United States Uterine Fibroids Treatment Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

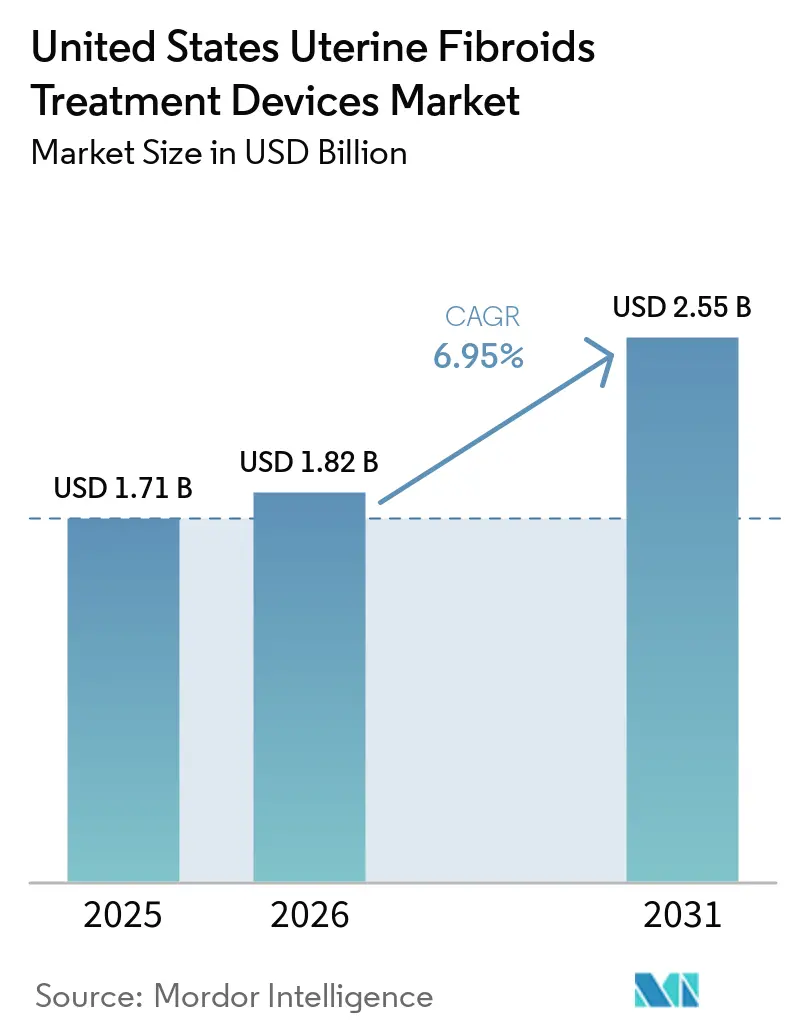

| Base Year Market Size (2025) | USD 1.71 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Uterine Fibroids Treatment Devices Market Analysis by Mordor Intelligence

The United States Uterine Fibroids Treatment Devices Market size is projected to expand from USD 1.71 billion in 2025 and USD 1.82 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 6.95% between 2026 to 2031.

Uterine fibroids affect up to 70% of women by age 50 in the United States, and the much higher prevalence reported among Black women continues to create stronger procedure demand in large, demographically diverse metro areas within the United States uterine fibroids treatment devices market. The United States uterine fibroids treatment devices market is also being supported by a steady shift away from definitive surgery toward uterus-preserving options, as patients and physicians place more weight on recovery time, fertility considerations, and outpatient care pathways. Wider payer acceptance for laparoscopic radiofrequency ablation and clearer guideline support have reduced adoption barriers for ablation platforms, which is improving access across hospital, ASC, and office-based settings in the United States uterine fibroids treatment devices market. Platform consolidation after Hologic’s Gynesonics acquisition and continued robotic procedure growth from Intuitive Surgical show that scale, distribution depth, and site-of-care expansion are becoming more important competitive tools in the United States uterine fibroids treatment devices market. Even so, uneven reimbursement for MRgFUS and limited rural interventional radiology access continue to cap near-term adoption outside well-resourced urban systems in the United States uterine fibroids treatment devices market.

Key Report Takeaways

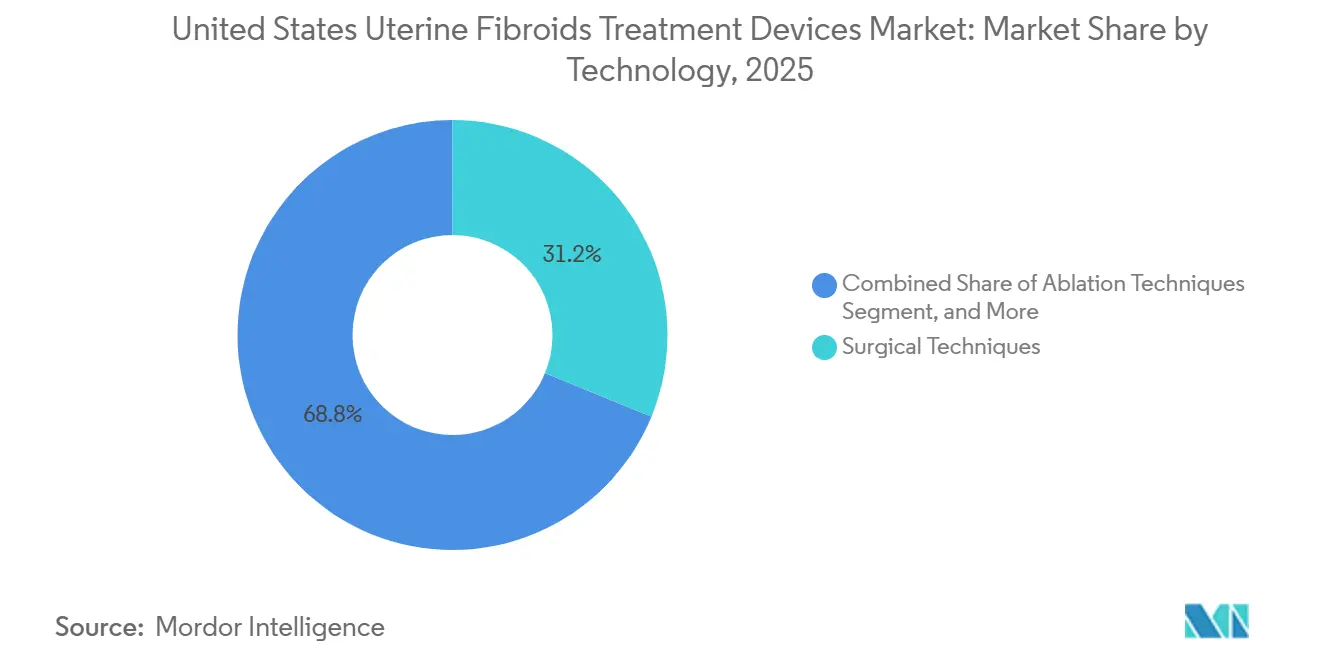

- By technology, surgical techniques held 31.23% of the United States uterine fibroids treatment devices market share in 2025, while ablation techniques are projected to expand at a 7.41% CAGR through 2031.

- By mode of treatment, invasive treatment commanded 53.35% of the market in 2025, while minimally invasive treatment is forecast to grow at an 8.39% CAGR through 2031.

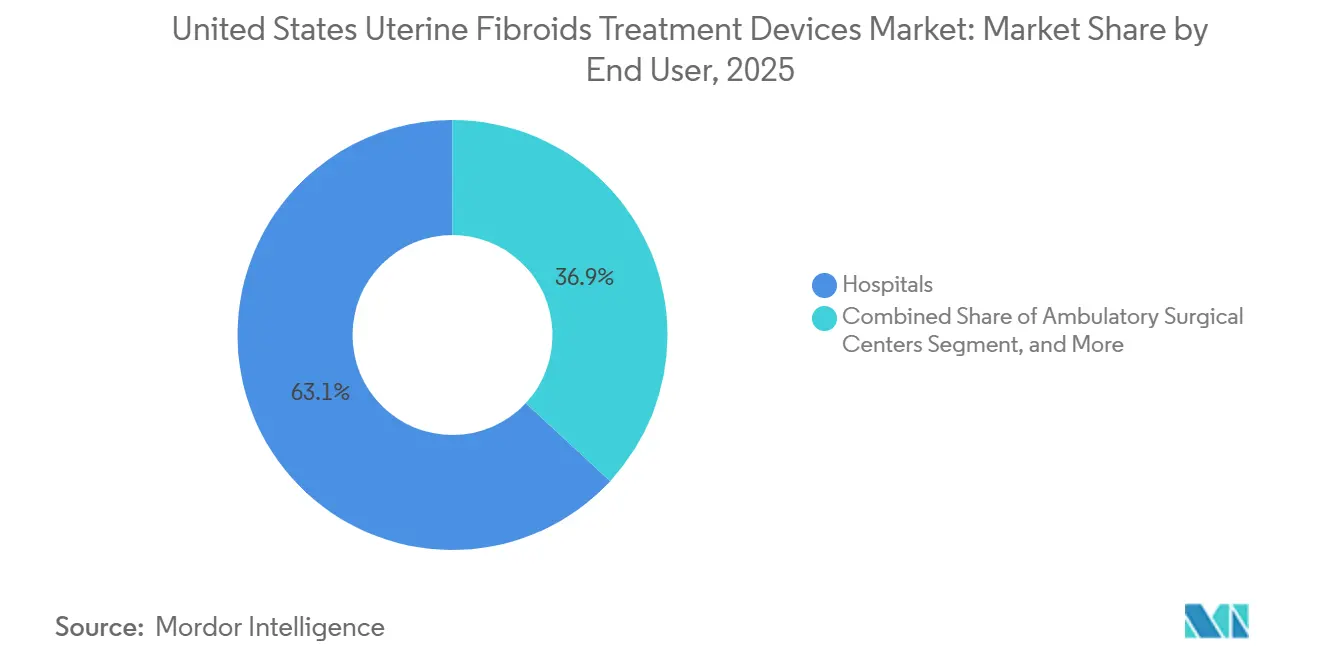

- By end user, hospitals held 63.12% share in 2025, while ambulatory surgical centers are expected to record the fastest growth at a 7.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Uterine Fibroids Treatment Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uterus-Preserving Treatment Preference | +2.1% | National, concentrated in Northeast and West Coast urban markets | Medium term (2-4 years) |

| Payer Expansion for Lap-RFA | +1.4% | National, with early gains in high commercial-insurer penetration states | Short term (≤ 2 years) |

| Shift to Office and ASC Hysteroscopy Workflows | +0.9% | National, concentrated in suburban and metro markets | Short term (≤ 2 years) |

| Hologic Portfolio Expansion After Sonata Integration | +0.7% | National | Short term (≤ 2 years) |

| Transradial UFE Workflow Improvements | +0.5% | Academic medical centers and high-volume IR practices in major metros | Medium term (2-4 years) |

| Imaging-Integrated Non-Incisional Ablation Platforms | +0.6% | Major metropolitan centers with advanced IR and radiology infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Uterus-Preserving Treatment Preference

Patient preference for uterus-sparing care has changed referral behavior across the United States uterine fibroids treatment devices market, especially in health systems that now offer multiple procedural alternatives before hysterectomy is considered. A 2025 JAMA Network Open study showed that hysterectomy still represented 73.4% of fibroid treatment encounters, while UFE accounted for only 3.5%, which shows how much room remains for device-led treatment substitution.[1]JAMA Network Open, “Disparities in Utilization of Uterine Fibroid Embolization,” JAMA Network Open, jamanetwork.com. This demand pattern is stronger among reproductive-age women who want symptom control without losing the uterus, and it matters even more in populations where fibroids appear earlier and with greater severity. In the United States uterine fibroids treatment devices market, that preference does not benefit only one modality because it lifts interest in RFA, embolization, and focused ultrasound at the same time. The result is a broader expansion path for manufacturers that can fit different patient profiles and care settings inside the same treatment journey.

Payer Expansion for Lap-RFA

Reimbursement has been one of the main commercial barriers for laparoscopic radiofrequency ablation, so payer coverage gains are now one of the most immediate growth supports for the United States uterine fibroids treatment devices market.[2]Medica, “Radiofrequency Ablation of Uterine Fibroids, Coverage Policy,” Medica, medica.com. Medica’s published policy covers laparoscopic RFA for uterine fibroids, and ACOG Practice Bulletin 228 continues to support the procedure in the clinical decision framework used by providers and payers. As coverage improves, more cases can move into ASC and office-based settings, which lowers system friction for ablation adoption and broadens the commercial reach of the United States uterine fibroids treatment devices market. This shift also favors manufacturers that built compact or single-use tools rather than relying only on large installed-capital systems. CMS fee schedule rules and local coverage processes continue to shape procedure economics, so reimbursement execution remains central to near-term adoption even when clinical support is already in place.

Shift To Office and ASC Hysteroscopy Workflows

The movement of gynecologic hysteroscopy into office and ambulatory settings is becoming a practical growth driver for the United States uterine fibroids treatment devices market because it addresses cost pressure, scheduling delays, and patient convenience at the same time. Innovations Surgery Center in Rockville became the first ASC in the Mid-Atlantic region to offer robotic-assisted gynecologic surgery in January 2026, which shows that more complex fibroid procedures are moving beyond the hospital campus. Office-compatible hysteroscopic tools are also reducing setup burden and helping practices perform more procedures without a full operating-room infrastructure. In the United States uterine fibroids treatment devices market, this shift improves recurring procedure volume for vendors with disposables and procedure kits rather than one-time capital sales. The commercial effect is important because it changes revenue mix toward repeat consumable use and helps manufacturers build steadier account activity across community gynecology practices.

Hologic Portfolio Expansion After Sonata Integration

Hologic’s January 2025 acquisition of Gynesonics created the first dual-modality RFA portfolio in the United States uterine fibroids treatment devices market, combining laparoscopic and transcervical fibroid ablation under one commercial structure. The FDA then cleared Sonata System 2.2 in April 2025, which gave Hologic an updated platform for continued rollout after the integration.[3]U.S. Food and Drug Administration, “510(k) Premarket Notification K250705, Sonata Transcervical Fibroid Ablation System 2.2,” U.S. Food and Drug Administration, accessdata.fda.gov. This portfolio now allows Hologic to address different patient pathways with one sales force, which strengthens its position in hospital systems and higher-volume community accounts. In the United States uterine fibroids treatment devices market, that kind of channel breadth is difficult for single-product competitors to match because physician access, training, and contracting all improve when the vendor can cover multiple care scenarios. The integration also narrows the time window for smaller challengers that previously competed against only one RFA modality at a time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven Reimbursement for MRgFUS | -0.8% | National, disproportionate in non-coastal and small-metro markets | Medium term (2-4 years) |

| Fertility and Pregnancy Evidence Gaps | -0.5% | National | Medium term (2-4 years) |

| Rural Interventional Radiology Access Shortage | -0.6% | Rural and semi-rural US counties, especially the Southeast and Midwest | Long term (≥ 4 years) |

| Morcellation-Related Safety Controls | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uneven Reimbursement for MRgFUS

MRgFUS remains clinically relevant in the United States uterine fibroids treatment devices market, but commercial uptake is still limited because payers continue to classify the relevant CPT codes as investigational. Cigna, Blue Shield policies, and similar payer positions keep most volumes concentrated in academic centers where alternative funding or research pathways are more realistic. That gap between FDA approval and broad reimbursement slows market conversion even when the clinical value proposition is clear. In the United States uterine fibroids treatment devices market, this means non-invasive platforms have not translated their technology profile into wide commercial volume. Until a stronger cost-effectiveness case is accepted at scale, MRgFUS will likely remain more important in select centers than in broad routine care.

Fertility And Pregnancy Evidence Gaps

Evidence on fertility and pregnancy outcomes still shapes treatment choice in the United States uterine fibroids treatment devices market, especially for women who want future conception and are weighing minimally invasive options against myomectomy. A 2026 systematic review reported favorable fertility outcomes for laparoscopic and hysteroscopic myomectomy, while noting that ablative approaches still need stronger prospective reporting for fetal and pregnancy outcomes. That evidence gap drives conservative referral behavior, with physicians more likely to default to myomectomy when fertility remains a primary treatment objective. The effect is important because reproductive-age women represent a major treated population across the United States uterine fibroids treatment devices market. Manufacturers that can produce stronger multicenter fertility data will be better positioned to expand clinical acceptance and strengthen longer-term guideline support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Ablation Disrupts the Surgical Baseline

Surgical techniques held 31.23% of the United States uterine fibroids treatment devices market share in 2025, which kept surgery as the largest technology category by revenue. That position remained supported by hysterectomy and myomectomy, which continue to offer definitive symptom resolution and strong institutional familiarity. A 2025 JAMA Network Open analysis found that hysterectomy represented 73.4% of fibroid treatment encounters nationally, which shows why surgical volume still anchors the technology mix. Broad insurance coverage and well-established hospital workflows also helped preserve surgical relevance across the United States uterine fibroids treatment devices market. Laparoscopic Techniques stayed between surgery and ablation in the adoption curve, with robotic-assisted myomectomy gaining ground as da Vinci access expands across outpatient sites.

The United States uterine fibroids treatment devices market size for ablation techniques is projected to grow at a 7.41% CAGR through 2031, making it the fastest-growing technology group. This growth reflects Hologic’s dual-platform RFA position after the Gynesonics integration and rising physician comfort with transcervical and laparoscopic workflows. The Sonata pivotal study reported a 2.2-day median return to normal activity, which aligns with patient preference for lower-disruption treatment paths. MRgFUS and USgHIFU remain part of the ablation opportunity, but reimbursement limits still restrict their contribution to the United States uterine fibroids treatment devices market. Embolization Techniques remain clinically established, and Merit’s Embosphere data continue to support strong physician loyalty in a consumable-driven part of the portfolio mix.

By Mode of Treatment: Minimally Invasive Routes Gain Procedural Share

Invasive treatment commanded 53.35% of the market in 2025, which shows that open and robotic-assisted surgery still formed the largest treatment pathway by revenue. This leadership persisted because many hospitals already had mature coding, credentialing, and surgical referral systems for hysterectomy and myomectomy. Reimbursement structure also matters, since payer policy can steer treatment selection even when alternative options are clinically available. In the United States, the uterine fibroids treatment devices industry kept invasive procedures deeply embedded in institutional practice, especially for patients with larger fibroids, more complex presentations, or physicians who prefer definitive surgical management. Robotic surgery added resilience to the invasive segment because hospitals and larger outpatient centers already understand the da Vinci workflow and have started extending it into ASC environments.

Minimally invasive treatment is forecast to grow at an 8.39% CAGR from 2026 to 2031, which puts it well above the overall rate of the United States uterine fibroids treatment devices market. The main drivers are hysteroscopic and laparoscopic procedures moving into ASCs and office settings, plus a stronger commercial scale for RFA systems after Hologic’s platform consolidation. Non-invasive Treatment remains the smallest mode, but it continues to attract strategic attention from health systems and device developers that want to compete on recovery time and patient experience. Profound Medical and Pro Familia reported 500 Sonalleve MRI-guided HIFU procedures at one center in February 2026, which adds useful real-world evidence for incision-free treatment models. The FDA’s higher evidentiary burden for MRgFUS under the PreMarket Approval path continues to slow iteration compared with the 510(k) route used by most RFA systems.

By End User: Hospitals Anchor Volume, ASCs Lead on Growth Rate

Hospitals retained 63.12% share in 2025, which kept them as the core end-user base in the United States uterine fibroids treatment devices market. Their lead reflects the concentration of interventional radiology suites, MRI capability for MRgFUS, and operating resources needed for higher-complexity surgical cases. Academic medical centers also remained important because they train physicians on Lap-RFA, robotic myomectomy, and evolving embolization workflows. Hospital-affiliated IR programs still handle most UFE activity, which keeps embolization volumes tied to larger urban systems rather than broadly distributed community sites. This hospital-centered structure continues to shape referral patterns, capital allocation, and procedure concentration across the United States uterine fibroids treatment devices market.

The United States uterine fibroids treatment devices market size for Ambulatory Surgical Centers is projected to grow at a 7.81% CAGR through 2031, making ASCs the fastest-growing end-user category. Favorable reimbursement for laparoscopic and hysteroscopic procedures and lower operating overhead are encouraging physicians to shift eligible cases into these settings. The January 2026 robotic gynecologic surgery launch at Innovations Surgery Center shows that even more advanced fibroid procedures are moving into freestanding outpatient environments. Office-based gynecology clinics are also gaining relevance, supported by products like Minerva Surgical’s HERizon Hysto-Kit, which was built to simplify in-office hysteroscopy setup. Interventional radiology centers remain more dependent on hospital affiliation because of capital and staffing needs, although telehealth consultations and mobile models are starting to improve access in harder-to-reach locations.

Geography Analysis

The Northeast and West Coast account for the largest share of the United States uterine fibroids treatment devices market size because they combine dense academic hospital networks, stronger commercial insurance penetration, and more established interventional radiology infrastructure. These regions also show strong demand for ablation and embolization procedures, especially in urban corridors where patients have access to multiple uterus-preserving treatment pathways. The prevalence gap reported between Black women and White women gives these metro markets a pronounced clinical demand base, particularly in cities with large Black and African American populations. Awareness activity around UFE and other uterus-sparing options has gained more traction in cities such as New York, Chicago, and Los Angeles, where referral depth and hospital capability are already present. The Cook Medical and Siemens Healthineers integrated iMRI Suite unveiled at SIR 2026 was aimed directly at this academic and high-resource tier, where imaging-led intervention is more feasible as the United States uterine fibroids treatment devices market evolves.

The South and Midwest present a less favorable access profile for the United States uterine fibroids treatment devices market, even though disease burden remains high in many communities. A very small share of UFE procedures occurred in rural hospitals, while more than 67% were concentrated in large urban facilities, which shows how strongly location still shapes treatment access. Registry-based reporting also showed that fewer than 1 in 6 US counties had a practicing SIR-registered physician, which continues to restrict UFE availability in rural and semi-rural areas. Telehealth-enabled consultations and mobile procedural programs are beginning to respond to this gap, but their reach remains limited in 2026.

The Mountain West and Pacific Northwest remain smaller in procedure volume, but they are important to the United States uterine fibroids treatment devices market because payer conditions and patient mix favor non-hysterectomy pathways. University-linked practices in California, Washington, and Colorado continue to act as early adopters for new ablation systems and imaging-integrated platforms. These geographies also benefit from a higher mix of privately insured patients, which tends to improve reimbursement conditions for newer procedures. As robotic gynecologic surgery expands in ASC settings and Intuitive Surgical continues to report strong procedure growth, the Pacific Coast is likely to contribute a disproportionate share of minimally invasive expansion within the United States uterine fibroids treatment devices market.

Competitive Landscape

The United States uterine fibroids treatment devices market is moderately concentrated, with leadership clustered in procedure-specific categories rather than controlled by one vendor across the full treatment spectrum. Hologic holds a stronger position in ablation after its USD 350 million acquisition of Gynesonics, which gave it both the Acessa ProVu Lap-RFA system and the Sonata transcervical RFA platform under one commercial umbrella. In embolization, Merit Medical Systems and Terumo Interventional Systems remain important because physician confidence in embolic performance directly influences repeat brand use and account loyalty. Intuitive Surgical leads robotic myomectomy through the da Vinci platform, supported by installed-base depth and continuing migration into outpatient settings. Boston Scientific’s October 2025 FDA clearance for OBSIDIO Conformable Embolic also shows that differentiation in embolization consumables remains an active competitive lane.

A major white-space opportunity in the United States uterine fibroids treatment devices market sits at the intersection of imaging and intervention. Cook Medical and Siemens Healthineers signaled that direction through their integrated Interventional MRI Suite, which reflects a longer-term bet on MRI-guided procedures in higher-acuity centers. If MRgFUS reimbursement broadens, companies such as INSIGHTEC and Profound Medical could benefit from a market structure that increasingly values precision imaging and incision-free treatment. Axora Medical’s January 2026 acquisition of Minerva Surgical’s assets also shows that competition is moving toward site-of-care efficiency, especially in office and ASC gynecology.

The next phase of competition in the United States uterine fibroids treatment devices market is likely to be shaped as much by software and workflow design as by hardware alone. The narrative around AI-assisted mapping and real-time treatment planning points to a future in which procedure accuracy, case selection, and workflow speed become stronger selling points. That favors companies that can combine clinical evidence, physician training, and broad channel access rather than relying only on a single device claim. It also means smaller vendors can still compete when they solve a specific site-of-care problem better than larger diversified players.

United States Uterine Fibroids Treatment Devices Industry Leaders

Boston Scientific Corporation

GE HealthCare Technologies Inc.

Medtronic

Olympus Corporation

Terumo Interventional Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: GEST 2026 (New York): A sub-analysis of the prospective, multicenter RAVI registry, sponsored by Terumo and presented by Jessica K. Stewart (UCLA), reported 100% procedural success for transradial UFE across 70 patients at 6 US academic centers, fibroid infarction rates of 90-100% at 12 months, and no major access-site complications. The analysis adds the first prospective multicenter evidence base supporting radial-access UFE and shows significantly faster same-day discharge rates versus transfemoral access, with direct implications for hospital throughput and patient experience.

- February 2026: Profound Medical and Pro Familia announced the milestone of 500 Sonalleve MRI-guided HIFU procedures at a single center, advancing the evidence base for non-invasive uterine fibroid and adenomyosis treatment and demonstrating real-world clinical velocity for an incision-free, uterus-preserving platform. The milestone is clinically significant because it represents the largest single-center Sonalleve uterine experience publicly reported to date.

- January 2026: Axora Medical acquired the business assets of Minerva Surgical on January 30, 2026, consolidating a minimally invasive gynecologic AUB portfolio, including the Symphion uterine fibroid and polyp resection system, Minerva EAS endometrial ablation, Genesys HTA, and Resectr, under a single commercial entity focused on office-based and ASC gynecology. The acquisition restructures the competitive landscape for hysteroscopic device competition.

- January 2026: Innovations Surgery Center (Rockville, Maryland) became the first ASC in the Mid-Atlantic region to offer robotic-assisted gynecologic surgery using the da Vinci Xi platform, explicitly including fibroid, endometriosis, and adenomyosis cases. The development documents that complex fibroid surgery, historically requiring hospital infrastructure, is now commercially viable in a freestanding ASC, accelerating the site-of-care shift.

United States Uterine Fibroids Treatment Devices Market Report Scope

The United States Uterine Fibroids Treatment Devices Market encompasses the medical instruments, imaging systems, and surgical tools used to diagnose and manage symptomatic uterine fibroids. It includes devices for minimally invasive procedures (like radiofrequency ablation), non-invasive techniques (like focused ultrasound), and invasive surgeries (like myomectomies and hysterectomies).

The United States Uterine Fibroids Treatment Devices Market is segmented by technology, mode of treatment, and end user, reflecting the wide range of clinical approaches used to manage fibroids. By technology, the market includes surgical techniques such as hysterectomy and myomectomy; laparoscopic techniques, including laparoscopic myomectomy and myolysis; ablation techniques, such as laparoscopic radiofrequency ablation, transcervical radiofrequency ablation, MRI‑guided focused ultrasound, and ultrasound‑guided high‑intensity focused ultrasound; and embolization techniques, including uterine fibroid embolization, embolic microspheres, and PVA particles.

By mode of treatment, the market is categorized into invasive treatments such as open surgery and robotic‑assisted surgery; minimally invasive treatments, including laparoscopic procedures, hysteroscopic procedures, and uterine artery embolization; and non‑invasive treatments such as MR‑guided focused ultrasound and ultrasound‑guided high‑intensity focused ultrasound. By end user, the market serves hospitals, ambulatory surgical centers, office‑based gynecology clinics, and interventional radiology centers.

| Surgical Techniques | Hysterectomy |

| Myomectomy | |

| Laparoscopic Techniques | Laparoscopic Myomectomy |

| Myolysis | |

| Ablation Techniques | Laparoscopic Radiofrequency Ablation |

| Transcervical Radiofrequency Ablation | |

| MRI-guided Focused Ultrasound | |

| Ultrasound-guided High-intensity Focused Ultrasound | |

| Embolization Techniques | Uterine Fibroid Embolization |

| Embolic Microspheres | |

| PVA Particles |

| Invasive Treatment | Open Surgery |

| Robotic-assisted Surgery | |

| Minimally Invasive Treatment | Laparoscopic Procedures |

| Hysteroscopic Procedures | |

| Uterine Artery Embolization | |

| Non-invasive Treatment | MR-guided Focused Ultrasound |

| Ultrasound-guided High-intensity Focused Ultrasound |

| Hospitals |

| Ambulatory Surgical Centers |

| Office-based Gynecology Clinics |

| Interventional Radiology Centers |

| By Technology | Surgical Techniques | Hysterectomy |

| Myomectomy | ||

| Laparoscopic Techniques | Laparoscopic Myomectomy | |

| Myolysis | ||

| Ablation Techniques | Laparoscopic Radiofrequency Ablation | |

| Transcervical Radiofrequency Ablation | ||

| MRI-guided Focused Ultrasound | ||

| Ultrasound-guided High-intensity Focused Ultrasound | ||

| Embolization Techniques | Uterine Fibroid Embolization | |

| Embolic Microspheres | ||

| PVA Particles | ||

| By Mode of Treatment | Invasive Treatment | Open Surgery |

| Robotic-assisted Surgery | ||

| Minimally Invasive Treatment | Laparoscopic Procedures | |

| Hysteroscopic Procedures | ||

| Uterine Artery Embolization | ||

| Non-invasive Treatment | MR-guided Focused Ultrasound | |

| Ultrasound-guided High-intensity Focused Ultrasound | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Office-based Gynecology Clinics | ||

| Interventional Radiology Centers | ||

Key Questions Answered in the Report

What is the 2031 outlook for uterine fibroids treatment devices in the United States?

The United States uterine fibroids treatment devices market is projected to reach USD 2.55 billion by 2031 from USD 1.82 billion in 2026, growing at a 6.95% CAGR.

Which treatment approach is expanding the fastest through 2031?

Minimally invasive treatment is forecast to grow at an 8.39% CAGR through 2031, ahead of the overall market pace, because more procedures are shifting into ASC and office settings.

Why are ablation devices gaining traction in fibroid care?

Ablation techniques are projected to grow at a 7.41% CAGR, supported by payer expansion for Lap-RFA, stronger guideline support, and Hologic’s dual-platform RFA portfolio.

Why do hospitals still account for the largest end-user share?

Hospitals held 63.12% share in 2025 because they house MRI systems, interventional radiology suites, and the surgical infrastructure needed for higher-complexity fibroid procedures.

What is limiting broader adoption of non-invasive fibroid treatment options?

Uneven reimbursement for MRgFUS remains the main brake, since important payer policies still classify the procedure codes as investigational, which limits broad commercial uptake.

Page last updated on: