U.S. Reprocessed Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

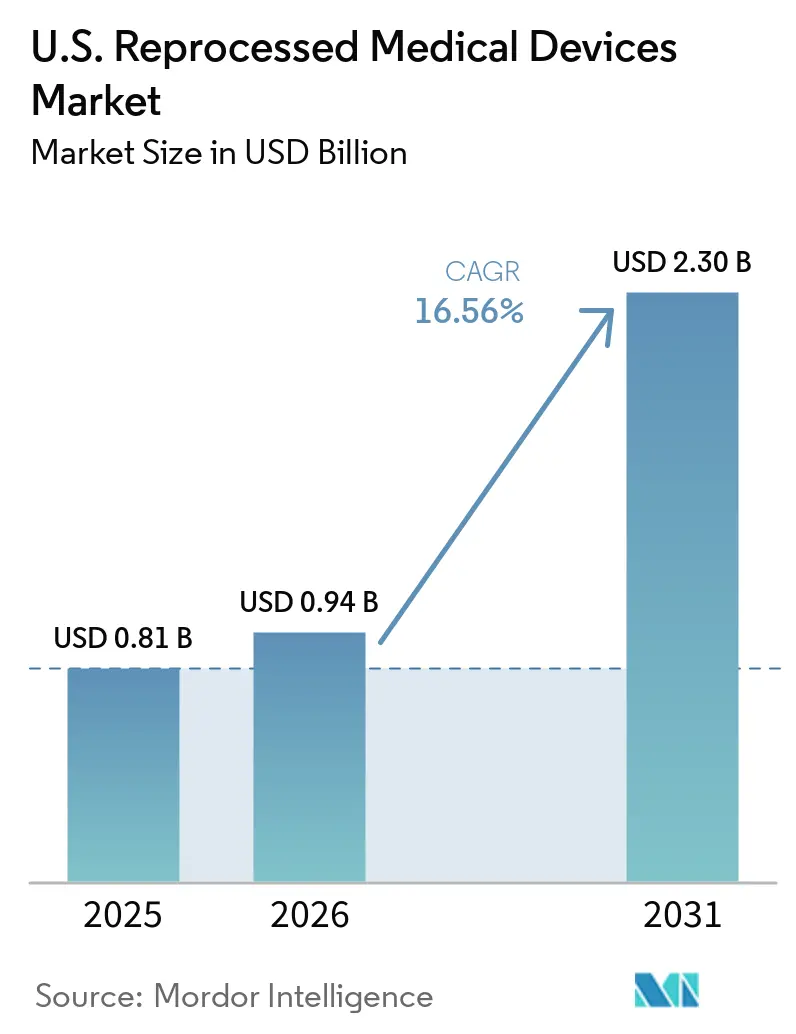

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 2.30 Billion |

| Growth Rate (2026 - 2031) | 16.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Reprocessed Medical Devices Market Analysis by Mordor Intelligence

The U.S. Reprocessed Medical Devices Market size was valued at USD 0.81 billion in 2025 and is estimated to grow from USD 0.94 billion in 2026 to reach USD 2.30 billion by 2031, at a CAGR of 16.56% during the forecast period (2026-2031).

Hospitals in the United States are increasingly integrating reprocessed medical devices into their supply chain strategies. This approach reduces procedure costs, minimizes waste, and improves budget planning across departments. In 2025, AMDR reported that member companies sold 39,387,336 reprocessed single-use devices to 11,458 healthcare facilities, generating USD 495.5 million in hospital savings and reflecting widespread adoption nationwide. The United States reprocessed medical devices market is also benefiting from legal actions against anti-reprocessing practices and expanded FDA clearances, which are increasing the range of devices considered for reuse. Innovative Health noted that favorable court rulings and compliance measures related to electrophysiology catheters are creating opportunities for independent reprocessors in high-value categories.

Key Report Takeaways

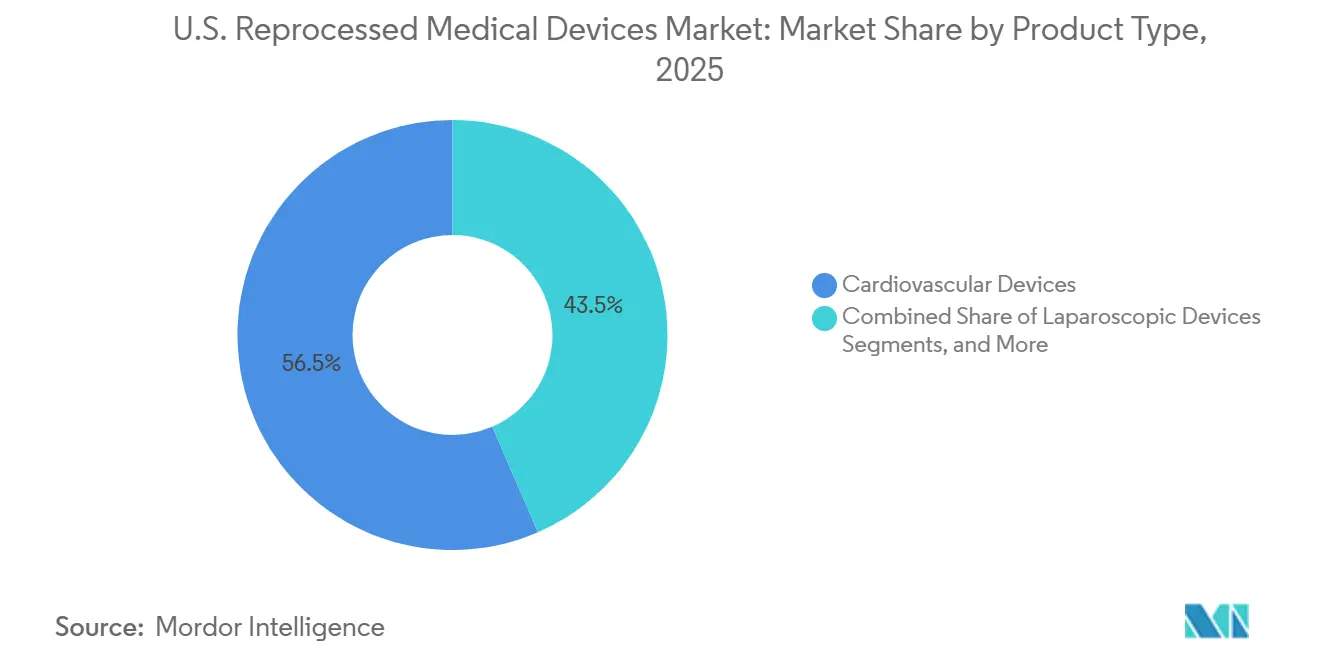

- By product type, cardiovascular devices held 56.50% share in 2025, while laparoscopic devices are projected to grow at a 16.20% CAGR from 2026 to 2031.

- By reprocessing model, third-party and commercial reprocessing captured 84.12% share in 2025, and the same segment is projected to expand at a 16.99% CAGR through 2031.

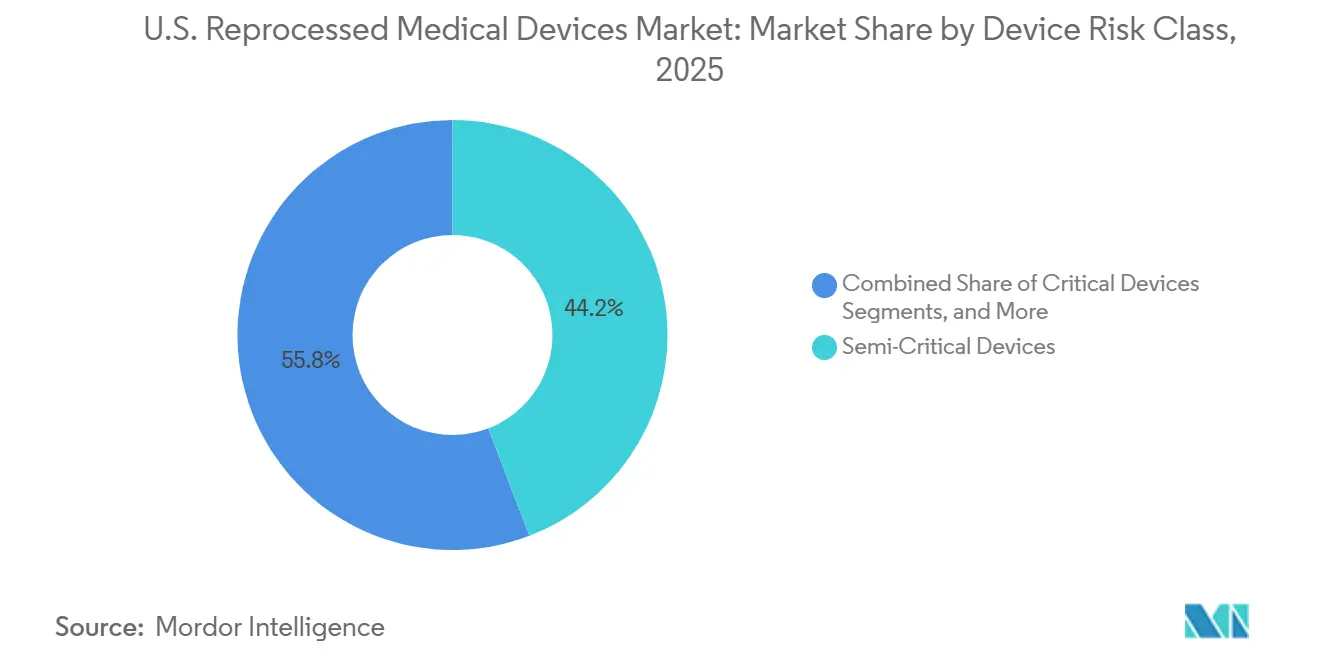

- By device risk class, semi-critical devices led with 44.18% share in 2025, while critical devices are forecasted to record the fastest CAGR at 17.34% during 2026 to 2031.

- By clinical application, cardiology and electrophysiology accounted for 40.25% share in 2025, while gastroenterology is projected to grow at a 17.25% CAGR through 2031.

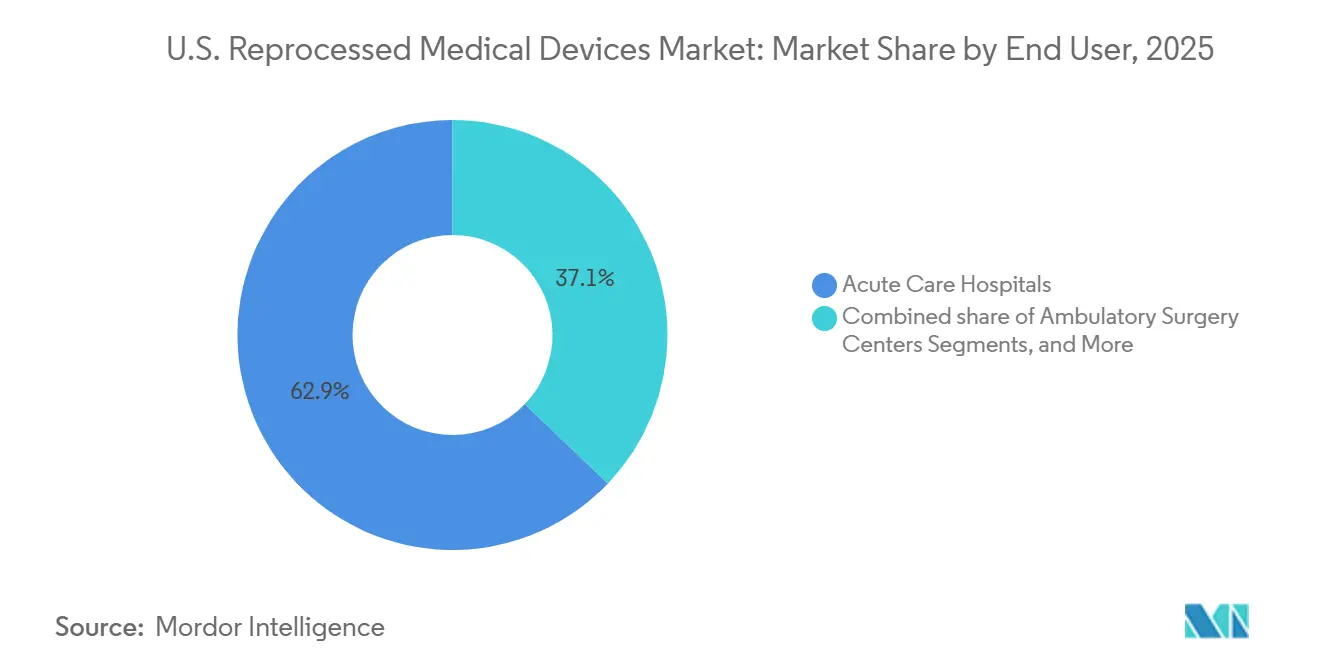

- By end user, acute care hospitals commanded 62.86% share in 2025, while ambulatory surgery centers are forecasted to expand at an 18.90% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Reprocessed Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hospital supply cost containment and recurring per procedure savings | +3.0% | National, most pronounced in Northeastern and Midwestern integrated health systems | Short term (≤ 2 years) |

| Rising cardiovascular and electrophysiology procedure volumes | +2.8% | National, highest procedural density in Northeast, Southeast, and West Coast metro markets | Medium term (2-4 years) |

| Waste reduction and health system decarbonization goals | +2.5% | National, strongest mandate driven adoption in California, New York, and New England states | Medium term (2-4 years) |

| FDA cleared category expansion lifting buyer confidence | +2.0% | National, early adoption concentrated in academic medical centers and large integrated health systems | Medium term (2-4 years) |

| ASC migration increasing demand for lower cost invasive devices | +1.8% | National, most acute in Sun Belt states with rapid ASC facility expansion | Short term (≤ 2 years) |

| Digital traceability strengthening reprocessor selection | +1.2% | National, fastest adoption in large urban health systems with mature EHR infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hospital Supply Cost Containment and Recurring Per-Procedure Savings

Hospital cost pressures remain a key driver in the United States reprocessed medical devices market, as purchasing teams can assess budget impacts on a case-by-case basis rather than during annual reviews. In 2025, AMDR reported that member reprocessors saved hospitals USD 495.5 million, making reprocessing a critical strategy for finance teams under margin pressure. These savings are recurring, as cleared reuse cycles allow repeated cost reductions within the same fiscal period.[1]Association of Medical Device Reprocessors, “Hospitals and Surgical Centers Saved over $495M (€421M), Eliminated the Need for 6.3 Million Gallons of Gasoline, by Using Reprocessed ‘Single-Use’ Medical Devices from AMDR Members in 2025,” AMDR, amdr.org In 2024, Innovative Health noted a 50% increase in electrophysiology labs saving over USD 1 million annually through reprocessing, with average partner lab savings rising 17% due to new FDA clearances. This shift is prompting hospitals to treat reprocessing as a core procurement strategy rather than an optional initiative.

Rising Cardiovascular and Electrophysiology Procedure Volumes

Increasing cardiovascular and electrophysiology procedure volumes are driving the United States reprocessed medical devices market, as these specialties rely heavily on expensive single-use products. Atrial fibrillation procedures have been growing at nearly 17% annually, with device costs reaching USD 2.5 billion annually.[2]Cardinal Health, “Driving Sustainability for U.S. Hospitals,” Cardinal Health Newsroom, newsroom.cardinalhealth.com High case volumes amplify savings, as reprocessing a single intracardiac echo catheter can reduce unit costs from USD 3,500 to USD 1,400–1,750 in high-volume programs. A 49-hospital health system achieved USD 4.9 million in savings over four years while diverting over 19,000 pounds of waste, reinforcing the financial and operational benefits of reprocessing in high-throughput labs.[3]Association of Medical Device Reprocessors, “Hospitals and Surgical Centers Saved over $495M, Eliminated the Need for 6.3 Million Gallons of Gasoline, by Using Reprocessed ‘Single-Use’ Medical Devices from AMDR Members in 2025,” AMDR, amdr.org

Waste Reduction and Health-System Decarbonization Goals

Hospital sustainability goals are accelerating the United States reprocessed medical devices market, with board-level focus on environmental impact. Reprocessing has been shown to reduce greenhouse gas emissions by 41%, cut the carbon footprint of compression sleeves by 40%, and lower waste disposal costs by 90%. AMDR reported that member activities in 2025 eliminated emissions equivalent to 6.38 million gallons of gasoline. The combination of cost savings and waste reduction is increasingly compelling for decision-makers. In 2024, 3,773 healthcare facilities were recognized for sustainability leadership, collectively diverting 5 million pounds of waste, aligning reprocessing with both purchasing and environmental accountability.

FDA-Cleared Category Expansion Lifting Buyer Confidence

Expanding FDA-cleared device categories are boosting buyer confidence in the United States reprocessed medical devices market. Innovative Health achieved its 50th FDA clearance in January 2026, including expanded uses for Abbott’s Agilis NxT Steerable Introducer, averaging one approval every 10 weeks over the past decade. This consistent regulatory pathway reassures procurement teams and supports adoption in categories once considered too complex for reuse. Restore Robotics further strengthened confidence in 2025 by securing clearance for remanufacturing the widely-used da Vinci Xi instrument, demonstrating the potential for reprocessing in previously untapped categories.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| OEN anti reprocessing design and contracting tactics | -1.8% | National, most acute in academic and specialty centers with deep OEM clinical relationships | Medium term (2-4 years) |

| FDA validation and quality system burden | -1.5% | National, disproportionate impact on regional and independent reprocessors outside major metro markets | Long term (≥ 4 years) |

| Clinician perception and value analysis committee friction | -1.2% | National, most persistent in high volume cardiac and orthopedic centers with established OEM clinical ties | Medium term (2-4 years) |

| Low return yield and turnaround complexity for advanced catheters | -1.0% | National, most impactful in cardiology and interventional device categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OEM Anti-Reprocessing Design and Contracting Tactics

In the United States reprocessed medical devices market, original equipment manufacturers (OEMs) leverage their scale and contractual power to hinder the adoption of reprocessed devices, despite the demand for cost-effective solutions. Tactics such as bundling practices, software controls, and selective support create barriers for hospitals seeking reprocessed options. Although legal verdicts against Medtronic and Biosense Webster in 2026 marked a shift in addressing anti-competitive practices, commercial challenges and evolving OEM strategies continue to slow market penetration in high-value device categories.

FDA Validation and Quality-System Burden

Regulatory compliance remains a significant challenge in the United States reprocessed medical devices market, as reprocessors must meet stringent cleaning, sterilization, and documentation standards without the design advantages of OEMs. Larger operators manage these demands by leveraging scale, while smaller firms struggle with limited resources. The dominance of third-party reprocessors with national networks reflects the need for consistent volume to sustain compliance investments and engineering capabilities. This dynamic supports market growth but slows portfolio expansion and limits smaller players' ability to scale operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cardiovascular Devices Anchor Revenue While Laparoscopic Adoption Builds

In 2025, cardiovascular devices accounted for 56.50% of the United States reprocessed medical devices market share, driven by the high unit value of electrophysiology catheters and a long history of reprocessing in cardiac labs. Administrators benefit from significant savings in electrophysiology, with reprocessing reducing procedure costs by nearly 30%, making cardiovascular devices a key revenue driver as hospitals expand reuse programs.

Orthopedic and arthroscopy devices, along with general surgery products, held mid-tier positions due to repeatable designs and efficient collection workflows. Laparoscopic devices are projected to grow at a 16.20% CAGR from 2026 to 2031, supported by the shift to outpatient settings where cost efficiency is critical, aligning with the need for affordable solutions without disrupting surgical workflows.

By Reprocessing Model: Third-Party Commercial Operators Define the Core Structure

Third-party and commercial reprocessing dominated the United States reprocessed medical devices market in 2025, with an 84.12% share, reflecting the preference for scale, logistics, and regulatory expertise. Large operators manage collection, validation, and compliance efficiently, offering cost advantages and operational insights that smaller programs cannot match.

This model benefits from processing large volumes, enabling data-driven improvements in quality and cycle management. With a projected 16.99% CAGR from 2026 to 2031, outsourcing remains the preferred approach as hospitals prioritize risk reduction and administrative simplicity alongside reprocessed devices.

By Device Risk Class: Semi-Critical Devices Lead While Critical Devices Gain Ground

Semi-critical devices held a 44.18% share in 2025, supported by established reprocessing systems for gastrointestinal, urology, and pulmonology instruments. Non-critical devices contribute significant volume, serving as entry points for hospitals new to reprocessing, easing staff adaptation to broader reuse programs.

Critical devices are expected to grow at a 17.34% CAGR from 2026 to 2031, driven by increased hospital confidence in complex products with proven clearance records. Advancements in FDA clearances and remanufacturing approvals indicate that critical device reuse is expanding into previously challenging surgical platforms.

By Clinical Application: Cardiology and Electrophysiology Stay Largest While Gastroenterology Rises Fast

Cardiology and electrophysiology represented 40.25% of the United States reprocessed medical devices market in 2025, driven by high unit costs and substantial savings potential in high-volume labs. Hospitals achieving significant cost reductions through reprocessing highlight the economic appeal of these applications.

General surgery and orthopedic applications followed due to standardized instruments that streamline collection and reuse. Gastroenterology is projected to grow at a 17.25% CAGR from 2026 to 2031, supported by rising procedure demand and existing automated reprocessing infrastructure, enabling smoother adoption compared to other categories.

By End User: Acute Care Hospitals Lead While ASCs Deliver the Fastest Growth

Acute care hospitals held a 62.86% share in 2025, driven by high device volumes, diverse clinical services, and the ability to evaluate long-term cost savings. Large health systems benefit from multi-site collection programs that enhance logistics and standardize reuse protocols.

Government facilities remain underutilized despite significant potential, while ambulatory surgery centers are projected to grow at an 18.90% CAGR from 2026 to 2031. This growth reflects the cost sensitivity of outpatient care, positioning ASCs as a key growth channel for commercial reprocessors.

Geography Analysis

The Northeast is the most mature regional cluster in the United States reprocessed medical devices market due to its dense hospital networks, major academic medical centers, and procurement teams experienced in formal value analysis reviews. Institutions like Massachusetts General, NewYork-Presbyterian, and Penn Medicine influence broader adoption as clinical programs in large teaching systems often impact affiliated community hospitals.

California leads the West in shaping the United States reprocessed medical devices market by linking procurement decisions to environmental reporting and digital workflow advancements. Urban systems in the state were early adopters of programs integrating reuse, traceability, and sustainability metrics. This alignment enables hospitals to measure cost savings and waste reduction effectively, driving higher-value adoption even in specialties with cautious clinical uptake.

The South and Sun Belt regions are gaining importance in the United States reprocessed medical devices market as ambulatory surgery center growth increases demand for cost-efficient invasive devices in outpatient settings. Commercial reprocessors benefit from offering streamlined collection and return programs tailored to these centers. In the Midwest, integrated delivery systems emphasize purchasing discipline and long-term savings, aligning with the recurring economics of reprocessed devices.

Competitive Landscape

The United States reprocessed medical devices market is moderately concentrated, with a few key players dominating through national logistics systems, FDA-cleared portfolios, and long-standing hospital relationships. Major providers such as Stryker Corporation's Sustainability Solutions, Cardinal Health's Sustainable Technologies, Medline's ReNewal, and Arjo's ReNu Medical are typically the first options hospitals consider for program expansion. These companies focus on process consistency and operational reach, as large health systems increasingly demand vendor support in collection, reporting, training, and audit readiness. Innovative Health strengthened its position in January 2026 by achieving its 50th FDA clearance, addressing hospital buyers' preference for visible regulatory progress.

Stryker has enhanced its value proposition by emphasizing sustainability recognition and waste diversion results, aligning with hospitals' growing interest in environmental data alongside cost savings. Innovative Health has focused on regulatory expansion and addressing anti-competitive practices to deepen its presence in electrophysiology. These strategies highlight that leadership in the United States reprocessed medical devices market relies on operational credibility as much as product diversity.

Opportunities are most evident in complex device categories and among institutions that have yet to adopt reprocessed products at scale. In 2025, Restore Robotics secured FDA clearance for remanufacturing the da Vinci Xi 8mm Monopolar Curved Scissors and advanced to first-in-human use, opening new possibilities in robotic surgery. By October 2025, its robotic recycling and remanufacturing program had expanded to over 300 United States hospitals and surgery centers, demonstrating how quickly a new category can gain traction with a clear regulatory pathway.

U.S. Reprocessed Medical Devices Industry Leaders

Stryker Corporation

Medline Industries, LP

Johnson & Johnson

Cardinal Health, Inc.

Innovative Health LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Innovative Health announced that Biosense Webster complied with a court order by updating software and communication protocols, expanding EP catheter reprocessing access in U.S. hospital EP labs.

- January 2026: Innovative Health achieved its 50th FDA 510(k) clearance, authorizing two additional uses of Abbott's Agilis NxT Steerable Introducer and expanding its hospital customer base.

- October 2025: Restore Robotics surpassed 300 U.S. hospitals and surgery centers in its da Vinci Xi robotic instrument recycling program, with further FDA clearances anticipated in 2026.

- May 2025: Restore Robotics achieved the first human use of FDA-cleared remanufactured Da Vinci Xi instruments, marking a milestone in robotic instrument reprocessing.

- March 2025: Restore Robotics, through Iconocare Health, received FDA 510(k) clearance for remanufacturing da Vinci Xi 8mm Monopolar Curved Scissors, offering hospitals a cost-effective alternative.

U.S. Reprocessed Medical Devices Market Report Scope

As per the scope of the report, U.S. reprocessed medical devices are previously used, single-use devices (SUDs) that undergo a rigorous, FDA-regulated cycle of cleaning, reconditioning, testing, and sterilization. Handled by third-party companies or hospitals, these remanufactured items are cleared for an additional safe clinical use, cutting healthcare costs and reducing medical waste.

The U.S. reprocessed medical devices market is segmented by product type, reprocessing model, device risk class, clinical application, and end-user. By product type, the market includes cardiovascular devices, laparoscopic devices, general surgery devices, gastroenterology devices, orthopedic and arthroscopy devices, ENT devices, and non-invasive patient care devices. By reprocessing model, the market is segmented into third-party/commercial reprocessing, in-house hospital reprocessing, and blended OEM-reprocessor programs. By device risk class, the market is categorized into critical devices, semi-critical devices, and non-critical devices. By clinical application, the market is segmented into cardiology and electrophysiology, gastroenterology, general surgery, orthopedic and arthroscopy, ENT, vascular surgery, and urology and gynecology. By end-user, the market is segmented into acute care hospitals, ambulatory surgery centers, specialty clinics and cath labs, government and federal facilities, and academic and research hospitals. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Cardiovascular Devices |

| Laparoscopic Devices |

| General Surgery Devices |

| Gastroenterology Devices |

| Orthopedic and Arthroscopy Devices |

| ENT Devices |

| Non-invasive Patient Care Devices |

| Third-Party / Commercial Reprocessing |

| In-House Hospital Reprocessing |

| Blended OEM-Reprocessor Programs |

| Critical Devices |

| Semi-Critical Devices |

| Non-Critical Devices |

| Cardiology and Electrophysiology |

| Gastroenterology |

| General Surgery |

| Orthopedic and Arthroscopy |

| ENT |

| Vascular Surgery |

| Urology and Gynecology |

| Acute Care Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics and Cath Labs |

| Government and Federal Facilities |

| Academic and Research Hospitals |

| By Product Type | Cardiovascular Devices |

| Laparoscopic Devices | |

| General Surgery Devices | |

| Gastroenterology Devices | |

| Orthopedic and Arthroscopy Devices | |

| ENT Devices | |

| Non-invasive Patient Care Devices | |

| By Reprocessing Model | Third-Party / Commercial Reprocessing |

| In-House Hospital Reprocessing | |

| Blended OEM-Reprocessor Programs | |

| By Device Risk Class | Critical Devices |

| Semi-Critical Devices | |

| Non-Critical Devices | |

| By Clinical Application | Cardiology and Electrophysiology |

| Gastroenterology | |

| General Surgery | |

| Orthopedic and Arthroscopy | |

| ENT | |

| Vascular Surgery | |

| Urology and Gynecology | |

| By End User | Acute Care Hospitals |

| Ambulatory Surgery Centers | |

| Specialty Clinics and Cath Labs | |

| Government and Federal Facilities | |

| Academic and Research Hospitals |

Key Questions Answered in the Report

What is the current value of the U.S. reprocessed medical devices market?

The U.S. reprocessed medical devices market is valued at USD 0.810 billion in 2026 and is forecast to reach USD 2.3 billion by 2031 at a CAGR of 16.56%.

Which product category leads revenue in this space?

Cardiovascular devices lead with 56.50% share in 2025 because electrophysiology and related cardiac labs offer strong unit economics and repeatable savings.

Why are ambulatory surgery centers becoming important buyers?

ASCs are projected to grow at an 18.90% CAGR from 2026 to 2031 because fixed fee reimbursement makes lower device cost per procedure more important.

What is the main financial reason hospitals adopt reprocessed devices?

Hospitals adopt them for recurring per procedure savings. AMDR reported USD 495.5 million in savings in 2025 across 11,458 healthcare facilities using member reprocessors.

Which clinical application is expanding the fastest?

Gastroenterology is the fastest-growing clinical application, with a projected CAGR of 17.25% from 2026 to 2031, supported by rising procedure demand and existing reprocessing infrastructure.

How concentrated is competition among suppliers?

Competition is moderately concentrated, with national operators such as Stryker, Cardinal Health, Medline, and Arjo holding strong positions, while specialists like Innovative Health and Restore Robotics expand in targeted categories.

Page last updated on: