Hematocrit Test Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

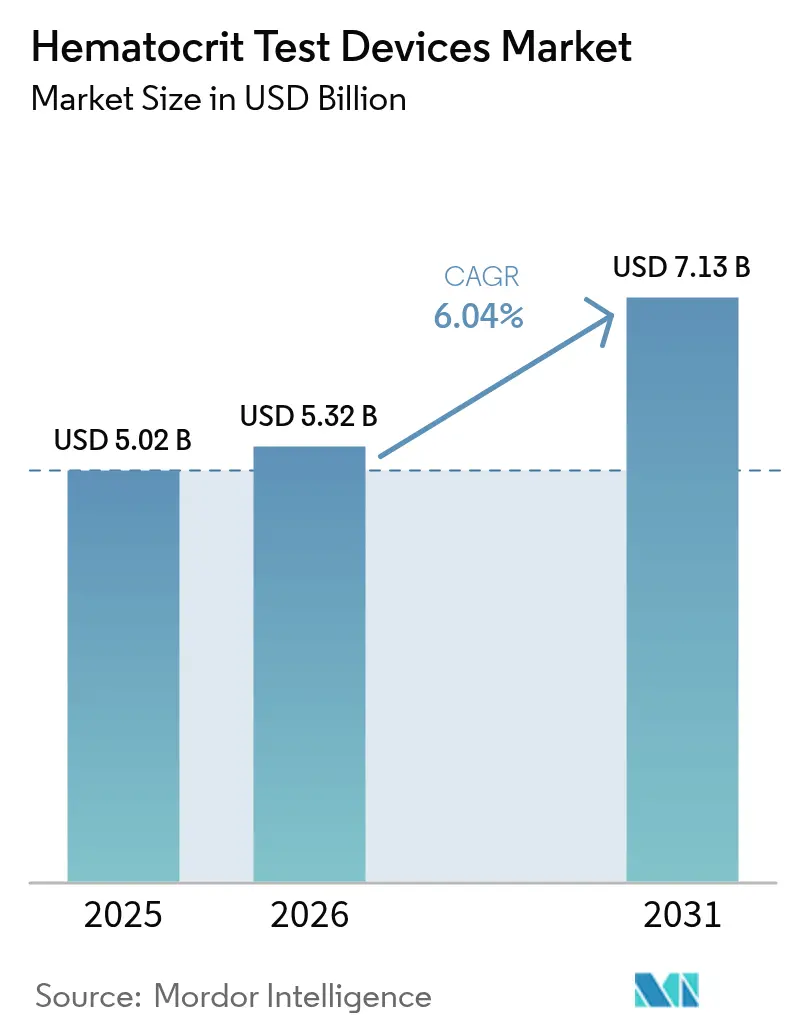

| Market Size (2026) | USD 5.32 Billion |

| Market Size (2031) | USD 7.13 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hematocrit Test Devices Market Analysis by Mordor Intelligence

The hematocrit test devices market size was valued at USD 5.02 billion in 2025 and estimated to grow from USD 5.32 billion in 2026 to reach USD 7.13 billion by 2031, at a CAGR of 6.04% during the forecast period (2026-2031). Expanding diagnostic demand created by the global anemia burden, rapid migration toward automated 5-part differential analyzers, and integration of artificial intelligence into point-of-care (POC) platforms are the primary growth catalysts. Hospitals continue to upgrade to high-throughput systems that cut manual workload, while militaries and emergency services drive adoption of ultra-portable microfluidic meters that deliver hematocrit (Hct) results within seconds. Regulatory tightening, such as the 2024 CLIA rule that cut allowable Hct error margins by one-third, is simultaneously raising performance expectations and spurring innovation. Competitive intensity is moderate; incumbents leverage global installed bases and reagent lock-in models, yet handheld and smartphone-based entrants are reshaping customer expectations around convenience and cost.

Key Report Takeaways

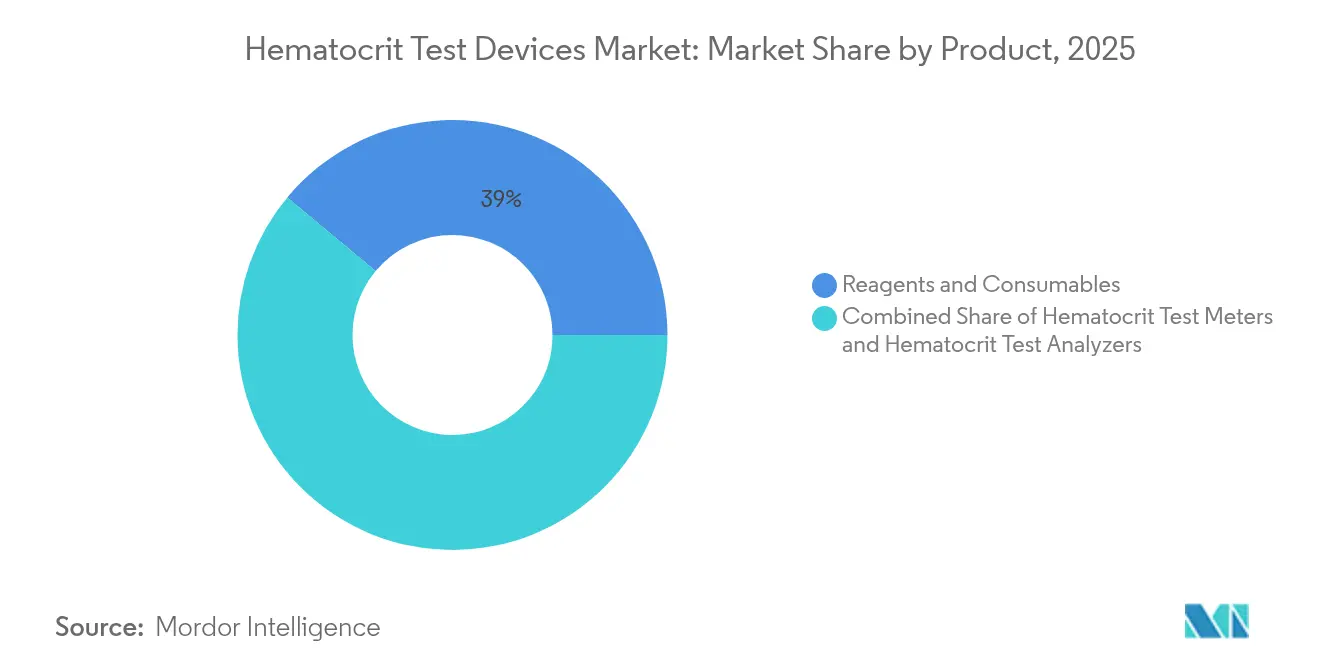

- By product category, reagents and consumables led with 38.95% revenue share in 2025, while hematocrit test analyzers are forecast to expand at a 11.92% CAGR to 2031.

- By technology, electrical impedance held 38.10% of hematocrit test devices market share in 2025, whereas microfluidic platforms are projected to grow at 13.2% CAGR through 2031.

- By application, anemia diagnosis and monitoring accounted for a 59.55% share of the hematocrit test devices market size in 2025; dialysis and renal care is advancing at a 12.95% CAGR to 2031.

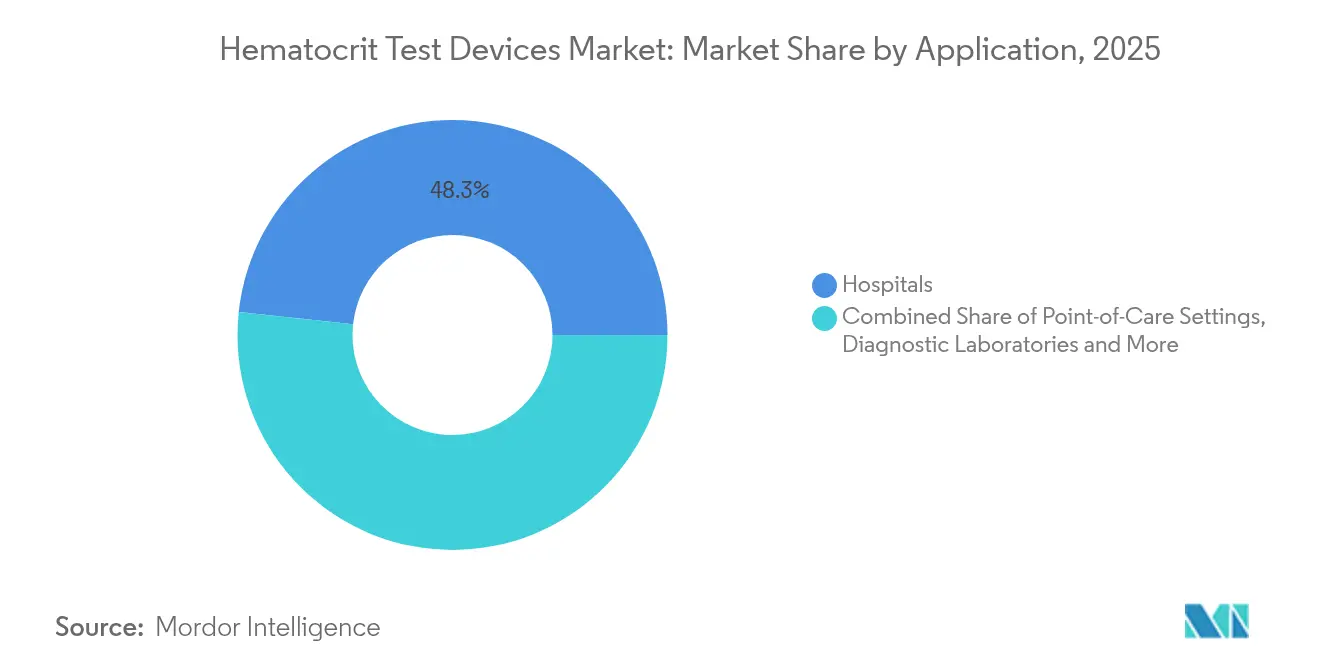

- By end user, hospitals captured 48.30% revenue share in 2025, yet point-of-care settings show the highest 13.95% CAGR through 2031.

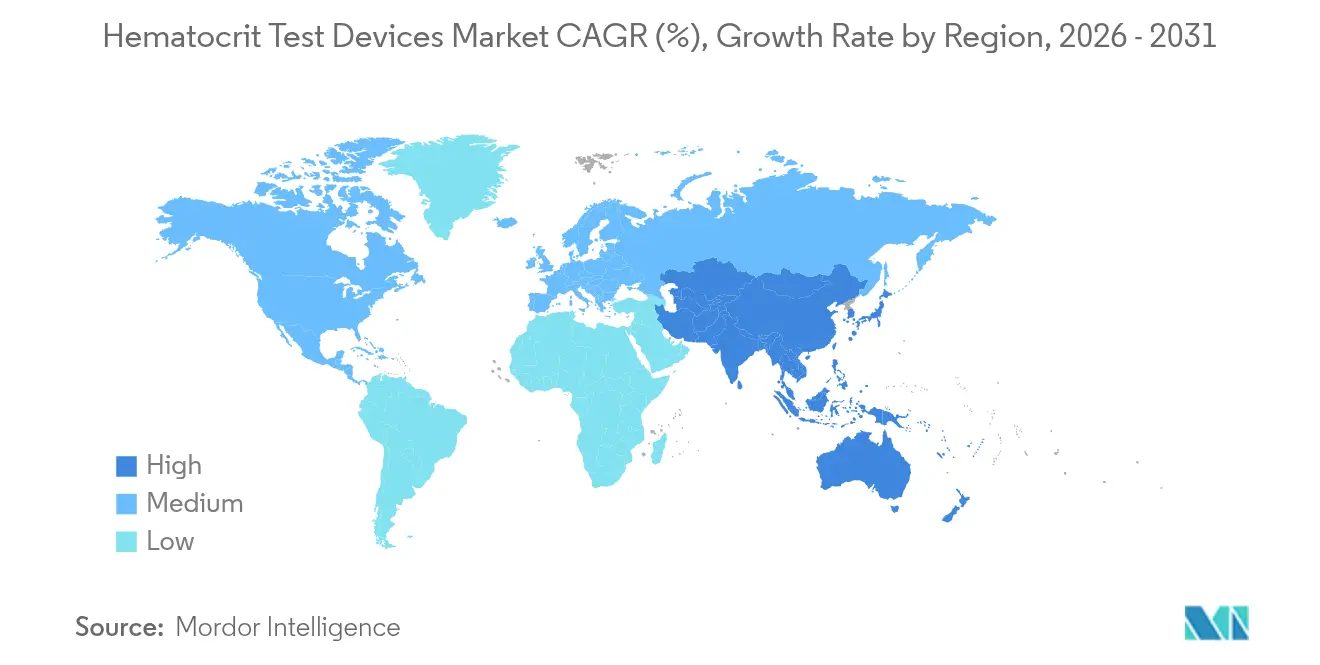

- By geography, North America commanded 39.20% revenue in 2025, while Asia-Pacific is expanding at 13.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hematocrit Test Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of anemia worldwide | +1.8% | Global, highest in Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Rapid adoption of fully automated 5-part analyzers | +1.2% | North America & EU, rising in Asia-Pacific | Medium term (2-4 years) |

| Growing geriatric population with blood disorders | +1.5% | Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Shift to intra-operative Hct monitoring to cut transfusion costs | +0.9% | Global, earliest in developed markets | Medium term (2-4 years) |

| Military demand for ultra-portable microfluidic meters | +0.4% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Integration of AI-enabled self-testing apps for chronic care | +0.8% | Global, fastest in tech-forward regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Anemia Worldwide

Anemia affects nearly 2 billion people and 39.8% of children under five, driving continuous demand for reliable hematocrit testing devices[1]World Health Organization, “Anaemia,” who.int. Updated 2024 WHO hemoglobin cutoffs tightened diagnostic thresholds, compelling providers to deploy more precise instruments in both clinics and resource-limited outreach settings. Regions with high iron-deficiency rates, notably South Asia, are funding mobile screening programs that rely on battery-operated Hct meters. These initiatives reinforce long-term uptake of the hematocrit test devices market, particularly for consumables that accompany each field test. Preventing disease progression through early Hct screening also lowers treatment costs and improves maternal and child health outcomes.

Rapid Adoption of Fully Automated 5-Part Analyzers

Clinical laboratories confront staff shortages and mounting sample volumes, prompting a shift toward automated 5-part differential systems capable of handling thousands of complete blood counts per hour. Sysmex recorded 2,977 million CBCs in fiscal 2023, reflecting its 54.6% share of the automated hematology field[2]Sysmex Corporation, “Sustainability Data Book 2024,” sysmex.co.jp. New platforms embed digital cell morphology and AI algorithms that now identify arterial oxygen saturation patterns with 96% accuracy during hemodialysis. Partnerships such as Siemens Healthineers-Scopio Labs shorten turnaround times by 60%, raising clinical throughput.

Growing Geriatric Population With Blood Disorders

People over 75 increasingly present with complex anemia linked to chronic kidney disease, inflammation, and nutritional deficits, especially across aging Asian economies. Mendelian randomization links eosinophil and lymphocyte counts to biological aging, reinforcing the value of routine Hct monitoring for precision geriatric care. Health systems respond with age-specific reference intervals, spurring demand for easy-to-use analyzers adaptable to outpatient, long-term care, and home settings.

Shift to Intra-Operative Hct Monitoring

Hospitals invest in real-time Hct sensors during surgery to cut transfusion costs and reduce postoperative complications. In cardiac bypass, Quantum Perfusion achieved deviation of only 0.2 percentage points compared with standard blood-gas systems. Such accuracy supports closed-loop fluid management protocols and aligns with tighter CLIA limits, boosting demand for integrated blood-management consoles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA & CE approval timelines | -0.7% | North America & Europe | Medium term (2-4 years) |

| Limited awareness & training in low-income regions | -0.5% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Microfluidic cartridge supply-chain fragility | -0.3% | Global, high Asia-Pacific concentration | Short term (≤ 2 years) |

| Accuracy concerns in non-invasive optical Hct wearables | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent FDA & CE Approval Timelines

The FDA now requires manufacturers to flag supply-chain disruptions and submit broader clinical datasets, stretching approval cycles for innovative Hct platforms[3]U.S. Food and Drug Administration, “Medical Device Supply Chain Vulnerabilities,” fda.gov. Class II designation for coagulation devices illustrates the agency’s tighter stance, which raises entry barriers for start-ups. In Europe, MDR compliance adds cost and paperwork, delaying commercialization of novel microfluidic cartridges and AI software.

Accuracy Concerns in Non-Invasive Optical Wearables

Optical devices appeal to consumers but still show bias up to 0.75 g/dL versus reference methods, limiting their use as stand-alone clinical tools. Ambient light, tissue variability, and hydration status can distort readings, so clinicians treat them as trend monitors rather than absolute measures. Ongoing calibration research aims to improve precision, but the restraint will curb near-term adoption rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Sustain Recurring Revenue

Reagents and consumables held 38.95% of 2025 revenue, a testament to the installed-base model that locks in repeat purchases of cuvettes, cartridges, and quality-control reagents for every test run. Each new analyzer installation amplifies this annuity stream across hospitals, diagnostics labs, and field units, making the category a profit anchor for suppliers. Hematocrit test analyzers, the fastest-growing product group at 11.92% CAGR, reflect laboratories’ migration to fully automated 5- or 6-part systems that integrate CBC, ESR, and blood-gas functions in one console.

Handheld meters are carving out niches in emergency medical services and rural clinics by offering six-second turnaround using capillary blood, while veterinary practices adopt mobile analyzers validated for canine hematology applications. This broadening user mix keeps the hematocrit test devices market expanding on both capital equipment and disposable fronts. In dollar terms, the hematocrit test devices market size for reagents is projected to widen in tandem with global analyzer placements, reinforcing suppliers’ focus on supply-chain resilience and predictable pricing contracts.

By Technology: Microfluidics Reshapes Diagnostics

Electrical impedance retained 38.10% hematocrit test devices market share in 2025 due to decades of trust among lab directors. Yet microfluidic and lab-on-chip platforms are outpacing legacy methods at 13.2% CAGR because they require only microliters of blood and function with gravity-driven flow, slashing pump costs. Researchers now fabricate polymer channels with femtosecond lasers at one-eighth of traditional cost, accelerating commercialization.

Optical spectrometry remains valuable for non-invasive monitoring, though precision still lags invasive assays. Conductivity and acoustofluidic techniques add options for niche applications such as platelet-free plasma preparation and red-cell deformability studies. As microfluidic production scales, vendors bundle cloud analytics and AI algorithms, redefining value beyond simple cell counting. The hematocrit test devices market size for microfluidic systems is on track to command a growing revenue slice as buyers prioritize portability without sacrificing laboratory-grade accuracy.

By Application: Dialysis Drives New Volume

Anemia diagnosis and monitoring accounted for 59.55% of 2025 revenue, mirroring clinicians’ everyday reliance on Hct values to guide iron therapy and nutritional interventions. Dialysis and renal care, however, posts the fastest 12.95% CAGR, because real-time Hct monitoring optimizes fluid removal and limits intradialytic hypotension. Relative blood-volume sensors embedded in dialysis machines correlate with lower hospitalization, encouraging clinics to standardize on integrated Hct modules.

Cardiac surgery, critical care, and oncology supportive care collectively add incremental demand, leveraging closed-loop systems that maintain precise oxygen-carrying capacity during complex procedures. In hemodynamics research, online Hct sensors now inform perfusion decisions every few seconds, creating data streams for algorithm-driven fluid therapy. The result is a broader clinical mandate that keeps the hematocrit test devices market growing across acute and chronic care pathways.

By End User: Point-of-Care Takes Off

Hospitals remained the largest buyers with 48.30% of 2025 spend, supported by centralized laboratories and OR integration. Yet point-of-care environments, spanning physician offices, ambulances, and retail clinics, register the quickest 13.95% CAGR. Capillary collection technologies like BD MiniDraw enable trained staff to obtain high-quality samples without traditional venipuncture, lowering both patient anxiety and infrastructure barriers.

Diagnostic laboratories still manage mass screening and reference testing, while blood banks depend on rapid Hct checks to safeguard donors. Military and disaster-response units prefer battery-operated analyzers that withstand harsh climates, and home-health models are emerging through AI-enabled apps that link personal devices to cloud dashboards. Together these trends expand the hematocrit test devices market size beyond hospital walls and closer to the patient.

Geography Analysis

North America held 39.20% of global revenue in 2025, underpinned by sophisticated hospital networks, favorable reimbursement, and rapid uptake of integrated hematology workstations. Defense funding for blood substitutes and the FDA’s active supply-chain surveillance further shape demand by ensuring product continuity and elevating quality benchmarks. Canada and Mexico contribute through public-sector modernization programs that broaden access to automated CBC testing.

Asia-Pacific is the fastest-growing region at a 13.05% CAGR as China, India, Japan, South Korea, and Southeast Asian nations overhaul infrastructure and address aging demographics. Government tenders in China now favor mid- and low-end analyzers, pressuring pricing yet lifting unit volumes. India’s smartphone-based anemia screening exemplifies leapfrog adoption in areas with limited laboratory capacity. Japan’s elderly population, where up to 50% of males exceed normal hemoglobin thresholds, fuels sustained analyzer demand tailored to geriatric reference ranges. Europe remains a key revenue pillar thanks to strict quality protocols and broad insurance coverage. Germany, the United Kingdom, and France lead high-end analyzer deployments, while Southern European markets scale POC meters to manage chronic-disease clinics. Middle East and Africa witness rising procurement backed by anemia prevalence that tops 60% among children in parts of the continent. South America follows, with Brazil and Argentina investing in public lab upgrades to combat nutritional anemia and renal disease. Collectively, these regional dynamics ensure the hematocrit test devices market continues its steady global expansion.

Competitive Landscape

Market concentration is moderate, with global leaders capturing scale benefits while nimble entrants disrupt selected niches. Sysmex sustains a commanding 54.6% share of the automated hematology segment and processed nearly 3 billion CBC tests in 2023, illustrating the moat created by installed bases and reagent contracts. Siemens Healthineers deepened its portfolio through a global OEM pact with Sysmex for hemostasis devices and a distribution deal with Scopio Labs for digital cell morphology, positioning itself as a full workflow provider.

Beckman Coulter focuses on compliance leadership, releasing DxH-520 for low-volume labs aligned with the 2024 CLIA precision mandate. HORIBA blends CBC and ESR into compact analyzers that address small hospital budgets, while Nova Biomedical targets emergency services with six-second Hct meters. In dialysis, Fresenius integrates Crit-Line sensors to cut patient admissions, illustrating how vertical specialists create sticky platforms.

Disruptors challenge incumbents through handheld and AI-powered solutions. CytoChip secured FDA clearance and a CLIA waiver for its palm-sized CBC analyzer, signalling regulatory confidence in miniaturized hematology. Sanguina’s Ruby app estimates iron status from fingernail photos, pointing to consumer-centric business models. Supply-chain fragility in microfluidic cartridges motivates partnerships with contract manufacturers outside Asia and investments in additive manufacturing, potentially reshaping cost structures. As performance standards climb, only firms able to balance accuracy, usability, and logistics will sustain share in the hematocrit test devices market.

Hematocrit Test Devices Industry Leaders

Abbott Laboratories

Nova Biomedical

Sysmex Corporation

EKF Diagnostics Holdings plc

Danaher Corporation (Beckman Coulter)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CytoChip received 510(k) clearance and a CLIA waiver for its handheld CitoCBC analyzer, enabling U.S. commercialization.

- March 2025: BD and Babson Diagnostics published studies confirming MiniDraw capillary collection delivers accuracy equal to venous draws.

Global Hematocrit Test Devices Market Report Scope

As per the scope of the report, a hematocrit test is part of a complete blood count that measures different components of the blood. Hematocrit test helps in diagnosing blood disorders such as anemia, polycythemia vera, and others. The hematocrit is typically measured from a blood sample by an automated machine that makes several other measurements of the blood at the same time.

The hematocrit test devices market is segmented by product (hematocrit test meter, hematocrit test analyzer, and reagents and consumables), application (anemia, polycythemia vera, congenital heart disease, and other applications), end user (hospitals, diagnostic centers, and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above segments.

| Hematocrit Test Meters | Hand-held POC Meters |

| Benchtop Meters | |

| Hematocrit Test Analyzers | Automated 3-part Differential |

| Automated 5/6-part Differential | |

| Integrated Blood-gas & Hct Platforms | |

| Veterinary-specific Analyzers | |

| Reagents & Consumables | Hct Cuvettes & Micro-tubes |

| Calibration & QC Reagents | |

| Test Cartridges/Strips |

| Electrical Impedance |

| Optical / Photometric |

| Conductivity-based |

| Microfluidic & Lab-on-Chip |

| Non-invasive Spectroscopy |

| Anemia Diagnosis & Monitoring |

| Polycythemia Vera Management |

| Congenital Heart Disease |

| Surgery & Critical-Care Blood Management |

| Dialysis & Renal Care |

| Oncology Supportive Care |

| Hospitals |

| Diagnostic Laboratories |

| Blood Banks & Transfusion Centers |

| Point-of-Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Hematocrit Test Meters | Hand-held POC Meters |

| Benchtop Meters | ||

| Hematocrit Test Analyzers | Automated 3-part Differential | |

| Automated 5/6-part Differential | ||

| Integrated Blood-gas & Hct Platforms | ||

| Veterinary-specific Analyzers | ||

| Reagents & Consumables | Hct Cuvettes & Micro-tubes | |

| Calibration & QC Reagents | ||

| Test Cartridges/Strips | ||

| By Technology | Electrical Impedance | |

| Optical / Photometric | ||

| Conductivity-based | ||

| Microfluidic & Lab-on-Chip | ||

| Non-invasive Spectroscopy | ||

| By Application | Anemia Diagnosis & Monitoring | |

| Polycythemia Vera Management | ||

| Congenital Heart Disease | ||

| Surgery & Critical-Care Blood Management | ||

| Dialysis & Renal Care | ||

| Oncology Supportive Care | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Blood Banks & Transfusion Centers | ||

| Point-of-Care Settings | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hematocrit test devices market?

The market was valued at USD 5.32 billion in 2026 and is forecast to reach USD 7.13 billion by 2031 at a 6.04% CAGR.

Which product category generates the highest revenue?

Reagents and consumables lead with 38.95% of 2025 sales, driven by recurring demand across installed analyzers.

Why are microfluidic technologies gaining traction?

They enable laboratory-grade accuracy from microliter blood volumes, lower per-test costs, and support portable devices, fuelling a 13.2% CAGR.

Which region is expanding fastest?

Asia-Pacific is growing at 13.05% CAGR through 2031, supported by healthcare modernization and mobile diagnostics adoption.

How do regulatory changes affect market growth?

Tightened CLIA precision rules and extended FDA evaluation timelines raise compliance costs, delaying product launches but improving device reliability.

What role do AI-enabled smartphone apps play?

They provide non-invasive hemoglobin estimation, expanding screening into communities with limited laboratory access and boosting POC segment momentum.

Page last updated on: