Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.33 Billion |

| Market Size (2031) | USD 6.99 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

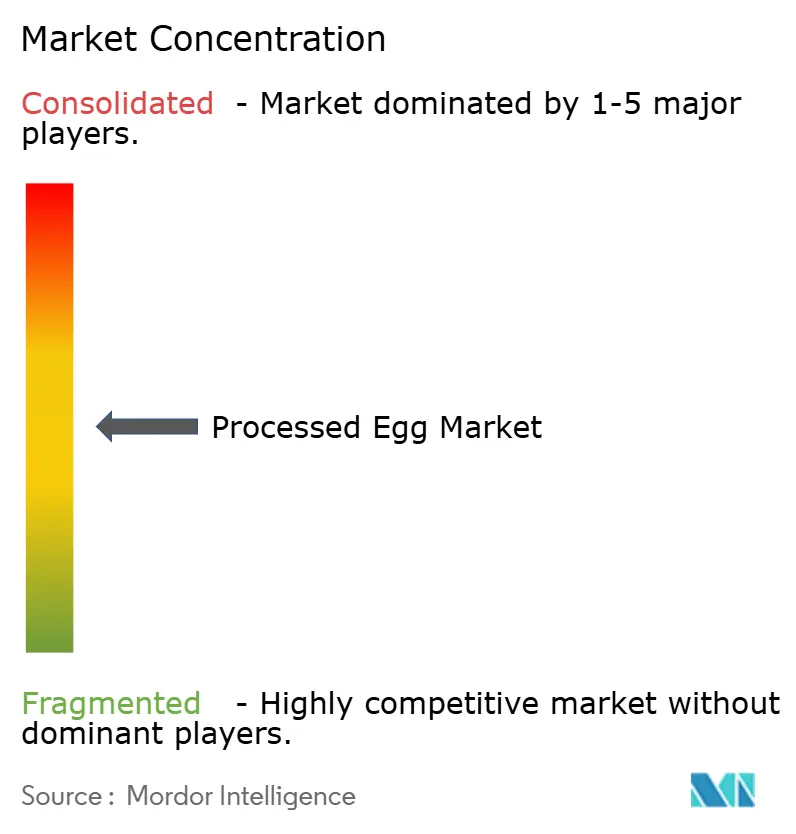

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

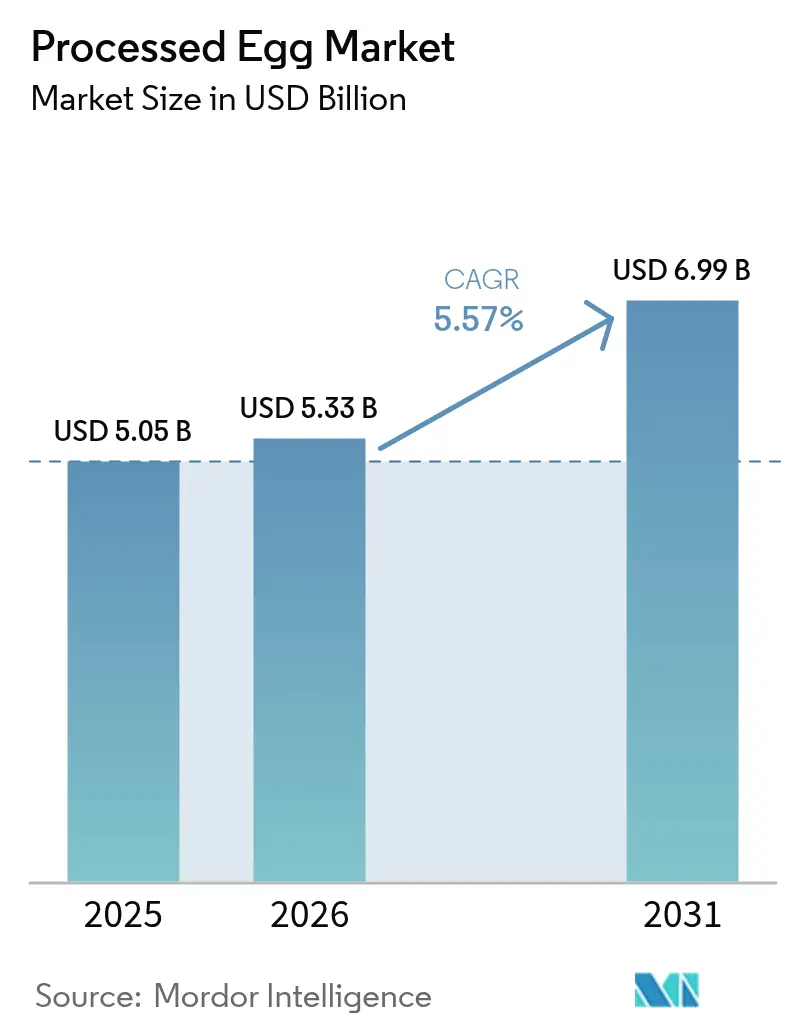

Processed Egg Market Analysis by Mordor Intelligence

The processed egg market size is projected to expand from USD 5.05 billion in 2025 and USD 5.33 billion in 2026 to USD 6.99 billion by 2031, registering a 5.57% CAGR between 2026 and 2031. The shift from traditional shell eggs to shelf-stable, pathogen-reduced processed egg products is being driven by food manufacturers, HoReCa (Hotels, Restaurants, and Catering) operators, and modern retailers. These processed alternatives offer multiple advantages, including enhanced food safety, extended shelf life, and simplified logistics, making them a preferred choice. The processed egg market has demonstrated resilience in the face of challenges, such as outbreaks of highly pathogenic avian influenza (HPAI), which have disrupted the supply of shell eggs. Additionally, the bakery, confectionery, and sports nutrition industries are key contributors to market demand, as they rely on standardized protein inputs to maintain consistent quality in their products. In emerging economies, processed egg formats address cold-chain distribution limitations that hinder shell-egg supply. Furthermore, these formats align with stringent food-safety regulations that increasingly favor pasteurized products, further driving their adoption.

Key Report Takeaways

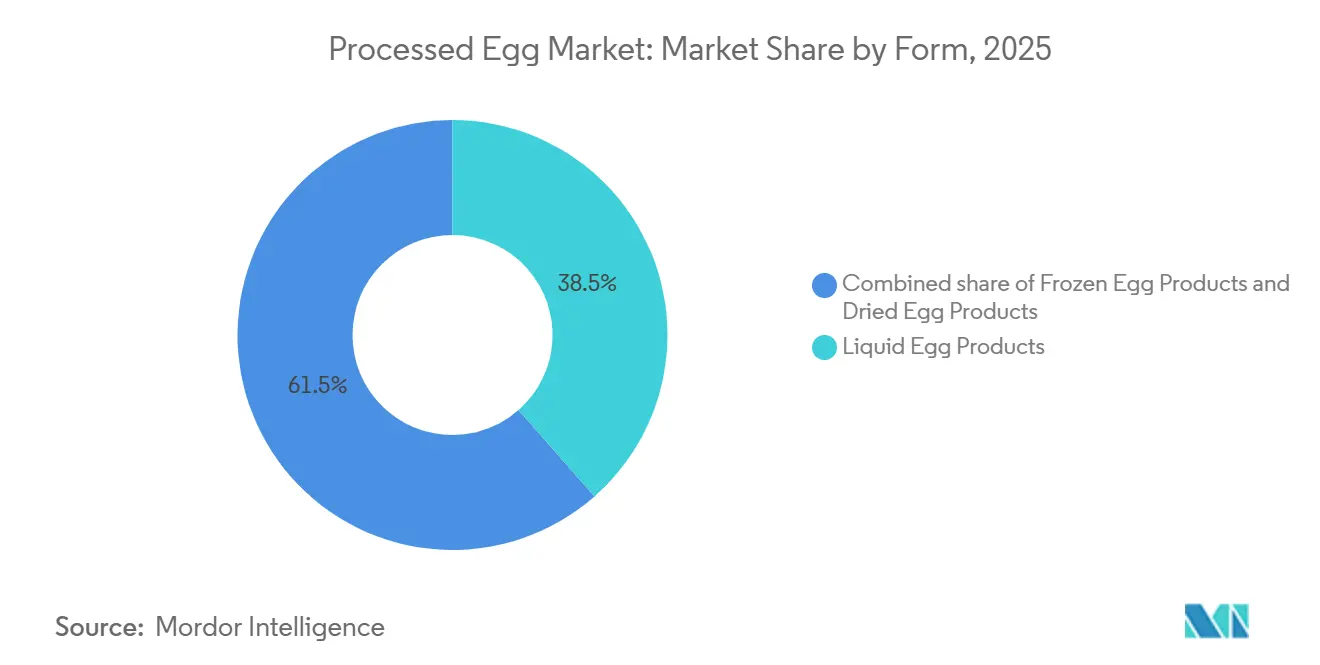

- By form, liquid egg products led with 38.52% processed egg market share in 2025, while frozen egg products are set to expand at a 7.35% CAGR through 2031.

- By product type, whole egg held 67.54% of the processed egg market size in 2025; egg white is advancing at a 6.91% CAGR to 2031.

- By end user, the HoReCa segment commanded 52.20% revenue in 2025 and is forecast to grow at a 7.15% CAGR over 2026-2031.

- By geography, North America maintained 36.24% share in 2025, whereas the Asia-Pacific is projected to register an 8.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Processed Egg Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of bakery and confectionery industries | +1.2% | Global, with concentration in North America, Europe, and urban Asia Pacific | Medium term (2-4 years) |

| Convenience-food demand and urban lifestyles | +1.4% | Asia Pacific core, spill-over to Middle East and Latin America | Long term (≥ 4 years) |

| Surge in protein-rich diet and sports nutrition | +0.9% | North America and Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| Food-safety focus and pasteurization mandates | +0.8% | Global, regulatory-led in North America and EU | Short term (≤ 2 years) |

| Technological advancements in egg processing and preservation | +0.7% | North America and Europe, gradual adoption in Asia Pacific | Long term (≥ 4 years) |

| Increased adoption of liquid egg products in foodservice | +1.1% | Global, accelerated in North America and Asia Pacific HoReCa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of bakery and confectionery industries

Industrial bakeries and confectionery manufacturers are increasingly integrating processed eggs into their production lines. This move aims to ensure batch consistency and cut down on labor costs tied to cracking and separating shell eggs. This trend is especially evident in high-volume categories like sandwich bread, cakes, and pastries. Here, liquid whole eggs and egg yolks provide emulsification and moisture retention, eliminating the variability associated with shell eggs. The market is also buoyed by a rising trend among premium bakeries. The American Bakers Association reported a 4.2% uptick in United States commercial bakery output for 2024[1]Source: American Bakers Association, “State of the Baking Industry 2025,” americanbakers.org. This growth is fueled by a surge in demand for premium artisan breads and clean-label snack cakes, both of which require a higher egg-solid content. Food safety concerns are another driving force behind the bakery sector's shift to processed formats. A single contaminated shell egg poses a risk to an entire batch, but the use of pasteurized liquid eggs mitigates the Salmonella enteritidis threat right at the ingredient stage. Meanwhile, in Europe, the push for certified organic processed eggs is gaining momentum. This is largely due to the EU Regulation 2092/91 for organic bakery products, with manufacturers aiming to simplify compliance across their multi-country operations.

Convenience-food demand and urban lifestyles

Urbanization across the Asia Pacific and Middle Eastern markets is significantly reducing meal-preparation time, driving a surge in demand for ready-to-eat and ready-to-cook meal formats. These formats increasingly rely on processed eggs as a convenient and reliable protein source. This shift in consumer behavior is creating a preference for shelf-stable and refrigerated processed egg products, which are more durable and less susceptible to breakage during last-mile delivery compared to fragile shell eggs. In China, egg production reached an impressive 35.88 million metric tons in 2024, as reported by the China National Bureau of Statistics[2]Source: China National Bureau of Statistics, "National data", data.stats.gov.cn. Urbanization is reshaping the distribution landscape, with consumers moving away from traditional wet markets and embracing modern retail outlets and foodservice channels. This transition is fueling demand for liquid and frozen egg products. Additionally, the growing need for convenience is evident in the foodservice sector, where labor shortages are encouraging quick-service restaurants and hotel kitchens to replace the manual cracking of shell eggs with pre-portioned liquid egg products. These products not only reduce preparation time but also enhance operational efficiency.

Surge in protein-rich diet and sports nutrition

Egg white protein is increasingly gaining popularity in sports nutrition and functional food applications, primarily due to its complete amino acid profile, high biological value, and its clean-label positioning when compared to whey and soy protein isolates. Gaspari Nutrition's Proven Egg line, which delivers 25 grams of protein per scoop, serves as a notable example of the growing commercialization of egg white protein within the sports supplement category. This rising trend is further driven by growing consumer distrust of synthetic additives. The single-ingredient transparency of egg white protein strongly appeals to clean-label advocates and aligns with the global sports nutrition market's ongoing shift toward whole-food-based protein sources. Furthermore, according to the International Food Information Council, 70% of Nutrient consumers in the United States are expected to prioritize protein consumption by 2025, underscoring the increasing demand for high-quality protein options[3]Source: International Food Information Council, "Food & Health Survey 2025", ific.org.

Food-safety focus and pasteurization mandates

In North America and Europe, regulatory efforts to eliminate Salmonella enteritidis from the egg supply chain are driving increased adoption of pasteurized processed eggs. The FDA's Egg Safety Rule requires environmental testing and refrigeration for shell eggs, but pasteurized liquid, dried, and frozen formats provide a reliable alternative that complies with USDA FSIS pathogen-reduction standards without depending on on-farm controls. Mid-sized processors seeking to enhance food safety without the high costs of traditional thermal pasteurization are adopting radiofrequency pasteurization, which uses electromagnetic fields to achieve a 5-log Salmonella reduction while preserving the eggs' functional properties. Additionally, cold plasma and ozone-based systems are emerging as non-thermal methods to extend shelf life and reduce microbial load, though their commercial application remains limited to pilot-scale operations. HACCP certification has become a standard requirement for processed egg suppliers serving institutional foodservice and retail private-label markets, creating a compliance barrier that benefits established players with audit-ready traceability systems.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shell-egg price volatility | -0.9% | North America and Europe, episodic in Asia Pacific | Short term (≤ 2 years) |

| Outbreaks of avian influenza and other poultry diseases | -1.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Stringent food safety and hygiene regulations | -0.5% | North America and EU, emerging in Asia Pacific | Medium term (2-4 years) |

| Rising competition from plant-based egg alternatives | -0.4% | North America and Europe, nascent in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shell-egg price volatility

Processors face significant challenges due to shrinking margins and unstable contract pricing, driven by fluctuations in raw-material costs. These cost swings are primarily caused by feed-grain inflation, rising energy prices, and disruptions in layer flocks. Processors operating under fixed-price supply agreements experience margin compression when input costs increase, as they are unable to adjust prices accordingly. Conversely, processors who pass on these cost increases to customers risk losing market share to competitors, such as plant-based alternatives or large foodservice operators that choose to perform in-house shell-egg cracking. The issue is further exacerbated by the lengthy 18-24 month period required to rebuild layer flocks following disease-related culls. This prolonged recovery time results in extended periods of supply shortages, which tend to favor vertically integrated producers with their own captive flocks. In contrast, merchant processors, who rely on spot-market purchases, are left at a competitive disadvantage during these periods of supply tightness.

Stringent food safety and hygiene regulations

Small and mid-sized processors encounter significant challenges due to the capital and operational costs associated with complying with the FDA's Egg Safety Rule, USDA FSIS pathogen-reduction standards, and HACCP protocols. The FDA's Egg Safety Rule imposes stringent requirements, including environmental testing, refrigeration during storage and transport, and the implementation of traceability systems that connect shell eggs to their originating farms. These measures substantially increase regulatory compliance costs, particularly for processors who source from multiple suppliers. Similarly, in the European Union, Regulation 834/2007 mandates that egg products marketed as organic must obtain organic certification. This process involves third-party audits and the establishment of segregated processing lines, which heighten capital intensity for producers. Although these regulations are designed to enhance food safety and strengthen consumer confidence, they inadvertently create barriers to entry. These barriers restrict competition and slow the adoption of processed eggs, especially in price-sensitive markets such as institutional foodservice and retail private-label channels, where cost considerations are critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominates, Frozen Accelerates

In 2025, liquid egg products commanded a dominant 38.52% share of the market, underscoring their pivotal role in industrial bakeries, quick-service restaurants, and institutional foodservice operations. These sectors value the ease of handling and precise portion control that liquid formats provide. By using liquid formats, businesses can sidestep the labor-intensive tasks of shell-egg cracking and separation, minimize waste from broken shells, and seamlessly integrate into the automated mixing and dispensing systems favored by high-volume food manufacturers. Meanwhile, dried egg products, prized for their ability to be stored at ambient temperatures and their extended shelf life, find specialized uses in military rations, emergency food supplies, and export markets. These markets often grapple with limited cold-chain infrastructure. Additionally, the use of spray drying technology allows processors to convert liquid eggs into powder with moisture content below 5%. This not only extends the product's shelf life but also empowers processors to capitalize on surplus production and navigate seasonal price fluctuations.

Frozen egg products are set to lead the pack, with a projected CAGR of 7.35% through 2031. This growth is buoyed by strategic investments in cold-storage infrastructure across Asia Pacific and the Middle East, particularly in foodservice hubs. Merging the best of both worlds, frozen formats offer the immediate convenience of liquid eggs while boasting the long shelf stability characteristic of dried products. With a refrigerated shelf life spanning 12-18 months, they perfectly cater to the inventory-management demands of regional distributors and multi-unit restaurant operators. The segment's upward trajectory is further fueled by the burgeoning presence of international hotel chains and Western-style quick-service restaurants. In markets like Vietnam, Indonesia, and the Philippines, these establishments leverage frozen egg products to standardize their menus, sidestepping dependence on local shell-egg supply chains.

By Product Type: Whole Egg Leads, Egg White Surges

In 2025, whole egg formulations accounted for 67.54% of the market, driven by their adaptability in bakery, confectionery, and prepared-food sectors. These applications benefit from the yolk's emulsification properties and the white's foaming capabilities. Whole eggs are essential in creating mayonnaise, custards, and pasta dough, where the combined functionality of yolk and white is crucial for achieving the desired texture and flavor. The segment demonstrates maturity with steady growth, primarily attributed to population increases and per-capita egg consumption, rather than significant changes in demand. Egg yolk, while holding a smaller market share, serves specialized roles in sauces, dressings, and ice cream. Its unique emulsifying qualities and rich mouthfeel justify the additional costs of separation and processing.

Egg white is projected to grow at a strong CAGR of 6.91% through 2031. This growth is fueled by its popularity in sports nutrition, protein supplements, and the increasing demand for clean-label functional foods, leveraging egg white's high 83.3% protein density and complete amino acid profile. Gaspari Nutrition's Proven Egg line, which provides 25 grams of protein per scoop, exemplifies egg white's commercial success in sports supplements. Similarly, Sussex Wholefoods caters to fitness enthusiasts and meal-replacement brands with its egg white powder. The bakery industry also supports this growth, utilizing egg white's unmatched foaming properties in meringues, macarons, and angel food cakes, outperforming plant-based alternatives. However, challenges persist: egg white's reliance on separation technology and the need to monetize the co-product yolk create margin pressures. This situation increasingly benefits vertically integrated processors with diverse product portfolios.

By End User: HoReCa Dominates and Accelerates

In 2025, HoReCa channels constituted 52.20% of end-user demand and are anticipated to grow at a 7.15% CAGR through 2031. This growth stems from labor shortages and rising wages, prompting restaurants, hotels, and catering services to shift from shell-egg cracking to pre-portioned liquid formats. Quick-service restaurants and hotel breakfast buffets are increasingly adopting liquid egg products to ensure consistent portion control, reduce preparation time, and minimize waste from broken shells. The foodservice industry's preference for liquid eggs is further supported by food safety concerns. A single contaminated shell egg can result in a health department citation, whereas pasteurized liquid eggs, with their 5-log pathogen reduction, comply with regulatory safe-harbor standards.

Industrial end users, including food manufacturing and non-food sectors, rely on processed eggs for batch consistency, pathogen reduction, and functional performance. These applications range from pasta and baked goods to cosmetics and pharmaceuticals. Food manufacturers favor liquid and dried egg formats that integrate seamlessly into automated production lines, eliminating the variability and labor costs associated with shell-egg cracking and separation. Although smaller in scale, non-food applications are significant: egg-based binders in pharmaceutical tablets and egg whites in cosmetics utilize hypoallergenic properties and film-forming characteristics, justifying their premium pricing.

Geography Analysis

In 2025, North America contributed 36.24% of the processed egg market revenue, driven by strict safety regulations and an integrated supply chain connecting layer farms to processors. In 2024, HPAI significantly reduced supply, causing shell-egg prices to reach record highs and triggering a surge in imports from Brazil in early 2025. Despite this disruption, processors restored capacity through biosecurity improvements and restocking efforts. By late 2025, Cal-Maine had stabilized its flocks at 44.51 million hens. Canada and Mexico provided additional volumes, with Mexico emerging as a cost-efficient processing hub for U.S. buyers. California's cage-free mandate is transforming the West Coast's supply chain, encouraging the adoption of capital-intensive cage-free barns and processed formats to reduce seasonal price volatility.

Asia-Pacific is set to be the fastest-growing region, with an expected 8.43% CAGR through 2031. China, the largest global producer of raw eggs, has processed egg penetration below 10%, presenting significant growth potential as urban wet markets decline. In India, while modern layer farms and cold-chain facilities are receiving support, fragmented regulations are slowing the adoption of retail processed foods. Southeast Asia, supported by tourism-driven foodservice investments, is experiencing double-digit liquid-egg import growth in Vietnam and the Philippines.

Europe, South America, and the Middle East and Africa complete the global market landscape. Europe's emphasis on animal welfare and organic labeling, though increasing costs, creates premium market opportunities. Companies such as Eurovo, Interovo, and Groupe Avril capitalize on their multi-country operations. Brazil's export surge to the U.S. during HPAI-related shortages highlighted South America's role as a contingency supplier. In the Gulf Cooperation Council states, investments in cold storage facilities aim to support the growing hospitality market, driving demand for frozen eggs.

Competitive Landscape

The processed egg market demonstrates moderate concentration, with leading players holding a significant share of global capacity. However, regional fragmentation remains due to the perishable nature of liquid eggs and the logistical advantages of localized processing. Producers like Cal-Maine Foods, which oversees 44.51 million hens across various U.S. states, rely on captive layer flocks. This approach helps stabilize raw material costs and ensures long-term supply agreements with foodservice distributors and industrial clients. Diversified processors such as Michael Foods and Rembrandt Enterprises compete by offering a wide range of products, including liquid, dried, and frozen eggs, as well as value-added options like pre-cooked scrambled eggs and portion-controlled omelets, which are particularly beneficial for quick-service restaurants. Specialty players like Vital Farms are carving out premium retail niches by focusing on pasture-raised certifications and transparent supply chains.

Technological advancements are altering the competitive landscape. Innovations such as radiofrequency pasteurization, cold plasma, and ohmic heating enable mid-sized processors to meet USDA FSIS and FDA Egg Safety Rule standards without the high capital investment required for traditional thermal methods. Sanovo Technology Group and Moba B.V. are at the forefront of equipment innovation, offering modular processing lines that integrate breaking, pasteurization, and aseptic packaging into a single compact system, reducing capital requirements for regional processors entering the market.

White-space opportunities include egg white protein for sports nutrition, frozen egg products for the Asia Pacific foodservice sector, and organic certified formats for European retail. These segments challenge incumbents due to margin pressures or limited distribution reach. Emerging disruptors, such as plant-based egg startups Fabumin and Burcon-Puratos, are gaining traction in vegan bakery and foodservice applications. However, their functional performance and cost competitiveness still fall short compared to conventional eggs in most industrial applications.

Processed Egg Industry Leaders

-

Cal-Maine Foods Inc.

-

Michael Foods

-

Rose Acre Farms

-

Rembrandt Enterprises

-

Eurovo Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cal-Maine Foods is invested USD 75 million to boost its cage-free liquid egg production in Texas. This expansion will introduce 2 million layer hens and a new pasteurization line, set to process 500,000 pounds of liquid eggs weekly. With national quick-service restaurant chains pledging to source 100% cage-free by 2026, Cal-Maine's move positions it to seize additional market volume, especially as rivals grapple with certification deadlines.

- February 2025: Eurovo Group has acquired a Polish egg-processing facility from a regional competitor, boosting its capacity by 80,000 metric tons annually for liquid and dried eggs. This move caters to Central European bakery and pasta manufacturers. The acquisition not only solidifies Eurovo's foothold in the EU market but also offers geographic diversification amid moderating growth in Western Europe.

- January 2025: Michael Foods, a subsidiary of Post Holdings, has unveiled a new range of organic liquid egg whites. These egg whites, certified by the USDA National Organic Program and sourced from cage-free flocks, are aimed at North America's sports-nutrition and foodservice sectors. Priced at a 20% premium over their conventional counterparts, the product caters to the rising consumer demand for clean-label protein.

- December 2024: Rembrandt Enterprises has formed a partnership with a Chinese cold-chain logistics provider to distribute frozen egg products in tier-two and tier-three cities. Utilizing the partner's refrigerated trucking network, the company aims to access markets that have traditionally depended on dried egg powder. This partnership is projected to generate an additional USD 15 million in revenue by 2026.

Global Processed Egg Market Report Scope

Processed egg products are obtained by breaking the egg and processing the liquid inside to get an acceptable egg product. The processed egg market report is segmented by form, product type, end user, and geography. By form, the market is segmented into liquid, dried, and frozen. By product type, the market is segmented into whole egg, egg yolk, and egg white. By end user, the market is segmented into industrial, horeca, and retail. By Geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. Market forecasts are provided in terms of value (USD) and volume (Tons) for all the above segments.

By Form

| Liquid Egg Products |

| Dried Egg Products |

| Frozen Egg Products |

By Product Type

| Whole Egg |

| Egg Yolk |

| Egg White |

End User

| Industrial | Food Manufacturing |

| Non-Food End Use | |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Speciality Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Liquid Egg Products | |

| Dried Egg Products | ||

| Frozen Egg Products | ||

| By Product Type | Whole Egg | |

| Egg Yolk | ||

| Egg White | ||

| End User | Industrial | Food Manufacturing |

| Non-Food End Use | ||

| HoReCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Speciality Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the processed egg market be by 2031?

It is projected to reach USD 6.99 billion by 2031, growing at a 5.57% CAGR from 2026.

Which form is expanding the fastest?

Frozen egg products are forecast to post a 7.35% CAGR through 2031, fueled by Asian and Middle Eastern foodservice demand.

Why are HoReCa buyers switching to liquid eggs?

Liquid eggs cut prep time by up to 40%, lower labor costs, and meet stringent food-safety standards, driving a 7.15% CAGR in HoReCa uptake.

What drives the rise of egg-white protein?

Egg white offers 83.3% protein density and clean-label appeal, supporting a 6.91% CAGR in egg-white demand, especially for sports nutrition.

Page last updated on: