Surgical Dressing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

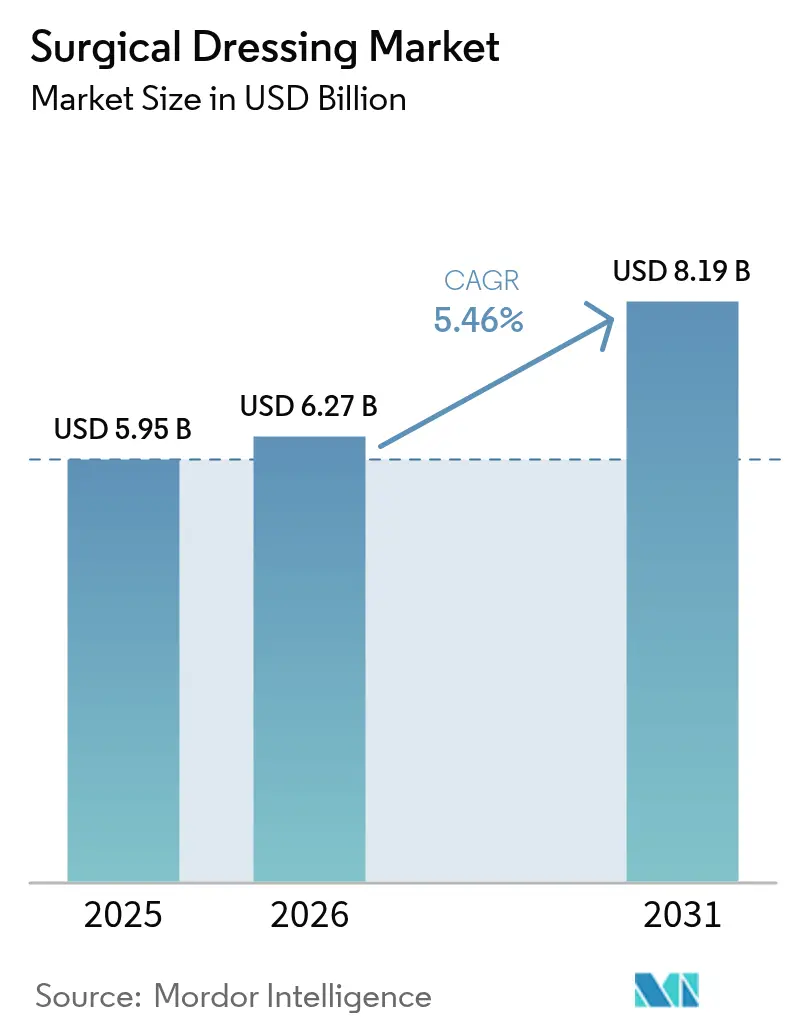

| Market Size (2026) | USD 6.27 Billion |

| Market Size (2031) | USD 8.19 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Dressing Market Analysis by Mordor Intelligence

The surgical dressings market size is expected to grow from USD 5.95 billion in 2025 to USD 6.27 billion in 2026 and is forecast to reach USD 8.19 billion by 2031 at 5.46% CAGR over 2026-2031. Demand growth rests on three pillars: the accelerating incidence of chronic wounds among older adults, the migration of procedures to outpatient settings, and steady innovation in smart, antimicrobial, and bio-active dressings. Real-time sensor integration, such as Caltech’s iCares bandage that measures biomarkers in exudate, signals a shift from passive coverage to active therapy. Regulatory reforms in China, India, and the United States lower adoption barriers for premium products, while payer policies that now reimburse skin-substitute dressings broaden market access. Supply chain risks in specialty polymers and possible FDA reclassification of antimicrobial dressings temper optimism, yet the underlying demographic and clinical need continues to anchor the surgical dressings market trajectory.

Key Report Takeaways

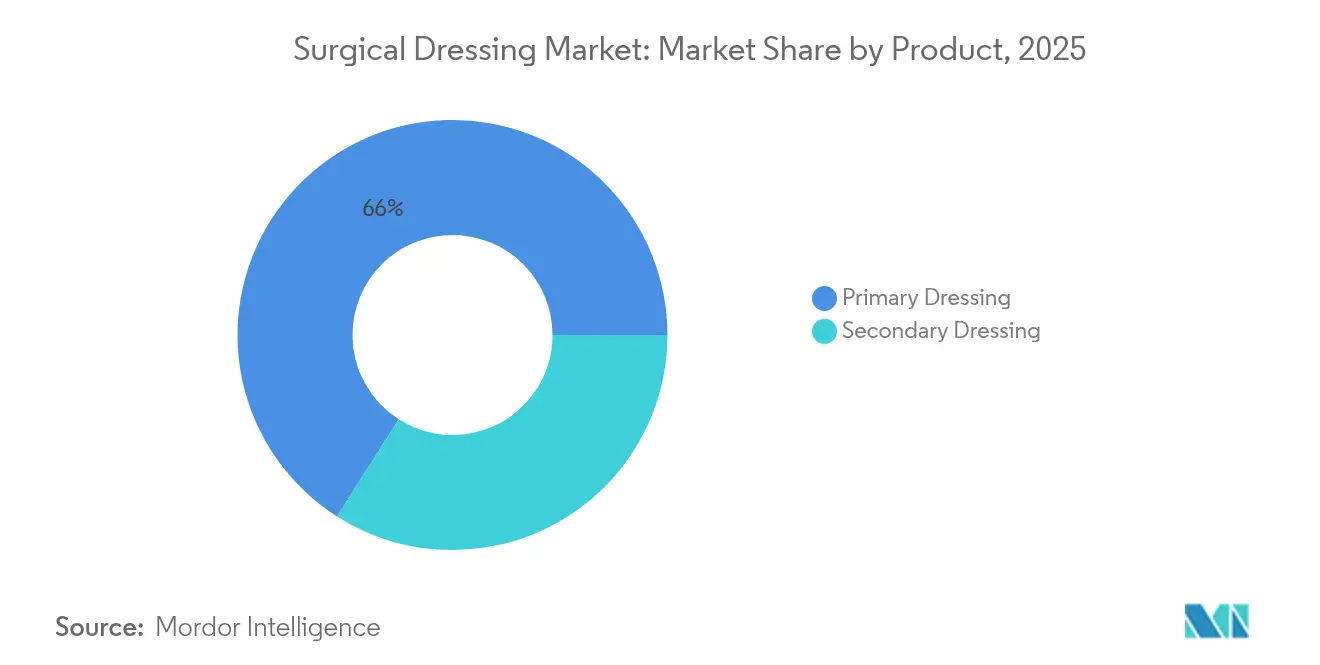

- By application, ulcer treatment accounted for 31.02% of the surgical dressings market size in 2025 and diabetes-related surgery is advancing at a 5.79% CAGR through 2031.

- By end-user, hospitals and clinics held 53.88% of the surgical dressings market share in 2025, whereas ambulatory surgical centers record the highest projected CAGR at 5.92% to 2031.

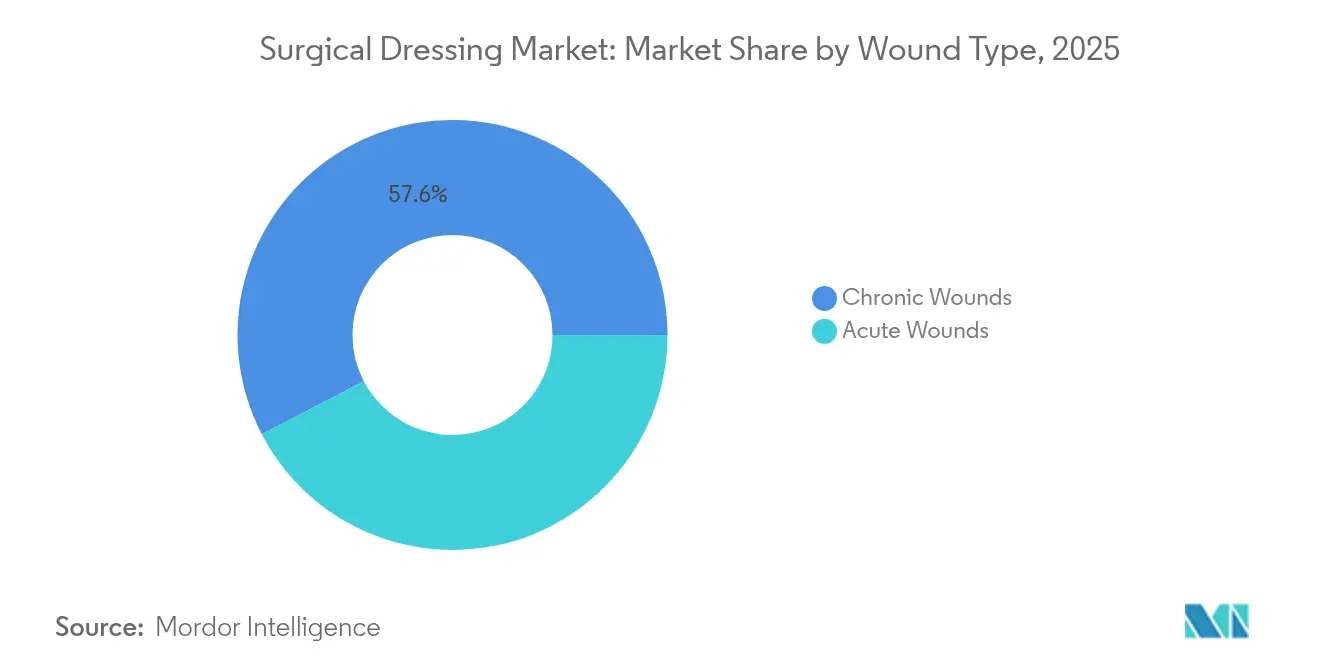

- By wound type, chronic wounds captured 57.63% share of the surgical dressings market size in 2025 and acute wounds are growing at a 6.12% CAGR through 2031.

- By material, synthetic polymers retained 38.41% share in 2025, while bio-engineered composites are forecast to grow at 6.55% CAGR to 2031.

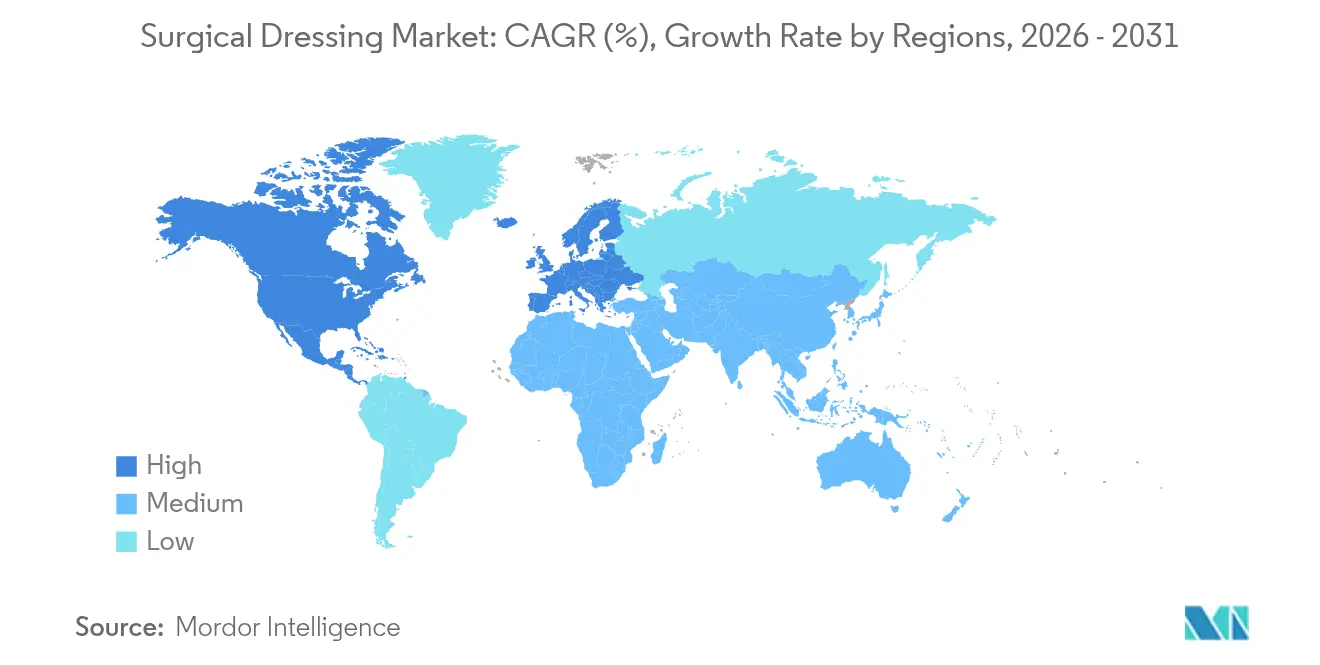

- By geography, North America commanded 41.72% share of the surgical dressings market in 2025; Asia-Pacific is the fastest-growing region, expanding at 6.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Dressing Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rise in chronic wounds | +1.8% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Shift toward outpatient and home-based care | +1.2% | North America & EU, spreading to APAC | Medium term (2-4 years) |

| Product innovation in antimicrobial and bio-active dressings | +1.0% | Global, led by North America & Europe | Medium term (2-4 years) |

| Reimbursement expansion for advanced dressings | +0.8% | North America & EU | Short term (≤ 2 years) |

| Growth of surgical volumes in emerging Asia | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Integration of smart or IoT sensors in dressings | +0.4% | North America & EU, early APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Rise in Chronic Wounds

Chronic wounds already affect more than 40 million people worldwide and cost the United States healthcare system over USD 28 billion each year [1]Gwendolen Carberry, “Chronic Wound Care Burden and Cost in the United States,” Frontiers in Bioengineering and Biotechnology, frontiersin.org. Diabetes and peripheral arterial disease elevate ulcer risk, prompting the International Working Group on the Diabetic Foot to recommend sucrose octasulfate dressings for non-healing ulcers [2]Eelco M. W. van Gelder, “Sucrose Octasulfate Dressings for Diabetic Foot Ulcers,” Journal of Wound Care, onlinelibrary.wiley.com. Medicare reports that 10.5% of beneficiaries present with chronic wounds but generate outsized resource use, so payers welcome therapies that shorten healing time. Meta-analyses show advanced dressings can accelerate closure by an average of 1.09 days and lower pain scores versus traditional gauze. This demographic driver supports steady, recession-resistant demand across advanced and standard products in the surgical dressings market.

Shift Toward Outpatient & Home-Based Care

Procedure migration to ambulatory sites raises need for dressings that stay in place longer and simplify self-care. Remote monitoring platforms such as WoundConnect help clinicians oversee healing progress without daily visits, reducing hospital utilization by up to 15%. New CMS codes (G0541, G0542) pay for caregiver wound-care training delivered via telehealth, incentivizing home-based management. Solventum’s V.A.C. Peel & Place dressing, designed for seven-day wear and two-minute application, typifies products tailored to the outpatient shift. These factors collectively lift demand across the surgical dressings market for extended-wear, low-skill solutions.

Product Innovations in Antimicrobial & Bio-Active Dressings

Composite materials that combine antimicrobial action with bio-active healing stimulate premium adoption. Bacterial cellulose loaded with cerium-dioxide nanoparticles blocks both E. coli and B. subtilis while releasing drugs in a controlled profile. The FDA approval of NexoBrid for enzymatic burn debridement after a prolonged review validates appetite for specialized therapies. Trials indicate alginate dressings shorten healing by more than one day on average and reduce pain significantly. Research into artificial spider-silk scaffolds produced via engineered microbes shows faster wound closure in diabetic models and points to a new generation of sustainable biomaterials.

Reimbursement Expansion for Advanced Dressings (US, EU)

Regulators now treat cellular and tissue-based products as wound management tools rather than skin substitutes, bringing them under the physician fee schedule and adding clarity to payment pathways. Local Coverage Determinations allow up to four applications per ulcer within 12 weeks if the wound contracts at least 50% in the first month of treatment. In Europe, the Medical Device Regulation harmonizes evidence requirements while granting transition time for legacy devices to December 2027, rewarding firms with robust clinical dossiers. Clearer reimbursement encourages hospitals to adopt premium dressings that promise lower overall cost of care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-jurisdiction regulatory pathways | −0.9% | Global, pronounced in EU & APAC | Medium term (2-4 years) |

| Price erosion from tender-driven procurement | −0.7% | Global, acute in Europe & emerging markets | Short term (≤ 2 years) |

| Supply-chain volatility in specialty polymers | −0.5% | Global, concentrated in APAC sourcing | Short term (≤ 2 years) |

| Clinical evidence gaps for smart dressings | −0.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdiction Regulatory Pathways

The EU Medical Device Regulation now demands comprehensive clinical evaluation and post-market surveillance, adding 12-18 months and significant expense to approval timelines. The FDA is consulting on reclassifying antimicrobial dressings from Class I to Class II or III, which could shift many legacy products into a stricter pre-market review. Japan continues to post the longest med-tech approval lag among G7 countries, averaging 24-36 months according to its Pharmaceuticals and Medical Devices Agency. Smart dressings that incorporate software draw additional cybersecurity scrutiny, challenging smaller firms. These hurdles slow roll-out of novel technologies within the surgical dressings market.

Price Erosion from Tender-Driven Hospital Procurement

Public hospitals in Europe and parts of Asia award bulk tenders based mainly on price, compressing gross margins for commodity gauze and film products. Company filings show Paul Hartmann’s traditional wound portfolio faced 20-30% price undercutting by private labels in 2024, even as demand stayed strong. Integrated delivery networks in the United States increasingly request risk-share contracts in which suppliers refund part of the product cost if healing targets are missed. Without high-quality health-economic data, many mid-tier suppliers struggle to defend premium pricing, exerting near-term drag on the surgical dressings market growth rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Primary Dressings Lead Innovation

Primary dressings generated 65.98% of surgical dressings market revenue in 2025 due to their central role at the wound bed. Hydrogel and alginate variants maintain an ideal moisture balance, and recent trials show a 1.09-day faster closure versus gauze. Film dressings now house printed pH sensors that flag infection ahead of visible symptoms, giving clinicians an early-warning advantage. Foam dressings with super-absorbent polymers gained share after Paul Hartmann reported EUR 608.9 million in wound revenue on strong silicone-foam uptake. Secondary dressings grow fastest at 5.98% CAGR because layered protocols call for added absorption and securement. Companies refine adhesive borders to reduce skin trauma in frail patients while retaining seal integrity for seven-day wear.

Smart primary dressings capable of Bluetooth connectivity remain a niche, limited by battery life and cost, yet pilot studies in veteran hospitals show high patient satisfaction. Synthetic polymer films still dominate volume but bio-engineered cellulose composites that release antimicrobials on demand capture clinician interest. As value-based contracts reward lower readmissions, purchasers weigh the higher unit price of active dressings against demonstrated reductions in total care costs. Continuous innovation keeps primary dressings at the forefront of the surgical dressings market.

By Application: Diabetes-Related Surgery Drives Growth

Ulcer care contributed 31.02% to the surgical dressings market size in 2025, reflecting the ongoing burden of pressure and venous ulcers among aging populations. Yet diabetes-related surgery represents the fastest-growing use case at 5.79% CAGR. The International Working Group on the Diabetic Foot now endorses sucrose octasulfate dressings when neuro-ischemic ulcers stall after four weeks of standard care. Negative-pressure therapy after cardiovascular procedures further broadens application scope.

Burn treatment remains dependent on silver-impregnated options, but debate over optimal ion release persists. Organ‐transplant recipients demand high-performance dressings that guard against opportunistic infections while promoting granulation. Payers increasingly require photographic proof and digital planimetry to authorize multiple high-cost dressing applications, pushing suppliers to embed image-capture tools within smart products. These evolving needs reinforce growth prospects for specialty segments within the wider surgical dressings market.

By End-User: Ambulatory Centers Accelerate Adoption

Hospitals and clinics accounted for 53.88% of surgical dressings market share in 2025, anchored by complex trauma and surgical workloads. Ambulatory surgical centers, however, are expanding at a 5.92% CAGR as insurers favor same-day procedures. Extended-wear foams that tolerate showering and gentle movement suit outpatient recovery. Telehealth follow-up reduces skilled-nursing visits, and CMS now compensates virtual wound assessments, enhancing center economics .

Home health services employ caregiver education codes to train family members in basic dressing changes, widening adoption of intuitive, color-coded packaging. Long-term care facilities deploy prophylactic sacral dressings for pressure-ulcer prevention, an approach that evidence shows can lower Stage III ulcer incidence by 43%. End-user mix diversification supports balanced expansion across the surgical dressings market.

By Wound Type: Chronic Wounds Command Premium

Chronic wounds captured 57.63% of market revenue in 2025 because of their prolonged care cycles and need for advanced therapy. Smart dressings that track nitric oxide or glucose levels help clinicians detect early deterioration, preventing costly debridement. AI models trained on wound-bed images now predict healing likelihood with 98% accuracy, guiding timely treatment escalation.

Acute wound management is growing at 6.12% CAGR on rising elective surgeries and trauma cases. Evidence from Sub-Saharan Africa shows multimodal bundles that pair modern dressings with antimicrobial stewardship can cut surgical site infection rates by up to 95%. Device makers therefore promote combined toolkits that include pre-op cleansers, intra-op incise drapes, and post-op dressings, strengthening share capture across the surgical dressings market.

By Material: Bio-Engineered Solutions Gain Traction

Synthetic polymers still hold 38.41% revenue share, supported by mature supply chains and consistent properties demanded in high-volume production. However, composite and bio-engineered materials post the highest growth at 6.55% CAGR, driven by sustainability and performance. Bacterial cellulose paired with cerium oxide shows potent antibacterial action without cytotoxicity, while chitosan hydrogels exhibit self-healing behavior that conforms to irregular defects.

Collagen-based scaffolds, such as Integra’s dermal template, now have FDA clearance for diabetic ulcers, marking regulatory acceptance of biologics in mainstream care. Artificial spider silk harvested from engineered microbes delivers high tensile strength and biocompatibility, with early studies showing superior wound closure times in diabetic mice. Continued material science advances will push higher-margin segments of the surgical dressings market toward bio-derived options over the coming decade.

Geography Analysis

North America maintains leadership, holding 41.72% of the surgical dressings market in 2025. Robust reimbursement under Medicare and private payers rewards technologies that shorten healing or reduce clinic visits. The Department of Defense in 2025 awarded Smith+Nephew a USD 75 million contract for negative-pressure systems, signaling government confidence in advanced modalities. Recent CMS policy shifts that classify certain skin substitutes as wound management products simplify billing, fostering faster uptake of premium offerings. FDA fast-track designations for cellular therapies such as Aurase Wound Gel indicate regulatory support for biologic innovation.

Asia-Pacific is the fastest-growing region, expanding at a 6.88% CAGR through 2031. China’s 2024 medical device law tightens quality management while setting accelerated review lanes for urgently needed products via its National Medical Products Administration. India’s voluntary code on medical device promotion encourages ethical marketing and clearer labeling, improving clinician trust. Japan’s USD 40 billion device market grows as its aging population and universal coverage sustain demand, although lengthy approval timelines constrain rapid launches. Australia’s recognition of select overseas approvals speeds registration for dressings that already hold FDA clearance, benefiting exporters.

Europe records steady growth under the Medical Device Regulation despite higher compliance costs. Companies that invested early in clinical data and post-market surveillance now gain a competitive edge. Hartmann reported 4.4% organic wound-care growth in 2024, aided by silicone foam uptake, even as hospital tenders drove pricing pressure. Sustainability goals in Nordic countries have prompted pilots of biodegradable dressings, aligning with circular-economy policies. Post-Brexit, UK manufacturers must file separate CE and UKCA submissions, adding complexity but also stimulating domestic innovation grants. Across all sub-regions, diverse reimbursement schemes require localized economic evidence, compelling suppliers to tailor value dossiers to each payer system.

Competitive Landscape

The surgical dressings market is moderately fragmented. Smith+Nephew plans to invest USD 1.24 billion in wound care between 2025 and 2030, including a new United Kingdom R&D center that will focus on smart dressings and regenerative matrices. The USD 660 million acquisition of Osiris Therapeutics added viable allograft products and underlines an industry trend toward combining biologics with traditional dressings.

3M leverages its polymer science platform to engineer silicone adhesive films that reduce skin stripping in elderly patients, while Mölnlycke expands its Exufiber range with gelling technology that locks in exudate under compression. ConvaTec and Coloplast compete in negative-pressure therapy through portable, single-use pumps aimed at ambulatory patients. Collaboration between academics and industry accelerates innovation: Caltech works with venture partners to move the iCares sensor bandage toward FDA clearance, demonstrating the pull of digital health inside the surgical dressings market.

Supply chain resilience now factors into competitive positioning. Cardinal Health diversified gauze sourcing across two continents after cotton shortages in 2024, and Medline added domestic foam capacity to cut lead times for U.S. hospitals. Firms also pursue environmental, social, and governance goals, with Urgo Medical piloting bio-based polyurethane foams that lower carbon footprint by 38% relative to petrochemical counterparts. As reimbursement ties payment to outcomes, manufacturers race to publish real-world evidence linking their dressings to lower readmissions and total cost of care, a strategy expected to reshape share allocation over the next five years.

Surgical Dressing Industry Leaders

3M

Smith and Nephew

ConvaTec Inc.

Johnson and Johnson

Cardinal Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2023: Real-time pH wound monitoring made possible using a nanocellulose dressing developed at Linköping University in Sweden.

- March 2023: Healthium Medtech launched Theruptor Novo antimicrobial dressings for chronic leg and foot ulcers.

- June 2022: Collagen Matrix obtained FDA 510(k) clearance for a fibrillar collagen wound dressing that absorbs exudate and controls minor bleeding.

- May 2022: Winner Medical introduced a transparent film line and sodium carboxymethyl cellulose (CMC) dressing in France.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical dressing market as all sterile pads, films, foams, alginates, hydrocolloids, hydrogels, and related advanced materials that are placed on surgical or chronic wounds to absorb exudate and support tissue repair. Both disposable and reusable primary and secondary dressings distributed through institutional or retail channels worldwide are captured.

Scope exclusion: drapes, gowns, wound-cleansing fluids, and negative-pressure devices are not covered.

Segmentation Overview

- By Product

- Primary Dressing

- Film Dressing

- Hydrogel Dressing

- Hydrocolloid Dressing

- Foam Dressing

- Alginate Dressing

- Other Primary Dressings

- Secondary Dressing

- Absorbents

- Bandages

- Adhesive Tapes

- Protectives

- Other Secondary Dressings

- Primary Dressing

- By Application

- Ulcers

- Burns

- Organ Transplants

- Cardiovascular Surgery

- Diabetes-Related Surgery

- Other Applications

- By End-User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home-Care & Other End-Users

- By Wound Type

- Acute Wounds

- Chronic Wounds

- By Material

- Natural Fibers

- Synthetic Polymers

- Bio-engineered / Composite

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed wound nurses, OR supply managers, and distributors across North America, Europe, and Asia-Pacific, letting us verify consumption ratios, net pricing ranges, and post-COVID stock rules that public data miss.

Desk Research

We collected baseline volumes and prices from the WHO Global Health Observatory, CMS and Eurostat surgery files, and UN Comtrade customs codes. Peer-reviewed sources such as Advances in Wound Care and EWMA guidelines supplied prevalence and usage norms. Hospital counts and corporate revenues were cross-checked in D&B Hoovers; Dow Jones Factiva tracked recent launches, and Questel patents flagged material innovations that alter mix and value. The sources named are illustrative, and many others informed each data point.

Market-Sizing & Forecasting

We begin with annual surgical case volumes, chronic-wound prevalence, and dressings used per case, then multiply by blended selling prices in a top-down model. Supplier roll-ups and sampled invoices offer bottom-up checks. Variables such as diabetes incidence, outpatient surgery share, polymer cost trends, antimicrobial adoption rate, and reimbursement code changes feed a multivariate regression projecting demand to 2030. Gaps are filled through regional substitution ratios validated in interviews.

Data Validation & Update Cycle

Outputs face variance limits versus historical series and external filings, and any breach triggers a re-run before sign-off. Models refresh yearly, with interim edits when recalls, tariffs, or epidemics materially shift inputs.

Why Our Surgical Dressing Baseline Earns Trust Worldwide

Published estimates vary because studies differ in scope, price basis, and refresh timing, yet decision makers still need one dependable anchor.

Most divergences arise when other analyses drop secondary dressings, apply list instead of transaction prices, or freeze growth on pre-pandemic surgical trends. Mordor Intelligence converts every input to constant-2025 dollars and revisits key drivers each year, narrowing drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.95 B (2025) | Mordor Intelligence | - |

| USD 5.26 B (2024) | Regional Consultancy A | Omits adhesive tapes and home-care sales |

| USD 6.00 B (2022) | Trade Journal B | Bundles drapes and wound cleansers, older price base |

The comparison shows that our disciplined scope choices and living refresh cycle give clients a transparent, balanced baseline they can trace back to clearly defined drivers.

Key Questions Answered in the Report

What is the current Surgical Dressing Market size?

The market stands at USD 6.27 billion in 2026 and is projected to reach USD 8.19 billion by 2031.

Who are the key players in Surgical Dressing Market?

3M, Smith and Nephew, ConvaTec Inc., Johnson and Johnson and Cardinal Health, Inc. are the major companies operating in the Surgical Dressing Market.

Which is the fastest growing region in Surgical Dressing Market?

Asia-Pacific is advancing at a 6.88% CAGR through 2031, outpacing all other regions.

Which region has the biggest share in Surgical Dressing Market?

In 2025, the North America accounts for the largest market share in Surgical Dressing Market.

Which segment holds the largest surgical dressings market share?

Primary dressings lead, generating 65.98% of 2025 revenue.

Page last updated on: