Thrombectomy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

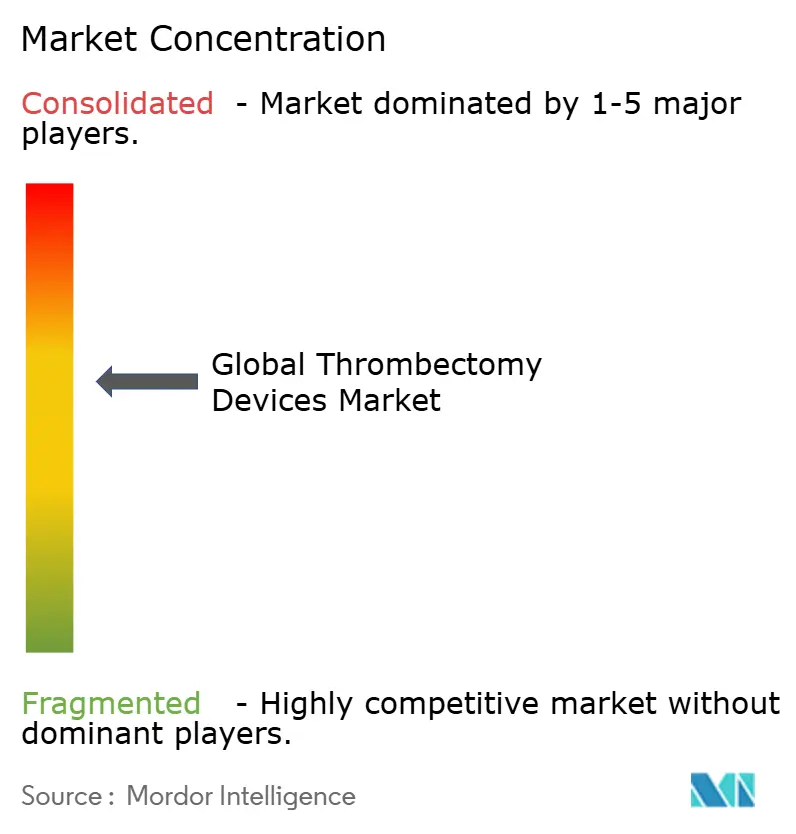

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thrombectomy Devices Market Analysis by Mordor Intelligence

The thrombectomy devices market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.87 billion in 2026 to reach USD 2.62 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031). Clinical evidence demonstrating superior functional recovery, an aging population that is living longer with vascular risk factors, and steady reimbursement expansion are accelerating adoption across stroke centers and peripheral-vascular programs. Mechanical systems continue to command the largest installed base, yet rapid innovation in aspiration catheters and computer-assisted vacuum pumps is redefining procedural efficiency. Manufacturers are pursuing portfolio breadth through acquisitions and next-generation launches, while hospitals are investing in hub-and-spoke stroke networks to relieve capacity shortages. Meanwhile, regulatory harmonization in growth geographies is shortening time-to-market and nurturing local demand, positioning the thrombectomy devices market for sustained double-digit unit growth.

Key Report Takeaways

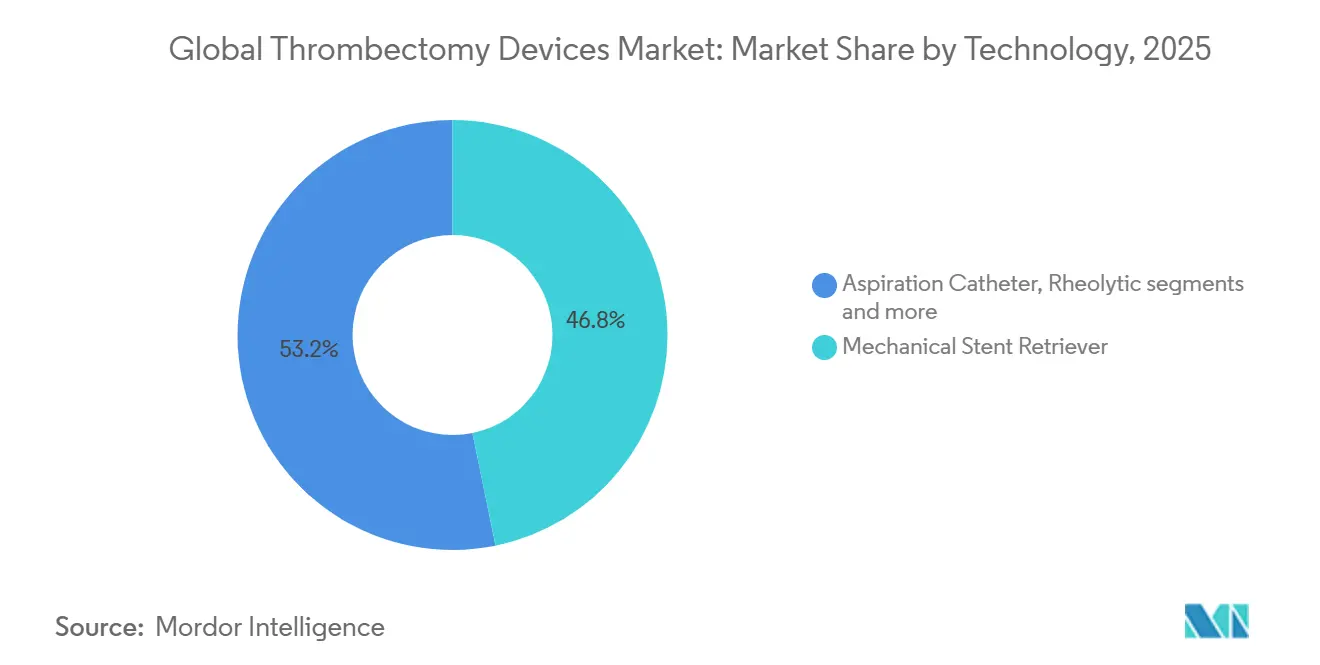

- By technology, mechanical platforms led with 46.80% of thrombectomy devices market share in 2025; aspiration catheters are projected to post the fastest 7.78% CAGR through 2031.

- By type, manual systems captured 52.20% of the thrombectomy devices market in 2025, while automated systems are advancing at a 7.44% CAGR.

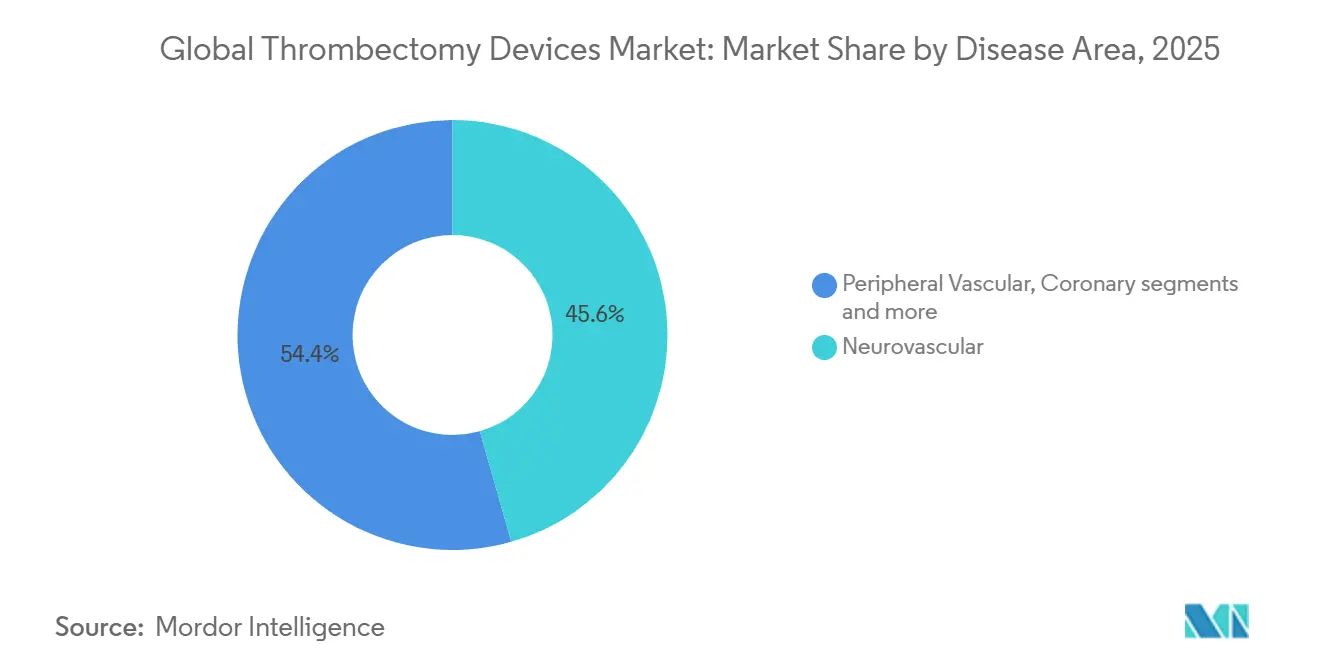

- By disease area, neurovascular applications accounted for 45.60% of the market in 2025; pulmonary embolism interventions hold the top growth outlook at 7.98% CAGR to 2031.

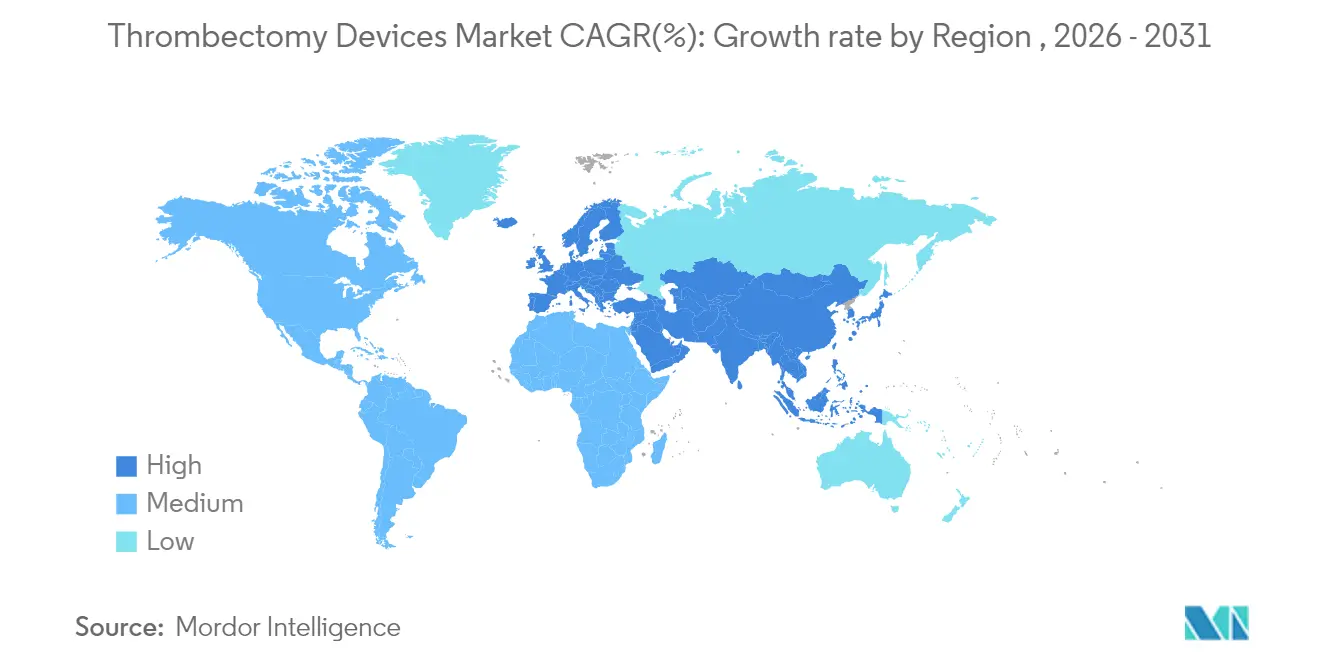

- By geography, North America dominated with 38.10% revenue share in 2025, whereas Asia-Pacific is forecast to expand the fastest at an 8.11% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thrombectomy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Rising Stroke Incidence | +2.80% | Global, with highest impact in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements in Device Design | +2.10% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Expanding Clinical Evidence and Guidelines | +1.60% | Global, with regulatory-driven adoption in developed markets | Medium term (2-4 years) |

| Improved Healthcare Infrastructure | +1.20% | Asia-Pacific, Latin America, and Middle East & Africa | Long term (≥ 4 years) |

| Favorable Reimbursement Policies | +0.80% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing Awareness of Minimally Invasive Procedures | +0.60% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Stroke Incidence

Growing life expectancy is swelling the global pool of stroke patients and, by extension, candidates for mechanical clot removal. Worldwide stroke events are projected to climb from 11.81 million in 2021 to 21.43 million by 2050, an 81% surge that will underpin steady procedure growth even if age-adjusted rates fall modestly [1]Source: H. Cho, “Global Stroke Incidence Projections,” Journal of the American Heart Association, ahajournals.org. China already records 2.77 million ischemic strokes per year, and U.S. modeling shows potential thrombectomy-eligible volumes quadrupling as guideline criteria widen. These trends turn thrombectomy devices from a discretionary technology into essential hospital infrastructure, guaranteeing recurrent replacement demand.

Technological Advancements in Device Design

Innovation is narrowing the gap between difficult anatomy and dependable recanalization. Stanford’s milli-spinner prototype achieved 90% success on hard clots versus 50% for conventional capture, using vortex-induced compression that avoids fragmentation [2]Source: G. Chen, “Milli-Spinner Device Demonstrates 90% Success,” Nature News, news.stanford.edu. Penumbra’s Lightning Flash 2.0 shortens active device time to 13 minutes through dual clot-detection algorithms that modulate suction in real time. Such improvements attack the 10-30% of cases that still end in incomplete reperfusion and are driving hospitals to upgrade ahead of schedule.

Expanding Clinical Evidence and Guidelines

Registries now report major adverse event rates below 2% for complex pulmonary embolism cases and document meaningful hemodynamic relief within minutes of device deployment. European cost-utility studies show mechanical thrombectomy is either cost-effective or cost-saving in 31 of 32 countries, persuading payers to widen coverage. As evidence reaches medium-vessel occlusions and peripheral beds, professional societies are updating guidelines, converting a once-experimental therapy into mainstream practice.

Improved Healthcare Infrastructure

Legislative shifts such as Brazil’s ANVISA IN 290/2024 let manufacturers cross-reference FDA approvals for local registration, slicing market-entry times by months emergobyul.co. Mobile stroke units and tele-triage pathways are extending thrombectomy access beyond metropolitan hubs. Early Asia-Pacific studies with large-bore suction catheters achieved 87.5% survival to discharge and 21.4% pulmonary-pressure reductions, confirming suitability for lower-resource settings.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Costs and Budget Constraints | -1.40% | Global, with highest impact in emerging markets and public healthcare systems | Short term (≤ 2 years) |

| Shortage of Trained Specialists | -0.90% | Global, with acute shortages in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Risk of Complications and Side Effects | -0.50% | Global, with higher concern in emerging markets | Medium term (2-4 years) |

| Limited Access in Rural Areas | -0.40% | Asia-Pacific, Latin America, and rural regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device Costs and Budget Constraints

Episode-of-care costs reach USD 10,682 for mechanical thrombectomy and up to USD 19,669 for rheolytic systems, with the single-use device the largest line item. Although long-term savings outweigh capital outlays, the initial USD 5,040 price tag for a FlowTriever kit can exceed fixed reimbursement in public systems. Hospitals therefore ration use to the highest-acuity patients, slowing penetration in cost-sensitive regions.

Shortage of Trained Specialists

France performs 7,500 thrombectomies a year against a need for 20,500, reflecting labor, transfer, and bed constraints. The learning curve extends beyond the operator to an entire acute-stroke team, and pediatric applications complicate training further because adult-sized devices risk vessel injury in children. Without systematic workforce expansion, infrastructure upgrades alone cannot close the access gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Mechanical Dominance Faces Aspiration Innovation

Mechanical platforms captured 46.80% of thrombectomy devices market share in 2025 as physicians rely on well-validated stent-retriever workflows. The thrombectomy devices market size for mechanical systems is expected to expand at 6.95% CAGR through 2031, supported by engineering refinements such as braided nitinol designs that improve clot engagement. First-pass success rates routinely exceed 80%, yet performance drops on calcified or elongated clots, highlighting limits that pure mechanical force cannot breach.

Aspiration catheters are closing that gap and are forecast to grow the fastest at 7.78% CAGR, propelled by computer-guided suction and larger inner lumens that preserve flow while evacuating debris. Hybrid techniques such as mini-SOLUMBRA marry direct aspiration with stent assistance to treat medium-vessel occlusions that account for up to 40% of ischemic strokes. Future segmentation will likely align devices to clot phenotype, moving the conversation from “mechanical versus aspiration” toward precision-guided therapy bundles.

By Type: Manual Systems Lead Despite Automation Advances

Manual systems retained 52.20% revenue share in 2025 thanks to intuitive tactile feedback and minimal capital overhead. Operators value the flexibility to modulate force instantaneously when confronted with tortuous anatomy. The thrombectomy devices market size for manual platforms is expected to record a steady 6.28% CAGR, buoyed by upgrades such as hydrophilic coatings that lower friction.

Automated pumps, however, are climbing at 7.44% CAGR as hospitals seek reproducible outcomes independent of operator skill. Penumbra’s dual-sensor algorithms and Stryker’s forthcoming pressure-responsive pumps exemplify how real-time data loops minimize blood loss and shorten procedural time. As reimbursement shifts toward bundled payments, consistency becomes a strategic purchasing criterion. Over the forecast horizon, hybrid consoles that let physicians toggle between manual override and automatic optimization are anticipated to capture share by blending familiarity with efficiency.

By Disease Area: Leadership with Pulmonary Embolism Surge

Neurovascular interventions represented 45.60% of applications in 2025, reflecting decades of stroke network development and compelling functional-recovery data. Hospitals view thrombectomy suites as revenue-positive because early reperfusion trims disability-related costs that would burden post-acute budgets. The thrombectomy devices market size for neurovascular care is projected to expand at 6.62% CAGR, sustained by guideline updates that widen eligibility to medium-vessel occlusions.

Pulmonary embolism is emerging as the next breakout segment, poised to grow at an 7.98% CAGR to 2031 as real-world data confirm 1.8% device-related adverse events and durable hemodynamic gains. AlphaVac and FlowTriever launches are broadening device choice, while payer recognition of right-heart strain metrics is driving earlier intervention. Deep-vein thrombosis and peripheral arterial clots round out a diversified pipeline, signaling that thrombectomy is morphing from stroke-specific therapy into a pan-vascular standard.

Geography Analysis

North America held 38.10% of 2025 revenue as mature stroke systems, reliable reimbursement, and high specialist density sustain procedure volumes. U.S. modeling suggests that endovascular-eligible patient counts could quadruple if recent trial criteria are applied universally, creating a multi-year volume tailwind for the thrombectomy devices market. Device vendors increasingly bundle capital leases with per-procedure disposables, easing hospital cash-flow barriers. Corporate activity exemplified by Stryker’s USD 4.9 billion acquisition of Inari Medical underscores the region’s leadership in portfolio expansion.

Asia-Pacific is the fastest-growing territory at an 8.11% CAGR through 2031; China’s 2.77 million annual ischemic strokes illustrate an unmet need, while Japan’s PMDA clearance of ClotTriever signals regulatory receptiveness to advanced devices. Mobile CT units and AI-driven tele-stroke pathways are being piloted to bypass distance barriers across Indonesia, India, and rural provinces of China. Early multicenter data show 87.5% survival to discharge after large-bore suction thrombectomy in resource-constrained hospitals, reinforcing the business case for regional expansion.

Europe combines sophisticated neuro-interventional know-how with capacity bottlenecks: France manages only one procedure for every three potential candidates, and Germany reports 6.7% thrombectomy transfer rates from primary centers. Cost-utility analyses covering 32 nations confirm broad economic justification, but scaling hinges on training and cross-border referral pathways. Latin America and Middle East & Africa offer incremental upside as ANVISA’s new fast-track and Gulf Cooperation Council tender reforms compress device registration timelines, enabling faster uptake of best-in-class systems.

Competitive Landscape

The thrombectomy devices market is moderately consolidated yet fiercely innovative. Top multinationals leverage M&A to fill technology gaps, illustrated by Stryker’s purchase of Inari Medical, which broadens its reach into venous and pulmonary beds.

Technology leadership focuses on speed, safety, and clot-specific customization. Penumbra’s Lightning Flash 2.0 integrates dual sensors that alter suction thresholds in real time, a differentiator that reduces average case time to 38 minutes. Start-ups from academic incubators, such as Stanford’s milli-spinner team, target hard-to-scale niches where current first-pass yield lags, forcing incumbents to fund external collaborations to keep pace.

Procurement is shifting toward outcome-weighted contracting. Value-based analyses show net benefits topping USD 100,000 per patient when disability costs are included, a bargaining chip vendors use to justify premium pricing. Yet hospitals demand evidence through post-market registries; the FDA’s emphasis on real-world surveillance could favor companies with robust data infrastructures. As portfolios diversify across vascular beds, integrated service models covering training, inventory management, and tele-mentoring will become pivotal differentiators.

Thrombectomy Devices Industry Leaders

Stryker

Boston Scientific Corporation

Medtronic PLC

Terumo Corporation

Koninklijke Philips NV (Spectranetics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stryker completed its USD 4.9 billion acquisition of Inari Medical, adding venous thrombo-embolism solutions to its thrombectomy lineup.

- May 2024: AngioDynamics received CE Mark for the AlphaVac F1885 System, targeting Europe’s 435,000 annual pulmonary-embolism events.

- February 2024: FDA cleared the XACT Carotid Stent System, enriching the stroke-prevention toolkit that complements thrombectomy procedures.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global thrombectomy devices market as revenue generated from sales of minimally invasive aspiration, mechanical or rheolytic systems that physically remove blood clots in neurovascular, peripheral vascular, pulmonary, and coronary vessels during interventional procedures. Disposable catheters, console components, and single-use accessories sold with each system are included.

Scope exclusion: Recanalization drugs, laser atherectomy tools, and purely diagnostic guidewires are outside this scope.

Segmentation Overview

- By Technology

- Mechanical Stent Retriever

- Aspiration Catheter

- Rheolytic

- Ultrasonic / Rotational

- By Type

- Automated

- Manual

- By Disease Area

- Neurovascular

- Peripheral Vascular

- Coronary

- Pulmonary Embolism

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed interventional neurologists, vascular surgeons, cath lab managers, and procurement heads across North America, Europe, and key Asian hubs. Discussions clarified adoption thresholds, average selling prices, replacement cycles, and the share shift toward aspiration catheters, allowing us to refine model assumptions gathered from desk research.

Desk Research

We began with structured searches across tier-1 public domains such as the WHO stroke database, OECD Health Statistics, United States CDC NVSR mortality files, Eurostat hospital procedural volumes, and Japan's MHLW medical device shipment survey. Company 10-Ks, recent device 510(k) clearances on the FDA MAUDE archive, and conference abstracts from the International Stroke Conference added product-level clues. To benchmark installed base and pricing, we referenced D&B Hoovers and Dow Jones Factiva. Numerous additional open and subscription sources were consulted beyond this illustrative list.

Market-Sizing & Forecasting

A top-down build starts with country-level ischemic stroke, pulmonary embolism, and PAD procedure volumes, reconstructed from hospital discharge datasets and further filtered through treatment eligibility ratios derived from clinical literature. These demand pools are then multiplied by weighted device utilization rates to create 2025 unit estimates. Selective bottom-up cross-checks, supplier sales roll-ups, and sampled ASP × volume interviews anchor the totals. Key drivers such as population over 65, reperfusion treatment window expansion, stent retriever penetration, reimbursement tariff shifts, and average device ASP erosion inform the model. We forecast using multivariate regression that links procedure growth and ASP trends to macro variables like health expenditure per capita; scenario analysis adjusts for emerging first-pass combined systems. When partial bottom-up inputs are missing, regional proxies and peer-validated ratios bridge the gaps.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated variance scans, senior analyst logic checks, and domain expert sign-off. Models are refreshed annually, with interim updates triggered by major approvals or reimbursement changes, ensuring clients always receive the latest vetted view.

Why Mordor's Thrombectomy Devices Baseline Is Distinctly Reliable

Published values often diverge because publishers choose different device mixes, service add-ons, and refresh cadences.

Key gap drivers include variations in whether coronary kits are counted, if accessory disposables are bundled, the aggressiveness of ASP compression assumptions, and how quickly new aspiration technology uptake is baked into forecasts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.75 B (2025) | Mordor Intelligence | - |

| USD 1.95 B (2025) | Global Consultancy A | Includes capital consoles and related imaging catheters inflating totals |

| USD 1.76 B (2025) | Regional Consultancy B | Excludes pulmonary and coronary indications, leading to narrower scope |

| USD 1.64 B (2025) | Trade Journal C | Uses static ASPs without accounting for price erosion |

In sum, Mordor's disciplined scope definition, dual-path modelling, and yearly refresh create a balanced, transparent baseline that decision makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the thrombectomy devices market?

The market is valued at USD 1.87 billion in 2026 and is set to reach USD 2.62 billion by 2031, growing at a 6.98% CAGR during 2026-2031.

Which technology segment leads the thrombectomy devices market?

Mechanical platforms dominate with 46.80% market share, but aspiration catheters are the fastest-growing at 7.78% CAGR.

Which region shows the highest growth potential?

Asia-Pacific is forecast to expand at an 8.11% CAGR through 2031, outpacing all other regions.

Why are hospitals adopting automated thrombectomy systems?

Automated pumps deliver reproducible outcomes, shorten device time to 13 minutes, and reduce blood loss, meeting bundled-payment efficiency goals.

What restrains broader adoption of thrombectomy devices?

High upfront device costs and a global shortage of trained specialists limit procedural capacity, especially in emerging markets.

Page last updated on: