United States Egg Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

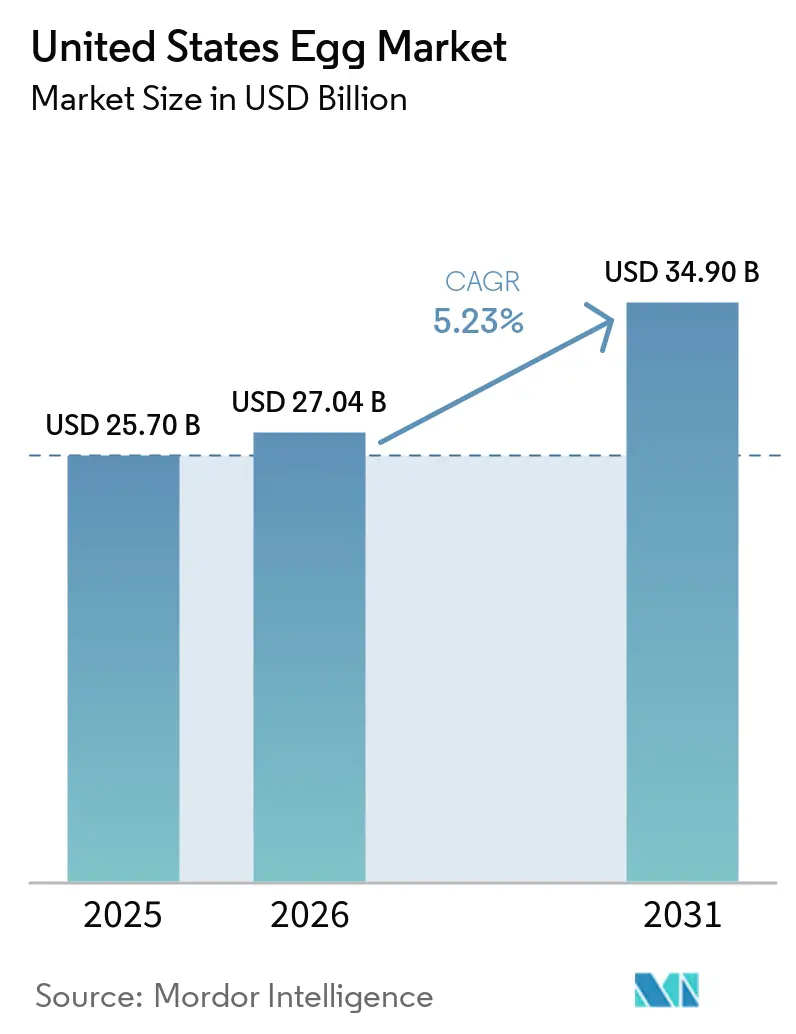

| Base Year Market Size (2025) | USD 25.70 Billion |

| Market Size (2026) | USD 27.04 Billion |

| Market Size (2031) | USD 34.90 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

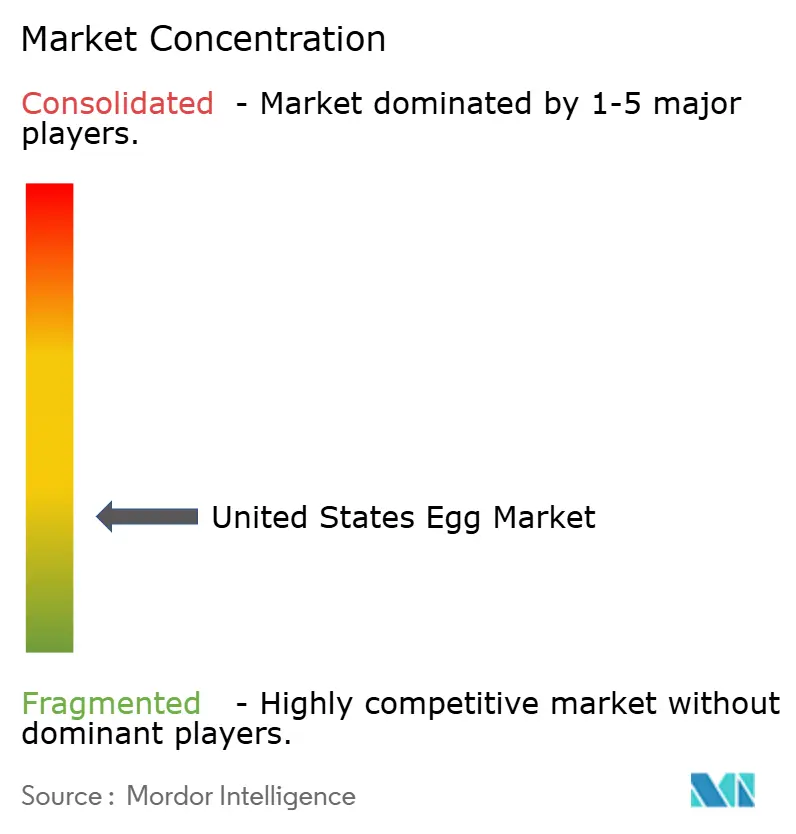

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Egg Market Analysis by Mordor Intelligence

The United States egg market size is expected to grow from USD 25.7 billion in 2025 to USD 27.04 billion in 2026 and is forecast to reach USD 34.90 billion by 2031, at a 5.23% CAGR over 2026-2031. The United States egg market is undergoing a structural transformation, shifting from short-term supply shocks toward a more stable, demand-driven trajectory. This transformation is driven by consistent consumer demand for cost-effective protein sources, increasing preferences for value-added egg products, and a growing commitment to environmentally sustainable sourcing practices. Foodservice operators and retailers are increasingly incorporating processed and specialty egg products into their offerings, indicating a strong and sustained demand that extends beyond typical price fluctuations. However, producers continue to face significant challenges, including the recurrence of avian diseases and volatility in feed costs, both of which exert pressure on profit margins and operational efficiency. Nevertheless, the alignment of health and nutrition trends, advancements in product innovation, and the recovery of institutional procurement activities position the market for sustained growth and strategic opportunities in the coming years.

Key Report Takeaways

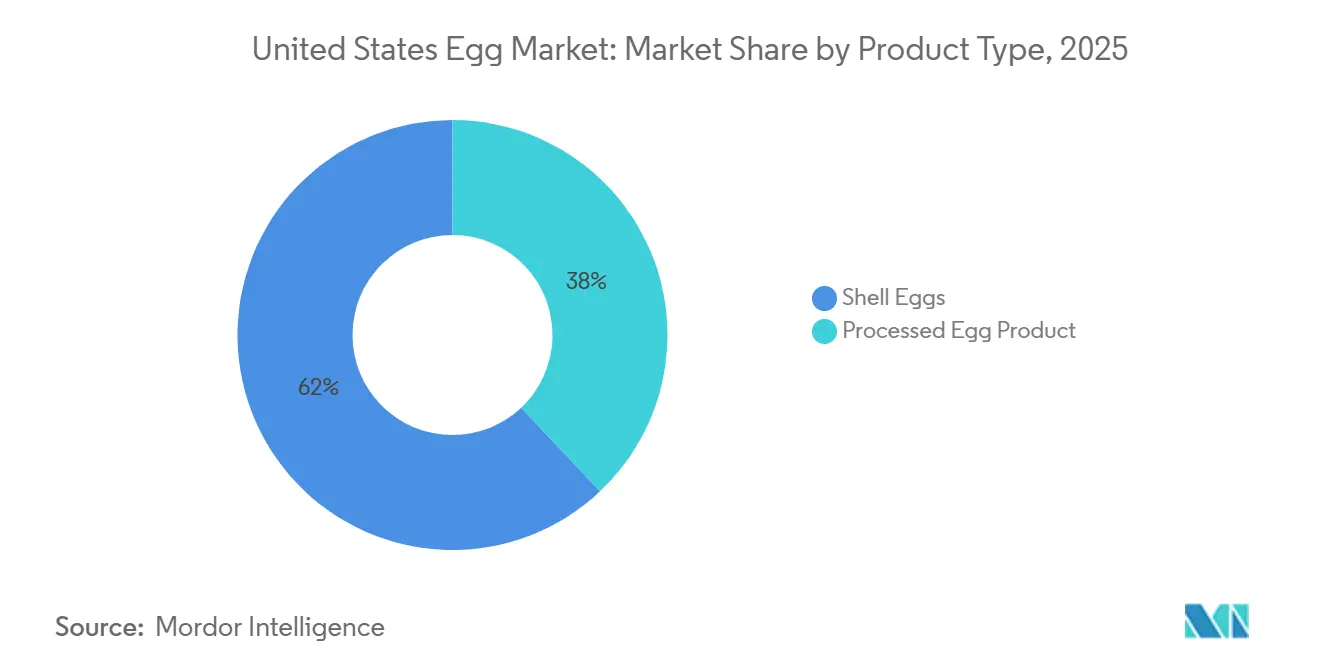

- By product type, shell eggs led the United States egg market with a share of 62.04% in 2025, while processed egg products are anticipated to register the fastest CAGR of 6.86% during 2026-2031.

- By form, whole egg retained 57.36% share in 2025, whereas egg white is forecast to expand at a 5.92% CAGR through 2031.

- By category, conventional held 68.69% of 2025 revenue, but free-from is expected to grow fastest at 6.94% through 2031.

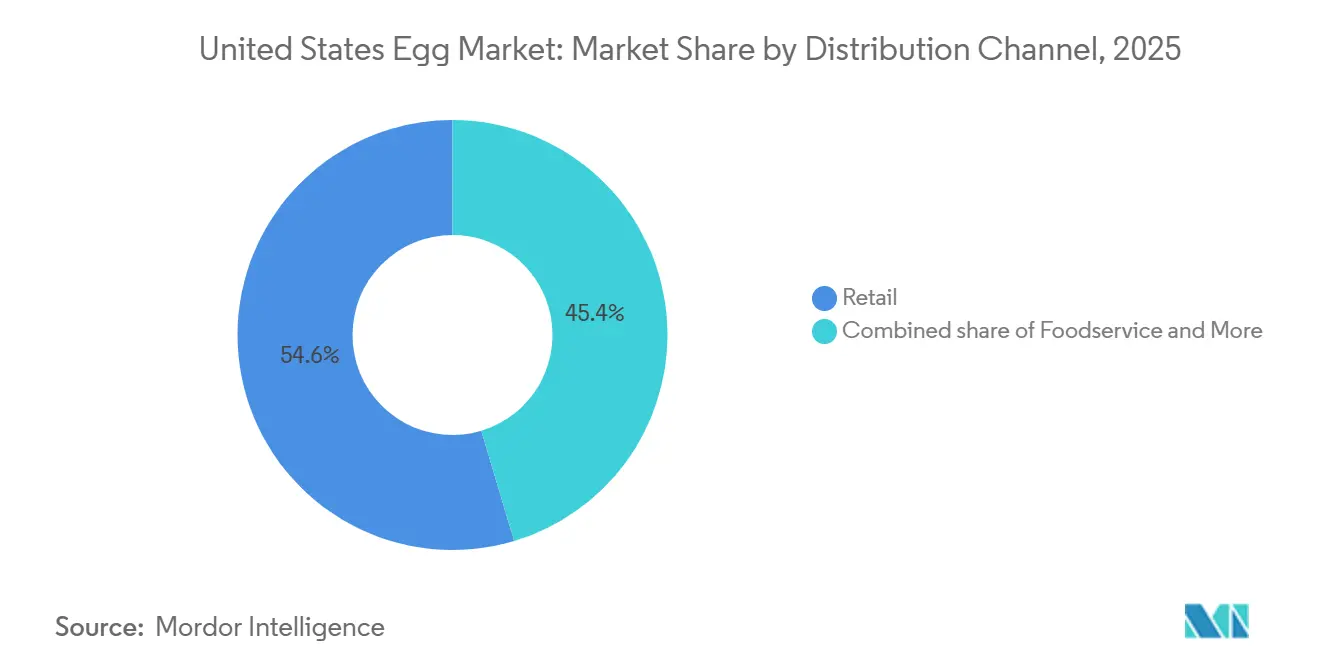

- By distribution channel, retail led the United States egg market with a share of 54.63% in 2025, while foodservice is anticipated to register the fastest CAGR of 6.12% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Egg Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for high-protein and nutrient-dense foods | +1.4% | National, with stronger pull in urban and suburban markets | Long term (≥ 4 years) |

| Accelerating shift toward functional and value-added eggs | +0.8% | National, concentrated in premium retail channels in the Northeast, West Coast, and major metros | Medium term (2–4 years) |

| Expanding use of processed egg products in food manufacturing | +0.7% | National; Midwest processing hubs (Iowa, Ohio, Indiana) lead volume | Medium term (2–4 years) |

| Growth of convenience foods and ready-to-eat meal consumption | +0.6% | National, with highest penetration in densely populated states | Medium term (2–4 years) |

| Strong foodservice recovery supporting institutional egg demand | +0.5% | National; South and West regions leading foodservice traffic recovery | Short term (≤ 2 years) |

| Growing popularity of egg whites in fitness and sports nutrition | +0.4% | National, concentrated in states with high gym and wellness market density | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for high-protein and nutrient-dense foods

In the United States, eggs are increasingly recognized as a reliable, nutrient-dense protein source that aligns with both cost-efficiency and health-conscious consumer preferences. As the market shifts away from ultra-processed food products, eggs have gained prominence as a whole, identifiable protein option with broad demographic appeal. Their versatility in culinary applications, coupled with growing acknowledgment in clinical nutrition and strategic dietary planning, underscores their importance in supporting health and wellness across various age groups, particularly among senior populations. Notably, the 2025–2030 Dietary Guidelines for Americans, issued jointly by the United States Department of Agriculture (USDA) and the Department of Health and Human Services (HHS), explicitly prioritize eggs as the leading recommended animal-based protein. These guidelines also establish daily protein intake targets of 1.2 to 1.6 grams per kilogram of body weight[1]Source: American Health Care Association and the National Center for Assisted Living (AHCA/NCAL), "DHHS and USDA Release 2025-2030 Dietary Guidelines for Americans," ahcancal.org. This federal endorsement strengthens consumer confidence and reinforces eggs' position as a foundational component of modern dietary patterns. Collectively, these factors provide a robust basis for sustained demand, positioning eggs as a dependable, adaptable, and economically viable element of everyday nutrition.

Accelerating shift toward functional and value-added eggs

In the United States egg market, a significant transformation is taking place, driven by increasing consumer preference for functional and value-added categories. The demand for cage-free, organic, and pasture-raised eggs is prompting substantial structural changes across the supply chain. This trend toward premiumization is supported by legislative requirements focused on animal welfare and a growing consumer emphasis on transparency regarding product origins. Brands that prioritize and adhere to certified standards are not only gaining market share but also fostering long-term customer loyalty. Notably, despite price volatility, the demand for specialty eggs remains strong and volume-driven, indicating a level of category elasticity that supports sustained growth. Leading producers like Cal-Maine are expanding their farm networks and shifting their strategies from capacity-building to deeper market penetration. This evolution signals that value-added eggs are transitioning from niche adoption to becoming a fundamental component of mainstream consumption. Furthermore, consumer willingness to prioritize welfare-certified products, even in price-sensitive scenarios, reinforces this momentum. Overall, this progression underscores the critical role of ethical sourcing and functional innovation in redefining the competitive landscape and shaping the next phase of growth for the market.

Expanding use of processed egg products in food manufacturing

As United States food manufacturers increasingly prioritize processed egg products over traditional shell eggs, the United States egg market is undergoing a significant transformation. These processed formats, such as liquid egg products, frozen egg products, and dried egg products, are valued for their operational efficiency, product consistency, and enhanced safety standards. Foodservice operators, who initially adopted these products during periods of price volatility, have transitioned to long-term usage, driving sustained market growth. Simultaneously, food manufacturers are incorporating processed egg products into a wide range of applications, including bakery products, sauces, meal kits, and clinical nutrition solutions, further embedding these products into the value chain. Regulatory oversight under the Egg Products Inspection Act strengthens the competitive position of large-scale processors, fostering industry consolidation and creating a robust competitive advantage. Collectively, these developments highlight the evolution of processed egg products from temporary contingency measures to strategic growth drivers, fundamentally reshaping supply chain structures and demand patterns within the market.

Strong foodservice recovery supporting institutional egg demand

In the United States, the recovery of the foodservice sector is significantly driving institutional egg demand. Restaurants, hotels, airlines, and catering services are increasingly adopting standardized, value-added egg formats. The National Restaurant Association forecasts that by 2026, the United States restaurant and foodservice industry sales will reach USD 1.55 trillion[2]Source: National Restaurant Association, "State of the Restaurant Industry 2026," restaurant.org. This growth is primarily driven by full-service and fast-casual dining, with institutional catering also experiencing expansion. Quick-service restaurants and fast-casual dining establishments, particularly those focused on breakfast offerings, are prioritizing pre-cooked and portion-controlled egg products. This shift represents a move away from traditional loose shell eggs, emphasizing processed solutions that deliver consistency, safety, and labor efficiency. This transformation is not merely a return to pre-crisis consumption patterns but a strategic reconfiguration of procurement practices, favoring large-scale, certified suppliers capable of meeting specification-driven contracts. As vertically integrated producers expand their prepared foods portfolios, the foodservice channel is becoming a critical growth driver, reinforcing the role of eggs as a versatile and indispensable ingredient across institutional dining platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring avian influenza outbreaks disrupting supply and pricing | -1.2% | National; Mississippi Flyway and Central Flyway states face highest seasonal exposure | Long term (≥ 4 years) |

| Increasing regulatory scrutiny on animal welfare and production practices | -0.4% | National; strongest compliance pressure in California, Massachusetts, and states adopting similar standards | Medium term (2–4 years) |

| Growing competition from plant-based egg alternatives | -0.3% | National; concentrated impact in urban retail and premium foodservice | Long term (≥ 4 years) |

| Escalating feed costs pressuring producer margins | -0.5% | National; greatest impact in states with higher feed transportation distances from Corn Belt | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Recurring avian influenza outbreaks disrupting supply and pricing

In the United States egg market, recurring outbreaks of highly pathogenic avian influenza (HPAI) have become a critical destabilizing factor. These outbreaks result in extended supply disruptions and significant price volatility, impacting both retail and foodservice channels. The primary challenge stems from the asymmetry in the supply response: while flock depopulation during outbreaks occurs immediately, the process of rebuilding flocks requires several months, creating prolonged supply gaps that buyers find difficult to mitigate. According to the American Farm Bureau Federation, nearly 21 million birds were affected between January and March 2026[3]Source: American Farm Bureau Federation, "Declining Egg Prices Squeeze Farmers," fb.org. This data highlights that the outbreak cycle remains active, episodic, and seasonally tied to migratory bird flyways. These ongoing risks not only destabilize the market and erode consumer confidence but also accelerate the adoption of substitutes, such as plant-based alternatives and imported egg products. Despite efforts to achieve breakthroughs in biosecurity measures, the industry continues to operate under a model where supply shocks are factored into pricing. This environment places increased pressure on producers to balance resilience, strategic investments, and innovation to sustain long-term competitiveness in the market.

Escalating feed costs pressuring producer margins

In the United States egg market, rising feed costs, driven by the fluctuating prices of corn and soybean meal, are significantly compressing producer profit margins and destabilizing the overall industry. Feed expenses, which constitute the largest component of production costs, have escalated to the point where numerous producers are operating at a financial loss. This has accelerated the consolidation of smaller farming operations and introduced vulnerabilities into the supply chain. Furthermore, changes in trade policies, particularly tariff implementations impacting grain markets, have added another layer of complexity, exacerbating price volatility and hindering long-term strategic planning. Consequently, producers are reevaluating their competitive strategies, focusing on achieving a balance between operational efficiency, scalability, and resilience. The persistent volatility in feed costs has evolved from a temporary challenge to a structural risk within the industry. This financial strain is driving producers to explore diversification opportunities and invest in innovative product formats to mitigate margin pressures. Ultimately, the increasing feed costs represent not just a short-term obstacle but a critical factor influencing the industry's future development and consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Processed Formats Rebalancing a Shell-Egg-Dominated Market

In 2025, shell eggs commanded a dominant 62.04% share of the United States egg market, solidifying their status as the primary choice for household consumption across both retail and foodservice channels. Supermarkets predominantly promote conventional white shell eggs, while specialty retailers position brown shell eggs as a premium product, often associated with free-range and heritage breeds. The widespread recognition and consumer trust in shell eggs firmly establish them as the cornerstone of the market, even as consumer demand patterns evolve. Their entrenched role in daily diets underscores their critical importance within the industry's value chain.

Conversely, processed egg products, including liquid egg products, frozen egg products, and dried egg products, are experiencing rapid growth, with a projected CAGR of 6.86% from 2026 to 2031. This growth reflects a structural shift in foodservice and manufacturing toward specification-driven procurement, which prioritizes consistency, safety, and operational efficiency. Applications in bakery products, sauces, meal kits, and clinical nutrition further highlight their growing relevance. Additionally, advancements in drying and filtration technologies are unlocking new opportunities in protein supplements and industrial food programs. This upward trajectory positions processed egg formats as a strategic growth driver, gradually reducing the market's historical reliance on shell eggs. Their adaptability across diverse applications not only reinforces their significance but also establishes them as a key factor in future market expansion and competitive differentiation.

By Form: Whole Egg Dominates, Egg White Gains as a Functional Ingredient

In the United States egg market, whole eggs maintain a dominant position, accounting for 57.36% of the market value in 2025. This leadership is driven by their comprehensive nutritional profile and broad culinary applicability. Whole eggs are extensively utilized across retail, foodservice, and industrial sectors. The growing popularity of fast-casual breakfast offerings further strengthens their demand. Although other egg forms are gaining market share, whole eggs remain a cornerstone of consumer diets and industrial applications due to their adaptability across various culinary and nutritional contexts. This entrenched position underscores their critical role in the market, ensuring stability and continuity as the market evolves.

Conversely, egg whites represent the fastest-growing segment, with a projected CAGR of 5.92% from 2026 to 2031. This growth is primarily driven by the increasing influence of fitness culture, the adoption of protein-centric dietary practices, and the rising demand for low-fat, high-bioavailability ingredients. Their incorporation into sports nutrition products and clinical dietary formulations is further supported by federal dietary guidelines, which emphasize eggs as a preferred source of protein. Beyond institutional applications, the retail adoption of liquid egg whites has accelerated following the 2025 price surge, fostering a repeat-purchase consumer base that extends beyond fitness-focused individuals. This upward trajectory positions egg whites as a strategic growth driver, combining functional versatility with strong consumer appeal, and signaling their evolution from a niche product to a mainstream protein solution.

By Category: Conventional Holds Scale, Free-From Commands Value Growth

In 2025, conventional eggs dominated the United States egg market, holding a 68.69% market share. Their market leadership is supported by cost-sensitive retail buyers, large-scale foodservice chains, and bulk industrial users. Although their extensive scale ensures they generate the majority of absolute revenue, their pricing power is structurally limited due to retailer and foodservice commitments to sourcing cage-free eggs. Within this category, brown eggs command a modest premium, attributed to consumer perceptions of farm freshness and natural feeding practices. This differentiation provides producers with a competitive advantage that is independent of certified animal welfare standards. As the market transitions toward higher-value alternatives, conventional eggs continue to serve as the backbone of the supply chain, ensuring stability and meeting demand.

On the other hand, the free-from category, which includes cage-free, organic, and pasture-raised egg formats, represents the fastest-growing segment, with a projected CAGR of 6.94% from 2026 to 2031. This growth is being driven by mandatory compliance deadlines under California’s Proposition 12 and similar state-level regulations, which are reshaping sourcing strategies across the retail and foodservice sectors. Producers such as Vital Farms are leading the way by implementing precision pasture management practices, signaling a shift toward data-driven production methods in what has traditionally been a relationship-based supply chain. With price premiums often ranging from two to three times higher than conventional eggs, Free-from products are capturing consumer loyalty and enabling early adopters with certified provenance to secure stronger positions in contract negotiations. This growth trajectory underscores how welfare-certified and provenance-driven egg formats are not only driving value creation but also redefining competitive dynamics within the industry.

By Distribution Channel: Retail Dominance Anchoring Market Value

In 2025, retail, led by supermarkets and hypermarkets, dominated the United States egg market with a 54.63% share, catering to diverse income levels. Urban and suburban areas, characterized by smaller basket sizes and frequent purchases, see added reach from convenience and grocery stores. E-commerce is carving out a vital niche, facilitating direct-to-consumer cold-chain fulfillment for perishable goods. Subscription-based models are providing specialty and pasture-raised brands with a competitive advantage, strengthening customer loyalty and ensuring consistent demand. This retail dominance not only serves as a cornerstone of market value but also evolves in response to the growing influence of digital platforms.

Meanwhile, the foodservice/HoReCa channel is on a growth trajectory, projected to expand at a CAGR of 6.12% from 2026 to 2031. This growth is driven by the recovery of restaurants, hotels, airlines, and institutional catering services. The National Restaurant Association's forecast of United States Dollar (USD) 1.55 trillion in total United States foodservice sales for 2026 highlights the substantial opportunities available for egg suppliers. A significant trend within this channel is the rapid adoption of pre-processed products — such as liquid eggs, frozen omelets, and pre-cooked patties, valued for their consistency, safety, and labor efficiency. Vertically integrated producers, particularly those with certified food safety credentials, are capitalizing on this trend, supported by large-scale supply contracts and their ability to meet specification-driven requirements. As the foodservice sector expands, it not only drives volume growth but also catalyzes structural changes within the eggs market.

Geography Analysis

The Midwest stands firm as the cornerstone of the United States egg market. Bolstered by large-scale operations, its proximity to feed grain production, and robust distribution networks, the Midwest ensures a steady supply. This region's strong ties to both retail and foodservice channels further cement its pivotal role in national egg availability. Despite challenges like feed cost fluctuations and disease threats, the Midwest's expansive scale and infrastructure solidify its industry anchor status.

The Western region is rapidly ascending, driven by regulatory pushes and a consumer shift towards cage-free, organic, and pasture-raised eggs. California's Proposition 12, for instance, has fast-tracked the move towards these 'Free-From' categories. This shift not only benefits compliant producers but also taps into consumers' readiness to invest in ethically sourced products. As a result, the Western region is carving out a niche at the forefront of premiumization and innovation in the national egg market.

The Southern and Northeastern regions serve as a dynamic duo, harmonizing supply with demand. The Southern region, with its burgeoning foodservice sector and export logistics, complements the Northeastern region's urban markets that crave specialty and branded eggs. This synergy not only diversifies the national landscape but also fortifies it, balancing large-scale consistency with premium growth. The Midwest's stability, the Western region's momentum, and the Southern-Northeastern partnership highlight the geographical nuances shaping strategies in the egg market.

Competitive Landscape

The competitive landscape of the United States egg market is defined by fragmentation, with a mix of national leaders, regional producers, and niche specialists competing across commodity and specialty segments. Cal-Maine Foods stands out as the largest domestic producer, actively restructuring its business model through acquisitions and diversification into specialty and prepared foods. Its deliberate pivot toward higher-margin categories reflects a broader industry trend of reducing reliance on volatile shell egg cycles. At the premium end, Vital Farms continues to expand its certified pasture-raised model, strengthening brand loyalty and positioning itself as a leader in provenance-driven products. Meanwhile, international capital has entered the market through Global Eggs, which acquired Hillandale Farms in May 2025, signaling growing global interest in United States egg production and consolidation opportunities.

Beyond these headline players, white-space opportunities are emerging in premium branded products and processed egg ingredients. Smaller producers are leveraging provenance, regenerative agriculture, and sustainability credentials to command strong retail premiums, while integrators are focusing on supplying specification-compliant volumes to industrial buyers. Rembrandt Foods exemplifies this model, bypassing the volatile shell egg retail market by competing on consistency, customization, and food safety credentials for food manufacturers and foodservice chains. Innovation is also reshaping the competitive frontier, with companies like The EVERY Company pursuing precision fermentation of egg proteins and others advancing spray-drying technologies for egg white powders, potentially disrupting cost structures and supply models.

Regional producers such as MPS Egg Farms, Daybreak Foods, Herbruck’s Poultry Ranch, and Weaver Brothers remain critical to the competitive mix, emphasizing reliability, direct customer relationships, and sustainability practices. Weaver Brothers, for instance, has partnered with Ductor Americas to develop renewable energy and organic fertilizer solutions, showcasing how circular agriculture credentials are becoming relevant differentiators in procurement decisions. Together, these players illustrate a market where scale, innovation, and sustainability are increasingly decisive levers of competitive advantage, shaping both current positioning and long-term strategy.

United States Egg Industry Leaders

-

Cal-Maine Foods, Inc.

-

Rose Acre Farms, Inc.

-

Michael Foods, Inc.

-

Hillandale Farms

-

Rembrandt Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Global Eggs, led by Ricardo Faria, acquired Pearl Valley Egg Farms, a family-owned egg producer based in Illinois. Through this acquisition, Global Eggs expanded its flock by approximately two million layers. For Pearl Valley Farms, the transaction represented a significant new chapter.

- March 2026: Cal-Maine Foods, Inc. completed the acquisition of the shell egg, egg products, and prepared foods assets of Creighton Brothers LLC, including Crystal Lake LLC, for approximately USD 128.5 million, subject to customary post-closing adjustments. This acquisition expanded the company’s scale and geographic reach in the shell egg market, covering both specialty and conventional eggs, and added significant growth to its portfolio.

- March 2026: Global Egg Company, the world's leading producer and distributor of table eggs, has secured an agreement with Warburg Pincus, a trailblazer in global growth investing. With the investment pegging the company's valuation at a notable USD 8 billion, Warburg Pincus is reaffirming its dedication to collaborating with standout founders and backing global entities poised for significant growth. The capital for this transaction is sourced from the Warburg Pincus Capital Solutions Founders Fund (“WPCS FF”).

United States Egg Market Report Scope

Eggs are a natural food product laid by birds, most commonly hens, and are widely consumed as a staple source of protein and essential nutrients. Structurally, they consist of a protective shell, an albumen (egg white), and a yolk, each serving distinct biological and nutritional functions.

The United States egg market is segmented by product type, form, category, and distribution channel. By product type, the market is segmented into shell eggs and processed egg products. By form, the market is segmented into whole egg, egg yolk, and egg white. By category, the market is segmented into conventional and free-from. By distribution channel, the market is segmented into industrial, foodservice/horeca, and retail.

| Shell Eggs | White |

| Brown | |

| Processed Egg Products | Liquid Eggs |

| Frozen Eggs | |

| Dried/Powdered Eggs |

| Whole Egg |

| Egg Yolk |

| Egg White |

| Conventional |

| Free-From |

| Industrial | Food Manufacturing |

| Non-Food End Use | |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Others |

| By Product Type | Shell Eggs | White |

| Brown | ||

| Processed Egg Products | Liquid Eggs | |

| Frozen Eggs | ||

| Dried/Powdered Eggs | ||

| Form | Whole Egg | |

| Egg Yolk | ||

| Egg White | ||

| By Category | Conventional | |

| Free-From | ||

| By Distribution Channel | Industrial | Food Manufacturing |

| Non-Food End Use | ||

| Foodservice/HoReCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Others | ||

Key Questions Answered in the Report

What is the size of the United States egg market?

The market was valued at USD 25.7 billion in 2025 and is projected to reach USD 34.9 billion by 2031, growing at a 5.23% CAGR (2026–2031).

Which product type holds the largest share?

Shell eggs led with 62.04% share in 2025, while processed egg products are the fastest-growing, at a 6.86% CAGR (2026–2031).

Which form dominates consumption?

Whole eggs accounted for 57.36% share in 2025, whereas egg whites are expanding fastest with a 5.92% CAGR (2026–2031).

What category leads the market?

Conventional eggs held 68.69% share in 2025, while Free-From eggs (cage-free, organic, pasture-raised) are the fastest-growing, at a 6.94% CAGR (2026–2031).

Which distribution channel is largest?

Retail accounted for 54.63% share in 2025, while foodservice is the fastest-growing channel, at a 6.12% CAGR (2026–2031).

Page last updated on: