United States Hemorrhoid Treatment Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

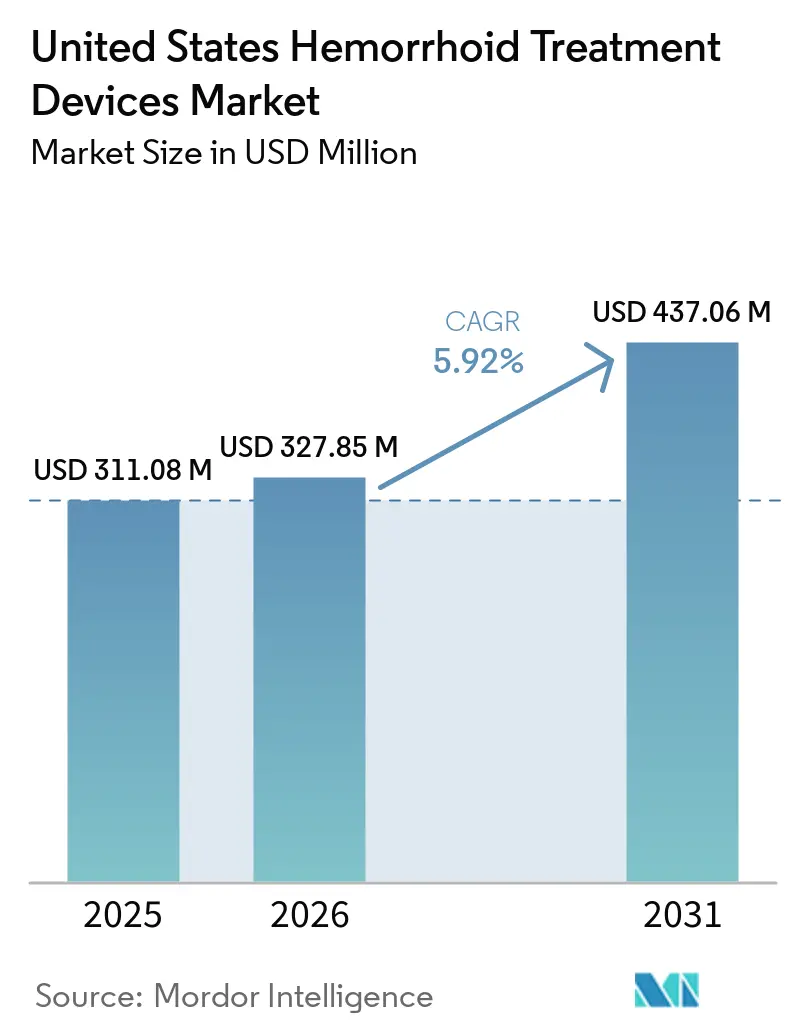

| Base Year Market Size (2025) | USD 311.08 Million |

| Market Size (2026) | USD 327.85 Million |

| Market Size (2031) | USD 437.06 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

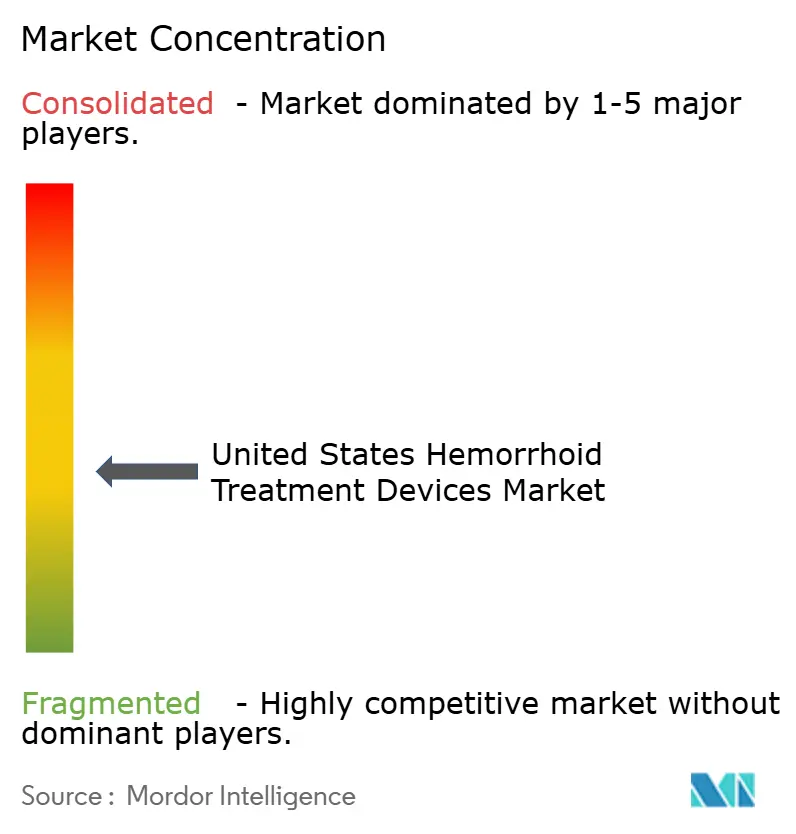

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Hemorrhoid Treatment Devices Market Analysis by Mordor Intelligence

The United States Hemorrhoid Treatment Devices Market size was valued at USD 311.08 million in 2025 and is estimated to grow from USD 327.85 million in 2026 to reach USD 437.06 million by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

The United States hemorrhoid treatment devices market is supported by a large and persistent treatment pool, because hemorrhoids account for more than 2.2 million outpatient evaluations each year in the United States, and symptomatic disease is common among adults aged 50 and above. The United States hemorrhoid treatment devices market is also benefiting from a steady move toward same-day treatment, low-discomfort procedures, and office or outpatient care models that fit grade I to grade III disease management pathways endorsed in current clinical guidance. Medicare support for CPT code 46221 continues to anchor procedural economics in physician offices and ambulatory settings, which keeps band ligator consumables and related accessories central to the procurement cycle. At the same time, the United States hemorrhoid treatment devices market faces a clear access ceiling in rural counties with limited gastroenterology coverage, while OTC symptom management and uneven payer alignment for newer energy platforms continue to slow procedural conversion for a portion of the patient pool.

Key Report Takeaways

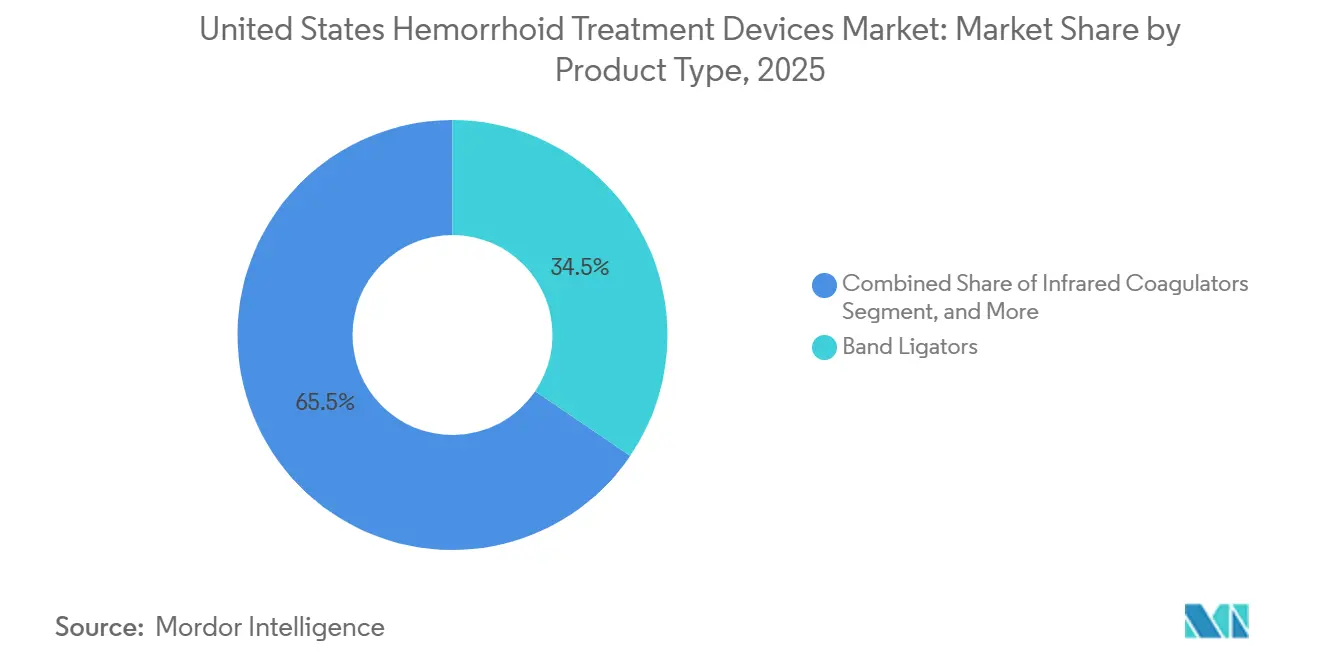

- By product type, band ligators held 34.48% of the United States hemorrhoid treatment devices market share in 2025, while cryotherapy devices are projected to expand at a 7.36% CAGR through 2031.

- By procedure type, non-surgical procedures accounted for 51.17% of the United States hemorrhoid treatment devices market size in 2025, while minimally invasive surgical procedures recorded the highest projected CAGR at 8.87% through 2031.

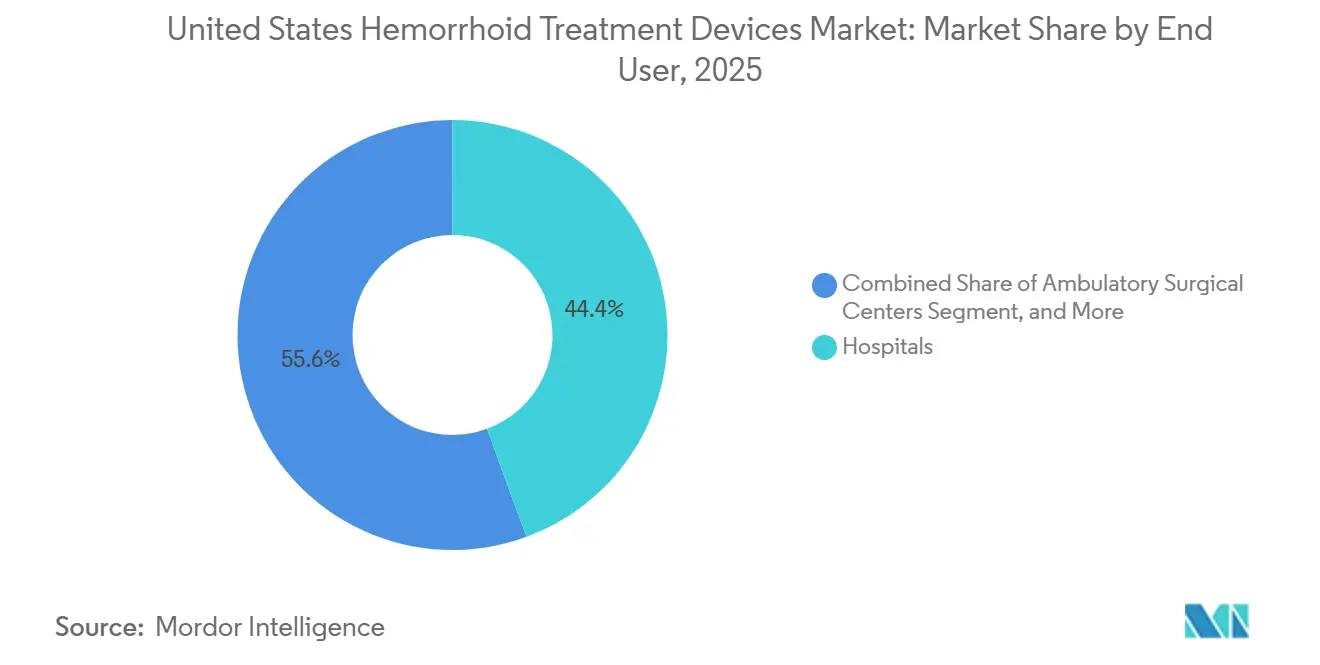

- By end user, hospitals captured 44.42% of the United States hemorrhoid treatment devices market size in 2025, while ambulatory surgical centers are advancing at a 7.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hemorrhoid Treatment Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Symptomatic Hemorrhoids In Adults Over 50 | +1.4% | National, with highest burden in Southern and Midwestern states with aging rural demographics | Long term (≥ 4 years) |

| Shift Toward Minimally Invasive And Outpatient Treatment Pathways | +1.2% | National, strongest adoption in Northeast and urban South | Medium term (2-4 years) |

| Expansion Of ASC Utilization For Proctology Procedures | +1.0% | National, ASC growth particularly pronounced in the South and West | Medium term (2-4 years) |

| Medicare Reimbursement Support For Rubber Band Ligation And Related Procedures | +0.8% | National, CMS-certified ASC network across all 50 states | Short term (≤ 2 years) |

| Rising Demand For Single-Use, Infection-Control-Focused Devices | +0.5% | National, accelerated in high-volume outpatient clinics and ASCs | Short term (≤ 2 years) |

| Growth In Patient Preference For Home Recovery And Low-Discomfort Treatment Options | +0.4% | National, with early traction in patient-directed care markets in the Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Symptomatic Hemorrhoids in Adults Over 50

The United States hemorrhoid treatment devices market continues to draw support from age-linked disease prevalence and a large untreated patient base. Current guidance states that nearly half of Americans develop symptomatic hemorrhoids by age 50, and the condition affects 10.4 million people in the country at any given time.[1]American Society of Colon and Rectal Surgeons, “Management of Hemorrhoids,” ASCRS Clinical Practice Guidelines Toolkit, ascrsu.com The same source indicates that 1 million new cases arise each year, and 10% to 20% of those patients require procedural treatment. Medicare fee-for-service data also show hemorrhoid-associated diagnoses in 4.2% of beneficiaries aged 65 to 84, with the highest burden in the 70 to 74 group, which keeps the age-driven demand base intact for the United States hemorrhoid treatment devices market. This means future volume in the United States hemorrhoid treatment devices market depends not only on prevalence, but also on how effectively office procedures can convert symptomatic patients into treated cases.

Shift Toward Minimally Invasive and Outpatient Treatment Pathways

The United States hemorrhoid treatment devices market is moving further toward minimally invasive care because current ASCRS guidance identifies rubber band ligation as the most effective office-based option for symptomatic grade I to grade III internal hemorrhoids. The guideline review cites an 86.7% asymptomatic rate at 8 weeks in a 2,635-patient retrospective series, which reinforces the appeal of office procedures that avoid operating room use for a large share of patients. This treatment pattern is redirecting procurement toward band ligators, anoscopes, and sclerotherapy injector kits rather than hospital-centered surgical instrumentation. Sclerotherapy is also gaining ground, because polidocanol foam has shown 98% symptom resolution at 4 weeks in a prospective 2,000-patient series and 95.6% success at 1 year in a phase II multicenter trial. As a result, the United States hemorrhoid treatment devices market is broadening beyond banding alone and is creating room for newer office-ready injector platforms.

Expansion of Outpatient Procurement, Reimbursement Support, and Single-Use Formats

The United States hemorrhoid treatment devices market is also gaining from payment certainty in outpatient care, especially for rubber band ligation in office and ASC settings. Cook Medical’s 2024 reimbursement guide shows that CPT code 46221 has established Medicare support, with an ASC facility fee of USD 871.7 for the procedure, which helps preserve the revenue logic for routine banding.[2]Cook Medical, “2024 Coding and Reimbursement Guide, Hemorrhoidectomy via Simple (Rubber Band) Ligation,” Cook Medical, cookmedical.com That certainty supports recurring purchases of ligator consumables and accessories, while also favoring products that fit high-throughput treatment flow. The same shift is increasing demand for single-use devices, because outpatient clinics value quick turnover, simple setup, and infection-control discipline in busy procedural environments. This combination of reimbursement visibility and disposable design is keeping the United States hemorrhoid treatment devices market closely tied to outpatient workflow economics rather than to large capital budgets alone.

Patient Preference for Home Recovery and Lower-Discomfort Treatment

The United States hemorrhoid treatment devices market is also shaped by patient preference for shorter recovery and less post-procedural discomfort. This preference fits office-based banding and sclerotherapy, and it also supports interest in cryotherapy and laser-based systems for selected patients. The CYPHER randomized controlled trial found that intra-anal cryotherapy reduced pain after defecation in the early postoperative period after grade III hemorrhoidectomy, which strengthens the case for technologies that improve the recovery experience. The regulatory path is also active, because FDA 510(k) clearances in 2024 covered new cryoablation systems with hemorrhoid and proctology applications. Together, these factors are helping the United States hemorrhoid treatment devices market extend beyond standard office devices into newer low-discomfort platforms that still fit the same-day care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Specialist Access In Rural And Underserved Areas | -0.5% | National, most acute in Wyoming, Alaska, Idaho, North Dakota, and rural South | Long term (≥ 4 years) |

| OTC Topical And Home Remedy Substitution Delaying Device Adoption | -0.4% | National, highest substitution rates in lower-income and rural consumer markets | Short term (≤ 2 years) |

| Reimbursement Friction For Newer Or Higher-Cost Device Platforms | -0.3% | National, variability by payer mix in Southern and Midwestern states | Medium term (2-4 years) |

| Sustainability Pressure On Disposable Device Plastics And Packaging | -0.2% | National, emerging compliance pressure in states with advanced EPR legislation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Specialist Access in Rural and Underserved Areas

The United States hemorrhoid treatment devices market continues to face a structural access constraint in countries with limited specialist coverage. A 2026 study in Digestive Diseases and Sciences found that more than two-thirds of 3,149 US counties lacked a gastroenterologist, and 49 million to 50 million Americans lived more than 25 miles from GI specialty care.[3]Charles Hassan et al., “Geographic Disparities in the Supply and Demand of Gastroenterologists Across the United States, Forecasting a National Shortage,” Digestive Diseases and Sciences, link.springer.com In 2025, non-metropolitan areas had a gastroenterologist workforce adequacy of only 29.7%, compared with 106% in metropolitan areas, and the South remained the weakest region, even within metro geographies, at 87% adequacy. The same access problem is likely to persist because more than two-thirds of rural GI specialists were older than 55, and nearly half were older than 65, which points to additional retirement pressure on procedural capacity. Rural primary care constraints reinforce the same issue, as 66.3% of all primary care Health Professional Shortage Areas were in rural locations as of September 2024.

OTC Substitution, Reimbursement Friction, and Sustainability Pressure

The United States hemorrhoid treatment devices market also loses procedural volume because many patients manage symptoms with OTC topical products and home care instead of seeking intervention. This pattern is supported by the ASCRS recommendation that dietary and behavioral changes remain first-line treatment, and randomized trial evidence shows fiber supplementation reduced the relative risk of persistent symptoms to 0.47 and bleeding to 0.50. That conservative treatment pathway delays entry into device-based care until symptoms worsen or conservative management fails. At the same time, higher-cost modalities such as laser hemorrhoidoplasty and newer cryotherapy systems do not yet benefit from the same reimbursement clarity that supports rubber band ligation, which creates uneven payer acceptance across the United States hemorrhoid treatment devices market. Sustainability scrutiny around disposable plastics and packaging adds a longer-term operating pressure for suppliers whose growth plans depend heavily on single-use formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Band Ligators Hold the Lead While Cryotherapy and Laser Systems Lift the Growth Profile

Band ligators held 34.48% of the United States hemorrhoid treatment devices market share in 2025, which kept them in the leading product position. Their position reflects continued endorsement in ASCRS guidance, a well-defined office procedure role, and established reimbursement support for routine banding. The product class also benefits from continued movement toward disposable and pre-loaded systems, with platforms such as the CRH O’Regan System built around office and outpatient workflow efficiency. Infrared coagulators, sclerotherapy injectors, and bipolar probes remain clinically relevant in grade I to grade II disease, in anticoagulated patients, and in adjunctive procedural settings where banding is not the only preferred choice.

Cryotherapy devices are the fastest-growing product segment, and this part of the United States hemorrhoid treatment devices market size is projected to rise at a 7.36% CAGR through 2031. The CYPHER trial gave this category stronger clinical support by showing lower early postoperative pain after grade III hemorrhoidectomy when intra-anal cryotherapy was used. FDA 510(k) clearances for the XSense Cryoablation System and the Co-Ablation System in 2024 showed that the regulatory channel remains open for newer cryotherapy options in proctology. Laser probes still hold a smaller current position, but they are gaining interest as hospitals and advanced outpatient centers adopt consoles that address grade II to grade IV disease with a lower pain profile than conventional excisional approaches in selected cases.

By Procedure Type: Non-Surgical Procedures Lead Revenue While Minimally Invasive Surgery Expands Faster

Non-surgical procedures accounted for 51.17% of the United States hemorrhoid treatment devices market size in 2025, which confirms that office-based care still carries the largest volume base. This pattern is consistent with ASCRS guidance that office procedures remain first-line for most grade I to grade III presentations. The segment draws support from the scale of rubber band ligation across gastroenterology and colorectal clinics, where speed, repeatability, and reimbursement clarity matter more than large capital purchases. A 2025 multicenter randomized trial also reinforced the practical appeal of this category by showing a return-to-work time of 1 day for rubber band ligation compared with 9 days for hemorrhoidectomy in grade III disease.

Minimally invasive surgical procedures are projected to post the fastest CAGR at 8.87% through 2031 in the United States hemorrhoid treatment devices market. Growth in this segment reflects wider use of stapled hemorrhoidopexy, Doppler-guided hemorrhoid artery ligation, and laser hemorrhoidoplasty for patients who need more than office treatment but want to avoid conventional excision. These procedures raise the average device value per case because they depend more on capital equipment and higher-cost platforms than non-surgical approaches do. Conventional hemorrhoidectomy remains necessary for grade IV disease and mixed internal-external presentations, but its role is tied more to treatment failure and advanced disease than to broad-based procedural expansion.

By End User: Hospitals Retain Scale While Ambulatory Surgical Centers Add the Strongest Momentum

Hospitals held 44.42% of the United States hemorrhoid treatment devices market size in 2025, giving them the largest end-user position. Their lead reflects the need for anesthesia support, post-procedure monitoring, and capital equipment in conventional hemorrhoidectomy and several minimally invasive surgical procedures. Hospital purchasing also tends to favor multi-purpose platforms and reusable instrument sets, which support diversified suppliers with broader GI portfolios. Specialty clinics and colorectal centers sit between hospitals and ASCs, because they deliver steady procedural throughput and rely heavily on standardized office-based protocols such as band ligation and infrared coagulation.

Ambulatory surgical centers are the fastest-growing end-user group in the United States hemorrhoid treatment devices market, with a 7.07% CAGR expected through 2031. Their appeal comes from same-day workflow, lower overhead, and procedure models that fit disposable ligators, anoscopes, and ready-to-use kits more naturally than large hospital procurement systems do. This shift is changing go-to-market strategy, because suppliers need product bundles and direct contracting approaches that match physician-led outpatient sites rather than only hospital group purchasing relationships. As outpatient care expands, the United States hemorrhoid treatment devices market is likely to see stronger competition around simplicity, turnover speed, and device formats built for high-volume ambulatory use.

Geography Analysis

The Northeast currently shows the strongest specialist supply conditions within the United States hemorrhoid treatment devices market. A 2025 study reported gastroenterologist workforce adequacy of 134% in the region, making it the only part of the country where supply exceeded estimated demand. Massachusetts, Connecticut, and New York also recorded gastroenterologist density above 7.0 per 100,000 people, which supports a dense referral network for office-based hemorrhoid procedures. That setting supports steady demand for band ligators, coagulation devices, and single-use accessories in physician offices and specialty colorectal clinics.

The South presents the broadest opportunity in the United States hemorrhoid treatment devices market, but it also carries the sharpest structural access limits. The same 2025 national shortage study showed regional adequacy of only 87% in the South, which was the lowest among all US regions. This matters because aging rural populations in the region keep the patient pool large even when specialist coverage is thin. Device demand therefore tends to cluster in metropolitan referral hubs, hospital systems, and larger outpatient sites that can absorb volume from a wide catchment area. Rural care gaps also persist across the wider primary care network, which limits early diagnosis and slows the path from symptoms to procedure in many counties.

The Midwest and West follow different access patterns, and each influences the United States hemorrhoid treatment devices market in a different way. The Midwest has a relatively more distributed rural GI practitioner base than the South, which supports a broader spread of procedural activity across community settings. The West has strong metropolitan concentration, but frontier states remain thinly covered, and Nevada was projected to have only 43.5% gastroenterologist adequacy by 2037. Arizona and other rural western communities also remain far from GI care access, which keeps procedure volume concentrated in large urban centers rather than evenly spread across the region.

Competitive Landscape

The United States hemorrhoid treatment devices market remains moderately fragmented, with a mix of diversified medical device companies and focused procedure specialists competing across office, outpatient, and hospital settings. Cook Medical has strengthened its position with the ShortShot Saeed Hemorrhoidal Multi-Band Ligator and TriView Anoscope configuration, which fits standardized GI suite workflow and supports quick procedural setup. Boston Scientific’s Speedband Superview Super 7 remains a recognizable ligation platform, although FDA MAUDE reports in 2024 drew attention to deployment reliability and quality-control scrutiny at the procurement stage.

Single-use and outpatient-focused companies continue to shape a distinct layer of competition inside the United States hemorrhoid treatment devices market. CRH Medical remains relevant through the CRH O’Regan System, a procedure format built around office efficiency and disposable workflow. Regulatory activity also points to broader competition across energy modalities, because FDA clearances in 2024 covered cryoablation systems with hemorrhoid and proctology indications. In 2026, TRIANGEL Medical received FDA 510(k) clearance for Endolaser V6, a dual-wavelength diode laser system designed for proctology applications including grade II to grade IV hemorrhoids and laser hemorrhoidoplasty. These developments are increasing pressure on older infrared coagulation offerings and are widening the set of treatment choices available to providers.

Procedure-specific firms such as A.M.I. Agency for Medical Innovations, Privi Medical, and Ultroid Technologies compete more through focused device design than through full portfolio scale. J&J MedTech also remains active in stapled hemorrhoidopexy through the PROXIMATE PPH Hemorrhoidal Circular Stapler Set, which continues to serve as a hospital-based alternative in surgical care pathways. For larger suppliers, strong hospital relationships alone are no longer enough, because the United States hemorrhoid treatment devices market is placing more value on evidence-backed disposable formats and outpatient usability. Compliance with FDA 510(k) requirements and quality system rules under 21 CFR Part 820 remains a significant barrier, which limits easy entry for undercapitalized companies and helps established firms protect their positions.

United States Hemorrhoid Treatment Devices Industry Leaders

B. Braun Melsungen AG

CONMED Corporation

Karl Storz SE and Co. KG

Teleflex Incorporated

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Pexy Easy, a new venture introduced under the LEAD company framework with the mission of transforming hemorrhoid treatment. Founded by surgeon Johan Ungerstedt, the initiative stems from his extensive experience in emergency and trauma surgery and his frustration with the limitations of existing hemorrhoid procedures. Inspired by a study he encountered in 2011 during a colorectal surgery course in Linköping, which demonstrated that hemorrhoids could be stitched and repositioned rather than surgically removed, Ungerstedt set out to design a gentler, more accessible solution.

- May 2025: Apollo Spectra Hospital in Chennai introduced a new minimally invasive procedure for haemorrhoids, designed to reduce patient discomfort and speed up recovery. The treatment, known as the Rafaelo procedure (radiofrequency ablation of haemorrhoids under local anaesthesia), was originally developed in Poland and has now been launched in India. Unlike traditional surgical methods that often require significant recovery time, Rafaelo enables patients to avoid the pain of major surgery and return to normal daily activities much sooner. This marks a significant advancement in haemorrhoid care, expanding access to gentler and more effective treatment options.

- May 2025: Apollo has announced the introduction of the Rafaelo procedure, a minimally invasive therapy designed to treat haemorrhoids more effectively and comfortably. Delivered as a daycare therapy, Rafaelo uses radiofrequency ablation under local anaesthesia, offering patients a gentler alternative to traditional surgical methods.

United States Hemorrhoid Treatment Devices Market Report Scope

The United States Hemorrhoid Treatment Devices Market refers to the industry segment encompassing specialized medical instruments and equipment designed to diagnose, manage, and surgically or non-surgically remove hemorrhoids, swollen veins in the anus and lower rectum. It excludes topical drugs like creams and ointments.

The United States Hemorrhoid Treatment Devices Market is segmented by product type, procedure type, and end user. By product type, the market includes band ligators, infrared coagulators, sclerotherapy injectors, bipolar probes, cryotherapy devices, and laser probes. By procedure type, treatments are categorized into non‑surgical procedures, minimally invasive surgical procedures, and conventional hemorrhoidectomy. By end user, adoption is driven by hospitals, ambulatory surgical centers, and specialty clinics and colorectal centers.

| Band Ligators |

| Infrared Coagulators |

| Sclerotherapy Injectors |

| Bipolar Probes |

| Cryotherapy Devices |

| Laser Probes |

| Non-Surgical Procedures |

| Minimally Invasive Surgical Procedures |

| Conventional Hemorrhoidectomy |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics and Colorectal Centers |

| By Product Type | Band Ligators |

| Infrared Coagulators | |

| Sclerotherapy Injectors | |

| Bipolar Probes | |

| Cryotherapy Devices | |

| Laser Probes | |

| By Procedure Type | Non-Surgical Procedures |

| Minimally Invasive Surgical Procedures | |

| Conventional Hemorrhoidectomy | |

| By End User | Hospitals |

| Ambulatory Surgical Centers | |

| Specialty Clinics and Colorectal Centers |

Key Questions Answered in the Report

What is the projected value of the United States hemorrhoid treatment devices market by 2031?

The United States hemorrhoid treatment devices market is projected to reach USD 437.06 million by 2031, rising from USD 327.85 million in 2026 at a 5.92% CAGR over 2026-2031.

Which product category leads revenue in the United States hemorrhoid treatment devices market?

Band ligators led the United States hemorrhoid treatment devices market in 2025 with a 34.48% share, supported by guideline endorsement and established reimbursement.

Which procedure category is growing the fastest through 2031?

Minimally invasive surgical procedures are forecast to grow the fastest, with an 8.87% CAGR through 2031, as providers expand use of stapled, Doppler-guided, and laser-based options.

Which end-user group is expanding the quickest?

Ambulatory surgical centers are the fastest-growing end-user group, with a 7.07% CAGR through 2031, because same-day workflow and lower overhead fit hemorrhoid procedures well.

What is the main factor supporting long-term demand?

Aging demographics remain the main support factor, as nearly half of Americans develop symptomatic hemorrhoids by age 50 and hemorrhoid-related diagnoses remain common in older Medicare populations.

What is the biggest constraint on procedure volumes in the United States?

Limited specialist access is the key constraint, because more than two-thirds of US counties lack a gastroenterologist and 49 million to 50 million people live more than 25 miles from GI specialty care.

Page last updated on: