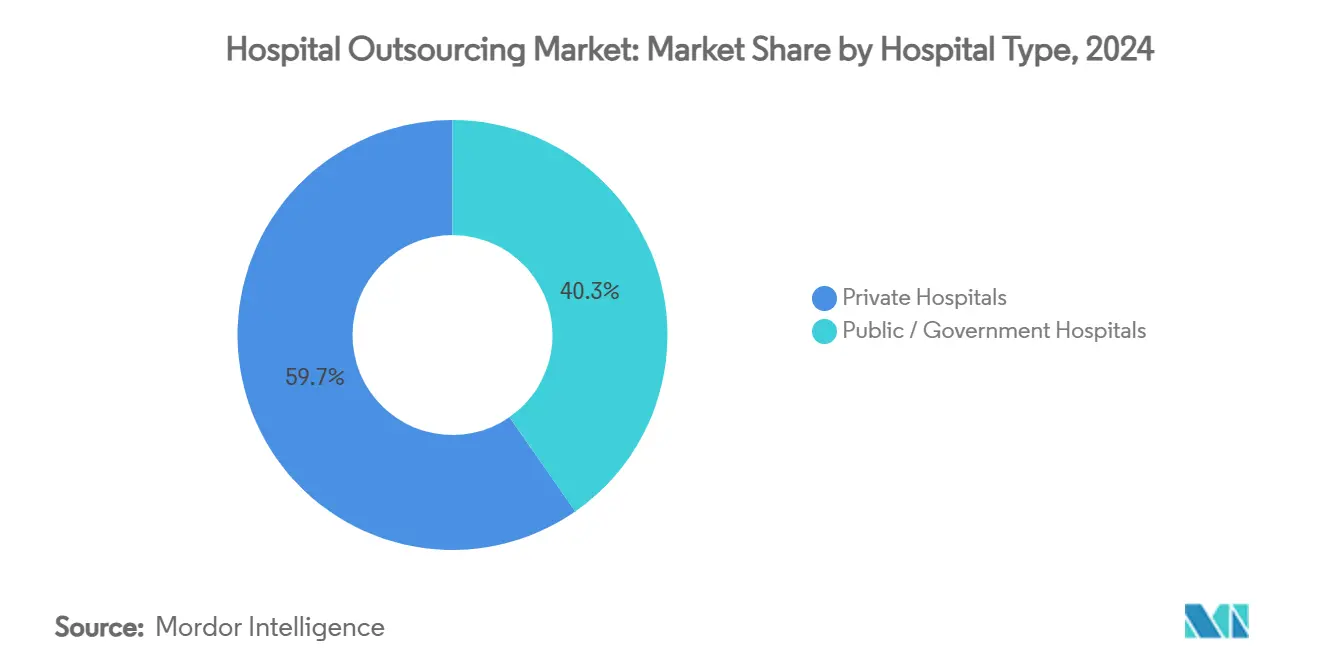

- By hospital type, private hospitals accounted for 59.67% of the hospital outsourcing market size in 2024; public and government hospitals are advancing at a 12.43% CAGR over the forecast horizon.

- By end-user, general medical and surgical hospitals commanded 53.34% share of the hospital outsourcing market size in 2024 and specialty hospitals are progressing at an 11.44% CAGR through 2030.

- By geography, North America led with 37.76% share of the hospital outsourcing market size in 2024, whereas Asia-Pacific is growing fastest at an 11.18% CAGR to 2030.

Global Hospital Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Staffing-shortage crisis amplifies demand for outsourced clinical staff | +2.5% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Escalating cyber-risk prompts managed security outsourcing | +1.8% | Global, concentrated in developed markets | Short term (≤2 years) |

| AI-enabled revenue-cycle automation delivers 15-20% cost savings | +2.1% | North America and European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Value-based-care incentives shift fixed overhead to variable BPO models | +1.4% | North America primary, European Union secondary | Long term (≥4 years) |

| ESG-linked facilities contracts gain premium pricing in OECD hospitals | +0.9% | OECD countries, emerging in Asia-Pacific | Long term (≥4 years) |

| Home-hospital programs boost third-party logistics and remote monitoring | +1.2% | North America and Europe, pilot programs in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Staffing-shortage crisis amplifies demand for outsourced clinical staff

A sustained global nursing and allied-health shortage is redefining workforce planning across the hospital outsourcing market. The American Nurses Association confirmed that 78% of hospitals reported gaps in critical care units during 2024, pushing administrators toward agency partnerships and worker-owned staffing cooperatives that guarantee continuity of care while cutting recruitment costs. Rural facilities are most exposed and increasingly outsource entire departments—such as respiratory therapy and imaging—to maintain licensure requirements. Multisite health systems are locking in long-term contracts that bundle recruitment, credentialing and training, allowing internal teams to focus on complex cases and value-based-care reporting.

Escalating cyber-risk prompts managed security outsourcing

Healthcare breaches surged in 2024, exposing 45 million patient records and highlighting the vulnerability of electronic health-record platforms. New U.S. HIPAA security rules effective 2025 apply uniform safeguards regardless of organization size, driving hospitals toward specialized managed-security-service providers that deliver 24/7 threat monitoring and compliance documentation. Large integrated delivery networks are negotiating outcome-based contracts pegged to mean-time-to-detect metrics, while mid-tier hospitals rely on shared-service security operations centers to spread costs.

AI-enabled revenue-cycle automation delivers 15-20% cost savings

Hospitals deploying AI bots for prior authorization, coding and denial management report 15-20% cost avoidance and near-perfect clean-claim rates. Banner Health and Auburn Community Hospital achieved materially faster payment cycles after outsourcing revenue-cycle tasks to AI-centric partners certified in major payer portals.[1]American Hospital Association Center for Health Innovation, “AI in Revenue-Cycle Management”, aha.org Private-equity interest remains high, exemplified by TowerBrook and CD&R’s USD 8.9 billion purchase of R1 RCM that funds further automation rollouts. As denial rates sit near 20% industry-wide, CFOs view AI-driven outsourcing as an essential liquidity lever.

Value-based-care incentives shift fixed overhead to variable BPO models

The migration from fee-for-service to value-based contracts in U.S. Medicare and commercial plans rewards hospitals that convert fixed costs into variable outsourcing agreements aligned with performance metrics. Business-process-outsourcing vendors now embed population-health nurses, analytics dashboards and remote-monitoring kits, billing only when clinical indicators improve. Early adopters among safety-net hospitals demonstrate stronger margins and higher quality scores, bolstering the perception of outsourcing as a strategic capability rather than expense pruning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin squeeze from inflationary service-provider wage hikes | -1.3% | Global, acute in developed markets | Short term (≤2 years) |

| Quality-of-care variability at multisite vendors triggers backlash | -0.8% | Global, concentrated in large health systems | Medium term (2-4 years) |

| Data-sovereignty laws restrict cross-border IT outsourcing | -1.1% | North America and European Union, expanding globally | Long term (≥4 years) |

| Rising unionization of hospital support staff hampers contract renewals | -0.6% | North America and European Union, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin squeeze from inflationary service-provider wage hikes

Nursing and technician salaries climbed 7.2% in 2024, forcing outsourcing firms to raise prices as collective-bargaining agreements reset compensation scales. Contract renewals negotiated before the inflation spike now deliver narrow margins, prompting vendors to seek cost-of-living escalators or risk contract exit. Hospitals meanwhile reassess make-or-buy decisions, occasionally insourcing dietary or environmental-services teams when external costs outpace internal benchmarks.

Quality-of-care variability at multisite vendors triggers backlash

Large vendors operating across hundreds of hospitals face scrutiny when sentinel events occur at a single site. Root-cause analyses reveal training inconsistencies and cultural misalignment that erode clinician trust. Health-system boards are instituting stricter key-performance-indicator (KPI) clauses, and some facilities pivot to regional providers that offer tailored oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IT leadership and accelerating clinical uptake

IT services retained the largest slice of the hospital outsourcing market in 2024, accounting for 39.69% of revenue as hospitals sought robust cybersecurity, electronic-health-record optimization and advanced analytics capabilities. The hospital outsourcing market size tied to IT contracts is projected to grow steadily as regulatory compliance and digital-transformation mandates intensify. Clinical services outsourcing is advancing at a 13.23% CAGR, driven by tele-intensive-care-unit hubs, laboratory consolidation and radiology teleresourcing that alleviate chronic staffing shortages. Facilities management and security remain stable contributors, underpinned by hygiene innovation such as UV-C disinfection robots that cut infection-control costs.[2]Sodexo Group, “Sodexo Partners with UVD Robots to Enhance Healthcare Hygiene”, sodexo.comRevenue-cycle and medical-billing services continue to attract AI-centric vendors delivering measurable denials reduction and faster cash cycles. Ancillary offerings—transport, linen, catering and marketing—provide incremental savings but carry lower strategic impact, leading many hospitals to bundle them into multi-service contracts for administrative simplicity.

Technology integration differentiates leading providers across every service line. Vendors embed predictive maintenance sensors in HVAC assets, deploy computer-vision tools for tray-audit accuracy and integrate claims-scrubbing algorithms that learn payer edits in real time. Hospitals prioritizing outcome-based contracts share data dashboards with vendors to align incentives and monitor performance on infection rates, readmissions and patient-satisfaction scores. As competitive intensity rises, smaller regional specialists focus on single-service excellence—for example, AI-powered pathology networks—while conglomerates assemble broad portfolios through mergers and partnerships that expand geographical reach.

By Hospital Size: Scale advantage and SME momentum

Large hospitals with at least 300 beds accounted for 67.84% of 2024 spending, leveraging their scale to negotiate enterprise-wide agreements that integrate multiple disciplines under shared governance models. These institutions deploy centralized command centers aggregating vendor performance metrics across campuses, unlocking network-wide efficiency gains. Because capital budgets remain constrained, large systems increasingly shift non-clinical upgrades—such as smart pharmacy robots—to vendor-financed models that minimize upfront outlay.

Small and medium hospitals under 300 beds generate the highest growth at 12.68% CAGR as they tap outsourcing to access clinical specialists and modern IT infrastructure without carrying full-time staff. The hospital outsourcing market share captured by this cohort is modest today, yet their rising adoption signals a democratization of sophisticated services beyond tertiary centers. Providers tailor offerings—fractional biomedical engineering, shared medical physicist pools and remote pharmacy verification—to fit lower patient volumes and rural coverage requirements. Cloud-based contract-management portals streamline oversight, allowing lean administrative teams to monitor service levels in real time and flag deviations for corrective action.

By Hospital Type: Private-sector leadership and public-sector catch-up

Private hospitals represented 59.67% of global revenue in 2024, reflecting their agility in procurement decision-making and focus on margin preservation through operational efficiency. They often pilot emerging technologies first, such as autonomous supply-chain robots or AI-driven chatbots for patient intake, and then scale system-wide upon proven return on investment. Strategic alliances with diagnostics giants enable outsourcing of entire laboratory operations, freeing capital for high-acuity service lines.

Public and government facilities record the fastest uptake at 12.43% CAGR as policymakers encourage public-private partnerships that reduce taxpayer burden while safeguarding care quality. National health services are rebidding legacy contracts with stringent key-performance thresholds, and some convert state-owned labs into joint ventures with specialist operators. Outsourcing of food, laundry and estate maintenance remains common, yet growing focus lies in digital patient-record hosting and command-center coordination for waiting-list management.

By End User: General hospitals dominate, specialties accelerate

General medical and surgical hospitals captured 53.34% of 2024 spend, owing to their broad service mix that requires extensive administrative, clinical and facilities support. Multispecialty academic centers embed integrated vendor teams that co-locate within departments to expedite issue resolution and foster continuous improvement cultures. Specialty hospitals—oncology, orthopedics, cardiovascular—are growing at an 11.44% CAGR, motivated by the need for highly skilled staff and cutting-edge technology calibrated to narrow clinical pathways. Outsourcing supports around-the-clock coverage for imaging, sterile processing and inventory management, enabling clinicians to concentrate on complex procedures.

Nursing homes and assisted-living centers increasingly rely on third-party clinical-pharmacy and tele-consultation networks as resident acuity rises. Clinics and outpatient centers embrace flexible cleaning, security and billing services aligned with extended operating hours. The hospital outsourcing industry accommodates these varied care settings by offering modular service bundles that scale with patient turnover and regulatory complexity.

Geography Analysis

North America retained 37.76% of global revenue in 2024, anchored by sophisticated health systems confronting rising labor costs and regulatory scrutiny. The region benefits from entrenched outsourcing cultures and mature vendor ecosystems able to meet stringent Health Insurance Portability and Accountability Act requirements. UnitedHealth Group’s Optum division deepened vertical capabilities through acquisitions, including the USD 8 billion Kelsey-Seybold deal, to provide integrated clinical and administrative services.[3]UnitedHealth Group Investor Relations, “Optum Strategy and Growth Update 2025”, unitedhealthgroup.comU.S. hospitals also lead adoption of AI-infused revenue-cycle tools, deploying machine-learning models that auto-code charts and flag denials pre-submission.

Asia-Pacific is the fastest-growing territory at an 11.18% CAGR, powered by hospital construction booms and liberalizing investment rules. India added over 50,000 new beds during 2024, prompting demand for outsourced diagnostic imaging, linen and security operations. Indonesia’s policy shift allowing up to 100% foreign ownership in private hospitals lowers entry barriers for global service companies seeking anchor clients. Rapid urbanization and the region’s aging population spur home-hospital pilot programs that depend on third-party logistics and remote-monitoring vendors.

Europe shows steady expansion as cross-border regulatory harmonization gains traction. Germany’s switch to service-based reimbursement disrupts historic revenue streams, incentivizing hospitals to partner with outsourcing firms that can deliver cost transparency and accountability. The EU AI Act classifies most clinical-decision support tools as high risk, creating a compliance services niche for consultancies embedded inside vendor contracts. Sustainability directives and carbon-reduction targets further propel uptake of ESG-linked facilities-management solutions.

South America and the Middle East & Africa contribute smaller shares yet demonstrate rising interest as governments invest in healthcare infrastructure and encourage public-private collaboration. Multinational vendors establish regional hubs to localize services and comply with emerging data-localization laws. Demonstration projects in Saudi Arabia’s giga-cities and Brazil’s oncology centers illustrate the breadth of opportunity for technology-enabled outsourcing partners.

Competitive Landscape

The hospital outsourcing market is moderately fragmented, with a cohort of global conglomerates and a long tail of regional specialists. Sodexo, Aramark and Compass Group leverage integrated portfolios covering food, cleaning, security and facilities maintenance. Each boosted fiscal-year 2024 revenue by investing in automation, robotics and data analytics platforms, and industry speculation persists around potential consolidation deals that could reshape scale economics.

UnitedHealth Group’s Optum unit embodies convergence between payer, provider and services domains, employing acquisitions of physician groups and revenue-cycle organizations to offer end-to-end solutions spanning clinic operations to claim adjudication. Oracle Health collaborates with health systems and technology firms to embed AI governance frameworks within electronic health records, underscoring a trend toward platformization wherein software, hardware and domain expertise converge in single vendor relationships.

Niche players achieve differentiation through depth rather than breadth. Jorie Healthcare Partners focuses on AI-enabled claims optimization, while tele-ICU firms deploy intensivist oversight across rural facilities, monetizing outcome improvements. Diagnostic giants Quest Diagnostics and Fresenius Medical Care embed acquisition strategies that integrate hospital labs and dialysis centers into wider service networks, reinforcing their influence over test-utilization guidance and supply chains. Private-equity investors fuel expansion through buy-and-build roll-ups, particularly in revenue-cycle management and specialty staffing. Contract structures increasingly tie fees to jointly defined key-result indicators—infection-rate reduction, denial-rate improvement—that align vendor incentives with hospital quality metrics.

Barriers to entry include credentialing requirements, cyber-risk insurance costs and escalating demand for measurable ESG performance. Vendors that demonstrably enhance patient-safety indicators and meet strict data-security certifications secure multi-year renewals and preferred-supplier status within purchasing coalitions. As hospitals mesh clinical excellence with operational efficiency, the relative bargaining power of service partners rises, but so too does accountability for outcome delivery.

Hospital Outsourcing Industry Leaders

UnitedHealth Group

ISS World Services A/S

Compass Group PLC (Medirest)

Aramark Healthcare+

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Simplify Healthcare partnered with Atento to pilot a customer-experience program for U.S. payers, deploying the Xperience1 platform to improve member and provider engagement.

- March 2025: TC BioPharm initiated a decentralization strategy, outsourcing several corporate functions and reducing headcount to enhance agility.

- August 2024: R1 RCM closed its USD 8.9 billion buy-out by TowerBrook Capital Partners and Clayton, Dubilier & Rice, unlocking funding for automation and analytics expansion

Global Hospital Outsourcing Market Report Scope

| Information Technology Services |

| Facility Management & Security |

| Clinical Services (e.g., Laboratory, Radiology, Tele-ICU) |

| Revenue-Cycle / Medical Billing Services |

| Business & Administration Services |

| Others (Transport, Laundry, Catering, Marketing) |

| Large Hospitals (≥300 beds) |

| Small & Medium Hospitals (<300 beds) |

| Private Hospitals |

| Public / Government Hospitals |

| General Medical & Surgical Hospitals |

| Specialty Hospitals |

| Nursing Homes & Assisted-Living Facilities |

| Clinics & Outpatient Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Information Technology Services | |

| Facility Management & Security | ||

| Clinical Services (e.g., Laboratory, Radiology, Tele-ICU) | ||

| Revenue-Cycle / Medical Billing Services | ||

| Business & Administration Services | ||

| Others (Transport, Laundry, Catering, Marketing) | ||

| By Hospital Size | Large Hospitals (≥300 beds) | |

| Small & Medium Hospitals (<300 beds) | ||

| By Hospital Type | Private Hospitals | |

| Public / Government Hospitals | ||

| By End User | General Medical & Surgical Hospitals | |

| Specialty Hospitals | ||

| Nursing Homes & Assisted-Living Facilities | ||

| Clinics & Outpatient Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the hospital outsourcing market?

The hospital outsourcing market size reached USD 424.73 billion in 2025 and is projected to grow to USD 658.22 billion by 2030.

2. Which service line commands the largest spending share?

Information-technology outsourcing accounts for 39.69% of total revenue, reflecting hospitals’ focus on cybersecurity and digital transformation.

3. Which region is expanding fastest?

Asia-Pacific leads growth with an 11.18% CAGR through 2030, propelled by hospital construction, policy liberalization and an aging population.

4. Why are hospitals outsourcing clinical services?

Persistent staffing shortages and the need for specialized expertise make outsourcing a practical path to maintain care quality and regulatory compliance.

5. How does AI influence outsourcing decisions?

AI-enabled revenue-cycle platforms reduce billing costs by up to 20% and improve clean-claim rates, prompting hospitals to favor partners that embed advanced automation.

Page last updated on: