Breakfast Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 223.11 Billion |

| Market Size (2031) | USD 276.81 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

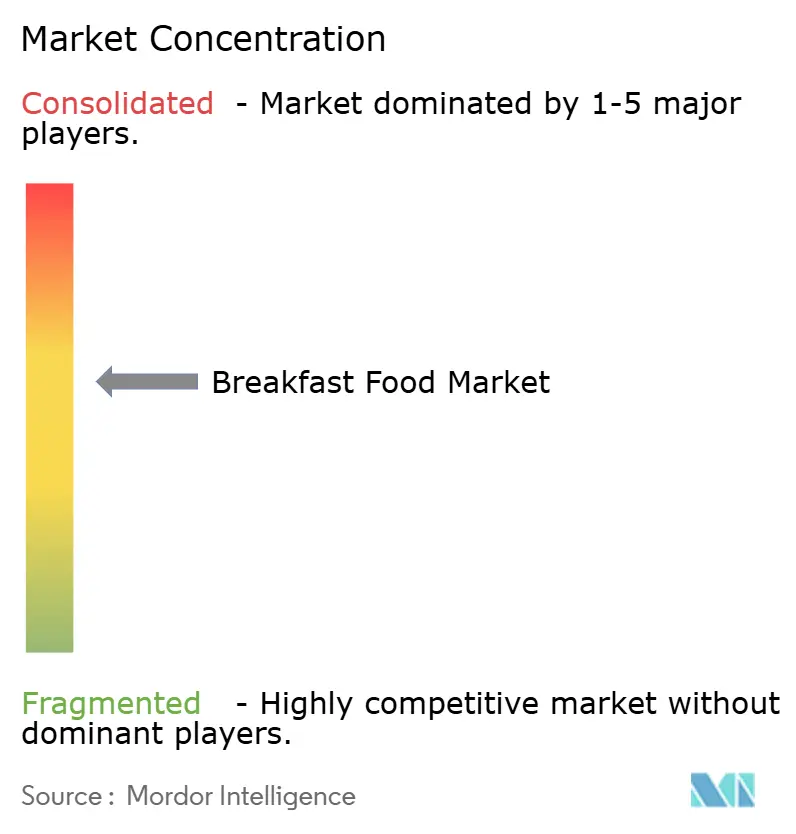

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Breakfast Food Market Analysis by Mordor Intelligence

The breakfast food market size in 2026 is estimated at USD 223.11 billion, growing from the 2025 value of USD 214.05 billion, with 2031 projections showing USD 276.81 billion, growing at a 4.41% CAGR over 2026-2031. Consumers are shifting breakfast habits toward faster, healthier, and more sustainable options. Demand for convenient, nutrient-dense breakfasts is rising as regulatory pressures on sugar content and nutritional labeling push reformulation toward cleaner profiles, such as FDA front-of-pack sugar labels and EU transparency rules. This health focus accelerates organic and free-from variants over conventional staples, backed by trusted certifications that build shopper trust. According to a US Department of Agriculture (USDA) study, 85% of adults aged 20 years and older in the United States consume one or more food and/or beverage items at breakfast[1]Source: US Department of Agriculture, "Breakfast Consumption by U.S. Adults", ars.usda.gov. Online channels erode supermarket dominance through subscriptions and AI personalization, letting consumers lock in repeat orders tailored to their needs and skip impulse aisles entirely. Packaging engineered for recyclability and portion control under EU mandates creates another innovation frontier that aligns convenience with sustainability. These intersecting forces keep the breakfast food market in structural transition even as aggregate growth remains steady.

Key Report Takeaways

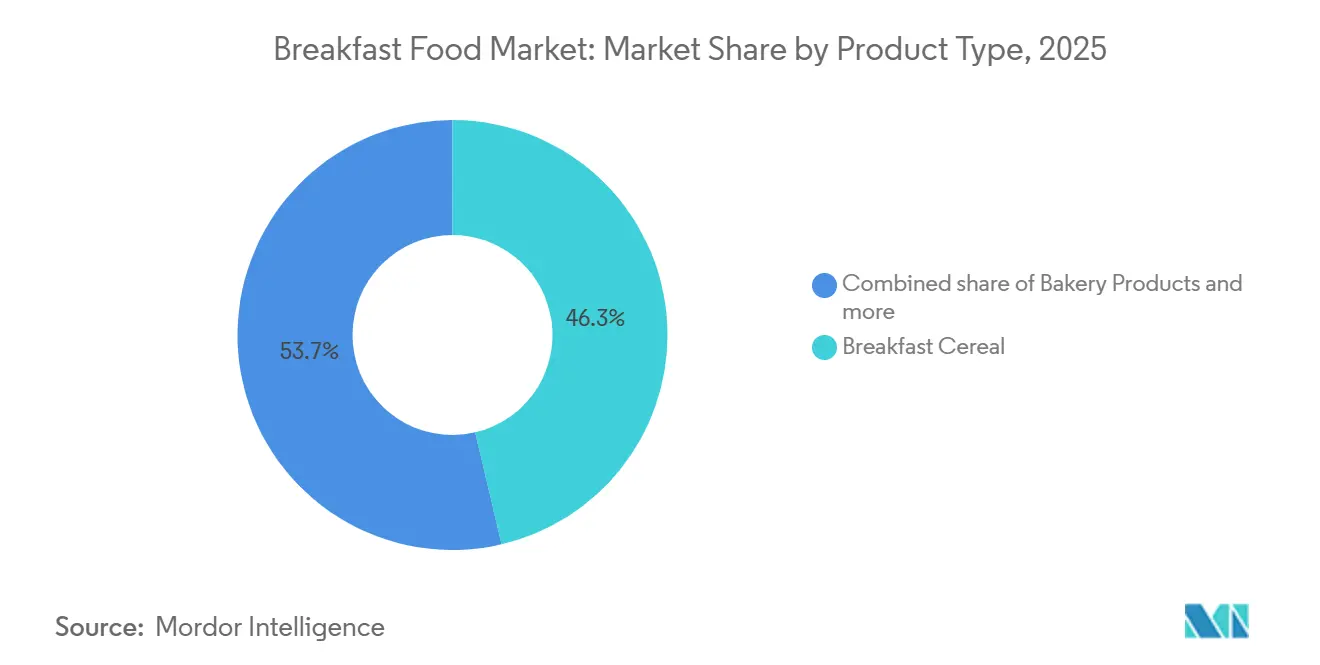

- By product type, breakfast cereals held 46.34% of the breakfast food market share in 2025, whereas waffle/pancake (frozen premixes) are projected to expand at a 5.59% CAGR through 2031.

- By category, conventional items accounted for 83.19% of the breakfast food market size in 2025, while organic/free-from lines are poised to grow at a 6.80% CAGR.

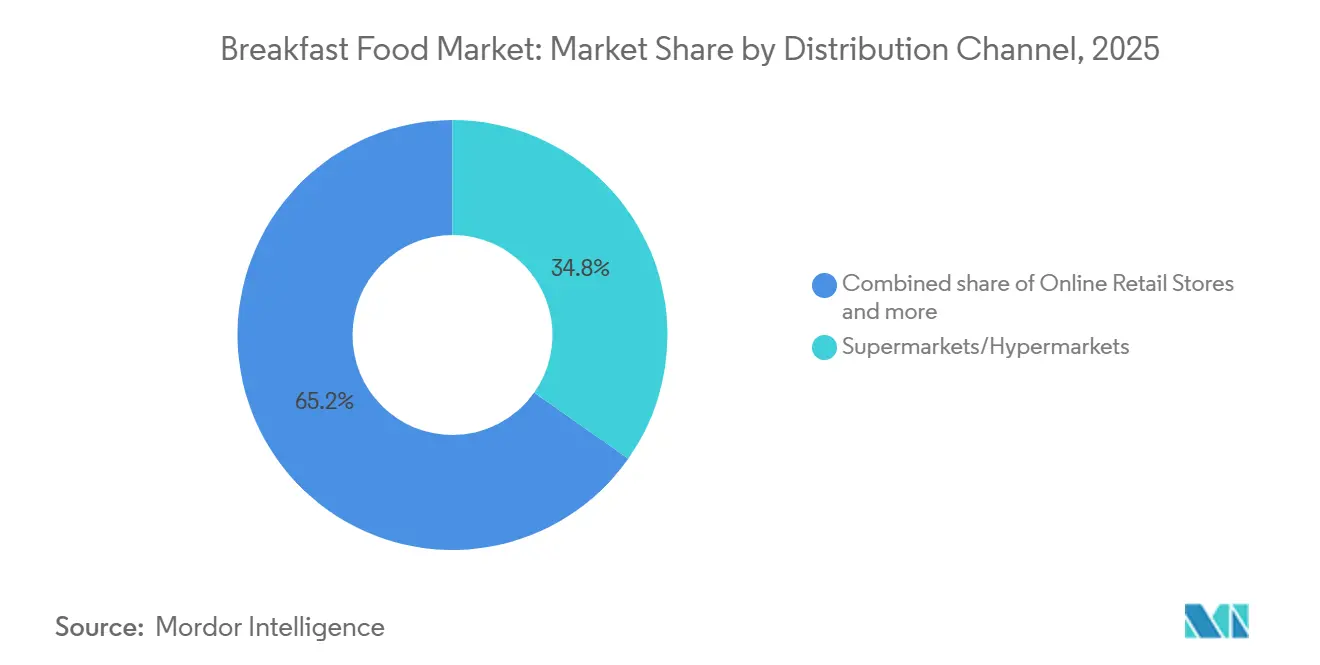

- By distribution channel, supermarkets/hypermarkets led with 34.76% revenue share in 2025, and online retail is the fastest channel at a 7.37% CAGR to 2031.

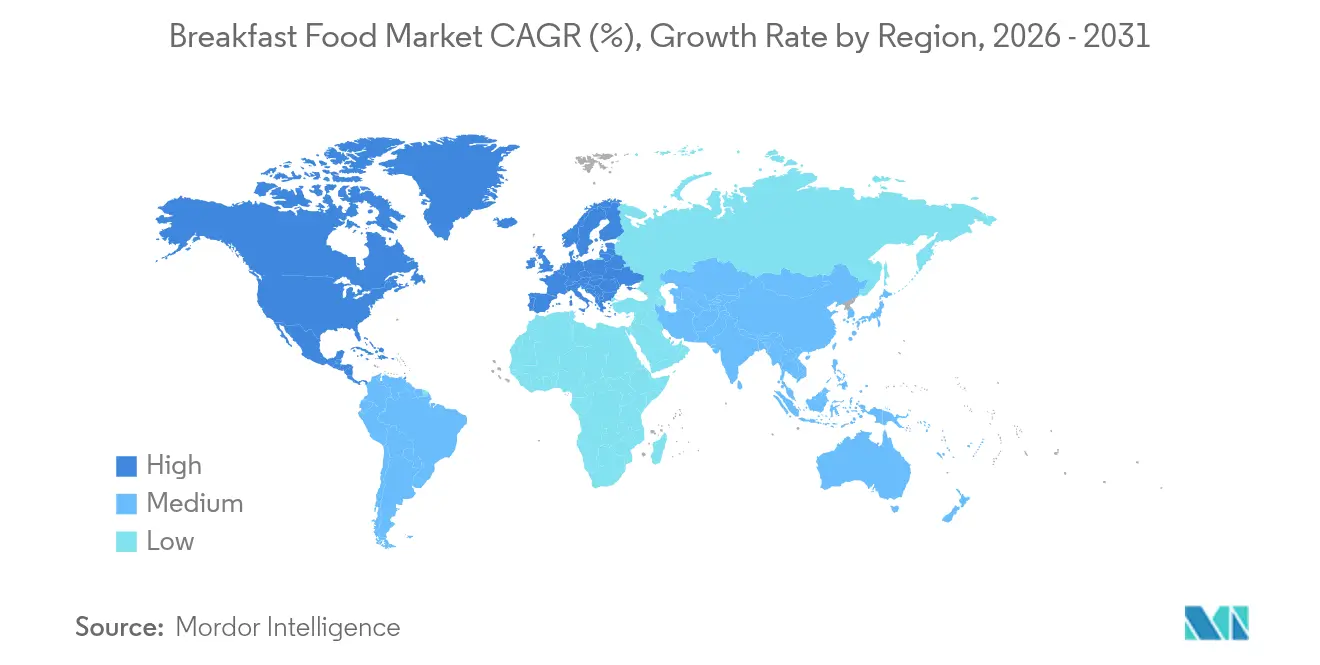

- By geography, North America commanded 33.40% of the breakfast food market in 2025, but the Asia-Pacific is anticipated to advance at a 5.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breakfast Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient, ready-to-eat breakfast options | +0.9% | Global, with urban centers in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Growing popularity of organic, free-from, and clean-label breakfast products | +0.8% | North America and Europe, expanding into affluent Asia-Pacific markets | Medium term (2-4 years) |

| Growth of plant-based diets | +0.6% | Global, strongest in North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of high-protein breakfast SKUs | +0.7% | North America, Europe, and fitness-focused segments in Asia-Pacific | Short term (≤ 2 years) |

| Inclination towards functional and fortified breakfast options | +0.5% | Global, with regulatory support in North America and Europe | Long term (≥ 4 years) |

| Advancements in packaging technology | +0.4% | Global, with early adoption in Europe due to sustainability mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient, ready-to-eat breakfast options

Consumers are increasingly turning to grab-and-go breakfasts as hectic dual-income lifestyles and extended urban commutes leave limited time for morning routines, favoring formats like bars, single-serve cereal cups, and frozen waffles that heat up quickly. People are skipping sit-down traditional breakfasts, creating strong demand for portable, shelf-stable options that deliver filling nutrition without prep hassle. Manufacturers meet this shift with innovations like modified atmosphere packaging and natural preservatives for longer ambient shelf life, freeing products from fridge dependency and boosting availability in convenience stores and vending machines. Portion-controlled, individually wrapped servings fit perfectly into car cup holders, office drawers, or gym bags, transforming breakfast into a seamless mobile occasion for commuters and busy professionals. This convenience surge particularly accelerates frozen premixes and breakfast bars, which offer speed without quality compromise, aligning with broader urbanization trends compressing daily schedules across North America and Asia-Pacific. Shoppers reward these practical solutions with repeat purchases, driving category outperformance as lifestyles prioritize efficiency over elaborate morning rituals.

Growing popularity of organic, free-from, and clean-label breakfast products

Consumers increasingly favor organic, free-from, and clean-label breakfast products, driven by distrust of synthetic additives and pesticide residues, particularly among millennials and Gen Z, who pay premiums for transparent health benefits. Shoppers prioritize USDA-certified options like Nature's Path Heritage Flakes with rigorous traceability and third-party audits that build instant credibility. Clean-label appeal extends further with short, recognizable ingredient lists free of artificial colors, flavors, and high-fructose corn syrup, resonating across grocery aisles and e-commerce. Regulatory frameworks such as the USDA National Organic Program and EU Organic Regulation 2018/848 mandate stringent traceability and third-party verification[2]Source: European Union, "Regulation - 2018/848 - EN - EUR-Lex - European Union", eur-lex.europa.eu. This shift, with strict standards that smaller brands embrace as a form of differentiation, while conventional manufacturers scramble to simplify recipes amid consumer scans of nutrition labels. This preference accelerates categories like cereals, bars, and premixes, where certifications signal safety and sustainability, turning breakfast into a daily wellness choice rather than mere convenience. Shoppers reward verifiable purity with loyalty, fueling premium pricing power and category outperformance as clean eating becomes a mainstream morning routine expectation.

Advancements in Packaging Technology

Packaging innovations are transforming the breakfast food market by extending shelf life, reducing waste, and boosting shopper appeal through smart, sustainable designs that align with modern lifestyles. Active systems like oxygen scavengers and moisture regulators keep cereals crisp without preservatives, meeting clean-label demands while ensuring quality from pantry to plate. Consumers love freshness indicators and QR codes for traceability, turning routine opens into engaging experiences that confirm sourcing and nutrition. In a notable move, Post Cereal pledged to adopt 100% recyclable packaging. Meanwhile, in May 2024, General Mills unveiled its "Smart Pour" technology for Wheaties, underscoring how functional enhancements can set commodity products apart. Canada's Zero Plastic Waste Initiative, which focuses on reducing 75% of plastic waste by 2030 through increased recycling and sustainable packaging solutions, is driving the adoption of bio-based films and mono-materials for easier recycling, aligning with eco-conscious preferences[3]Source: Government of Canada, "Canada's actions to reduce plastic waste and pollution", canada.ca. Resealable, portion-controlled pouches suit single households and commuters, minimizing leftovers and fitting perfectly into grab-and-go routines. E-commerce thrives as durable, unboxing-friendly packs protect during shipping and drive repeat buys, giving brands a competitive edge in convenience-driven growth.

Inclination towards functional and fortified breakfast options

Consumers now treat breakfast as a targeted wellness boost, seeking fortified options packed with vitamins, probiotics, fiber, and bioactive compounds to support immunity, gut health, cognitive sharpness, and daily energy needs. The FDA's 2024 "healthy" definition incentivizes additions like vitamin D, potassium, and fiber, addressing key nutrient gaps, while EU EFSA rules demand clinical proof for health claims, ensuring only substantiated products stand out on shelves. Probiotic cereals and prebiotic granola bars lead this charge, appealing to wellness-focused shoppers who prioritize digestive and mental performance benefits over basic nutrition. Major brands like General Mills offer Cheerios Protein in Strawberry and Cinnamon flavors, delivering 8g protein per serving. These functional formats command 20-30% price premiums, reflecting consumer willingness to invest in proven efficacy, turning routine meals into strategic health rituals. Brands succeed by clearly communicating benefits through compliant labeling, driving loyalty among fitness enthusiasts, parents, and aging demographics, managing specific needs like bone health or focus, and positioning fortified breakfasts as essential daily supplements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory scrutiny on sugar levels, nutritional claims, and labeling | -0.6% | Global, with stringent enforcement in North America and Europe | Short term (≤ 2 years) |

| Volatile grain and dairy commodity prices | -0.5% | Global, with acute impact in regions dependent on imports | Short term (≤ 2 years) |

| Nutritional and flavor limitations of alternatives | -0.3% | Global | Medium term (2-4 years) |

| Competition from alternative meal options | -0.4% | Global, strongest in urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile grain and dairy commodity prices

Breakfast food manufacturers face significant challenges due to sharp price fluctuations in key inputs such as wheat, oats, corn, and dairy. These fluctuations are driven by factors like weather disruptions, geopolitical tensions, and rising energy costs, complicating budgeting and profitability. This has led to increased costs for products like yogurt parfaits, cereal milks, and cheese bites, which consumers expect year-round. Major players such as Kellogg and General Mills mitigate these challenges through long-term grain contracts and in-house processing, ensuring supply stability. Meanwhile, smaller players are turning to alternatives like pulse flours or oat milk powders, though these substitutions require recipe adjustments and consumer acceptance for taste and texture. This volatility is also accelerating the shift toward clean-label products, as shoppers notice subtle formula changes, pressuring manufacturers to balance cost control with quality perception. Retailers' resistance to frequent price hikes further hampers innovation and category expansion, forcing manufacturers to either absorb the costs or risk losing shelf space.

Competition from alternative meal options

Urban consumers are increasingly shifting away from traditional packaged breakfast foods in favor of meal replacement shakes, protein smoothies, and hot delivery options from platforms like Uber Eats and DoorDash. Younger demographics particularly prefer these freshly prepared alternatives from convenience stores and coffee chains, which offer premium sandwiches and overnight oats that are perceived as fresher and more customizable compared to cereal boxes. In early 2024, Abbott Laboratories unveiled its high-protein shake, PROTALITY, targeting consumers focused on weight loss and muscle building, effectively positioning it as a breakfast replacement. Furthermore, in 2024, brands like Soylent broadened their high-protein shake offerings to cater to "on-the-go" consumers in search of a nutritionally complete meal. This shift is reducing the volume of sales for bars, cereals, and premixes, especially during peak commute hours when portability aligns with on-demand convenience. Additionally, direct-to-consumer meal kits are intensifying the competition by securing weekly breakfast subscribers who bypass traditional grocery shopping altogether. As consumers increasingly associate value with preparation quality over mere convenience, traditional breakfast food brands are under pressure to innovate rapidly or risk losing relevance in a delivery-driven morning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Premixes Outpace Legacy Cereal

In 2025, breakfast cereals command a 46.34% market share as a breakfast staple, offering familiar convenience across generations, but face pressure from sugar reduction rules and protein-packed rivals pushing reformulation toward whole grains and fiber boosts. Ready-to-eat options remain pantry favorites for quick pours, while hot cereals like oatmeal gain from heart-healthy positioning and sustained energy claims, highlighted by Quaker Oats' 2025 probiotic-fortified instant formats that appeal to wellness-focused mornings. Consumers value versatility for topping with fruits or nuts, though clean-label demands challenge legacy sweetness profiles.

Waffle/pancake products, encompassing both frozen and premix formats, are projected to grow at a 5.59% CAGR through 2031, delivering restaurant-quality taste and texture, perfect for time-crunched households prioritizing speed without compromise. These products cater to busy lifestyles, offering customizable indulgent experiences while preserving breakfast authenticity. In 2025, General Mills launched 8 new breakfast products, including protein cereals and character-licensed varieties. This segment thrives as shoppers trade traditional prep for indulgent yet effortless starts, with easy storage and minimal cleanup, sealing loyalty in busy routines. While bakery products thrive on premiumization trends and artisanal branding, breakfast bars and granola products seize on-the-go consumption moments, a space where traditional cereals fall short. Yogurt and plant milks pair seamlessly with cereals or stand alone, as Chobani's 2025 oat yogurt captures flexitarians blending dairy tradition with plant-based flexibility.

By Category: Conventional Dominance Faces Premium Challenge

Conventional breakfast foods dominate the market with an 83.19% share, through unmatched scale, widespread distribution in supermarkets, and everyday affordability that keeps them in family pantries worldwide. These trusted staples from giants like Kellogg's Corn Flakes and General Mills' Cheerios benefit from decades of brand loyalty and high-velocity shelf space, delivering reliable taste at budget prices for broad appeal. However, they face gradual share erosion as consumers demand cleaner profiles, forcing reformulations to cut sugar and additives while defending value positioning against rising premium rivals.

Organic/free-from alternatives are on the rise, boasting a 6.80% CAGR through 2031. This surge is driven by affluent consumers who prioritize health and environmental benefits over cost. The organic segment enjoys a competitive edge, bolstered by the USDA National Organic Program's stringent standards. These standards mandate certified organic production methods and ban synthetic inputs, creating barriers that shield compliant manufacturers from non-certified rivals. Meanwhile, the clean label trend has evolved. It's no longer just about organic certification; consumers now demand ingredient transparency, minimal processing, and a clear avoidance of additives. This shift underscores a growing consumer sophistication, where genuine authenticity is valued over mere marketing claims. These variants expand reach to dietary-restricted consumers while commanding premium prices, accelerating adoption through trust in rigorous standards over conventional mass production.

By Distribution Channel: E-Commerce Reshapes Reach

Supermarkets/hypermarkets accounted for 34.76% of breakfast food distribution in 2025, while online retail stores are projected to grow at a 7.37% CAGR through 2031, emerging as the fastest-growing channel. Supermarkets and hypermarkets remain pivotal in breakfast food distribution, benefiting from high foot traffic and impulse purchases that drive sales of family staples like cereals and bread during weekly shopping trips. Their strength lies in offering a wide assortment and promotional displays that encourage trial of new products. However, growth in this channel is slowing as consumers increasingly shift repeat purchases to automated online subscriptions, reducing the frequency of in-store restocking.

Online retail stores are driving channel growth by offering unparalleled convenience through platforms like Amazon Fresh and Instacart. These platforms leverage AI-driven recommendations and auto-replenishment features to foster loyalty for staples such as cereals and bars. Consumers are adopting subscription models that accurately predict their needs, while durable packaging and high-quality imagery enhance trust without the need for physical product handling. Convenience stores and other distribution channels cater to specific consumption occasions and impulse purchases, complementing primary retail channels rather than competing directly. This evolving distribution landscape creates opportunities for brands that can effectively tailor channel-specific assortments, pricing strategies, and consumer engagement efforts, all while maintaining a cohesive brand image.

Geography Analysis

North America holds a dominant 33.40% share of the breakfast food market, driven by established consumption patterns for cereals and bakery staples, supported by extensive retail networks and high spending on convenience products that cater to busy lifestyles. This infrastructure efficiently manages a wide range of products, from protein yogurts and frozen waffles to fresh juice bundles. While the FDA's nutrient thresholds increase reformulation costs, major cereal manufacturers leverage economies of scale and advanced research and development capabilities to ensure compliance while maintaining shelf presence. In Canada, provincial clean-label regulations are accelerating the adoption of organic and plant-based products, while in Mexico, urbanization and Grupo Bimbo's local production are driving growth by meeting the rising demand from the middle class.

Asia-Pacific emerges as the most dynamic region, with a projected CAGR of 5.01% through 2031. Urban households are increasingly adopting Western eating habits and reducing meal preparation time, leading to higher demand for on-the-go bread rolls, single-serve fortified porridge cups, and flavored plant-based milks. Local companies like Glico are introducing almond protein drinks to cater to the region's lactose-intolerant population, while global players such as Nestlé and Kellogg's Company are expanding manufacturing in tier-2 cities. Japan and South Korea show a preference for functional fortified products targeting aging populations, although varying FSSAI and Chinese labeling regulations necessitate localized formulations.

Europe, South America, and the Middle East and Africa each contribute uniquely to the breakfast food market. Europe maintains steady per-capita consumption but is shifting toward organic, free-from, and sustainability-compliant packaging in line with EU Green Deal objectives. In South America, the region's abundant grain production supports competitively priced private labels, though fluctuations in purchasing power limit the adoption of premium products. Meanwhile, urban growth in Gulf Cooperation Council nations and sub-Saharan Africa is driving demand for ready-to-eat cereals and frozen pastries, with adaptations for halal standards and environmentally-conscious storage solutions. Across all regions, aligning flavor profiles, packaging sizes, and certification labels with local preferences remains critical for sustained market success.

Competitive Landscape

The breakfast food market demonstrates moderate concentration, with multinational corporations such as Nestlé, General Mills, Kellogg's, and PepsiCo holding significant market share due to their strong brand equity and extensive distribution networks. These companies leverage vertical integration by securing long-term grain contracts and operating proprietary manufacturing facilities, which help mitigate commodity price volatility. Strategic acquisitions remain a key growth strategy, as seen in General Mills' acquisition of Blue Buffalo, with breakfast-specific acquisitions continuing through 2025. Patent filings in 2025 highlight innovation priorities, including Kellogg's resealable cereal packaging with embedded freshness sensors and Nestlé's fermentation-derived flavor enhancers designed to improve sugar-reduced formulations.

Opportunities for growth lie in the convergence of convenience and functional nutrition, particularly in single-serve, high-protein formats targeting fitness enthusiasts and aging populations. Emerging disruptors like Magic Spoon and Catalina Crunch have entered the cereal category with keto-friendly, low-sugar products. Technology adoption is accelerating, with direct-to-consumer brands utilizing subscription models and data analytics to personalize product recommendations and optimize replenishment timing. Established players are responding by enhancing their e-commerce capabilities and collaborating with third-party delivery platforms to maintain their channel share.

Regulatory compliance continues to serve as a competitive advantage, as companies with robust quality assurance systems and regulatory expertise navigate labeling mandates and health claim substantiation more efficiently than smaller competitors. White-space opportunities also exist in premium segments, where niche players capitalize on clean-label, organic, and functional product positioning. Meanwhile, major players continue to diversify their portfolios to capture emerging growth segments and appeal to younger demographics, ensuring their relevance in an evolving market landscape.

Breakfast Food Industry Leaders

-

Kellogg Company

-

Nestlé S.A.

-

General Mills Inc.

-

PepsiCo Inc.

-

Post Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: PepsiCo's Quaker Oats division introduced instant oatmeal fortified with probiotics and prebiotic fiber in China, to meet rising consumer demand for functional foods and address growing concerns over digestive health.

- August 2025: Kellogg Company launched a new line of frozen protein waffles under the Eggo brand, featuring 12 grams of protein per serving and targeting fitness-conscious consumers. The product rollout included partnerships with major grocery chains for prominent freezer placement.

- January 2025: Mondelez International expanded its belVita breakfast biscuit portfolio, introducing non-GMO-verified, kosher-certified belVita energy snack bites featuring no high-fructose corn syrup and no artificial flavors, colors, or sweeteners.

- June 2024: Marico expanded its breakfast offerings in India as it launched Saffola Muesli. The product aimed to leverage the brand's equity in the adult breakfast segment and capitalize on the growing demand for healthy breakfast foods. The strategic move was designed to capitalize on the Saffola brand's strong equity in the healthy adult breakfast segment, building on its success in the oats and extensions into products like honey and peanut butter.

Global Breakfast Food Market Report Scope

Breakfast is eaten primarily as the first meal of the day. Breakfast can be cereal grains like oats, muesli, wheat, and corn. As it is the first meal of the day, breakfast is expected to be highly nutritious, and it should provide energy for the whole day.

The breakfast food market is segmented by product type, category, distribution channel, and geography. Based on product type, the market is segmented into breakfast cereals, bakery products, breakfast bars and granola, dairy and dairy alternatives, food spreads and sauces, and waffle/pancake (frozen premixes). By category, the market is segmented into conventional and organic/free-form. By distribution channels, the market has been segmented into hypermarkets/supermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (units).

| Breakfast Cereal | Ready-to-Eat Cereals |

| Hot Cereals | |

| Bakery Products | Bread and Toast |

| Pastries, Cakes, Muffins | |

| Croissant | |

| Breakfast Biscuits | |

| Others (Rolls, bagels, savory pastries, etc) | |

| Breakfast Bars and Granola | Cereal Bar/Granola Bar |

| Protein Bar | |

| Meal Replacement Bar | |

| Dairy and Dairy Alternatives | |

| Food Spreads and Sauces | |

| Waffle/Pancake (Frozen Premixes) |

| Conventional |

| Organic/Free-From |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Breakfast Cereal | Ready-to-Eat Cereals |

| Hot Cereals | ||

| Bakery Products | Bread and Toast | |

| Pastries, Cakes, Muffins | ||

| Croissant | ||

| Breakfast Biscuits | ||

| Others (Rolls, bagels, savory pastries, etc) | ||

| Breakfast Bars and Granola | Cereal Bar/Granola Bar | |

| Protein Bar | ||

| Meal Replacement Bar | ||

| Dairy and Dairy Alternatives | ||

| Food Spreads and Sauces | ||

| Waffle/Pancake (Frozen Premixes) | ||

| By Category | Conventional | |

| Organic/Free-From | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the breakfast food market?

The breakfast food market size reached USD 223.11 billion in 2026 and is projected to hit USD 276.81 billion by 2031.

Which product category leads global revenue?

Breakfast cereals remain the largest contributor, holding 46.34% of the breakfast food market share in 2025.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to expand at a 5.01% CAGR as urbanization and Western meal patterns boost demand.

How are online channels shaping category growth?

Online retail stores is advancing at a 7.37% CAGR, aided by subscription models and dynamic pricing strategies on platforms such as Amazon.

What regulatory change is most influencing product reformulation?

The FDA’s 2025 “healthy” definition enforces lower sugar, saturated fat, and sodium thresholds, spurring widespread recipe updates.

Which consumer trend is lifting premium price realization?

Growing demand for organic/free-from breakfast foods is driving faster growth, 6.80% CAGR, within premium tiers.

Page last updated on: