Postpartum Hemorrhage Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

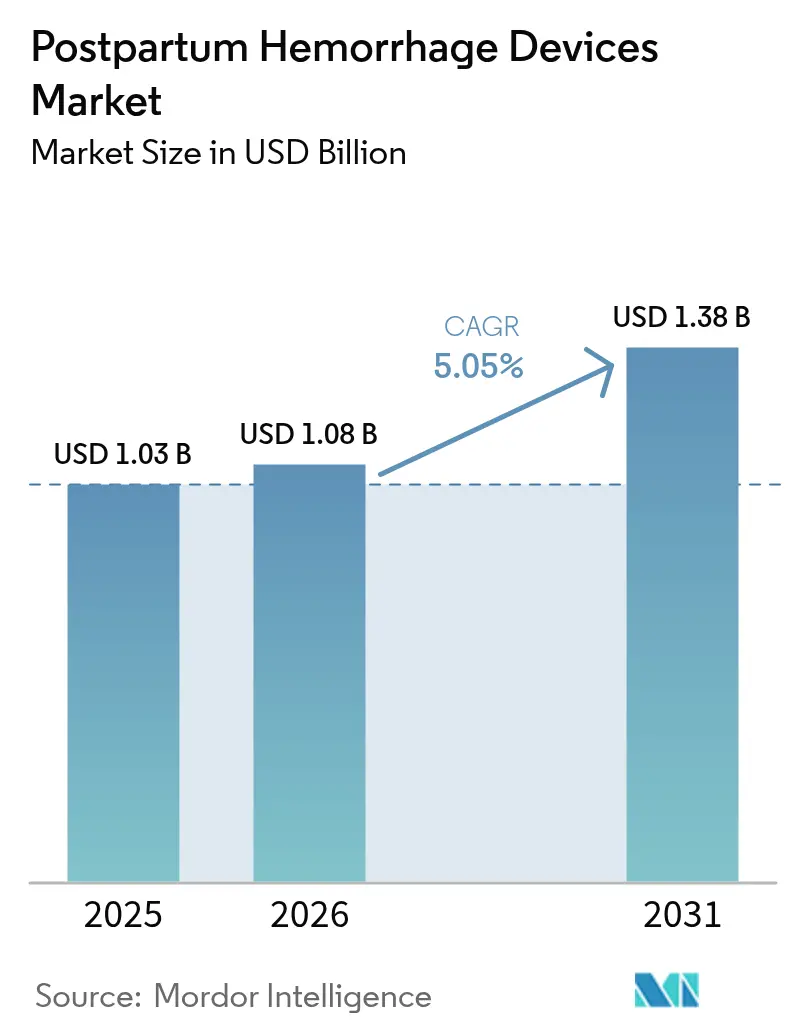

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

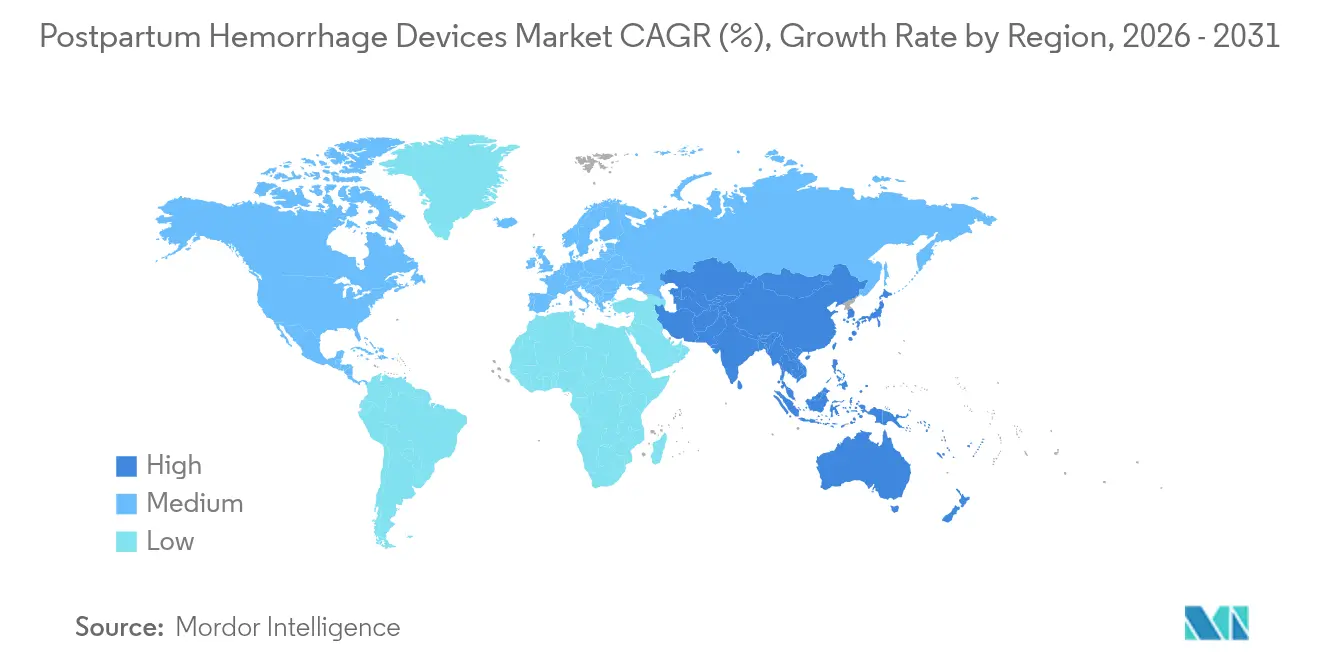

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

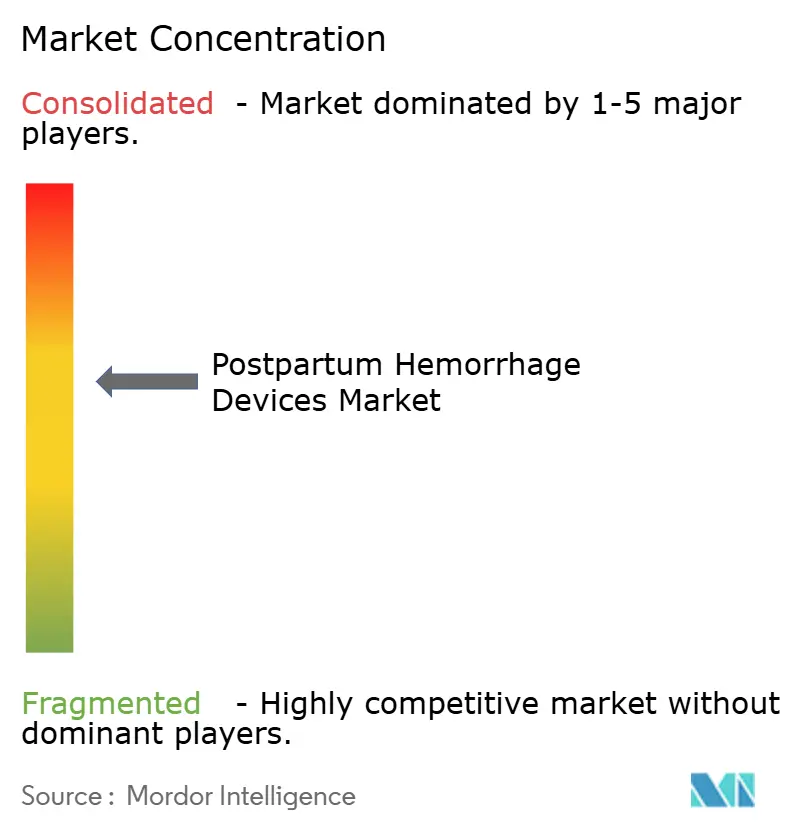

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Postpartum Hemorrhage Devices Market Analysis by Mordor Intelligence

postpartum hemorrhage devices market size in 2026 is estimated at USD 1.08 billion, growing from 2025 value of USD 1.03 billion with 2031 projections showing USD 1.38 billion, growing at 5.05% CAGR over 2026-2031. Demand acceleration stems from the convergence of supportive regulation, maturing artificial-intelligence architectures and persistent gaps in maternal-mortality reduction strategies. Device makers that combine predictive analytics with mechanical or pharmacological interventions are reshaping care pathways, pulling investment from hospital capital budgets toward earlier, technology-enabled risk mitigation. Regulatory bodies in the United States and Europe have compressed approval timelines, improving commercialization velocity, while the World Health Organization’s large-scale roll-out programs have widened access in low-resource geographies. Competitive positioning therefore hinges on demonstrating superior clinical outcomes, embedding seamlessly into electronic health-record (EHR) workflows and aligning pricing with value-based procurement mandates across public and private payers.

Key Report Takeaways

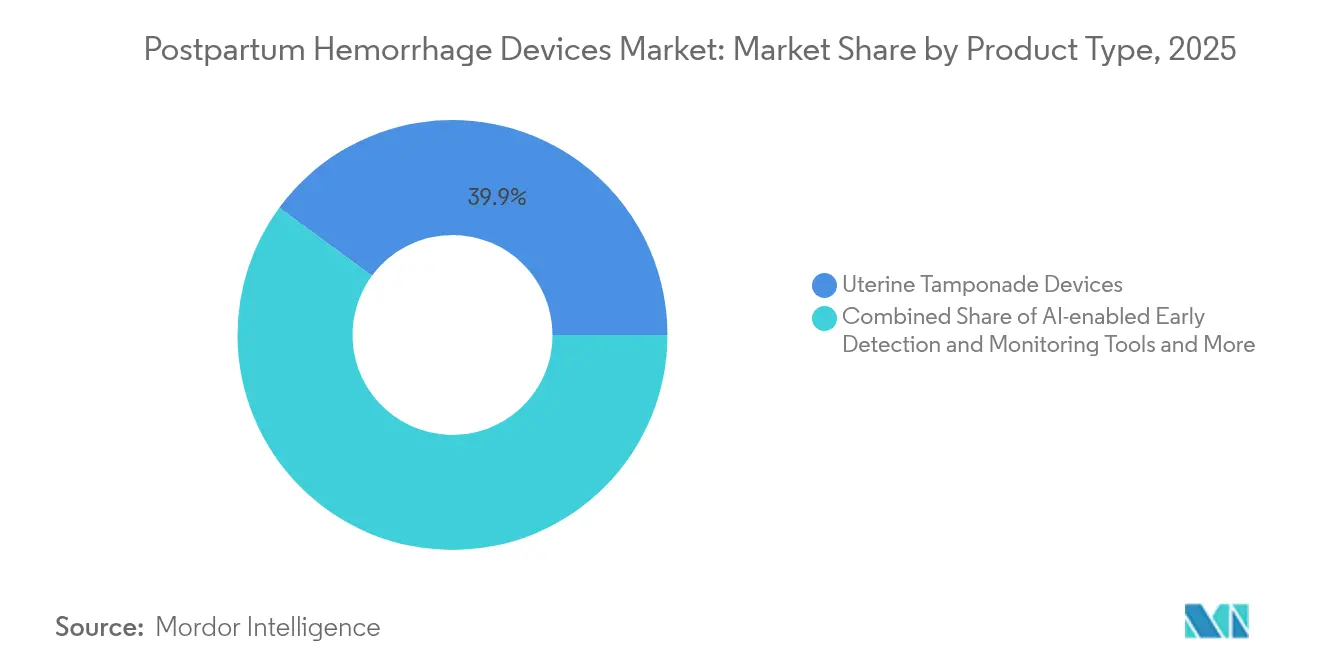

- By product category, uterine tamponade devices held a 39.92% postpartum hemorrhage devices market share in 2025, while AI-enabled detection platforms are projected to grow at a 11.72% CAGR through 2031.

- By end user, hospitals accounted for 67.35% of the market size in 2025, whereas ambulatory surgical centers are expected to grow at a 9.25% CAGR through 2031.

- By geography, North America dominated with 35.02% share in 2025, while Asia-Pacific is projected to log the fastest 8.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Postpartum Hemorrhage Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vacuum-Induced Hemorrhage-Control Devices Gain FDA & EU Approvals | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Reimbursement Expansion For Bakri/EBB Balloons In EU & U.S. | +0.8% | North America & Europe | Short term (≤ 2 years) |

| WHO-Backed Roll-Out Of Low-Cost Condom-UBT Kits In LMICs | +0.9% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Integration Of AI-Based PPH Risk-Scoring Into EHR Platforms | +1.1% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Hospital ESG Mandates Favour Reusable NASG Garments | +0.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Climate-Resilient Cold-Chain Gaps Spur Demand For Pre-Filled Heat-Stable Oxytocin Devices | +0.6% | Sub-Saharan Africa, South Asia, rural regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vacuum-Induced Hemorrhage-Control Devices Gain FDA & EU Approvals

Regulators in both the United States and the European Union have shortened review cycles for vacuum-induced systems, turning a formerly experimental concept into a mainstream alternative that complements or replaces balloon tamponade. The FDA’s 510(k) pathway now admits designs that incorporate closed-loop pressure sensors and automatic safety valves, reassuring clinicians about tissue-trauma risks and pushing adoption across large obstetric units. Parallel alignment under the EU Medical Device Regulation has reduced average CE-marking time from 18–24 months to 8–12 months, amplifying first-mover advantages for firms able to furnish randomized-trial evidence. Hospital technology-assessment committees weigh these data alongside cost-of-care metrics, often finding shorter procedure times and lower transfusion rates relative to balloon techniques. The resulting procurement decisions cascade through group-purchasing organizations, expanding addressable volumes and strengthening the overall postpartum hemorrhage devices market.

Reimbursement Expansion for Bakri/EBB Balloons in EU & U.S.

Coverage decisions issued in 2024 eliminated a long-standing financial hurdle for intrauterine balloons. Medicare now reimburses prophylactic as well as emergency use, turning the device from a cost center into a revenue-compatible intervention for hospitals. Major European payers, led by Germany’s statutory insurers and the U.K.’s NHS, have mirrored this stance with procedure fees ranging EUR 200–450 (USD 210–475) per case. Commercial insurers in the United States now cover 78 % of eligible deliveries, creating predictable revenue streams that justify staff-training budgets and inventory build-ups. Device makers exploit this policy tailwind with outcome-based contracting, placing capital equipment at no upfront cost in exchange for per-procedure payments. Such models further cement the postpartum hemorrhage devices market in hospital formularies[1]CooperSurgical Product Team, “Bakri Balloon with Rapid Instillation Components,” coopersurgical.com.

WHO-Backed Roll-Out of Low-Cost Condom-UBT Kits in LMICs

The World Health Organization’s distribution of USD 5 condom-based uterine balloon tamponade kits across 47 low-income and middle-income countries dramatically widens treatment availability. Randomized field studies conducted in 12 nations reported 89 % hemorrhage-control efficacy when kits are applied by trained midwives. Localized manufacturing partnerships reduce dependency on imported medical devices and retain economic spillovers inside host countries. WHO’s accompanying competency-based training modules accelerate skills transfer, allowing task-shifted cadres such as community health workers to deploy the kits confidently. As a result, rural facilities that previously lacked any advanced intervention can now avert hysterectomies and transfusions, creating a bottom-up expansion vector for the postpartum hemorrhage devices market.

Integration of AI-Based PPH Risk-Scoring into EHR Platforms

Machine-learning models that ingest maternal vitals, obstetric histories and in-labor signals are now embedded within mainstream EHR suites. Early-warning scores surface 30 minutes before overt bleeding, giving labor teams a window to stage tamponade devices or prepare uterotonics. Health systems integrating these modules report 23 % fewer severe hemorrhage episodes and 31 % fewer emergency hysterectomies, translating into lower intensive-care occupancy and shorter postpartum stays. Seamless data-flow inside the EHR avoids the standalone-device learning curve, speeding clinician acceptance. Compliance with HIPAA and GDPR frameworks addresses data-security objections, allowing vendors to scale internationally without code rewrites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device Sticker-Price Greater Than USD 900 Limits Uptake In Tier-2 Hospitals | -0.7% | Global, particularly pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage Of PPH-Trained Obstetricians In Rural Regions | -0.9% | Rural areas globally, acute in Sub-Saharan Africa & rural U.S. | Long term (≥ 4 years) |

| Regulatory Ambiguity On Classification Of Hybrid Drug-Device Injectors | -0.3% | Global, with variations by regulatory jurisdiction | Medium term (2-4 years) |

| Data-Privacy Concerns Around AI Uterine-Imaging Tools | -0.4% | Developed markets with strict data protection laws | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device Sticker-Price Greater Than USD 900 Limits Uptake in Tier-2 Hospitals

Mid-tier facilities typically allocate device budgets 18–24 months in advance and require demonstrated utilization of at least 15 cases per month to meet return-on-investment thresholds. Premium systems priced beyond USD 900 frequently miss this benchmark, confining their penetration to high-volume urban centers. Leasing and rental programs attempt to distribute costs but often raise total ownership expenses because of bundled maintenance fees. The resulting two-tiered technology landscape leaves rural communities dependent on lower-cost balloon kits that may lack advanced safety features such as pressure sensors. This dynamic slows diffusion and dampens the postpartum hemorrhage devices market trajectory in sizeable yet budget-constrained segments.

Shortage of PPH-Trained Obstetricians in Rural Regions

Forty-six percent of U.S. counties have no practicing obstetrician-gynecologist, a shortage that mirrors physician-density gaps in parts of South America, Africa and Asia. Training requirements for advanced hemorrhage devices span 8–12 hours of hands-on instruction plus periodic competency audits—time commitments rural practitioners struggle to accommodate. Tele-mentoring initiatives and expanded midwife scopes of practice partly mitigate the gap, but regulatory caps in many jurisdictions inhibit non-physician deployment of higher-risk devices. This human-resource constraint directly curtails installation volumes, moderating postpartum hemorrhage devices market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: AI-Enabled Tools Drive Innovation

Uterine tamponade devices anchored 39.92 % of the postpartum hemorrhage devices market in 2025 on the strength of entrenched clinical protocols and favorable reimbursement. Balloon systems, including Bakri and EBB variants, dominate due to broad obstetric training and decades of outcome data. Vacuum-induced versions are expanding share after recent 510(k) clearances demonstrated shorter intervention times and reduced transfusion requirements. Non-pneumatic anti-shock garments supply a rapid-stabilization option in pre-hospital settings, whereas heat-stable oxytocin injectors plug pharmacologic gaps where cold-chain reliability is low. The postpartum hemorrhage devices market size attached to balloon products is projected to expand at a 4.05% CAGR through 2031 as tender volumes grow in government facilities.

AI-enabled detection platforms record a 11.72% CAGR, the highest among all product lines, because predictive analytics align with payer incentives that reward avoided complications. Vendors bundle algorithmic risk scores with cloud-based dashboards, subscription support and periodic model retraining. Hospitals that integrate these modules into obstetric EHR workflows report procedure-related cost reductions that offset licensing fees. Topical hemostatic sealants occupy a surgical adjunct niche, often packaged alongside cesarean-section kits. Future product roadmaps point toward unified platforms that combine monitoring, mechanical intervention and drug delivery, indicating that the postpartum hemorrhage devices market will increasingly favor integrated ecosystems over single-purpose devices.

By End User: ASCs Challenge Hospital Dominance

Hospitals commanded 67.35 % of postpartum hemorrhage devices market share in 2025 because comprehensive infrastructure and established supply-chain contracts facilitate swift technology adoption. Academic medical centers drive early trials and skills dissemination, while tertiary hospitals act as referral hubs for high-risk deliveries. Community hospitals, under reimbursement pressure, favor mid-priced balloon options that balance efficacy with budget discipline. The postpartum hemorrhage devices market size generated by hospitals is expected to expand at a 4.45% CAGR, paced by replacement cycles and guideline-driven updates.

Ambulatory surgical centers enjoy a 9.25% CAGR because outpatient deliveries align with value-based care economics. These facilities leverage lower staffing overhead and streamlined credentialing to deploy novel devices without lengthy committee approvals. Firms court ASCs with pay-per-use models and compact consoles tailored to limited floor space. Homebirth and community health providers form an emergent segment catalyzed by WHO community-midwifery programs. Device miniaturization and improved training modules allow certain balloon systems and NASGs to migrate safely into these environments, broadening the postpartum hemorrhage devices market beyond hospital walls.

Geography Analysis

North America retained 35.02 % of revenue in 2025, supported by dense insurance coverage, rapid regulatory clearance and robust clinical-trial infrastructure. Medicare’s broad reimbursement of prophylactic balloon use removes financial friction, while private payers follow established coverage determinations. Large group-purchasing organizations negotiate volume discounts, boosting unit throughput. Academic consortia continuously publish peer-reviewed outcome studies, reinforcing evidence-based procurement. Provincial formularies in Canada echo U.S. trends, creating continent-wide homogeneity that accelerates technology diffusion and solidifies the postpartum hemorrhage devices market.

Asia-Pacific is the fastest-growing territory at 8.28% CAGR. China’s Healthy China 2030 agenda earmarks substantial provincial outlays for maternal-mortality reduction, driving high-volume procurement of balloon and NASG systems. India’s National Health Mission allocated INR 192 billion (USD 2.3 billion) toward obstetric-care upgrades in 2024, part of which finances AI-infused monitoring pilots across district hospitals. ASEAN regulatory harmonization enables simultaneous device launches in Malaysia, Indonesia and Thailand, providing economies of scale that accelerate price erosion and broaden access. As disposable incomes rise and urban birth volumes increase, the postpartum hemorrhage devices market embeds deeper into private obstetric chains that cater to middle-class families.

Europe records steady mid-single-digit expansion under the EU Medical Device Regulation’s tightened but harmonized compliance regime. Nordic nations lead per-capita adoption of AI-risk-scoring tools given their high EHR digitization rates. Central-and-Eastern Europe relies heavily on EU cohesion funds to refresh equipment lines, creating clustered tender opportunities for mid-tier manufacturers. The Middle East and Africa offer long-run upside sparked by sovereign investment in maternity-hospital buildouts and WHO-sponsored training programs. South America’s Mercosur tariff reductions ease cross-border device shipment, and expanding private insurance coverage in Brazil and Mexico underwrites elective prophylactic use. Collectively, these trends extend the geographic footprint of the postpartum hemorrhage devices market.

Competitive Landscape

Market concentration is moderate, with the five leading brands controlling significant global revenue. Incumbents pursue vertical integration to bind hardware, software and consumables into subscription-laden ecosystems. BD’s USD 4.2 billion acquisition of Edwards Lifesciences’ critical-care assets underscores the premium placed on data-driven decision support that can layer onto hardware fleets[3]BD Investor Relations, “BD Announces Intent to Separate Biosciences and Diagnostic Solutions Business,” investors.bd.com. CooperSurgical focuses on iterative improvements to its Bakri balloon, adding rapid-instillation components that trim placement time. Samsung’s acquisition of ultrasound-AI developer Sonio in 2024 positions the conglomerate to embed predictive capabilities into imaging consoles, potentially challenging standalone AI vendors.

Challenger companies exploit gaps in price-sensitive emerging markets by offering low-cost balloon kits bundled with remote-training apps. Outcome-based contracts emerge as differentiators; vendors absorb device costs upfront and charge providers only when specific quality benchmarks—such as hemorrhage-related transfusion avoidance—are met. Telehealth-enabled specialists supervise midwives in real time during complicated deliveries, enabling disruptive entrants to bypass traditional hospital gatekeepers and capture share in under-served rural zones.

Technology convergence blurs categorical lines, bringing imaging, predictive analytics and mechanical intervention into single platforms. Firms able to demonstrate closed-loop hemorrhage management—from early risk detection to definitive uterine-tamponade—create switching costs that lock in customers for multiyear cycles. Data-interoperability standards such as HL7 FHIR are thus battlefield terrain where alliances and joint ventures spring up. The net effect is a dynamic yet disciplined postpartum hemorrhage devices market where brand credibility, clinical-evidence depth and data-integration proficiency dictate competitive outcomes.

Postpartum Hemorrhage Devices Industry Leaders

Cook Medical

Utah Medical Products, Inc.

Organon & Co.

Becton, Dickinson and Company

Laborie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Willow acquired British femtech company Elvie to consolidate wearable maternal-health technology portfolios and resolve pending intellectual-property litigation.

- September 2024: Organon Canada introduced the JADA System nationwide, extending controlled vacuum aspiration into routine obstetric protocols under the country’s universal.

Global Postpartum Hemorrhage Devices Market Report Scope

As per the scope of the report, Postpartum hemorrhage devices are a type of treatment device when there is significant vaginal bleeding that occurs after a baby is born. Postpartum hemorrhage is a dangerous illness that can result in death. Dizziness, faintness, and blurred vision are further symptoms of postpartum bleeding. Postpartum hemorrhage can develop after delivery or up to 12 weeks after giving birth. Early detection and prompt treatment with proper devices can lead to a full recovery. The postpartum hemorrhage devices market is segmented by Product Type (Non-Pneumatic Anti-Shock Garment, Prefilled Injection System, Uterine Tamponade Devices), End Users (Hospitals, Clinics & Other End Users), Geography (North America, Europe, Asia-Pacific, Middle East and Africa and South Africa). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Uterine Tamponade Devices | Balloon Tamponade |

| Vacuum-Induced Devices | |

| Non-Pneumatic Anti-Shock Garments (NASG) | |

| Prefilled Uterotonic Injection Systems | |

| Topical Hemostatic & Sealant Applicators | |

| AI-enabled Early Detection & Monitoring Tools |

| Hospitals |

| Maternity Clinics & Birthing Centers |

| Ambulatory Surgical Centers |

| Homebirth & Community Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Uterine Tamponade Devices | Balloon Tamponade |

| Vacuum-Induced Devices | ||

| Non-Pneumatic Anti-Shock Garments (NASG) | ||

| Prefilled Uterotonic Injection Systems | ||

| Topical Hemostatic & Sealant Applicators | ||

| AI-enabled Early Detection & Monitoring Tools | ||

| By End User | Hospitals | |

| Maternity Clinics & Birthing Centers | ||

| Ambulatory Surgical Centers | ||

| Homebirth & Community Healthcare Providers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Why is the postpartum hemorrhage devices market expected to grow at a 5.05% CAGR?

Growth reflects faster regulatory approvals, broader reimbursement and rising adoption of AI-enabled early-warning systems that shift care from reactive to preventive.

Which product segment leads the postpartum hemorrhage devices market?

Uterine tamponade devices held 39.92% market share in 2025, driven by well-established clinical protocols and payer coverage.

What region shows the fastest growth in postpartum hemorrhage device demand?

Asia-Pacific posts an 8.28% CAGR to 2031 thanks to government-funded maternal-health programs and expanding private hospital networks.

How are ambulatory surgical centers impacting industry dynamics?

ASCs record a 9.25% CAGR as outpatient delivery models gain favor, encouraging device makers to design compact, cost-efficient systems.

What role does artificial intelligence play in postpartum hemorrhage management?

AI-based risk-scoring embedded in EHR platforms flags high-risk patients 30 minutes before bleeding begins, enabling early intervention and reducing severe cases by 23%.

Page last updated on: