Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

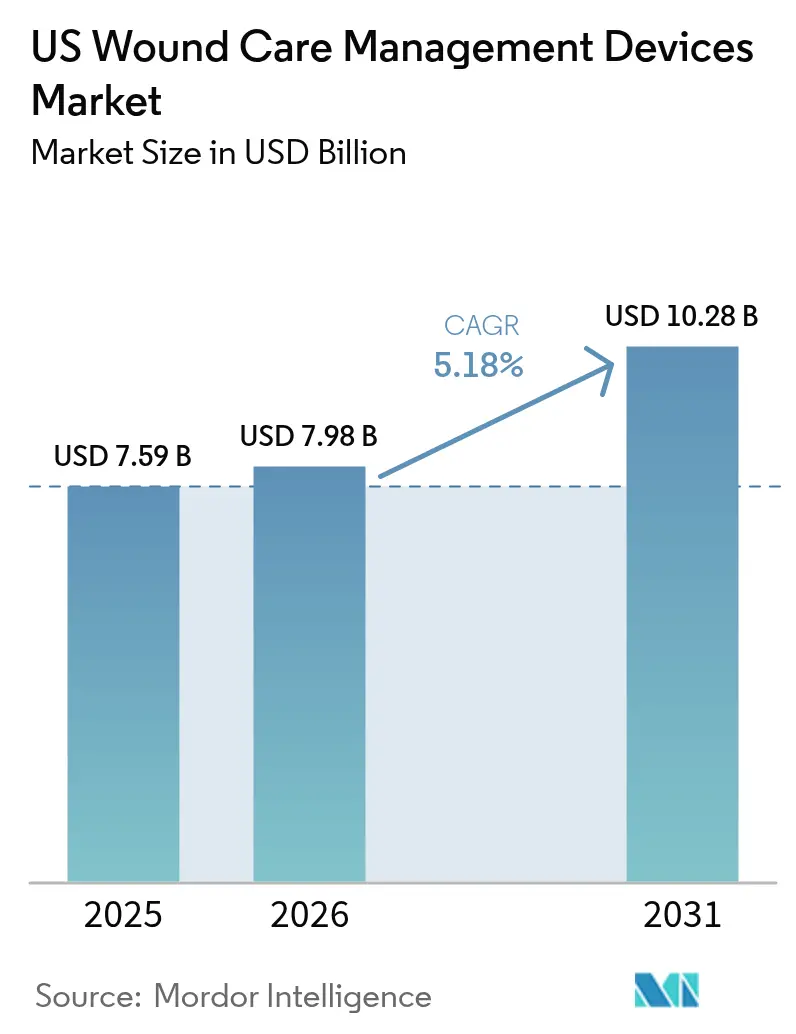

| Base Year Market Size (2025) | USD 7.59 Billion |

| Market Size (2026) | USD 7.98 Billion |

| Market Size (2031) | USD 10.28 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Wound Care Management Devices Market Analysis by Mordor Intelligence

The US wound care management devices market size was valued at USD 7.59 billion in 2025 and estimated to grow from USD 7.98 billion in 2026 to reach USD 10.28 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). Demand momentum reflects the convergence of an aging population, higher diabetes prevalence, and post-pandemic recovery in surgical volumes. Home-based treatment adoption, reimbursement incentives for telehealth visits, and payer scrutiny of avoidable readmissions are reshaping procurement decisions. Leading manufacturers are accelerating digital integration—remote monitoring, predictive analytics, and smart dressings—to align with value-based care targets. In parallel, consolidation among suppliers is unlocking scale advantages in sourcing, clinical education, and bundled product offerings.

Key Report Takeaways

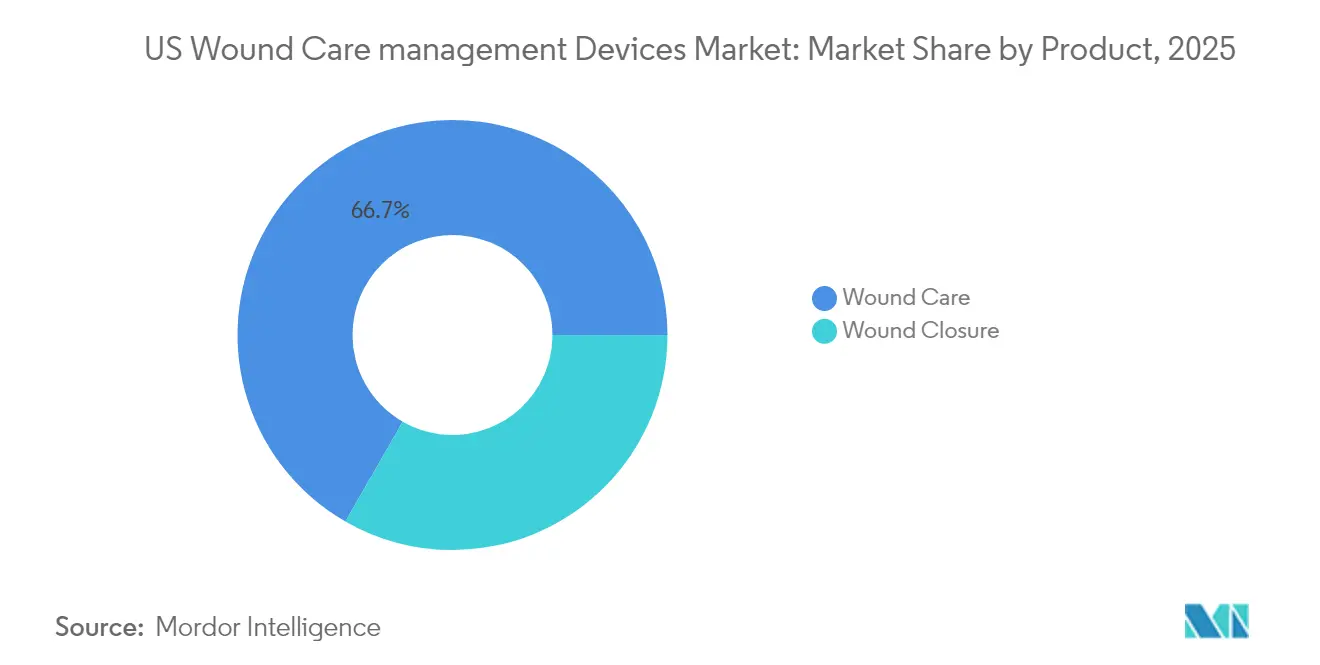

- By product type, wound care products held 66.70% of United States wound care management devices market share in 2025, while wound closure devices are expanding at a 5.74% CAGR through 2031.

- By wound type, chronic wounds accounted for 59.05% share of the United States wound care management devices market size in 2025; acute wounds are rising at a 5.93% CAGR.

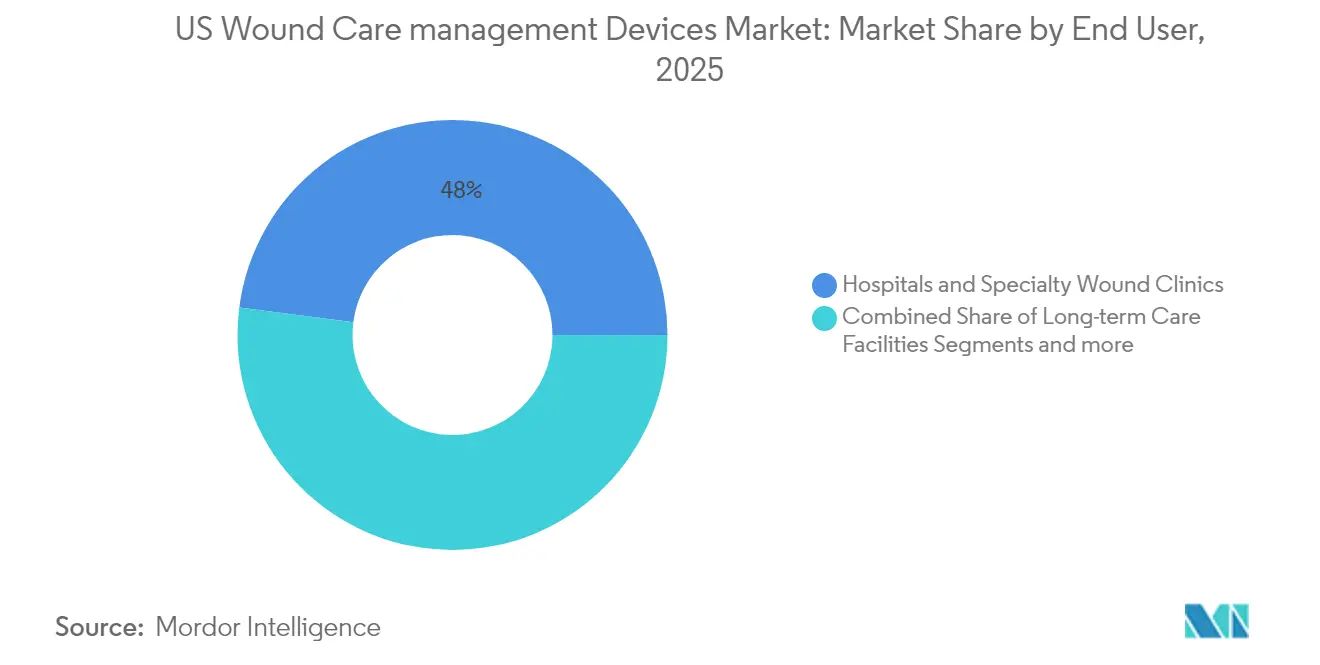

- By end user, hospitals and specialty clinics retained a 47.95% share in 2025, whereas home healthcare settings are advancing at a 6.12% CAGR.

- By mode of purchase, institutional procurement contributed 66.85% revenue in 2025; retail and over-the-counter channels show the fastest 6.27% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of chronic & diabetic wounds | +1.8% | National; concentrated in Southeast, Southwest | Medium term (2-4 years) |

| Growing volume of surgical procedures | +1.2% | National; higher impact in urban centers | Short term (≤ 2 years) |

| Rising geriatric population base | +1.5% | National; early gains in Florida, Arizona, Texas | Long term (≥ 4 years) |

| Rapid adoption of advanced therapies such as NPWT and skin substitutes | +0.9% | National; led by Northeast and West Coast | Medium term (2-4 years) |

| Reimbursement-linked telehealth & smart dressing deployment | +0.8% | National; faster adoption in rural areas | Short term (≤ 2 years) |

| Rising hospital-acquired wound cases and infection control mandates | +1.1% | National; higher impact in large hospital systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing incidence of chronic and diabetic wounds

Chronic wound prevalence among Medicare beneficiaries rose, equating to roughly 8.2 million patients requiring ongoing management. Diabetic foot ulcers alone incur a large sum in annual Medicare spending and show a high recurrence rate within one year. Geographic clustering in Texas, Florida, and California stems from elevated diabetes prevalence, reinforcing regional demand for advanced dressings, NPWT systems, and adjunctive therapies.

Growing volume of surgical procedures

Annual surgical incisions have rebounded to nearly 100 million, each requiring closure devices or dressings. The outpatient migration of procedures fuels demand for portable NPWT pumps and bio-active tissue adhesives suited to home recovery. Johnson & Johnson’s Ethizia wound-sealing patch exemplifies this trend, offering hemostasis plus antimicrobial protection. Hospitals emphasize technologies that lower surgical site infection costs, which can exceed USD 20,000 per readmission.

Rising geriatric population base

Adults aged ≥ 65 years represent the fastest-growing demographic and account for a disproportionate share of pressure ulcers and venous leg ulcers. States with large retiree communities—Florida, Arizona and Texas—are early adopters of smart dressings that alert caregivers to exudate changes. CMS coverage of telehealth-based caregiver training further supports remote management models.

Rapid adoption of advanced therapies such as NPWT and skin substitutes

Single-use NPWT systems reduce total treatment costs by up to 41% versus conventional pumps. Smith+Nephew’s lightweight RENASYS EDGE platform enhances patient mobility and recently earned a Red Dot design award. Interim suspension of proposed local coverage determinations on skin substitutes in 2025 preserves near-term reimbursement access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA regulations & CMS coding hurdles | -0.7% | National regulatory impact | Medium term (2-4 years) |

| High total cost of care and device pricing | -0.5% | National; higher impact in rural areas | Short term (≤ 2 years) |

| Heightened payer scrutiny of skin substitutes | -0.4% | National; concentrated in high-utilization states | Medium term (2-4 years) |

| Shortage of certified wound-care specialists | -0.6% | National; acute in rural and underserved areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent FDA regulations and CMS coding hurdles

The FDA has proposed reclassifying antimicrobial dressings, pushing many products from the 510(k) pathway to Class III PMA. Manufacturers must also comply with updated Quality System Regulation amendments aligning with ISO 13485 standards by 2026. Parallel CMS policy demands peer-reviewed evidence for skin substitutes, prompting longer and costlier clinical programs.

High total cost of care and device pricing

Advanced dressings and adjunctive devices can raise episode-of-care charges beyond payer reimbursement limits, particularly in rural hospitals with tight operating margins. Providers mitigate budget pressure by forming group purchasing organization contracts and adopting outcome-based payment models that favor devices that lower readmissions. Telehealth triage and AI-guided monitoring reduce nursing visits, easing cost barriers in underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Device Innovation Drives Market Differentiation

The United States wound care management devices market share favored wound care products at 66.70% in 2025. Foam and hydrocolloid dressings have displaced traditional gauze due to better moisture control, extended wear, and decreased nursing workload. Antimicrobial agents embedded in dressings target biofilm formation without frequent changes, while flexible printed sensors capture pH, temperature, and exudate volume for real-time feedback.

Wound closure devices, though smaller in base revenue, are advancing at 5.74% CAGR. Tissue adhesives, absorbable strips, and sprayable sealants are gaining traction among surgeons who value faster application and improved cosmesis. Smart staplers equipped with compression sensors provide intraoperative guidance that lowers leak rates. Increasing bariatric and orthopedic volumes support demand for bio-active patches that combine hemostasis with infection suppression.

By Wound Type: Managing Complexity in Chronic and Acute Lesions

Chronic wounds retained 59.05% of the United States wound care management devices market share in 2025. Diabetic foot ulcers and pressure ulcers consume the largest share of Medicare spending, driving adoption of off-loading devices, NPWT, and skin substitutes that expedite closure. AI-driven imaging tools achieve expert-level accuracy in predicting healing trajectories, enabling earlier therapy escalation .

Acute wounds are expanding at a 5.93% CAGR as elective surgeries rebound and trauma care protocols intensify infection control. The United States wound care management devices market size for acute applications is poised to benefit from bio-resorbable sealants and negative-pressure dressings that shorten hospital stays. Burns constitute a niche segment where advanced dermal matrices like AVITA’s Cohealyx support scar minimization and rapid re-epithelialization.

By End User: Home Healthcare Transformation Accelerates Growth

Hospitals and dedicated wound clinics held 47.95% revenue share in 2025. Specialized centers report healing rates of 66.8%, attributable to multidisciplinary care teams and ready access to adjunctive modalities. Facilities that adopt integrated data dashboards reduce time-to-closure by tracking wound surface area, tissue type, and exudate trends.

Home settings represent the fastest 6.12% CAGR channel through 2031. Remote monitoring platforms transmit photos and sensor data to nurses who titrate dressings without in-person visits, decreasing skilled nursing utilization by double-digit percentages. The United States wound care management devices market size for home use will be reinforced by CMS billing codes G0541-G0543, which reimburse caregiver tele-training.

By Mode of Purchase: Institutional Contracts Face Retail Disruption

Institutional purchasing produced 66.85% of 2025 revenue. Hospitals rely on group purchasing organizations to negotiate tiered pricing and value-based clauses requiring suppliers to present readmission reduction data. Bundled payment pilots reward device bundles that compress the average length of stay for pressure ulcer cases.

Retail and OTC channels will grow quickest at 6.27% CAGR as patients self-manage lower-grade ulcers between clinic visits. Pharmacy chains expand wound care aisles to include foam dressings, alginate pads, and silver sprays previously limited to hospital supply. Direct-to-consumer e-commerce models ship personalized dressing kits accompanied by smartphone apps that remind users to change products and submit images for clinician review.

Geography Analysis

Regional demand aligns closely with demographic patterns and healthcare infrastructure density. The Northeast and West Coast account for the earliest adoption of sensor-enabled dressings and AI imaging because of higher physician specialist density and proximity to device R&D hubs. Academic medical centers in Boston, New York, and Los Angeles serve as reference sites for clinical trials, accelerating commercial uptake.

The Southeast and Southwest deliver the largest chronic wound volumes, catalyzed by elevated diabetes incidence. Texas and Florida combine large Medicare populations with robust outpatient clinic networks that generate steady sales of NPWT consumables. California, while boasting advanced care capabilities, also faces a burden from diverse socioeconomic groups, stimulating interest in low-cost smart dressings backed by tele-coaching.

Rural counties nationwide struggle with specialist shortages, prompting telehealth adoption rates that surpass urban averages. Portable imaging kits and AI-assisted decision support enable primary care physicians to triage and manage ulcers effectively. State Medicaid expansion status introduces reimbursement variability, but the CY 2025 Medicare final rule extends telehealth coverage for caregiver education, which is expected to narrow access gaps.

Regulatory Landscape

Wound care management devices in the United States are regulated by the US Food and Drug Administration (FDA) under a risk-based framework (Class I-III) for medical devices (e.g., under 21 CFR Part 878 for general and plastic surgery devices). Within wound care, the FDA maintains device-specific expectations through guidance and special controls for certain Class II products, including wound dressings with specific antimicrobial additives and low-energy ultrasound wound cleaners, shaping performance testing, labeling, and clinical evidence requirements.

A key compliance milestone is the FDA Quality Management System Regulation (QMSR), which takes effect on February 2, 2026 and aligns device quality requirements more closely with ISO 13485, increasing documentation and audit readiness needs across manufacturers and contract suppliers serving US providers. In parallel, 2026 trade-policy actions have surfaced as an operational variable for device supply chains: the Office of the United States Trade Representative (USTR) initiated proposed Section 301 tariff actions in June 2026, and the American Hospital Association (AHA) commented in July 2026 on the potential impact to medical device costs and access, reinforcing procurement scrutiny around verified-origin sourcing and supply continuity.

Competitive Landscape

The United States wound care management devices market is fragmented. Companies offer portfolios spanning advanced dressings, NPWT, closure devices, and digital platforms, enabling hospitals to streamline sourcing under bundled contracts. Smith+Nephew recently secured a USD 75 million Department of Defense award for advanced therapy systems, underscoring traction in complex wound indications.

Strategic M&A continues: Medline purchased Ecolab's surgical offerings for nearly USD 1 billion to deepen vertical integration. Coloplast acquired fish-skin graft innovator Kerecis to enter biologic matrices. Emerging entrants leverage precision sensors, electrical stimulation, and plasma therapy to carve niches. Swift Medical's platform has logged more than 50 million assessments, providing anonymized datasets that inform algorithmic product refinement.

Digital capabilities differentiate competitors as payers reward documented healing acceleration. [3]North Carolina State University. "Electric bandage holds promise for treating chronic wounds." ScienceDaily, sciencedaily.com Solventum's V.A.C. Peel and Place reduces application time to two minutes, addressing nursing labor shortages. Electric bandage prototypes at Science Daily demonstrate 30% faster closure, and cold atmospheric plasma devices target resistant biofilms. Genomic and microbiome-based personalization pipelines are emerging frontiers that may disrupt standard dressing paradigms over the next decade.

US Wound Care Management Devices Industry Leaders

-

ConvaTec Group PLC

-

Smith & Nephew

-

Medtronic

-

Solventum

-

Coloplast

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Care delivery migration to lower-acuity sites is creating whitespace for wound-care solutions that reduce visit frequency and standardize application in home health and outpatient pathways, aligning with payer attention to avoidable readmissions and remote management. This is translating into demand for extended-wear dressings and simplified negative pressure wound therapy workflows that lower nursing time, supported by manufacturers integrating digital documentation and monitoring into product portfolios to fit value-based purchasing. In the provider channel, the move toward centralized purchasing and tighter supplier rosters inside large health systems is encouraging broader, bundle-ready portfolios (advanced dressings, NPWT, and closure products) and evidence packages that demonstrate total-cost-of-care performance.

On the product side, 2026 FDA clearances and launches highlight opportunities in differentiated matrices and debridement options that address complex surgical and chronic wound cases. Examples include Kreate Medical receiving FDA 510(k) clearances in May 2026 for absorbable synthetic matrix product lines, Cuprina receiving FDA 510(k) clearance in June 2026 for MEDIFLY Maggots (a Lucilia cuprina maggot debridement product), and Ventris Medical receiving FDA 510(k) clearance in July 2026 for Connext Surgical Matrix, a collagen-based wound dressing for post-surgical complications. With the FDA having proposed reclassification of certain antimicrobial wound dressings and liquid wound washes (and the targeted May 2026 finalization not materializing by mid-2026), manufacturers are also prioritizing regulatory optionality and clinical evidence generation, which favors suppliers that can maintain continuity across 510(k)-cleared portfolios while preparing for higher-burden pathways if classification requirements tighten.

Recent Industry Developments

- July 2026: Smith+Nephew communicated a new German expert clinical consensus providing risk-based recommendations for single-use NPWT use on closed surgical incisions, supporting clinical adoption of its PICO 7 sNPWT offering. The guidance adds structured decision support that hospitals and surgeons can reference in protocol development and product selection.

- June 2026: Solventum introduced the V.A.C. Peel and Place Dressing for NPWT, designed for up to seven days of wear time using a multilayer construction with a polyurethane manifolding core. Longer wear time and simplified dressing management target fewer dressing changes and reduced staff burden in both inpatient and outpatient care.

- July 2024: AOTI received expanded FDA 510(k) clearance for its NEXA NPWT system covering acute, extended, and home care settings. The broader indicated-use footprint supports standardized NPWT utilization across care transitions and strengthens the case for institutional contracting around a single platform.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers revenue earned in the United States from wound care management devices used to treat acute and chronic wounds across clinical and home-health settings. It includes device-based therapies and advanced wound care products that are typically prescribed or used under clinical guidance.

Scope exclusions: We exclude over-the-counter first aid items like basic strips and commodity gauze that are not used under clinical supervision.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

We started by setting a clear line for what counts as a wound care management device in the US, and then we mapped the care settings where these products are purchased and used. Public sources were used to anchor demand drivers and care delivery shifts, such as CDC data on diabetes and chronic disease burden, CMS and Medicare utilization summaries, and NIH and PubMed literature on chronic wound prevalence and treatment patterns.

To make the inputs usable in a market model, we also tracked signals that explain purchasing and pricing, including US FDA device classifications and approvals where relevant, US Census and trade statistics for import and export directionality, and hospital and outpatient care indicators published by official agencies. Company filings, investor presentations, and credible press were reviewed to understand portfolio mix, price movement, and channel changes, and then a paid subscription for company financials, patent checks, and shipment level trade reads was used to sanity check direction and timing. The desk sources named here are illustrative rather than exhaustive, and other references were also used for data collection, cross-checks, clarification, and validation.

Primary Interviews and Surveys

Our primary work focused on confirming what is actually being bought in hospitals, wound clinics, and home-health channels, and how therapy choices are shifting for chronic wounds like diabetic foot ulcers and pressure ulcers. We spoke with a mix of clinicians, procurement and distribution stakeholders, and product and commercial leaders so that pricing, channel share, and utilization assumptions could be tested and corrected across the US.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | |

| Mid tier: 46% | Functional/Unit leaders: 30% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

The core sizing started with a top-down build where US wound burden and treated patient pools were converted into a device demand pool by care setting, then priced using realistic average selling prices. Once the totals were formed, they were corroborated with selective bottom-up approximations, such as sampled ASP times estimated procedure or dressing volumes by setting, followed by reasonability checks using supplier exposure visible in public financial disclosures.

Key model inputs included the share of chronic versus acute wounds treated in organized care, the penetration of advanced dressings and negative pressure wound therapy in eligible cases, shifts from inpatient to outpatient and home-health care, and reimbursement linked adoption patterns that affect utilization. Average price movement was handled by separating mix shift (for example, higher share of advanced therapies) from inflationary pricing, and gaps in any one product line were handled using proxy utilization ratios reviewed with interview feedback.

For forecasting, scenario analysis was applied to the near term, followed by an ARIMA style time series check on the final revenue trajectory so the curve stays consistent with the historical pace of adoption. The final forecast was then adjusted using expert consensus on category level growth headwinds and tailwinds, keeping the model practical and traceable to market inputs.

Data Validation & Update Cycle

We validated outputs by checking whether the implied per patient spend and per setting utilization looked realistic against independent healthcare signals, then reworked outliers until the logic was consistent. Large variances were reviewed by a second analyst, followed by an internal review so assumptions, math, and scope lines match the written narrative.

The report is refreshed annually, and interim updates are made when material events affect pricing, therapy adoption, or care delivery. Before delivery, an analyst runs a fresh pass of key inputs and market signals so clients receive the latest view.

Mordor Intelligence's USA Wound Care Management Devices Market Estimate Compared With Other Published Estimates

Published market sizes for US wound care management devices can differ more than buyers expect, even when the titles sound similar. The gaps usually come from how each publisher draws the line between clinically guided products and general wound supplies, plus differences in how pricing and timing are handled in the model.

When the estimate is refreshed, the biggest swing is often tied to whether average selling prices reflect recent mix shifts, and whether currency timing is aligned to the base year. Those checks are applied in the 2025 figure used by Mordor Intelligence. Some other estimates also expand the scope into the broader wound care market, which can pull in adjacent product buckets and raise the headline number even if device volumes are similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.59 B (2025) | |

| Industry Publisher A | USD 5.05 B (2024) | Uses an earlier base year and a narrower device-only definition, which can undercount advanced dressing usage routed through mixed clinical and home-health channels. |

| Healthcare Publisher B | USD 6.69 B (2024) | Represents the broader wound care market rather than devices only, and the definition can blend general wound supplies with clinically guided therapies and devices. |

The spread in the table mainly tracks back to scope boundaries and timing, not to a single growth assumption. By keeping the counted revenue tied to clinically guided device use and by updating pricing in step with mix and base-year timing, the final number stays traceable to inputs that can be rechecked and repeated.

Key Questions Answered in the Report

What is the current United States wound care management devices market size?

The market reached USD 7.98 billion in 2026.

How fast will the United States wound care management devices market grow?

It is projected to expand at a 5.18% CAGR, hitting USD 10.28 billion by 2031.

Which product segment is growing quickest?

Wound closure devices are increasing at a 5.74% CAGR through 2031, driven by tissue adhesives and bio-active patches.

Why is home healthcare adoption accelerating?

New Medicare billing codes reimburse telehealth caregiver training, and patients prefer recovery at home, supporting a 6.12% CAGR for the segment.

How are digital technologies influencing market competition?

AI-enabled imaging, smart sensors and remote monitoring platforms differentiate suppliers by proving faster healing and fewer readmissions.

What regulatory shifts should device manufacturers monitor?

The FDA’s proposed reclassification of antimicrobial dressings and the 2026 Quality System Regulation alignment with ISO 13485 will raise compliance requirements.

Page last updated on: