Gastrointestinal Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

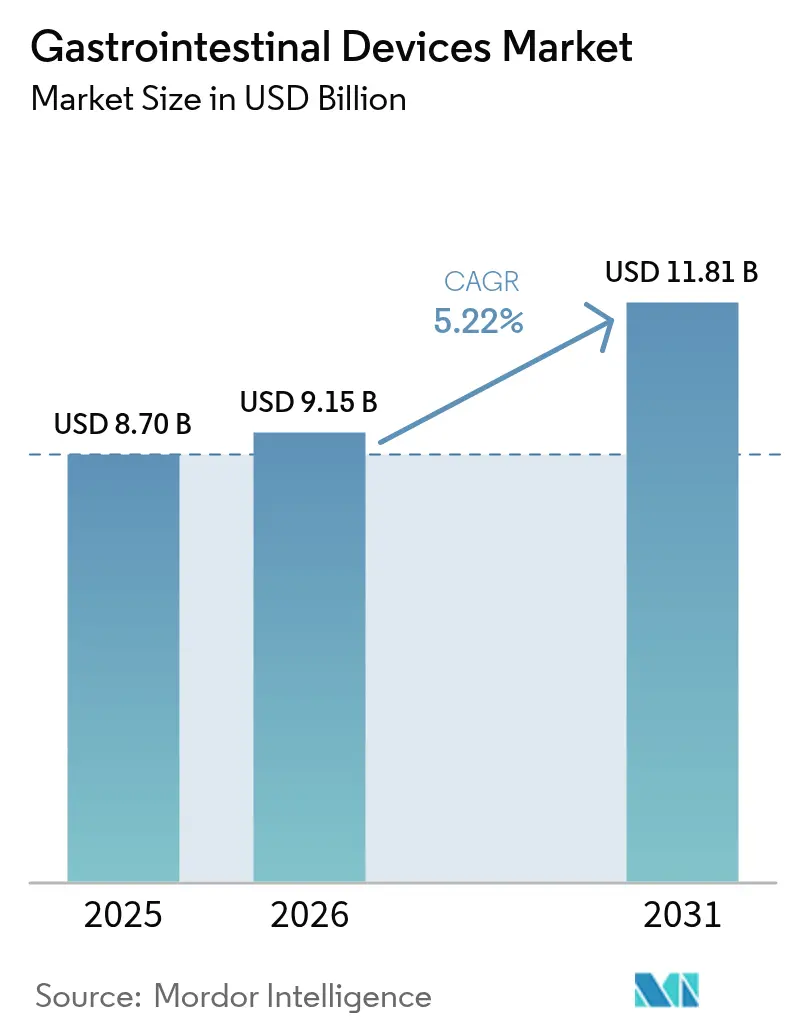

| Market Size (2026) | USD 9.15 Billion |

| Market Size (2031) | USD 11.81 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

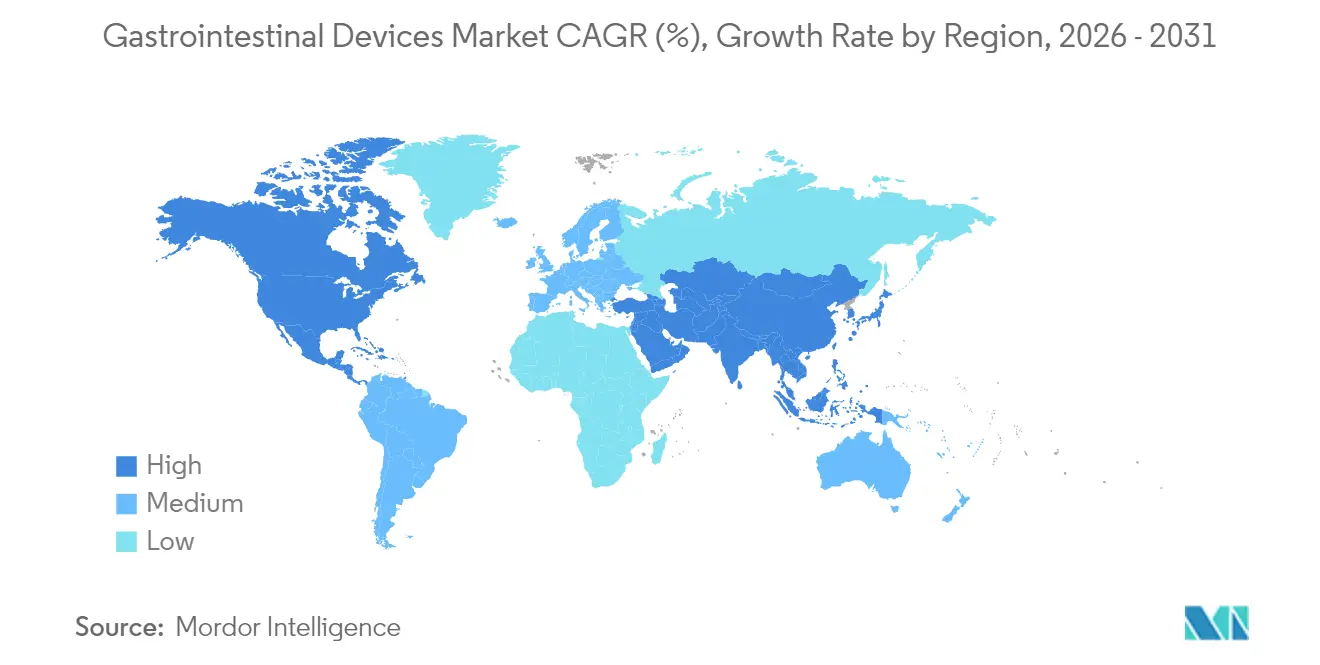

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastrointestinal Devices Market Analysis by Mordor Intelligence

The gastrointestinal devices market size is expected to grow from USD 8.70 billion in 2025 to USD 9.15 billion in 2026 and is forecast to reach USD 11.81 billion by 2031 at 5.22% CAGR over 2026-2031. Growth rests on the dual force of rising gastrointestinal disease prevalence and continuous product innovation, particularly in AI-enabled endoscopy systems that shorten procedure time and raise detection accuracy. Wider reimbursement for outpatient procedures, together with the acceleration of smart wearable and ingestible diagnostics, is expanding the addressable patient pool while shifting volumes from inpatient to ambulatory settings. Competitive intensity remains moderate as the top five suppliers hold a combined 68% share, yet the field stays open to specialized entrants introducing niche solutions such as electrical-mapping wearables and robotic suturing systems. Regionally, North America accounts for 40.02% of revenue on the back of mature screening programs and early AI adoption, while Asia-Pacific records the fastest 7.90% CAGR as infrastructure upgrades meet a steep rise in cancer incidence.

Key Report Takeaways

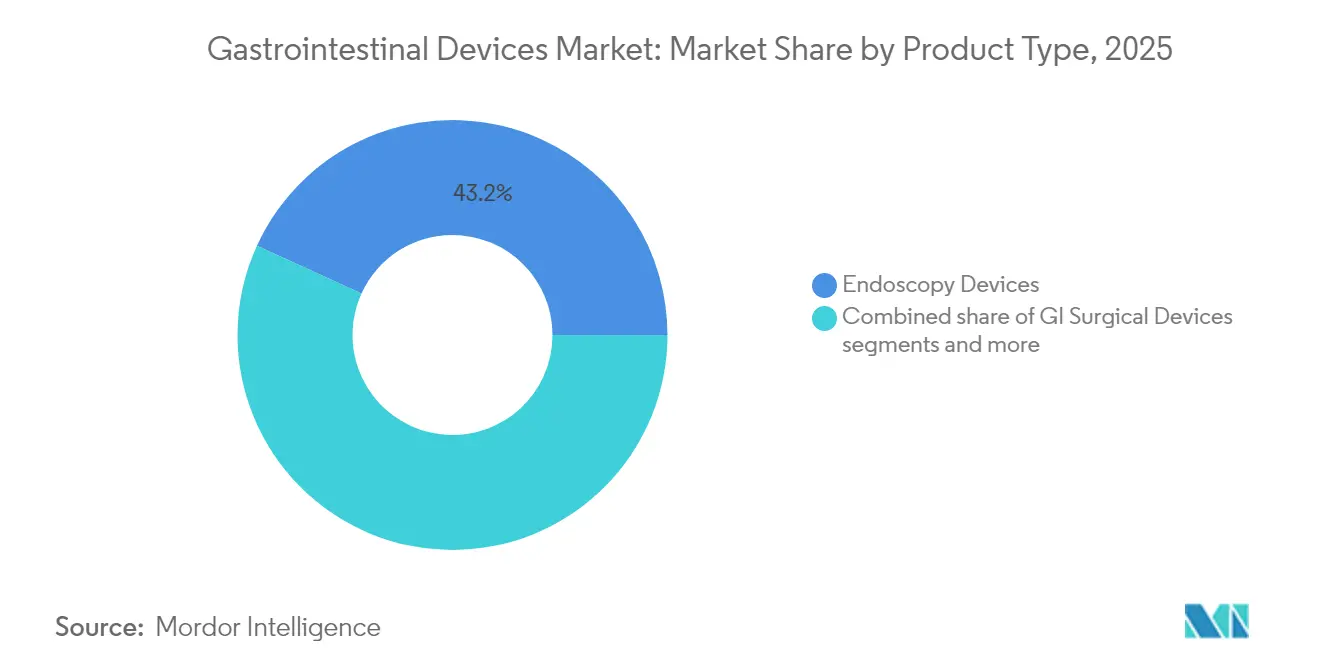

- By product type, endoscopy devices led with 43.18% revenue share in 2025; bariatric surgery devices are forecast to expand at a 6.03% CAGR through 2031.

- By end user, hospitals held 53.25% of the gastrointestinal devices market share in 2025, while specialty clinics and GI labs are projected to grow at 7.15% CAGR to 2031.

- By disease/disorder, colorectal cancer applications accounted for a 38.08% share of the gastrointestinal devices market size in 2025 and inflammatory bowel disease treatments are advancing at a 6.56% CAGR through 2031.

- By geography, North America commanded 39.62% of revenue in 2025; Asia-Pacific exhibits the highest 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastrointestinal Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of GI disorders | +1.8% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Growing adoption of minimally-invasive endoscopy | +1.2% | Global, led by developed markets | Medium term (2-4 years) |

| Ageing population & higher screening compliance | +0.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Expansion of reimbursement for outpatient GI procedures | +0.7% | North America, select European markets | Medium term (2-4 years) |

| AI-assisted endoscopy improving detection | +0.5% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Smart ingestible sensing capsules enabling remote care | +0.3% | Global, pilot programs in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of GI Disorders

Colorectal cancer shows the highest age-standardized incidence in Asia at 23.88 per 100,000 and stomach cancer continues as the top GI cancer killer, pushing demand for earlier detection tools. Non-oncologic burdens, notably inflammatory bowel disease, escalate procedure volumes that rely on advanced imaging, biopsy, and hemostasis devices. Dietary westernization, urban pollution, and sedentary lifestyles magnify disease risk across emerging economies, while the global shift toward older populations further elevates screening frequency. Collectively, these trends create durable pull for both diagnostic and therapeutic solutions within the gastrointestinal devices market.

Growing Adoption of Minimally-Invasive Endoscopy

Endoscopic balloon dilation now defers surgery in inflammatory bowel disease strictures, improving quality of life and trimming inpatient costs. Robotic endoluminal systems enter routine use to navigate tortuous anatomy with millimeter precision, which lowers complication rates and shortens recovery times. Imaging advances such as narrow-band and confocal modalities allow histology-level visualization during a single session, enabling immediate therapy. These combined benefits underpin the expanding share of minimally-invasive interventions inside the gastrointestinal devices market.

Ageing Population & Higher Screening Compliance

Guardant’s Shield blood test detects 83% of colorectal cancers, offering a convenient non-invasive route that boosts adherence among older, risk-averse adults. Medicare’s 2025 ASC payment update lifts reimbursement by 2.6% and broadens covered endoscopic procedures, reinforcing outpatient uptake. As longevity climbs, healthcare systems adopt age-specific surveillance protocols demanding high-definition endoscopes and AI triage software to manage screening loads with limited staff.

Expansion of Reimbursement for Outpatient GI Procedures

CMS proposes adding 547 GI-related codes to the ASC list for 2026, aligning payments with hospital outpatient rates. Separate payment for non-opioid adjuncts encourages facilities to embrace innovative pain-sparing devices. Countries in Europe mirror this shift, recognizing the economic efficiency of advanced endoscopy to shorten stays and prevent costly complications, thereby strengthening commercial prospects for vendors that document measurable outcome gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & device costs | -0.8% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Stringent FDA & CE regulatory clearance timelines | -0.6% | Global, primary impact in North America & Europe | Medium term (2-4 years) |

| Shortage of skilled gastroenterologists | -0.4% | Global, acute in rural and emerging markets | Long term (≥ 4 years) |

| Device-related adverse-event publicity | -0.3% | Global, amplified by social media | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Costs

Premium systems such as robotic platforms and AI processors command high capital outlays and recurring disposables, creating affordability hurdles for lower-income providers. FDA import holds on Olympus inventories illustrate how supply disruptions can tighten availability and sustain pricing power in the United States. Hospitals respond by demanding value-based evidence that links technology cost to quantifiable outcome improvement, lengthening procurement cycles.

Stringent FDA & CE Regulatory Clearance Timelines

EU Medical Device Regulation requires expanded clinical dossiers and ongoing surveillance, pushing recertification deadlines into 2027–2028 and consuming manufacturer resources. Parallel FDA recalls, including Boston Scientific’s embolic agent for lower GI bleeding, reinforce a cautious climate that can delay releases and elevate R&D budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Endoscopy Dominance and Bariatric Momentum

Endoscopy devices contribute 43.18% of 2025 revenue, making them the anchor of the gastrointestinal devices market. The gastrointestinal devices market size for endoscopy is USD 3.76 billion in 2025 and is projected to grow at a 4.85% CAGR through 2031. Continuous breakthroughs such as Olympus EZ1500 extended-depth-of-field scopes improve visualization and raise adenoma detection. AI overlays like Fujifilm CAD EYE deliver a 17% boost in adenoma detection without prolonging procedure time. The segment also benefits from disposable endoscopes that curb infection risk, aligning with stricter reprocessing regulations.

Parallel growth emerges in bariatric surgery devices, the fastest-expanding category at a 6.03% CAGR. MIT’s controllable gastric balloon hints at next-generation implants that can be adjusted post-placement, reducing revision rates. The incisionless ForePass device combines sleeve and balloon principles to cut weight gain by 79% while enhancing insulin sensitivity. Vendors now bundle endoscopic suturing, stapling, and hemostasis consumables to present holistic obesity interventions, expanding the addressable base beyond surgical suites into advanced endoscopy centers.

By Disease/Disorder: Cancer Screening Prevails; IBD Therapy Gains Speed

Colorectal cancer retains 38.08% revenue share in 2025, supported by mandated screening starting at age 45 and the rollout of AI-enhanced colonoscopy that reduces adenoma miss rates by 50%. Endoscopic submucosal dissection and full-thickness resection devices expand curative options without open surgery, preserving bowel function and speeding recovery.

Inflammatory bowel disease shows the fastest 6.56% CAGR as biologic and small-molecule therapies drive endoscopic monitoring frequency. Dual biologic strategies improve remission to 58.6% versus 39.5% with monotherapy, necessitating precise mucosal assessment through high-resolution scopes. Capsule-based motility and bleed detection solutions gain traction in remote disease management, complementing hospital-based therapeutic endoscopy. Obesity and GERD segments expand on the back of incisionless suturing, gastric electrical stimulation, and reflux barrier implants that deliver durable symptom relief without permanent anatomical alterations.

By End User: Hospitals Remain Anchor While Specialty Clinics Accelerate

Hospitals command 53.25% of 2025 sales due to their capacity to manage complex multi-disciplinary cases and emergencies. The gastrointestinal devices market share advantage is reinforced by integrated imaging suites, interventional radiology support, and intensive care backup that smaller facilities cannot match. The segment retains steady growth as tertiary centers adopt robotic platforms, AI video analytics, and hybrid OR suites for advanced resections.

Specialty clinics and GI labs record the highest 7.15% CAGR as payers favor sites offering lower cost per case. Ambulatory surgical centers are projected to perform 44 million procedures by 2034, a 21% volume jump driven largely by endoscopy. Private equity investment accelerates this shift, financing purpose-built facilities equipped with single-use scopes and cloud AI platforms that ensure rapid turnover. Home-based capsule endoscopy assisted by 5G connectivity achieves 88% patient satisfaction and slashes travel-related emissions, pointing to a nascent but important extension of care pathways.

Geography Analysis

North America holds 39.62% revenue in 2025 owing to robust reimbursement and swift technology adoption. Early commercial deployment of AI cloud platforms and the FDA clearance of robotic systems such as Johnson & Johnson’s OTTAVA underscore the region’s innovation leadership. Supply-chain setbacks, including import holds on key endoscope models, can create intermittent device shortages yet also trigger rapid supplier diversification.

Asia-Pacific posts a 7.78% CAGR, the fastest worldwide, thanks to higher cancer incidence, economic growth, and government spending on advanced imaging suites. The launch of India’s Gastro AI Academy illustrates dedicated efforts to upskill clinicians in AI-augmented workflows. China and South Korea channel state funding into domestic manufacturing of endoscopes and capsules to reduce import reliance, while Australia pilots nationwide tele-endoscopy programs in rural communities.

Europe shows steady mid-single-digit growth tempered by Medical Device Regulation complexity. Extended recertification deadlines strain SME suppliers but enhance patient safety confidence in the long term. Major economies prioritize colorectal cancer screening adherence, underpinning sustained system purchases of advanced colonoscopy stacks.

Latin America and the Middle East & Africa together contribute a smaller but rising share. Brazil’s regulator ANVISA modernizes review pathways, attracting multinational suppliers, whereas Chile’s clinical-trial uptick signals growing regional R&D importance. Gulf Cooperation Council members invest in AI and robotics ranging from tele-endoscopy to print-on-demand stents, positioning the region for above-average future expansion.

Competitive Landscape

The five largest companies command’s more than half of global sales, signifying moderate consolidation yet leaving meaningful room for specialist challengers. Olympus maintains its edge through continual optical upgrades and the first cloud-based AI detection service cleared by FDA. Boston Scientific’s share benefitted from the 2023 Apollo Endosurgery buyout that expanded bariatric solutions, while Medtronic strength of its GI Genius analytics engine.

Digital platform strategies dominate competitive positioning. Johnson & Johnson’s Polyphonic ecosystem couples video editing, case management, and AI modelling, supported by an NVIDIA alliance to scale real-time analytics in the OR. Canon Medical and Olympus cooperate on endoscopic ultrasound, illustrating a trend toward selective partnership rather than head-to-head competition[1]Source: Med-Tech Innovation, “Canon Medical and Olympus Team up,” med-technews.com .

Disruptors concentrate on novel sensing and access devices. Alimetry’s electrical-mapping wearable targets functional gut disorders outside conventional endoscopy, and AnX Robotica’s NaviCam system advances AI-guided capsule navigation. Strategic acquisitions such as Stryker’s USD 4.9 billion purchase of Inari Medical widen vascular access to GI bleeding applications[2]Source: Stryker Corporation, “Completes Acquisition of Inari Medical,” investors.stryker.com .

Gastrointestinal Devices Industry Leaders

Medtronic

Boston Scientific Corporation

CONMED Corporation

Olympus Corporation

Stryker

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus Corporation announced FDA clearance of EZ1500 endoscopes with extended depth of field

- February 2025: Stryker closed its USD 4.9 billion acquisition of Inari Medical, expanding into mechanical thrombectomy

Global Gastrointestinal Devices Market Report Scope

As per the scope of the report, gastrointestinal devices are used to examine the internal lining of the gastrointestinal tract. Additionally, they are used for diagnosing and treating medical conditions related to the digestive system or gastrointestinal tract.

The gastrointestinal devices market is segmented by product type (GI videoscopes, biopsy devices, endoscopic retrograde cholangiopancreatography devices (ERCP), capsule endoscopy, endoscopic ultrasound, other product types), end-users (hospitals, clinics & other end-users), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions.

The report offers the value in USD for the above segments.

| Endoscopy Devices | Endoscopes |

| Visualization & Insufflation Systems | |

| GI Surgical Devices | |

| Bariatric Surgery Devices | |

| GI Hemostasis Devices | |

| GI Stent Devices | |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & GI Labs |

| Home-Care Settings |

| Colorectal Cancer |

| Inflammatory Bowel Disease (IBD) |

| Obesity |

| Gastro-Esophageal Reflux Disease (GERD) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Endoscopy Devices | Endoscopes |

| Visualization & Insufflation Systems | ||

| GI Surgical Devices | ||

| Bariatric Surgery Devices | ||

| GI Hemostasis Devices | ||

| GI Stent Devices | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & GI Labs | ||

| Home-Care Settings | ||

| By Disease/ Disorder | Colorectal Cancer | |

| Inflammatory Bowel Disease (IBD) | ||

| Obesity | ||

| Gastro-Esophageal Reflux Disease (GERD) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the gastrointestinal devices market?

It stands at USD 9.15 billion in 2026 and is forecast to reach USD 11.81 billion by 2031.

Which product segment contributes the largest revenue?

Endoscopy devices generate 43.18% of 2025 sales due to their central role in diagnostics and therapy.

Which region is expanding the fastest?

Asia-Pacific shows a 7.78% CAGR through 2031 as infrastructure investment meets rising disease incidence.

How are AI tools affecting colonoscopy outcomes?

AI systems such as GI Genius deliver 99.7% sensitivity and cut adenoma miss rates by half, raising screening effectiveness.

Why are specialty clinics gaining share from hospitals?

Payers favor their lower cost per procedure and rapid turnover, and ASCs are projected to perform 44 million procedures by 2034.

What regulatory change most influences device availability in Europe?

The EU Medical Device Re

Page last updated on: