Moist Wound Dressings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.31 Billion |

| Market Size (2031) | USD 6.86 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

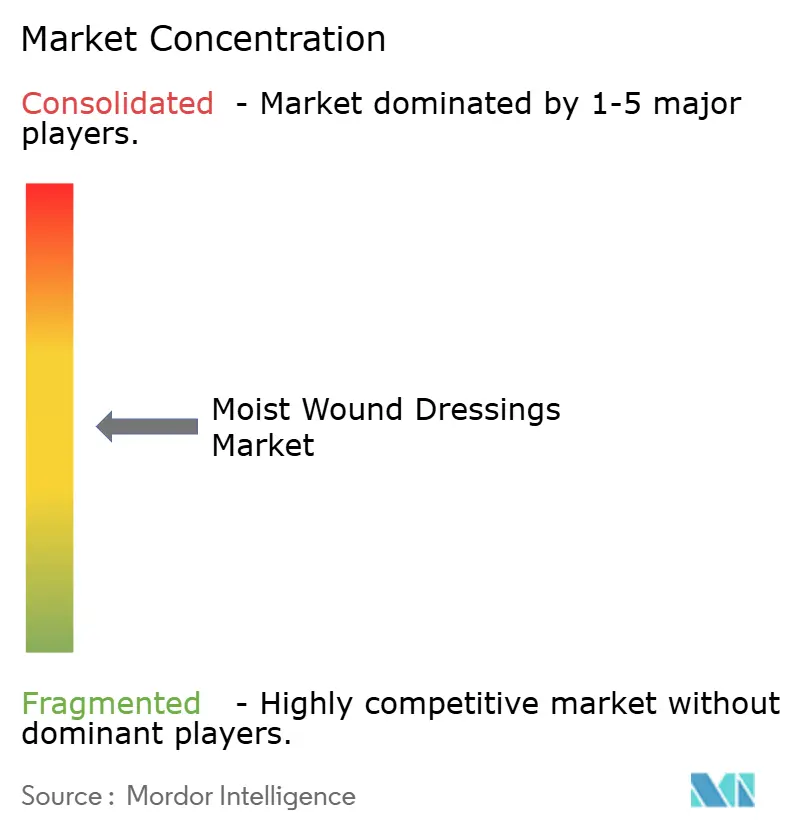

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Moist Wound Dressings Market Analysis by Mordor Intelligence

Moist wound dressings market size in 2026 is estimated at USD 5.31 billion, growing from 2025 value of USD 5.05 billion with 2031 projections showing USD 6.86 billion, growing at 5.24% CAGR over 2026-2031. Continuous migration from dry gauze to moisture‐retentive solutions underpins this advance, as clinical data confirm that controlled hydration speeds epithelialization and limits scarring. Hospitals and payers increasingly recognize that optimized moisture balance reduces lengthy inpatient stays and costly complications, a realization amplified by the global rise in chronic wounds linked to aging and diabetes. Competitive intensity is heightening as smart sensor layers, pH‐responsive polymers, and antimicrobial additives alter what healthcare providers expect from a dressing, transforming a once commodity-like product into a data-enabled therapeutic. Regulatory momentum further supports innovation: the U.S. Food and Drug Administration (FDA) designated enzymatic infection-sensing dressings as Class II devices in June 2025, clarifying the pathway for next-generation monitoring technologies. In parallel, reimbursement reforms that reward demonstrable healing outcomes are nudging purchasing decisions toward evidence-backed brands, encouraging consolidation around manufacturers able to pair materials science with measurable clinical benefit.

Key Report Takeaways

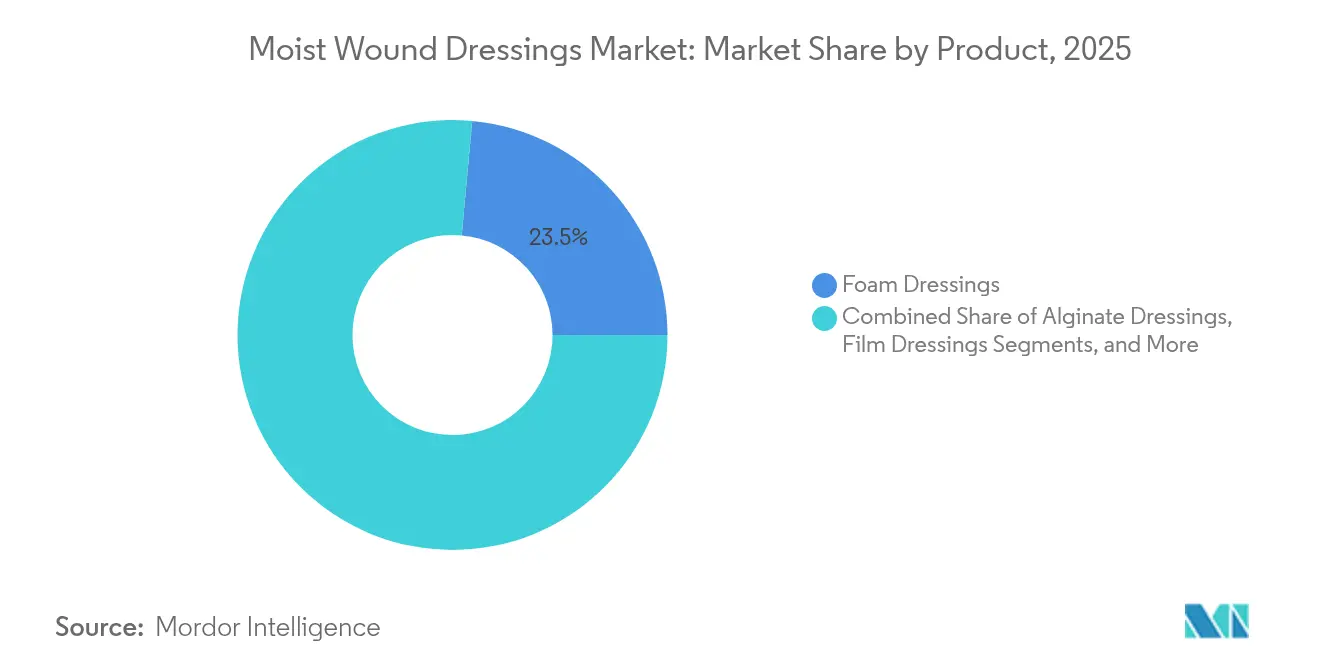

- By product type: Foam dressings led with 23.54% of moist wound dressings market share in 2025; hydrocolloid dressings are projected to grow at 5.93% CAGR through 2031.

- By application: Surgical and traumatic wounds accounted for 36.21% of the moist wound dressings market size in 2025, while diabetic foot ulcers are advancing at 6.27% CAGR to 2031.

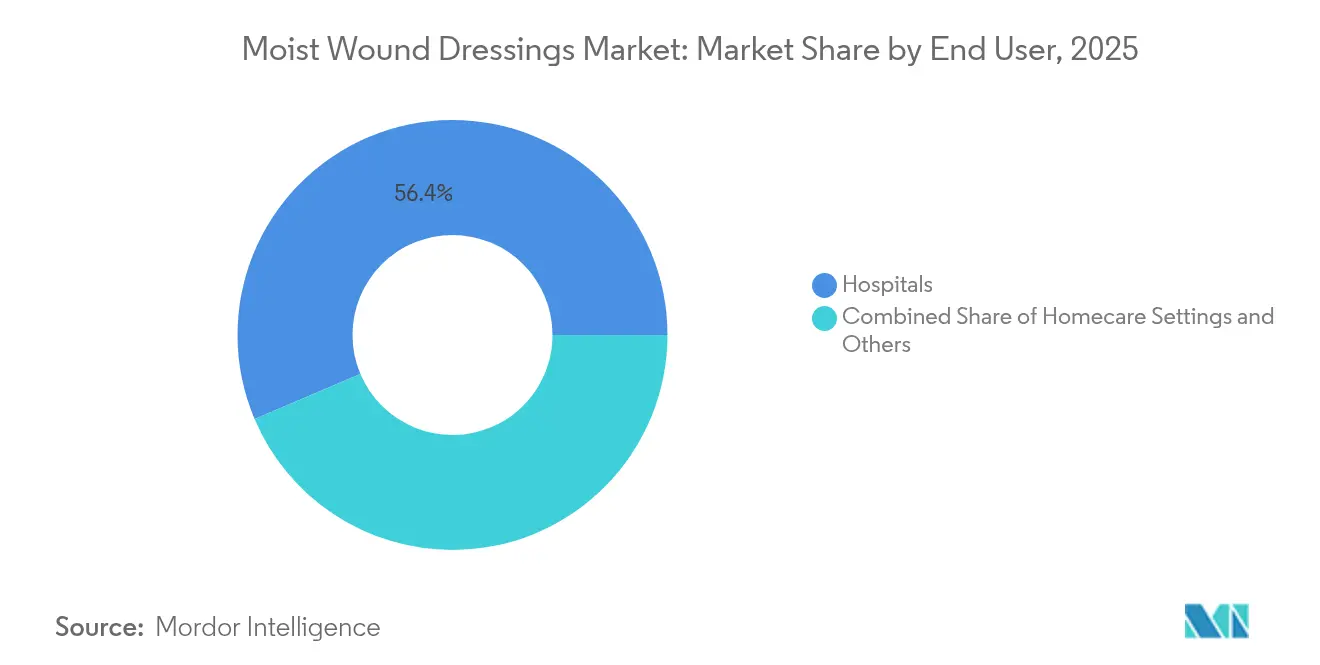

- By end user: Hospitals held 56.38% revenue share in 2025, yet homecare settings record the highest forecast CAGR at 6.49% to 2031.

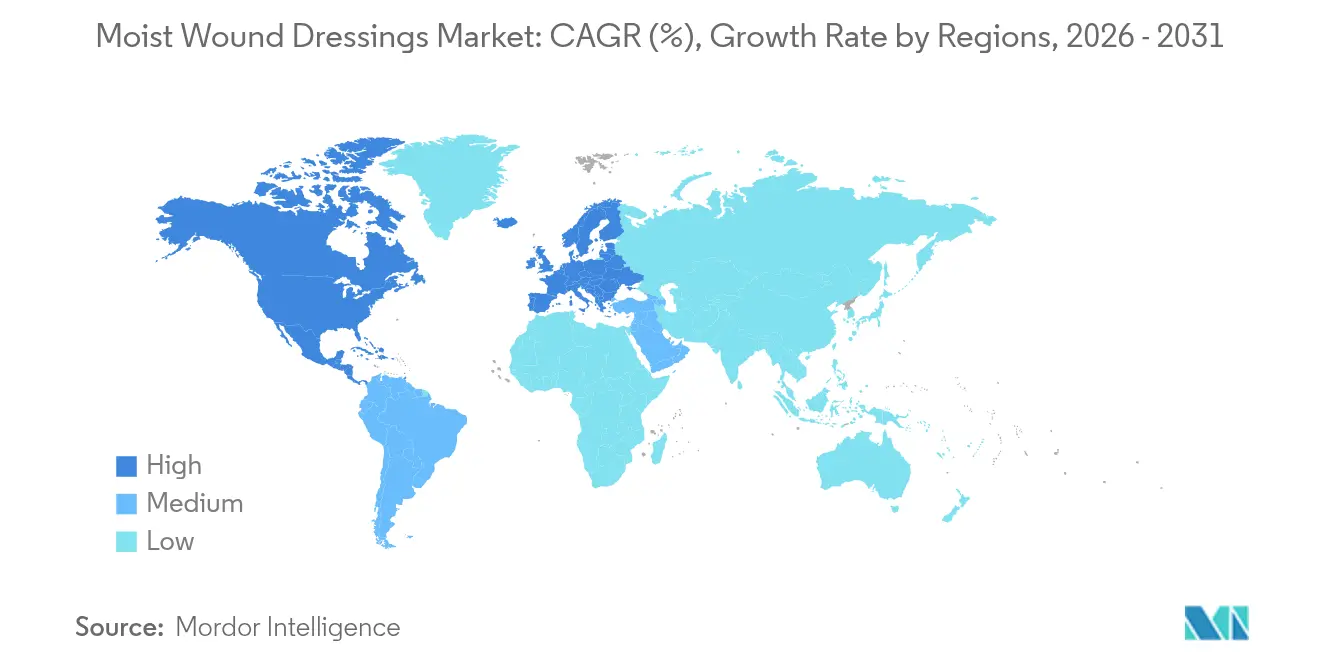

- By geography: North America captured 43.41% of the moist wound dressings market in 2025; Asia-Pacific is poised to expand at 6.78% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Moist Wound Dressings Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of chronic & acute wounds | +1.1% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Growing geriatric population & diabetes prevalence | +1.4% | Global, highest impact in Asia-Pacific | Long term (≥ 4 years) |

| Accelerating adoption of home-based chronic-wound management | +0.6% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Favorable reimbursement reforms in OECD outpatient settings | +0.7% | North America & Europe | Medium term (2-4 years) |

| Rise of smart-sensor dressings enabling tele-monitoring | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Climate-linked uptick in burn & trauma cases | +0.3% | Global, seasonal variations by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Chronic & Acute Wounds

Roughly 6.7 million Americans live with a chronic wound, a population expected to climb as peripheral arterial disease, obesity, and diabetes intersect with older age. The American Heart Association noted in 2024 that diabetic foot ulcer patients face a >25% lifetime risk and a 70% five-year post-amputation mortality rate [1]John Doe, “Diabetic Foot Ulcer: Lifetime Risks and Outcomes,” American Heart Association, ahajournals.org. Such statistics are steering providers toward early use of advanced moist dressings that shorten healing cycles and curb readmissions. Hospital cost modeling in the European Union shows diabetic foot ulcer admissions averaging EUR 4,888 (USD 5,308) per patient, with 88% of costs tied to prolonged stays. Payers therefore view moisture-retentive protocols not as optional extras but as cost-avoidance tools.

Growing Geriatric Population & Diabetes Prevalence

Asia-Pacific adds more than 45 million individuals aged ≥65 each year, and many also live with diabetes, peripheral neuropathy, or vascular insufficiency. Scientific Reports found that 44.4% of diabetes patients developed neuropathy, 21.7% underwent amputations, and 96.9% reported poor quality of life [2]Jane Smith, “Smart Bandages with pH-Responsive Hydrogels,” Nature, nature.com . Hyperglycemia triggers oxidative stress and macrophage imbalance, slowing natural closure phases. Advanced moist dressings address such biological hurdles by preserving endogenous growth factors and optimizing exudate management, making them first-line therapy in many specialty clinics.

Favorable Reimbursement Reforms in OECD Outpatient Settings

The Centers for Medicare & Medicaid Services (CMS) introduced caregiver training codes G0541 and G0542 in its 2025 Outpatient Prospective Payment System rule, letting clinicians bill for remote wound-care instruction. CMS also expanded coverage for cellular tissue-based products from four to eight applications across 16 weeks when specific criteria are met [3]Centers for Medicare & Medicaid Services, “CY 2025 OPPS Final Rule,” CMS, cms.gov. Private payers followed suit; Organogenesis now reports access under 1,500 commercial plans covering 90% of U.S. lives. Such reimbursement breadth encourages clinicians to adopt premium dressings with proven efficacy, reinforcing value-based purchasing.

Rise of Smart-Sensor Dressings Enabling Tele-Monitoring

Caltech’s iCares smart bandage continuously samples wound fluid and flags infection-related biomarkers up to 24 hours before visible symptoms, reducing unnecessary clinic visits. The FDA cleared Microlyte Ag/Lidocaine, the first antimicrobial dressing containing lidocaine for pain relief, highlighting regulatory acceptance of multifunctional platforms. Academic prototypes combining pH-responsive hydrogels with Bluetooth patches achieved 30% faster closure than gauze in a 2024 Nature study. As hospital systems push digital care models, manufacturers that merge moisture control with real-time analytics stand to differentiate in the moist wound dressings market.

Restraints Impact Analysis of Moist Wound Dressings Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product & procedure cost | -0.7% | Global, particularly emerging markets | Medium term (2-4 years) |

| Limited reimbursement in emerging economies | -0.5% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Infection risk from improper moist-dressing usage | -0.3% | Global, higher in resource-limited settings | Medium term (2-4 years) |

| Stricter eco-toxicity rules on silver dressings | -0.2% | Europe, North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product & Procedure Cost

In Spain, chronic wound care consumed EUR 34,991,854 (USD 38,057,000) in primary care over three years, with materials alone costing EUR 8,455,787 (USD 9,203,000) and clinician time making up the remainder. Multiple dressing changes per week compound expenses for payers and patients. Similar patterns appear in India, where diabetic foot ulcer treatment is often paid out of pocket, shrinking access to advanced dressings. Tiered product ranges and smaller pack sizes aim to bridge price gaps but risk commoditizing innovations.

Limited Reimbursement in Emerging Economies

Advanced wound care adoption in many low- and middle-income countries is hampered by limited national insurance coverage, prioritization of communicable diseases, and a scarcity of wound-care specialists. Although Asia-Pacific contains large diabetic populations, only a fraction of public hospitals routinely stock hydrocolloids or hydrogels. Over the forecast period, economic growth and donor-supported universal health schemes could unlock latent demand, yet reimbursement gaps remain a near-term drag on the moist wound dressings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Moist Wound Dressings Market Segment Analysis

By Product:

Foam Leadership Meets Hydrocolloid InnovationFoam dressings accounted for 23.54% of moist wound dressings market share in 2025, reflecting their broad applicability across postoperative, pressure, and trauma wounds. Their polyurethane matrix balances high absorption with thermal insulation, reducing dressing changes and protecting peri-wound skin. Technological upgrades, such as Smith+Nephew’s ALLEVYN Ag+ SURGICAL, which combines silver ions with a flexible trilaminate, strengthen clinical appeal. Hydrocolloid formats, although smaller in today’s revenue terms, display the fastest 5.93% CAGR. High gel-forming capacity and seven-day wear time make hydrocolloids an increasingly preferred preventive measure for pressure injury in immobile patients, particularly in homecare. The FDA’s streamlined 510(k) exemption for hydrocolloid formulations lowers entry barriers and sparks niche players to innovate on odor control, transparency, and biodegradability.

Over 2026-2031, alginate and hydrogel categories are expected to carve distinct roles rather than challenge foam outright. Alginate’s calcium-sodium ion exchange underpins hemostatic performance in profusely exuding wounds, ensuring it remains indispensable in emergency departments. Hydrogel sheets, prized for cooling analgesic effects, dominate oncology-related radiation burns and necrotic tissue debridement. Film, contact-layer, and composite dressings retain niche status but gain renewed attention as sensor backings for smart platforms. Together these dynamics reinforce a multi-product portfolio imperative for firms seeking durable positions in the moist wound dressings market.

By Application:

Surgical Dominance Yields to Diabetic ExpansionPost-operative and traumatic wounds generated 36.21% of 2025 revenue, evidencing surgeons’ near-universal preference for moisture-retentive coverings that lower seroma formation and minimize hypertrophic scarring. Protocol standardization, often embedded in enhanced recovery pathways, supports predictable order volumes from acute care hospitals. However, diabetic foot ulcers will see the briskest 6.27% CAGR through 2031, as population-level diabetes prevalence surpasses 10% in several G20 economies. Multidisciplinary foot clinics increasingly adopt hydrofiber-foam hybrids and oxygen-permeable hydrocolloids to curb amputation incidence, transforming a once episodic procurement pattern into steady demand.

Pressure ulcer prophylaxis represents another sizable slice, fueled by mandatory reporting of hospital-acquired pressure injuries and associated reimbursement penalties. Venous leg ulcer therapy, while smaller, receives momentum from guidelines calling for compression-compatible moist dressings that accelerate epithelial resurfacing. Burn units and plastic surgery departments continue exploring copper- and chitosan-laden variants that shorten donor-site healing by an estimated two days. These divergent application pathways ensure that no single dressing type meets all clinical scenarios, perpetuating innovation cycles and reinforcing competitive breadth within the moist wound dressings market.

By End User:

Hospital Infrastructure Supports Homecare TransitionHospitals captured 56.38% of the moist wound dressings market in 2025 owing to centralized purchasing, dedicated wound care teams, and immediate access to advanced therapies. In-patient settings remain the testing ground for smart dressings that link with electronic health records and deliver data on exudate pH or protease activity. Yet hospitals increasingly discharge stable patients earlier to lower costs, shifting responsibilities toward community nurses and family caregivers. CMS caregiver training reimbursement, coupled with proliferation of telehealth platforms, empowers non-specialists to maintain sophisticated dressing regimens at home.

Homecare is forecast to post a 6.49% CAGR, outpacing all other venues. Adoption hinges on simplified “peel-and-seal” formats, integrated change indicators, and video-assisted application guides. Long-term care facilities also show emerging appetite for moisture-retentive prophylactics that cut pressure ulcer incidence, aligning with regulatory quality metrics. Ambulatory wound clinics, often embedded in retail pharmacies, provide convenience for follow-up debridement and enable subscription-based dressing supply programs. Overall, end-user diversification diffuses purchasing power and compels manufacturers to tailor packaging, education tools, and supply-chain logistics to disparate care environments within the moist wound dressings market.

Geography Analysis

North America Moist Wound Dressings Market

North America remains the epicenter of technological and reimbursement evolution. The region’s payer mix, Medicare, commercial insurers, and the Veterans Health Administration, collectively drives rapid diffusion of clinically proven products. Providers increasingly deploy remote monitoring kits that bundle foam dressings with smartphone-linked pH sensors, enabling same-day intervention when inflammation spikes. Cross-border supply chains are resilient due to the United States-Mexico-Canada Agreement, though manufacturers are localizing production to mitigate tariff and freight volatility.

APAC Moist Wound Dressings Market

Asia-Pacific’s trajectory reflects a convergence of epidemiology and policy. China’s Healthy China 2030 plan earmarks funds for chronic disease prevention, channeling investment into diabetic foot clinics where hydrofiber dressings cut debridement frequency. In India, state-level health insurance schemes reimburse advanced dressings for low-income patients undergoing limb-salvage surgery, stimulating public-sector tenders. Japanese and South Korean markets focus on pressure-injury prevention in super-aged populations, fostering adoption of silicone-foam prophylactics designed to remain intact during MRI scans.

Broader European Markets

Europe exhibits nuanced growth. Northern European health systems emphasize home-based care, prompting high uptake of antimicrobial foams with twelve-day wear protocols that minimize nurse visits. Southern Europe’s constrained public budgets favor cost-effectiveness studies; recent NHS England real-world data showed a 19% reduction in weekly dressing changes when switching from plain gauze to hydrocolloid, saving USD 1.7 million annually. East European accession to common procurement procedures brings price harmonization but also intensifies competition from Asia-Pacific suppliers, pressuring local incumbents to differentiate through sustainability certifications and recyclable packaging.

Regulatory Landscape

Moist wound dressings are regulated primarily as medical devices, with classification and controls varying by material composition and whether the product incorporates antimicrobial or other active components. In the United States, the FDA framework spans Class I dressings that may be 510(k)-exempt when they do not contain added drug/biologic/animal-derived components, and higher-risk products routed through Class II controls and premarket submissions when they incorporate antimicrobial or chemically active features. A key compliance shift occurred when the FDA Quality Management System Regulation (QMSR) became effective on February 2, 2026, aligning 21 CFR Part 820 with ISO 13485:2016 requirements and changing how manufacturers document quality systems across design, production, and postmarket controls.

In Europe, Regulation (EU) 2017/745 (MDR) continues to govern wound dressing access, tightening clinical evidence expectations and post-market clinical follow-up for many dressing categories, particularly substance-based and functionally active products. This raises the importance of technical documentation, clinical evaluation, and vigilance reporting across multinational portfolios, and pushes suppliers to standardize evidence generation and quality systems to support both MDR and FDA requirements.

Value Chain Analysis

The moist wound dressings value chain begins with specialized raw materials, including polymers and elastomers, hydrocolloid/hydrofiber constituents such as carboxymethyl cellulose, and absorbent substrates and films, followed by conversion and assembly steps such as coating, lamination, hot-melt adhesive application, and sterilization (often irradiation) before packaging and release. Product performance and regulatory readiness are closely tied to upstream material specifications (for absorbency, adhesion, and antimicrobial performance where applicable) and validated manufacturing controls that sustain sterility assurance and consistent wear-time behavior across batches.

Commercial distribution runs through a mix of direct sales and healthcare distribution networks, with hospital systems and group purchasing organizations (GPOs) playing a central role in formulary access, standardization, and tender-driven pricing. Procurement increasingly favors suppliers that can provide broad category coverage across foams, hydrocolloids, alginates, hydrogels, films, and antimicrobial variants, along with clinical support and continuity of supply. This structure elevates the importance of packaging and logistics capability for sterile, single-use products, and places additional emphasis on compliance infrastructure as US and EU requirements raise documentation and validation expectations for advanced and antimicrobial-containing dressings.

Competitive Landscape

The moist wound dressings market supports a mid-tier concentration profile characterized by diversified portfolios and region-specific strengths. Smith+Nephew, Mölnlycke, 3M (under spin-off Solventum), ConvaTec, and Coloplast collectively hold an estimated 60% of global revenue, leveraging proprietary foams, hydrofibers, and silicone adhesives. R&D pipelines emphasize multifunctionality; examples include Mölnlycke’s Mepilex Border Flex Plus, which integrates Flex Technology for conformability and Safetac silicone for atraumatic removal, and ConvaTec’s Aquacel Ag + Extra, combining ionic silver with Hydrofiber gelling.

Strategic moves frequently pair acquisition with technology cross-pollination. Coloplast’s 2024 purchase of Kerecis injected fish-skin xenograft know-how into its dressing portfolio, opening an entry into biologics. 3M’s Solventum division is piloting carbon-nanotube-embedded sensors that transmit exudate viscosity data to clinicians, aiming for FDA De Novo clearance in 2026. Meanwhile, regional players such as HARTMANN strengthen European presence through evidence-based marketing.

Start-ups and academic spin-offs intensify innovation pressure. U.S.-based Swift Medical offers a computer-vision platform that quantifies wound size and suggests dressing types, partnering with foam manufacturers for integrated care bundles. Singapore’s WoundMaestro develops enzymatic hydrogels that release antimicrobial peptides in response to pH shifts, targeting Southeast Asian diabetic populations. Collectively, these entrants prompt incumbents to accelerate digital integration, sustainability initiatives, and clinical validation, maintaining a dynamic competitive equilibrium in the moist wound dressings market.

Moist Wound Dressings Industry Leaders

Fleming Medical Ltd

Smith & Nephew plc

Essity AB

DermaRite Industries LLC

AMERX Health Care Corporation

- *Disclaimer: Major Players sorted in no particular order

Moist Wound Dressings Market Companies Covered in this Report

- Smiths Group

- Molnlycke Health Care

- 3M (Health Care)

- Convatec

- Coloplast

- Essity AB (BSN medical)

- Cardinal Health

- B. Braun

- Medtronic plc (Acelity/KCI)

- Johnson & Johnson

- Lohmann & Rauscher GmbH

- Hartmann Group

- Urgo Medical

- Hollister

- Integra LifeSciences

- DermaRite Industries

- AMERX Health Care Corp.

- Fleming Medical Ltd.

- Derma Sciences (Nipro)

- Milliken Healthcare

Market Opportunities and Future Outlook

A clear whitespace is emerging around dressings that combine moist healing with measurable, decision-support functionality in decentralized care, especially where payers and providers are shifting chronic wound management toward the home. CMS introduced caregiver training codes G0541 and G0542 in its 2025 Outpatient Prospective Payment System rule, supporting reimbursable education for remote wound-care instruction and reinforcing demand for easier-to-apply formats, guided workflows, and monitoring-compatible dressings. Within product strategy, manufacturers have room to pair high-volume foam and hydrocolloid platforms with sensor backings or indicators that fit telehealth protocols, building differentiation beyond basic moisture retention.

Regulatory tightening also creates opportunity for manufacturers that can meet higher evidence and quality bars while simplifying cross-market compliance. The FDA QMSR effective February 2, 2026, which incorporates ISO 13485:2016, supports a more harmonized quality-system approach for firms operating across the United States and MDR-regulated European markets. At the same time, the proposed FDA approach to classifying currently unclassified wound dressings based on antimicrobial resistance (AMR) risk highlights an opening for validated antimicrobial alternatives, optimized silver use, and non-antibiotic antimicrobial mechanisms that can satisfy special controls and postmarket expectations. On the provider side, guideline-led, evidence-based dressing selection, reinforced by NHS trust guidance and EWMA clinical consensus, elevates demand for products supported by comparative outcomes data and clear use criteria rather than broad, one-size-fits-all claims.

Recent Industry Developments in Moist Wound Dressings Market

- March 2026: Smith+Nephew launched the next-generation ALLEVYN COMPLETE CARE foam dressing in the United States. The launch expanded the company\'s advanced foam portfolio for chronic wounds and supported premiumization as providers move toward moisture-retentive and prevention-focused protocols.

- September 2025: Smith+Nephew extended its advanced wound bioactives offering in the United States with the CENTRIO platelet-rich plasma (PRP) system. While distinct from routine dressings, the addition strengthens bundled wound-care propositions in settings that combine dressings with adjunctive therapies and can influence vendor selection within hospital and outpatient wound programs.

- April 2024: Smith+Nephew announced a multi-hospital pilot program with NHS trusts to evaluate integrated wound-care pathways leveraging ALLEVYN dressings and related therapy devices, advancing evidence generation for home and facility-based care.

Moist Wound Dressings Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers sterile dressings designed to maintain a moist wound environment, manage exudate, and support tissue repair in acute and chronic wounds across care settings.

Scope exclusions: Traditional dry gauze, negative-pressure wound therapy devices, and bioengineered skin substitutes are excluded from this sizing.

Segments Covered in This Report

- By Product

- Foam Dressings

- Alginate Dressings

- Hydrocolloid Dressings

- Hydrogel Dressings

- Film Dressings

- Collagen Dressings

- Antimicrobial/Silver Dressings

- Contact-Layer Dressings

- Others

- By Application

- Burn Wounds

- Pressure Ulcers

- Diabetic Foot Ulcers

- Surgical / Traumatic Wounds

- Venous Leg Ulcers

- Other Applications

- By End User

- Hospitals

- Homecare Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and commercial boundaries and to build starting inputs that could be checked later in interviews. We mainly referenced public sources such as the US FDA device databases, the US CDC burden indicators for diabetes and chronic wounds, CMS and other public reimbursement references, OECD health statistics, and peer-reviewed wound care journals that discuss dressing usage and healing pathways.

To connect demand signals to revenues, we also reviewed company filings and investor decks for product mix clues, plus association and hospital procurement webpages where dressing types and protocols are described. For pricing and trade related checks, we used an import/export shipment-level database and a company financials and intelligence subscription to confirm manufacturer presence, category exposure, and directional pricing movements. These desk sources are illustrative only, and many other public references were also reviewed to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work was used to pressure test the dressing scope, average selling price ranges, and how usage shifts by wound type and care setting, which often cannot be cleanly read from public sources. We spoke with manufacturers, distributors, clinicians, and procurement stakeholders across APAC, EMEA, and the Americas so assumptions on volumes, formulary adoption, and the channel mix could be adjusted, then rechecked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 45% |

| Mid tier: 49% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 15% | Managers: 57% | Americas: 26% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand pool build that ties wound prevalence and treated population to dressing utilization, and then converts expected unit use into value through country level pricing logic. Where the math had to be made practical, the model was corroborated with selective bottom-up approximations such as sampled ASP multiplied by estimated consumption in key care settings, distributor channel checks, and supplier presence roll ups to keep totals realistic.

Inputs were selected because they are observable and repeatable, even when perfect data is not available. The key variables include chronic wound and diabetes burden indicators, surgical procedure volumes, outpatient and homecare penetration for wound management, reimbursement coverage changes that influence product selection, and ASP progression by dressing class (for example foam versus hydrocolloid versus alginate). In countries where unit volumes were harder to observe, gaps were handled by using proxy utilization rates from comparable health systems and then scaling by population and care setting mix, before being revisited in follow-up calls.

For forecasting, scenario analysis was used around the main demand drivers, and the trend lines were tuned with expert consensus on adoption speed and pricing, which is where short-term volatility tends to appear. Currency conversion was kept consistent year by year to avoid overstating growth driven only by FX movements.

Data Validation & Update Cycle

Validation is done in layers so one weak assumption does not drive the final number. Analysts compare the modeled totals with independent signals such as procedure trends, reimbursement updates, and the expected split of advanced dressings within overall wound care spend, and then any large variances are investigated before sign-off.

When a mismatch is seen, we re-check the unit assumptions, pricing ranges, and the country mix, and interview follow-ups are triggered if the issue is material. Reports are refreshed annually, and interim updates are made when major events occur, such as policy shifts or large pricing moves. Before delivery, a final review pass is completed so clients receive the latest updated view based on the newest available inputs.

Mordor Intelligence's Moist Wound Dressings Market Size Compared With Other Published Estimates

Published market values for moist wound dressings can look different across sources, even when they sound like they cover the same topic. The gaps usually come from timing of currency conversion, how price averages are built, and whether the scope is limited to moist dressings or expands into adjacent wound care categories.

In this study, the biggest spread is typically explained by how frequently assumptions are refreshed and how price progression is validated, because hospital contracts and reimbursement shifts can change realized ASPs quickly. This point is handled through an annual refresh cadence and year-specific FX timing in the model used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.05 B (2025) | |

| Trade Publisher A | USD 4.91 B (2025) | Uses a manufacturer revenue framing and a short historic-to-forecast step, which can undercount channel markups and local pricing differences when converting to consumption value. |

| Industry Publisher B | USD 5.50 B (2025) | Includes a broader product basket and applies higher average pricing across dressing classes, which can lift totals if premium mix assumptions are not rechecked by care setting. |

The table shows that the range is mainly driven by scope boundaries and the way prices and currency are handled for the same year. By keeping inclusions explicit and tying ASP and volume assumptions back to observable care setting and wound burden signals, our estimate stays traceable and easier to replicate when inputs are updated.

Key Questions Answered in the Report

How big is the Moist Wound Dressings Market?

The Moist Wound Dressings Market size is expected to reach USD 5.31 billion in 2026 and grow at a CAGR of 5.24% to reach USD 6.86 billion by 2031.

Why are diabetic foot ulcers a high-growth application?

Rising diabetes prevalence and guideline-driven focus on limb preservation propel diabetic foot ulcer dressings at a 6.27% CAGR.

Who are the key players in Moist Wound Dressings Market?

Fleming Medical Ltd, Smith & Nephew plc, Essity AB, DermaRite Industries LLC and AMERX Health Care Corporation are the major companies operating in the Moist Wound Dressings Market.

Which is the fastest growing region in Moist Wound Dressings Market?

Asia-Pacific leads regional growth at 6.78% CAGR, driven by expanding healthcare infrastructure and increasing chronic wound incidence.

Which region has the biggest share in Moist Wound Dressings Market?

In 2025, the North America accounts for the largest market share in Moist Wound Dressings Market.

Which product category leads the market?

Foam dressings hold the leading 23.54% share, favored for versatility and high absorption.

Page last updated on: