Medical Clothing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

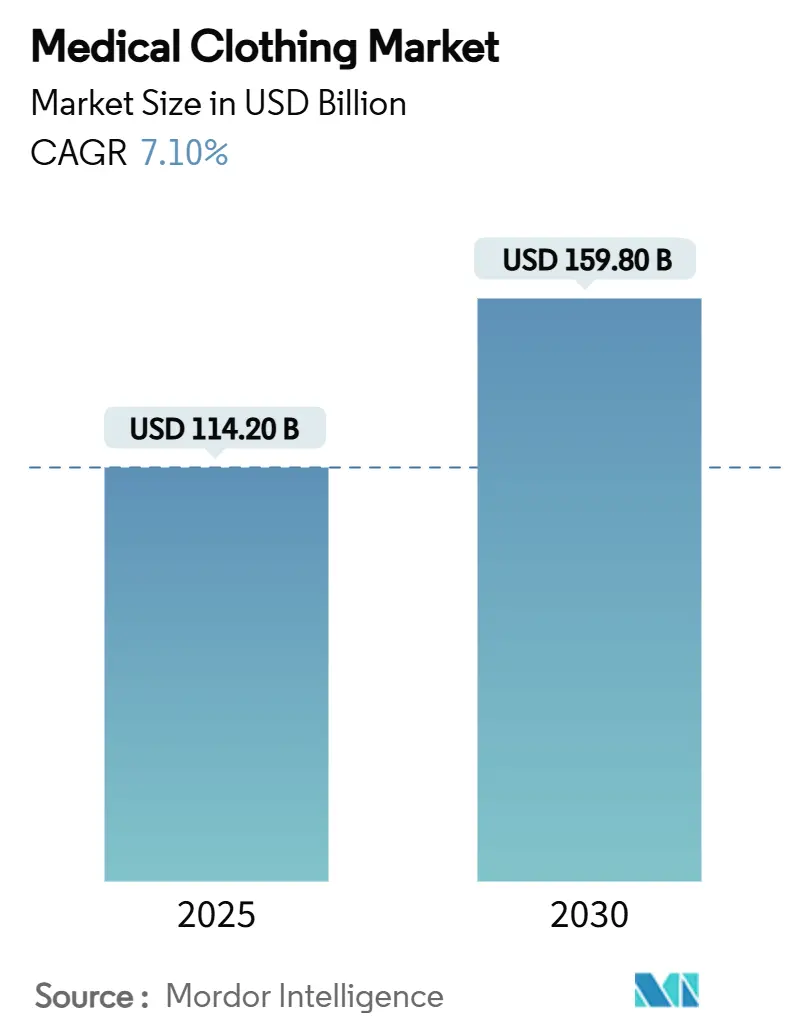

| Market Size (2025) | USD 114.20 Billion |

| Market Size (2030) | USD 159.80 Billion |

| Growth Rate (2025 - 2030) | 7.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Clothing Market Analysis by Mordor Intelligence

The global medical clothing market size stood at USD 114.2 billion in 2025 and is forecast to reach USD 159.8 billion by 2030, advancing at a 7.1% CAGR over the period. Heightened infection-prevention protocols, steady outpatient procedure growth, and rapid material innovation are steering the market away from commodity garments toward function-rich, sensor-enabled apparel that supports patient monitoring in real time. Disposable products dominate present demand because hospitals now place greater value on barrier performance than on reuse economics, yet sustainability requirements are pushing suppliers to integrate biodegradable or recyclable inputs that satisfy circular-economy goals. Technology-enabled entrants have blurred the line between clinical wear and connected health devices, using blockchain-backed B2B portals and subscription models to deliver just-in-time inventory while capturing valuable usage data. Finally, home-care expansion and bariatric–geriatric case growth are creating niches for adaptive garments that favor comfort and mobility, signaling that future competitive advantage will hinge on design versatility, digital connectivity, and verifiable ESG credentials.

Key Report Takeaways

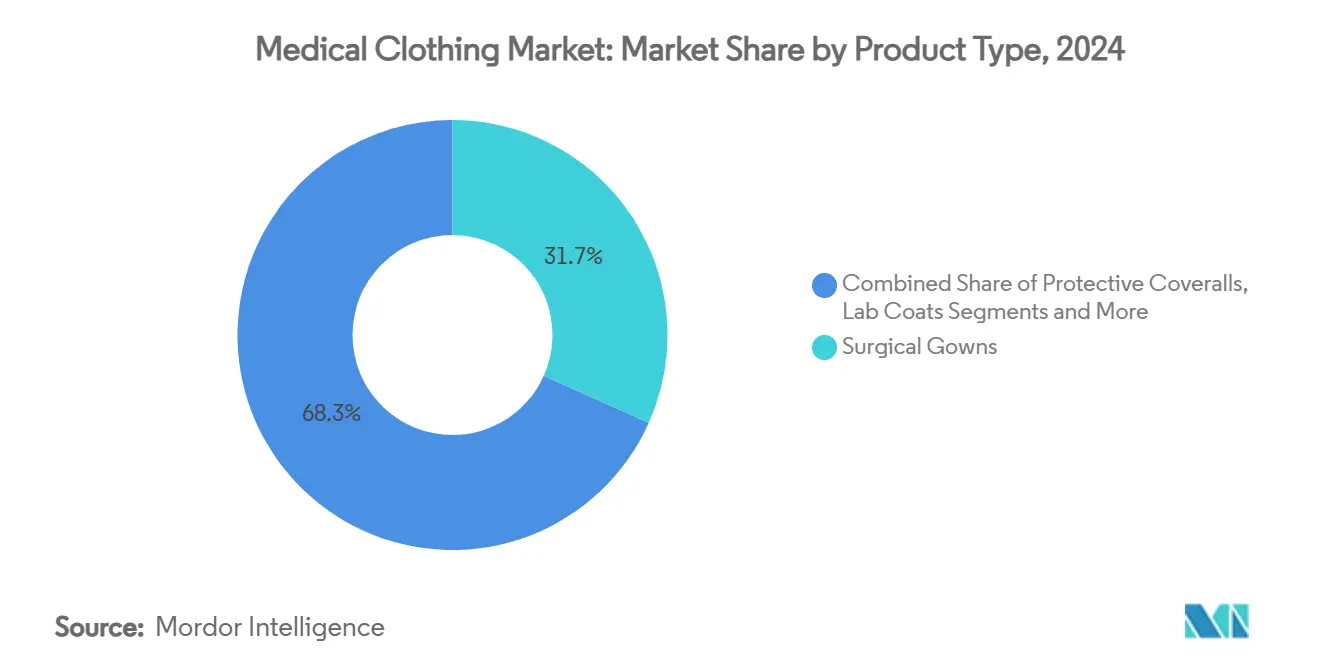

- By product type, surgical gowns led with 31.7% revenue share in 2024, while smart sensor-enabled scrubs are projected to grow at 11.8% CAGR through 2030.

- By usability, disposable apparel controlled 74.1% of 2024 demand and is expanding at 8.4% CAGR, whereas reusable systems lag but gain traction in circular-textile pilots growing at 5.2% CAGR.

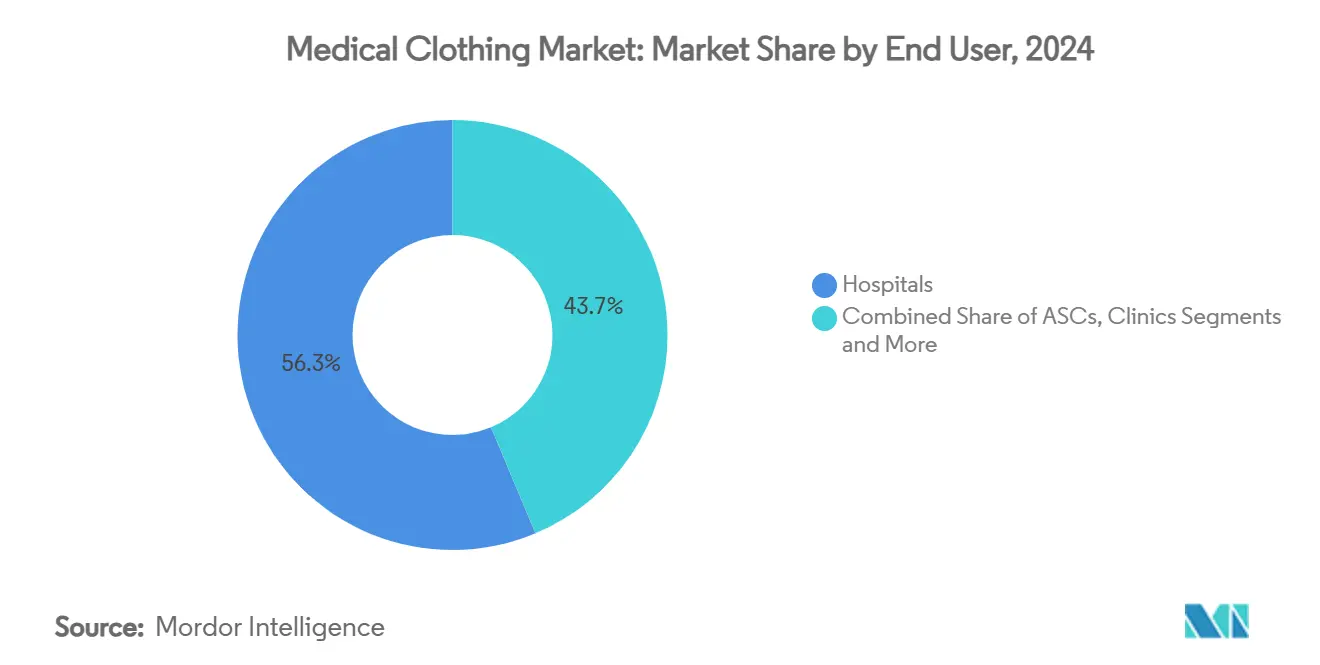

- By end user, hospitals retained 56.3% share in 2024, yet home-health and long-term-care settings post the fastest growth at 10.1% CAGR.

- By material, polypropylene SMS captured 38.6% share in 2024; antimicrobial smart textiles headline growth at 12.5% CAGR.

- By distribution channel, direct institutional procurement held 62.8% share in 2024; e-commerce platforms are outpacing all others at 15.2% CAGR.

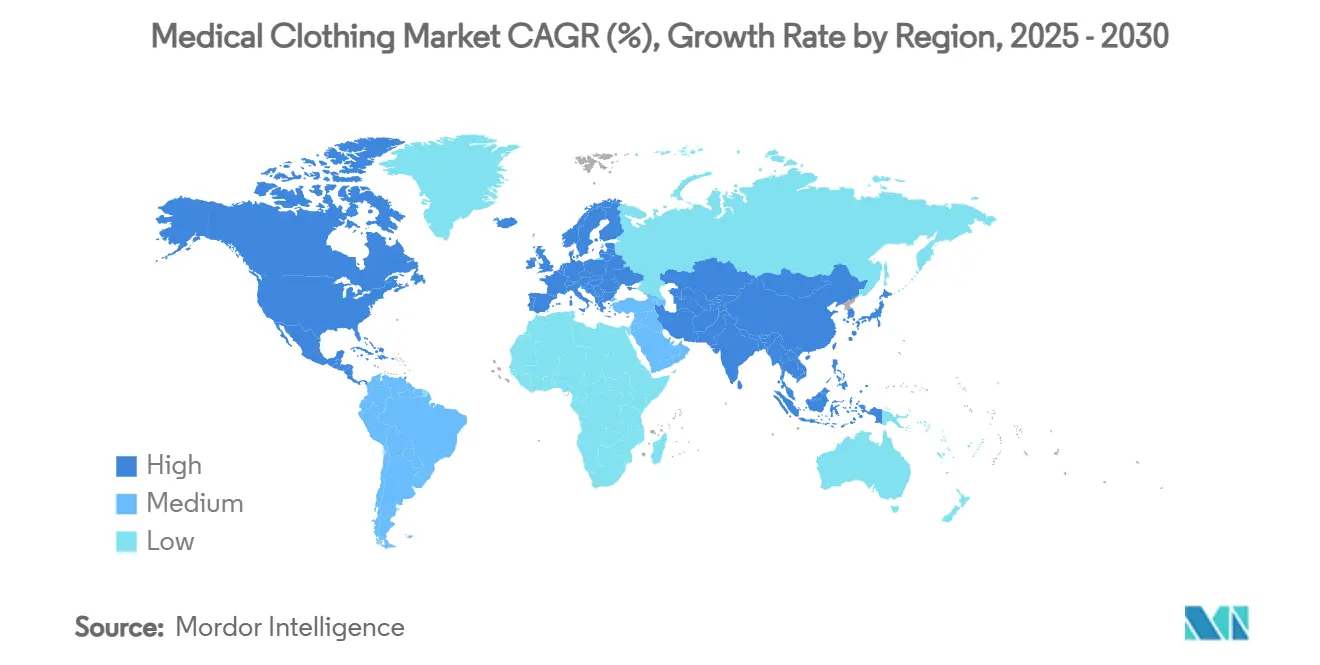

- By geography, North America accounted for 37.9% of the medical clothing market share in 2024, while Asia-Pacific is forecast to post a 9.7% CAGR to 2030.

Global Medical Clothing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID IPC mandates boost demand for single-use apparel | +1.80% | Global, highest in North America & EU | Short term (≤ 2 years) |

| Rapid growth in outpatient & ASC procedures | +1.20% | North America core, expanding to APAC | Medium term (2-4 years) |

| Surge in antimicrobial & fluid-impervious textile adoption | +0.90% | Global, led by developed markets | Medium term (2-4 years) |

| Shift toward hospital-managed B2B e-commerce uniform portals | +0.70% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Rise of adaptive garments for bariatric & geriatric care | +0.60% | North America & EU | Long term (≥ 4 years) |

| ESG-driven circular-textile contracts with take-back clauses | +0.40% | EU leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID IPC Mandates Boost Demand for Single-Use Apparel

The Centers for Disease Control now recommends Level 4 barrier protection for viral penetration in surgical settings, compelling hospitals to substitute reusable gowns with certified single-use options that meet ANSI/AAMI PB70 standards.[1]Centers for Disease Control and Prevention, “PPE-Info—ANSI/AAMI PB70 Class 4 Guidance,” cdc.gov Disposable garments subsequently captured 74.1% of global demand in 2024 and are rising 8.4% CAGR because infection-control officers treat high-performance apparel as litigation insurance rather than a consumable cost. Elevated usage also accelerates R&D into biodegradable spun-bond substrates, enabling providers to address waste-management rules without compromising safety. The result is a durable volume shift favoring single-use suppliers capable of evidencing standards compliance and waste-reduction metrics in the same offering.

Rapid Growth In Outpatient & ASC Procedures

Ambulatory surgery centers treated 3.3 million Medicare beneficiaries in 2022, accounting for USD 6.1 billion in spend, a figure that underpins specialty-focused demand for lightweight, turnover-friendly garments that maintain sterile-field integrity.[2]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” medpac.gov As gastrointestinal and ophthalmology procedures migrate away from inpatient settings, buyers prioritize standardized packs that minimize setup time and inventory complexity. Simultaneously, value-based reimbursement drives procurement teams to forge direct agreements that bypass distributor mark-ups, granting smaller apparel innovators a clear route to market and heightening competitive churn.

Surge In Antimicrobial & Fluid-Impervious Textile Adoption

Silver-based and chitosan-bound coatings able to withstand 75 wash cycles moving from pilot to mainstream, pushing antimicrobial smart-textile sales to a 12.5% CAGR trajectory.[3]Seyedali Mirmohammadsadeghi et al., “Durable Antibacterial Gel-Like Coatings for Textiles,” arxiv.orgHospitals regard such fabrics as a second-line defense against cross-contamination, particularly as multidrug-resistant infections climb. Material scientists now embed antimicrobial agents at fiber level rather than via surface treatments, delivering durability that justifies premium pricing. Natural antimicrobials aligned with ESG commitments are also drawing interest because they reduce chemical-exposure concerns among staff and auditors.

Shift Toward Hospital-Managed B2B E-Commerce Uniform Portals

U.S. supply-chain leaders expect 2025 to mark a decisive pivot toward direct, digital sourcing as hospitals deploy predictive-ordering dashboards that integrate usage analytics and automated re-stock triggers. Platforms expanding at 15.2% CAGR give buyers end-to-end transparency, reduce working-capital lock-up, and shrink distributor fees, forcing wholesalers to upgrade value propositions or cede share. Suppliers able to embed real-time order-status feeds, API-based product registries, and customizable staff-allotment tools gain privileged access to 62.8% of institutional budgets currently routed through in-house procurement teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polypropylene & cotton pricing | -1.10% | Global, highest in manufacturing hubs | Short term (≤ 2 years) |

| Medical-textile landfill scrutiny & tightening disposal rules | -0.80% | EU leading, expanding to North America | Medium term (2-4 years) |

| High ISO 16604 / ASTM F1671 certification costs for SMEs | -0.60% | Global, particularly emerging markets | Medium term (2-4 years) |

| Counterfeit PPE inflow eroding brand trust | -0.40% | Global, highest in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Polypropylene & Cotton Pricing

Feedstock costs account for up to 20% of revenue in medical-apparel manufacturing, and a sharp spike in polypropylene during 2024–25 cut gross margins by as much as 300 basis points for contract suppliers bound by annual pricing. To offset volatility, larger players pursue vertical integration or resin-hedging strategies, whereas SMEs often absorb higher input costs, delaying expansion plans and stalling innovation pipelines. The squeeze magnifies the gulf between scale leaders and niche newcomers, curbing market dynamism in the near term.

Medical-Textile Landfill Scrutiny & Tightening Disposal Rules

With UK healthcare waste topping 156,000 tonnes annually, regulators across Europe have tightened landfill quotas and are rolling out extended-producer-responsibility regimes that force suppliers to finance collection and recycling schemes. Compliance introduces added documentation, transport, and processing costs that weigh most heavily on single-use leaders. Although forward-looking firms treat the rules as a catalyst for product redesign, the need to secure additional permits and audits can stretch commercialization timelines and slow market penetration rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Sensor Integration Transforms Traditional Categories

Surgical gowns continued to secure the largest slice of 2024 revenue at 31.7%, underpinned by strict operating-room protocols. In contrast, smart sensor-enabled scrubs are projected to accelerate at 11.8% CAGR, the fastest rate across all categories. The medical clothing market size for surgical gowns is expected to climb steadily alongside rising surgical volumes, but growth now leans toward garments capable of recording body temperature, heart rate, and movement without external patches, thereby turning everyday uniforms into clinical data nodes.

Manufacturers embed microcontrollers inside yarns, enabling fitness-grade accuracy through routine washing, a feat that shrinks the accessory footprint in crowded theatres. At the same time, isolation and patient gowns benefit from extended infection-prevention standards enacted post-COVID, while lab coats and coveralls anchor demand in research and hazmat contexts. Caps, masks, and shoe covers remain high-volume, low-margin staples. Still, design tweaks—such as anti-fog visors and breathable ear loops—illustrate how even commodity items now compete on feature differentiation. Consequently, product competition will increasingly hinge on the ability to validate digital functionality within recognized regulatory frameworks.

By Usability: Disposable Dominance Reflects Safety Priorities

Disposable apparel sustained a commanding 74.1% share in 2024 and is expected to widen its lead with an 8.4% CAGR through 2030 as institutions embed single-use policies into standard operating procedures. The medical clothing market size for disposable PPE, therefore, tracks overall sector expansion, particularly in high-risk units such as oncology and transplant wards where sterility lapses carry heavy financial penalties.

Reusable systems nonetheless retain footholds in lower-acuity environments and in regions where environmental legislation incentivizes textile re-processing. Smart acoustic textiles leveraging piezoelectric fibers demonstrate viable multicycle durability, giving rehabilitation centers a compelling total-cost-of-ownership case. Chemical-free antimicrobial finishes and self-healing coatings further extend lifecycle value propositions, ensuring that disposable hegemony is not absolute but rather context specific. The emerging model is hybrid: disposables for viral-exposure intensive procedures and advanced reusables for chronic-care monitoring, each backed by evidence-based risk-stratification.

By End User: ASC Growth Reshapes Demand Patterns

Hospitals remained the principal buyers, holding 56.3% of global demand in 2024; however, market analysts predict that home-health and long-term-care facilities will clock a 10.1% CAGR, outpacing all other channels. ASC throughput continues to escalate under cost-saving mandates, redirecting garment specifications toward rapid-change designs that minimize peri-operative downtime.

Diagnostic imaging centers and labs call for radiation-attenuating fabrics and easy cable routing, whereas dental and veterinary clinics, though niche, insist on splash resistance and comfort during extended chair-side sessions. Research institutes double as test beds for new sensor-rich fabrics, accelerating time to regulatory approval. As virtual care and hospital-at-home programs proliferate, designers are adapting garments for non-institutional settings, blending clinical functionality with civilian aesthetics that support patient dignity.

By Material: Antimicrobial Innovation Drives Premium Segments

Polypropylene SMS led 2024 demand with 38.6% share thanks to superior hydrostatic pressure and bacterial-filtration metrics. Yet antimicrobial smart textiles headline growth at 12.5% CAGR because hospitals seek barrier redundancy via embedded biocides that reduce surface contamination between change cycles. The medical clothing market share held by SMS is expected to erode incrementally as silver-nanoparticle and plant-extract coatings prove equally protective and more ESG compliant.

Cotton-polyester blends serve administrative and ambulatory environments where breathability matters most, while polyethylene remains a low-cost option for low-risk areas. High-performance aramid composites answer extreme-hazard use cases but face substitution by lighter, sensor-compatible laminates. Material scientists now target multifunctionality—combining liquid repellence, antimicrobial efficacy, stretch, and conductivity in a single construction—to satisfy diverse clinical settings without increasing SKU complexity.

By Risk Level: Regulatory Standards Drive Segmentation

ANSI/AAMI PB70 classification anchors purchasing decisions, and Level 4 garments, though higher in cost, enjoy consistent reorder cycles because they protect against blood-borne pathogens in surgical environments. Market evidence shows that healthcare buyers are willing to absorb premium pricing for third-party certified gowns, making the category comparatively recession resistant.

Levels 1 to 3 dominate outpatient clinics where splash or light fluid resistance suffices, and minimal-risk garments populate administrative areas such as reception or billing. For SMEs, the path into Level 4 remains constrained by ISO 16604 and ASTM F1671 certification costs, prompting licensing partnerships with bigger players that already hold approvals. Over time, risk-based segmentation will likely incorporate digital-proof points—such as RFID or blockchain tags—for traceability, further raising entry barriers.

By Distribution Channel: Digital Transformation Accelerates

Direct institutional procurement captured 62.8% of sales in 2024, leveraging legacy enterprise-resource-planning integrations, yet e-commerce and B2B marketplaces are set to record a head-turning 15.2% CAGR through 2030. In practice, the medical clothing market size procured through online portals is climbing fastest where hospitals prioritize cost transparency and contractual agility.

Distributors respond by offering value-added kitting, sterilization, and same-day delivery, but margins continue to compress as customers benchmark fees against direct-from-manufacturer listings. Retail outlets remain relevant only for individual practitioners and small clinics purchasing limited volumes. As blockchain-enabled custody logs improve counterfeit detection, buyer trust in online channels is likely to strengthen, accelerating digital migration across mature and emerging regions alike.

Geography Analysis

North America commanded 37.9% of global revenue in 2024, supported by stringent Occupational Safety and Health Administration enforcement and a sophisticated reimbursement system that reimburses high-specification apparel more readily than generic alternatives. U.S. providers also spearheaded the adoption of sensor-integrated uniforms, converting clinician feedback into iterative design upgrades that feedback into procurement cycles. Canada and Mexico supply competitively priced manufacturing capacity that shortens lead times for regional buyers, while tariffs and reshoring incentives continue to reshape vendor footprints.

Asia-Pacific is the fastest-growing arena, projected to register a 9.7% CAGR as public-sector investment widens insurance coverage and local contract-manufacturing organizations scale exports. China is positioned as the largest production node, yet companies are diversifying into Vietnam, India, and Indonesia to mitigate geopolitical risk. Japan’s materials expertise spurs high-end smart-textile deployment, and South Korea’s electronics incumbents leverage existing sensor tech to move downstream into connected garments. Australia, though smaller in size, offers a regulatory pathway recognized across many Pacific and African nations, giving exporters broader reach.

Europe ranks third in absolute dollars but first in regulatory complexity, framing the medical clothing market as a test case for circular-textile mandates that could define global norms. The NHS projects USD 11 million in potential annual savings through reuse and remanufacturing, enticing suppliers to co-design garments with disassembly and recycling in mind. Germany and the United Kingdom act as innovation hubs for barrier-protection standards, while France and Italy leverage historic fashion infrastructure to infuse clinical wear with ergonomic aesthetics. Southern Europe provides cost-efficient manufacturing under the EU regulatory umbrella, supporting localized production for swift replenishment. Emerging markets in the Middle East and Africa exhibit double-digit unit growth, albeit from a low base, as tertiary-care expansion drives baseline compliance with global PPE guidelines.

Competitive Landscape

The medical clothing market displays moderate fragmentation: top ten players together account for roughly 55% of worldwide revenue, leaving room for niche innovators. Cardinal Health expanded its product suite via the launch of the Kendall SCD SmartFlow Compression System and continues to fortify positions in high-barrier gowns and gloves. Medline’s near USD 1 billion acquisition of Ecolab’s surgical solutions portfolio demonstrates vertical expansion into sterile-drape adjacencies that complement core garment lines.

Technology investment patterns highlight integration of AI, IoT, and antimicrobial chemistries as primary differentiation vectors. For example, Kimberly-Clark is deploying USD 2 billion over five years to automate regional plants, boosting agility and shortening response windows for demand spikes. Smaller entrants such as FIGS monetize brand affinity through lifestyle-driven D2C models, while Careismatic Brands’ restructuring illustrates the hazards of overreliance on single-channel wholesale agreements.

Strategically, larger incumbents increasingly co-invest with raw-material suppliers to stabilize polypropylene and silver-nanoparticle inputs, mitigating margin compression. Adaptive-garment specialists focus on co-creation with home-health agencies to lock down early mover advantages in non-acute segments. As digital procurement eliminates gatekeepers, manufacturers able to prove barrier integrity, ESG compliance, and staff-satisfaction metrics on a common data dashboard are best placed to win contract renewals.

Medical Clothing Industry Leaders

Cardinal Health

Medline Industries

3M Company

Owens & Minor

Kimberly-Clark

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kimberly-Clark announced an investment exceeding USD 2 billion to build an advanced facility in Warren, Ohio, alongside an automated distribution center in South Carolina. This will create more than 900 jobs and expand personal-care and medical-clothing capacity.

- February 2025: Owens & Minor reduced debt by USD 244 million and initiated a sale process for its Products & Healthcare Services segment, which houses medical-clothing production and logistics assets.

- November 2024: Cardinal Health unveiled the Kendall SCD SmartFlow Compression System featuring patient-sensing technology aimed at reducing venous-thromboembolism risk.

- May 2024: Medline agreed to acquire Ecolab’s surgical solutions business for nearly USD 1 billion, adding Microtek sterile-drape lines to its portfolio.

Global Medical Clothing Market Report Scope

| Medical Scrubs |

| Surgical Gowns |

| Isolation & Patient Gowns |

| Protective Coveralls / Hazmat Suits |

| Lab Coats |

| Caps, Masks & Shoe Covers |

| Compression & Support Garments |

| Adaptive / Patient Clothing |

| Cleanroom Apparel |

| Disposable |

| Reusable |

| Hospitals |

| Ambulatory Surgical Centres |

| Out-patient Clinics |

| Diagnostic & Imaging Labs |

| Home-health & Long-term Care |

| Dental & Veterinary Clinics |

| Research & Academic Institutes |

| Cotton |

| Polyester & Blends |

| Polypropylene (SMS / SMMS) |

| Polyethylene |

| Aramid & High-performance Blends |

| Antimicrobial-treated Textiles |

| Smart / Sensor-integrated Textiles |

| Minimal |

| Low |

| Moderate |

| High |

| Direct Institutional Procurement |

| Distributors & Wholesalers |

| Retail Stores |

| E-commerce & B2B Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Medical Scrubs | |

| Surgical Gowns | ||

| Isolation & Patient Gowns | ||

| Protective Coveralls / Hazmat Suits | ||

| Lab Coats | ||

| Caps, Masks & Shoe Covers | ||

| Compression & Support Garments | ||

| Adaptive / Patient Clothing | ||

| Cleanroom Apparel | ||

| By Usability | Disposable | |

| Reusable | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Out-patient Clinics | ||

| Diagnostic & Imaging Labs | ||

| Home-health & Long-term Care | ||

| Dental & Veterinary Clinics | ||

| Research & Academic Institutes | ||

| By Material | Cotton | |

| Polyester & Blends | ||

| Polypropylene (SMS / SMMS) | ||

| Polyethylene | ||

| Aramid & High-performance Blends | ||

| Antimicrobial-treated Textiles | ||

| Smart / Sensor-integrated Textiles | ||

| By Risk Level | Minimal | |

| Low | ||

| Moderate | ||

| High | ||

| By Distribution Channel | Direct Institutional Procurement | |

| Distributors & Wholesalers | ||

| Retail Stores | ||

| E-commerce & B2B Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical clothing market?

The medical clothing market size reached USD 114.2 billion in 2025 and is projected to hit USD 159.8 billion by 2030.

Which region is growing fastest in medical clothing demand?

Asia-Pacific is forecast to advance at a 9.7% CAGR through 2030, outpacing all other regions.

Why are disposable medical garments dominant?

Post-COVID infection-control mandates and ANSI/AAMI PB70 Level 4 requirements have pushed hospitals to prioritize single-use apparel that guarantees certified barrier performance.

What product category is expanding quickest?

Smart sensor-enabled scrubs are expected to grow at an 11.8% CAGR as healthcare providers seek real-time vital monitoring capabilities.

How are sustainability goals shaping procurement?

European and North American health systems increasingly demand circular-textile contracts with take-back clauses, incentivizing suppliers to adopt biodegradable materials and recycling programs.

What role do e-commerce platforms play in medical-clothing sourcing?

Hospital-managed B2B portals are growing 15.2% CAGR by offering real-time inventory visibility, predictive ordering, and reduced distributor fees.

Page last updated on: