Acute Hospital Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.68 Trillion |

| Market Size (2031) | USD 4.91 Trillion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Hospital Care Market Analysis by Mordor Intelligence

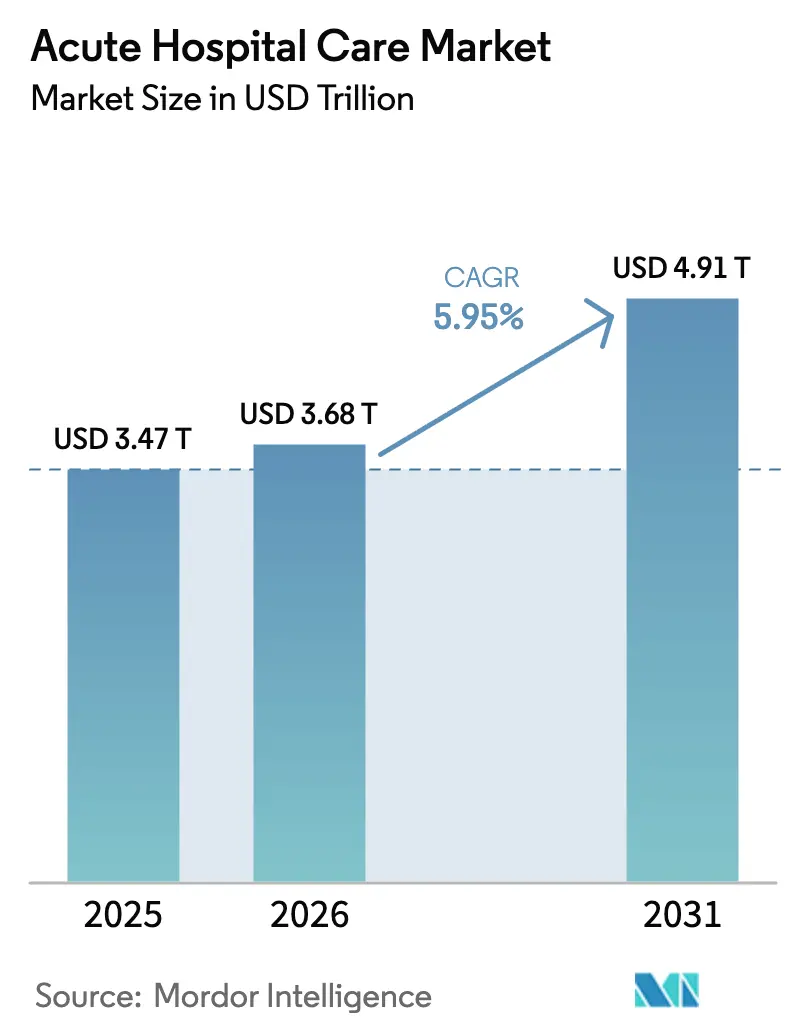

The Acute Hospital Care Market size was valued at USD 3.47 trillion in 2025 and estimated to grow from USD 3.68 trillion in 2026 to reach USD 4.91 trillion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031).

Clear-up of pandemic-era surgical backlogs, rapid population aging, and infrastructure investment across high-growth economies keep demand for hospital-based services on an upward trajectory. Elective procedures have returned to pre-2020 volumes, while complex multimorbidity among older adults supports longer lengths of stay and higher case acuity. Emerging markets add further momentum as governments channel capital into new facilities, digital records, and equipment modernization. Operators are also reshaping service portfolios toward robotic surgery, precision medicine, and integrated post-acute pathways to defend margins in an inflationary cost environment.

Key Report Takeaways

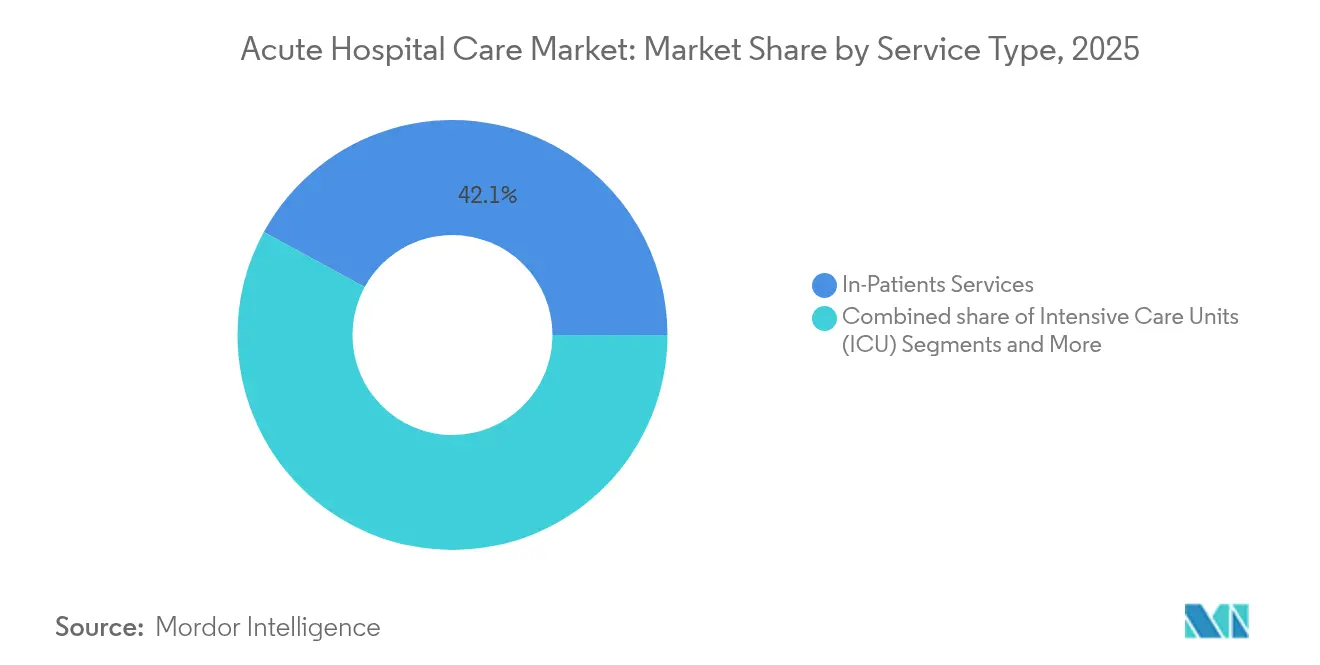

- By service type, in-patient services led with 42.05% of acute hospital care market share in 2025, while specialty surgery is set to expand at a 7.82% CAGR through 2031.

- By ownership, public and government facilities held 55.46% revenue share in 2025; private for-profit operators post the fastest growth at 8.41% CAGR to 2031.

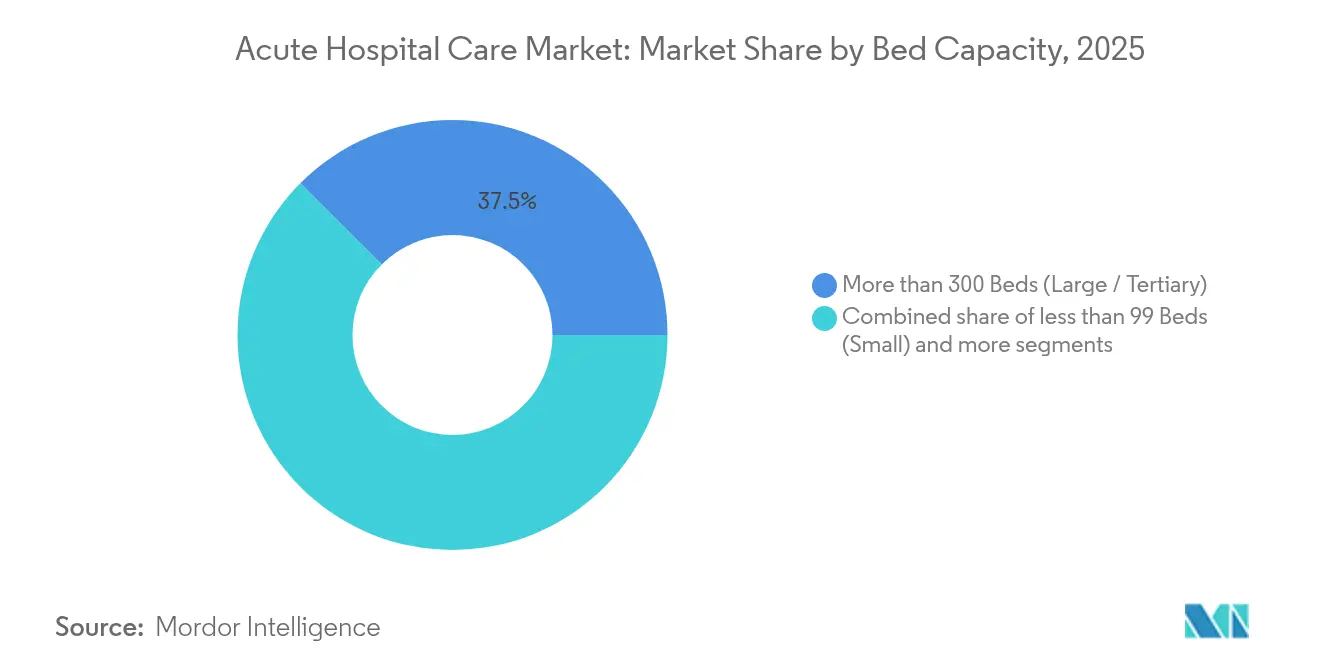

- By bed capacity, hospitals with more than 300 beds accounted for 37.52% value in 2025, whereas sub-99-bed facilities are advancing at 9.02% CAGR through 2031.

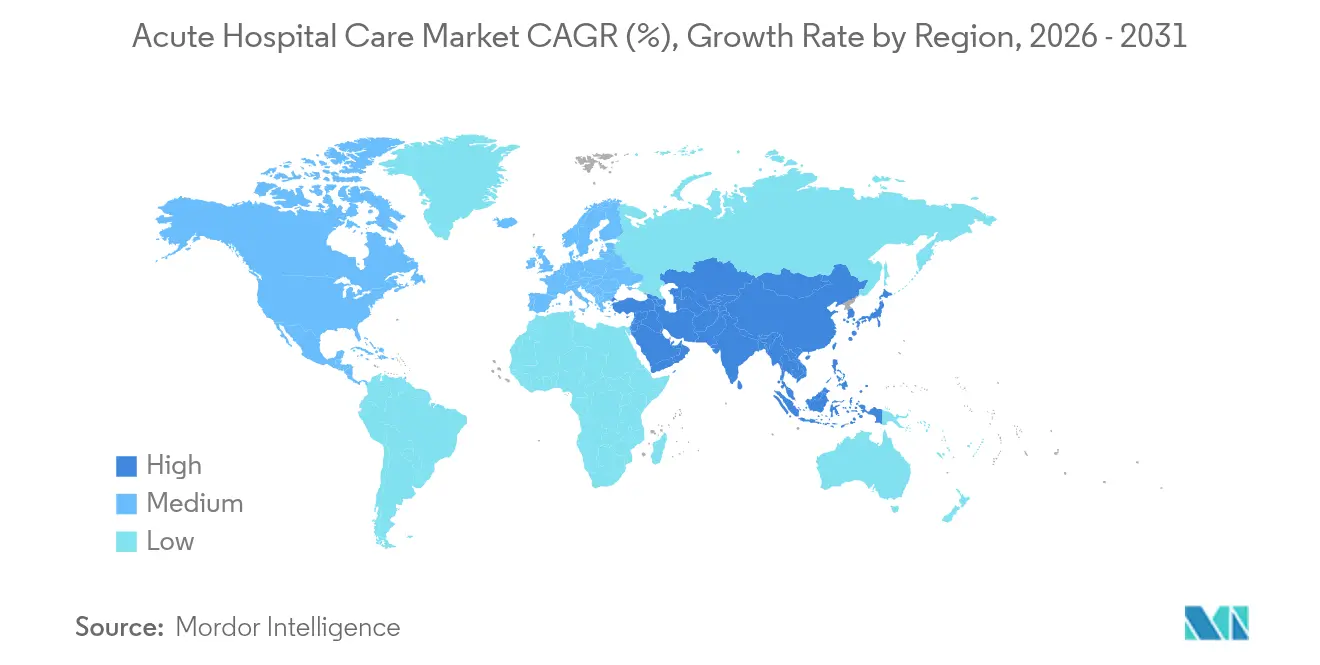

- By geography, North America contributed 42.21% revenue in 2025; Asia-Pacific is projected to deliver the highest CAGR at 9.69% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acute Hospital Care Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & chronic disease burden surge | +1.2% | Global, with highest impact in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Rising healthcare expenditure & coverage expansion | +0.8% | Global, with accelerated growth in emerging markets | Medium term (2-4 years) |

| Expansion of private insurance reimbursement | +1.1% | North America, Europe, and select APAC markets | Medium term (2-4 years) |

| Infrastructure boom in emerging economies | +0.9% | APAC core, Middle East, and Africa | Long term (≥ 4 years) |

| Increasing case-mix complexity favoring tertiary centres | +1.0% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Post-pandemic surgical backlog driving admissions | +0.8% | Global, with peak impact in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic Disease Burden

People aged 65+ consume three times more hospital care than younger cohorts, and this demographic now grows by 30 million each year worldwide. Hospitals see higher admissions for cardiovascular disease, diabetes, and cancer, conditions that often require multidisciplinary inpatient management. Tertiary centers profit from the uptick in valve replacement, complex oncology surgery, and advanced imaging. Workforce shortages, forecast to hit 10 million positions globally by 2030, create capacity pinch points just as demand peaks. Nevertheless, the enlarged elderly base underpins steady volumes that buffer the acute hospital care market against broader economic cycles.

Rising Healthcare Expenditure and Coverage Expansion

National health spending is projected to surge 70% to USD 7.7 trillion by 2032, supported by both public budgets and private payers. Expanded insurance coverage in Asia-Pacific and Latin America channels previously unmet demand into formal hospital settings. In the United States, the uninsured rate fell to 7.2% in 2023 after a decade of Affordable Care Act reforms, illustrating how policy changes convert latent demand into billable inpatient episodes[1]Source: Urban Institute, “Insurance Coverage Trends in the United States,” urban.org. As payment envelopes widen, hospitals deploy quality-improvement tools to align with value-based contracts that promise bonus pools for lower readmissions.

Expansion of Private Insurance Reimbursement

Commercial plans reimburse 150-200% of Medicare tariffs on average, creating a premium revenue stream for hospitals positioned in markets with strong employer-sponsored coverage. Growth in high-deductible plans shifts more cost to patients yet lessens payer resistance to negotiated hospital rates. In parallel, Medicare Advantage lives are forecast to top 90 million by 2027, giving providers predictable capitation income without material compression of yields. Many emerging economies replicate this pattern as middle-class households migrate to supplemental private coverage.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & operating expenditure | -0.6% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Critical shortage of skilled clinicians & nurses | -0.5% | Global, with severe impact in North America and Europe | Long term (≥ 4 years) |

| Accelerating shift to telehealth & outpatient settings | -0.4% | Global, with highest impact in developed markets | Medium term (2-4 years) |

| Bed-licensing & price-control regulations | -0.3% | North America, Europe, and select emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom in Emerging Economies

Indonesia earmarked USD 1 billion for hospital modernization in 2024, while China still approves more than 200 new hospital projects every year. India’s private sector plans 50,000 additional beds by 2027, and GCC states finance digital hospitals to lower outbound medical tourism. The building spree lifts near-term construction output and seeds long-term capacity for complex care, radiology, and intensive care units that depend on brick-and-mortar settings.

High Capital and Operating Expenditure

Modern tertiary hospitals cost USD 1-2 million per bed to construct, excluding diagnostics and IT infrastructure. Annual specialist fees climbed 9% in 2024 as competition for talent intensified. Rising energy, drug, and supply costs outstrip most reimbursement adjustments, squeezing EBITDA margins. Smaller rural hospitals struggle most because they lack volume leverage, prompting consolidation or service rationalization.

Critical Shortage of Skilled Clinicians and Nurses

The United States could face a 400,000 RN gap by 2027, while global deficits in nursing and physician labor may swell to 10 million by 2030. Turnover above 20% pushes recruitment spend higher and reduces available staffed beds even in facilities with spare physical capacity. Wage inflation exceeding 15% annually in critical care and perioperative specialties burdens budgets. International staff recruitment brings visa risk and cultural acclimatization challenges, and technology solutions cannot yet replace bedside care requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Specialty Surgery Drives Premium Growth

The in-patient category generated 42.05% of acute hospital care market share in 2025, anchoring revenue through admissions for cardiac events, stroke, and complex infection management. Specialty surgery, however, is forecast to grow at 7.82% CAGR on the back of robotic systems, image-guided navigation, and higher care acuity.

Advances in minimally invasive techniques shorten lengths of stay yet widen procedure eligibility, keeping operating rooms busy. Intensive care units remain a critical cost center, representing 13.2% of hospital expenditures worldwide, but they also drive bundled revenue under diagnosis-related group payment regimes. Diagnostics and imaging benefit from over 500 FDA-cleared AI radiology tools that enhance throughput, though rural hospitals face revenue cuts when payer schedules tighten. Rehabilitation and ancillary services gain traction as 45% of discharges now flow to integrated post-acute settings that keep patients inside hospital-owned networks.

By Ownership: Private Sector Momentum Accelerates

Public and government facilities captured 55.46% of 2025 revenue, underscoring their mandate to offer universal emergency cover regardless of patient solvency. Yet, private for-profit operators record an 8.41% CAGR to 2031, leveraging flexible capital access and service-line selectivity to chase commercially insured cohorts. Their efficiency stems from lean governance structures and data-driven scheduling that trims overtime spend.

Not-for-profit systems hold community benefits such as tax relief and philanthropic donations but still compete on quality metrics against investor-owned chains. In emerging markets, multilateral lenders and private equity funds inject capital into greenfield projects that accelerate private share gains. Value-based contracts favor owners capable of deploying population health analytics, a capability often best financed by private investors.

By Bed Capacity: Small Hospitals Defy Consolidation Trends

Facilities with more than 300 beds controlled 37.52% of acute hospital care market value in 2025 and remain indispensable for quaternary services like transplant surgery and complex oncology. Smaller hospitals under 99 beds, however, post the strongest 9.02% CAGR by offering community-centric care with lower overhead.

Tele-ICU platforms and remote specialty consults extend the clinical reach of these institutions without requiring bricks-and-mortar expansion, leading to nimble cost profiles. Rural access programs and federal stabilization grants also support solvency, especially in North America. Mid-sized hospitals face the toughest squeeze, lacking both major-system bargaining power and the intimacy of critical-access peers, which pushes them into affiliation agreements or niche specialization.

Geography Analysis

North America generated 42.21% of 2025 revenue thanks to high per-capita spend, insurance depth, and sophisticated service mix. Average daily hospital costs top USD 3,000 in major U.S. metro centers, and capital intensity supports cutting-edge robotics and genomic oncology programs. Nonetheless, nursing vacancies and state-level price caps temper near-term upside.

Asia-Pacific is projected to register a 9.69% CAGR through 2031, the fastest globally, propelled by China’s ongoing hospital construction boom and India’s targeted 50,000-bed private-sector expansion. Younger age structures bolster clinical workforce pools, while rapid aging in Japan and South Korea drives up complex admissions. Singapore’s medical tourism push lifts average case revenue as foreign patients seek premium cardiac and orthopedic care.

Europe continues steady growth supported by universal health coverage and aging demographics. Admission counts stay high, although average stays remain shorter than in North America because of integrated primary care pathways. Middle East and Africa show diverging trajectories: GCC members invest heavily in smart hospitals as part of economic diversification, whereas lower-income nations battle funding gaps and workforce scarcities. South America is mixed; Brazil’s sheer scale sustains demand but currency volatility in Argentina constrains capex planning.

Competitive Landscape

The acute hospital care market is moderately fragmented. In the United States, HCA Healthcare, Community Health Systems, and Tenet command regional clusters that support joint purchasing and centralized revenue-cycle platforms. Internationally, IHH Healthcare and Ramsay Health Care extend footprints through tactical acquisitions, such as IHH’s USD 901 million purchase of Island Hospital in Malaysia, consolidating the Southeast Asian premium segment.

Strategic imperatives revolve around margin defense via AI-assisted workflows that trim readmissions, perioperative robotics that enhance throughput, and portfolio realignment toward high-acuity service lines. Technology adoption also mitigates nurse shortfalls by automating documentation and predictive vitals monitoring. Disruption looms from ambulatory surgical centers and retail clinics siphoning lower-acuity volumes, so hospitals double down on emergency, trauma, and intensive care where barriers to entry stay high.

Regional consolidation accelerates where regulators permit cross-market mergers to preserve solvency of community facilities. Conversely, antitrust scrutiny rises in densely populated U.S. states, limiting mega-mergers and encouraging network-level collaboration instead of outright ownership transfers.

Acute Hospital Care Industry Leaders

Orlando Health

Sound Phyisicans

EnduraCare Acute Care Services, LLC

Community Health System, Inc.

Banner University Medical Center Phoenix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Community Health Systems agreed to sell Cedar Park Regional Medical Center, Texas

- January 2025: UnitedHealthcare introduced new commercial coding rules for shoulder arthroscopy and radiation therapy, mirroring CMS edits.

- September 2024: IHH Healthcare closed its USD 901 million acquisition of Island Hospital, Malaysia.

Global Acute Hospital Care Market Report Scope

According to the report's scope, acute hospital care refers to a level of medical treatment that involves treating patients for conditions caused by disease or trauma, as well as during recovery from surgery. The patient receives active, short-term treatment for a condition in an acute care setting.

The acute care hospital market report is segmented by service type into inpatient services, intensive care units, emergency & trauma care, general surgery, specialty surgery, diagnostic and imaging, and other services. By ownership, the market is segmented into public/government, private for-profit, and not-for-profit/charitable sectors. The bed capacity market is segmented into three categories: less than 99 beds, 100–299 beds, and more than 300 beds. By geography, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done based on value (in USD).

| In-patient Services |

| Intensive Care Units (ICU) |

| Emergency & Trauma Care |

| General Surgery |

| Specialty Surgery (Cardiac, Neuro, Ortho, etc.) |

| Diagnostics & Imaging |

| Other Services |

| Public / Government |

| Private For-profit |

| Not-for-profit / Charitable |

| less than 99 Beds (Small) |

| 100–299 Beds (Medium) |

| More than 300 Beds (Large / Tertiary) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | In-patient Services | |

| Intensive Care Units (ICU) | ||

| Emergency & Trauma Care | ||

| General Surgery | ||

| Specialty Surgery (Cardiac, Neuro, Ortho, etc.) | ||

| Diagnostics & Imaging | ||

| Other Services | ||

| By Ownership | Public / Government | |

| Private For-profit | ||

| Not-for-profit / Charitable | ||

| By Bed Capacity | less than 99 Beds (Small) | |

| 100–299 Beds (Medium) | ||

| More than 300 Beds (Large / Tertiary) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the acute hospital care market?

The acute hospital care market is valued at USD 3.68 trillion in 2026 and is projected to reach USD 4.91 trillion by 2031.

Which region is growing fastest in acute hospital care?

Asia-Pacific leads growth with a forecast 9.69% CAGR through 2031, driven by large-scale infrastructure projects and expanding insurance coverage.

Which service segment shows the highest growth?

Specialty surgery is expected to grow at 7.82% CAGR, supported by robotics adoption and rising procedural complexity.

How are private hospitals performing versus public facilities?

While public institutions hold 55.46% revenue share, private for-profit hospitals are expanding faster at an 8.41% CAGR owing to flexible capital access and selective service positioning.

Page last updated on: