Disposable Incontinence Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

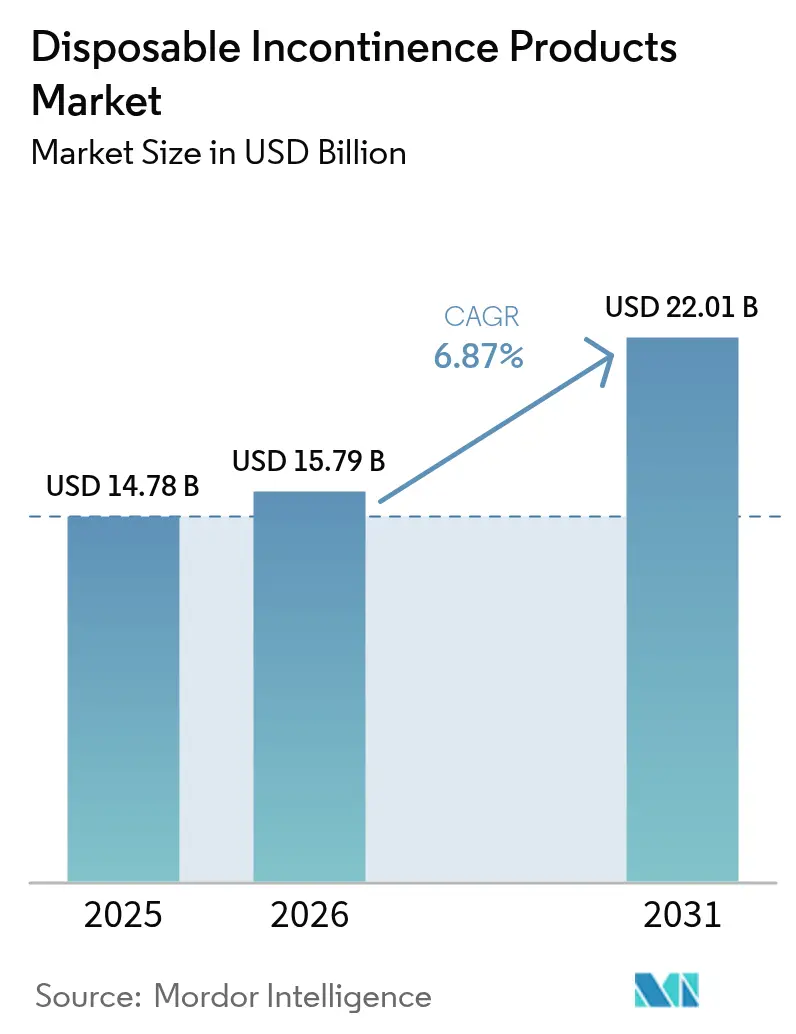

| Market Size (2026) | USD 15.79 Billion |

| Market Size (2031) | USD 22.01 Billion |

| Growth Rate (2026 - 2031) | 6.87% CAGR |

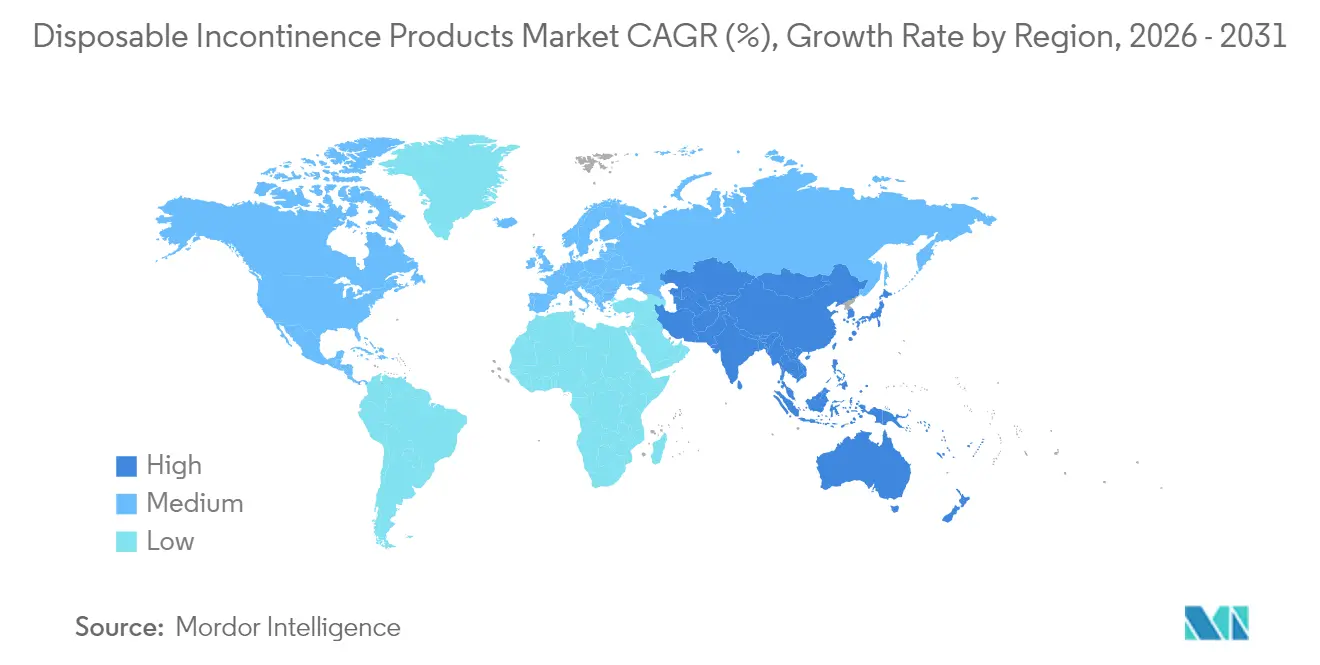

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Incontinence Products Market Analysis by Mordor Intelligence

The disposable incontinence products market size is expected to grow from USD 14.78 billion in 2025 to USD 15.79 billion in 2026 and is forecast to reach USD 22.01 billion by 2031 at 6.87% CAGR over 2026-2031. At its current growth rate, the disposable incontinence products market is benefitting from longer life expectancy, wider chronic kidney disease (CKD) screening, and upgrades to reimbursement codes that expand coverage for hydrophilic catheters and other advanced devices. Protective garments remain the mainstay purchase in long-term care facilities, yet smart catheter designs and biodegradable nonwovens are widening clinician choice. Intensifying plastic-waste regulations in Europe are accelerating the shift toward recyclable packaging, while direct-to-consumer (D2C) platforms improve product access and brand loyalty in home-care settings. The disposable incontinence products market is also finding steady demand from hospital systems that integrate incontinence management into CKD and benign prostatic hyperplasia (BPH) care pathways.

Key Report Takeaways

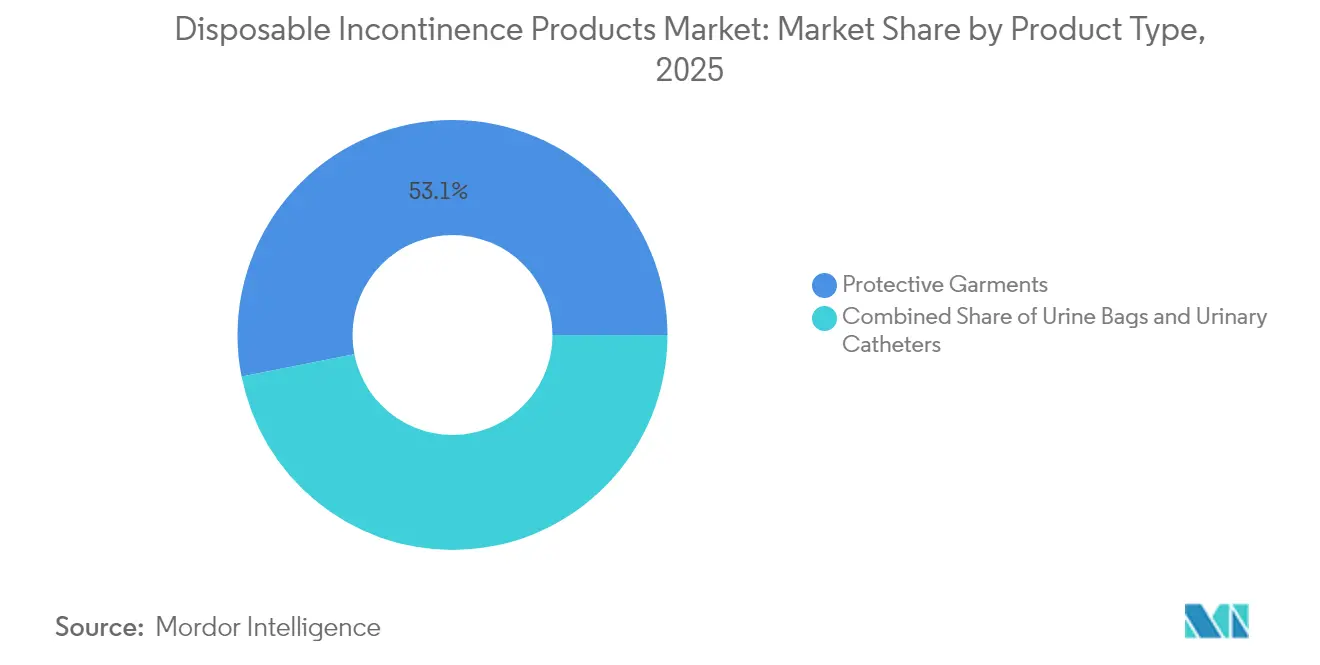

- By product type, protective garments led with 53.10% revenue share in 2025, whereas urinary catheters are set to expand at a 8.98% CAGR through 2031.

- By application, chronic kidney failure accounted for 30.25% of the disposable incontinence products market size in 2025, while BPH management is advancing at an 7.92% CAGR to 2031.

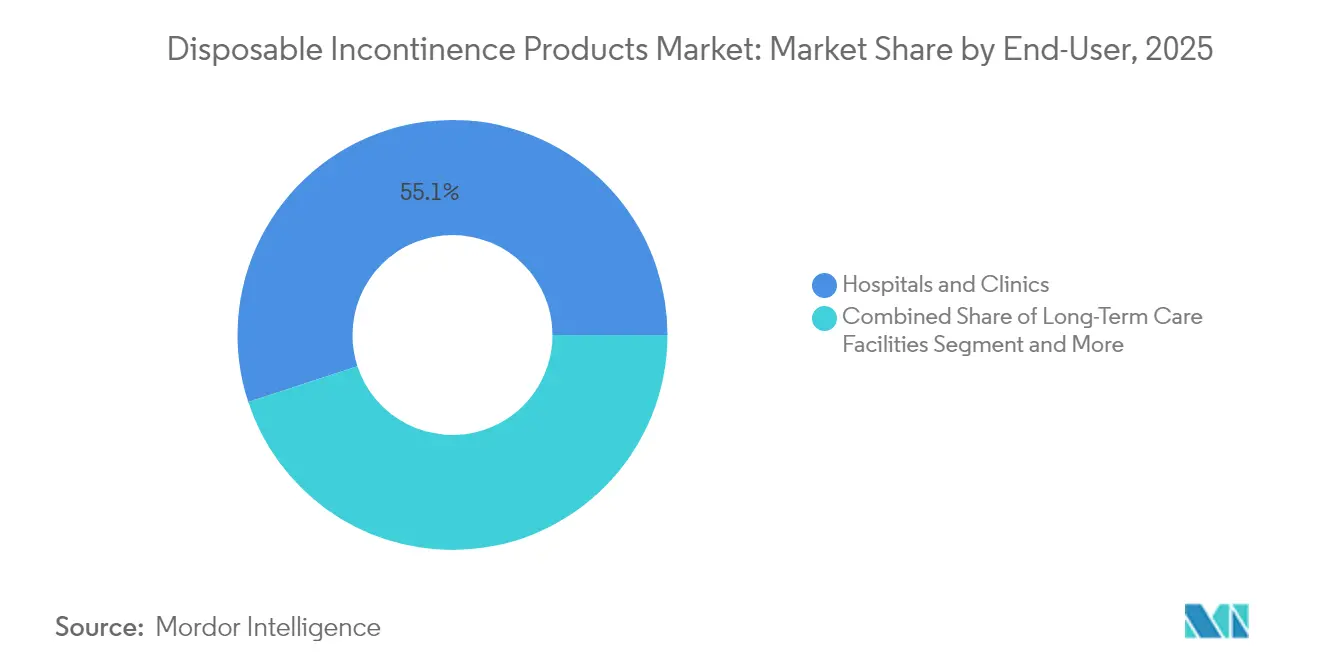

- By end-user, hospitals and clinics held 55.05% of the disposable incontinence products market share in 2025; home-care settings record the highest projected CAGR at 9.21% over the same period.

- By geography, North America held 43.05% of 2025 revenue, while Asia-Pacific is advancing at a 9.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Disposable Incontinence Products Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Renal & Urological Disorders | 1.8% | Global, with higher concentration in North America & Europe | Long term (≥ 4 years) |

| Aging Population & Higher Life Expectancy | 2.1% | Global, particularly Asia-Pacific & Europe | Long term (≥ 4 years) |

| Advances In Super-Absorbent & Breathable Nonwovens | 1.2% | Global, led by developed markets | Medium term (2-4 years) |

| E-Commerce & D2C Brands Expanding Access | 0.9% | Global, with early adoption in North America & Europe | Short term (≤ 2 years) |

| 2026 HCPCS Codes For Hydrophilic Catheters (Reimbursement Boost) | 0.6% | North America | Short term (≤ 2 years) |

| Adoption Of AI-Enabled "Smart Diapers" In Long-Term Care | 0.4% | Developed markets, early pilots in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Renal & Urological Disorders

CKD afflicts 35.5 million Americans, and prevalence rises to 50.94% among people aged 90 and older in Saudi Arabia[1]Centers for Disease Control and Prevention, “Chronic Kidney Disease in the United States, 2023,” cdc.gov. CKD’s direct link with diabetes and hypertension magnifies long-term demand for high-capacity absorbent products and catheter kits with infection-prevention coatings. Institutional purchasers now embed incontinence supplies into CKD care bundles, guaranteeing baseline order volumes that stabilize the disposable incontinence products market. Predictable chronic-care volumes allow suppliers to optimize production lines and negotiate multiyear contracts. The driver remains strongest in higher-income regions where CKD diagnostic coverage is highest, yet emerging markets are closing the gap as national health surveys expand.

Aging Population & Higher Life Expectancy

Asia-Pacific’s older-adult cohort will nearly double to 1.2 billion by 2050, raising the region’s incontinence case load sharply[2]Asian Development Bank, “Developing Asia and the Pacific Unprepared for Challenges of Aging Population,” adb.org. Many seniors lack consistent health-plan coverage, so governments are directing larger budget shares to elder-care subsidies. The demographic shift pushes demand for both premium breathable diapers in urban nursing homes and affordable pull-ups in rural clinics. Manufacturers rely on forward demand visibility to plan capacity investments across China, India, and Indonesia. As family-based care models evolve into paid in-home services, subscription programs for bulk deliveries of protective garments are gaining traction, further widening the disposable incontinence products market.

Advances in Super-Absorbent & Breathable Nonwovens

Material scientists have created hemp-based biodegradable super-absorbents that retain liquid more effectively than petroleum-derived powders[3]Purdue University, “Purdue Researchers Develop Sustainable, Biodegradable Superabsorbent Materials From Hemp,” purdue.edu. Core–shell composites now allow slow release of antibacterial agents, cutting dermatitis incidents in long-term wear. These innovations let brands command premium pricing while aiding compliance with European packaging waste directives. Improved fluid-locking structures also reduce product weight, lowering shipping costs and carbon footprints. As patents expire on first-generation SAPs, smaller firms can license novel chemistries and enter the disposable incontinence products market with differentiated value propositions.

E-Commerce & D2C Brands Expanding Access

Online channels remove the stigma often felt during in-store purchases and offer discreet home delivery. D2C subscription models gather usage data, enabling auto-replenishment algorithms that minimize stock-outs. Digital marketing lowers entry barriers for niche brands that focus on gender-specific fits or eco-friendly fabrics. In North America, oncology clinics are already providing affiliate links to approved catheter vendors, streamlining patient onboarding. First-time buyers frequently start online research on symptom forums, so SEO-optimized product pages play an outsized role in directing traffic toward the disposable incontinence products market.

Restraints Impact Analysis of Disposable Incontinence Products Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dermatitis & Infection Risks From Prolonged Product Use | -0.8% | Global, with higher impact in humid climates | Medium term (2-4 years) |

| Patchy Reimbursement In Emerging Economies | -1.1% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Sustainability Regulations On Single-Use Plastics & Landfill Waste | -0.7% | Europe, California, expanding globally | Medium term (2-4 years) |

| Shift Toward Reusable Pelvic-Floor Wearables & Stimulation Devices | -0.4% | Developed markets, urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dermatitis & Infection Risks From Prolonged Product Use

The U.S. FDA continues to record adverse-event filings that associate external catheters with skin irritation and urinary-tract infections. Infection fears lower compliance among cost-conscious patients who attempt to reuse single-use items. Facilities counter by specifying breathable backing films and silver-ion coatings in tender documents, which raises product costs. Skin-friendly innovations partially offset the restraint but add complexity to regulatory submissions. The issue is more acute in tropical regions where humidity accelerates bacterial growth, pressing manufacturers to tailor product guidelines and training materials accordingly.

Patchy Reimbursement in Emerging Economies

Although Indonesia earmarked IDR 218.5 trillion in 2025 to expand universal health insurance, device reimbursement remains uneven outside urban centers. Middle-income patients often pay out of pocket, favoring budget diapers and postponing catheter transition. Multinational firms segment their portfolios into premium and value lines, yet logistical costs erode margins on low-priced SKUs. Gradual policy harmonization through regional trade blocs could ease import fees, but timelines are uncertain, tempering growth in the disposable incontinence products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Disposable Incontinence Products Market Segment Analysis

By Product Type:

Catheters Drive Innovation Despite Garment DominanceProtective garments generated 53.10% of the disposable incontinence products market share in 2025, reflecting widespread adoption in hospitals, nursing homes, and at-home care routines. Demand is insulated from short-term economic swings because garments offer a familiar, low-training solution across mild-to-severe incontinence profiles. Innovations such as four-layer breathable panels and odor-lock gels extend wear time, thereby lowering daily change frequency for budget-tight facilities. Urinary catheters, while holding a smaller base, are advancing at a 8.98% CAGR as hydrophilic coatings reduce urethral trauma and new HCPCS reimbursement codes increase affordability. External catheter designs optimized for female anatomy are also winning regulatory clearance, opening untapped outpatient segments.

The disposable incontinence products market size for catheter solutions is forecast to rise steadily, supported by smart catheters that transmit real-time flow data to clinician dashboards. Disposable under-pads attract institutional buyers aiming to protect mattresses and wheelchairs against incidental leaks, while pull-up pants resonate with ambulatory adults seeking garment-like aesthetics. Leg urine bags gain share in home infusion programs where mobility is critical. Material upgrades in biodegradable polymers lower disposal costs, appealing to countries with landfill-tax regimes. The product-type landscape remains dynamic as cross-category hybrids—such as integrated diaper-catheter kits—enter clinical trials, promising further differentiation.

By Application:

BPH Growth Outpaces CKD DominanceChronic kidney failure retained 30.25% of the disposable incontinence products market size in 2025 because dialysis patients often require extended overnight protection. Hospitals bundle premium diapers into kidney-care reimbursement packages to prevent pressure ulcers and infections, ensuring stable-volume contracts through group-purchasing organizations. Yet BPH treatment is posting the fastest 7.92% CAGR. Earlier diagnostics and minimally invasive therapies allow men to resume daily routines more quickly, driving demand for discreet, high-absorbency pull-ups that can be worn under regular clothing. Clinical studies that correlate metabolic syndrome with BPH progression underscore the need for integrated urology-endocrinology care, expanding the disposable incontinence products market.

Bladder-cancer patients undergoing transurethral resections create episodic spikes in catheter use during recovery phases. Kidney-stone treatment protocols employ temporary leg bags to manage post-operative drainage, providing another periodic demand stream. Neurological disorders, from multiple sclerosis to spinal-cord injuries, require customized solutions that balance skin health and mobility, pushing R&D toward adaptive fasteners and pressure sensors. Future pipeline devices aim to pair pelvic-floor stimulation wearables with absorbent inserts, hinting at crossover categories that blur traditional application lines within the disposable incontinence products industry.

By End-User:

Home-Care Acceleration Reshapes DistributionHospitals and clinics accounted for 55.05% of revenue in 2025 because institutional protocols mandate 24-hour protection for bed-bound patients and surgical wards. Centralized procurement grants volume leverage that squeezes supplier margins but assures forecast clarity. Long-term care facilities uphold consistent reorder cycles tied to resident census and acuity levels. Home-care, however, is expanding at a 9.21% CAGR as Medicare’s Advanced Primary Care Management program reimburses remote monitoring of chronic conditions. Subscription boxes ship multi-week diaper supplies directly to doorsteps, reducing caregiver trips to pharmacies and tapping new revenue pools for the disposable incontinence products market.

Smart diaper sensors, validated in clinical trials for dermatitis prevention, resonate with tech-savvy caregivers who appreciate smartphone alerts that guide change intervals. Home-infusion patients use leg bags that attach seamlessly to mobility aids, favoring brands that provide free telehealth setup advice. Growth in this channel encourages manufacturers to partner with logistics firms to optimize last-mile cold-chain segments for hydrogel-based catheters sensitive to temperature swings. As payers broaden lists of covered home-medical items, the disposable incontinence products market will continue shifting toward decentralized care ecosystems.

Geography Analysis

North America Disposable Incontinence Products Market

North America led the disposable incontinence products market with a 43.05% revenue share in 2025, anchored by Medicare coding stability and mature long-term-care networks. Updated HCPCS codes effective January 2025 classify hydrophilic catheters in higher-reimbursement shells, prompting hospitals to upsell advanced variants. U.S. policy also widened coverage to lymphedema compression treatment items, signaling an overall device-friendly stance. Canada’s public health-insurance redesign expands home-support allowances, giving home-care suppliers greater wallet share. Mexico’s Seguro Popular replacement, INSABI, is channelling new funds to state clinics, creating a multi-tiered tender landscape. Sustainability mandates such as California’s SB 54, which enforces a 25% single-use plastic reduction by 2032, push brands to launch recyclable diaper wrappers that feed circular-economy pilots.

APAC and LATAM Disposable Incontinence Products Market

Asia-Pacific registered a 9.95% CAGR, the fastest globally, powered by population aging and higher CKD screening in China, Japan, and South Korea. China’s device makers are leveraging cost advantages to court Latin American buyers, exporting both pull-ups and catheter kits under CE-mark equivalency. Indonesia’s domestic factories benefit from government grants tied to local-content rules, supplying lower-priced diapers to public hospitals while premium imports capture the private-hospital tier. India’s e-pharmacies have started stocking discrete male guards and female pads, accelerating D2C penetration and adding volume to the disposable incontinence products market. Australia’s National Disability Insurance Scheme further boosts uptake of reusable pelvic-floor trainers that complement single-use absorbents.

Europe Disposable Incontinence Products Market

Europe remains a mature yet evolving arena where the EU Packaging and Packaging Waste Regulation mandates fully recyclable packaging by 2030 and a 5% plastic-waste reduction by the same year. Manufacturers must balance sustainability upgrades with strict Medical Device Regulation (MDR) documentation that now covers reprocessed single-use devices. Germany leads volume consumption, yet France’s eco-tax credits tilt purchasing toward compostable liners. The United Kingdom’s NHS Supply Chain is piloting outcome-based contracts that tie reimbursements to dermatitis reduction metrics, potentially reshaping supplier scorecards. Nordic countries, already leaders in recyclable diaper adoption, offer case studies that other EU states may emulate, further influencing the disposable incontinence products market trajectory.

Regulatory Landscape

Disposable incontinence products sit across medical-device and general-hygiene frameworks, so how products are positioned for intended use remains the key compliance lever. In the United States, protective incontinence garments are regulated by the FDA as Class I medical devices under 21 CFR 876.5920, with broad exemptions from 510(k) premarket notification, while manufacturers still need to follow baseline controls such as labeling, record-keeping, and complaint handling. For devices indicated for urinary incontinence treatment, FDA expectations for clinical investigations are laid out in agency guidance, which shapes study design and the evidence package required for catheter and device innovators.

In Europe, products marketed for medical incontinence purposes fall under the EU Medical Device Regulation (MDR) 2017/745 and commonly come under Class I (non-sterile, non-measuring) categories. That status requires CE marking and detailed technical documentation, along with stronger post-market surveillance and traceability. MDR-related transparency and reporting obligations are expected to tighten through 2026 as EUDAMED modules move toward mandatory use, increasing operational load for manufacturers and importers. Across regions, ISO 11948-1 and ISO 15621 provide recognized test-method anchors for performance evaluation of absorbent products, supporting more consistent substantiation in tenders and registrations.

Competitive Landscape

The disposable incontinence products market shows moderate consolidation: the top five manufacturers control a significant but not overwhelming portion of global revenue, leaving space for regional challengers. Kimberly-Clark’s adult-care division increased manufacturing capacity by more than 25% and targeted USD 3 billion in productivity savings, while investing in breathable nonwovens that align with its ESG roadmap. The 70% stake acquisition in Thinx enables entry into reusable underwear that counters single-use-plastic scrutiny and expands hybrid product offerings. Procter & Gamble supports its Always Discreet line with R&D spend that focuses on odor-locking channels and slimmer cores, leveraging USD 84 billion in 2024 net sales to cross-fund adult-care launches from baby-care learnings.

Essity (TENA), has translated Scandinavian sustainability standards into global roll-outs of plant-based topsheets and paper-based packaging. The company collaborates with recycling partners to close material loops, meeting EU waste benchmarks ahead of schedule. First Quality Enterprises expanded downstream by purchasing Henkel’s Retailer Brands and investing USD 400 million in Georgia and Pennsylvania diaper lines, a move that tightens quality control and reduces third-party dependency. Mid-tier entrants focus on AI-enabled sensors: start-ups license Bluetooth-connected moisture chips to traditional manufacturers that lack in-house electronics know-how, fostering mutually beneficial partnerships within the disposable incontinence products industry.

Regulatory compliance is becoming a strategic differentiator. MDR rules require notification of any supply interruption, forcing multinationals to secure dual-sourcing agreements for SAP resins. In the United States, the FDA Fast Track review for antimicrobial catheters shortens time-to-market for companies that can substantiate reduced infection rates. Venture funding gravitates toward firms with circular-economy narratives, especially in Europe where landfill levies tighten. Collectively, these dynamics spur a mix of defense-oriented acquisitions and offensive innovation pipelines, keeping competitive intensity at a steady yet manageable level across the disposable incontinence products market.

Disposable Incontinence Products Industry Leaders

Essity

Kimberly-Clark

Procter & Gamble

Unicharm

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Disposable Incontinence Products Market Companies Covered in this Report

- Becton, Dickinson & Co. (C.R. Bard)

- Cardinal Health

- Coloplast

- Kimberly-Clark Worldwide

- Abena

- Hollister

- Convatec

- First Quality Enterprises

- HARTMANN Group

- Medline Industries

- Essity

- Procter & Gamble

- Unicharm Corp.

- Teleflex

- B. Braun

- Boston Scientific

- Ontex Group

- TZMO SA

- Principle Business Enterprises

Market Opportunities and Future Outlook

Capacity additions and portfolio pivots are opening room for private label offerings, size-inclusive ranges, and faster-to-iterate SKUs, particularly as institutional buyers and D2C channels diversify sourcing. In North America, investment cycles and contract manufacturing arrangements create near-term paths to add volume. Kimberly-Clark announced a multi-year, USD 2 billion investment plan in its North America business, including a new advanced manufacturing facility in Warren, Ohio, and expansion at Beech Island, South Carolina, with construction starting in May 2025, while Principle Business Enterprises initiated an effort to double capacity for plus-size absorbent products at its Dunbridge, Ohio facility (announced May 2024). On the supply side for retailers and brands, Griffin Care completed an acquisition and expanded production capacity at its Bridgeton, New Jersey facility in April 2026 to support private label and contract manufacturing, indicating more availability of outsourced manufacturing for regional brands and healthcare distributors.

Regulatory and sustainability constraints are also redirecting product and packaging innovation budgets into compliance outcomes that can be tied to procurement decisions. EU MDR 2017/745 device requirements, along with the 2026 EUDAMED operational ramp-up, increase the value of turnkey regulatory documentation, post-market surveillance tooling, and standardized performance testing (for example, ISO-based containment metrics) that can be attached to hospital and long-term care tenders. At the same time, Europe-wide packaging recyclability targets for 2030 and tightening plastic-waste rules in markets such as California are pushing demand for recyclable packaging formats and lower-plastic constructions, reinforcing budgets for biodegradable nonwovens, plant-based topsheets, and redesigned wrappers that maintain performance while reducing waste-handling friction for facilities and home-care users.

Recent Industry Developments in Disposable Incontinence Products Market

- July 2026: Kimberly-Clark completed the divestment of its international tissue and professional business into the Suzano joint venture, Arbex, effective July 1, 2026. The transaction simplifies Kimberly-Clark's portfolio and frees management attention and resources for core personal-care categories, including adult incontinence and related hygiene platforms.

- February 2026: Essity completed its acquisition of Edgewell Personal Care's feminine care business for USD 340 million, including a manufacturing footprint in Dover, Delaware. The deal strengthens Essity's U.S. hygiene and personal-care platform and adds scale and operational assets that can support adjacent category execution across absorbent product segments.

- February 2026: Ontex launched its Sensitive range of adult incontinence products in Europe, featuring a skin-health positioning that includes Y-core technology and a botanical-enriched topsheet. The launch targets differentiation in premium tiers where facilities and consumers are actively managing dermatitis risk and are seeking performance-linked product upgrades.

Disposable Incontinence Products Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers single use products used to manage urinary or fecal leakage, mainly disposable briefs, pull ups, pads, liners, and underpads, along with related urine bags and urinary catheters sold through retail and institutional channels across major regions.

Scope exclusions: Reusable cloth incontinence products and drug or surgical treatment revenues are not counted in this sizing.

Segments Covered in This Report

- By Product Type

- Protective Garments

- Disposable Adult Diapers

- Disposable Under-pads

- Disposable Pull-up Pants

- Other Garments

- Urine Bags

- Leg Urine Bags

- Bedside Urine Bags

- Urinary Catheters

- Indwelling (Foley) Catheters

- Intermittent Catheters

- External Catheters

- Protective Garments

- By Application

- Chronic Kidney Failure

- Benign Prostatic Hyperplasia (BPH)

- Bladder Cancer

- Kidney Stone

- Other Applications

- By End-User

- Hospitals & Clinics

- Long-Term Care Facilities

- Homecare Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundary and to build the starting demand story before numbers are modeled. We reviewed public health statistics and demographic time series, such as CDC summaries, WHO aging publications tied to continence outcomes, and OECD health expenditure indicators, because these help map how the at risk population and care settings are shifting.

Trade and supply signals were also checked to keep the model realistic, such as UN Comtrade trade flows for relevant hygiene nonwoven categories, tariff notes from government portals, and peer reviewed papers on absorbent core materials and skin health outcomes. Company annual reports, investor presentations, and disclosures from major retailers and pharmacies were reviewed to understand product mix changes and pricing direction. When a single point was missing, paid subscriptions for company financials and patent databases were used selectively to verify filings, product launches, and ownership changes. The sources listed here are illustrative only, and other public references were used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary work focused on validating what drives volume and price by care setting, because that is where desk sources are often thin. We spoke with manufacturers, distributors, long term care procurement teams, and clinicians who influence product selection, and we balanced inputs across APAC, EMEA, and the Americas to avoid over reliance on one region's reimbursement and channel structure.

Respondents also clarified how urine bags and urinary catheters are treated in tenders versus retail product lists, since this affects both unit demand and revenue conversion into the market total.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 18% | APAC: 42% |

| Mid tier: 55% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 20% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top down build that reconstructs the demand pool by combining the addressable adult population, age mix, and the share of people in home care versus long term care, which is then translated into annual unit needs per user. To keep the total grounded, we corroborate it with selective bottom up checks, such as sampled average selling prices by product format, channel mix checks (institutional versus retail), and a supplier revenue roll up for a limited set of countries where disclosures are clearer.

A few practical inputs shape the model and are refreshed each cycle, including aging rate and dependency ratio trends, diagnosed incontinence prevalence ranges from public health studies, long term care bed capacity and occupancy signals, penetration of pull ups versus pads in retail baskets, and price progression tied to pulp and superabsorbent polymer cost direction. Where country level data is patchy, gap handling is done by mapping to a proxy market with similar income levels and care delivery patterns, and then adjusting for channel maturity and reimbursement intensity.

For forecasting, scenario analysis is used around two main uncertainties, which are reimbursement and institutional staffing constraints, and then results are smoothed using an exponential trend check so year to year shifts stay believable. The final forward view is discussed with primary respondents to confirm that the implied volume growth and pricing curve match what is being seen in contracts and shelf pricing.

Data Validation & Update Cycle

Validation is done in steps so errors do not pass through unnoticed. We compare outputs against independent signals like per capita hygiene spend, long term care expansion indicators, and import and export direction in key consuming countries, and then investigate any sharp variances before sign off.

An internal review pass is completed after model runs, followed by targeted re contacts when an assumption changes materially, such as a raw material shock, a reimbursement update, or a sudden channel shift toward e commerce. Reports are refreshed annually, and interim updates are made when major events change the demand outlook. Before delivery, the analyst runs a final check so the client receives the latest updated view.

Mordor Intelligence's Disposable Incontinence Products Market Estimate Compared With Other Published Estimates

Published market sizes for disposable incontinence products can look far apart even when the topic name is the same, because the counted products and the selling channels are not always aligned. Differences also come from how each publisher treats pricing, especially when retail promotions, institutional tenders, and currency timing are handled in different ways.

Key gaps usually show up in scope and in the demand yardsticks used to build volumes. Some estimates include only absorbent garments, while others also add urine bags and urinary catheters, and a few may mix disposable and reusable products under one label. Another driver is the base case used for penetration and reimbursement growth, since a more aggressive shift into long term care or e commerce can lift totals quickly if it is not cross checked against real world capacity and care setting constraints.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.78 B (2025) | |

| Industry Publisher A | USD 13.14 B (2026) | Uses a different base year and a slower growth path, and the disclosed framework emphasizes forecast smoothing that can understate near term pricing lifts from institutional contracts and product mix upgrades. |

| Research Publisher B | USD 15.50 B (2025) | Often expands segmentation depth but may apply broader inclusion rules across adjacent hygiene categories, and totals can shift depending on whether urine bags and catheters are treated as core scope or handled separately. |

The table shows that most of the spread is explained by what gets included and how price and channel weights are refreshed. By tracking channel mix and pricing movements each year, Mordor Intelligence keeps the total tied to actual consumption settings and avoids counting neighboring hygiene revenues that do not behave like incontinence demand.

Key Questions Answered in the Report

What is the current size of the disposable incontinence products market?

The disposable incontinence products market generated USD 15.79 billion in 2026 and is forecast to reach USD 22.01 billion by 2031, reflecting a 6.87% CAGR.

Which product segment is growing the fastest?

Urinary catheters constitute the fastest-growing product segment, expanding at a 8.98% CAGR through 2031 on the back of hydrophilic coatings and favorable reimbursement updates.

Why is Asia-Pacific the fastest-growing regional market?

Aging demographics and expanding health-insurance coverage are driving a 9.95% CAGR in Asia-Pacific, with the older-adult population projected to double by 2050.

How are sustainability regulations affecting manufacturers?

The EU Packaging and Packaging Waste Regulation mandates fully recyclable packaging by 2030, pushing manufacturers to invest in biodegradable absorbents and paper-based wraps.

What role do smart technologies play in product innovation?

AI-enabled diaper sensors and data-linked catheters help caregivers time changes accurately and reduce dermatitis, making connectivity a key differentiator in premium tiers of the disposable incontinence products industry.

Page last updated on: