United States Pressure Ulcer Prevention Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

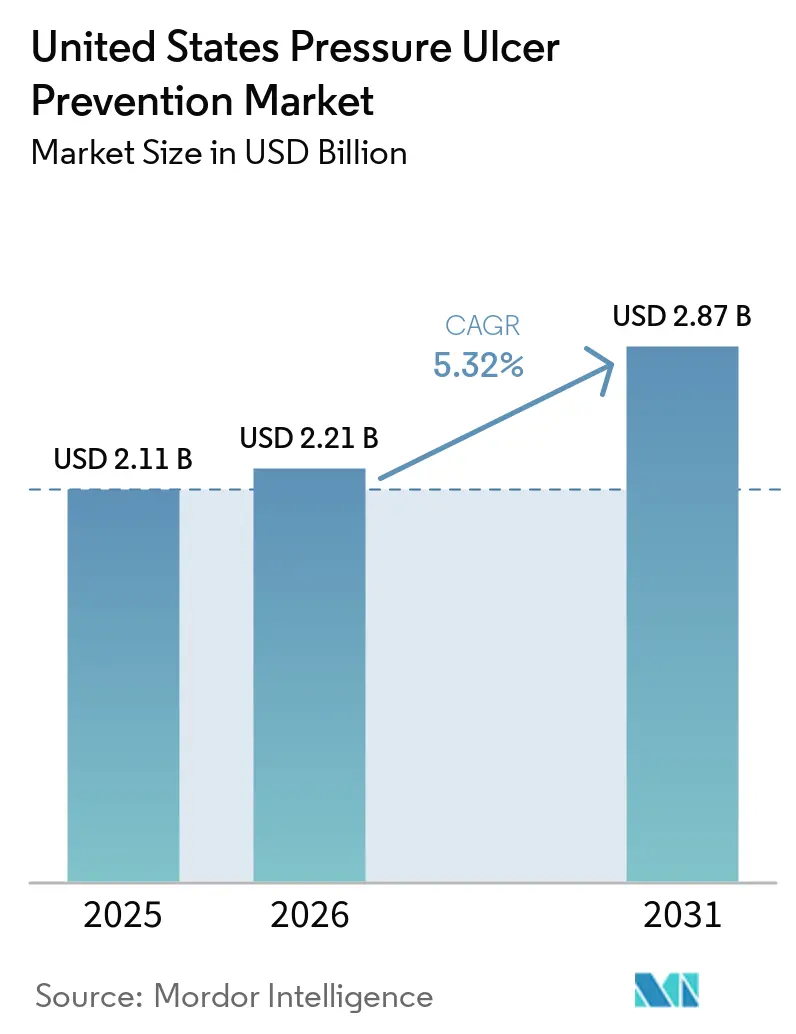

| Base Year Market Size (2025) | USD 2.11 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

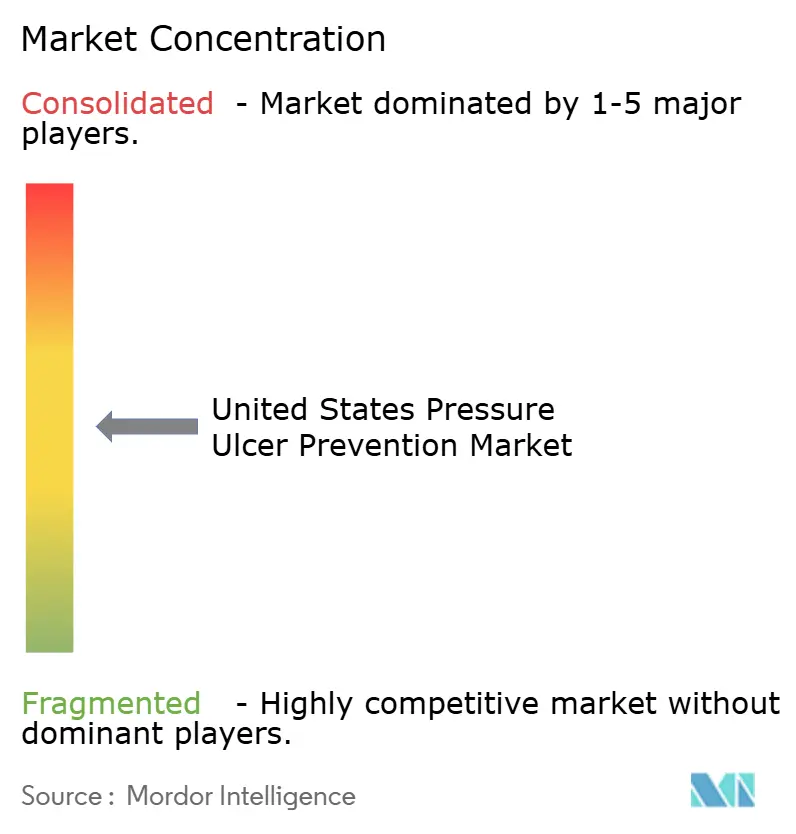

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Pressure Ulcer Prevention Market Analysis by Mordor Intelligence

The United States Pressure Ulcer Prevention Market size is expected to increase from USD 2.11 billion in 2025 to USD 2.21 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 5.32% over 2026-2031.

The pressure ulcer prevention market is being supported by a durable rise in older patients who live with limited mobility, longer recovery cycles, and more frequent critical care needs, which keeps prevention demand elevated across acute care, post-acute care, and home-based settings. The pressure ulcer prevention market is also benefiting from the fact that provider organizations now treat avoidable skin injury as a direct operating issue because prevention affects outcomes, care quality, performance, and the cost of extended treatment pathways. Demand is moving beyond basic redistribution products toward higher-value systems that support bariatric care, moisture management, and earlier risk detection, which raises average selling prices even when unit volumes rise at a steadier pace. The pressure ulcer prevention market is further strengthened by the shift of care into homes and community settings, where prevention has to continue after discharge instead of ending at hospital exit. Competition remains strongest around evidence-backed products, workflow support, and institutional contracting, while the biggest open opportunity sits in simpler solutions for caregivers and smaller facilities that struggle to match large-system prevention programs.

Key Report Takeaways

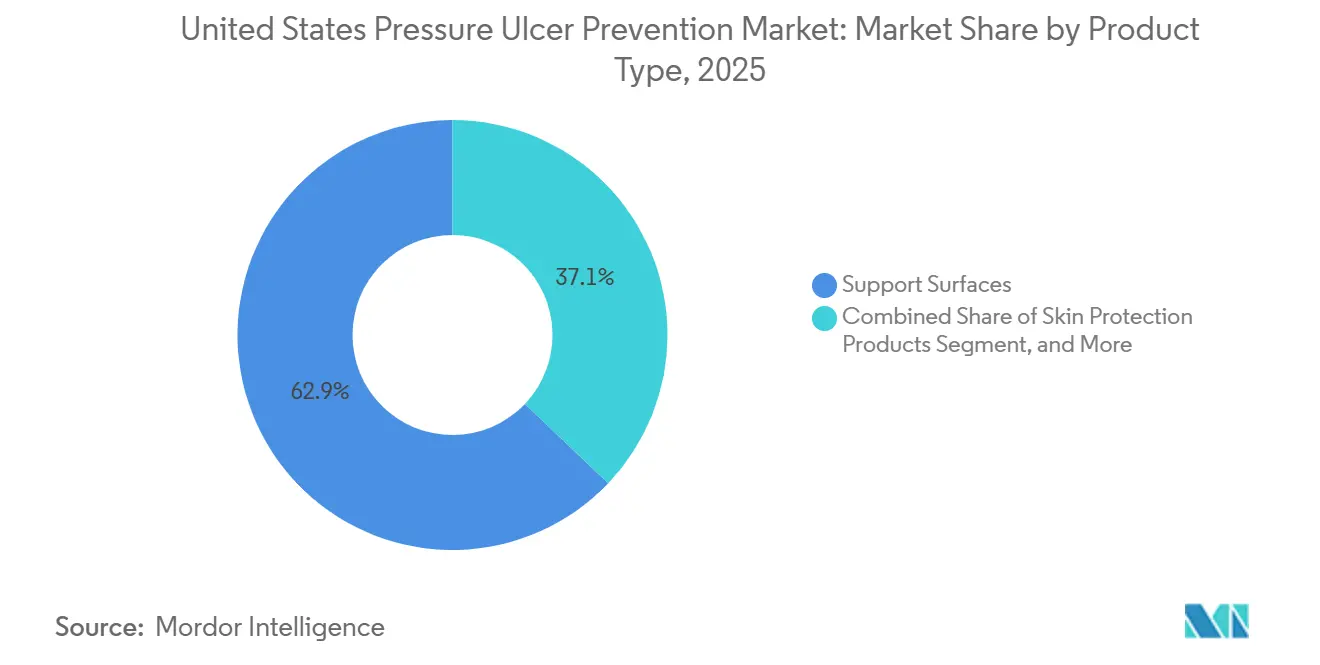

- By product type, support surfaces held 62.87% of the pressure ulcer prevention market share in 2025, while skin protection products are projected to expand at 6.36% CAGR through 2031.

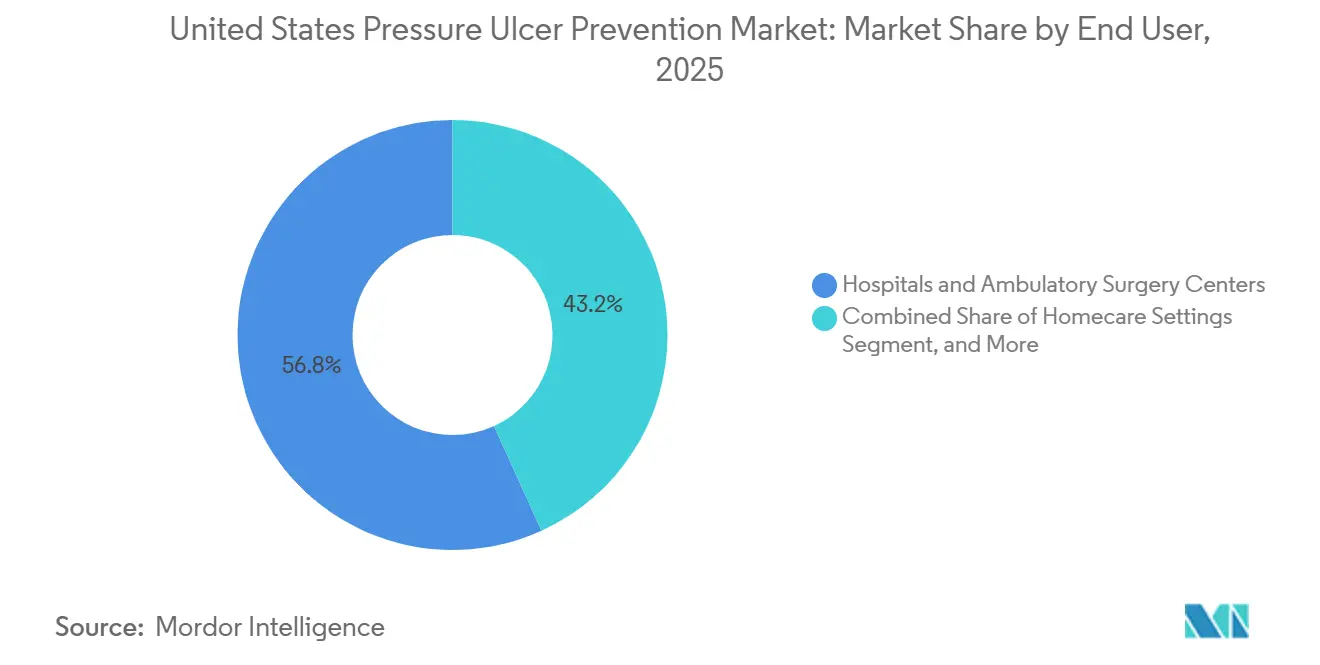

- By end user, hospitals & ambulatory surgery centers accounted for 56.83% share of the pressure ulcer prevention market size in 2025, while homecare settings are projected to advance at 7.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Pressure Ulcer Prevention Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Immobile And Critically Ill Patient Base | +1.8% | National, concentrated in Southeast, Sunbelt, and Midwest | Long term (≥ 4 years) |

| HAPI Cost And Quality Of Care Penalties | +1.5% | National, with acute impact in high-volume hospital markets in the Northeast and Midwest | Medium term (2-4 years) |

| Homecare And Post-Discharge Prevention Demand | +1.2% | National, with early gains in Florida, California, and Texas | Medium term (2-4 years) |

| Better Support Surfaces And Prophylactic Dressings | +0.9% | National, strongest at academic medical centers and Level 1 trauma hospitals | Short term (≤ 2 years) to Medium term (2-4 years) |

| HH-PI eCQM And POA Documentation Pressure | +0.5% | National, with near-term intensity at large teaching hospitals | Medium term (2-4 years) |

| Early Detection Workflows Using SEM And Thermal Imaging | +0.4% | National, with early gains in ICUs at systems with GPO agreements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging, Immobile, and Critically Ill Patient Base

The aging population remains the most durable demand base for the pressure ulcer prevention market because older adults are more likely to experience immobility, frailty, and longer inpatient stays. Baby boomers were in the 61 to 79 age range in 2025, which means the United States continues to carry a large cohort of patients who are more exposed to pressure injury risk across hospitals, long-term care sites, and home settings.[1]U.S. Census Bureau, “U.S. Population Aging as Nation Turns 250,” Census Bureau Stories, census.gov That demographic shift matters because prevention spending rises not only with patient numbers, but also with the severity and duration of care required for each high-risk admission. The product mix is also moving upward in value because older patients increasingly present with obesity, cardiovascular conditions, and other comorbidities that require bariatric-rated surfaces and better moisture control. This pattern gives the pressure ulcer prevention market a broader revenue base than simple bed occupancy growth would suggest.

HAPI Cost and Quality-Of-Care Penalties

Hospital-acquired pressure injuries now sit much closer to executive decision making because they affect cost control, care quality, and reputational risk at the same time. The pressure ulcer prevention market benefits from this shift because provider systems are putting more weight on prevention pathways that can be standardized, tracked, and defended during quality review. Cleveland Clinic reported a 36% reduction in hospital-acquired pressure injuries between 2024 and 2025 after implementing a systematic interprofessional prevention protocol, which shows that hospitals are willing to scale structured prevention when the operational case is clear.[2]Cleveland Clinic, “Protecting the Body’s Largest Organ: Nurse-Led Strategy Reduces Hospital-Acquired Pressure Injuries,” Consult QD, clevelandclinic.org Documentation standards are also becoming more important because facilities need stronger admission records and clearer proof of prevention activity throughout the patient's stay. That increases the appeal of products and workflows that support early assessment, consistent care delivery, and auditable records across nursing teams.

Homecare and Post-Discharge Prevention Demand

Homecare is becoming a larger growth engine for the pressure ulcer prevention market as discharge happens earlier and more preventive care moves outside institutional walls. This shift does not reduce risk, because many patients still leave acute care with limited mobility, fragile skin, and ongoing caregiver dependence after discharge. A 2025 JMIR Nursing study developed an AI-assisted decision support tool for home-visiting nurses managing pressure injuries and achieved expert-level agreement of 0.92 during validation, which supports the idea that home-based prevention can move closer to institutional clinical quality when guidance tools are in place.[3]JMIR Nursing, “An Expert Knowledge Algorithm and Model Predicting Wound Healing Trends for a Decision Support System for Pressure Injury Management in Home Care Nursing: Development and Validation Study,” JMIR Nursing, jmir.org The channel implication is significant because family caregivers and home health agencies need different products, packaging, and training than hospital buyers. That is why the pressure ulcer prevention market is opening new room for direct homecare distribution, simpler repositioning tools, and easy-to-use skin protection products.

Better Support Surfaces and Prophylactic Dressings

The pressure ulcer prevention market is also being lifted by better products that address pressure, friction, shear, and moisture together instead of treating them as separate problems. Smith+Nephew launched ALLEVYN COMPLETE CARE Foam Dressing in the United States in March 2026 with ShearDEFENSE Technology and reported 93% mechanical energy absorption along with clinical evidence of more than 65% pressure injury risk reduction. In January 2025, ECRI upgraded its Evidence Bar ratings for ALLEVYN LIFE Sacrum Foam Dressing and the LEAF Patient Monitoring System to favorable, which matters because hospital committees often rely on third-party evidence review when making formulary decisions. This makes evidence quality a practical barrier to entry for suppliers that lack peer-reviewed support or independent assessment. It also shortens the commercial life of older foam products that cannot match newer outcome data.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Replacement Cost Of Advanced Surfaces | -0.8% | National, disproportionate in rural community hospitals and small SNFs | Long term (≥ 4 years) |

| Variable Adherence To Turning And Skin-Assessment Protocols | -0.5% | National, acute in facilities with high nurse turnover and low staffing ratios | Medium term (2-4 years) |

| Device-Related Pressure Injury Complexity | -0.3% | National, concentrated in ICU and perioperative settings | Medium term (2-4 years) |

| Diagnostic Ambiguity Between POA Injury, Skin Failure, And HAPI | -0.2% | National, acute at hospitals with limited wound care specialist coverage | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Replacement Cost of Advanced Surfaces

High acquisition and replacement costs continue to limit how quickly the pressure ulcer prevention market can move deeper into smaller hospitals and nursing facilities. Advanced alternating-pressure and low-air-loss systems offer better clinical capability, but they also bring ongoing costs tied to maintenance, replacement covers, pumps, and staff familiarization. Rental models reduce the first purchase hurdle, yet they can also create dependence on third parties and slow standardization across a care network. This gap is most visible in rural hospitals and smaller skilled nursing facilities where prevention budgets compete directly with labor needs and other essential expenses. The result is a two-speed pressure ulcer prevention market in which large health systems upgrade faster while smaller sites stay on older or lower-specification surfaces.

Variable Adherence to Turning and Skin-Assessment Protocols

Clinical execution remains a major restraint because better products do not produce full value when repositioning, and skin checks are inconsistent. ANEDIDIC reported in 2025 that 95% of pressure injuries are clinically preventable, while still identifying caregiver knowledge and execution as the decisive barrier to better outcomes. Cleveland Clinic showed the opposite side of the issue when its structured interprofessional protocol reduced hospital-acquired pressure injuries by 36% between 2024 and 2025 through systematic execution rather than new hardware alone. This means adherence tools, wearable compliance devices, and digital documentation systems are becoming commercially relevant alongside mattresses and dressings. Vendors that solve the workflow problem as well as the product problem will be better placed in the pressure ulcer prevention market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Advanced Surfaces Hold the Largest Base While Skin Protection Moves Faster

Support surfaces captured 62.87% of revenue in 2025, which gave them the largest share within the pressure ulcer prevention market because critical care and perioperative settings still rely on active redistribution as a core prevention measure. This high share reflects the fact that ICU, step-down, and higher-acuity patients often need continuous support that basic surfaces cannot provide consistently. Dynamic systems such as alternating-air, low-air-loss, and lateral rotation platforms continue to command a larger portion of value because they are used for patients with the greatest risk exposure and the highest level of monitoring. Arjo remains well placed in this part of the pressure ulcer prevention market through platforms such as AtmosAir Velaris and Auralis, which support both standard and bariatric care needs across acute settings. Static foam, gel overlays, and hybrid reactive formats remain important in long-term care and home settings where budget discipline is tighter, and product simplicity matters more than full dynamic capability.

Skin protection products are projected to grow at 6.36% CAGR through 2031, which makes them the fastest-growing product category within the pressure ulcer prevention market. That growth reflects wider use of barrier films, no-sting protectants, and preventive skin management in perioperative pathways, ambulatory care, and discharge planning. The pressure ulcer prevention market size for Skin Protection Products is rising because these items are easier to standardize, easier to distribute into non-acute channels, and easier for caregivers to use outside clinical facilities. Prophylactic dressing innovation also supports the category because stronger evidence around friction and shear reduction encourages broader protocol adoption. Detection and Monitoring Technologies remain the smallest segment today, but institutional interest is increasing as providers seek earlier risk visibility and better workflow documentation, and Bruin Biometrics reported that its Provizio SEM Scanner had exceeded 1 million patient scans since commercialization, with an estimated 50,000 reportable pressure injuries prevented.

By End User: Hospitals Lead Current Spending While Homecare Changes the Next Phase

Hospitals & ambulatory surgery centers held 56.83% of end-user revenue in 2025, which gave them the leading position in the pressure ulcer prevention market share because the most severe risk still concentrates in inpatient and procedural care. This lead reflects the high burden seen in ICUs, step-down units, and perioperative suites where patients are immobile, medically complex, and often unable to reposition themselves. Device-related pressure injuries add another layer of need in these settings because masks, tubes, and other equipment create localized risk that standard surfaces alone cannot fully offset. Large hospitals are therefore the first buyers of evidence-backed surfaces, prophylactic dressings, early assessment tools, and workflow systems that support documentation and protocol consistency. Clinics and wound care centers are also gaining a larger role because many health systems now use them to stabilize patients during discharge transitions before care moves fully into the home.

Homecare settings are projected to expand at 7.37% CAGR through 2031, making them the fastest-growing end-user category in the pressure ulcer prevention market. This trend is being driven by earlier discharge, hospice expansion, and the transfer of prevention responsibility from staffed clinical settings to caregivers who need practical tools and clearer guidance. Long Term Care & Urgent Care Centers remain the second-largest institutional channel because they serve people with ongoing immobility risk and frequent dependence on Medicaid-linked reimbursement. The pressure ulcer prevention market size for Homecare Settings is increasing as caregivers need products that are easy to apply, easy to purchase, and simple to use without clinical training, which differs sharply from hospital-centered portfolios. That mismatch leaves a visible opening for manufacturers that can tailor products and packaging to caregiver-managed prevention instead of relying on repurposed institutional formats.

Geography Analysis

The United States pressure ulcer prevention market shows clear regional variation in patient mix, care settings, and product preferences. The Southeast, led by Florida, Georgia, and the Carolinas, carries a large share of older adults and therefore a larger base of patients with immobility-related risk. That profile supports strong demand across skilled nursing facilities, assisted living centers, and homecare providers that manage long-duration prevention needs. Pressure ulcer prevention market share is therefore supported by volume in the Southeast, even though a large part of demand remains concentrated in lower-cost surfaces and barrier products. Springer Nature reported persistent U.S. disparities in deaths with documented pressure injuries that track uneven care access and high rates of cardiovascular disease and diabetes, and those conditions remain overrepresented in several Southeastern care populations.

The Northeast and Mid-Atlantic corridor remains the strongest premium-tier adoption zone within the pressure ulcer prevention market. Academic medical centers in Boston, New York, Philadelphia, and nearby health systems are more likely to adopt evidence-backed dressings, early detection tools, and advanced workflows because they combine research capacity with large purchasing contracts. That environment helps newer technologies move faster from evaluation to protocol adoption. Cleveland Clinic’s 2025 quality-improvement results also reinforce how major systems in this broad corridor are setting visible benchmarks for HAPI reduction through structured prevention programs.

The Midwest presents a split picture for the pressure ulcer prevention market because large integrated delivery networks coexist with rural hospitals that face tighter capital limits. States such as Ohio, Illinois, Minnesota, and Michigan include sophisticated prevention programs, but they also include smaller facilities that cannot upgrade surfaces as quickly. Western states, especially California and Washington, are pushing prevention toward more digitally connected post-discharge care models. That makes the pressure ulcer prevention market more service-oriented in the West, with greater interest in remote assessment support, homecare continuity, and products that fit telehealth-linked care pathways.

Competitive Landscape

The United States pressure ulcer prevention market is moderately consolidated in premium product tiers and much more fragmented in the middle of the market. Smith+Nephew, Mölnlycke Health Care, and ConvaTec remain important in prophylactic dressings and skin protection because hospitals continue to favor products that are supported by evidence and already recognized by clinical buyers. Arjo holds a strong position in advanced support surfaces, especially where bariatric care, patient handling, and higher-acuity use cases matter most. Bruin Biometrics occupies a distinct position in early detection because it has built commercial traction around SEM scanning rather than competing directly in mattresses or foam dressings. That mix gives the pressure ulcer prevention market a layered structure in which no single company dominates every category, but a small group retains stronger leverage where evidence and workflow integration matter most.

Recent company actions show that competition in the pressure ulcer prevention market is being shaped less by broad branding and more by proof, contracting, and workflow fit. Smith+Nephew launched ALLEVYN COMPLETE CARE Foam Dressing in the United States in March 2026 and supported the product with evidence around mechanical energy absorption and pressure injury risk reduction. In January 2025, Smith+Nephew also received favorable ECRI Evidence Bar ratings for ALLEVYN LIFE Sacrum Foam Dressing and the LEAF Patient Monitoring System, which strengthened the company’s standing with hospital value-analysis committees. Bruin Biometrics reported more than 100 peer-reviewed publications linked to its Provizio SEM Scanner and more than 1 million patient scans, which gives it a meaningful evidence position in a specialized part of the pressure ulcer prevention market.

Competitive white space remains visible in three areas. The first is integrated prevention that combines hardware, compliance monitoring, and documentation support, because no single vendor fully owns that workflow across settings. The second is homecare and caregiver-managed prevention, where many current offerings still feel adapted from hospital portfolios rather than designed for consumers and home health teams. The third is bariatric prevention, where size range, weight thresholds, and ease of use still create gaps in many standard product lines. Arjo’s 2025 launch of the Maxi Move 5 and its continued emphasis on patient handling show how mobility support is becoming part of the broader prevention value proposition rather than a separate adjacent category.

United States Pressure Ulcer Prevention Industry Leaders

Baxter International Inc.

Cardinal Health, Inc.

Mölnlycke Health Care AB

Solventum Corporation

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smith+Nephew launched ALLEVYN COMPLETE CARE Foam Dressing in the United States, featuring ShearDEFENSE Technology with 93% mechanical energy absorption and clinically validated pressure injury risk reduction exceeding 65%.

- October 2025: Smith+Nephew published new peer-reviewed data for ALLEVYN COMPLETE CARE in the International Wound Journal, demonstrating its Frictional Energy Absorber Effectiveness mechanism of action that supported the product’s United States launch.

- April 2025: Arjo launched the Maxi Move 5 mobile patient floor lift in the United States, Germany, France, and the Netherlands, with rollout planned to approximately 40 countries by end-2025.

- January 2025: ECRI upgraded its Evidence Bar ratings for Smith+Nephew’s ALLEVYN LIFE Sacrum Foam Dressing and LEAF Patient Monitoring System to favorable following independent clinical evidence assessment.

United States Pressure Ulcer Prevention Market Report Scope

The Pressure Ulcer Prevention Market encompasses the industry of medical devices, wound care products, and software solutions designed to proactively prevent pressure sores (bedsores) in immobile or high-risk patients.

The United States Pressure Ulcer Prevention Market, reported in terms of value (USD), is segmented across several dimensions that define its structure and demand drivers. By product type, the market includes support surfaces, prophylactic dressings, positioners and protectors, skin protection products, and detection and monitoring technologies. In terms of end users, adoption spans hospitals and ambulatory surgical centers (ASCs), clinics, long‑term care and urgent care centers, as well as homecare settings.

| Support Surfaces | Dynamic Support Surfaces | Alternating-air Mattresses |

| Low-air-loss Mattresses | ||

| Air-fluidized and High-air-loss Mattresses | ||

| Lateral Rotation and Microclimate-enabled Surfaces | ||

| Static Support Surfaces | Foam Mattresses | |

| Gel Overlays | ||

| Static Air and Hybrid Reactive Overlays | ||

| Prophylactic Dressings | Sacral Dressings | |

| Heel Dressings | ||

| Anatomical Multi-site Dressings | ||

| Positioners & Protectors | Heel Off-loading Boots | |

| Turn and Repositioning Aids | ||

| Wheelchair Cushions and Seat Positioners | ||

| Skin Protection Products | Barrier Creams | |

| No-sting Barrier Films and Skin Protectants | ||

| Detection & Monitoring Technologies | SEM Scanners | |

| Wearable Turn-compliance Sensors | ||

| Thermal and Imaging-based Assessment Tools | ||

| Hospitals & Ambulatory Surgery Centers | Intensive Care Units |

| Medical-Surgical and Step-down Units | |

| Perioperative and PACU Settings | |

| Clinics | Wound Care Centers |

| Outpatient Specialty Clinics | |

| Long Term Care & Urgent Care Centers | Skilled Nursing Facilities |

| Nursing Homes and Assisted Living Facilities | |

| Urgent Care Centers | |

| Homecare Settings | Home Health Agencies |

| Hospice and Palliative Home Care | |

| Caregiver-managed Home Use |

| By Product Type | Support Surfaces | Dynamic Support Surfaces | Alternating-air Mattresses |

| Low-air-loss Mattresses | |||

| Air-fluidized and High-air-loss Mattresses | |||

| Lateral Rotation and Microclimate-enabled Surfaces | |||

| Static Support Surfaces | Foam Mattresses | ||

| Gel Overlays | |||

| Static Air and Hybrid Reactive Overlays | |||

| Prophylactic Dressings | Sacral Dressings | ||

| Heel Dressings | |||

| Anatomical Multi-site Dressings | |||

| Positioners & Protectors | Heel Off-loading Boots | ||

| Turn and Repositioning Aids | |||

| Wheelchair Cushions and Seat Positioners | |||

| Skin Protection Products | Barrier Creams | ||

| No-sting Barrier Films and Skin Protectants | |||

| Detection & Monitoring Technologies | SEM Scanners | ||

| Wearable Turn-compliance Sensors | |||

| Thermal and Imaging-based Assessment Tools | |||

| By End User | Hospitals & Ambulatory Surgery Centers | Intensive Care Units | |

| Medical-Surgical and Step-down Units | |||

| Perioperative and PACU Settings | |||

| Clinics | Wound Care Centers | ||

| Outpatient Specialty Clinics | |||

| Long Term Care & Urgent Care Centers | Skilled Nursing Facilities | ||

| Nursing Homes and Assisted Living Facilities | |||

| Urgent Care Centers | |||

| Homecare Settings | Home Health Agencies | ||

| Hospice and Palliative Home Care | |||

| Caregiver-managed Home Use | |||

Key Questions Answered in the Report

How large is the United States pressure ulcer prevention space in 2026?

It stands at USD 2.21 billion in 2026 and is projected to reach USD 2.87 billion by 2031 at a 5.32% CAGR.

Which product category leads current revenue?

Support surfaces lead with 62.87% of revenue in 2025 because higher-acuity care settings still rely on active pressure redistribution.

Which end-user setting is growing the fastest through 2031?

Homecare settings are projected to grow at 7.37% CAGR as more prevention shifts to caregiver-managed care after discharge.

Why are hospitals investing more in prevention workflows now?

Hospitals are tying prevention more closely to outcome management, documentation quality, and avoidable harm reduction, and Cleveland Clinic showed a 36% HAPI reduction from a structured protocol between 2024 and 2025.

Which companies are strongest in this space today?

Smith+Nephew, Mölnlycke, ConvaTec, Arjo, and Bruin Biometrics are among the most visible participants, with strength spread across dressings, surfaces, and early detection.

Page last updated on: