United States Enema Based Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

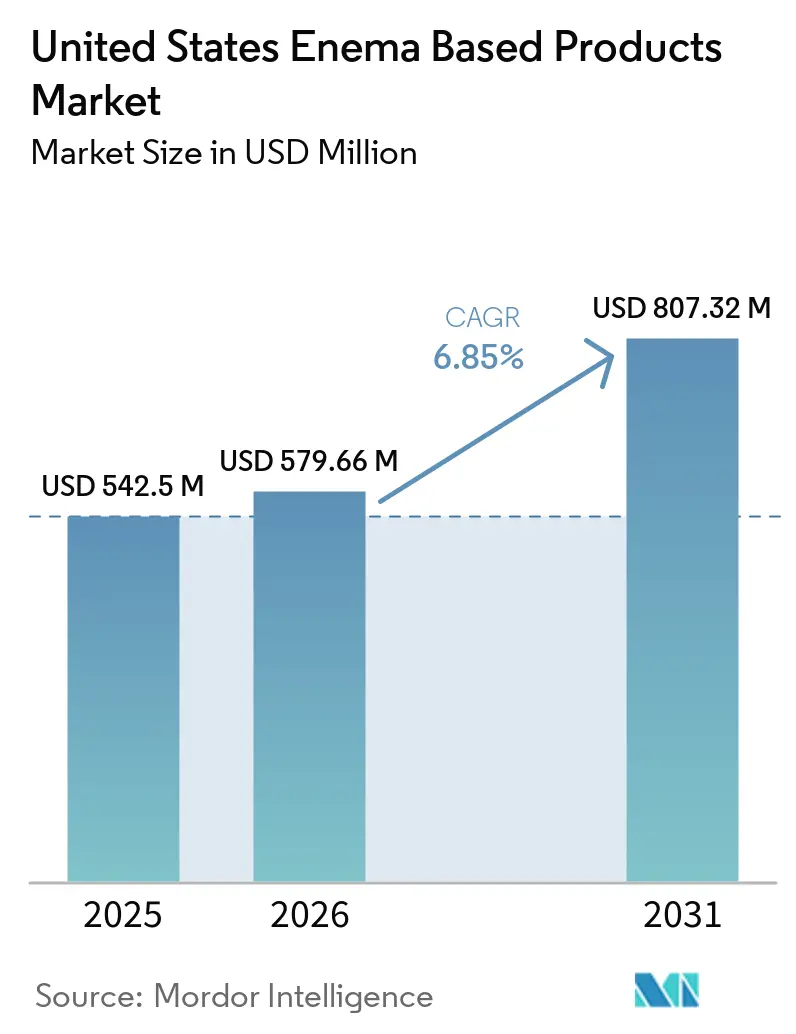

| Base Year Market Size (2025) | USD 542.5 Million |

| Market Size (2026) | USD 579.66 Million |

| Market Size (2031) | USD 807.32 Million |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Enema Based Products Market Analysis by Mordor Intelligence

The United States Enema Based Products Market size is expected to grow from USD 542.5 million in 2025 to USD 579.66 million in 2026 and is forecast to reach USD 807.32 million by 2031 at 6.85% CAGR over 2026-2031.

The market is supported by recurring demand from chronic constipation, especially among older adults, where constipation remains a persistent concern in both community and long-term care settings. The age profile of the country is reinforcing this demand base, since the population aged 65 and older reached 61.2 million and the national median age rose to 39.4 in 2025, which supports sustained need for gentler and caregiver-friendly bowel management products. The United States enema based products market is also being shaped by a steady move toward home-based care, which is expanding the role of pre-filled, easy-to-use, and reusable formats while raising the importance of product labeling, dosing clarity, and applicator design. Safety-related shifts in formulation are redirecting demand from phosphate-heavy products toward saline and oil-based alternatives in older and comorbid populations, while alternative preparations continue to attract consumer attention outside formal clinical pathways. Competitive activity in the United States enema based products market remains balanced between established OTC brands with strong retail visibility and institutional suppliers that compete through procurement reach, clinical support, and chronic-care platform development.

Key Report Takeaways

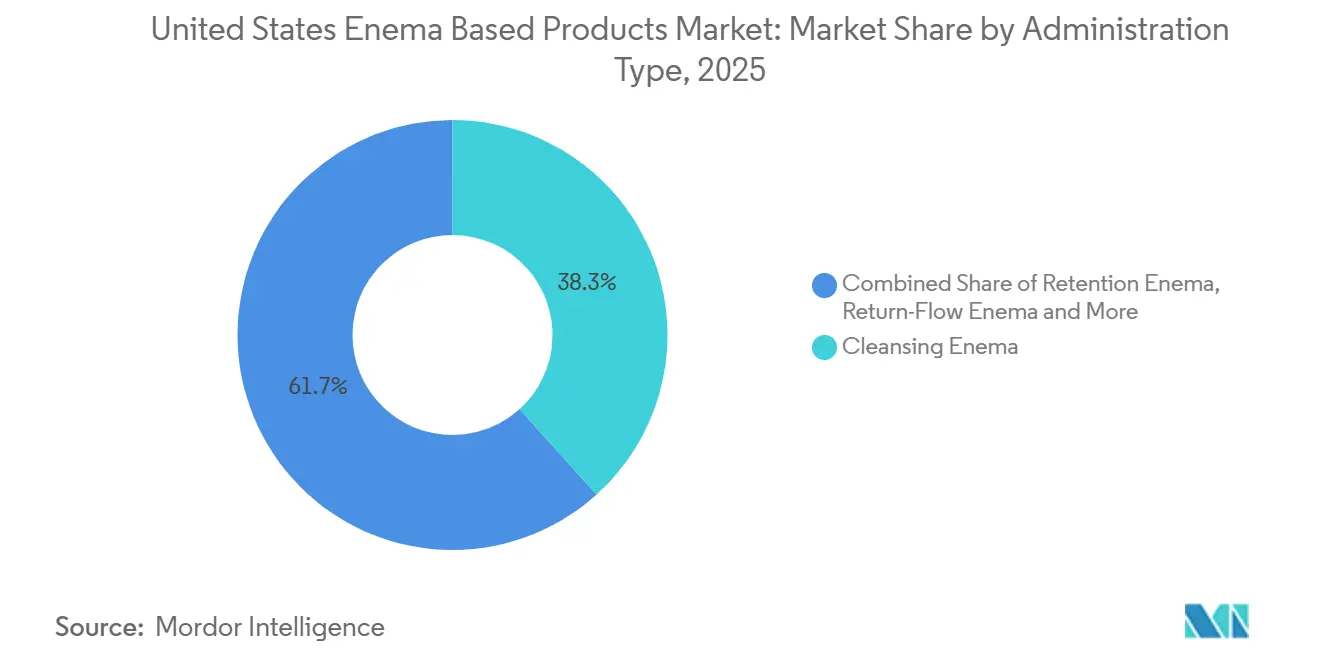

- By administration type, Cleansing Enema held 38.31% of the market in 2025, while Retention Enemas are forecast to expand at a 7.38% CAGR through 2031.

- By application, Constipation Relief held 42.24% of the market in 2025, while Intestinal Health Management is forecast to expand at a 7.52% CAGR through 2031.

- By preparation, Sodium Phosphate Enemas held 36.52% of the market in 2025, while Coffee Enemas are forecast to expand at a 8.55% CAGR through 2031.

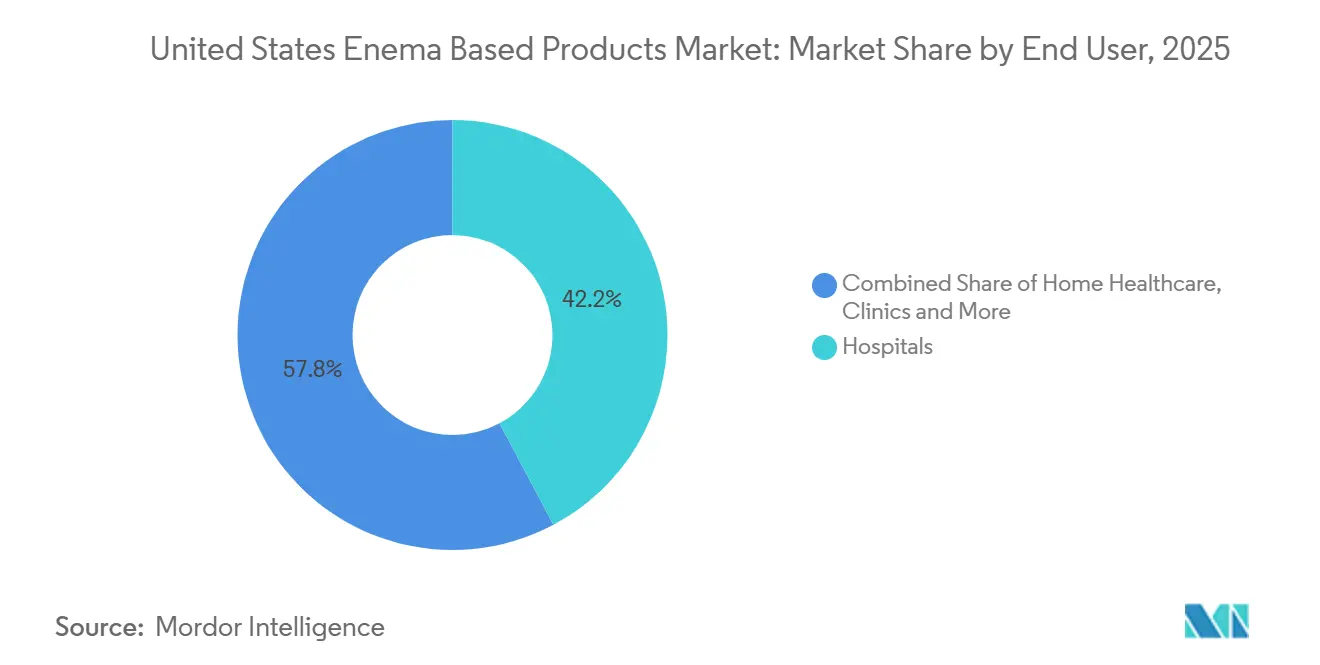

- By end user, Hospitals held 42.22% of the market in 2025, while Home Healthcare is forecast to expand at a 8.25% CAGR through 2031.

- By product format, Disposable Enema Kits held 45.52% of the market in 2025, while Reusable Enema Kits are forecast to expand at a 8.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Enema Based Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Constipation and Bowel Preparation Demand | +2.1% | National, with higher intensity in the South and Southeast aging communities | Short term (≤ 2 years) |

| Shift Toward Home-Based Self-Administration | +1.5% | National, with early gains in suburban and rural markets with limited clinical access | Medium term (2-4 years) |

| E-Commerce and Pharmacy Channel Expansion | +1.2% | National, accelerated in metro areas with high e-pharmacy penetration | Short term (≤ 2 years) |

| Safety-Driven Shift From Phosphate To Saline and Oil Formulations | +0.8% | National, highest adoption in geriatric and nephrology-focused care settings | Medium term (2-4 years) |

| Smart Packaging and Leak-Reduction Innovations | +0.5% | National, with early adoption in hospital procurement channels | Long term (≥ 4 years) |

| Preventive Digestive Health Behavior in Digitally Influenced Consumers | +0.6% | National, strongest in urban demographics aged 25-45 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Constipation and Bowel Preparation Demand

The United States enema based products market is closely tied to the recurring burden of chronic constipation in older age groups, where 30% to 40% of people over 65 report constipation as a persistent concern. This burden becomes more concentrated in institutional care, where up to 80% of long-stay nursing home residents are affected, creating steady and repeated demand rather than occasional use. The aging of the population is reinforcing this demand structure, since the 65-plus population reached 61.2 million and continues to expand. Clinical practice is also supporting utilization, because the 2025 consensus recommendations on bowel preparation reinforced standardized split-dose regimens and recognized adjunctive enema use in established protocols. In the United States enema based products market, this combination of age-related need, institutional density, and protocol-led bowel management keeps baseline demand structurally firm.

Shift Toward Home-Based Self-Administration

The United States enema based products market is benefiting from a steady shift of bowel management from supervised settings into the home. The U.S. Census Bureau reported that the national median age reached 39.4 in 2025, while the older population continued to grow, which supports higher demand for products designed for self-use and caregiver assistance. MedPAC reported a 19% FFS Medicare margin for freestanding home health agencies in 2025, which indicates that home-based care delivery remains financially viable under current conditions. That care model supports discharge pathways that shift bowel management toward products used outside hospitals and clinics. The home setting also changes the safety profile of the category, since the systematic review of self-administered coffee enema case reports documented colitis, electrolyte imbalance, and thermal injury, with no reported clinical efficacy. In the United States enema based products market, this is raising the value of pre-filled formats, ergonomic applicators, and clearer instructions that reduce user error.

E-Commerce and Pharmacy Channel Expansion

The United States enema based products market is positioned to benefit from continued expansion in OTC purchasing channels, which confirms the breadth of the consumer health channel that enema products can access. Within this category, digital purchasing matters more than it does for many other OTC products because privacy can remove a purchase barrier that limits in-store conversion. The FDA Additional Conditions for Nonprescription Use final rule, which became effective in January 2025, also creates a framework for digital self-selection and related nonprescription pathways[1]U.S. Food and Drug Administration, “Final Rule on Nonprescription Drug Product With an Additional Condition for Nonprescription Use,” FDA, fda.gov. That rule matters for the United States enema based products market because it supports broader acceptance of digital decision support in consumer bowel care. As physical and digital pharmacy channels continue to coexist, suppliers with strong e-commerce presentation, compliant labeling, and discreet fulfillment are better placed to capture demand that otherwise remains suppressed.

Safety-Driven Shift From Phosphate To Saline and Oil Formulations

The United States enema based products market is seeing a gradual mix shift as safety concerns alter prescribing behavior and consumer selection. Under 21 CFR 201.307, OTC sodium phosphate enemas carry mandatory warnings related to kidney disease, heart conditions, dehydration, dosage limits, and use beyond one enema in 24 hours. These restrictions are encouraging greater use of saline and mineral oil formulations in elderly and comorbid patients, especially where clinicians want lower risk bowel management options. This does not remove demand from the United States enema based products market, but it does redirect volume toward preparations viewed as safer in routine use. At the same time, coffee enemas remain the fastest-growing preparation type at 8.55%, even though the National Cancer Institute states that there is no scientific evidence supporting coffee enemas for treatment of any disease and published case reviews document safety concerns. The result is a split market where clinically grounded formulations hold medical relevance while non-clinical narratives continue to influence a portion of consumer demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social Stigma and User Discomfort | -1.2% | National, with highest suppression in conservative demographic and rural markets | Long term (≥ 4 years) |

| Safety Concerns and Adverse Event Risk | -1.0% | National, concentrated in elderly-care and home-use settings | Medium term (2-4 years) |

| Limited Reimbursement and Price Sensitivity | -0.8% | National, particularly affecting uninsured and lower-income demographics | Short term (≤ 2 years) |

| Substitution From Oral Bowel Regimens and Alternative Therapies | -0.7% | National, accelerating in primary care and digitally-engaged consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Social Stigma and User Discomfort

The United States enema based products market still faces a behavioral ceiling because many consumers remain uncomfortable with both the product category and the treatment method. That discomfort reduces first-time trial, limits repeat purchases, and also affects how openly patients discuss bowel issues with clinicians. Privacy in online purchasing can reduce some of this friction, but it does not fully solve hesitation that begins before a product search even starts. This is why neutral branding, discreet packaging, and plain-language instructions have become practical tools for expanding the reachable user base in the United States enema based products market. As long as embarrassment remains attached to category use, demand will continue to lag clinical need in parts of the market.

Safety Concerns and Adverse Event Risk

Safety concerns remain a direct restraint on the United States enema based products market because adverse events influence regulators, clinicians, caregivers, and consumers at the same time. The published review of self-administered coffee enema case reports documented colitis, electrolyte imbalance, thermal injury, and other complications without evidence of benefit. On the broader phosphate category, FDA labeling requirements for sodium phosphate enemas reflect continued concern around dehydration and renal risk, especially when products are misused. The National Cancer Institute also states that coffee enemas lack scientific support for disease treatment, which makes the fastest-growing preparation type one of the most exposed to scrutiny. In the United States enema based products market, this combination of safety alerts and weak consumer understanding can slow adoption even when overall need remains high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Administration Type: Retention Formats Gaining Clinical Relevance

Cleansing Enema held 38.31% of the United States enema based products market share within administration type in 2025, while Retention Enemas are projected to grow at a 7.38% CAGR through 2031. That pattern shows that the largest revenue pool still comes from bowel cleansing and immediate symptom management, even as clinically targeted use is expanding faster. Retention formats are gaining relevance because they support inflammatory bowel disease management and targeted drug delivery to the colonic mucosa, which gives this category a more protocol-driven demand layer. In the United States enema based products market, that makes retention products less exposed to casual substitution than purely OTC relief formats. It also shifts part of demand toward prescription-linked use cases where clinician preference, therapeutic consistency, and patient adherence matter more than broad shelf visibility.

This change is supported by product activity on the therapeutic side of the category. ANI Pharmaceuticals' mesalamine rectal suspension enema remained part of the clinical foundation of retention use after its FDA labeling update in February 2024[2]ANI Pharmaceuticals, “Mesalamine Rectal Suspension Enema Drug Label,” DailyMed, dailymed.nlm.nih.gov. Cleansing enemas still serve the acute-care and pre-procedural base of the United States enema based products market, but regulatory caution around sodium phosphate is gradually favoring saline-based and oil-based alternatives in older and comorbid populations. Carminative and return-flow enemas remain narrower categories, though both retain relevance in inpatient geriatric care and fecal impaction management. Their smaller scale leaves room for specialty suppliers that can tailor institutional offerings to long-term care and complex-care settings.

By Application: Preventive Bowel Health Expanding the Market's Clinical Mandate

Constipation Relief accounted for 42.24% share of the United States enema based products market size within application in 2025, while Intestinal Health Management is projected to expand at a 7.52% CAGR through 2031. This shows that the United States enema based products market still depends on constipation relief for its revenue foundation, but its faster growth is moving toward broader bowel health management. That shift reflects growing interest in sustained bowel regulation, microbiome-oriented care, and targeted rectal delivery in cases where oral therapy may be insufficient or poorly tolerated. The application mix is therefore moving from episodic rescue use toward longer-duration management in selected patient groups. In practical terms, that opens more room for clinically guided treatment pathways rather than one-time OTC purchase behavior.

Bowel Preparation for Procedures remains a stable and necessary application in the United States enema based products market because it is tied to established clinical workflows rather than discretionary demand. The 2025 U.S. Multi-Society Task Force update reinforced standardized bowel preparation practices and sustained the role of adjunctive enema use where clinically appropriate. Other applications, including pediatric fecal disimpaction, palliative care, and post-surgical recovery, represent a smaller share but still add meaningful demand across care settings. The growing recognition of constipation as a quality-of-life issue in oncology and end-of-life care is also widening the functional scope of the category. Manufacturers that support sustained bowel-health protocols and patient adherence tools are likely to benefit most as this application mix continues to evolve.

By Preparation: Social Media Reshaping Preparation-Type Demand

Sodium Phosphate Enemas held 36.52% of the United States enema based products market share within preparation type in 2025, while Coffee Enemas are forecast to grow at a 8.55% CAGR through 2031. Sodium phosphate remains the largest preparation class because it has long-standing use in bowel cleansing and strong familiarity across both consumer and institutional channels. Its position is still substantial in the United States enema based products market, but label restrictions and renal safety concerns are moderating how broadly it is recommended in vulnerable populations. Coffee enemas, by contrast, are expanding faster through consumer-led interest rather than clinical endorsement. This makes preparation type one of the clearest examples of how medical practice and wellness-led demand can move in different directions inside the same market.

The National Cancer Institute states that there is no scientific evidence supporting coffee enemas for disease treatment, yet consumer attention around these products continues to support faster category growth. Published case reports also continue to highlight safety concerns associated with self-administered coffee enemas PMC. Barium enemas and water-soluble contrast enemas remain tied to diagnostic radiology use and therefore follow procedure-linked demand rather than consumer preference swings. In the United States enema based products market, this creates two parallel go-to-market models, one built on physician trust and procurement consistency, and another built on digital consumer discovery. Suppliers that operate across both ends of this range need distinct risk management, communication, and product positioning strategies.

By End User: Hospitals Anchor Revenue While Home Care Accelerates

Hospitals held 42.22% share of the United States enema based products market size by end user in 2025, while Home Healthcare is projected to expand at a 8.25% CAGR through 2031. Hospitals remain the largest end-user group because they concentrate colonoscopy preparation, acute bowel management, surgical recovery, and the treatment of higher-acuity patients under supervised conditions. That established institutional role gives the United States enema based products market a dependable procurement base that is less volatile than purely retail demand. At the same time, Home Healthcare is growing faster because aging patients increasingly manage chronic bowel conditions outside hospitals once the immediate acute episode has passed. This end-user shift is changing not only where products are used, but also how they are packaged, explained, and supported.

MedPAC's March 2025 report showed a 19% FFS Medicare margin for freestanding home health agencies, which supports continued referral activity into home-based care models. Clinics remain a complementary sub-segment in the United States enema based products market, especially in gastroenterology and colorectal surgery settings where bowel preparation and follow-up management often happen in outpatient care. Nursing homes are particularly important because published research found that up to 80% of long-stay residents are affected by chronic constipation, creating concentrated and repetitive need. Other end users, including emergency departments and palliative care providers, add incremental volume where acute impaction or comfort-oriented bowel care is needed. The faster growth of home care also makes ergonomic design, pre-filled single-dose formats, and clearer directions more commercially important because self-administered use carries a higher risk of technique-related complications.

By Product Format: Disposability Dominates, Reusability Emerging

Disposable Enema Kits held 45.52% of the market in 2025, while Reusable Enema Kits are forecast to expand at a 8.05% CAGR through 2031. Disposable kits remain the largest format because they match infection-control priorities in supervised settings and they are convenient for consumers who want a ready-to-use product with minimal setup. In the United States enema based products market, this has helped disposable formats maintain broad relevance across both hospital procurement and OTC retail channels. Pre-Filled Enema Bottles also support this pattern because they simplify dosing and reduce preparation steps for home users. Enema Bags continue to occupy a smaller but stable niche where high-volume cleansing or specialized routines remain relevant.

Reusable kits are growing faster because some chronic-care consumers evaluate bowel management as a repeated need rather than a one-time purchase decision. That behavior is especially visible in the Home Healthcare portion of the United States enema based products market, where per-use economics and longer-term familiarity can justify investment in durable hardware. Reusable formats also create a different revenue model because refill solutions and accessory purchases can extend customer value beyond the first sale. This makes the reusable segment more suitable for direct-to-consumer, telehealth-adjacent, and subscription-style selling models than many disposable products. Companies that balance disposable and reusable portfolios are better positioned to serve both institutional volume and chronic home-care retention.

Geography Analysis

The United States enema based products market shows clear regional variation because demand is shaped by age structure, chronic disease burden, care access, and consumer behavior. The South and Southeast carry a heavier constipation burden because these regions combine higher shares of older residents with above-average rates of obesity and type 2 diabetes. Research published in BMC Public Health found a significant association between elevated BMI and constipation risk, which supports this regional pattern. Rural areas within these regions also rely more heavily on self-administered bowel management because specialist gastroenterology access is less dense. States such as Florida, Maine, Pennsylvania, and West Virginia stand out for older age profiles, which supports larger pools of elderly-care demand in the United States enema based products market[3]U.S. Census Bureau, “U.S. Population Aging as Nation Turns 250,” U.S. Census Bureau, census.gov.

The Northeast and Midwest remain important institutional centers for the United States enema based products market because they have dense networks of academic medical centers, procedural care settings, and established hospital procurement systems. In these regions, disposable kits, saline solutions, and retention formulations are more central to purchasing decisions because supervised use is more common. The 2025 bowel preparation consensus supports greater standardization in colonoscopy-related practice, which helps sustain consistent institutional demand across major metro markets. Digital comparison shopping also matters in these regions because consumers often move between physical retail and online purchasing when evaluating OTC bowel care products.

The West Coast has a stronger concentration of consumers interested in integrative medicine, preventive health, and microbiome-related care, which aligns with the faster growth of Intestinal Health Management in the United States enema based products market. This same regional profile helps explain why alternative preparations receive more attention there than in many other parts of the country. Price sensitivity still varies by state because OTC reimbursement remains limited, which can shift demand toward lower-cost or private-label options. Across all regions, online purchasing extends access into underserved communities and reduces the social visibility barrier that can otherwise delay product adoption.

Competitive Landscape

The United States enema based products market remains fragmented and is split between consumer OTC leaders and institutional bowel-care suppliers. Established OTC brands benefit from retail familiarity, repeat consumer recognition, and simple use formats that fit common constipation relief needs. Fleet Laboratories and its parent C.B. Fleet Company continue to hold a strong position in consumer saline enema formats through broad retail presence and long-standing brand recognition. Institutional competition is more distributed, with Coloplast, ConvaTec, and Hollister all pursuing bowel-management and adjacent care opportunities through product systems, clinical education, and procurement relationships. Medline Industries and Cardinal Health also matter in the United States enema based products market because hospital supply reach, contract depth, and distribution reliability shape share capture in supervised settings.

Competitive strategy is increasingly centered on chronic-condition platforms rather than single-product participation. Coloplast's Impact4 strategy, presented in September 2025, identified bowel care as one of the company's core growth areas, which signals continued investment in product development and market access. ConvaTec's AGM trading update in April 2026 highlighted the planned H2 2026 launch of Flexi-Seal Air, showing continued focus on bowel management innovation in institutional care. Cardinal Health added a channel-focused move in January 2026 through ContinuCare Pathway, which is designed to support patient transitions across care settings and can strengthen consumable product distribution. These actions show that competition in the United States enema based products market is increasingly shaped by care continuity, service support, and problem-specific platform depth.

A notable white space remains in reusable home-use kits, where no supplier appears to have built the same degree of category leadership that major OTC names hold in disposable formats. That leaves room for incumbents and specialty entrants that can combine ergonomic hardware, refill models, and discreet direct-to-consumer positioning. Hollister's April 2026 contract awards with Premier also reflect the ongoing value of institutional agreements for maintaining access and credibility in adjacent bowel-care channels. In the United States enema based products market, the companies that connect product reliability with channel fit are better placed to defend share than those relying on brand presence alone.

United States Enema Based Products Industry Leaders

Baxter International Inc.

B. Braun Melsungen AG

Coloplast Group

Hollister Incorporated

Medline Industries, LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cardinal Health introduced ContinuCare Pathway, a pharmacy-to-supplier referral program designed to enhance continuity of care for patients transitioning between care settings, supporting distribution of medical consumables, including bowel care products, through retail pharmacy channels.

- July 2025: Clinigen partnered with MaaT Pharma through an exclusive long-term licensing and distribution agreement, as well as a commercial supply agreement. MaaT Pharma, a biotechnology company in its late clinical stages, is working to make its microbiota-based therapy, MaaT013, available to patients in Europe and the UK.

United States Enema Based Products Market Report Scope

As per the scope of the report, enema-based products are medical or personal care items designed to introduce liquids into the rectum and lower bowel through the anus. These products are commonly used to relieve constipation, cleanse the bowel before medical examinations (such as a colonoscopy), or administer medications.

The segmentation for the United States enema-based products market is categorized by administration type, application, preparation, end user, and product format. By administration type, the market includes cleansing enema, carminative enema, retention enema, and return-flow enema. By application, it covers constipation relief, bowel preparation for procedures, intestinal health management, and other applications. By preparation, the segmentation includes sodium phosphate enemas, coffee enemas, barium enemas, and water-soluble contrast enemas. By end user, the market is divided into hospitals, clinics, home healthcare, and other end users. By product format, it comprises disposable enema kits, reusable enema kits, pre-filled enema bottles, and enema bags. For each segment, the market size and forecast are provided in terms of value (USD).

| Cleansing Enema |

| Carminative Enema |

| Retention Enema |

| Return-Flow Enema |

| Constipation Relief |

| Bowel Preparation for Procedures |

| Intestinal Health Management |

| Other Applications |

| Sodium Phosphate Enemas |

| Coffee Enemas |

| Barium Enemas |

| Water-Soluble Contrast Enemas |

| Hospitals |

| Clinics |

| Home Healthcare |

| Other End Users |

| Disposable Enema Kits |

| Reusable Enema Kits |

| Pre-Filled Enema Bottles |

| Enema Bags |

| By Administration Type | Cleansing Enema |

| Carminative Enema | |

| Retention Enema | |

| Return-Flow Enema | |

| By Application | Constipation Relief |

| Bowel Preparation for Procedures | |

| Intestinal Health Management | |

| Other Applications | |

| By Preparation | Sodium Phosphate Enemas |

| Coffee Enemas | |

| Barium Enemas | |

| Water-Soluble Contrast Enemas | |

| By End User | Hospitals |

| Clinics | |

| Home Healthcare | |

| Other End Users | |

| By Product Format | Disposable Enema Kits |

| Reusable Enema Kits | |

| Pre-Filled Enema Bottles | |

| Enema Bags |

Key Questions Answered in the Report

What is the 2026 value of the United States enema based products market?

The United States enema based products market stands at USD 579.66 million in 2026 and is forecast to reach USD 807.32 million by 2031 at a 6.85% CAGR.

Which application contributes the most revenue in 2025?

Constipation Relief held 42.24% in 2025, making it the largest application base for current revenue generation.

Which segment is growing the fastest through 2031?

Home Healthcare is the fastest-growing end-user segment at 8.25% CAGR, while Coffee Enemas lead preparation growth at 8.55% CAGR through 2031.

Why are home-use products gaining traction in the United States?

Aging demographics, financially viable home health delivery, and preference for managing chronic bowel conditions outside hospitals are supporting stronger home-use demand.

Why do disposable formats still lead even though reusable kits are growing faster?

Disposable Enema Kits held 45.52% in 2025 because they fit infection-control and convenience needs, while Reusable Enema Kits are rising on lower long-term cost and chronic-care use.

What are the main risks affecting future growth?

Social stigma, improper self-administration, and safety concerns around sodium phosphate and coffee enemas remain the main constraints on broader adoption.

Page last updated on: