Emergency Medical Services Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

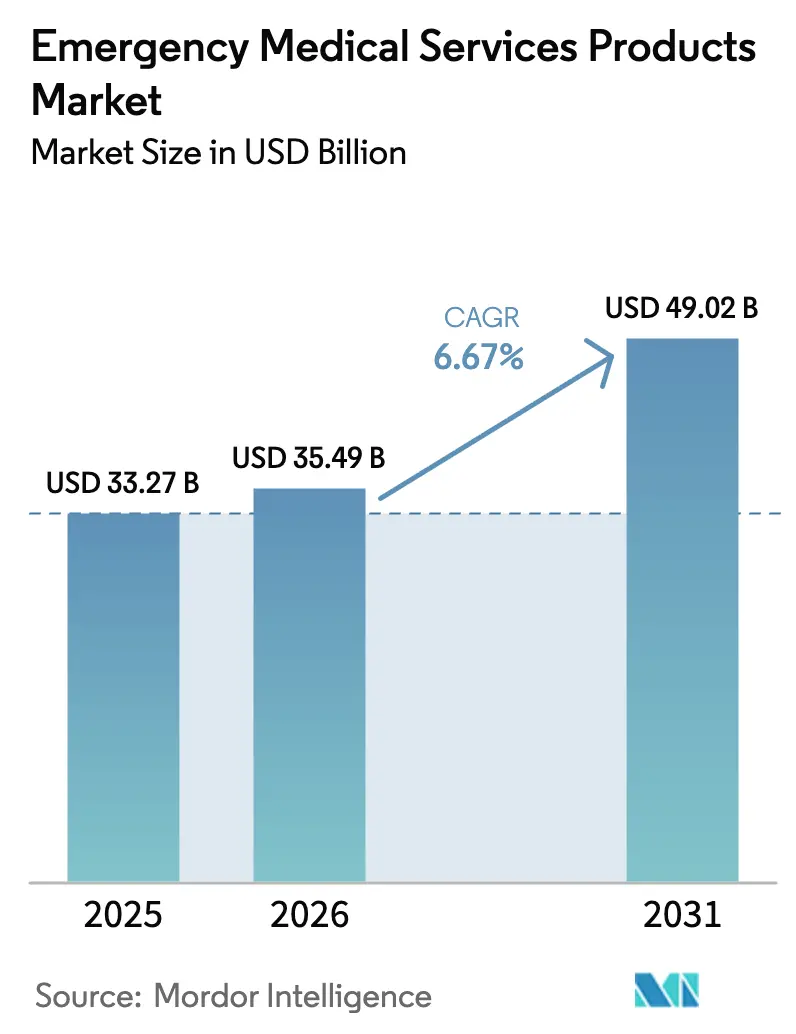

| Market Size (2026) | USD 35.49 Billion |

| Market Size (2031) | USD 49.02 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

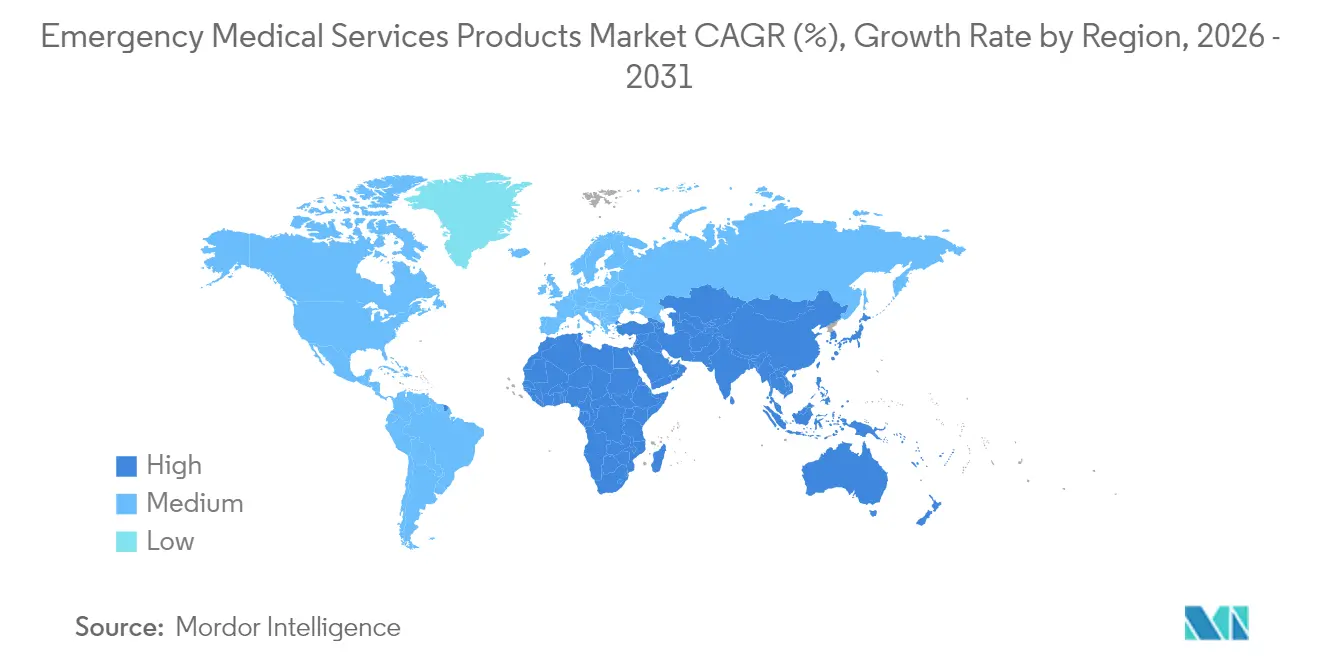

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

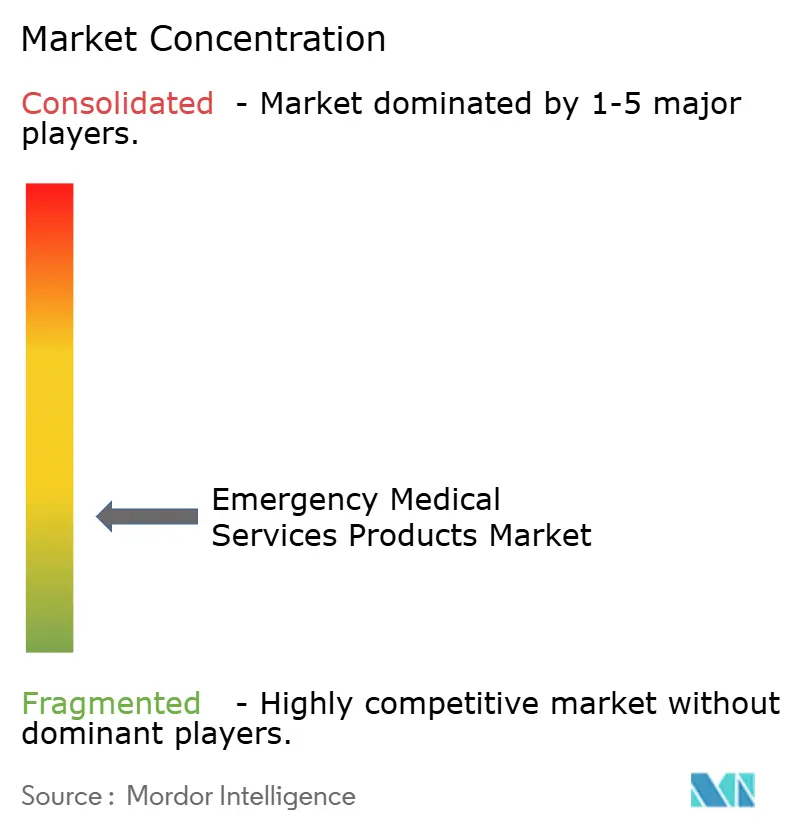

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emergency Medical Services Products Market Analysis by Mordor Intelligence

Emergency Medical Services Products Market size in 2026 is estimated at USD 35.49 billion, growing from 2025 value of USD 33.27 billion with 2031 projections showing USD 49.02 billion, growing at 6.67% CAGR over 2026-2031.

Demand arises from the confluence of aging populations, rising chronic-disease incidence, and technology that embeds artificial intelligence into portable monitors and defibrillators. AI-driven triage guidance now shortens on-scene assessment times, easing the paramedic workload during critical workforce shortages in rural districts. Community paramedicine programs, which dispatch clinicians to manage patients at home, have trimmed emergency-department visits by 17%, underscoring the market’s shift from reactive transport to proactive care. Mandates for public-access defibrillators, exemplified by Maryland’s 2024 school AED requirement, accelerate equipment adoption in non-healthcare venues. Simultaneously, aging ambulance fleets in OECD countries generate recurring replacement cycles that favor integrated, cloud-connected life-support systems. These dynamics collectively sustain a robust, geographically diversified revenue base for the Emergency medical services products market through the forecast horizon.

Key Report Takeaways

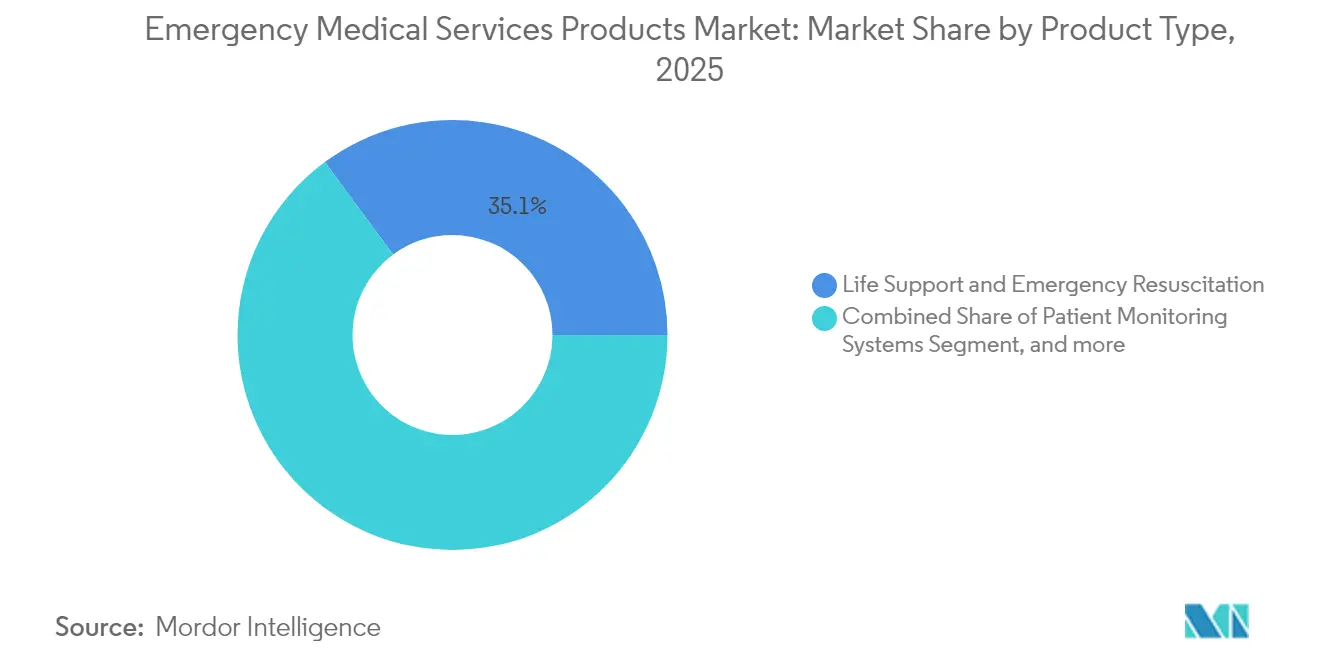

- By product type, life support and emergency resuscitation systems commanded a 35.12% revenue share in 2025, whereas automated chest compressors showed the strongest momentum, with a 7.72% CAGR through 2031.

- By application, cardiac care accounted for a dominant 42.10% of the emergency medical services products market share in 2025, while disaster & mass-casualty response is projected to expand at a 9.62% CAGR to 2031.

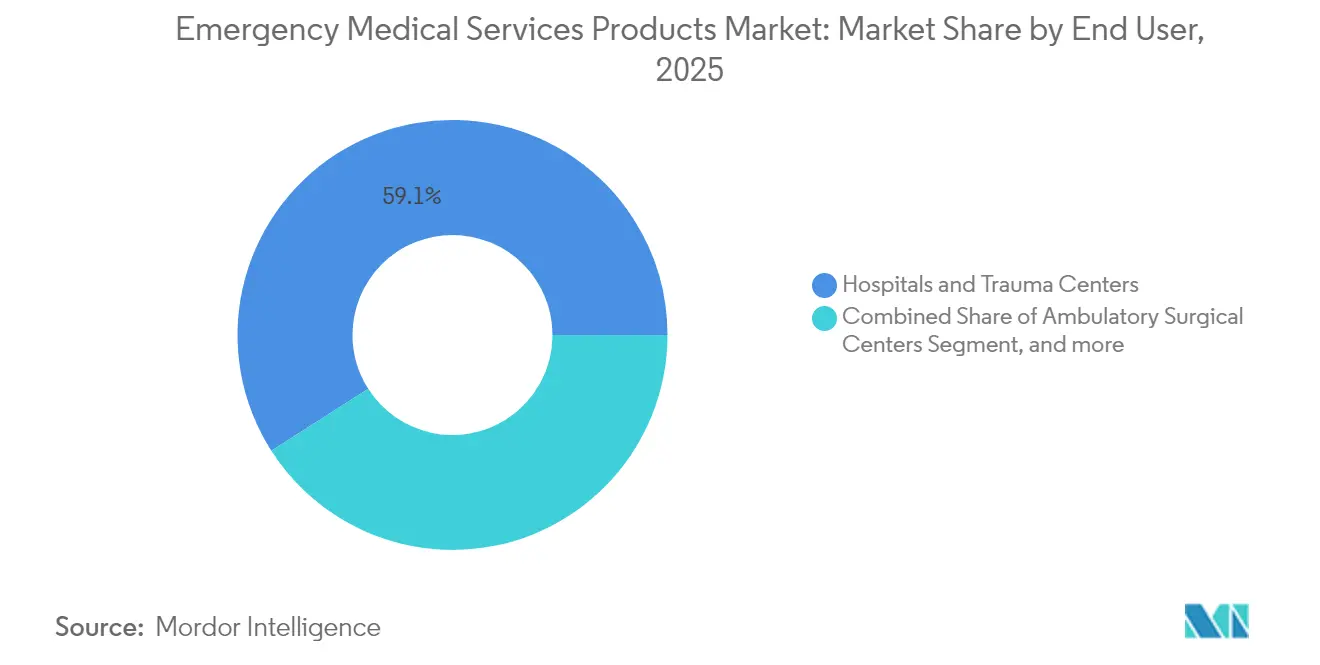

- By end user, hospitals & trauma centers held 59.05% of the emergency medical services products market size in 2025; ambulatory surgical centers are advancing at a 10.06% CAGR during the outlook period.

- By geography, North America led with a 36.78% revenue share in 2025, whereas Asia Pacific was the fastest-growing region, with a 8.97% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Emergency Medical Services Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Chronic Diseases & Injuries | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Ageing EMS Vehicle & Equipment Fleets in OECD Regions | +1.2% | North America & Europe primarily | Medium term (2-4 years) |

| Government Mandates for Public-Access Defibrillators | +1.0% | North America, Europe, with expansion to APAC | Medium term (2-4 years) |

| Expansion of Hospital-Based Community Paramedicine Programs | +0.9% | North America core, spill-over to Europe & APAC | Long term (≥ 4 years) |

| Surge in Extreme-Weather Disasters Driving Pre-Positioned Kits | +0.7% | Global, with emphasis on disaster-prone regions | Short term (≤ 2 years) |

| AI-Enabled Triage Devices for On-Scene Decision Support | +0.6% | North America & Europe early adoption, APAC following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Diseases & Injuries

Cardiovascular, diabetic, and trauma cases continue to climb, with cardiac events alone driving 42.64% of EMS product deployments. Portable monitors that transmit encrypted vitals directly into hospital records improve care continuity for these patients. Community paramedicine units that manage chronic illnesses at home cut treatment costs by up to 30%, reinforcing demand for rugged, multi-parameter devices. Hospital-at-home models, now green-lighted for 10% of inpatient populations, rely on field-grade technology with hospital-grade accuracy.[1]American Hospital Association, “Hospital-at-Home Expansion Primer,” aha.org Equipment capable of self-calibration ensures functionality in regions lacking biomedical technicians, further boosting the Emergency medical services products market.

Aging EMS Vehicle & Equipment Fleets in OECD Regions

Ambulances typically serve for 12 years, but electronics need refreshing every 5-7 years to stay compliant. This predictability creates replacement cycles that favor integrated telemedicine consoles over legacy devices. Electric ambulances introduce unique power-management constraints, driving demand for low-draw ventilators and defibrillators. Dual labeling under FDA and UKCA rules raises compliance costs, so providers increasingly select platforms that can be software-updated remotely to meet changing standards. Satellite-enabled communication modules ensure data flow in areas lacking stable cellular networks, reinforcing adoption across dispersed geographies.

Government Mandates for Public-Access Defibrillators

Statutes enacted in states such as Maryland obligate AED installation in schools, offices, and transport hubs, broadening the customer base beyond traditional EMS buyers.[2]ZOLL Medical Corporation, “School AED Compliance Guide,” zoll.com Europe’s parallel requirements under updated device legislation mirror this push. Each new deployment seeds a recurring revenue stream: pads must be replaced every 2-4 years, and batteries every 3-5 years. Public training programs demand manikins and simulation platforms, opening secondary revenue avenues for manufacturers already present in the Emergency medical services products market.

Expansion of Hospital-Based Community Paramedicine Programs

Health-systems now integrate EMS crews into value-based-care models that reward avoided admissions. Programs in the United States report 17% fewer emergency visits, validating the economic logic of equipping field teams with advanced diagnostics. Paramedics carry handheld ultrasound, point-of-care blood analyzers, and AI-enhanced triage tablets. These tools collect longitudinal data that hospitals mine for predictive analytics, creating a flywheel effect that continues to drive the Emergency medical services products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Complex Regulatory Approvals | -1.4% | Global, with emphasis on emerging markets | Long term (≥ 4 years) |

| Supply-Chain Disruptions for Critical Electronic Sub-Assemblies | -1.1% | Global, with particular impact on APAC manufacturing | Short term (≤ 2 years) |

| Talent Shortage of Biomedical Technicians in Rural Areas | -0.8% | North America & Europe rural regions | Medium term (2-4 years) |

| Growing Scrutiny on Single-Use Plastics in EMS Disposables | -0.5% | Europe primarily, expanding to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Complex Regulatory Approvals

Gaining FDA clearance for AI-embedded devices can stretch development timelines by three years and add USD 10-15 million to unit costs, deterring entrants and slowing rollout in low-resource settings. The EU Medical Device Regulation demands parallel technical files, doubling documentation. Smaller EMS agencies often rely on municipal grants to modernize fleets, yet budget ceilings still force staged procurement. The result is an adoption gap between flagship urban programs and cash-strapped rural services, constraining the Emergency medical services products market in price-sensitive segments.

Supply-Chain Disruptions for Critical Electronic Sub-Assemblies

Semiconductor shortages have lengthened component lead times to 52 weeks, prompting firms such as Stryker to dual-source printed circuit boards and boost inventory buffers.[3]Stryker Corporation, “Operational Update on Supply-Chain Diversification,” stryker.com Freight volatility adds further cost pressure. Design revisions that swap scarce chips for readily available equivalents necessitate fresh regulatory notifications, delaying shipments. The ripple effect is particularly harsh on start-ups that depend on just-in-time deliveries, dampening near-term growth prospects within the Emergency medical services products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Life Support Dominance Meets Automation Innovation

Life Support & Emergency Resuscitation gear retained a 35.12% slice of the emergency medical services products market in 2025. Adoption is anchored in the indispensable role of defibrillators, ventilators, and multi-parameter monitors during the golden hour of care. Mechanical CPR devices are transforming practice because they maintain consistent compressions during transport when the manual technique often deteriorates. The clinical evidence underpinning the LUCAS 3 and AutoPulse platforms has triggered procurement policies in multiple U.S. state EMS agencies. This trend is set to propel automated chest compressors at a 7.72% CAGR.

Wound-care consumables are under scrutiny due to mounting restrictions on single-use plastics. Manufacturers such as Verathon responded by introducing bio-based polymers that cut cradle-to-gate carbon footprints by 74% compared with petroleum-based equivalents. Patient handling rigs benefit from the aging demographic, while PPE demand persists amid ongoing pathogen vigilance. Drug-delivery and airway modules now incorporate audio prompts that coach correct dosing and tube placement, minimizing operator error in high-stress circumstances. Collectively, these sub-categories broaden solution suites and underpin the resilient trajectory of the Emergency medical services products market.

By Application: Cardiac Care Leadership Challenged by Disaster Preparedness

Cardiac care captured 42.10% of the revenue in 2025 of the emergency medical services products market. High cholesterol prevalence, sedentary lifestyles, and population aging sustain this dominance. At-scene defibrillation within three minutes triples survival odds, a statistic that continues to prioritize cardiac intervention devices on municipal spending agendas. However, disaster and mass-casualty response is expanding at a 9.62% CAGR. The frequency of extreme weather and geopolitical conflicts keeps curated response kits in permanent demand, especially across seismically active and conflict-prone territories.

Trauma & injury management equipment registers steady procurement, supported by public bleeding-control campaigns. Respiratory care devices enjoy renewed interest due to fresh air-quality concerns after consecutive wildfire seasons. Specialized applications such as pediatric resuscitation remain small but critical niches, attracting players with ultra-compact ventilators and dosing tools. The evolving risk landscape ensures balanced growth across use cases and continues to diversify the emergency medical services products market.

By End User: Hospital Concentration Faces Ambulatory Disruption

Hospitals & trauma centers represented 59.05% of spending in 2025, reflecting their role as regional hubs that orchestrate both ground and air transport. The cluster maintains a technology refresh cycle that prioritizes interoperability with electronic health records. Yet, ambulatory surgical centers are gaining ground, underpinned by procedure volumes that are 40-60% cheaper than hospital equivalents, and are projected to grow by 25% by 2030. These centers require ready-for-use code carts and portable ventilators to stabilize sudden complications, driving a 10.06% CAGR in purchases.

Municipal EMS agencies, fire departments, and volunteer squads operate within fixed budgets, encouraging bulk procurement of modular devices that share batteries and disposables. Industrial sites, sports arenas, and educational institutions adopt easy-to-use AEDs outfitted with animated instructions, ensuring layperson confidence. Cumulatively, this widening user base strengthens the revenue diversity of the Emergency medical services products market.

Geography Analysis

North America held 36.78% of the Emergency medical services products market in 2025, buoyed by stable reimbursement and mature trauma-care networks. More than 320 U.S. hospitals have CMS approval for hospital-at-home programs, compelling investment in broadband-enabled telemetry systems. Canada expands satellite-linked ambulance coverage to remote territories, while Mexico leverages medical tourism to benchmark equipment against international standards. The ongoing replacement of analog radios with secure digital protocols further stimulates spending across the region.

Europe combines steady demand with regulatory complexity. The EU Medical Device Regulation requires detailed clinical effectiveness data, prolonging launch timelines yet guaranteeing safety. Germany and France sustain procurement of AI-capable monitors, whereas the United Kingdom navigates dual MDR and UKCA filings. Nordic systems showcase end-to-end tele-EMS, integrating smart stretchers that weigh patients and adjust ventilator parameters in transit. Southern Europe, seeking cost-efficient answers, experiments with leasing models that spread capital outlays over contract lifecycles.

Asia Pacific is projected to clock a 8.97% CAGR through 2031. China’s rural emergency network expansion funnels grants into drone-assisted AED delivery in remote villages. India, now the world’s most populous nation, pairs its vibrant private hospital sector with public ambulance upgrades to maintain credentialing for global insurers. Japan pilots robotics in rapid extracorporeal CPR, whereas South Korea integrates 5G coverage to stream high-definition ultrasound from moving ambulances. Emerging ASEAN economies co-invest in regional training centers to standardize paramedic skill sets, securing a pipeline of consumables and durable medical hardware. The multi-layered growth map cements Asia’s role as the incremental engine of the Emergency medical services products market.

Competitive Landscape

The emergency medical services products market remains fragmented. Stryker, Medtronic, and GE HealthCare dominate high-acuity equipment by pairing long-standing brand trust with AI software roadmaps. Stryker’s USD 4.9 billion buyout of Inari Medical in 2024 broadened its vascular-emergency portfolio, while Medtronic deepened ties with cloud analytics firms to enrich remote-monitoring dashboards. GE HealthCare exploits its installed base in hospital imaging to cross-sell transport monitors that share user interfaces with stationary machines.

Private equity has intensified its presence, epitomized by Bridgefield Capital acquiring Philips’ Emergency Care division in January 2025. The carve-out underscores the financial-sponsor belief that scale and supply-chain consolidation can unlock margin expansion in a USD 26 billion addressable arena. Meanwhile, mid-tier challengers differentiate through eco-friendly materials. Verathon’s bio-polymer disposables resonate with European customers seeking to curb single-use plastic waste. Start-ups focus on AI-only solutions, but many partner with incumbents to access regulatory infrastructure.

Supply-chain resilience is emerging as a decisive moat. Stryker diversifies printed-circuit sourcing across three continents, reducing chip-shortage risk. ZOLL integrates edge-processing chips that reduce cloud dependency, delivering uninterrupted guidance in disaster zones. Players with vertically integrated manufacturing and in-house software talent are best positioned to navigate a landscape that increasingly rewards interoperability, data security, and environmental stewardship in the Emergency medical services products market.

Emergency Medical Services Products Industry Leaders

GE Healthcare

Medtronic

3M

Stryker Corporation

McKesson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Falck USA has expanded its footprint in the United States with the launch of ambulance operations in the Dallas/Fort Worth (DFW) Metroplex, marking a strategic entry into the Southwest region. This move brings Falck’s globally recognized standard of care to one of the country’s fastest-growing areas, strengthening its commitment to delivering exceptional emergency medical services.

- May 2025: KIMSHEALTH introduced Kerala’s first AI-integrated smart ambulance service, setting a new benchmark in tech-driven patient transport. The ambulance equipped with cutting-edge technology to enhance emergency response efficiency was officially inaugurated by CMD of KIMSHEALTH, in a ceremony at the hospital.

- November 2024: Red.Health, Asia’s first emergency response company accredited by JCI, has launched Salus EMS, a next-generation emergency medical services platform. Designed to transform the delivery of emergency care, Salus EMS enhances real-time coordination between ambulances and hospitals, ensuring faster interventions and better preparedness for critical cases.

- July 2024: Pinnacle Industries, a leader in automotive interiors and specialty vehicles in India, has unveiled its latest innovation in emergency care mobility: the AD-Gen Ambulance. This semi-premium variant features advanced design elements and high-tech components and is adaptable to all vehicle platforms. It is aimed at modernizing ambulance fleets across the country.

Global Emergency Medical Services Products Market Report Scope

Emergency medical surgical products refer to a wide range of medical devices, instruments, and supplies specifically designed and utilized in emergencies to provide immediate medical care and perform surgical procedures. These products are essential when rapid medical intervention is required to save lives, stabilize patients, or address critical injuries or illnesses.

The emergency medical services products market is segmented by type (life support & emergency resuscitation (defibrillators, ventilators, laryngoscopes, and other life support & emergency resuscitations), patient monitoring systems, wound care (dressings & bandages, sutures & staples, and other wound care), patient handling equipment (medical beds, wheelchairs & scooters, and other equipment), infection control supplies (disinfectant & cleaning agents, personal protection equipment, and other infection control supplies ), and other EMS products), end-user (hospitals & trauma centers, ambulatory surgical centers, other end-users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across significant regions globally.

The report offers the value (in USD) for the above segments.

| Life Support & Emergency Resuscitation | Defibrillators |

| Ventilators | |

| Laryngoscopes | |

| Automated Chest Compressors | |

| Other Systems | |

| Patient Monitoring Systems | |

| Wound Care Consumables | Dressings & Bandages |

| Sutures & Staples | |

| Hemostatic Agents | |

| Other Consumables | |

| Patient Handling Equipment | Medical Beds |

| Wheelchairs & Scooters | |

| Stretchers & Transfer Equipment | |

| Other Equipment | |

| Infection Control & PPE | Disinfectant & Cleaning Agents |

| Personal Protective Equipment | |

| Air Filtration & Isolation Supplies | |

| Other Supplies | |

| Drug Delivery & Airway Management | Intraosseous Access Devices |

| Bag Valve Masks | |

| Infusion Pumps | |

| Other Products |

| Cardiac Care |

| Trauma & Injury Management |

| Respiratory Care |

| Disaster & Mass-Casualty Response |

| Other Applications |

| Hospitals & Trauma Centers |

| EMS Agencies & Fire Departments |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Life Support & Emergency Resuscitation | Defibrillators |

| Ventilators | ||

| Laryngoscopes | ||

| Automated Chest Compressors | ||

| Other Systems | ||

| Patient Monitoring Systems | ||

| Wound Care Consumables | Dressings & Bandages | |

| Sutures & Staples | ||

| Hemostatic Agents | ||

| Other Consumables | ||

| Patient Handling Equipment | Medical Beds | |

| Wheelchairs & Scooters | ||

| Stretchers & Transfer Equipment | ||

| Other Equipment | ||

| Infection Control & PPE | Disinfectant & Cleaning Agents | |

| Personal Protective Equipment | ||

| Air Filtration & Isolation Supplies | ||

| Other Supplies | ||

| Drug Delivery & Airway Management | Intraosseous Access Devices | |

| Bag Valve Masks | ||

| Infusion Pumps | ||

| Other Products | ||

| By Application | Cardiac Care | |

| Trauma & Injury Management | ||

| Respiratory Care | ||

| Disaster & Mass-Casualty Response | ||

| Other Applications | ||

| By End User | Hospitals & Trauma Centers | |

| EMS Agencies & Fire Departments | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the emergency medical services products market?

It is valued at USD 35.49 billion in 2026 and is forecast to grow to USD 49.02 billion by 2031.

Which product category leads market revenue?

Life support & emergency resuscitation devices hold 35.12% of 2025 sales, led by defibrillators and ventilators.

Why are automated chest compressors gaining traction?

Clinical studies show consistent mechanical CPR improves survival, supporting a 7.72% CAGR for this segment.

Which region is expanding fastest?

Asia Pacific is growing at 8.97% CAGR due to infrastructure upgrades and rising healthcare investment.

How do public-access defibrillator mandates influence demand?

Legislation requiring AEDs in schools and workplaces expands installations and drives steady consumables revenue.

What challenges hamper market growth?

High regulatory costs and semiconductor supply-chain disruptions can delay product launches and inflate prices.

Page last updated on: