United States Brachial Plexus Injury Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

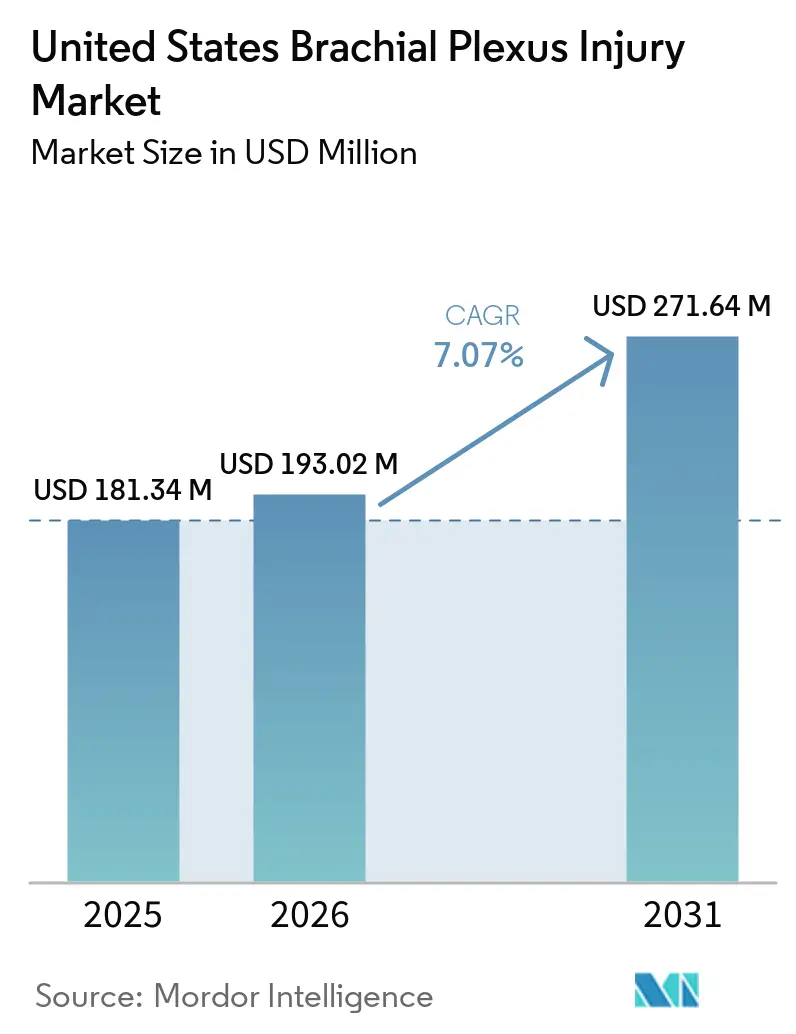

| Base Year Market Size (2025) | USD 181.34 Million |

| Market Size (2026) | USD 193.02 Million |

| Market Size (2031) | USD 271.64 Million |

| Growth Rate (2026 - 2031) | 7.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Brachial Plexus Injury Market Analysis by Mordor Intelligence

The United States Brachial Plexus Injury Market size is expected to increase from USD 181.34 million in 2025 to USD 193.02 million in 2026 and reach USD 271.64 million by 2031, growing at a CAGR of 7.07% over 2026-2031.

The United States brachial plexus injury market is supported by a steady injury pool, with 15,000 new cases reported each year across traumatic and obstetric presentations, and motorcycle accidents alone accounted for 32.8% of brachial plexus injuries in trauma registries. The United States brachial plexus injury market also draws structural demand from birth-related cases, as brachial plexus birth injuries occurred at 1.2 per 1,000 live births in the country and remained elevated against other industrialized nations. That pattern keeps procedure demand steady for early diagnostic work, microsurgical intervention, and long rehabilitation pathways, especially in infants with persistent upper limb deficits. The United States brachial plexus injury market is also benefiting from better reimbursement visibility for complex nerve repair, including a new CMS Level 3 Nerve Procedure Code in 2026 and a 221% increase in ambulatory surgical center reimbursement for nerve allograft repair since 2019. Even with that support, referral delays, the narrow 3 to 6 month surgical window, and the limited supply of fellowship-level peripheral nerve expertise still shape how much of the United States brachial plexus injury market can convert from diagnosis into surgery.

Key Report Takeaways

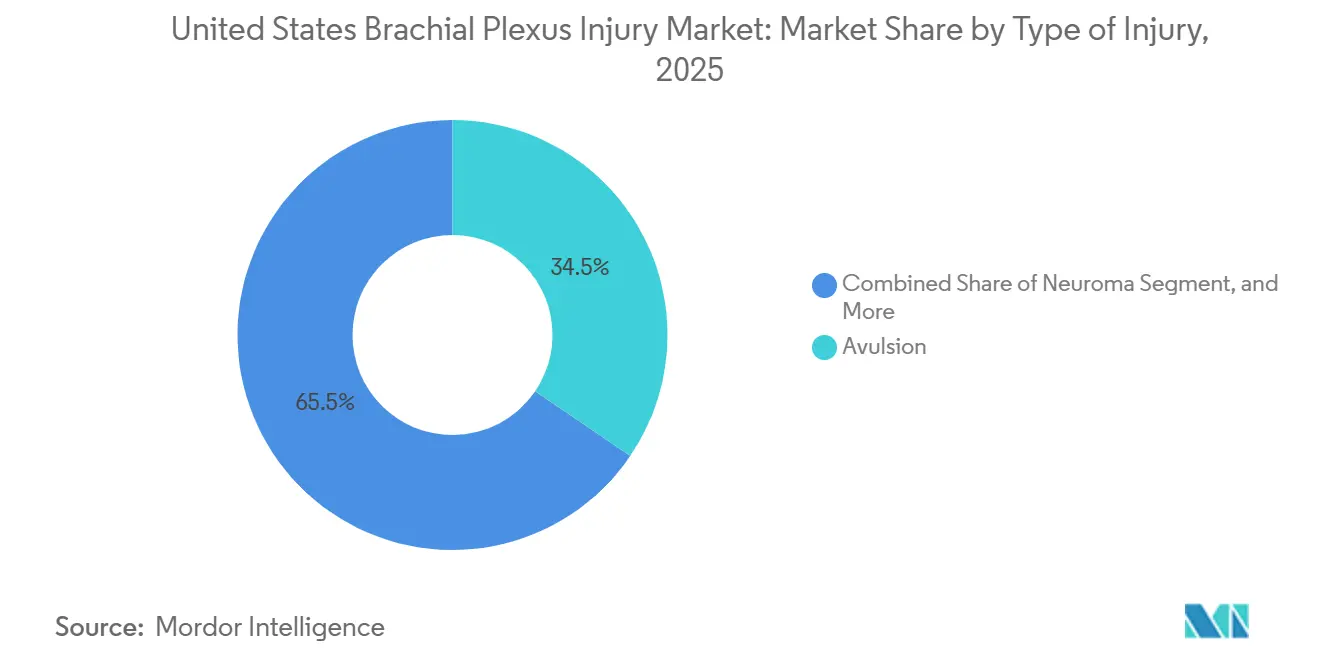

- By type of injury, avulsion held 34.48% of the United States brachial plexus injury market share in 2025, while neuroma is forecast to expand at 7.36% CAGR through 2031.

- By treatment type, surgical treatment accounted for 51.17% of the United States brachial plexus injury market size in 2025, while physical therapy is projected to advance at 8.87% CAGR through 2031.

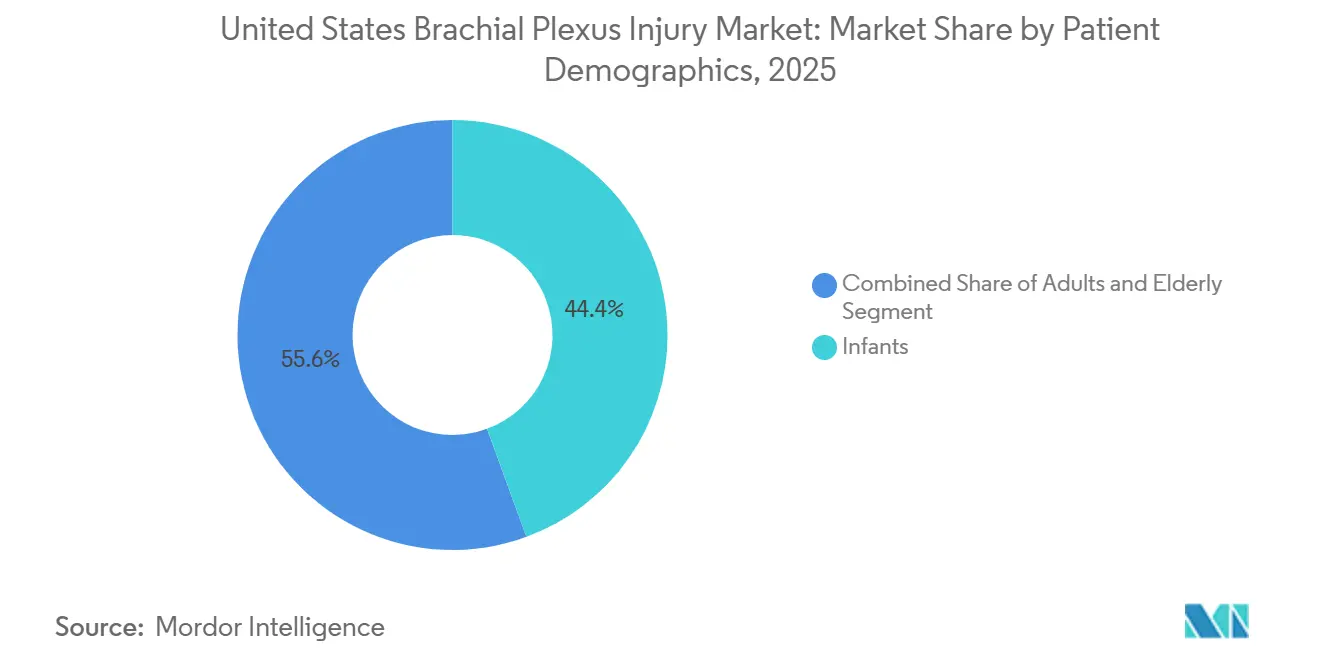

- By patient demographics, infants led with 44.42% revenue share in 2025, while the elderly segment is expected to grow at 7.87% CAGR through 2031.

- By diagnostic method, EMG represented 36.71% revenue share in 2025, while MRI is forecast to expand at 8.14% CAGR through 2031.

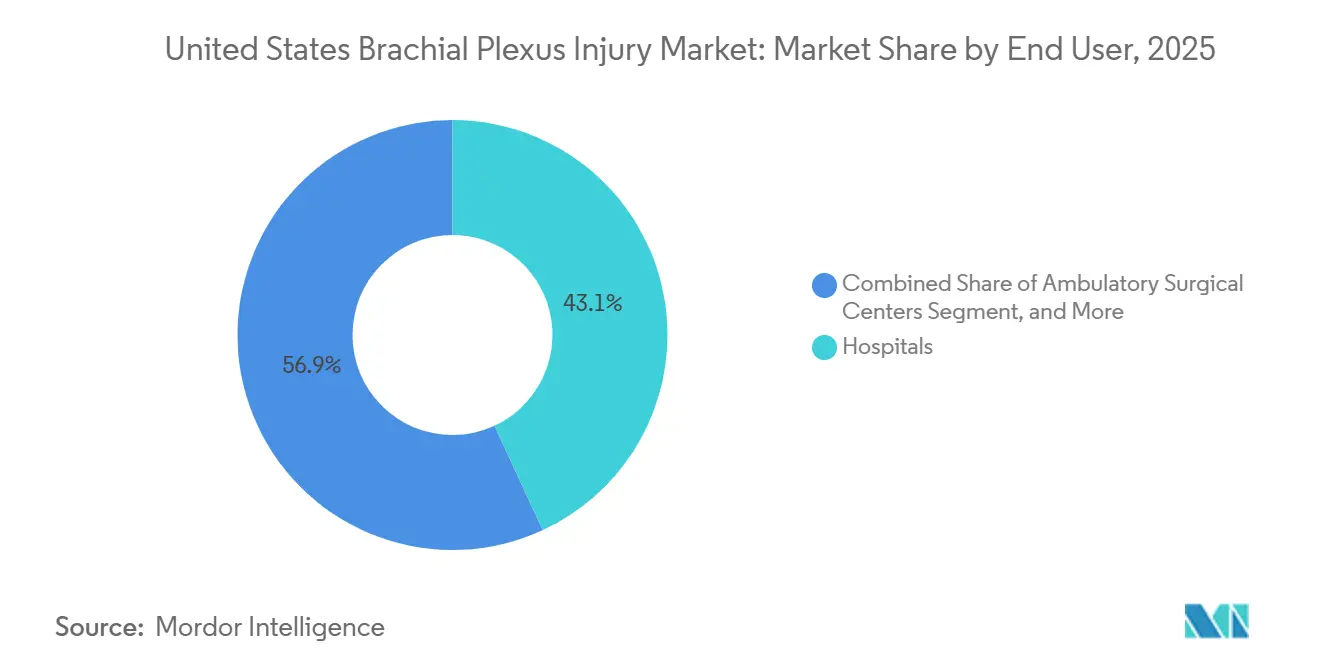

- By end user, hospitals held 43.12% of the United States brachial plexus injury market share in 2025, while ambulatory surgical centers are projected to grow at 7.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Brachial Plexus Injury Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising traumatic injury burden from road accidents and sports incidents | +1.2% | National, concentrated in South and Midwest states with high motorcycle and sports participation rates | Short term (≤ 2 years) |

| High surgical receptivity for severe root avulsion and complex plexus damage | +1.1% | National, with early volume gains in academic medical centers in Boston, New York, Chicago, and Houston | Medium term (2-4 years) |

| Growing clinical use of nerve transfer and microsurgical reconstruction | +1.0% | National, with early adoption concentrated in Level I trauma centers and academic brachial plexus programs | Long term (≥ 4 years) |

| Faster adoption of AI-assisted imaging and intraoperative nerve monitoring | +0.9% | National, highest in Northeastern and West Coast tertiary centers with imaging infrastructure investment | Medium term (2-4 years) |

| Expanding access to multidisciplinary nerve reconstruction and rehabilitation centers | +0.8% | National, with meaningful gains in Sun Belt states experiencing healthcare infrastructure expansion | Medium term (2-4 years) |

| Higher coverage for medically necessary reconstructive care and rehabilitation | +0.7% | National, with commercial insurance coverage driving short term volume while Medicare policy continues to evolve | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Traumatic Injury Burden From Road Accidents and Sports Incidents

Motorcycle accidents represented 32.8% of brachial plexus injury cases in trauma populations, and motor vehicle collisions accounted for another 16.7% of peripheral nerve injuries more broadly, which keeps a steady inflow of severe cases into the United States brachial plexus injury market.[1]Canadian Journal of Anesthesia, “Epidemiology of Peripheral Nerve and Brachial Plexus Injuries in a Trauma Population,” Canadian Journal of Anesthesia, pubmed.ncbi.nlm.nih.gov This pattern matters because road trauma produces high-force cervical root damage that is more likely to need advanced imaging, surgical triage, and long rehabilitation than lower-energy nerve injuries. The sports burden also matters, especially in younger patients, because pediatric traumatic brachial plexus injury data showed that motor vehicle accidents accounted for 35% of cases and sports incidents for 28%. Those same data showed that microsurgery was indicated in 41% of traumatic cases compared with 13% of birth injury cases, which means trauma cases generate a higher surgical conversion rate once they enter specialist care. As a result, the United States brachial plexus injury market continues to depend on trauma volume not just for patient counts, but for a disproportionate share of complex and high-value treatment episodes.

High Surgical Receptivity for Severe Root Avulsion and Complex Plexus Damage

The United States brachial plexus injury market remains highly responsive to severe cases because root avulsion and complete brachial plexus disruptions carried a 53% operative management rate, and nerve transfers were used in 48% of all brachial plexus injury surgeries. Avulsion injuries create strong procedure demand because preganglionic root loss prevents standard graft-based repair and pushes surgeons toward extraplexal donor strategies such as intercostal transfer or contralateral C7 transfer.[2]Handchirurgie Mikrochirurgie Plastische Chirurgie, “Der Kontralaterale C7 Transfer,” Handchirurgie Mikrochirurgie Plastische Chirurgie, thieme-connect.com Published clinical evidence in 2024 showed that contralateral C7 transfer is now viewed as a reliable pathway for patients with multiple root avulsions who lack intraplexal donor options, which expands the treatable population within the United States brachial plexus injury market. A 2025 meta-analysis also showed that upper trunk repairs achieved a 75% success rate, while complete injuries reached 29%, which reinforces the value of early case selection and rapid referral into specialized centers. That mix of technical feasibility and better-defined outcome expectations keeps surgery at the center of the United States brachial plexus injury market for the most disabling forms of nerve damage.

Faster Adoption of AI-Assisted Imaging and Intraoperative Nerve Monitoring

The United States brachial plexus injury market is seeing better diagnostic throughput as artificial intelligence compressed sensing for brachial plexus MRI reduced scan time by 55.1% at a 6.2x acceleration factor while preserving diagnostic image quality.[3]BMC Medical Imaging, “Comparison of Different Acceleration Factors of Artificial Intelligence Compressed Sensing for Brachial Plexus MRI Imaging Scanning Time and Image Quality,” BMC Medical Imaging, bmcmedimaging.biomedcentral.com That change brings neurography below the old workflow barrier of lengthy scan slots and makes advanced imaging easier to use in busy trauma settings. Ultrasound guidance is improving as well, because a convolutional neural network model validated for brachial plexus segmentation at the interscalene level achieved a mean Dice coefficient of 0.748 and outperformed earlier deep learning benchmarks. Faster and more consistent imaging matters for the United States brachial plexus injury market because delayed recognition often pushes patients outside the surgical timing window before they reach a referral center. Better imaging at community and tertiary sites therefore supports a larger downstream procedure pool, not only a better diagnostic experience.

Higher Coverage for Medically Necessary Reconstructive Care and Rehabilitation

Coverage support is improving the procedure economics of the United States brachial plexus injury market because complex brachial plexus surgeries are generally recognized by Medicare and private insurers as medically necessary reconstructive care. The ambulatory setting has become more attractive since Pacira BioSciences received CMS proposed separate reimbursement support for EXPAREL in both ambulatory surgical centers and hospital outpatient departments, effective January 1, 2025, which lowers pain-management cost pressure around outpatient nerve procedures. CMS also created a new Level 3 Nerve Procedure Code for 2026, which gives nerve allograft repair a more visible reimbursement framework in outpatient care and supports continued site-of-care migration. At the same time, local coverage determinations for peripheral nerve blocks are still evolving, and providers need tighter documentation when therapeutic pathways overlap with chronic pain management. Even so, broader recognition of reconstructive need and rehabilitation value gives the United States brachial plexus injury market a firmer reimbursement base than it had a few years ago.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow surgical timing window reduces treatable patient pool | -0.8% | National, most acute in rural and underserved markets where referral delays are longest | Short term (≤ 2 years) |

| Scarcity of subspecialty surgeons slows referral-to-treatment conversion | -0.7% | National, concentrated in non-metropolitan and Southern US markets | Long term (≥ 4 years) |

| High episode cost and rehabilitation intensity limit utilization | -0.6% | National, disproportionately affecting Medicaid and underinsured patient populations | Medium term (2-4 years) |

| Uneven access to specialized follow-up care limits functional recovery pathways | -0.5% | National, most severe in states with limited rehabilitation infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Narrow Surgical Timing Window Reduces Treatable Patient Pool

The United States brachial plexus injury market faces a hard biological limit because nerve regeneration moves at 1 mm per day, and delays beyond 3 to 6 months lower the chance of meaningful motor recovery. Early intervention matters in practical terms, since one multicenter series reported mean shoulder abduction of 110° for surgery performed within 6 months compared with 51° for delayed cases. This timing problem is especially important in the United States brachial plexus injury market because many patients first present to emergency departments or community hospitals that do not have a direct referral pathway into subspecialty nerve reconstruction. The result is not a full loss of demand, because those patients still use physical therapy and pain management, but it does remove them from the highest-value surgical funnel. That compression of eligible case volume limits how much revenue growth the United States brachial plexus injury market can realize from procedure innovation alone.

Scarcity of Subspecialty Surgeons Slows Referral-to-Treatment Conversion

The United States brachial plexus injury market also remains constrained by the limited number of surgeons with concentrated experience in complex plexus reconstruction. That shortage is visible in the way expertise clusters around a small group of academic and referral hubs, rather than across broad community-based orthopedic networks. The practical result is that patients in non-metropolitan regions often face longer referral times, more fragmented evaluation, and a greater chance of missing the preferred surgical window. This problem is harder to solve than a reimbursement gap because advanced brachial plexus reconstruction requires technical training, operating room support, and multidisciplinary follow-up that are not easily replicated outside specialized centers. Until that provider base widens, the United States brachial plexus injury market will continue to grow more slowly than the underlying burden of treatable cases would suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Injury: Avulsion Dominance Persists as Neuroma Demand Rises

Avulsion held 34.48% of the United States brachial plexus injury market share in 2025, which reflects its close link with the high-energy trauma patterns that dominate severe adult presentations. Avulsion is the most procedurally demanding form of brachial plexus injury because the nerve root is torn from the spinal cord, which removes the option of standard intraplexal grafting in many cases. That clinical severity raises the average treatment intensity in the United States brachial plexus injury industry, because surgeons often need extraplexal donor strategies such as intercostal or spinal accessory transfers. It also increases the role of academic referral centers, since complete and near-complete plexus injuries demand higher operating room coordination, advanced imaging, and longer follow-up.

Neuroma is the fastest-growing injury subtype, with a 7.36% CAGR through 2031, as clinicians are paying closer attention to painful nerve sequelae after incomplete recovery or failed reconstruction. That shift broadens the United States brachial plexus injury market beyond acute trauma repair and pushes more attention toward chronic functional loss, pain relief, and revision pathways. Rupture and stretch injuries remain important because they create a stable base of lower-acuity treatment demand across diagnostics, medication, therapy, and rehabilitation. Together, that mix leaves the United States brachial plexus injury market anchored by avulsion in value terms, while neuroma expands the addressable pool in later-stage care.

By Treatment Type: Surgical Primacy Intact but Rehabilitation Gains Clinical Ground

Surgical treatment accounted for 51.17% of the United States brachial plexus injury market size in 2025, which confirms that procedure-based care still drives the largest share of revenue. That segment includes nerve repair, grafting, transfer, and microsurgical reconstruction, which together carry the highest procedural complexity and the strongest reimbursement intensity in the United States brachial plexus injury market. Nerve transfer was used in 48% of all brachial plexus injury surgeries, which shows how central reconstructive strategy has become in current practice. Published outcomes also favor more advanced transfer protocols in selected cases, with the Oberlin 2 technique showing stronger sEMG signals for elbow flexion recovery than intercostal-to-musculocutaneous transfers.

Physical therapy is projected to grow at 8.87% CAGR through 2031, which makes it the fastest-growing treatment category in the United States brachial plexus injury market. This change reflects a broader clinical shift, because rehabilitation is increasingly treated as a co-primary pathway rather than something that starts only after surgery. German clinical guidance published in 2024 placed high importance on long-term ergotherapy and physiotherapy in interdisciplinary peripheral nerve care, and that position aligns with how leading U.S. programs now structure treatment planning. Medication and rehabilitation services, therefore, continue to support the United States brachial plexus injury industry even when delayed presentation, comorbidity, or payer rules prevent surgery.

By Patient Demographics: Birth Injury Volume Sustains Infant Segment

Infants accounted for 44.42% of the patient demographic segment in 2025, and that makes birth injury a central demand base for the United States brachial plexus injury market. Brachial plexus birth injuries occurred in the range of 1 to 3 per 1,000 births in U.S. literature, and the condition remains strongly associated with shoulder dystocia during delivery. U.S. incidence has also been described as high relative to other industrialized settings, and the relationship between cesarean rates and lower birth injury incidence adds a structural policy dimension to the United States brachial plexus injury market. Because early intervention often determines long-term arm and shoulder function, the infant segment supports steady demand for evaluation, observation, and microsurgical decision-making.

The elderly segment is expected to grow at 7.87% CAGR through 2031, which gives the United States brachial plexus injury market a second major demographic growth layer. Older patients bring a different clinical mix because fall-related injuries, polytrauma, and higher baseline comorbidity can alter both surgical selection and rehabilitation pace. Adult patients still remain the largest single pool for traumatic presentations tied to motor vehicle and occupational events, and they continue to anchor the highest-acuity surgical stream. This three-part demographic structure keeps the United States brachial plexus injury market broad, with infant cases stabilizing demand and adult and elderly cases shaping future growth.

By Diagnostic Method: EMG Anchors Volume as MRI Captures Complex Nerve Mapping

EMG held 36.71% of the diagnostic method segment in 2025, which reflects its role as the routine electrodiagnostic anchor in the United States brachial plexus injury market. It remains central to baseline denervation assessment, injury severity grading, and serial tracking of reinnervation after reconstructive care. That repeat-use profile supports steady utilization because EMG is relevant at diagnosis, during recovery, and in follow-up when clinicians need objective evidence of motor return. Ultrasound adds another useful layer by providing structural visualization and helping guide procedural planning in both anesthetic and surgical settings.

MRI is the fastest-growing diagnostic method, advancing at 8.14% CAGR through 2031, and that pace shows how imaging is moving deeper into decision-making for the United States brachial plexus injury market. Artificial intelligence compressed sensing has already shortened brachial plexus MRI neurography to under 3 minutes while preserving signal quality and interobserver consistency. The 3D SHINKEI sequence has also shown value in separating preganglionic from postganglionic injury, which directly affects surgical strategy and is not something EMG can resolve on its own. As a result, the United States brachial plexus injury market is shifting toward a more layered diagnostic workflow in which EMG retains volume leadership while MRI captures more of the complex mapping role.

By End User: Hospital Workflows Adapt as Ambulatory Centers Absorb Nerve Procedures

Hospitals held 43.12% of the United States brachial plexus injury market share in 2025, and they remain the dominant end-user setting because they control the most complex reconstructions. This leadership reflects their access to trauma teams, intraoperative neuromonitoring, advanced anesthesia support, and post-operative observation capacity that long and technically difficult plexus repairs often require. Specialty clinics and rehabilitation centers still play a large part in the United States brachial plexus injury market because patients need repeated evaluations, therapy sessions, pain management, and long-term monitoring over months or years. CMS reinforced the importance of specialized outpatient nerve repair when it created APC 5433, a new Level 3 Nerve Procedure Code effective January 2026, for nerve allograft repair.

Ambulatory surgical centers are projected to grow at 7.63% CAGR through 2031, making them the fastest-expanding end-user category in the United States brachial plexus injury market. That growth is tied directly to reimbursement changes, since nerve allograft repair reimbursement in ambulatory surgical centers has increased 221% since 2019. Wider outpatient coverage and dedicated peripheral nerve suites are making lower-acuity and selected reconstructive procedures easier to shift away from hospital outpatient departments. Even with that movement, the United States brachial plexus injury market is unlikely to see hospitals lose their central role, because the most severe avulsion and multistage cases still require resources that ambulatory centers cannot fully replicate.

Geography Analysis

The United States brachial plexus injury market benefits from a dense concentration of academic medical centers, higher procedural receptivity, and broader third-party payer support for complex nerve reconstruction than many peer markets. Within the country, expertise is centered in referral hubs such as Boston, New York, Chicago, Houston, and Los Angeles, where Level I trauma centers and dedicated brachial plexus programs receive complex cases from wider catchment areas. This concentration supports high-end surgical volumes, but it also means access is uneven outside major metro corridors. Global surgical practice data also showed that North America favored a later mean intervention age of 10.4 months for neonatal brachial plexus palsy, which extends the period of pre-operative observation and diagnostic testing that supports EMG and MRI demand.

Sun Belt states such as Texas, Florida, and Arizona represent some of the most attractive growth pockets within the United States brachial plexus injury market. Their appeal comes from population growth, expanding healthcare infrastructure, strong outpatient surgery investment, and exposure to road trauma patterns that support procedure demand. These states also carry a growing elderly population, which aligns with the fastest-growing patient demographic in the United States brachial plexus injury market. The same regional mix of demographic growth, trauma burden, and site-of-care expansion should keep the Sun Belt ahead of many slower-growing states over the forecast period.

Competitive Landscape

The United States brachial plexus injury market is moderately concentrated, with competition distributed across diversified medtech companies and a smaller group of nerve-focused specialists. Integra LifeSciences, Stryker, Medtronic, and Johnson & Johnson remain important incumbents because they combine broad surgical portfolios with long-standing hospital relationships and national distribution reach. Axogen holds a structurally important position in the United States brachial plexus injury market because it is closely tied to peripheral nerve repair and has been advancing both biologic and soft tissue products within the same treatment pathway. That position strengthened when AVANCE acellular nerve allograft received FDA biologics license approval in December 2025, which created a 12-year U.S. biosimilar exclusivity period for the product category. Axogen also expanded its portfolio in June 2024 with the launch of Avive+ Soft Tissue Matrix, which extended its reach into adjacent surgical bed protection and soft tissue support.

Strategy in the United States brachial plexus injury market is now moving beyond basic repair and toward broader nerve restoration and pain management. Medtronic’s announced USD 650 million acquisition of SPR Therapeutics in May 2026 added the SPRINT peripheral nerve stimulation system to its neuromodulation portfolio and showed that larger players are buying into non-opioid nerve-related pain care. CMS reimbursement changes are also reshaping competition because they improve the economics of outpatient nerve procedures and force established suppliers to balance hospital relationships with ambulatory growth. That favors companies that can support both complex reconstructive surgery in hospitals and lower-acuity or follow-on procedures in ambulatory settings.

White-space areas remain visible across the United States brachial plexus injury market, especially in neuroma-focused devices, elderly-specific reconstruction protocols, and tools that improve intraoperative nerve identification. Large incumbents still benefit from scale, but smaller, focused companies can move faster where clinical pathways are evolving, and reimbursement is becoming more favorable. This is why competitive pressure is rising even without a single dominant leader taking control of the entire United States brachial plexus injury market. The next phase of competition is likely to be defined less by broad catalog size alone and more by who can match product design, payer support, and surgical workflow to these narrower high-growth use cases.

United States Brachial Plexus Injury Industry Leaders

B. Braun Melsungen AG

Boston Scientific Corporation

Cardinal Health Inc.

Medtronic

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Medtronic plc announced its intent to acquire SPR Therapeutics for approximately USD 650 million, adding the FDA-cleared SPRINT peripheral nerve stimulation system to Medtronic's Neuromodulation portfolio. The deal expands Medtronic's presence in non-opioid, minimally invasive pain management for peripheral nerve injuries and is expected to close in the first half of Medtronic's fiscal year 2027.

- January 2026: Axogen closed an upsized public offering, raising USD 133.3 million in net proceeds from the sale of 4.6 million shares at USD 31 per share. USD 69.7 million was used to retire the company's term loan facility. CMS simultaneously implemented the new APC 5433 Level 3 Nerve Procedure Code effective January 2026, increasing nerve procedure reimbursement visibility for Axogen's product categories.

- December 2025: Axogen received FDA Biologics License Application approval for AVANCE acellular nerve allograft, covering sensory, mixed, and motor nerve discontinuities in adult and pediatric patients aged 1 month or older. Commercial availability of the licensed product was targeted for Q2 2026. The approval grants 12 years of U.S. biosimilar exclusivity.

United States Brachial Plexus Injury Market Report Scope

A Brachial Plexus Injury (BPI) refers to sudden damage, often by stretching, tearing, or avulsion, to the network of intertwined nerves branching off from the spinal cord in the neck. These nerves transmit electrical signals that control movement and feeling in the shoulders, arms, wrists, and hands. Common causes include severe trauma from motor vehicle or contact sport accidents, falls, and injuries during difficult childbirth.

The United States Brachial Plexus Injury Market is segmented across multiple categories. By type of injury, it includes Avulsion, Rupture, Neuroma, and Stretch injuries. By treatment type, the market is divided into Surgical Treatment, Physical Therapy, Medication, and Rehabilitation. By patient demographics, segmentation covers Infants, Adults, and the Elderly. By diagnostic method, the market is categorized into Electromyography, Ultrasound, and Magnetic Resonance Imaging. Finally, by end user, the market is segmented into Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Rehabilitation Centers.

| Avulsion |

| Rupture |

| Neuroma |

| Stretch |

| Surgical Treatment |

| Physical Therapy |

| Medication |

| Rehabilitation |

| Infants |

| Adults |

| Elderly |

| Electromyography |

| Ultrasound |

| Magnetic Resonance Imaging |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Rehabilitation Centers |

| By Type of Injury | Avulsion |

| Rupture | |

| Neuroma | |

| Stretch | |

| By Treatment Type | Surgical Treatment |

| Physical Therapy | |

| Medication | |

| Rehabilitation | |

| By Patient Demographics | Infants |

| Adults | |

| Elderly | |

| By Diagnostic Method | Electromyography |

| Ultrasound | |

| Magnetic Resonance Imaging | |

| By End User | Hospitals |

| Specialty Clinics | |

| Ambulatory Surgical Centers | |

| Rehabilitation Centers |

Key Questions Answered in the Report

What is the expected value of the United States brachial plexus injury sector by 2031?

It is projected to reach USD 271.64 million by 2031, rising from USD 193.02 million in 2026 at a 7.07% CAGR over 2026-2031.

Which injury type contributes the most revenue in this field?

Avulsion led in 2025 with 34.48% share because these cases are severe, technically demanding, and more likely to require complex reconstruction.

Why are infants such an important patient group in the United States?

Infants held 44.42% of the patient mix in 2025 because brachial plexus birth injuries remain relatively frequent in the country and often need early specialist follow-up.

Which treatment category is expanding the fastest through 2031?

Physical therapy is the fastest-growing treatment type with an 8.87% CAGR, reflecting its growing role as a co-primary pathway alongside surgery.

How is reimbursement changing procedure volumes for nerve repair?

CMS changes are improving outpatient economics, including a 221% increase in ASC reimbursement for nerve allograft repair since 2019 and a new Level 3 Nerve Procedure Code in 2026.

Which end-user setting is growing fastest for brachial plexus injury procedures?

Ambulatory surgical centers are growing fastest at 7.63% CAGR, although hospitals still lead in total share because they handle the most complex reconstructions.

Page last updated on: