Outpatient Oncology Infusion Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

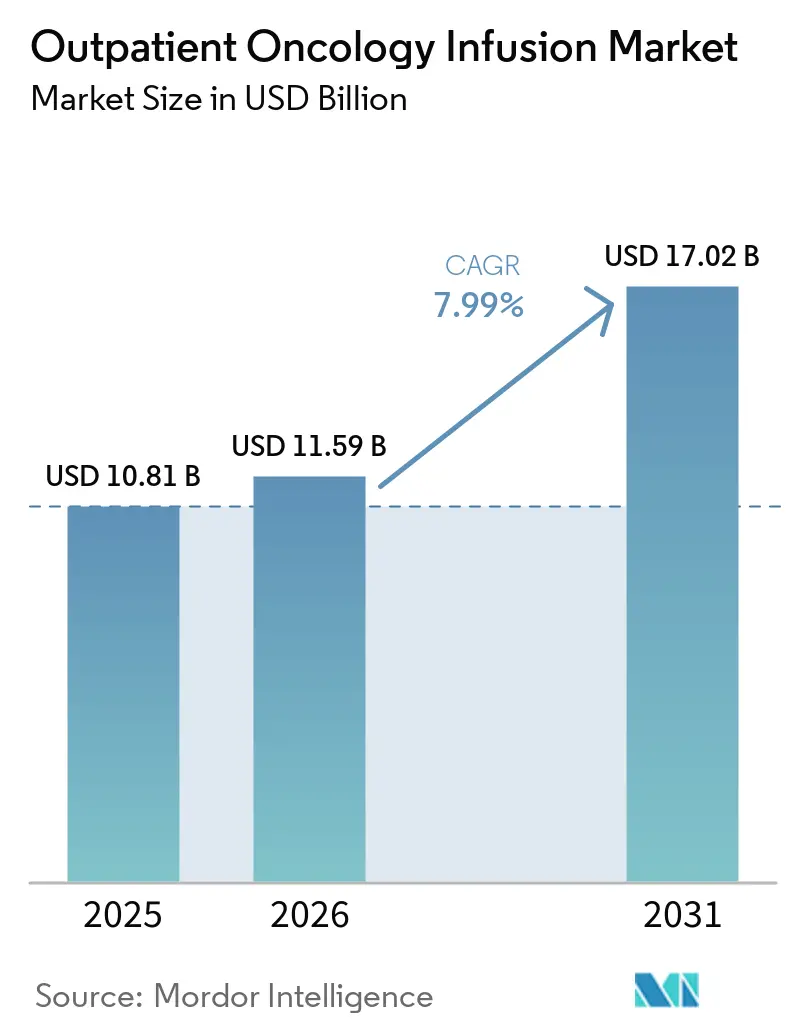

| Market Size (2026) | USD 11.59 Billion |

| Market Size (2031) | USD 17.02 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outpatient Oncology Infusion Market Analysis by Mordor Intelligence

The Outpatient Oncology Infusion Market size is expected to grow from USD 10.81 billion in 2025 to USD 11.59 billion in 2026 and is forecast to reach USD 17.02 billion by 2031 at 7.99% CAGR over 2026-2031.

Growth in the outpatient oncology infusion market is being shaped by the migration of complex drug administration away from inpatient wards toward lower-cost ambulatory and hospital outpatient departments, a shift reinforced by site-neutral payment policies and value-oriented contracting. New antibody-drug conjugates and broader immuno-oncology use are expanding infusion volumes while lengthening chair times due to observation and premedication needs, which increases operational complexity for providers. Payers and provider networks are aligning on pathway adherence and prior authorization reform that smooths regimen delivery and reduces administrative delays, which supports steady outpatient throughput. Infusion centers are adopting predictive scheduling and advanced capacity tools to raise chair utilization and shorten wait times without large capital outlays, which helps sustain access as reimbursement tightens. Margin compression from site-neutral rules and persistent staffing gaps remain near-term constraints, which make operational efficiency and targeted investment central to competitiveness in the outpatient oncology infusion market.

Key Report Takeaways

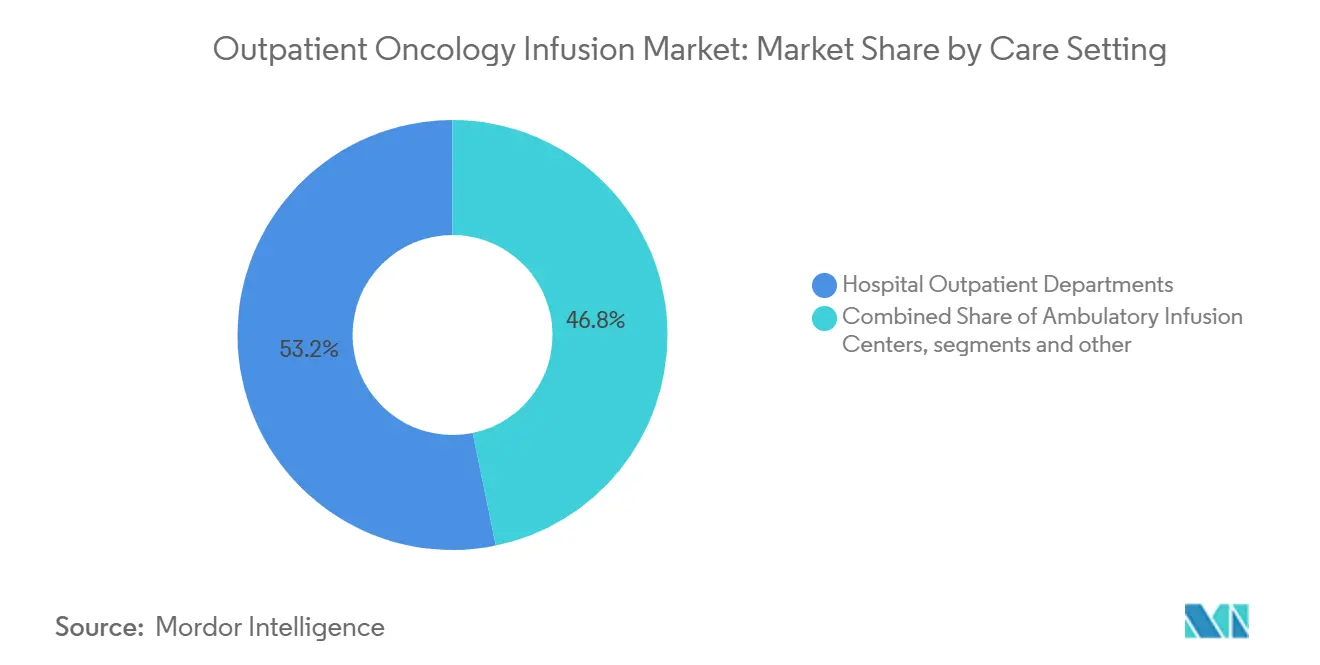

- By care setting, hospital outpatient departments led with 53.23% revenue share in 2025, while standalone ambulatory infusion centers are forecast to expand at a 9.01% CAGR to 2031.

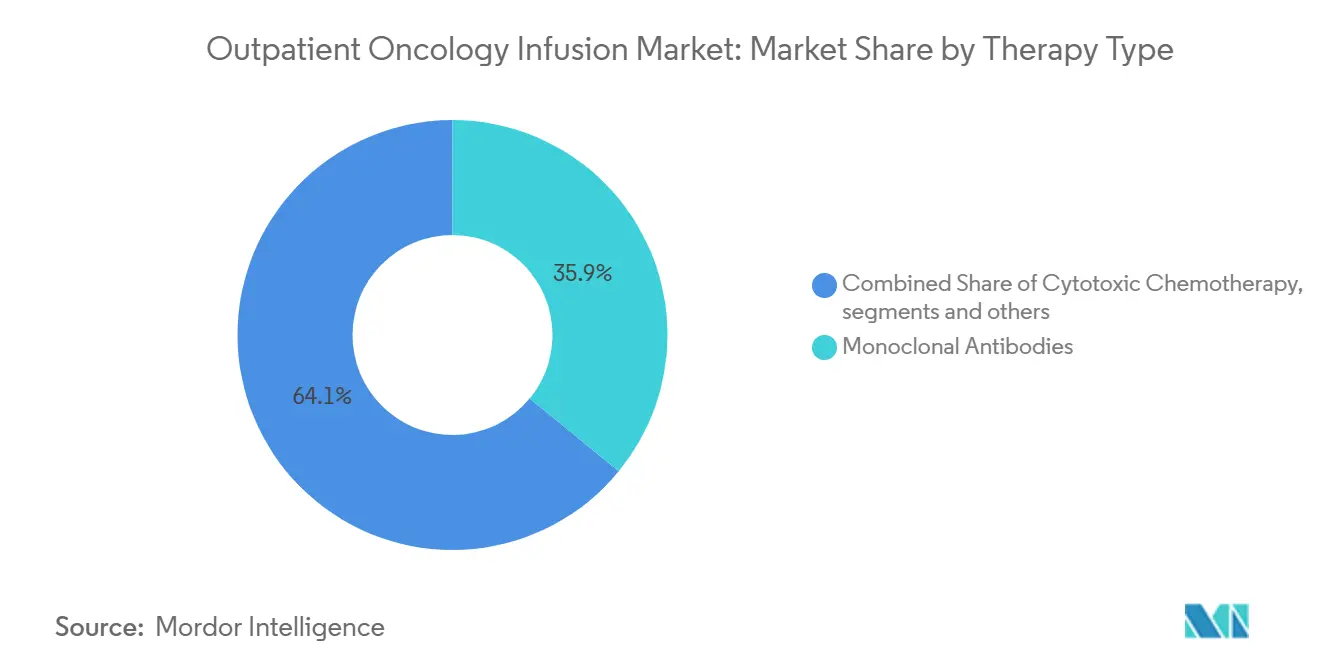

- By therapy type, monoclonal antibodies held 35.93% share in 2025, and antibody-drug conjugates are projected to advance at an 8.65% CAGR to 2031.

- By tumor type, breast cancer accounted for 21.34% of 2025 volumes, and lung cancer is projected to grow at a 10.45% CAGR through 2031.

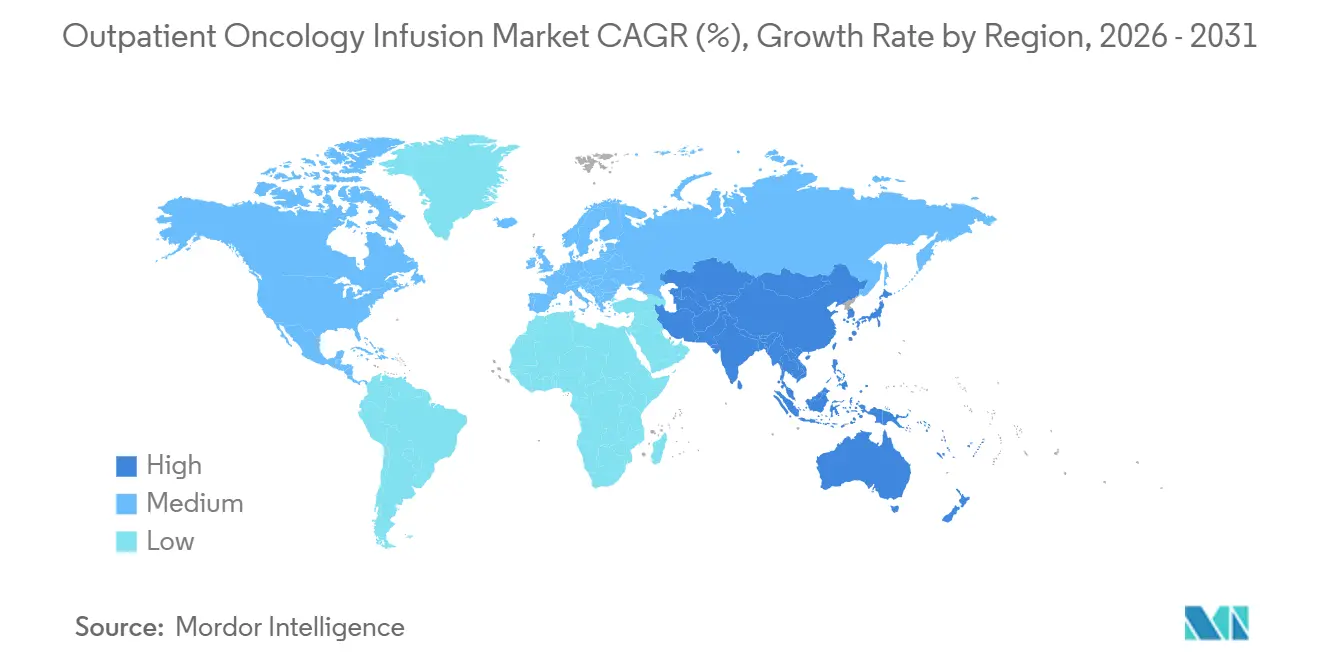

- By geography, North America held 43.24% share in 2025, and Asia-Pacific is set to grow at a 9.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Outpatient Oncology Infusion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of infusion-based immunotherapies and biologics | +2.8% | Global, with higher penetration in North America and Western Europe | Medium term (2-4 years) |

| Shift to outpatient and ambulatory settings for cost, access and patient experience | +2.1% | Global, accelerating in North America due to CMS site-neutral policies | Short term (≤ 2 years) |

| Rising cancer incidence and survivorship expanding outpatient infusion volumes | +1.5% | Global, with fastest growth in Asia-Pacific (China, India, Indonesia) | Long term (≥ 4 years) |

| Payer and policy incentives for site-of-care optimization and value-based oncology | +1.3% | Primarily North America and select European markets | Medium term (2-4 years) |

| Throughput technologies (AI scheduling, pharmacy automation) expanding capacity | +0.9% | North America, Western Europe, emerging in Australia and urban Asia-Pacific | Medium term (2-4 years) |

| Biosimilar adoption lowering acquisition costs and broadening access | +0.4% | North America, Europe, limited adoption in 340B-eligible U.S. hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Infusion-Based Immunotherapies and Biologics

Regulatory momentum behind antibody-drug conjugates has reshaped infusion demand by adding indications that require scheduled intravenous cycles, bundled premedication, and post-infusion monitoring, which raises average chair-time per visit. The approval path for datopotamab deruxtecan in breast cancer and subsequent expansion into lung cancer reinforces this trend as providers operationalize ADC-specific protocols that differ from legacy cytotoxic regimens. In 2026, ifinatamab deruxtecan received Priority Review for extensive-stage small cell lung cancer, signaling additional high-intensity infusion volumes if approved, and adding complexity through monitoring of immune-related toxicities[1]Merck & Co., “Ifinatamab Deruxtecan Granted Priority Review in the U.S.,” Merck, merck.com. Growth in the outpatient oncology infusion market is therefore being supported both by new agent approvals and by extended infusion administration and observation windows linked to immunotherapies. These dynamics reward centers that standardize premedication pathways and adverse event surveillance while sustaining patient experience. They also heighten the need for scalable scheduling models that accommodate longer chair occupancy without increasing cancellations or wait times.

Shift to Outpatient and Ambulatory Settings for Cost, Access, and Patient Experience

CMS finalized a site-neutral payment step that sets a significant share of the hospital outpatient rate for drug administration in excepted off-campus provider-based departments, which reduces reimbursement for services that had migrated to these locations after prior policy changes. This rule change increases incentives to deliver appropriate chemotherapy and biologic infusions in ambulatory or physician-aligned sites that offer lower total costs, shorter patient travel times, and streamlined scheduling. As the outpatient oncology infusion market adapts in 2026, providers that operate multiple sites are aligning service mix by acuity and resource intensity to protect margins and sustain access. Patients and referring clinicians favor locations that balance safety, timely starts, and consistent care teams, which has aided community-site growth for maintenance therapies and routine biologics. The result is a gradual redistribution of volume toward centers that offer predictable experience, transparent cost structures, and pathway-adherent regimens backed by payer alignment.

Payer and Policy Incentives for Site-of-Care Optimization and Value-Based Oncology

Commercial and risk-bearing networks are rolling out pathway adherence and prior authorization reforms that reduce administrative latency for evidence-based regimens. The American Oncology Network and Evolent Health partnership established a gold-carding mechanism that removes prior authorization for providers who adhere to high-quality pathways, which simplifies regimen starts and reduces re-reviews when plans are adjusted. These efforts complement Medicare’s site-neutral push and sustained quality reporting, aligning cost containment with clinically validated care delivery steps that fit the outpatient oncology infusion market. As gold-carding spreads, payers can free capacity by removing back-office friction, while providers benefit from predictable claim cycles that sustain investment in staffing and technology. The shared objective is steadier access for patients and reliable margins for centers that meet pathway standards. This alignment has begun to reduce the variance in start times and denials that previously added operational risk to infusion scheduling and pharmacy compounding.

Throughput Technologies (AI scheduling, pharmacy automation) Expand Capacity

Predictive scheduling and optimization tools have delivered measurable gains in chair utilization, wait times, and staff workload at leading centers. Northwestern Medicine used an AI-enabled scheduling platform to adjust templates and load-balance demand, which increased monthly patient throughput and cut wait times without adding physical capacity. Fred Hutchinson Cancer Center reported multi-hour daily savings in nurse assignment scheduling and large reductions in waitlists by applying similar analytics to queue management and nurse workload levelling. These optimizations support a larger share of same-day add-ons and minimize midday bottlenecks, which increases on-time starts and predictability for patients and staff. As reimbursement tightens, software-driven efficiency becomes a first-line lever to preserve access within existing square footage and staffing models. The outpatient oncology infusion market is seeing wider adoption of these tools as leaders codify change management playbooks and share operational benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology nurse and pharmacist shortages constraining throughput and expansion | -2.3% | Global, most acute in rural North America and select European regions | Short term (≤ 2 years) |

| Reimbursement pressure (site-neutral, 340B recoupment) compressing margins | -1.8% | Primarily United States, emerging in value-based European markets | Medium term (2-4 years) |

| Oncology drug shortages disrupting scheduling and regimen delivery | -0.7% | Global, episodic spikes in North America and Europe | Short term (≤ 2 years) |

| Shift to subcutaneous and at-home supportive care reducing chair-time revenue | -0.5% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Pressure (site‑neutral, 340B remedy) Compresses Margins

Site-neutral policies now pay significantly of the hospital outpatient rate for drug administration in excepted off-campus departments, which directly reduces reimbursement in locations that captured growing shares of infusion services in prior years. CMS has also implemented a multi-year 340B-related recoupment adjustment to the non-drug OPPS update, which further tightens hospital budgets and raises the bar for capital commitments to infusion chairs and pharmacies. Provider associations have flagged that uniform site-neutral rates do not fully account for the standby capacity and intensive staffing needed to support complex oncology infusions, especially for sicker populations served by academic and safety-net systems. The combined effect is more selective expansion, closer alignment of service mix by acuity, and faster adoption of scheduling and pharmacy workflows that minimize waste. In the outpatient oncology infusion market, these pressures reward centers with strong operational discipline and payer alignment that can sustain high on-time starts and predictable costs. Over the medium term, the policy environment is expected to drive more volume into cost-efficient sites and curb the growth of higher-cost locations.

Oncology Drug Shortages Disrupt Scheduling and Regimen Delivery

Infusion centers require nurses with specialized training in biologic and chemotherapy administration, hypersensitivity management, and recognition of immune-related adverse events, and recruitment for these roles has remained challenging in many markets. Pharmacists and technicians with sterile compounding and hazardous drug handling expertise are also in short supply across systems that continue to expand outpatient infusion footprints. Staffing tightness is most acute in rural areas and in centers that manage higher-acuity regimens requiring longer chair times and closer monitoring. These constraints affect throughput, increase reliance on overtime, and can limit the pace of new chair additions even when demand is strong. In 2026, providers are responding with greater focus on workload leveling, cross-training, and technology that trims administrative time so clinicians can spend more effort on direct patient care. The outpatient oncology infusion market is adjusting by sequencing expansions toward sites that can be staffed at consistent quality with predictable costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Care Setting: Hospital Departments Retain Share, Yet Ambulatory Centers Capture Margin-Conscious Growth

Hospital outpatient departments accounted for 53.23% of the outpatient oncology infusion market in 2025, underpinned by integrated diagnostics, surgical coordination, and the governance required for complex biologics and cellular therapies, while standalone ambulatory infusion centers are projected to grow at a 9.01% CAGR through 2031 as payer site-neutral policies favor lower-cost settings. This volume split reflects the ability of hospital sites to manage higher acuity and clinical trial workflows, while ambulatory centers focus on maintenance regimens and pathway-adherent biologics that fit predictable scheduling blocks. The outpatient oncology infusion market is reorganizing around this mix as health systems align service lines by acuity and standardize case selection to sustain quality and margin. Payer policy has reinforced the trend by setting lower payment levels for drug administration in certain off-campus departments, which redirects volume to settings with lean overhead and strong throughput.

Patient experience preferences also matter, since community sites often offer shorter travel, faster starts, and consistent nursing teams. Hospital-based departments remain critical for rapid escalation of care, adverse event management, and access to multidisciplinary expertise within the same campus. In 2026, the balance is not a zero-sum shift but a targeted reallocation of appropriate cases toward centers that combine safety with lower all-in costs. Providers that operate across both settings are adopting centralized triage and scheduling models to place each regimen in the right site.

Over the forecast period, hospital outpatient departments are expected to retain complex protocols such as cellular therapies and infusions requiring frequent lab-based dose adjustments, where co-located pharmacy, emergency capability, and subspecialty consults are important. Ambulatory infusion centers are expected to outgrow the broader outpatient oncology infusion market on the strength of standardized regimens and efficient chair turnover that underpin payer-aligned cost advantages.

The outpatient oncology infusion market size will reflect this mix shift as centers refine premedication pathways, adopt predictive scheduling to level midday peaks, and closely manage infusion observation windows for biologics. Policy steps that lower payments for selected off-campus hospital-based services intensify the focus on cost per infusion start and on-time performance. Accreditation standards and quality programs remain important differentiators for hospital-affiliated centers that manage higher-risk therapy. Network players that combine hospital and community footprints are prioritizing data-driven scheduling, consistent staffing, and patient support services to protect their share in the outpatient oncology infusion market.

By Therapy Type: ADC Surge Reshapes Mix as Biosimilars Broaden Choice

Monoclonal antibodies led the therapy mix with 35.93% share in 2025, supported by checkpoint inhibitors, HER2-targeted agents, and VEGF inhibitors, while antibody-drug conjugates are projected to grow at 8.65% to 2031 as a series of new indications move into routine care. Datopotamab deruxtecan’s recent progress in solid tumors illustrates the operational impact, as infusion teams implement observation protocols and premedication that differ from historic cytotoxic infusions.

Ifinatamab deruxtecan’s Priority Review for previously treated extensive-stage small cell lung cancer adds to the ADC pipeline that could expand infusion demand and chair time in 2026 if approved. The outpatient oncology infusion market will reflect these therapy shifts through scheduling templates that account for longer chair occupancy and standardized toxicity monitoring. Centers are refining pharmacy and nursing workflows to align premix timing, chair availability, and documentation standards. Supportive care biologics contribute steady volumes yet face incremental substitution by subcutaneous formulations that limit chair hours and favor home settings for select indications.

Across 2026-2031, therapy mix evolution will be characterized by sustained monoclonal antibody usage, growing ADC adoption, and targeted biosimilar entry that widens choice in established categories. The outpatient oncology infusion market size for monoclonal antibodies remains substantial, but the highest growth comes from ADC pipelines that extend into new lines of therapy and tumor types.

Biosimilar competition advanced with the FDA approval of bevacizumab-nwgd (Jobevne), which expands lower-cost options for several solid tumors and may support access gains in settings aligned with pathway protocols[2]American Association for Cancer Research, “First Approval for New Antibody-Drug Conjugate in Breast Cancer,” American Association for Cancer Research, aacr.org. Operational readiness for ADCs will remain a differentiator as infusion centers tune chair-time assumptions, staffing, and observation windows for these agents. Providers that institutionalize ADC playbooks with clear premedication and escalation guidance can limit cancellations and optimize capacity. These therapy trends reinforce the need for predictive scheduling and close coordination between clinic, pharmacy, and nursing to keep on-time starts steady as complexity rises.

By Tumor Type: Breast Cancer Volumes Meet Lung Cancer’s Acceleration

Breast cancer accounted for 21.34% of outpatient infusion volumes in 2025, sustained by mature HER2-directed care pathways and a wider range of targeted therapies that require ongoing administration and toxicity monitoring. These pathways support predictable scheduling patterns and standardized premedication across neoadjuvant and adjuvant settings, which helps stabilize chair utilization across cycles. The outpatient oncology infusion market share for breast cancer reflects entrenched infrastructure that can scale new antibody-drug conjugate protocols as indications broaden. Growth in this segment also benefits from pathway alignment that smooths payer approvals when regimens follow guideline-backed sequences. Infusion centers with robust nurse education on targeted agents and hypersensitivity management can maintain on-time performance across complex breast cancer protocols. As therapy options expand, consistent patient education and toxicity triage will remain central to maintaining adherence and care continuity.

Lung cancer is projected to grow at a 10.45% CAGR through 2031, which adds pressure on infusion capacity as more regimens shift to outpatient delivery and as therapy lines expand. Operational readiness for lung protocols emphasizes careful scheduling of pre-infusion labs, imaging-based response checks, and observation for toxicity profiles typical of newer biologic combinations. Hospital-affiliated centers remain essential for escalations and acute interventions, while community sites handle protocol-stable maintenance regimens. Cellular therapy and transplant-adjacent services also influence regional capacity, with health systems adding specialized bays to manage advanced programs where regulatory and clinical oversight must be co-located. The outpatient oncology infusion market is expected to maintain a diversified tumor mix, with colorectal, hematologic, and genitourinary cancers contributing steady volumes under pathway-based regimens. Scheduling discipline and efficient pharmacy compounding remain critical to match chair-time assumptions to real-world duration distributions across tumor types.

Geography Analysis

North America held 43.24% of the outpatient oncology infusion market in 2025, supported by mature oncology networks, broad availability of advanced biologics, and payer contracts that enable pathway-aligned operations at scale. The policy environment in 2026 reinforces cost discipline through site-neutral payment steps and ongoing quality reporting, which have encouraged service mix optimization and broader adoption of predictive scheduling. Providers that deploy multi-site models balance hospital-based oversight for complex regimens with community site access for maintenance therapies. Ongoing accreditation, compliance, and staff education remain table stakes for leaders serving higher-acuity patients. As payers press for value, providers that align pathway adherence with streamlined prior authorization benefit from more predictable starts and fewer re-reviews. The outpatient oncology infusion market in North America is therefore characterized by steady access combined with disciplined cost management and technology-enabled throughput.

Asia-Pacific is projected to grow at a 9.13% CAGR through 2031, reflecting investment in capacity expansion across large urban centers and regional hubs. Private and public providers continue to build oncology services that improve access to infusion care within expanding hospital systems. As payers and ministries of health invest in broader oncology infrastructure, infusion centers are focusing on standard operating procedures and pharmacist training to ensure safe, reliable administration of complex biologics. Over the forecast period, adoption of scheduling analytics and dose preparation standards is expected to rise, particularly in urban markets with growing biologic use. This creates opportunities for cross-center standardization that supports scale and clinical governance. The outpatient oncology infusion market will reflect these investments through more predictable patient flow and modernization of pharmacy compounding across major cities.

In other regions, providers are moving at different speeds depending on funding, workforce availability, and local disease burden. Europe continues to balance national payment frameworks with the need for specialty capacity that can manage complex regimens in a decentralized fashion. Middle East and Africa markets are gradually adding infusion sites within broader oncology programs, often anchored by tertiary hospitals that centralize advanced protocols. Latin America maintains demand for infusion services, shaped by local payer mix and variable access to recent biologic launches. Across regions, scalability of training, quality monitoring, and scheduling tools remains central to raising productivity and patient experience. The outpatient oncology infusion market continues to favor operators that pair clinical governance with accessible community footprints.

Competitive Landscape

The outpatient oncology infusion market shows moderate fragmentation at the national level with regional concentration where health systems and network operators have scaled multi-site delivery. Integrated community oncology networks are investing in pathway adherence and authorization reform that supports faster regimen initiation. A prominent example is the American Oncology Network partnership with Evolent Health, which uses analytics and gold-carding to remove prior authorization for pathway-adherent providers, reducing friction and promoting consistent regimen delivery. Operational leaders are also prioritizing predictive scheduling tools that balance daily demand, limit midday bottlenecks, and protect on-time starts. Northwestern Medicine reported measurable gains from template optimization and queue management, while Fred Hutchinson Cancer Center achieved multi-hour daily scheduling savings and large reductions in waitlists using similar approaches. These capabilities differentiate providers on access and predictability.

Health systems with academic and tertiary capabilities continue to invest in specialized infusion and adjacent services that require concentrated expertise and licensing. A 2025 expansion at a major U.S. cancer institute added infusion bays to support transplant and advanced therapies, reinforcing the role of hospital-affiliated sites in managing higher-risk regimens that demand close monitoring and rapid escalation pathways. On the manufacturer side, the innovation cadence in antibody-drug conjugates and targeted biologics continues to create new infusion protocols and observation needs that ripple through provider operations. The Priority Review for ifinatamab deruxtecan in small cell lung cancer highlights the near-term potential for regimen additions that add to chair-time and nursing requirements. Biosimilar entrants such as bevacizumab-nwgd (Jobevne) broaden options in established tumor types and support pathway adherence where payers and providers are aligned.

Policy continues to shape competitive positioning by compressing reimbursement in selected hospital-based off-campus sites and by tightening adjustments related to 340B payment history. Associations representing cancer centers have raised concerns about uniform site-neutral rates for complex oncology, which underscores strategic moves to allocate regimens by acuity across hospital and ambulatory footprints. In this environment, the outpatient oncology infusion market rewards scale economies that support data-driven scheduling, consistent staffing, and playbooks for ADC and immunotherapy management. Providers that blend centralized governance with distributed access can defend share across urban and suburban catchments. Over 2026-2031, technology adoption, payer alignment, and clinical protocol standardization will remain the most important levers for leaders to sustain growth and service quality.

Outpatient Oncology Infusion Industry Leaders

American Oncology Network (AON)

Apollo Cancer Centers

HCA Healthcare / Sarah Cannon Cancer Institute

Ramsay Health Care (Australia)

The US Oncology Network (McKesson)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Merck and Daiichi Sankyo’s ifinatamab deruxtecan received FDA Priority Review with an October 2026 PDUFA date for adults with previously treated extensive-stage small cell lung cancer who progressed on or after platinum-based chemotherapy, following Phase 2 results that showed a survival benefit versus chemotherapy.

- November 2025: Evolent Health and the American Oncology Network launched a model that uses real-time EHR data to identify pathway-adherent care and gold-card providers, removing most prior authorization requirements to accelerate treatment starts and reduce administrative burden.

- April 2025: The FDA approved bevacizumab-nwgd (Jobevne), a biosimilar referencing Avastin, across multiple indications including colorectal, non-small cell lung, glioblastoma, renal cell carcinoma, cervical, ovarian, fallopian tube, and primary peritoneal cancers, expanding biosimilar choice for infusion centers.

Global Outpatient Oncology Infusion Market Report Scope

As per the report’s scope, outpatient oncology infusion involves the delivery of cancer-fighting therapies—such as chemotherapy, immunotherapy, or targeted treatments—along with blood products and supportive fluids, administered intravenously in a clinical setting. This model of care facilitates same-day discharge, eliminating the need for overnight hospitalization. The outpatient oncology infusion is segmented into care setting, therapy type, tumor type, and geography.

By care setting, the market is segmented into hospital outpatient departments, physician office/community oncology, and ambulatory infusion centers. By therapy type, the market is segmented into cytotoxic chemotherapy, monoclonal antibodies, checkpoint inhibitors (PD‑1/PD‑L1, CTLA‑4), antibody‑drug conjugates (ADCs), and supportive care biologics and agents (e.g., G‑CSF, IVIG, iron). By tumor type, the market is segmented into breast cancer, lung cancer, colorectal cancer, prostate cancer, hematologic malignancies (e.g., lymphoma, leukemia, myeloma), gynecologic cancers, melanoma, head & neck cancers, gastric & esophageal cancers, liver & pancreatobiliary cancers, bladder cancer, and renal cell carcinoma. By geography, the market is segmented as North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Hospital Outpatient Departments |

| Physician Office / Community Oncology |

| Ambulatory Infusion Centers |

| Cytotoxic Chemotherapy |

| Monoclonal Antibodies |

| Checkpoint Inhibitors (PD‑1/PD‑L1, CTLA‑4) |

| Antibody‑Drug Conjugates (ADCs) |

| Supportive Care Biologics and Agents (e.g., G‑CSF, IVIG, iron) |

| Breast Cancer |

| Lung Cancer |

| Colorectal Cancer |

| Prostate Cancer |

| Hematologic Malignancies (e.g., lymphoma, leukemia, myeloma) |

| Gynecologic Cancers |

| Melanoma |

| Head & Neck Cancers |

| Gastric & Esophageal Cancers |

| Liver & Pancreatobiliary Cancers |

| Bladder Cancer |

| Renal Cell Carcinoma |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Care Setting | Hospital Outpatient Departments | |

| Physician Office / Community Oncology | ||

| Ambulatory Infusion Centers | ||

| By Therapy Type | Cytotoxic Chemotherapy | |

| Monoclonal Antibodies | ||

| Checkpoint Inhibitors (PD‑1/PD‑L1, CTLA‑4) | ||

| Antibody‑Drug Conjugates (ADCs) | ||

| Supportive Care Biologics and Agents (e.g., G‑CSF, IVIG, iron) | ||

| By Tumor Type | Breast Cancer | |

| Lung Cancer | ||

| Colorectal Cancer | ||

| Prostate Cancer | ||

| Hematologic Malignancies (e.g., lymphoma, leukemia, myeloma) | ||

| Gynecologic Cancers | ||

| Melanoma | ||

| Head & Neck Cancers | ||

| Gastric & Esophageal Cancers | ||

| Liver & Pancreatobiliary Cancers | ||

| Bladder Cancer | ||

| Renal Cell Carcinoma | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the outpatient oncology infusion market size today and where is it heading by 2031?

The outpatient oncology infusion market size was USD 10.81 billion in 2025 and is projected to reach USD 17.02 billion by 2031 at a 7.99% CAGR over 2026-2031.

Which settings will capture the most growth in outpatient oncology infusions through 2031?

Standalone ambulatory infusion centers are projected to grow fastest, supported by site-neutral payment shifts and efficiency gains, while hospital outpatient departments retain complex, higher-acuity care.

Which therapies are shaping scheduling and chair-time planning for infusion centers?

New antibody-drug conjugates and broader immuno-oncology use are increasing observation and premedication needs, which lengthen chair time and raise the need for predictive scheduling.

How are payers changing the operating environment for infusion providers in 2026?

Site-neutral payment steps and gold-carding for pathway-adherent providers are reducing reimbursement in some hospital-based sites while streamlining approvals and promoting predictable starts.

What operational tactics are leaders using to expand infusion capacity without more chairs?

Predictive scheduling, load levelling, and standardized premedication and observation windows are raising throughput and cutting wait times, which improves on-time starts and staff productivity.

Which tumor areas are most relevant for near-term infusion growth?

Breast cancer volumes remain large and stable, while lung cancer is projected to grow faster through 2031 as newer regimens expand outpatient use.

Page last updated on: