Wound Cleanser Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

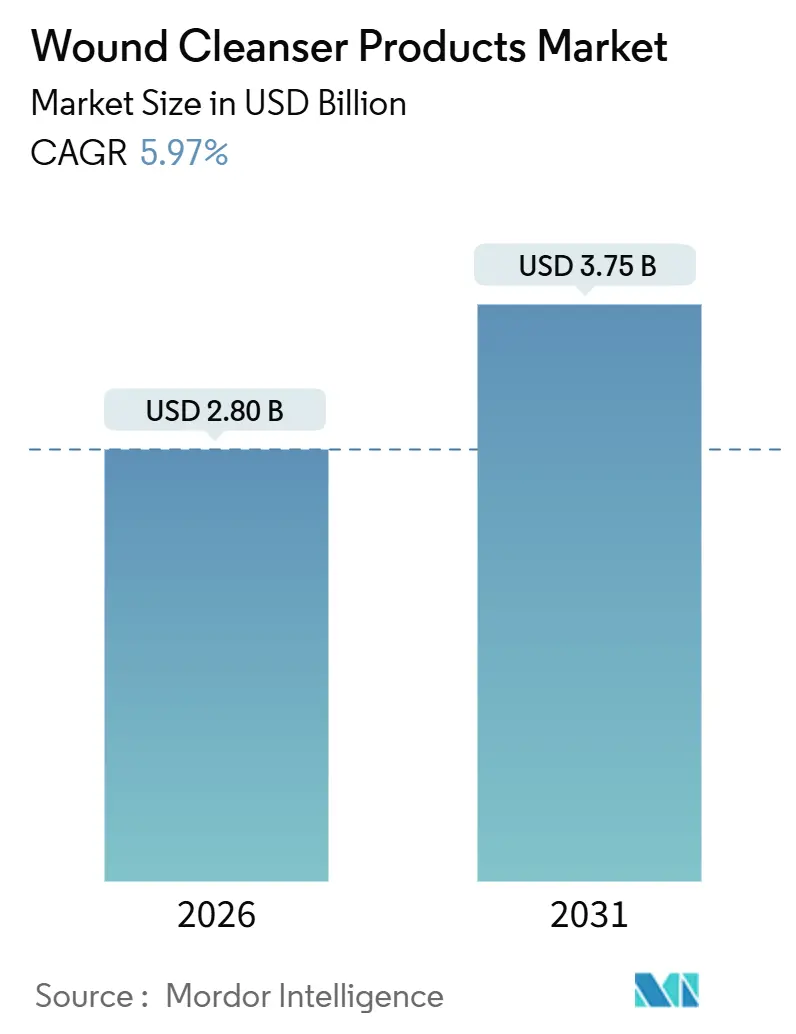

| Market Size (2026) | USD 2.80 Billion |

| Market Size (2031) | USD 3.75 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

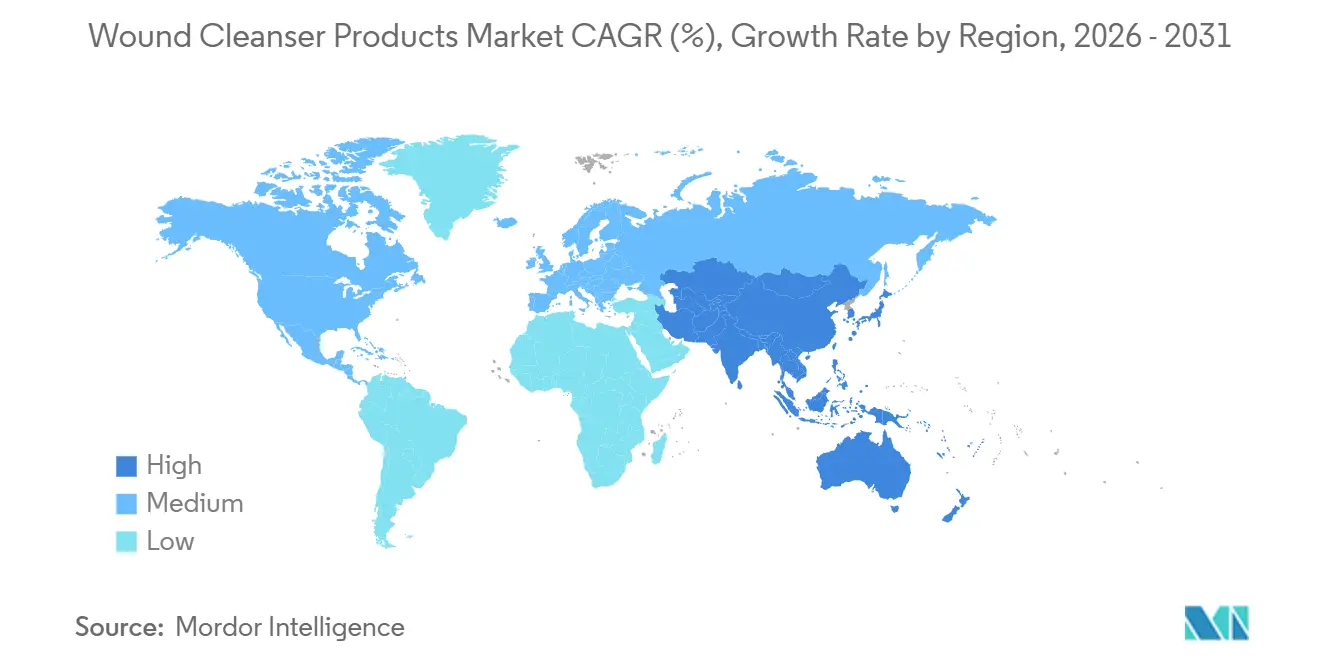

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wound Cleanser Products Market Analysis by Mordor Intelligence

The Wound Cleanser Products Market size is estimated at USD 2.80 billion in 2026, and is expected to reach USD 3.75 billion by 2031, at a CAGR of 5.97% during the forecast period (2026-2031).

The near-6% growth pace reflects a rapid pivot away from commodity saline irrigation and toward precision solutions that combine broad-spectrum antimicrobial action with high biocompatibility and tight regulatory alignment. Institutional support is a primary catalyst; the World Health Organization’s 2024 proposal to add hypochlorous acid (HOCl) to its Essential Medicines List established a global benchmark for non-cytotoxic cleansers. At the same time, the U.S. Food and Drug Administration’s (FDA) November 2023 proposal to reclassify wound washes that contain medically important antimicrobials into Class III devices signals intensifying oversight of preservative chemistry and resistance pathways. Clinical evidence from randomized controlled trials confirms faster epithelialization and lower infection rates for HOCl versus saline in diabetic foot ulcers, reinforcing hospital formulary shifts. Finally, telemedicine platforms that pair remote image capture with algorithm-driven cleanser protocols are reducing in-person nursing visits, widening end-user acceptance across home-care settings.

Key Report Takeaways

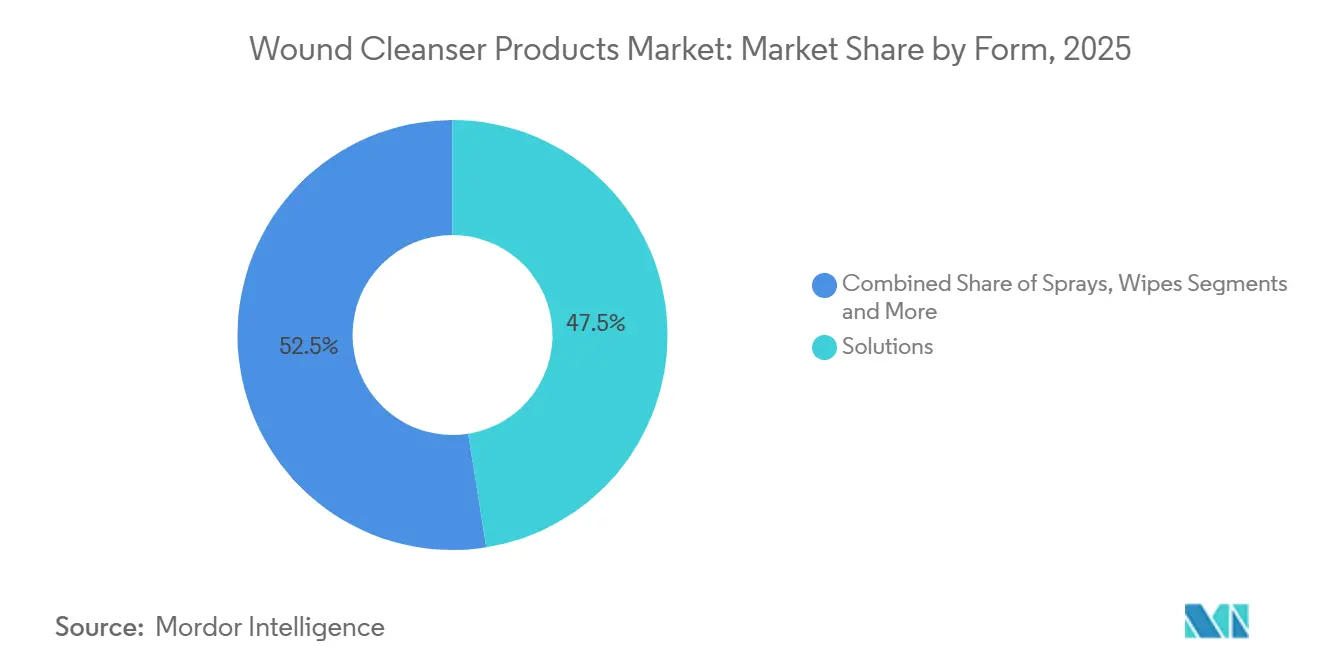

- By form, Solutions held 47.55% revenue share in 2025; Sprays are forecast to record a 6.25% CAGR between 2026 and 2031.

- By ingredient, Saline claimed 33.53% of the Wound Cleanser Products market share in 2025, while Hypochlorous Acid is set to expand at 6.85% through 2031.

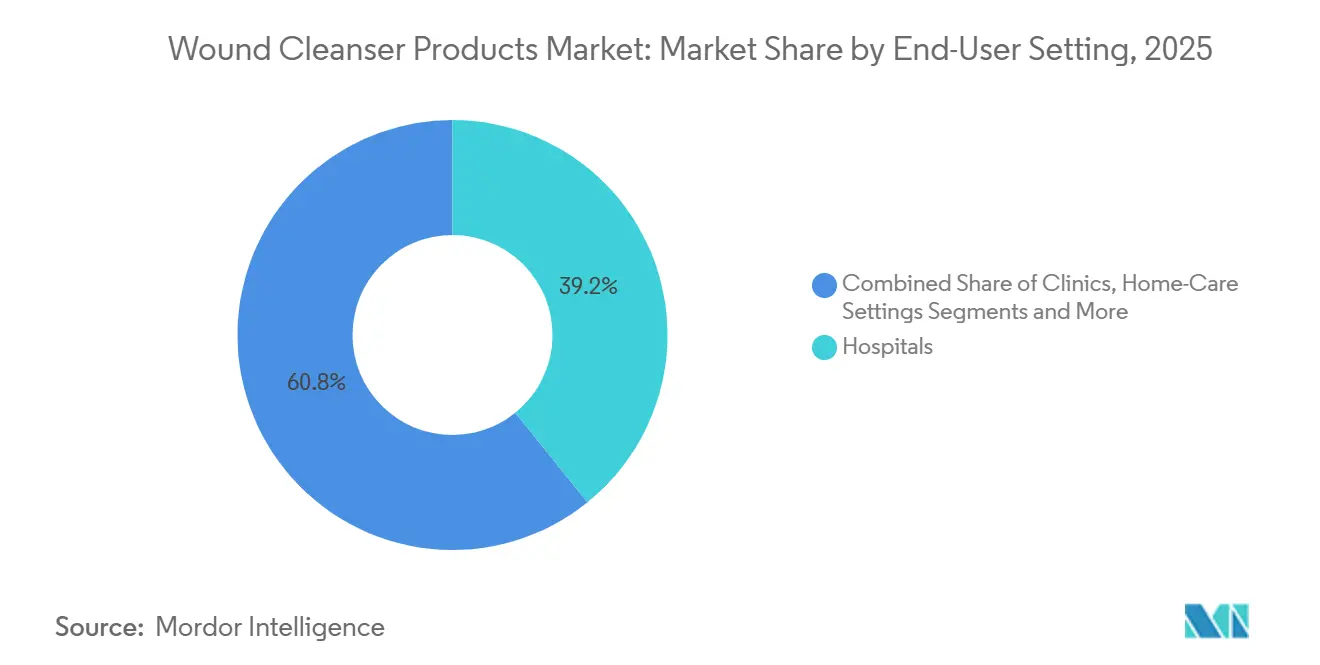

- By end-user, Hospitals generated 39.23% of 2025 demand; Home-Care Settings will grow at 7.15% CAGR to 2031.

- By geography, North America led with 38.25% revenue in 2025, whereas Asia-Pacific is projected to advance at 6.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wound Cleanser Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & diabetic wounds | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Growing surgical procedure volumes worldwide | +1.0% | Global, with fastest growth in Asia-Pacific (China, India, Southeast Asia) | Medium term (2-4 years) |

| Adoption of non-cytotoxic, pH-balanced cleansers | +0.9% | North America & Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Shift to single-dose sterile packaging | +0.8% | North America, Europe, and Japan | Short term (≤ 2 years) |

| Telemedicine-driven home-care demand surge | +0.7% | North America, Western Europe, and Australia | Short term (≤ 2 years) |

| Eco-friendly & biodegradable formulation mandates | +0.5% | Europe (EU MDR), California, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Diabetic Wounds

Chronic lesions now affect an estimated 2.5% of the U.S. population, and 34% of individuals with diabetes develop a foot ulcer during their lifetime[1]American Academy of Family Physicians, “Chronic Wound Care Guidelines and Recommendations,” aafp.org. This burden keeps the Wound Cleanser Products market in sustained demand, because clinicians require solutions that disrupt biofilms while preserving keratinocyte viability. FDA biocompatibility guidance released in 2023 forces manufacturers to prove that surfactant residues and preservatives do not impede re-epithelialization. As a result, formulators are replacing povidone-iodine and chlorhexidine with HOCl and polyhexanide-betaine blends that achieve a log-4 bacterial reduction and fibroblast viability above 90%. Hospitals that adopt these biocompatible solutions report shorter inpatient stays, a critical economic driver as diagnosis-related group reimbursement tightens in 2026.

Growing Surgical Procedure Volumes Worldwide

Post-pandemic backlog clearance elevated global surgical volumes, with Asia-Pacific centers posting the fastest acceleration. Each incision site needs sterile irrigation that lowers bacterial counts below the 105 CFU/g threshold. Ambulatory surgical centers favor single-dose spray canisters, eliminating the compounding step, shaving three minutes of nursing time per case, and aligning with U.S. CMS infection-control mandates that penalize facilities with excess surgical-site infections[2]Centers for Medicare & Medicaid Services, “Hospital-Acquired Condition Reduction Program,” cms.gov. Increased throughput directly expands consumables spend, reinforcing high-volume contracts for leading vendors.

Adoption of Non-Cytotoxic, pH-Balanced Cleansers

The Essential Medicines List draft positioned HOCl as a front-line agent after trials showed 21% faster wound closure versus saline. HOCl’s pH of 3.5–5.5 mirrors the acidic microenvironment of healing tissue, suppresses protease activity, and preserves neutrophil function. FDA draft guidance issued in 2024 limits residual hypochlorite to 10 ppm, prompting in-house analytical capability investment by market leaders. Sonoma Pharmaceuticals leveraged this regulatory clarity to introduce Microdacyn60 Antimicrobial Wound Gel in 2024, underscoring the commercial momentum behind pH-balanced compounds.

Shift to Single-Dose Sterile Packaging

The Joint Commission’s 2024 alert recommended single-use irrigation for all surgical and chronic wounds. Multi-dose bottles become contaminated within 48 hours, even with preservative inclusion, whereas single-dose formats remove benzalkonium chloride exposure, a medium antimicrobial-resistance concern flagged by an earlier FDA rule. Sterisol’s valve-sealed dispensers reached 1,200 U.S. hospitals in 2025, demonstrating clinician confidence in preservative-free delivery. Packaging upgrades also serve FDA supply-chain resilience goals by allowing multiple regional fill-finish partnerships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost versus traditional saline or antiseptics | -0.8% | Global, with acute sensitivity in South America, MEA, and rural Asia-Pacific | Medium term (2-4 years) |

| Stringent multi-region regulatory approvals | -0.6% | Global, with longest timelines in North America, Europe, and Japan | Long term (≥ 4 years) |

| HOCl supply-chain bottlenecks | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Preservative (BAC) reformulation pressures | -0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost Versus Traditional Saline or Antiseptics

Premium cleansers containing HOCl or polyhexanide-betaine are priced 300–500% above saline, slowing uptake where reimbursement coverage is weak. Out-of-pocket payments represent more than 40% of total health expenditure in many Latin American markets, confining adoption to urban private hospitals. Although WHO endorsement could invite generic entrants, HOCl’s cold-chain requirement—it degrades 15% monthly at ambient temperature—keeps manufacturing costs high. Vendors therefore focus on evidence-based dossiers to secure tender wins in upper-income segments.

Stringent Multi-Region Regulatory Approvals

FDA reclassification of antimicrobial washes into Class III devices demands Premarket Approval submissions, stretching timelines to at least 180 days and raising trial costs. EU MDR conformity assessments face bottlenecks at Notified Bodies, with median reviews beyond 24 months. Japan’s PMDA applies additional cytotoxicity and sensitization tests, often requiring bridging studies despite prior CE Mark or FDA clearance. Coloplast’s USD 1.3 billion purchase of Kerecis highlights the premium attached to assets that already hold multi-region clearances, compressing the window for novel formulations to recoup R&D investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Sprays Gain Share Through Sterile Single-Dose Formats

Sprays captured a rising share of the Wound Cleanser Products market in 2026 and are on track for a 6.25% CAGR to 2031, reflecting ambulatory surgical center and home-care preference for turnkey, contamination-free delivery. Solutions maintained 47.55% revenue in 2025 because legacy squeeze bottles remain embedded in hospital contracts, but Joint Commission alerts and infection-control penalties are accelerating a shift toward single-dose devices. Wipes, foams, and gels serve niche but critical roles. Sonoma Pharmaceuticals’ gel formulation, with viscosity near 20,000 cP, sustains HOCl contact for ten minutes, favoring deep pressure ulcers[3]Sonoma Pharmaceuticals, “Fiscal Year 2024 Financial Results,” sonomapharma.com.

Pulsed lavage systems, although capable of automated high-pressure irrigation, stay limited to operating rooms due to capital costs exceeding USD 5,000 per unit. Acelity’s V.A.C. VERAFLO CLEANSE CHOICE integrates instillation therapy, delivering 50–125 mL of cleanser per soak cycle, and anchors a bundled consumable model that drives recurring revenue. Regulatory demands around aerosol propellants and surfactant residues push vendors to document biocompatibility rigorously; FDA guidance released in October 2023 requires complete cytotoxicity and irritation testing for any spray that contacts breached skin.

By Ingredient: Hypochlorous Acid Gains Momentum Post-WHO Endorsement

Hypochlorous Acid is the fastest-growing ingredient segment, projected at 6.85% CAGR. Data from randomized trials show 21% faster closure of diabetic foot ulcers compared with saline. Saline remains the baseline at 33.53% revenue in 2025 due to cost advantage and absence of preservatives, yet lack of antimicrobial activity forces adjunct antiseptic use in contaminated wounds. Chlorhexidine faces erosion because cytotoxicity emerges above 0.05% concentrations, and FDA classifies it as a medium resistance risk. Surfactant blends such as polyhexanide-betaine reach log-4 reductions while maintaining >90% fibroblast viability, securing premium reimbursement in Germany and the Nordics.

Manufacturers must also address extractables; FDA chemical-characterization draft guidance sets 10 ppm as the maximum residual hypochlorite and chlorate limit. Vendors with in-house analytical labs gain speed-to-market advantages by rapidly iterating formulations that satisfy localized standards without reformulation delays.

By End-User Setting: Home-Care Expands Through Telemedicine Integration

Home-Care Settings are climbing at a 7.15% CAGR, the fastest among end-users. CenterWell’s study proved that remote protocols reduce nursing visits and shorten healing times, which aligns with payer imperatives to curb readmissions. Hospitals nonetheless remain the largest purchasers, holding 39.23% revenue in 2025, because of surgical-site irrigation and chronic wound burden. Ambulatory Surgical Centers treat more than 28 million U.S. procedures annually; they opt for pre-filled sprays that cut per-case supply costs by USD 2–4 and eliminate sterile compounding.

Clinics act as prescribing gatekeepers, especially in primary-care settings. The American Academy of Family Physicians’ 2024 guidelines recommend non-cytotoxic cleansers for all chronic wounds, a stance that is driving rural adoption where telemedicine fills specialist gaps. Standardized protocols bolster provider confidence, thereby reducing unwarranted variance in home-care regimens.

Geography Analysis

North America generated 38.25% of 2025 revenue, supported by high per-capita health spending and mature reimbursement frameworks for advanced wound care. The FDA’s Class III reclassification is likely to consolidate share among cash-rich manufacturers that can absorb Premarket Approval costs. Europe maintains robust demand because EU MDR emphasizes biocompatibility and environmental stewardship, favoring biodegradable, non-cytotoxic formulations. Coloplast’s Wound & Skin Care revenue hit DKK 2.0 billion (USD 290 million) in FY 2024/25, underscoring regional appetites for premium products.

Asia-Pacific is the quickest-growing geography, forecast at 6.21% CAGR. China and India drive volume via expanded surgical capacity and diabetes prevalence above 10%. The Medical Device Single Audit Program is standardizing regulatory reviews, shortening market-entry timelines for global suppliers. Japan’s stringent PMDA testing extends review periods, but high aging-related chronic wound incidence sustains spend. Middle East and Africa markets remain fragmented; Gulf Cooperation Council countries modernize procurement faster than Sub-Saharan Africa, yet WHO Essential Medicines List status could unlock public-sector HOCl tenders. South America contends with high out-of-pocket costs, but private clinics in Brazil and Argentina adopt premium cleansers to differentiate services, as evidenced by Sonoma’s distribution pact with Mexico’s Invekra.

Competitive Landscape

The Wound Cleanser Products market exhibits moderate concentration. The top five suppliers capture a significant percentage of global revenue, but no single firm dominates. Smith+Nephew recorded USD 1.681 billion in Advanced Wound Management revenue in 2025, growing 5.1% year over year and supported by bundling cleansers with negative-pressure therapy devices. ConvaTec’s FY 2024 Advanced Wound Care sales reached USD 742.7 million, a 7.4% lift, aided by its InnovaMatrix acquisition and nitric-oxide dressing platform. Solventum’s 2024 extended-wear dressing showcases convergence between cleansing, debridement, and negative-pressure modalities that cut nursing labor and simplify inventory.

Barriers to entry include electrolytic HOCl capacity, cold-chain logistics, and stringent ISO 10993 test batteries. FDA chemical-characterization guidance further raises hurdles by requiring residual hypochlorite quantification below 10 ppm. Vertical integration across raw-material sourcing, in-house electrolysis, and sterile fill-finish provides cost advantages. Strategic M&A focuses on acquiring cleared portfolios that sidestep elongated approval timelines, exemplified by Coloplast’s Kerecis buyout.

Emerging regional disruptors target unmet needs, such as biodegradable packaging or localized electrolysis to bypass HOCl degradation. Yet supply-chain bottlenecks for HOCl precursors in North America and Europe constrain ramp-up, reinforcing incumbent leverage.

Wound Cleanser Products Industry Leaders

Solventum Corporation

Smith & Nephew

Coloplast

ConvaTec

Medline Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Sonoma Pharmaceuticals launched a new HOCl wound cleanser manufactured for Medline Industries.

- October 2024: Mölnlycke Health Care completed the acquisition of P.G.F. Industry Solutions, producer of Granudacyn wound cleansing solutions.

Global Wound Cleanser Products Market Report Scope

As per the scope of the report, wound cleanser products are specialized solutions or agents designed to clean and decontaminate wounds. They help remove debris, dirt, bacteria, and necrotic tissue to promote healing and prevent infection.

The segmentation of the wound cleanser products market is categorized by form, ingredient, end-user setting, and geography. By form, the market includes solutions, sprays, wipes, foams & gels, and pulsed lavage systems. By ingredient, it is segmented into saline (isotonic), hypochlorous acid, chlorhexidine, povidone-iodine, and surfactant-based/others. By end-user setting, the market is divided into hospitals, ambulatory surgical centers, clinics, and home-care settings. By geography, the market covers North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Sprays |

| Wipes |

| Foams & Gels |

| Pulsed Lavage Systems |

| Saline (Isotonic) |

| Hypochlorous Acid |

| Chlorhexidine |

| Povidone-Iodine |

| Surfactant-Based / Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Form | Solutions | |

| Sprays | ||

| Wipes | ||

| Foams & Gels | ||

| Pulsed Lavage Systems | ||

| By Ingredient | Saline (Isotonic) | |

| Hypochlorous Acid | ||

| Chlorhexidine | ||

| Povidone-Iodine | ||

| Surfactant-Based / Others | ||

| By End-User Setting | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Wound Cleanser Products market in 2026?

The market stands at USD 2.80 billion in 2026 and is forecast to reach USD 3.75 billion by 2031.

Which product form is growing the fastest?

Spray formats are slated for a 6.25% CAGR between 2026 and 2031, gaining share due to single-dose sterile delivery.

What ingredient category is expected to outperform?

Hypochlorous Acid leads ingredient growth at 6.85% CAGR, supported by WHO endorsement and strong clinical evidence.

Why is home-care demand accelerating?

Telemedicine platforms that guide cleanser selection reduce nursing visits and align with payers that reward lower readmissions.

Which region shows the highest growth potential?

Asia-Pacific is projected to grow at 6.21% CAGR through 2031, propelled by rising surgical volumes and regulatory harmonization.

Page last updated on: