Ileostomy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

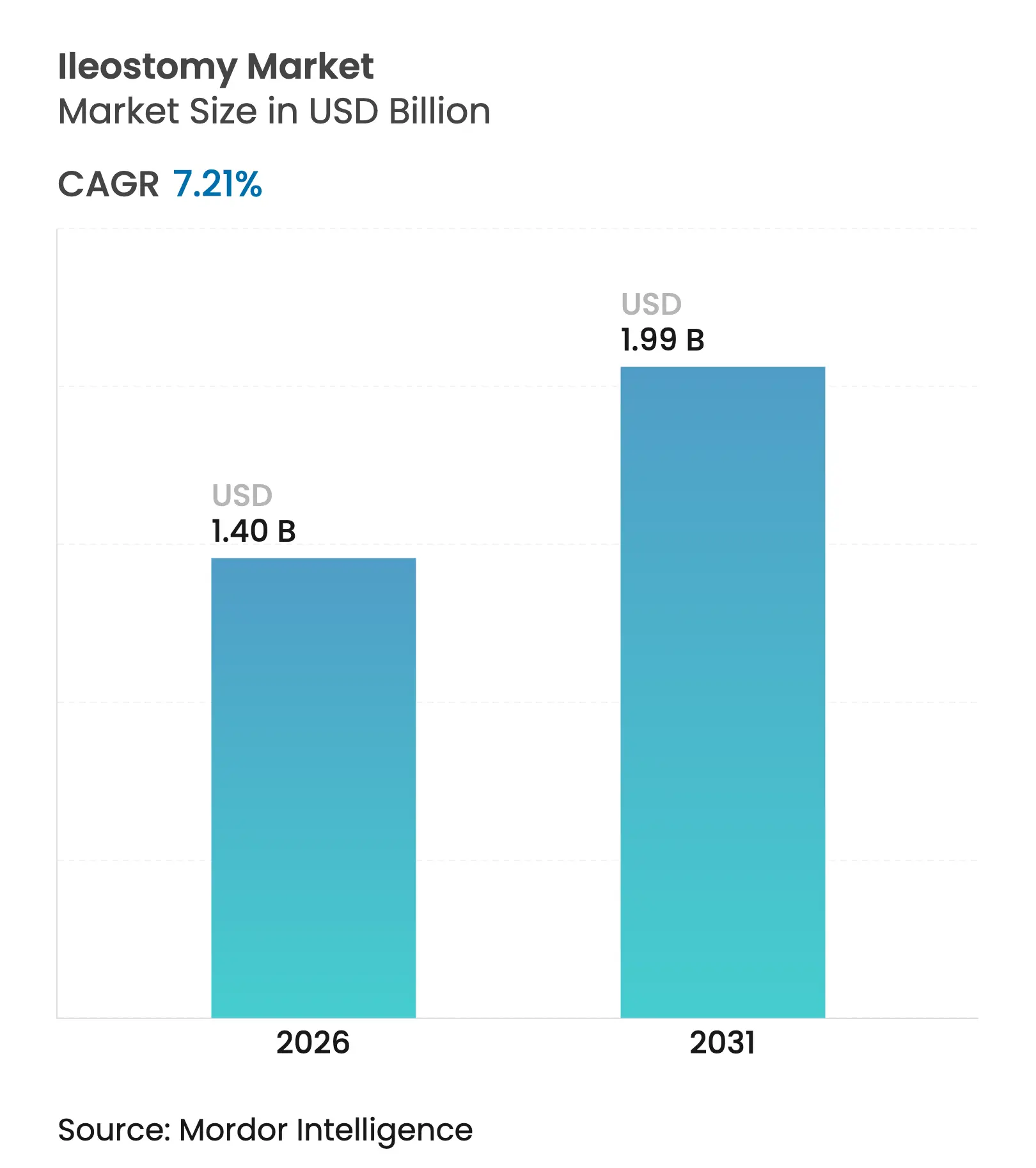

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 7.21 % CAGR |

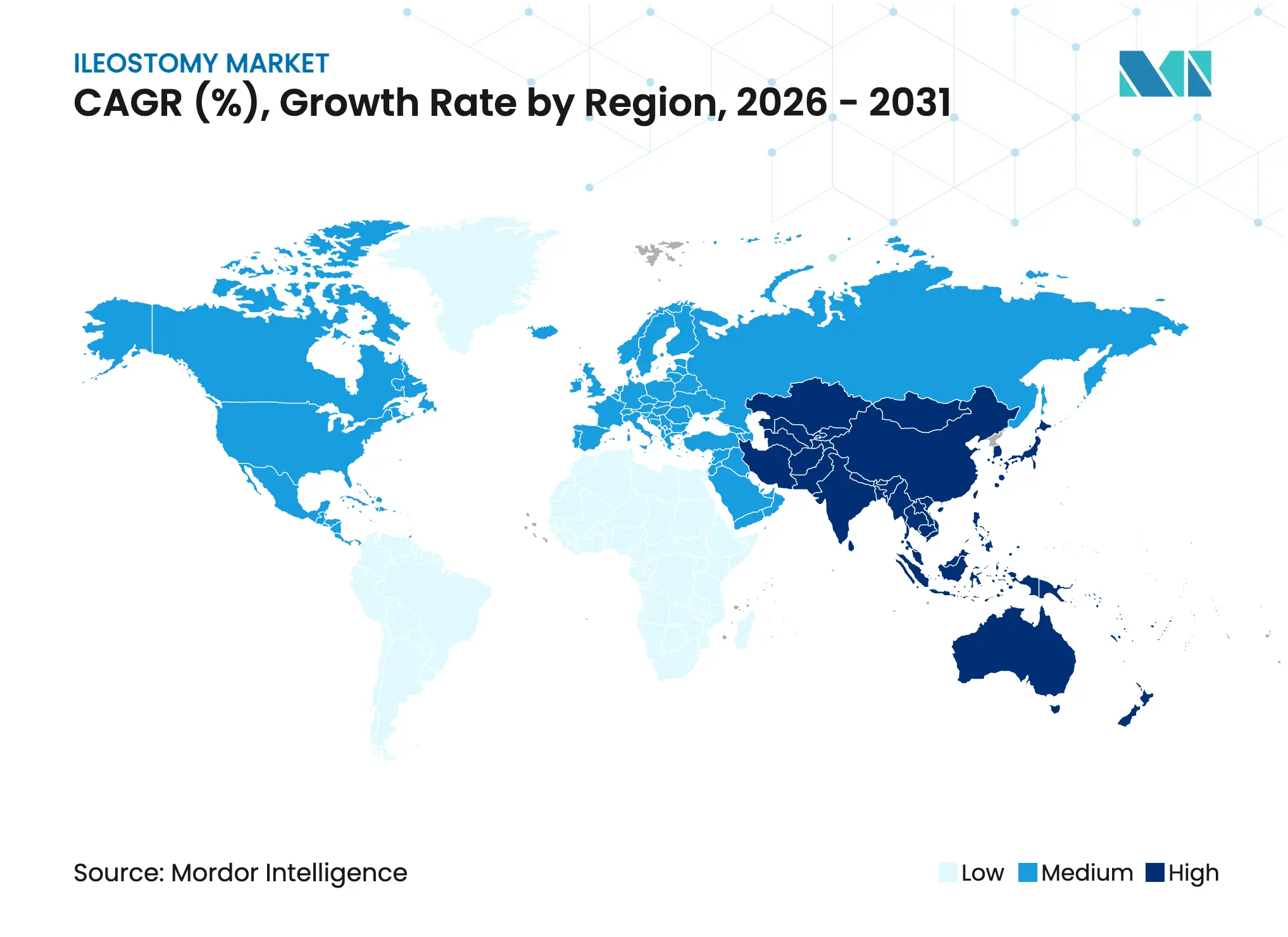

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ileostomy Market Analysis by Mordor Intelligence

The expansion stems from three converging forces: an ageing population with higher inflammatory bowel disease (IBD) incidence, steady colorectal-cancer surgery volumes, and rapid product innovation in two-piece drainable systems. North America remains the largest regional contributor, while Asia-Pacific registers the quickest uptake thanks to hospital-capacity upgrades and growing life expectancy. Procedure patterns are also evolving; surgeons now favour temporary loop ileostomies for bowel preservation, yet permanent end procedures still dominate volumes. Competitive intensity is moderate as leading firms differentiate through digital leakage alerts, mouldable skin barriers, and service-backed care ecosystems.

Key Report Takeaways

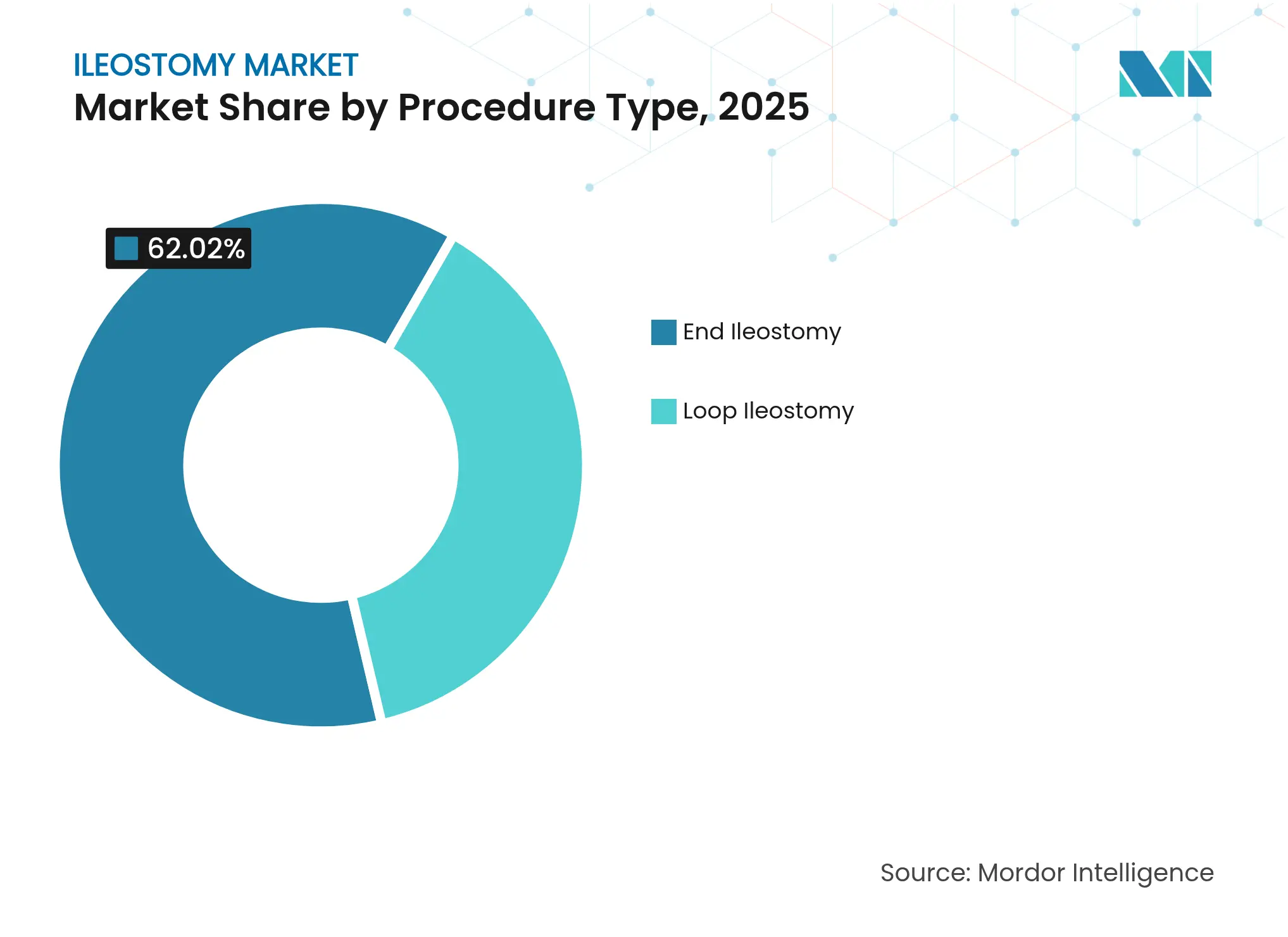

- By procedure type, end ileostomy led with 62.02% of ileostomy market share in 2025, whereas loop ileostomy is forecast to post a 7.55% CAGR through 2031.

- By system type, two-piece products captured 57.68% of the ileostomy market in 2025; one-piece solutions are projected to expand at 7.78% CAGR to 2031.

- By equipment, stoma bags accounted for 75.62% of the ileostomy market size in 2025; accessories and others segment is set to grow at 7.84% CAGR during 2026-2031.

- By disease, cancer contributed 42.55% revenue share in 2025, while Crohn’s disease is advancing at 8.42% CAGR to 2031.

- By end user, hospitals held 50.88% share of the ileostomy market size in 2025, and home care is projected to rise at 8.06% CAGR over the forecast period.

- By geography, North America commanded 42.97% share of the ileostomy market in 2025; Asia-Pacific is the fastest-growing region at 8.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ileostomy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

prevalence of inflammatory bowel disease (IBD)

Rising

prevalence of inflammatory bowel disease (IBD)

| +1.8% | North America & Europe highest, global spread to Asia & Latin America | Long term (≥ 4 years) |

(~)

% Impact on CAGR Forecast

:

+1.8%

|

Geographic

Relevance

:

North

America & Europe highest, global spread to Asia & Latin America

|

Impact

Timeline

:

Long

term (≥ 4 years)

|

Growing

colorectal-cancer surgical incidence

Growing

colorectal-cancer surgical incidence

| +1.5% | Global, with accelerating volumes in Asia-Pacific | Medium term (2-4 years) | |||

Ageing

population & chronic disease burden

Ageing

population & chronic disease burden

| +1.2% | Core impact in Asia-Pacific, spill-over to North America & Europe | Long term (≥ 4 years) | |||

Advances

in two-piece drainable bags

Advances

in two-piece drainable bags

| +0.9% | Early adoption in developed markets, expanding worldwide | Short term (≤ 2 years) | |||

Emergence

of digital stoma-monitoring wearables

Emergence

of digital stoma-monitoring wearables

| +0.6% | North America & EU first, rolling out to Asia-Pacific | Medium term (2-4 years) | |||

Adoption

of 3-D printed custom-fit skin barriers

Adoption

of 3-D printed custom-fit skin barriers

| +0.4% | Pilot programmes in North America & EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of IBD

Age-standardized IBD incidence climbed from 4.22 to 4.45 per 100,000 between 1990 and 2022. Elderly cohorts show the sharpest rise, with women aged 60-89 exhibiting the greatest case growth. Newly industrialised nations in Asia, Africa, and Latin America are entering an acceleration phase, signalling sustained global demand for advanced stoma solutions. As medical therapy fails for complex cases, permanent or temporary ileostomies become essential, boosting premium product uptake that preserves peristomal skin integrity while accommodating multiple comorbidities.

Growing Colorectal-Cancer Surgical Incidence

Colorectal cancer constitutes 38.5% of the lifetime risk for gastrointestinal tumours worldwide [1]Jean-Nicolas Vauthey et al., “Lifetime GI-Cancer Risk Analysis,” thelancet.com. Early-onset cases are advancing fastest, compelling surgeons to perform protective diverting ileostomies in younger, active patients who prioritise discreet appliances. Colon cancer rates among Asian Americans rose from 155 to 755 per 100,000 between 2017 and 2022, underscoring the shift toward high-quality, lifestyle-compatible systems. Demand centres on devices that simplify short-term use and safeguard skin for planned reversals.

Ageing Population & Chronic Disease Burden

Adults aged over 45 face a mounting hernia and bowel-surgery burden that often culminates in ostomy formation [2]BMC Gastroenterology, “Hernia Disease Projection,” bmcgastroenterol.biomedcentral.com. China illustrates the economic scale: per-capita health outlays are expected to climb to USD 30,800 by 2060 under current demography. Older users need easy-to-handle barriers and caregiver-friendly closures, prompting manufacturers to refine ergonomic flanges, colour-coded coupling, and belt-integrated support for limited dexterity.

Advances in Two-Piece Drainable Bags

ConvaTec’s mouldable technology maintained healthy peristomal skin in 95% of users and improved dermatitis scores in 86% of switchers. Surveys reveal over 90% of wearers find mouldable two-piece appliances faster and less stressful than cut-to-fit types. Randomised data show belts raise overall life satisfaction and body image after eight weeks of use. These gains spur premium demand in developed markets and reinforce two-piece leadership within the ileostomy market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shift

toward minimally-invasive bowel-sparing procedures

Shift

toward minimally-invasive bowel-sparing procedures

| -0.8% | Greatest effect in developed markets | Medium term (2-4 years) |

(~)

% Impact on CAGR Forecast

:

-0.8%

|

Geographic

Relevance

:

Greatest

effect in developed markets

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Cost

& reimbursement gaps in developing economies

Cost

& reimbursement gaps in developing economies

| -0.6% | Asia-Pacific, Middle East & Africa, Latin America | Short term (≤ 2 years) | |||

Supply-chain

vulnerability of hydrocolloid adhesives

Supply-chain

vulnerability of hydrocolloid adhesives

| -0.4% | Global, regional variability | Short term (≤ 2 years) | |||

Waste-disposal

regulations for single-use ostomy products

Waste-disposal

regulations for single-use ostomy products

| -0.3% | EU & North America first, extending globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Shift Toward Minimally-Invasive Bowel-Sparing Procedures

Robotic colorectal surgeries now report fewer complications and shorter stays versus open approaches. US data show robotic use rising in stoma reversals, indicating surgeon preference for direct anastomosis when technology reduces risk. Professional guidelines confirm laparoscopic and robotic methods lessen pain and length of stay while maintaining oncologic safety. As proficiency spreads, fewer patients require protective ileostomies, tempering demand in advanced health systems.

Cost & Reimbursement Gaps in Developing Economies

Surveys in Malawi, Nigeria, India, and the Philippines document limited access to affordable stoma supplies and counselling. Out-of-pocket purchasing, inconsistent insurance, and sparse rural distribution restrict premium uptake, urging suppliers to launch low-cost lines with simpler adhesives. These constraints widen the quality divide between high-income and price-sensitive segments in the ileostomy market.

Segment Analysis

By Procedure Type – End Procedures Dominate but Loop Demand Accelerates

End ileostomy accounted for 62.02% of 2025 revenue, anchoring the ileostomy market with long-term users whose appliance lifespan can exceed a decade. Post-operative complexity and higher stoma output push hospitals to select durable two-piece barriers with reinforced hydrocolloid bases. The competing loop segment, though smaller, posts a 7.55% CAGR as surgeons increasingly construct temporary diversions for low-anterior resections. Quality-improvement projects prove that timely reversal trims 30-day readmissions from 20.10% to 8.75%. Manufacturers therefore design lightweight, skin-gentle systems that simplify changes during the short active period.

The loop surge expands the ileostomy market by recruiting younger patients who value ease of removal before re-anastomosis. Educational apps guide them through emptying schedules, output tracking, and early warning signs. Combined with nurse-led tele-follow-ups, these tools cut emergency visits and reinforce brand loyalty. Consequently, procedure-specific kits with pre-cut sizing and colour-coded panels are gaining traction among colorectal centres.

Note: Segment shares of all individual segments available upon report purchase

By Equipment Type – Stoma Bags Retain Core Value While Accessories Flourish

Stoma bags represented 75.62% of 2025 revenue, confirming their central role in the ileostomy market. High demand persists for drainable pouches with integrated filter membranes that mitigate ballooning and odour. Yet accessories and others segment races ahead at 7.84% CAGR, propelled by barrier wipes, adjustable belts, and deodorising gels. Clinicians now deploy malodour-reducing additives that lower odour intensity scores and enhance social confidence.

Risk-stratified protocols limit peristomal skin complications to 6.2% by 90 days when advanced barrier rings and convex cushions are combined with structured teaching. This evidence encourages suppliers to bundle pouches with accessory starter packs, embedding long-term usage habits and elevating average selling price. The growing accessory mix further diversifies revenue streams within the ileostomy market.

By Disease Type – Cancer Still Leads as IBD Drives Future Growth

Cancer surgeries captured 42.55% of 2025 sales, anchoring the ileostomy market in oncology wards. Nonetheless, Crohn’s disease delivers the steepest 8.42% CAGR as chronic relapses mandate repeat surgeries and possible permanent diversion. Fecal calprotectin measurement from stoma effluent offers a non-invasive biomarker for flare monitoring. Product designers now integrate sampling ports that allow clinicians to collect effluent without detaching pouches, easing disease surveillance.

Regional epidemiology reinforces the trend. India is projected to witness disproportionate IBD prevalence growth by 2050. Consequently, suppliers are tailoring high-output pouches with extended-wear taps that connect to bedside collectors, addressing unpredictable drainage patterns typical of severe Crohn’s. These disease-specific advances preserve momentum in the ileostomy market

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By System Type – Two-Piece Flexibility Versus One-Piece Simplicity

Two-piece systems owned 57.68% of 2025 revenue, reflecting user preference for changing bags without disturbing the skin barrier, an essential feature in high-output scenarios. Improved coupling clicks and tactile feedback reassure visually impaired or elderly wearers. Conversely, the one-piece category logs a 7.78% CAGR as adhesive science and flexible wafers reduce leakage anxiety. Surveys confirm mouldable one-piece products now rival two-piece for wear-time while simplifying morning routines.

Continuous product education underpins better outcomes; an AAH white paper links correct system choice with up to 40% fewer peristomal complications. As differentiation narrows, firms add QR-code videos and multilingual guides to drive proper fitting. Both system types thus sustain parallel growth corridors, expanding the overall ileostomy market size for system innovators.

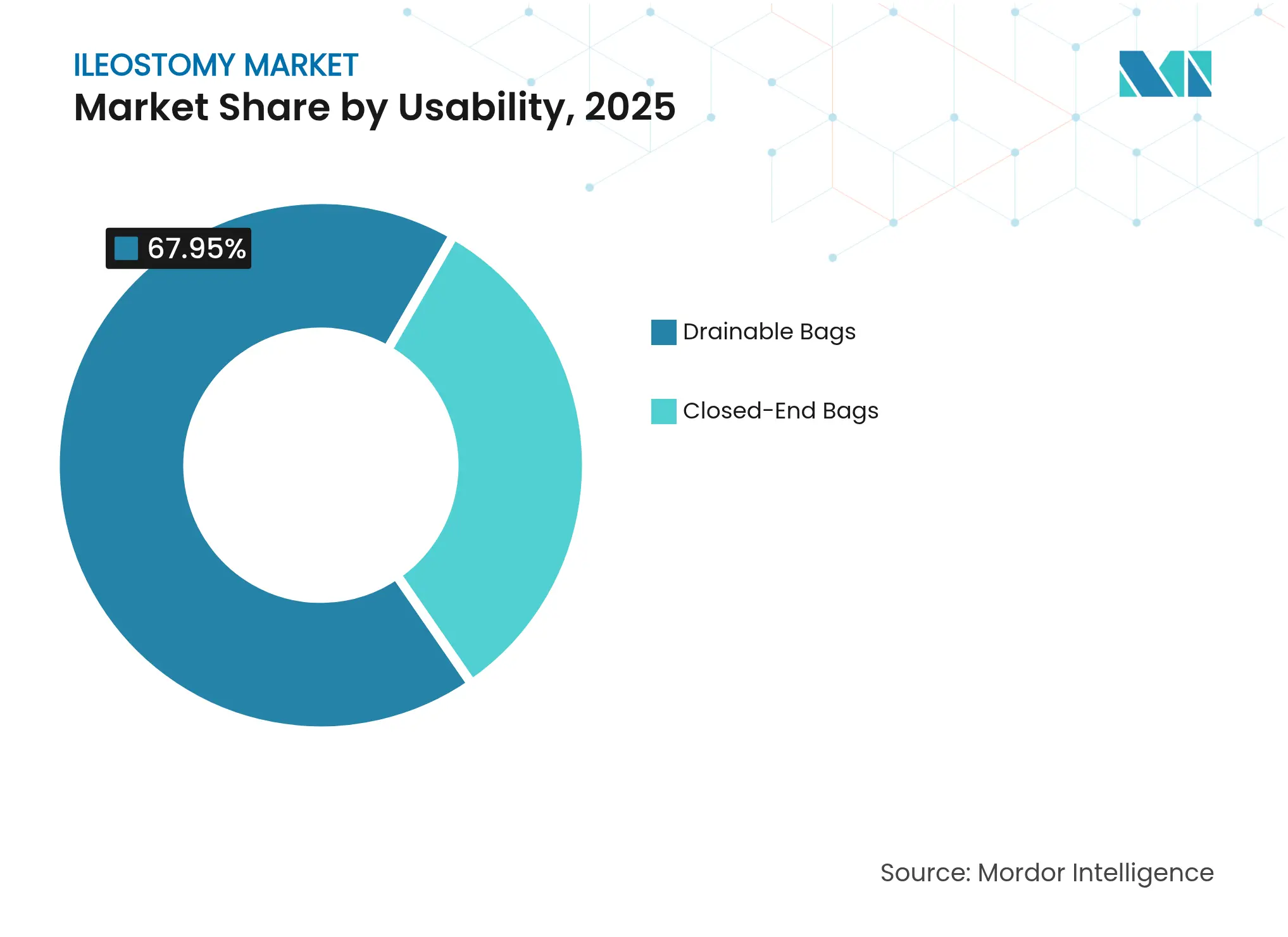

By Usability – Drainable Bags Prevail yet Closed-End Niches Rise

Drainable options dominated 67.95% of 2025 expenditure, meeting the clinical reality of liquid output. Soft-tap extensions now attach directly to bed-side containers, reducing nocturnal emptying for hospitalised patients and freeing nursing time. Closed-end bags, though smaller, rise at 7.95% CAGR, serving travel, sports, and intimate-activity niches where single-use discretion outweighs cost.

Selective continence devices such as internal plugs yield 67.4% continence and 74.9% quality-of-life gains. Producers therefore invest in hybrid bags that toggle between drainable and closed-end modes, merging convenience with environmental waste reduction goals. This dual-design trend underlines how usability features fuel continuous differentiation within the ileostomy market.

Note: Segment shares of all individual segments available upon report purchase

By End User – Care Shifts from Inpatient to Home

Hospitals held 50.88% revenue share in 2025, but policymakers worldwide now promote same-day colorectal surgery and tele-follow-up, favouring home-based recovery. The home-care channel hence climbs at 8.06% CAGR as families assume daily stoma management. Early rehabilitation programmes help 72% of working-age patients return to employment within six months when supported by interdisciplinary teams.

App-linked reorder reminders and subscription deliveries reduce supply lapses, further entrenching home care growth. Ambulatory surgical centres, with lean cost structures, expand ostomy volume too, especially for elective loop closures. Collectively, shifting sites of service recalibrate demand patterns, stimulating fresh go-to-market models in the ileostomy industry.

Geography Analysis

North America generated 42.97% of 2025 revenue, cementing its leadership through specialist nursing density, widespread insurance coverage, and rapid adoption of digital leakage monitors. FDA alignment with ISO 13485 in 2025 ensures smoother premarket submissions, fostering swift technological upgrades. Despite laparoscopic uptake tempering new stoma creation, premium upselling offsets volume softness, keeping the ileostomy market size resilient.

Asia-Pacific remains the quickest climber with an 8.29% CAGR to 2031. Urban hospitals in China and India now stock convex-fit barriers and adjustable belts, reflecting higher disposable incomes. China’s health-spend trajectory towards USD 33.4 trillion by 2060 reinforces structural demand for chronic-care devices. Emerging reimbursement pilots in Thailand and Indonesia further unlock access, although rural distribution gaps persist.

Europe presents a mature yet innovation-minded landscape. The EU Packaging and Packaging Waste Regulation forces all medical packaging to be recyclable by 2030. Producers have responded with thinner, mono-material pouches that sustain barrier properties while cutting plastic weight. Simultaneously, single-use-device reprocessing rules guide safe recycling of support belts and closure clips. These regulatory nudges drive sustainable product redesign within the ileostomy market.

Competitive Landscape

Market Concentration

Coloplast, ConvaTec, and Hollister collectively anchor the competitive field, each backing flagship launches with educational platforms. Coloplast advanced digital sensing through Heylo, offering real-time leakage alerts via smartphones. Hollister reinforced high-output management with integrated soft-tap pouches for critical-care settings.

Mid-tier firms B. Braun and 3M sharpen differentiation on region-specific lines such as Flexima Active for Asian users needing slimmer profiles. The FDA’s predetermined change-control plans enacted in 2024 streamline iterative upgrades, incentivising rapid material tweaks without fresh regulatory dossiers [3]Federal Register, “FDA Quality System Regulation Amendments,” federalregister.gov. Competitive focus has therefore shifted from price to lifetime episode cost, with vendors bundling tele-nurse support, skin-monitoring apps, and replenishment logistics into subscription models.

White-space opportunities persist in paediatric stomas, personalised 3-D printed barriers, and AI-powered wearables predicting effluent pH shifts before leakage. Start-ups collaborating with university additive-manufacturing labs can now prototype customised flanges within 24 hours, trimming fitting appointments and hospital revisits. As digital ecosystems mature, future winners in the ileostomy market will likely marry physical devices with data-driven service layers that guarantee outcome-based contracting to payers.

Ileostomy Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ForLife Produktions- und Vertriebsgesellschaft für Heil- und Hilfsmittel mbH and Oakmed Ltd. have officially come together under a new name — Unora. As part of this transformation, Unora introduced Silkura, a silicone-based ostomy pouch designed to make life easier.

- November 2025: Mather Hospital, part of Northwell Health in Port Jefferson, achieved a major milestone by performing New York State's first magnetic duodenal ileostomy (MagDI) procedure.

Table of Contents for Ileostomy Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence of Inflammatory Bowel Disease (IBD)

- 4.2.2Growing Colorectal Cancer Surgical Incidence

- 4.2.3Ageing Population & Chronic Disease Burden

- 4.2.4Advances in Two-Piece Drainable Bags

- 4.2.5Emergence of Digital Stoma-Monitoring Wearables

- 4.2.6Adoption of 3-D Printed Custom-Fit Skin Barriers

- 4.3Market Restraints

- 4.3.1Shift Toward Minimally Invasive Bowel-Sparing Procedures

- 4.3.2Cost & Reimbursement Gaps in Developing Economies

- 4.3.3Supply-Chain Vulnerability of Hydrocolloid Adhesives

- 4.3.4Waste-Disposal Regulations for Single-Use Ostomy Products

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts

- 5.1By Procedure Type

- 5.1.1End Ileostomy

- 5.1.2Loop Ileostomy

- 5.2By Equipment Type

- 5.2.1Stoma Bags

- 5.2.2Belts & Girdles

- 5.2.3Accessories & Others

- 5.3By Disease Type

- 5.3.1Cancer

- 5.3.2Crohn’s Disease

- 5.3.3Ulcerative Colitis

- 5.3.4Other Indications

- 5.4By System Type

- 5.4.1One-Piece Systems

- 5.4.2Two-Piece Systems

- 5.5By Usability

- 5.5.1Drainable Bags

- 5.5.2Closed-End Bags

- 5.6By End User

- 5.6.1Hospitals

- 5.6.2Home-care Settings

- 5.6.3Ambulatory Surgical Centers

- 5.7By Geography

- 5.7.1North America

- 5.7.1.1United States

- 5.7.1.2Canada

- 5.7.1.3Mexico

- 5.7.2Europe

- 5.7.2.1Germany

- 5.7.2.2United Kingdom

- 5.7.2.3France

- 5.7.2.4Italy

- 5.7.2.5Spain

- 5.7.2.6Rest of Europe

- 5.7.3Asia-Pacific

- 5.7.3.1China

- 5.7.3.2Japan

- 5.7.3.3India

- 5.7.3.4Australia

- 5.7.3.5South Korea

- 5.7.3.6Rest of Asia-Pacific

- 5.7.4Middle East and Africa

- 5.7.4.1GCC

- 5.7.4.2South Africa

- 5.7.4.3Rest of Middle East and Africa

- 5.7.5South America

- 5.7.5.1Brazil

- 5.7.5.2Argentina

- 5.7.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Coloplast A/S

- 6.3.2ConvaTec Group Plc

- 6.3.3Hollister Incorporated

- 6.3.4B. Braun Melsungen AG

- 6.3.53M Healthcare

- 6.3.6Salts Healthcare Ltd

- 6.3.7Flexicare Medical Ltd

- 6.3.8Marlen Manufacturing & Development

- 6.3.9Smith & Nephew Plc

- 6.3.10Welland Medical Ltd

- 6.3.11Nu-Hope Laboratories Inc.

- 6.3.12Cymed Micro Skin

- 6.3.13ALCARE Co., Ltd.

- 6.3.14Medline Industries LP

- 6.3.15Torbot Group Inc.

- 6.3.16Trio Healthcare

- 6.3.17Safe N Simple LLC

- 6.3.18Fittleworth Medical Ltd

- 6.3.19SecuriCare (Medical) Ltd

- 6.3.20Stomocare International

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ileostomy market as the global sales of single-use or reusable collected-waste systems, bags, skin barriers, belts, pastes, and ancillary accessories used after surgically bringing the ileum to the abdominal surface, whether the stoma is temporary or permanent.

Scope exclusion: Devices meant strictly for colostomy or urostomy procedures are outside our baseline.

Segmentation Overview

- By Procedure Type

- End Ileostomy

- Loop Ileostomy

- End Ileostomy

- By Equipment Type

- Stoma Bags

- Belts & Girdles

- Accessories & Others

- Stoma Bags

- By Disease Type

- Cancer

- Crohn’s Disease

- Ulcerative Colitis

- Other Indications

- Cancer

- By System Type

- One-Piece Systems

- Two-Piece Systems

- One-Piece Systems

- By Usability

- Drainable Bags

- Closed-End Bags

- Drainable Bags

- By End User

- Hospitals

- Home-care Settings

- Ambulatory Surgical Centers

- Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next interview colorectal surgeons, stoma nurses, procurement heads at hospitals, and home-care distributors across North America, Europe, Asia-Pacific, and the GCC to sense-check adoption curves, average selling prices (ASP), and accessory attachment rates, and to validate early desk assumptions that seemed volatile.

Desk Research

We start by mapping patient pools and surgery volumes from open datasets such as GLOBOCAN cancer registries, WHO IBD prevalence files, OECD hospital-discharge statistics, and U.S. Medicare HCPCS reimbursement logs. We then layer insights from national ostomy associations and peer-reviewed journals on stoma care. Company 10-Ks, FDA 510(k) summaries, and Dow Jones Factiva news help us refine launch timelines and price corridors. D&B Hoovers provides revenue splits that anchor vendor roll-ups. This list is illustrative; many more public and subscription sources underpin the desk phase.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort model converts incident colorectal-cancer and severe IBD cases into ileostomy procedures, adjusts for reversal rates and mortality, and multiplies by device usage norms. Supplier roll-ups and sampled ASP × volume checks provide a bottom-up lens for reconciliation before the totals are finalized. Key drivers baked into the model include: 1) elective colorectal-surgery backlog clearance, 2) shift toward two-piece drainable systems, 3) home-care penetration, 4) regional ASP erosion, and 5) aging population elasticity. A multivariate regression on these variables, inflation-adjusted, generates the 2025-2030 curve, with scenario analysis used to stress adverse reimbursement shocks. Gap pockets in bottom-up estimates are bridged through regional weighting based on import shipment data.

Data Validation & Update Cycle

Outputs undergo three-stage peer review, variance flags trigger secondary calls, and any material regulatory or recall event prompts an interim refresh. Reports are rebuilt annually, and we perform a last-minute sweep before client delivery.

Why Mordor's Ileostomy Baseline Earns Decision-Maker Confidence

Benchmark comparison

Published estimates diverge because firms vary stoma-type scope, bundle accessories differently, and apply unlike ASP progressions.

Key gap drivers include: some sources merge colostomy with ileostomy revenues, others apply uniform global prices, or use historic procedure rates without discounting reversals. Our analysts, by contrast, isolate ileostomy-only devices, apply region-specific ASP ladders validated each quarter, and refresh patient pools annually.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.31 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.20 B (2024) | Global Consultancy A | Merges ostomy sub-types; static ASP; two-year refresh cycle | ||

USD 2.05 B (2025) | Industry Association B | Counts accessories sold for colostomy; assumes uniform device replacement interval |