Blood Transfusion Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

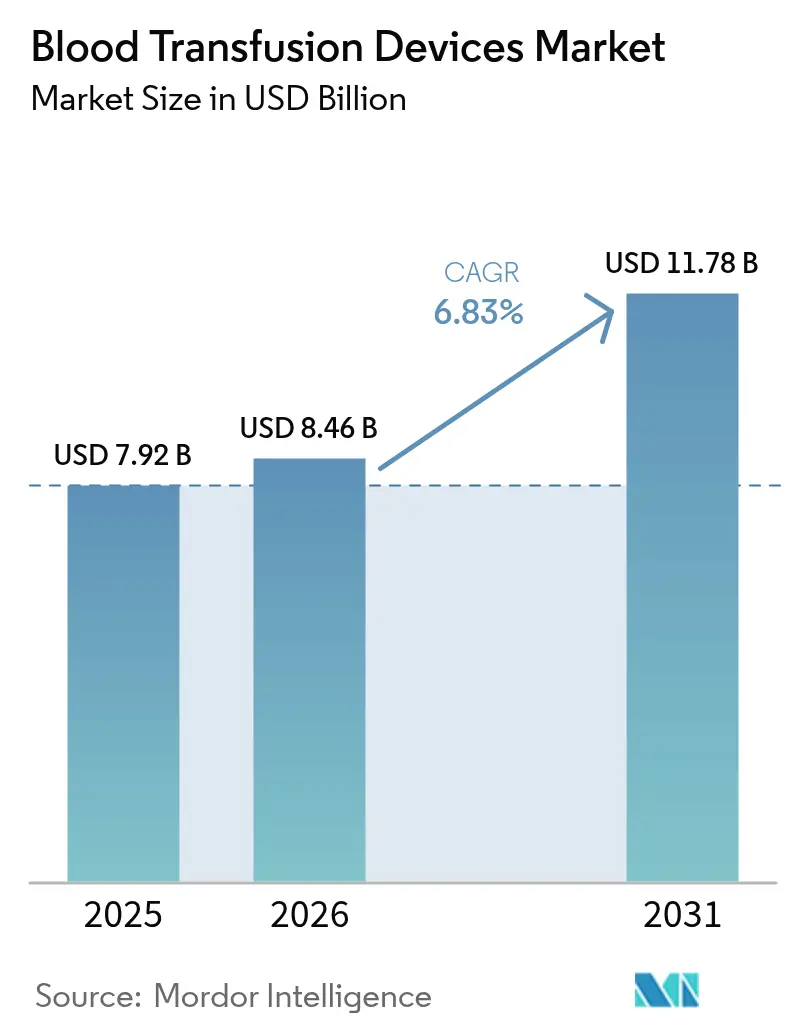

| Market Size (2026) | USD 8.46 Billion |

| Market Size (2031) | USD 11.78 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

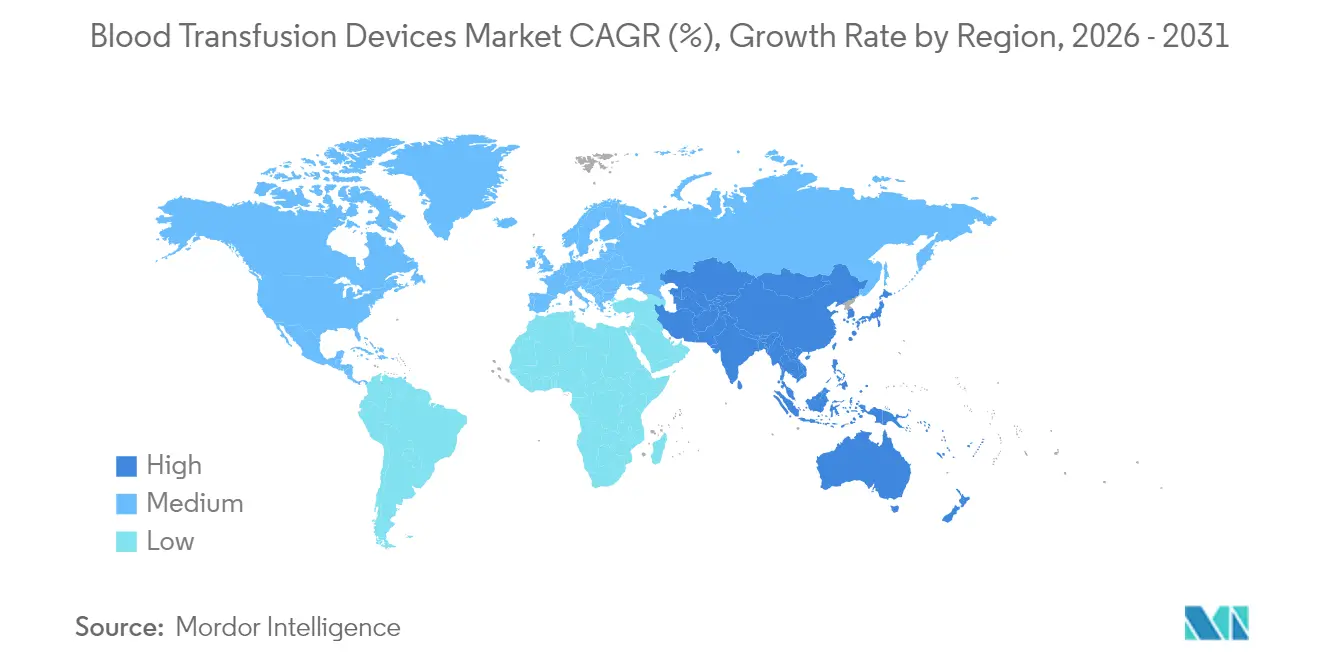

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

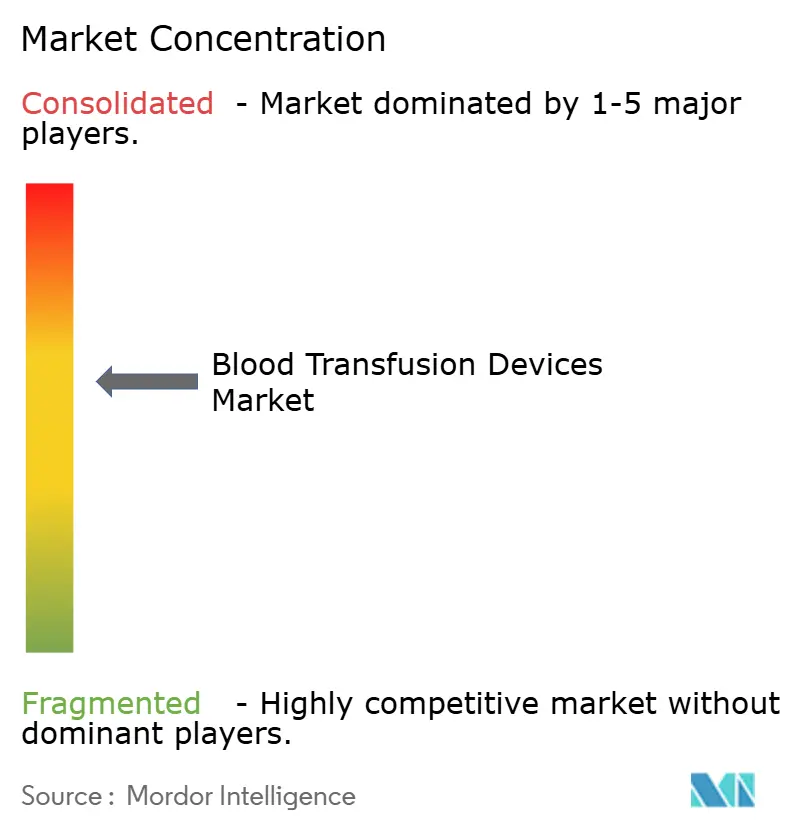

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Transfusion Devices Market Analysis by Mordor Intelligence

Blood transfusion devices market size in 2026 is estimated at USD 8.46 billion, growing from 2025 value of USD 7.92 billion with 2031 projections showing USD 11.78 billion, growing at 6.83% CAGR over 2026-2031. Steady demand arises from higher surgical procedure volumes, a growing burden of hematological disorders, and rapid uptake of pathogen-reduction systems that neutralize emerging pathogens. Digital inventory analytics are lowering wastage, and government-backed blood-safety programs are expanding in emerging economies. Automation is rising as healthcare providers seek labor savings, while patient blood-management initiatives encourage optimized transfusion practices that, in turn, spur equipment upgrades. Although stringent regulations and cold-chain expenses weigh on profitability, industry stakeholders continue launching integrated solutions that enhance safety, efficiency, and traceability across the transfusion workflow.

Key Report Takeaways

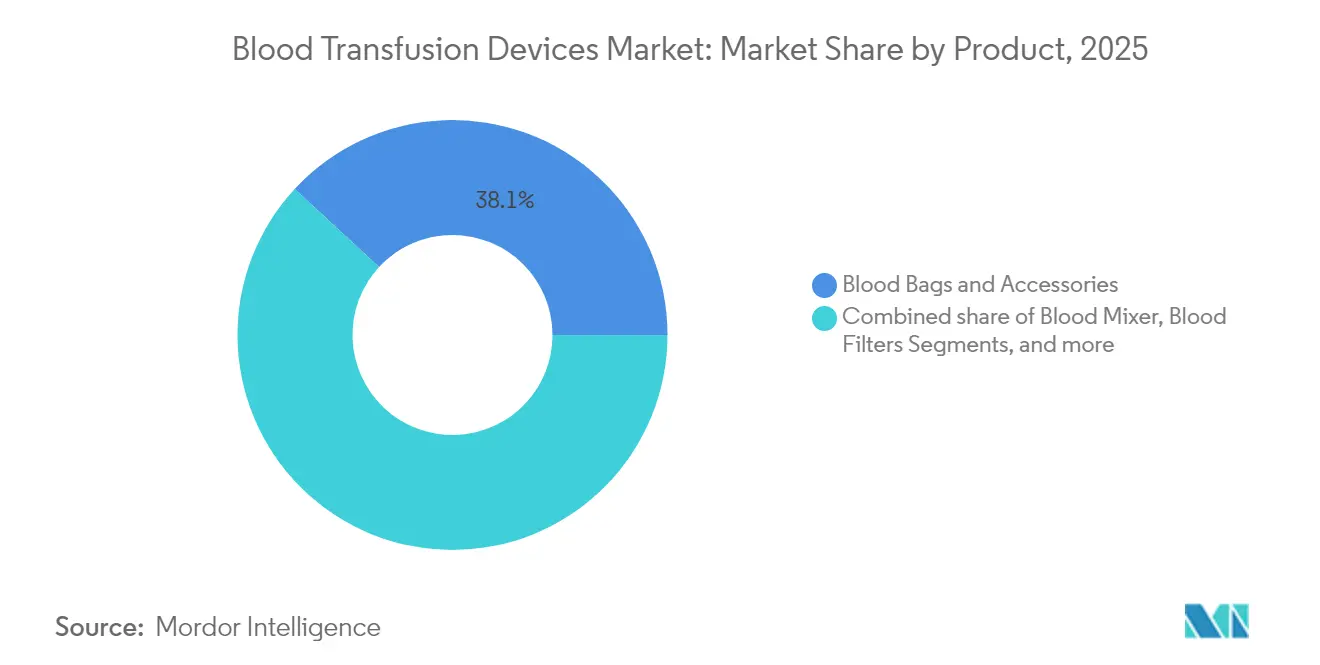

- By product category, Blood Bags & Accessories led with 38.12% of blood transfusion devices market share in 2025, whereas Pathogen Reduction Systems are forecast to advance at a 8.92% CAGR to 2031.

- By technology, Manual/Conventional platforms held 54.10% share of the blood transfusion devices market size in 2025, while Automated/Integrated solutions are projected to expand at 8.41% through 2031.

- By application, Collection accounted for 43.15% of the blood transfusion devices market size in 2025; Transfusion & Administration is growing the fastest at 9.02% CAGR to 2031.

- By end-user, Hospitals captured 47.60% revenue share in 2025; Ambulatory Surgical Centres are set to rise at a 9.88% CAGR between 2026-2031.

- By geography, North America dominated with 40.10% blood transfusion devices market share in 2025, while Asia-Pacific is poised for the quickest growth at an 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Transfusion Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes | +1.8% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Growing prevalence of hematological disorders | +1.2% | APAC, emerging markets | Long term (≥ 4 years) |

| Rapid technological advances in transfusion equipment | +1.5% | North America, EU, accelerating APAC | Short term (≤ 2 years) |

| Government support for blood-safety initiatives | +0.9% | APAC core, MEA and Latin America spill-over | Medium term (2-4 years) |

| Deployment of patient blood-management programs | +0.7% | North America, EU, expanding APAC | Medium term (2-4 years) |

| Digital inventory analytics integration | +0.6% | Early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes Worldwide

Global surgical demand continues to climb, with the World Health Organization projecting a 25% increase by 2030[1]World Health Organization, “Global Surgery and Blood Safety – 2025 Update,” who.int. Cardiovascular, orthopedic, and oncologic procedures consume the most blood components, making automated processing equipment essential in high-volume hospitals. Terumo’s Reveos system cuts manual steps by 65% and improves component consistency, illustrating how efficiency gains align with rising case loads. Stable procedure growth underpins equipment replacement cycles, though strained donor pools still challenge overall supply chains.

Growing Prevalence of Hematological Disorders

Greater life expectancy and better diagnostics reveal more cases of sickle cell disease, thalassemia, and hematologic cancers. Regular transfusions remain standard therapy, sustaining predictable equipment demand. Novel gene therapies temporarily lift transfusion requirements during pre-conditioning regimens, pushing apheresis device usage upward. Safety concerns for immunocompromised patients further accelerate pathogen-reduction adoption.

Rapid Technological Advancements in Transfusion Equipment

Pathogen-reduction platforms such as INTERCEPT, MIRASOL, and THERAFLEX add a critical layer of safety by inactivating viruses, bacteria, and parasites beyond current screening capabilities. Artificial-intelligence tools optimize inventory, while robotic phlebotomy reaches 87% first-stick accuracy, easing labor shortages[2]AABB, “AI and Robotic Automation in Modern Blood Banking,” aabb.org. Such convergence of automation, analytics, and robotics reshapes equipment expectations toward fully integrated solutions.

Expanding Government Support for Blood-Safety Initiatives in Emerging Markets

China’s “Healthy China 2030” plan underwrites domestic production of advanced collection systems, prompting Terumo to invest USD 15 million in local manufacturing. The EU’s Regulation (EU) 2024/1938 sets harmonized standards that stimulate adoption of next-generation devices across member states[3]European Commission, “Regulation (EU) 2024/1938 on Substances of Human Origin,” ec.europa.eu. Subsidized procurement lowers entry barriers for hospitals in Asia and Latin America, widening the install base for pathogen-reduction and automation platforms.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory and quality compliance requirements | -1.4% | Global, most pronounced in North America & EU | Long term (≥ 4 years) |

| High operational costs of blood collection and cold chain | -1.1% | Global, particularly challenging in emerging markets | Medium term (2-4 years) |

| Sustainability pressures on PVC-based blood-bag materials | -0.6% | Global, driven by North America & EU regulatory attention | Medium term (2-4 years) |

| Shrinking eligible donor base due to demographic shifts | -0.8% | North America & Europe leading, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Quality Compliance Requirements

The FDA’s 2025 agenda lists five new blood-component guidances, while Europe’s SoHO rule revamps compliance reporting. The pivot away from DEHP introduces costly material validation cycles. Smaller OEMs face submission expenses topping USD 2 million for complex devices, extending development timelines by up to five years and tilting competitive advantage toward firms with deep regulatory resources.

High Operational Costs of Blood Collection and Cold Chain

Automated processors can cost USD 500,000–2 million per site, a hurdle for mid-sized hospitals. Cold-chain energy accounts for up to 20% of blood-bank budgets, and fuel price shocks since 2022 have lifted distribution costs by 30%. Rural facilities struggle with grid reliability, amplifying wastage from temperature excursions. Staff turnover surpassing 25% in some regions further elevates training costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Pathogen Reduction Systems Drive Safety Innovation

Blood Bags & Accessories led the segment with 38.12% blood transfusion devices market share in 2025, supported by universal demand across collection sites. The blood transfusion devices market size for Blood Bags & Accessories is expected to advance steadily through 2031 as procedure volumes increase. Pathogen-Reduction Systems, posting the quickest 8.92% CAGR, align with regulatory pushes for proactive safety and have now reached over 100 global blood centers.

The segment’s second growth driver involves automated component separators that enhance platelet quality while trimming processing time. Leukoreduction filters are now mandated in most developed markets, creating incremental replacement demand. Blood-warming devices focus on microprocessor accuracy and electronic health-record interoperability, while consumable kits face margin compression due to group-purchasing contracts.

By Technology: Automation Accelerates Despite Manual Dominance

Manual/Conventional platforms retained 54.10% share of the blood transfusion devices market in 2025, reflecting affordability for low-resource settings. Yet Automated/Integrated systems are gaining ground at 8.41% CAGR. The blood transfusion devices market size for Automated/Integrated solutions is rising as labor constraints and error-reduction targets encourage adoption. Terumo’s Reveos illustrates ROI: one device cuts platelet processing steps from 26 to 9 and yields more platelets per donation.

Artificial-intelligence modules embedded in automation suites enable predictive maintenance and quality analytics, reducing downtime. Interfaces that connect with hospital information systems improve traceability reporting and compliance. As funding models evolve, manual devices are expected to persist in lower-volume centers, while automation becomes standard in regional hubs.

By Application: Transfusion & Administration Gains Sophistication

Collection activities accounted for 43.15% share in 2025, anchoring demand for phlebotomy and storage products. The blood transfusion devices market size for Collection equipment should expand steadily with rising procedure counts, though incremental growth is moderating. Transfusion & Administration posts the highest 9.02% CAGR as smart pumps and bedside verification tools gain widespread use.

Integration of barcode and biometric confirmation at the bedside reduces mismatch risks. Processing & Separation benefits from broader use of automated platforms that standardize component quality. Storage & Preservation innovations center on cloud-connected refrigerators that alert staff before temperature deviations, helping to cut wastage.

By End-user: Ambulatory Centres Challenge Hospital Dominance

Hospitals absorbed 47.60% of overall revenue in 2025, a result of complex surgery volumes and in-house blood banks. Ambulatory Surgical Centres, rising at 9.88% CAGR, drive demand for compact, user-friendly devices. The blood transfusion devices industry must therefore tailor product designs to outpatient facilities where space and staffing differ from tertiary hospitals.

Blood banks are consolidating operations to leverage economies of scale, investing in pathogen-reduction and high-throughput separators. Specialty clinics and research labs contribute modest growth as cell therapies expand, requiring precise apheresis and storage capabilities.

Geography Analysis

North America commanded 40.10% of global revenue in 2025 thanks to stringent oversight, early pathogen-reduction adoption, and high per-patient spending. The FDA’s active guidance pipeline shapes global best practice, and suppliers benefit from predictable reimbursement. Yet donor shortages remain acute: the American Red Cross cites a 40% decline over two decades, and extreme weather led to 19,000 canceled drives in 2024 alone. Investment in automated processing and recruitment campaigns aims to stabilize supply.

Asia-Pacific is the fastest-growing region at an 8.19% CAGR through 2031. China’s localization strategy encourages domestic production of advanced systems, while Japan’s artificial-blood trials position the region at the innovation frontier. Rising surgical volumes, expanding insurance coverage, and government-subsidized safety upgrades underpin sustained equipment demand from India to Southeast Asia.

Europe sustains a sizable install base and will implement the SoHO framework by 2027, harmonizing standards and stimulating uptake of DEHP-free bags and pathogen-reduction across member states. Middle East & Africa and South America trail in total revenue but exhibit strong demand fundamentals tied to urbanization and non-communicable disease treatment expansion.

Regulatory Landscape

Blood transfusion devices sit under medical-device rules and blood-safety oversight, which tends to push manufacturers toward tighter quality systems and postmarket surveillance. In the United States, FDA requirements such as Medical Device Reporting under 21 CFR Part 803 govern mandatory adverse-event reporting by manufacturers, importers, and user facilities, while device classification frameworks cover blood-establishment software and related accessories with defined special controls.

In Europe, the Medical Device Regulation (EU) 2017/745 increases expectations around technical documentation and conformity assessment for device makers supplying blood establishments, alongside classification guidance from the Medical Device Coordination Group (MDCG 2021-24). A specific signal for MDR transition progress is Fresenius Kabi AG receiving an EU Technical Documentation Assessment Certificate for its Blood Donation Systems (Compoflex, CompoFlow, Composelect), effective March 26, 2026. Standards also feed into global compliance and purchasing specifications, including ISO 13485 quality management requirements and ISO 1135-5:2025 requirements for single-use transfusion sets designed for use with pressure infusion apparatus.

Competitive Landscape

Market rivalry is moderate, with the top six suppliers accounting for about 55% of global revenue. Becton Dickinson leverages its Medication Delivery franchise to bundle collection devices, reporting USD 5.2 billion in Q1 FY2025 revenue. Terumo extends vertically from collection to cell therapy, adding a Global Therapy Innovations unit in late 2024. Haemonetics sharpened its hospital focus by divesting whole-blood assets for USD 67.8 million to GVS in January 2025.

Strategic acquisitions deepen portfolios: BD agreed to split its Biosciences and Diagnostics arm to become a pure-play MedTech vendor, while Teleflex paid EUR 760 million for BIOTRONIK’s vascular line in May 2025. Automation partnerships, such as the 10-year Sanquin–Terumo pact, secure long-term equipment placements and recurring consumables sales. Competitive advantage now hinges on regulatory expertise, digital integration, and the ability to finance multi-year clinical programs needed for next-generation safety technologies.

Blood Transfusion Devices Industry Leaders

Becton Dickinson and Company

Terumo Corporation

Haemonetics Corporation

Grifols SA

Fresenius Kabi AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clear whitespace is appearing around end-to-end workflow integration, as blood centers and hospitals connect device fleets with inventory, traceability, and donor-to-patient data flows. One concrete signal is InVita Healthcare Technologies acquiring MAK-SYSTEM in July 2026 to build a connected blood management ecosystem that integrates the eProgesa platform for blood lifecycle management, aligning software with device utilization and compliance documentation. Similar demand drivers are showing up in automated processing, where suppliers are positioning integrated platforms to reduce manual steps and standardize workflows across high-throughput labs.

Product innovation is also addressing cold-chain and shelf-life constraints that affect operating cost and wastage. In 2026, Velico Medical installed the first veliPod containerized spray-dried plasma manufacturing system at the French Armed Forces Blood Transfusion Centre (CTSA) and Versiti installed next-generation spray-dried plasma equipment to support room-temperature stable plasma for emergency use. For red blood cell storage, Hemanext announced a production partnership with OneBlood in July 2026 to expand adoption of oxygen-controlled RBC storage (Hemanext ONE) across multiple processing facilities, pointing to continued investment in storage technologies that can improve component quality management and logistics efficiency.

Recent Industry Developments

- April 2026: Becton, Dickinson and Company commercially launched the BD CentroVena One Insertion System after U.S. FDA 510(k) clearance and acceptance into the FDA Safer Technologies Program. The all-in-one central venous catheter insertion approach streamlines a critical step in transfusion and acute-care workflows, strengthening BD's positioning in vascular access devices used alongside blood administration.

- January 2025: Terumo Corporation reported that Carter BloodCare completed the first U.S. deployment of the Reveos Automated Blood Processing System together with the Lumia Software Platform. The combination of automation and software supports standardized component processing and traceability, reinforcing the shift from manual workflows toward integrated systems in blood centers.

- October 2024: Terumo Corporation launched the Reveos Automated Blood Processing System in the United States in collaboration with Blood Centers of America, with a debut at Carter BloodCare. The U.S. rollout expanded reference sites for automated whole-blood processing, accelerating adoption of higher-throughput processing platforms and associated consumables.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices and related consumables used to safely collect, store, prepare, and administer whole blood and blood components in healthcare settings, including hospital and blood bank transfusion workflows.

Scope exclusions: Blood transfusion diagnostics (such as screening reagents and cross-matching analyzers) and stand-alone IV infusion pumps are not counted in this market.

Segmentation Overview

- By Product

- Blood Bags & Accessories

- Blood Mixer

- Blood Filters

- Blood Component Separator

- Apheresis Device

- Pathogen Reduction System

- Blood & Fluid Warmer

- Blood Collection & Processing Consumables

- Other Products

- By Technology

- Manual / Conventional

- Automated / Integrated

- By Application

- Collection

- Processing & Separation

- Storage & Preservation

- Transfusion & Administration

- By End-user

- Hospitals

- Ambulatory Surgical Centres

- Blood Banks

- Other End-users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map the transfusion workflow and list the device categories that directly touch collection, component separation, storage, warming, and administration. We relied on public sources such as the US FDA device databases, CDC publications, WHO blood safety resources, and NHS Blood and Transplant type materials to understand safety requirements and standard practices.

To anchor demand signals, we also reviewed government and multilateral statistics on blood donation and usage volumes, along with publications from professional societies and peer-reviewed journals on transfusion rates, component usage patterns, and adverse-event prevention. Company filings, investor presentations, and credible press were used to check product mix changes, pricing direction, and regional expansion. Where needed, paid subscriptions supporting company financials and intelligence, patent landscapes, and shipment-level trade signals were used to cross-check supplier activity and category momentum. These are illustrative sources only, and many other references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were run with a mix of device manufacturers, distributors, blood bank operators, and hospital transfusion and procurement stakeholders to confirm what gets purchased, how frequently it is replaced, and what drives switching. Respondent input was also used to validate regional differences in transfusion volumes, the split between whole blood and components, and the pace of adoption for items such as filters, warmers, and pathogen-reduction related systems.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | APAC: 47% |

| Mid tier: 55% | Functional/Unit leaders: 29% | EMEA: 33% |

| Smaller Players: 18% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up hybrid, where transfusion activity and installed-base signals are translated into device and consumable demand, and then validated using selective supplier and channel checks. The top-down path starts from country level blood collection and transfusion volumes, which are converted into demand pools using usage rates for sets, bags, filters, and related components, followed by adjustment for wastage, safety protocol intensity, and care setting mix.

For cross-checks, we use sampled price times volume approximations for high-usage consumables, and we compare these with revenue exposure cues from public financial disclosures and distributor feedback. Key model inputs include blood donation volume trends, transfusion rate per hospital bed, share of component transfusions, adoption of leukoreduction or filtration practices, procedure mix that drives acute transfusion demand, and average selling price movement by device type. When bottom-up data is incomplete for smaller countries or niche categories, gaps are handled through proxy ratios linked to transfusion activity and healthcare spend, and then reviewed with primary experts.

Forecasts lean on scenario analysis, where the base case is shaped by expected blood usage growth, policy push for safer transfusions, and replacement cycles for capital equipment. Assumptions are stress-tested with interview feedback so the final outlook remains explainable with observable indicators.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, such as transfusion volumes, device category penetration, and supplier activity markers, and then checked for sudden jumps that do not match known clinical or policy changes. Variance checks are run across regions and product groups so outliers can be traced back to a clear driver, such as a change in transfusion safety practices or a one-time stocking effect.

Before sign-off, the model is reviewed in multiple steps, including an internal peer review of assumptions, unit conversions, and currency treatment. If gaps remain or a number looks inconsistent, respondents are re-contacted to clarify pricing, usage rates, or category inclusion. Reports are refreshed annually, with interim updates triggered by material events, and a final pre-delivery scan is completed so the shared view reflects the latest available information.

Mordor Intelligence's Blood Transfusion Device Market Size Measured Against Other Published Estimates

Published numbers for this market can look far apart, even when the topic label is the same, because each publisher draws the line around different device groups and then applies different activity indicators and pricing logic. Timing also affects comparability since some estimates are anchored to older base years or are converted using different currency assumptions.

Diagnostic reagents and cross-matching analyzers sit outside Mordor Intelligence's scope, which is one clear reason why some published totals appear larger when they bundle transfusion testing into the same value pool. Other gaps often come from whether stand-alone infusion pumps are counted, how autotransfusion is treated versus routine transfusion sets, and whether the model uses transfusion volumes versus broader hospital purchasing proxies. Differences also show up when pricing is projected using a flat uplift instead of category-specific ASP movement, which we see reflected in buyer and distributor checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.46 B (2026) | |

| Global Consultancy A | USD 6.40 B (2025) | Uses an earlier base year and a narrower surgery-led application lens, which can undercount routine hospital and blood bank consumable throughput and related replacement demand. |

| Industry Publisher B | USD 5.84 B (2025) | Appears to center the model on a limited product list with broad end-user splits, and it is less explicit about workflow-linked usage rates and cross-checks against transfusion activity indicators. |

The comparison mainly shows how scope and activity proxies move the total, especially when transfusion testing, infusion hardware, or limited product baskets are mixed into the same headline. By keeping the inputs tied to transfusion volumes, usage rates, and category-level pricing checks, the estimate stays traceable to steps that can be repeated during updates.

Key Questions Answered in the Report

What is the current value of the blood transfusion devices market?

The market generated USD 8.46 billion in 2026 and is forecast to hit USD 11.78 billion by 2031.

Which region is growing the fastest for blood transfusion devices?

Asia-Pacific is set to expand at an 8.19% CAGR through 2031 thanks to healthcare modernization and government safety programs.

Why are pathogen-reduction systems gaining traction?

They inactivate a broad range of pathogens, closing gaps left by traditional screening and supporting stricter safety regulations.

How is automation influencing blood processing?

Automated systems cut manual steps, reduce errors, and integrate with digital inventory tools, driving an 8.41% CAGR for the technology segment.

What challenges limit market growth?

Stringent regulatory compliance, high capital costs for automation and cold chain, and shrinking donor pools pose headwinds to expansion.

Which end-user segment is rising quickest?

Ambulatory Surgical Centres are the fastest-growing customers, posting a 9.88% CAGR as outpatient procedures increase.

Page last updated on: