Wound Dressings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

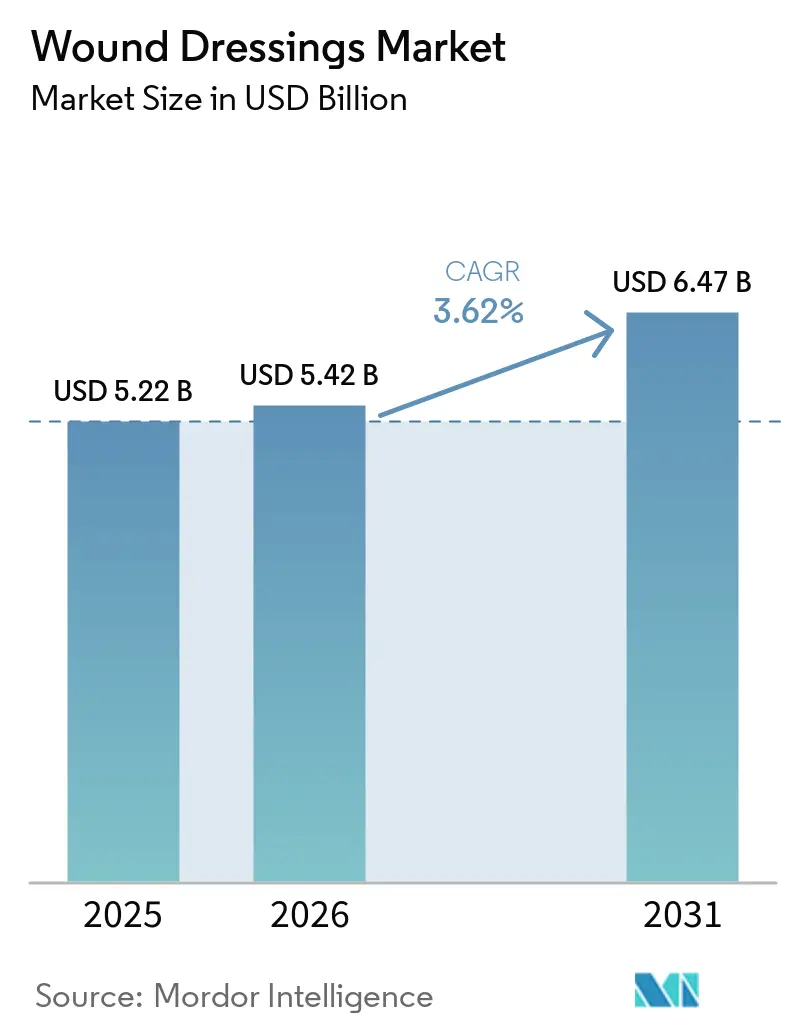

| Market Size (2026) | USD 5.42 Billion |

| Market Size (2031) | USD 6.47 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wound Dressings Market Analysis by Mordor Intelligence

The Wound Dressings Market size is expected to grow from USD 5.22 billion in 2025 to USD 5.42 billion in 2026 and is forecast to reach USD 6.47 billion by 2031 at 3.62% CAGR over 2026-2031.

Advanced products dominate the revenue mix but price-sensitive procurement programs in low- and middle-income countries are funneling volume toward traditional gauze, cotton rolls, and bandages. Demographic aging, a worldwide diabetes surge, and post-pandemic telehealth normalization are expanding demand for chronic-wound solutions that can be managed in non-hospital settings. Reimbursement reforms, especially the 2024 U.S. decision to grant separate payment for disposable negative-pressure wound therapy, are channeling investment into single-use NPWT and sensor-integrated platforms. Meanwhile, Europe’s hospital decarbonization mandates are nudging buyers toward bio-derived and compostable dressings that lower waste footprints.

Key Report Takeaways

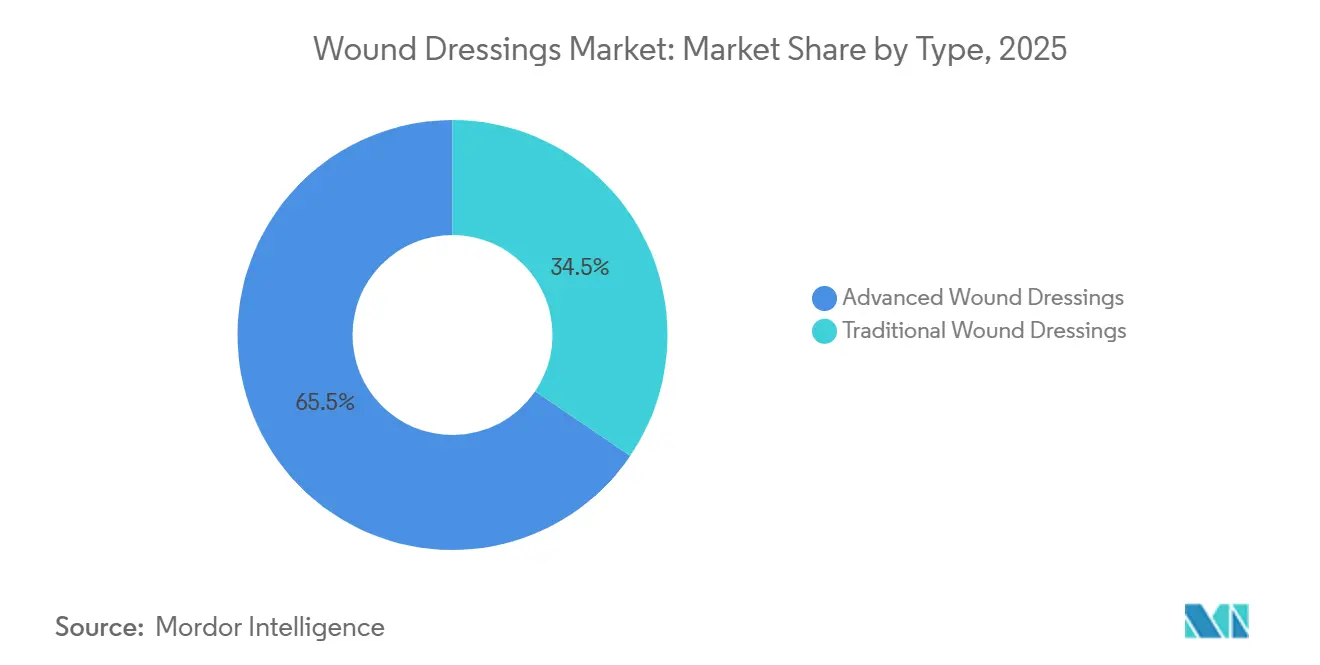

- By type, advanced dressings led with 65.55% of wound dressings market share in 2025. Traditional dressings are projected to expand at a 5.25% CAGR to 2031.

- By application, surgical and traumatic wounds commanded 35.53% of the wound dressings market size in 2025, while diabetic foot ulcers record the fastest growth at 4.85% CAGR through 2031.

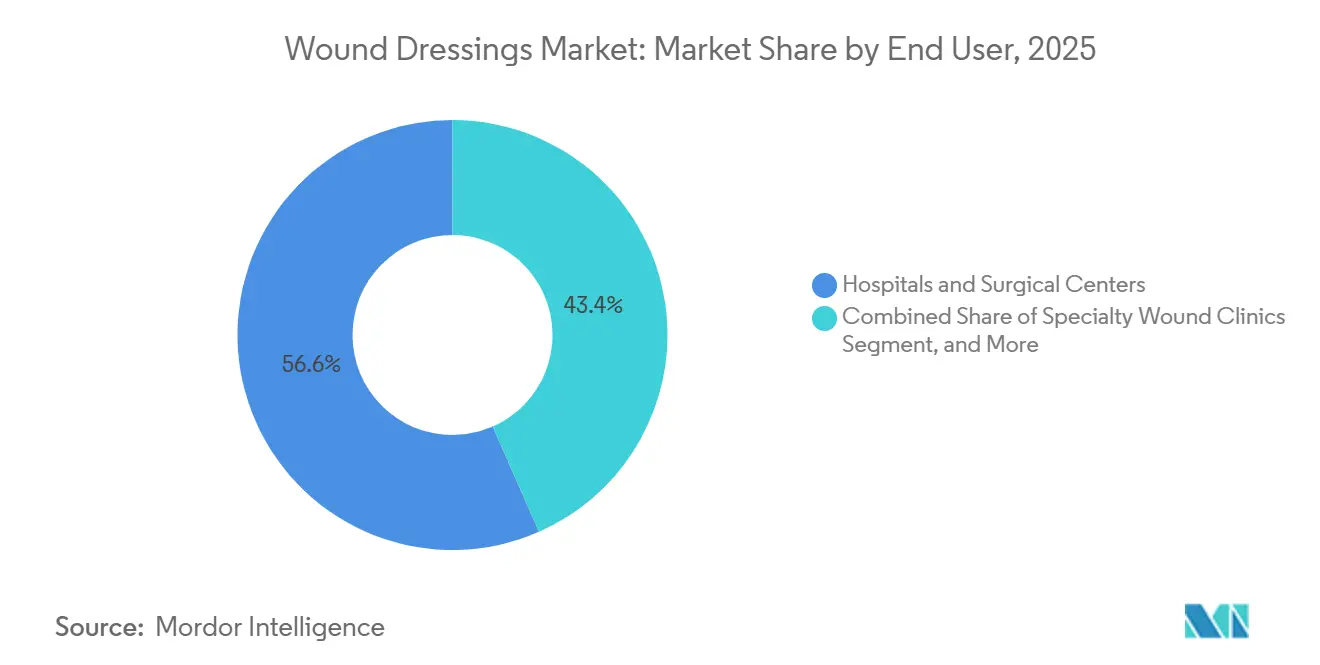

- By end user, hospitals and surgical centers held 56.63% revenue in 2025; home healthcare, however, is advancing at 4.17% CAGR to 2031.

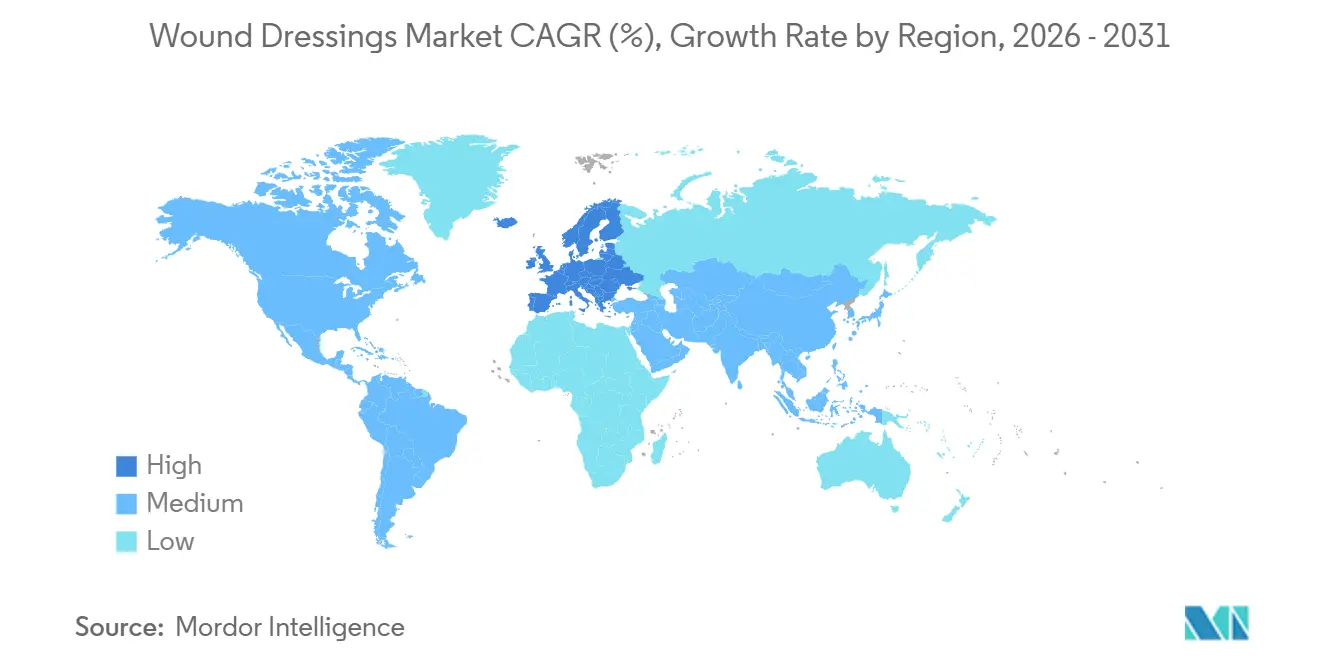

- By geography, North America captured 45.13% share in 2025; Europe registers the fastest regional CAGR at 4.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wound Dressings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic wounds & diabetic ulcers | +1.2% | Global, concentrated in North America, Europe, Asia-Pacific (China, India) | Long term (≥ 4 years) |

| Escalating volume of surgical procedures worldwide | +0.9% | Global, with higher intensity in North America, Europe, emerging surgical hubs in Asia-Pacific | Medium term (2-4 years) |

| Technological shift toward moist-active & NPWT-integrated dressings | +0.8% | North America, Europe, Australia, Japan | Medium term (2-4 years) |

| Expanding reimbursement for home-based wound care in OECD nations | +0.6% | North America (U.S., Canada), Europe (Germany, UK, France), Japan | Short term (≤ 2 years) |

| Hospital decarbonization targets favoring bio-derived & compostable dressings | +0.3% | Europe (NHS, EU hospitals), select North American health systems | Long term (≥ 4 years) |

| Smart dressings enabling tele-wound-care billing & remote dosing algorithms | +0.4% | North America, Europe, early adoption in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Wounds & Diabetic Ulcers

Global diabetes prevalence hit 828 million adults in 2022 and is projected to reach 1.31 billion by 2050, triggering an upsurge in chronic wounds that strain health-system capacity. Between 19% and 34% of people with diabetes develop foot ulcers over their lifetime, and up to 24% of those cases progress to amputation[1]International Working Group on the Diabetic Foot, “IWGDF Guidelines 2023,” iwgdfguidelines.org. Moisture-retentive hydrocolloids, antibacterial silver foams, and collagen matrices are increasingly adopted to accelerate granulation, but cost barriers persist in resource-limited regions. Multidisciplinary foot-care teams recommended by the American Diabetes Association have gained traction in OECD countries, yet clinician shortages and low health literacy impede replication elsewhere. As a result, diabetic ulcer management is emerging as the primary growth engine of the wound dressings market.

Escalating Volume of Surgical Procedures Worldwide

More than 300 million surgeries are performed each year, and surgical site infections continue to complicate up to 11% of cases in low-resource settings[2]Centers for Disease Control and Prevention, “Surgical Site Infection (SSI),” cdc.gov . High-risk procedures such as joint replacements and cardiac bypass increasingly rely on prophylactic single-use NPWT systems that reduce edema and bacterial contamination. Devices like Smith & Nephew’s PICO and Solventum’s Prevena earned FDA clearances in 2024–2025, underscoring regulatory confidence in miniaturized pump formats. Conversely, the majority of clean, low-risk wounds in emerging economies are still managed with gauze due to budget ceilings, sustaining dual-track product demand within the wound dressings market.

Technological Shift Toward Moist-Active & NPWT-Integrated Dressings

Disposable NPWT has migrated from inpatient vacuum systems to lightweight, battery-powered devices used at home, removing logistical barriers that once limited adoption. CMS created a separate payment pathway for single-use NPWT in January 2024, catalyzing uptake in community settings and tele-nursing programs. Smart dressings embedding pH, temperature, and bacterial sensors now transmit real-time data via Bluetooth, allowing clinicians to titrate antimicrobials remotely. Broader scale-up hinges on interoperability with hospital electronic health records and regulatory clearance of the embedded software under FDA SaMD rules.

Expanding Reimbursement for Home-Based Wound Care in OECD Nations

Aging populations are fueling a policy swing toward home care. Nearly 21% of Europeans were aged 65+ in 2023, and that share will approach 30% by 2050. CMS remote-patient-monitoring codes 99453, 99454, 99457, and 99458 reimburse tele-wound-care activities worth USD 100-150 per patient each month, sparking rapid deployment of connected dressings in the United States. Germany, France, and Japan have introduced diagnosis-related group or fee-for-service adjustments that partially mirror U.S. incentives, though coverage heterogeneity inside Europe hampers pan-regional scale. Collectively, these payment reforms support decentralization and lift the growth curve of the wound dressings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price-premium over traditional dressings | -0.7% | Global, most acute in Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Limited clinician & patient awareness in emerging economies | -0.4% | Asia-Pacific (excluding Japan, Australia), Middle East & Africa, South America | Long term (≥ 4 years) |

| Regulatory scrutiny on cumulative silver-ion exposure | -0.2% | North America, Europe | Short term (≤ 2 years) |

| Volatile supply of marine & crustacean biopolymers due to aquaculture disease outbreaks | -0.3% | Global, supply chains concentrated in Asia-Pacific (China, Thailand, Vietnam) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price-Premium Over Traditional Dressings

Advanced foams, hydrocolloids, and NPWT devices cost five to twenty times more than basic gauze, a differential that blocks uptake in publicly funded hospitals across Asia, Africa, and Latin America. The WHO Essential Medicines List continues to recommend gauze and bandages, reinforcing low-cost procurement preferences. Bulk purchasing contracts that bundle wound products with surgical supplies further steer budgets toward traditional dressings, fueling a growth rate that already exceeds the overall wound dressings market trajectory.

Limited Clinician & Patient Awareness in Emerging Economies

Fewer than 20% of primary-care physicians in India and Indonesia receive formal training in advanced wound management, according to a 2024 survey published in Wound Repair and Regeneration. Patient education is similarly sparse; many individuals with diabetic foot ulcers present only when infection or gangrene is advanced, limiting the therapeutic window for premium dressings. Company-run workshops rarely penetrate rural health centers, perpetuating low adoption even where products are commercially available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Advanced Dominance Meets Traditional Acceleration

Advanced dressings accounted for 65.55% of wound dressings market revenue in 2025, anchored by foam, hydrocolloid, and silver platforms widely used in chronic-wound clinics. Foams and hydrocolloids thrive on versatility, handling everything from pressure ulcers to post-surgical incisions. Antimicrobial formats harness silver, iodine, or PHMB, but tightening stewardship policies could soften growth. Smart sensor-enabled dressings remain in pilot phases pending FDA software validation, while alginate, collagen, and super-absorbent materials occupy niche positions addressing highly exudative or regenerating tissues.

Traditional dressings, despite lower value capture, are growing at 5.25% CAGR through 2031, well above the wound dressings market average, as governments in India, Nigeria, and Indonesia scale mass-procurement of gauze for primary-care and emergency stockpiles. Disaster relief protocols also favor gauze for scalability and shelf stability. The widening price gap sustains a dual-speed landscape: advanced innovations push clinical outcomes in high-income settings, while basic products retain primacy wherever cost ceilings prevail.

By Application: Surgical Wounds Lead; Diabetic Foot Ulcers Accelerate

Surgical and traumatic wounds captured 35.53% of the wound dressings market size in 2025, buoyed by more than 300 million annual operations worldwide and persistent infection risks that demand robust post-operative care. Negative-pressure systems paired with antimicrobial foams are becoming standard for orthopedic and cardiothoracic incisions in high-income countries. Yet cost-driven protocols in emerging regions frequently default to gauze, limiting premium penetration.

Diabetic foot ulcers are the fastest-growing application, advancing at 4.85% CAGR through 2031, as global diabetes prevalence climbs toward 1.31 billion cases by 2050. Chronicity, high exudate loads, and infection propensity necessitate moisture-retentive, antibacterial, and bioactive dressings, elevating average revenue per case. Nevertheless, reimbursement gaps in many low-resource settings restrain adoption, reinforcing a two-tier delivery pattern inside the wound dressings industry.

By End User: Hospitals Dominate, Home Healthcare Gains Momentum

Hospitals and surgical centers controlled 56.63% of 2025 revenue, reflecting deep inventories, bulk contracts, and clinical expertise. Integrated care pathways for complex wounds, operating theater proximity, and access to advanced devices reinforce hospital primacy. Specialty outpatient clinics act as transitional hubs, often deploying NPWT or enzymatic debridement before handoff to community nurses.

Home healthcare exhibits a 4.17% CAGR through 2031, driven by aging demographics and reimbursement incentives that compensate remote monitoring and disposable NPWT. User-friendly dressing kits, adhesive sensors, and tele-consult platforms underpin this shift, positioning companies with caregiver-oriented product lines to capture incremental share in the wound dressings market.

Geography Analysis

North America retains leadership with 45.13% share in 2025, propelled by Medicare coverage, high per-capita spending, and mature specialty-wound networks. The prevalence of diabetes, exceeding 37 million adults in the United States, together with 17.3% of the population aged 65+ in 2023, sustains a heavy chronic-wound caseload. Market growth in the region is moderated by value-based purchasing models that pressure suppliers to prove outcome parity at lower cost.

Europe posts the fastest regional CAGR at 4.51% to 2031, supported by 500-plus specialized wound centers in Germany, net-zero procurement mandates under the Greener NHS framework, and extensive home-care reimbursement in France and the Nordics. The continent’s 65-plus cohort will reach nearly 30% by 2050, guaranteeing chronic-wound demand expansion. Regulatory heterogeneity across member states complicates portfolio rollouts yet offers scope for localization strategies.

Asia-Pacific, Middle East & Africa, and South America represent the steepest volume growth, led by rising surgical counts and the world’s largest diabetes cohorts in China and India. Procurement remains dominated by traditional dressings, but tier-one urban hospitals are piloting NPWT and hydrocolloids, setting an adoption runway as purchasing power improves. Companies able to navigate divergent approval pathways and price thresholds stand to gain an incremental slice of the wound dressings market.

Competitive Landscape

The wound dressings industry is moderately fragmented. Market leaders Smith & Nephew, Solventum, Mölnlycke, ConvaTec, and Coloplast leverage established channels and regulatory fluency to defend hospital contracts[3]Smith & Nephew, “Annual Report 2023,” smith-nephew.com. Solventum’s 2024 spin-out sharpened focus on healthcare, accelerating R&D in incision-management and NPWT platforms. Smith & Nephew is doubling down on single-use NPWT and enzymatic debridement, aiming to siphon share from gauze and hydrogel incumbents.

Start-ups are targeting sensor-enabled dressings, biodegradable polymers, and AI-driven wound-imaging software, filing more than 200 patents in 2024–2025 across the USPTO and EPO. Yet commercial traction hinges on payer recognition: solutions aligned with CMS remote-monitoring codes or European DRG incentives scale faster than purely technology-led offerings. Raw-material security is another differentiator; firms that diversify beyond marine biopolymers mitigate supply shocks and margin volatility. Overall, rivalry balances steady incremental innovation with sporadic regulatory and reimbursement shocks that can abruptly reorder the competitive deck.

Wound Dressings Industry Leaders

Solventum Corporation

Smith & Nephew

ConvaTec Group

Mölnlycke Health Care

Coloplast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Tiger BioSciences has strengthened its position in regenerative medicine and advanced wound care with the acquisition of Platelet-Rich Fibrin Matrix (PRFM) technology from Bahia Medical Inc.

- November 2025: The Department of Atomic Energy and Cologenesis Pvt. Ltd. commercially launched ColoNoX, a nitric-oxide-releasing dressing aimed at diabetic foot ulcer management in India.

- January 2025: Beiersdorf introduced its first plaster under the Hansaplast brand built on advanced hydrocolloid technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the global wound dressings market as revenues generated from sterile coverings specifically designed to protect and promote healing of acute or chronic skin breaks, including foam, film, hydrocolloid, alginate, hydrogel, collagen, antimicrobial, and other advanced or traditional dressings that are sold as finished packs to healthcare providers or home users.

Scope exclusion: devices such as negative-pressure systems, surgical sutures, and topical biologics are not counted.

Segmentation Overview

- By Type

- Advanced Wound Dressings

- Foams

- Hydrocolloids

- Films

- Alginates

- Hydrogels

- Collagens & ECM

- Antimicrobial / Silver

- Super-absorbent Polymers

- Interactive Smart Dressings

- Traditional Wound Dressings

- Bandages

- Gauzes

- Sponges & Pads

- Cotton Rolls & Others

- Advanced Wound Dressings

- By Application

- Surgical & Traumatic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous & Arterial Ulcers

- Burns

- Other Chronic / Acute Wounds

- By End User

- Hospitals & Surgical Centers

- Specialty Wound Clinics

- Home-Healthcare Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To verify desk findings, we interview clinicians, hospital buyers, and distributors across North America, Europe, Asia-Pacific, and key emerging nations. These discussions clarify real-world adoption rates, average selling prices, and near-term reimbursement changes before figures are finalized.

Desk Research

Our analysts extract baseline volumes and pricing from open datasets issued by bodies such as the US CDC, Centers for Medicare & Medicaid Services, the International Diabetes Federation, Eurostat's trade codes, and the European Wound Management Association. Market context is enriched through tariff filings, peer-reviewed journals, and investor presentations, then checked against shipment trends housed in paid resources like D&B Hoovers and Dow Jones Factiva. A continual scan of regulatory bulletins, customs logs, and hospital procurement portals lets us spot sudden demand shifts. The desk research sources listed are illustrative; many additional feeds inform validation and gap fills.

Market-Sizing & Forecasting

A top-down build starts with national procedure counts, diabetic prevalence, surgical volumes, and hospital bed numbers, which are then linked to dressing usage norms and average prices. Results are cross-checked through selective bottom-up supplier roll-ups and channel checks to fine-tune outliers. Key model levers include incidence of chronic wounds, outpatient shift, average length of stay, material cost trends, and adoption of antimicrobial formats. Forecasts to 2030 apply multivariate regression blended with scenario analysis that weights policy shifts and technology penetration cues provided by experts.

Data Validation & Update Cycle

Outputs pass a two-step peer review, followed by variance checks against external series; anomalies trigger re-contact of sources. Mordor Intelligence refreshes the model annually and issues interim updates when material policy or recall events emerge.

Why Mordor's Wound Dressings Baseline Stays Dependable

Published estimates often differ because firms vary scope, pricing assumptions, and refresh cadence.

Key gap drivers include whether traditional gauze is bundled with advanced dressings, choice of exchange rates, and how hospital mark-ups are treated. Our study reports 2025 revenue at USD 5.23 billion, strictly for dressings; many publishers roll in tapes, therapy devices, or report ex-factory rather than end-user values, inflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.23 B (2025) | Mordor Intelligence | - |

| USD 14.77 B (2024) | Regional Consultancy A | Includes tapes and wound care devices |

| USD 10.95 B (2024) | Global Consultancy B | Uses list-price ASPs and aggregates bulk roll material sales |

| USD 7.83 B (2024) | Trade Journal C | Focuses only on advanced dressings yet applies hospital mark-ups |

Taken together, the comparison shows that by selecting a clearly bounded product set, validating price points directly with buyers, and updating figures every year, Mordor Intelligence offers decision-makers a balanced, transparent baseline they can trace back to observable variables.

Key Questions Answered in the Report

What will global wound dressings demand reach by 2031?

Spending is projected to approach USD 6.47 billion by 2031, up from USD 5.42 billion in 2026 as volumes expand across both advanced and traditional formats.

Which dressing category is expanding at the quickest pace?

Traditional gauze, bandages, and cotton rolls are advancing at a 5.25% CAGR through 2031, growing 45% faster than overall revenue thanks to cost-constrained public tenders in low- and middle-income regions.

How is the rise in diabetic foot ulcers shaping product needs?

With global diabetes cases expected to reach 1.31 billion by 2050, demand is tilting toward moisture-retentive hydrocolloids, silver foams, and collagen matrices that manage chronic, high-exudate diabetic wounds.

Why are single-use NPWT devices gaining traction in home care?

The U.S. Centers for Medicare & Medicaid Services created separate payment and remote-monitoring codes in 2024, allowing clinicians to bill for disposable negative-pressure therapy delivered outside hospitals.

In what ways are sustainability targets influencing dressing design?

European net-zero mandates are spurring the shift toward biodegradable chitosan, bacterial cellulose, and PLA dressings that reduce medical-plastic waste without compromising healing performance.

Page last updated on: