Plant-based Egg Replacers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

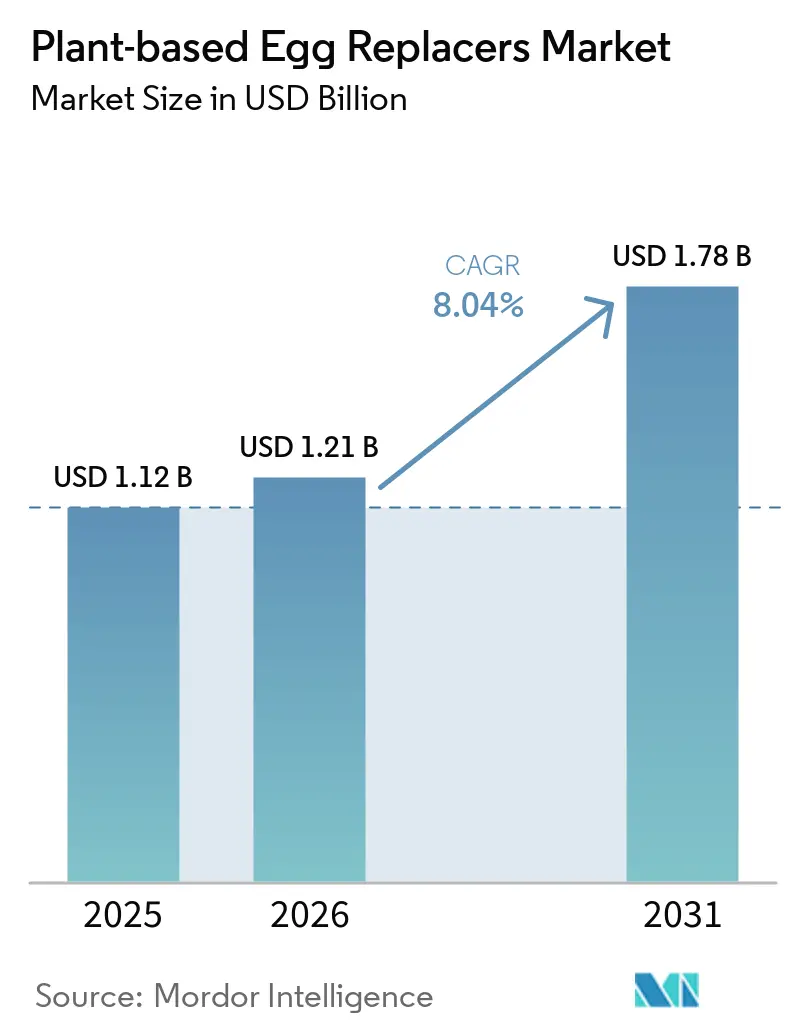

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 8.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plant-based Egg Replacers Market Analysis by Mordor Intelligence

The plant-based egg replacer market size was valued at USD 1.12 billion in 2025 and is estimated to grow from USD 1.21 billion in 2026 to USD 1.78 billion by 2031, at a CAGR of 8.04% during the forecast period (2026-2031). In 2026, demand stays closely linked to the need for supply stability, allergen management, and ingredient systems that can match egg performance in large-scale food production. Buyers are now using these ingredients less as a niche vegan claim and more as a practical way to reduce exposure to egg price swings and supply shocks. The 2025 avian influenza disruption changed procurement behavior in a lasting way, especially for bakery, sauce, and processed-food manufacturers that need dependable volumes across long production runs. Label transparency and allergy-related compliance are also expanding the role of these ingredients in packaged foods, as manufacturers seek simpler formulas and clearer allergen declarations across more product lines. The plant-based egg replacer market, therefore, remains open to both large ingredient suppliers and focused specialists that can deliver strong application support, consistent functionality, and reliable access to raw materials.

Key Report Takeaways

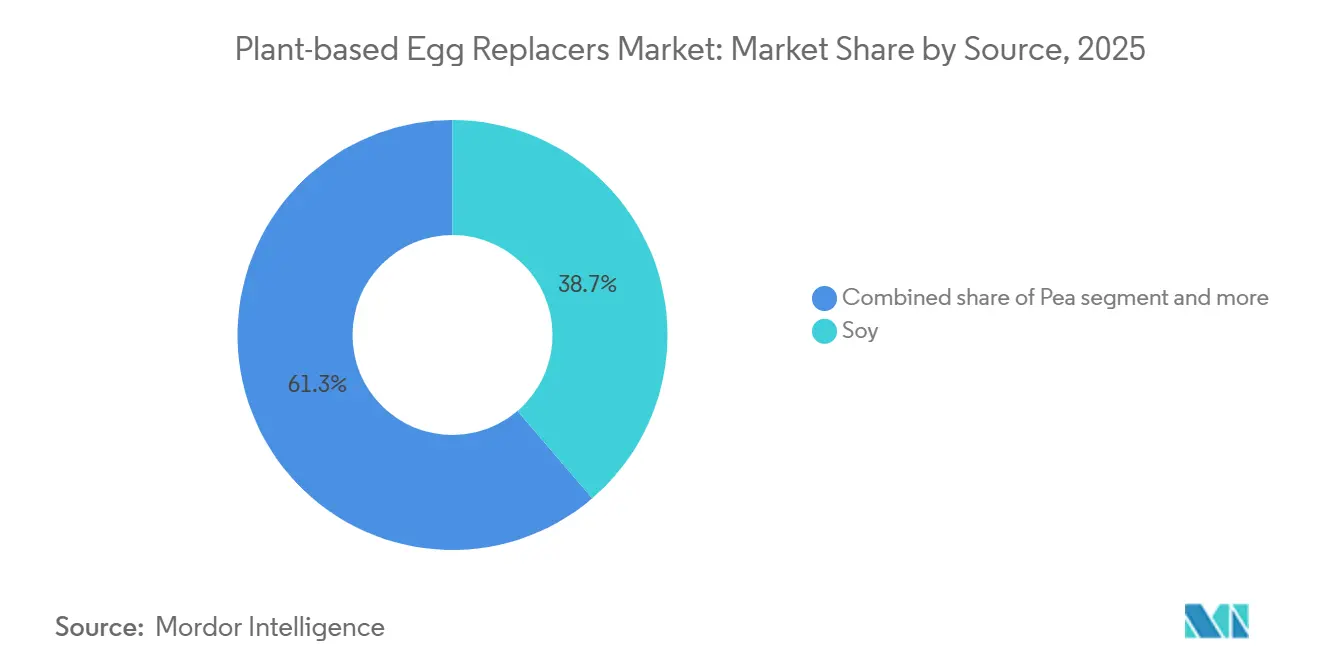

- By source, soy held 38.73% of the plant-based egg replacers market share in 2025, while pea is projected to grow at an 8.67% CAGR through 2031.

- By form, powder accounted for 63.56% of the plant-based egg replacers market size in 2025, while liquid is forecast to expand at an 8.75% CAGR through 2031.

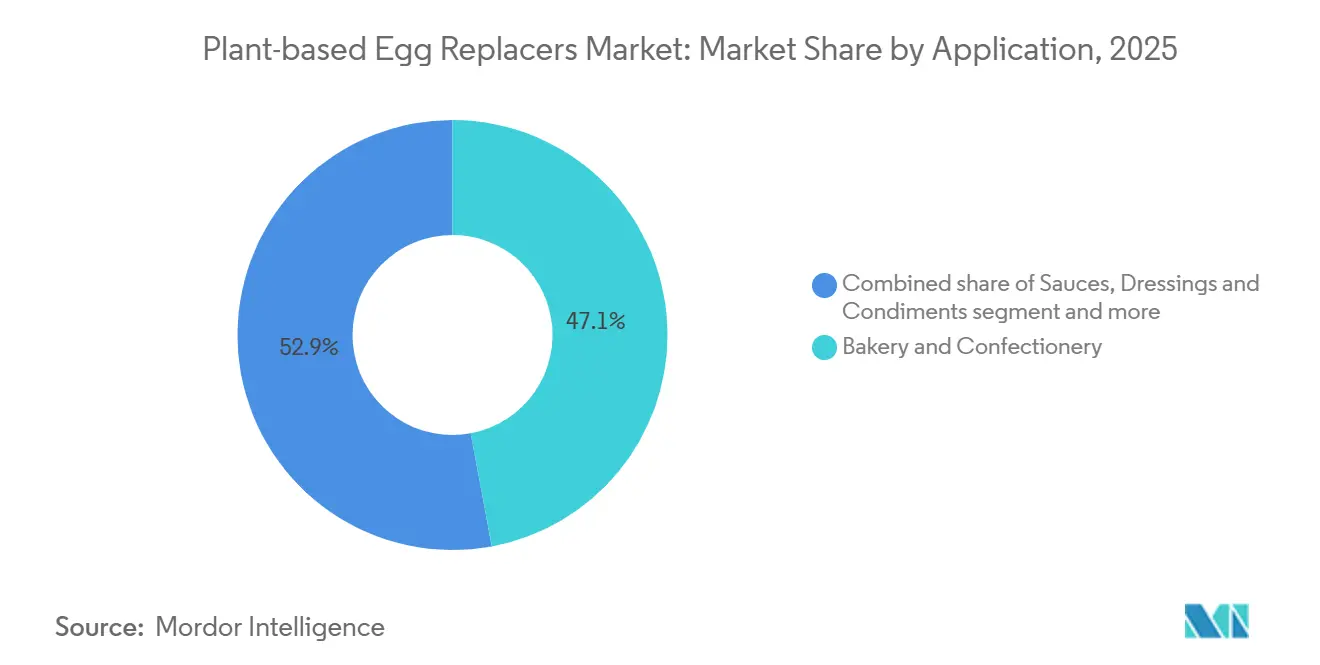

- By application, bakery and confectionery accounted for 47.08% of the plant-based egg replacer market in 2025, while sauces, dressings, and condiments are advancing at a 9.19% CAGR through 2031.

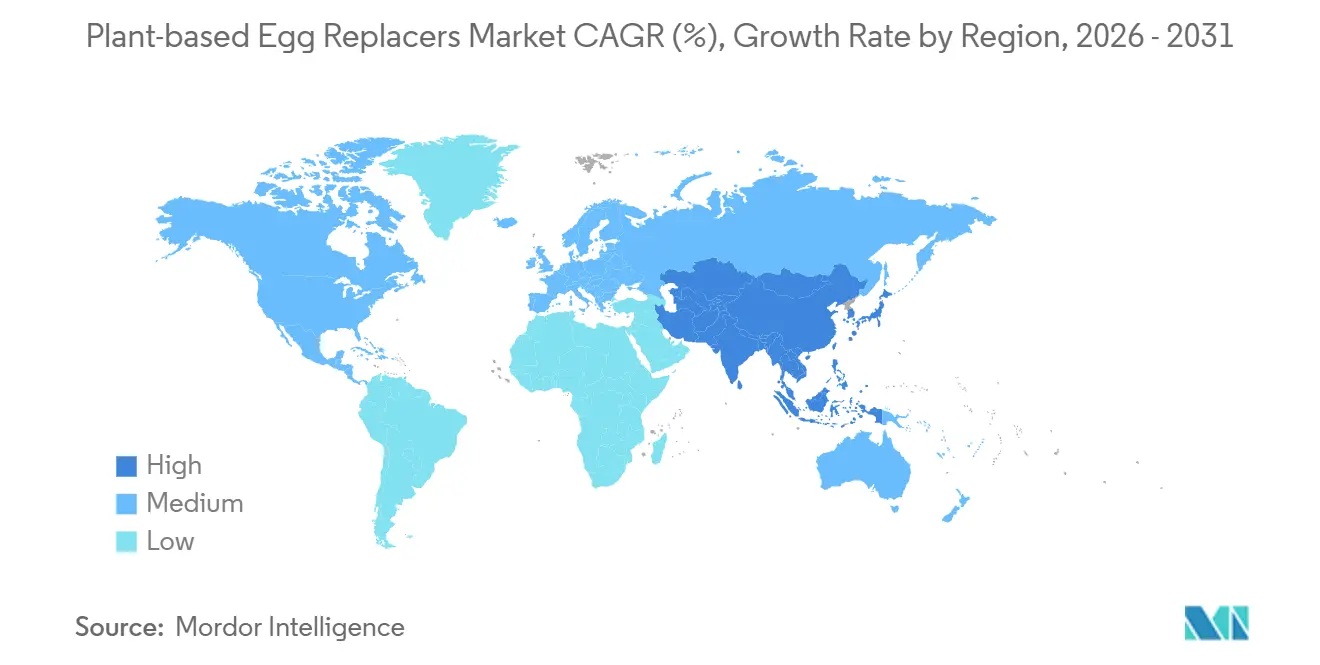

- By geography, North America held 44.36% of the plant-based egg replacers market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 9.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plant-based Egg Replacers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vegan and Flexitarian Adoption | +1.6% | Global, led by Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Clean-label Reformulation Across Bakery and Sauces | +1.3% | North America and Europe, spreading to Asia-Pacific urban centers | Medium term (2-4 years) |

| Egg Allergy and Cholesterol-free Positioning | +1.0% | Global, with higher relevance in North America and Europe | Medium term (2-4 years) |

| Demand for Functional Performance Parity in Industrial Baking | +0.9% | Global, strongest in North America, Europe, and Japan | Long term (≥ 4 years) |

| Growing Demand for Egg-free Bakery and Confectionery | +1.2% | Global, with Asia-Pacific and South America accelerating | Long term (≥ 4 years) |

| Technical Service-led Co-development by Ingredient Suppliers | +0.7% | North America and Europe, with early gains in Japan and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising vegan and flexitarian adoption

Flexitarianism, rather than strict veganism, is the primary structural driver of demand for plant-based egg replacers. Circana's 2025 data covering six EU core markets recorded plant-based food and drink revenues at EUR 16.3 billion, growing at +5.1% year on year between 2024 and 2025, with flexitarians expanding from 21% of Europeans in 2023 to 31% in 2024, making them the single largest diet-identity group ahead of omnivores in several national markets. Germany leads continental Europe: the Good Food Institute Europe reported that the German plant-based retail market reached EUR 1.71 billion in 2025, with value growth of 3.1% and volume growth of 6.2% versus 2024, with plant-based milk driving the largest absolute volume gains. In the United States, the Plant Based Foods Association and SPINS reported the retail plant-based food market at USD 7.9 billion in 2025, held largely steady despite modest unit-volume headwinds, with the Midwest emerging as the fastest-growing region at +2.4% in sales growth, indicating that flexitarian demand is spreading beyond coastal strongholds. The implication for ingredient formulators is that retailers and QSRs now require ingredient systems capable of performing across high-volume, cost-sensitive mainstream formats, not just premium SKUs, which expands the addressable market for industrial-grade plant-based egg replacers considerably.

Clean-label reformulation across bakery and sauces

Clean-label reformulation has moved from a differentiator to an operational mandate for bakery and sauce producers in 2026, reshaping the specification criteria for functional egg-replacement systems. Puratos presented its concept of "beyond clean label" at IDDBA 2026, arguing that ingredient transparency is now the foundation upon which additional consumer benefits, such as fiber enrichment and gut health, must be built, not an end goal in itself. ADM's 2026 bakery strategy, outlined at the World Bakers platform, explicitly prioritized clean-label reformulation in EMEA, focused on "recognizable ingredients to support positive nutritional attributes such as fiber, protein, and functional benefits". A downstream compliance consideration is the US "Make America Healthy Again" (MAHA) initiative, which gained legislative momentum in 2025 with accelerated timelines for removal of FD&C certified synthetic colors from seasonal bakery SKUs, effectively narrowing the permissible ingredient toolkit and elevating natural functional systems, including plant protein–based egg replacers, as compliant alternatives. Regulatory influence on labeling standards is thus creating a pull-through effect that benefits suppliers offering single-ingredient, recognizable-name plant proteins over multi-component synthetic blends.

Egg allergy and cholesterol-free positioning

Egg allergy prevalence creates a persistent, medically driven demand channel that is immune to commodity egg price cycles. According to the Food Allergy Research & Education (FARE) organization, approximately 2.7 million U.S. children and adults carry an egg allergy, making eggs one of the top nine major food allergens, a status enshrined through the FDA's Food Allergen Labeling and Consumer Protection Act (FALCPA) and reinforced by the FASTER Act of 2021[1]Source: Food Allergy Research & Education, “Food Allergy Facts and Statistics,” Food Allergy Research & Education, foodallergy.org. The CDC's National Center for Health Statistics reported in January 2026, using 2024 National Health Interview Survey data, that 6.7% of adults and 5.3% of children in the United States have a diagnosed food allergy, a broader population base that creates labeling compliance obligations for nearly every mid- to large-sized food manufacturer[2]Source: Amanda E. Ng, “Diagnosed Allergic Conditions in Children Ages 0–17, United States, 2024,” National Center for Health Statistics, cdc.gov . Beyond allergy management, the cholesterol-free positioning of plant-based egg replacers is clinically relevant: egg yolk is the most concentrated dietary source of cholesterol at approximately 185 mg per egg, and product reformulations that eliminate this while maintaining consumer-preferred texture directly support cardiovascular wellness claims that command premium shelf positioning. The regulatory compliance dimension here, FALCPA labeling and major allergen declarations, ensures steady volume demand irrespective of market cycles, providing formulators with a structural demand floor.

Demand for functional performance parity in industrial baking

Industrial bakery manufacturers are pushing ingredient suppliers toward application-specific performance equivalence rather than broad-spectrum egg substitution. Ingredion's protein fortification business, which includes pea protein isolates positioned for egg replacement, delivered a record year in 2025 with net sales growth exceeding 40%, and the company reported full contracted capacity for 2026, indicating that long-term supply agreements are now the commercial norm rather than spot procurement. A notable second-order dynamic is the role of GLP-1 weight management medications in reshaping industrial formulation priorities: Ingredion's management noted on investor calls that the GLP-1 user base is actively driving demand for smaller, protein-dense, satiating formats in bakery, and plant-based protein systems that deliver binding and structure at lower inclusion levels (such as Lasenor's VP-100 pea protein, effective at 0.5%–2.0% of formulation) align directly with this requirement. The performance benchmarking rigor demanded by industrial bakers is paradoxically strengthening specialist suppliers with deep application-lab capabilities, a dynamic that rewards companies that invest in co-development infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Functional Gap Versus Whole Egg in Aeration and Emulsification | -1.8% | Global, most acute in premium bakery segments in EU and North America | Long term (≥ 4 years) |

| Higher Formulation Cost Versus Commodity Eggs | -1.5% | Global, more pronounced in price-sensitive emerging markets in APAC and South America | Short term (≤ 2 years) |

| Label Acceptance Friction for Certain Hydrocolloids and Novel Inputs | -0.9% | North America & EU, where clean-label compliance scrutiny is highest | Medium term (2–4 years) |

| Reformulation Complexity for Industrial Food Manufacturers | -0.8% | Global, with concentration in mass-market processed food manufacturers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Functional gap versus whole egg in aeration and emulsification

Replicating the multifunctional performance of whole egg, simultaneously binding, emulsifying, aerating, and providing thermostable structure, remains the primary technical constraint limiting broader adoption of plant-based egg replacers in premium bakery applications. A 2025 study published in ScienceDirect evaluating compounded plant protein gels found that while soy-pea-chickpea composite systems showed the highest potential as egg substitutes, no single-protein system fully replicated the two-stage thermal gelation characteristic of egg whites. In fine patisserie and laminated dough applications, where egg's structural role is most pronounced, reformulation trials regularly require multi-ingredient compensation systems, enzyme combinations, hydrocolloid scaffolding, and starch modification, which increase research and development time and SKU complexity. Corbion's commercially validated strategy, launching separate Vantage 12E (up to 40% whole-egg reduction in cakes) and Vantage 11E (full-egg replacement in bread and buns) with distinct application claims, reflects the market reality that no single system spans the entire performance spectrum. Until a single clean-label input replicates the full functional stack of eggs in aerated batter systems, the premium bakery segment will remain a competitive frontier rather than a captive market.

Higher formulation cost versus commodity eggs

Even during periods of elevated shell egg prices, parity with isolated plant proteins is not guaranteed at the formulation system level. Cargill's HPAI-period egg price spike, with USDA data showing national retail prices reaching USD 6.23 per dozen in March 2025, accelerated plant-based system adoption in North America. Yet as HPAI cases fell approximately 45% year-on-year in early 2026 and wholesale egg prices declined by 86% from their 2025 peak, the cost calculation shifted back toward commodity eggs for price-sensitive SKUs. High-purity pea protein isolates suitable for industrial bakery applications incur raw material and processing costs that structurally exceed those of commodity dried whole egg on a per-function basis at current volumes. The ADM Arcon SFP case demonstrates that specific applications, high-egg-intensity products like panettone and enriched pasta, can achieve compelling economics, but lower-egg-intensity applications, such as basic bread and cookies, present a narrower economic case absent supply disruption. This cost sensitivity is a significant limiting factor in South America, MEA, and Southeast Asia, where egg affordability and availability remain high, constraining market penetration timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Pea Protein Rapidly Eroding Soy's Structural Advantage

Soy accounted for 38.73% of global plant-based egg replacer revenue in 2025, a position built on three decades of application data, cost-competitive extraction, and proven emulsification capacity in industrial sauces and bakery applications. ADM's Arcon SFP line and its broader soy isolate and concentrate portfolio, including its first textured vegetable protein launched in the 1960s, continue to underpin soy's dominance in high-egg-intensity formulations across South America and Southeast Asia, where soy processing infrastructure is densely established. A 2025 ScienceDirect study confirmed that soy protein isolate (SPI) remains the reference input for composite plant-based gel systems targeting egg white analog functionality, particularly in products requiring thermostable binding at temperatures above 80 °C.

Pea protein is growing at 8.67% CAGR (2026-2031), a rate that reflects structural advantages in clean-label compliance, non-GMO certification, and growing raw material availability following Roquette's expansion of its NUTRALYS portfolio in June 2025 with two new textured solutions, NUTRALYS T WHEAT 600L and NUTRALYS T PEA 700XC, designed specifically for industrial food manufacturers seeking functional scalability. Chickpea is gaining traction in bakery and confectionery, supported by Ingredion's March 2025 launch of chickpea protein isolates and flours targeting emulsification and foaming in vegan cakes and muffins, an allergen-free proposition that opens doors to retailers with strict label standards. Potato and algal sources remain niche but are advancing in specialist segments, with algal proteins gaining interest from DSM-Firmenich as part of precision nutrition platforms. The competitive shift from soy to pea is a structural trend, not a cyclical one, driven by European sourcing preferences and the regulatory trajectory around GM crop labelling.

By Form: Liquid Formats Gaining Ground in Foodservice and Ready Meals

Powder continues to represent 63.56% of 2025 revenue, a dominance rooted in logistics efficiency, extended shelf life, and compatibility with industrial continuous-mix systems used across bakery, dry mix, and confectionery manufacturing. For mass-market food processors managing global distribution, the shelf stability of powder egg replacers, typically 12 to 24 months, provides supply chain resilience that liquid formats cannot match without cold chain infrastructure. Puratos' clean-label enzyme-based Acti range, detailed at IDDBA in March 2026, functions in a dry-applied format, enabling 15–50% egg reduction in patisserie with no reformulation of existing powder-handling lines, demonstrating that powder systems still drive meaningful efficiency gains.

Liquid formats are the fastest-growing form, with a 8.75% CAGR (2026-2031), driven by the expansion of foodservice operators, ready-meal manufacturers, and food-to-go chains that use precision dosing systems and can accommodate refrigerated supply chains. Eat Just's Just Egg liquid product, made from mung bean protein, exemplifies the liquid format's consumer-facing momentum: the brand reported a 5-fold acceleration in sales growth in January 2025 during the HPAI egg shortage, with 56% repeat purchase rates (a 3-point improvement from 2024). Tate & Lyle's November 2025 presentation of its HAMULSION Stabiliser System for egg-free pourable dressings specifically targets the liquid application category, underscoring that major ingredient players are directing formulation innovation toward this rapidly growing format.

By Application: Sauces and Dressings Emerging as the Next High-Value Frontier

Bakery and confectionery at 47.08% market share in 2025 reflects a well-established demand base where egg replacers have the deepest functional validation and most extensive supplier portfolios. Industrial baking is where supply chain economics most clearly favor plant-based systems: CSM Ingredients' Egg 'n Easy Plus, a powder solution for yeast dough and batter applications co-developed with HIFOOD, was positioned as a cost-effective, customizable system directly addressing avian flu–era supply pressures, with launch coverage spanning commercial bakeries globally. In sponge cakes and muffins, Lasenor's VP-100 pea protein (developed with Meala FoodTech) achieved 50–100% egg reduction while maintaining aeration and moisture retention, a validated commercial proposition that is accelerating specification reviews at large-format cake producers in Europe.

Sauces, dressings, and condiments are the fastest-growing application segment at 9.19% CAGR (2026–2031), driven by the emulsification functionality of pea and soy proteins that closely mimics egg yolk lecithin, a property of increasing commercial importance as clean-label and vegan-certified condiment brands expand their product ranges. Tate & Lyle's HAMULSION system, Cargill's lecithin-led emulsification strategy, and Fiberstar's multifunctional citrus fiber systems collectively represent a wave of purpose-built egg replacement tools for the sauces segment. Snacks and savory products and processed foods are growing steadily, with the former benefiting from allergen-free reformulation mandates in export-market SKUs and the latter driven by cost-management initiatives in ready-meal manufacturing. Meat and seafood analogue applications remain early-stage but are strategically significant as blended protein matrices for texture replication increasingly incorporate egg-replacer functional systems.

Geography Analysis

North America accounted for 44.36% of the plant-based egg replacer market in 2025, and the region maintained its lead as avian influenza highlighted the vulnerability of the conventional egg supply. USDA data showed that U.S. egg production for the year ending November 2025 was 105 billion eggs, down 4% from 2024, while the average layer flock was 3% lower year over year[3]Source: U.S. Department of Agriculture, “Chickens and Eggs Annual Report,” USDA National Agricultural Statistics Service, nal.usda.gov . The Congressional Research Service also noted that U.S. retail egg prices reached USD 6.23 per dozen in March 2025, which pushed many food companies to review longer-term substitute strategies. USDA then committed up to USD 1 billion to a five-pronged response, which showed how serious the supply disruption had become at the national level. The United States drives most regional volume, while Canada is seeing steady reformulation activity, and Mexico is gaining importance as food manufacturing capacity expands.

Europe held the second-largest share of the plant-based egg replacer market, supported by strong clean-label expectations and greater attention to animal welfare standards. Germany and France remain the main anchors because they combine large food manufacturing bases with active demand for plant-based product development. The region also gives an edge to ingredients that fit simple labels and predictable regulatory pathways, which is helping pea and other non-soy options gain more ground. Across the plant-based egg replacers market, Europe stands out less for short-term supply shocks and more for the steady pull of reformulation, label clarity, and compliance.

Asia-Pacific is the fastest-growing region, with the plant-based egg replacers market size in the region forecast to rise at a 9.38% CAGR through 2031. China and India are the main growth engines, though they support demand in different ways, with China offering large-scale ingredient processing and India offering a strong pulse protein base. Japan, South Korea, and Australia are important for premium foodservice and higher-value formulations where quality and clean-label claims can carry better pricing. Southeast Asia is still earlier in development, but urban food demand and modern retail growth are opening more room for egg-free bakery, sauces, and ready-to-eat products. South America and the Middle East and Africa remain smaller, yet Brazil, the United Arab Emirates, and South Africa are becoming useful footholds for distribution and regional manufacturing in the plant-based egg replacers market.

Competitive Landscape

The plant-based egg replacer market is moderately concentrated, with Ingredion, ADM, Cargill, Kerry Group, and Roquette Frères holding significant positions without controlling the market. That balance keeps competition active because food manufacturers still compare suppliers on functionality, price, technical support, and ingredient availability. No single company leads across every source category, application, and geography, leaving room for mid-sized specialists to win business. The plant-based egg replacer market also has relatively high switching costs after validation, but they are not high enough to shut out challengers. This keeps the market stable at the top while still allowing movement in account wins and application niches.

A second layer of competition comes from specialists such as Corbion, BENEO, and Puratos, as well as newer companies working on more advanced protein systems. These players often focus on specific use cases, such as cakes, bread, sauces, or clean-label bakery formulas, rather than trying to serve every product type at once. The plant-based egg replacer market is also under pressure from fermentation-enabled entrants targeting the highest-performance applications where plant proteins still fall short. Intellectual property, application know-how, and process validation support now matter almost as much as ingredient cost. That is why the plant-based egg replacer market increasingly rewards suppliers that can solve a customer's production problem rather than simply selling a replacement ingredient.

Recent strategic moves show how leading companies are seeking to strengthen their positions in the plant-based egg replacer market. ADM launched 8 new plant-based protein products across North America and Europe in May 2026, strengthening its portfolio of soy isolates, concentrates, and diversified protein solutions for food manufacturers. Roquette expanded its NUTRALYS range in June 2025 with new textured wheat and pea proteins, which support its push into next-generation protein applications. Ingredion reported record 2025 growth in protein fortification and full contracted capacity for 2026, which signals strong customer commitment where functionality has already been proven. Together, these moves show that the plant-based egg replacers market is being shaped by scale, portfolio depth, and the ability to support customers through reformulation work.

Plant-based Egg Replacers Industry Leaders

Ingredion Incorporated

Archer Daniels Midland Company

Cargill, Incorporated

Kerry Group plc

Roquette Frères

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Puratos detailed its Acti range of clean-label enzyme solutions at IDDBA 2026, demonstrating that the system enables 15–50% egg reduction in patisserie while maintaining volume and texture. The company framed clean-label functionality as a commercial floor, not a differentiator, signaling a structural shift in industrial bakery specification standards.

- November 2025: Tate & Lyle presented HAMULSION Stabilizer System for egg-free pourable dressings at a major industry event, targeting the fast-growing sauces and condiments application segment. The system is designed to replicate egg yolk's emulsification and structural functions without any animal-derived inputs, providing clean-label compliance for sauce and dressing manufacturers.

- April 2025: Innophos launched LEVAIR Egg Replace for commercial bakeries, enabling full or partial replacement of egg yolks and dried whole eggs in cakes, donuts, muffins, and sponge cakes. The solution addresses cost volatility, supply chain disruptions, and microbiological safety risks associated with shell eggs in commercial baking.

- June 2024: Palsgaard and Aarhus University launched the EUR 5 million PIER (Plant-based Ingredients for Egg Replacement) project, inviting food manufacturers into a co-creation program focused on reducing egg use in bakery and desserts by 10% of global usage. The initiative is designed to give early participants first-mover access to validated replacement systems.

Global Plant-based Egg Replacers Market Report Scope

Plant-based egg replacers are ingredients derived from plant sources that replicate the binding, emulsifying, leavening, and textural properties of eggs in food formulations. The plant-based egg replacers market is segmented by source, form, application, and geography. By source, the market includes soy, pea, chickpea, potato, and other plant-based sources. Based on form, the market is categorized into powder, liquid, and other forms. By application, the market covers bakery and confectionery, sauces, dressings and condiments, snacks and savory products, processed foods and ready meals, meat and seafood alternatives, and other applications. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been conducted on a value basis (USD).

| Soy |

| Pea |

| Chickpea |

| Potato |

| Others |

| Powder |

| Liquid |

| Others |

| Bakery and Confectionery |

| Sauces, Dressings and Condiments |

| Snacks and Savory Products |

| Processed Foods and Ready Meals |

| Meat and Seafood |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Source | Soy | |

| Pea | ||

| Chickpea | ||

| Potato | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Application | Bakery and Confectionery | |

| Sauces, Dressings and Condiments | ||

| Snacks and Savory Products | ||

| Processed Foods and Ready Meals | ||

| Meat and Seafood | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the plant-based egg replacers market?

The plant-based egg replacers market stands at USD 1.21 billion in 2026 and is projected to reach USD 1.78 billion by 2031 at an 8.04% CAGR.

Why is North America leading demand for plant-based egg replacers?

North America led with 44.36% of revenue in 2025, helped by avian influenza-related egg supply disruption, higher egg prices, and faster reformulation by large food manufacturers.

Which source segment leads the plant-based egg replacers market?

Soy led the market with a 38.73% revenue share in 2025 because it has established processing capacity and a long history of use in binding and emulsification.

Which application area offers the strongest future growth?

Sauces, dressings, and condiments is the fastest-growing application at a 9.19% CAGR, driven by demand for egg-free emulsification systems.

Which form is growing fastest in egg replacement products?

Liquid is the fastest-growing form at an 8.75% CAGR through 2031, supported by foodservice, ready meals, and applications where easy dosing matters.

Page last updated on: