Saudi Arabia Eggs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

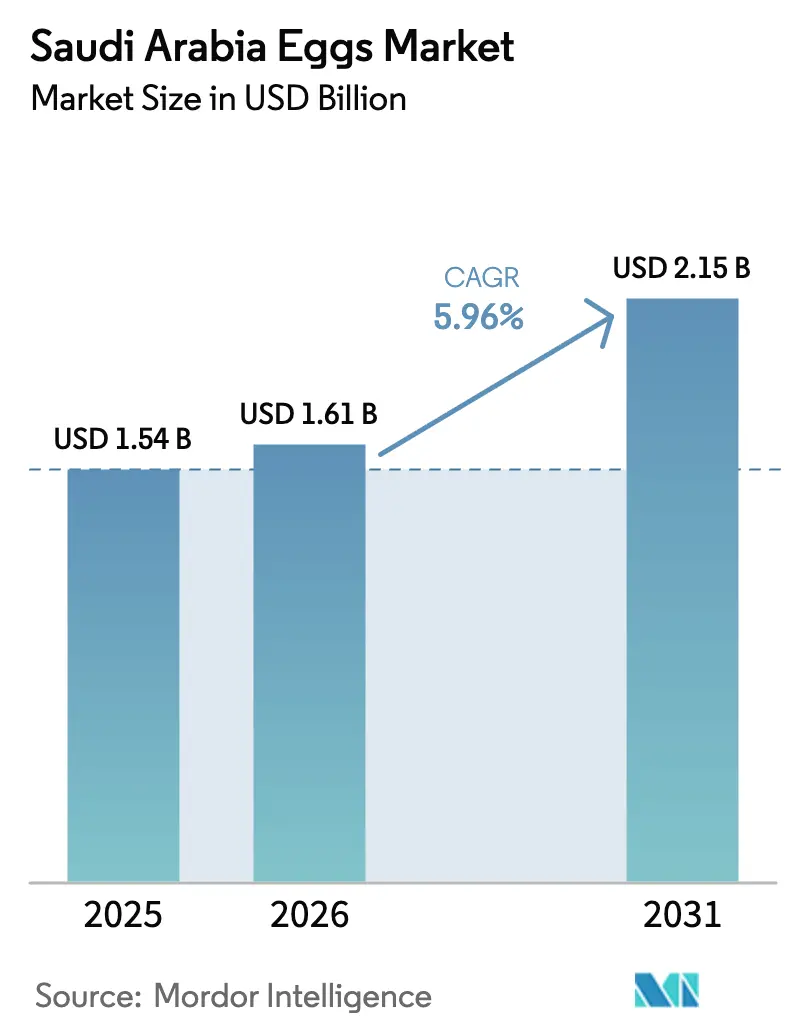

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

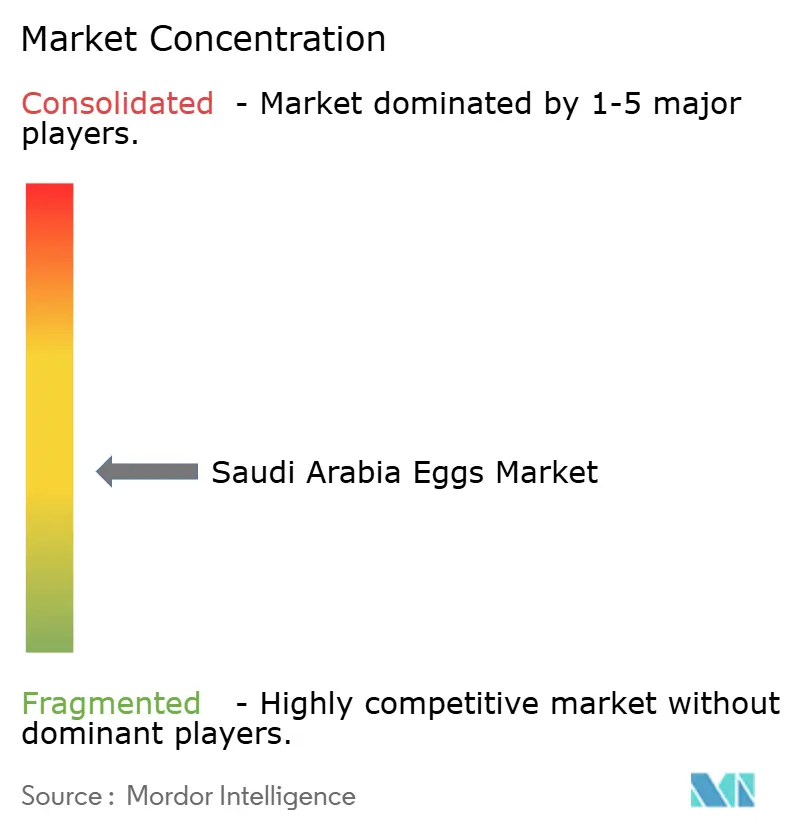

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Eggs Market Analysis by Mordor Intelligence

The Saudi Arabia eggs market size was valued at USD 1.54 billion in 2025 and is projected to grow from USD 1.61 billion in 2026 to USD 2.15 billion by 2031, registering a CAGR of 5.96% during the forecast period (2026-2031). This growth aligns with the Kingdom's focus on food security and agricultural self-sufficiency under Vision 2030, establishing the domestic egg industry as a key component of protein security. The government's agricultural funding of USD 2 billion by 2025 is driving significant infrastructure development, including the modernization of poultry farms, expansion of cold storage facilities, and adoption of advanced breeding technologies. These initiatives aim to enhance production efficiency and meet the growing domestic demand for eggs. Additionally, halal certification requirements enforced by the Saudi Food and Drug Authority present both compliance challenges and competitive opportunities for local producers, ensuring adherence to religious and quality standards while fostering consumer trust.

Key Report Takeaways

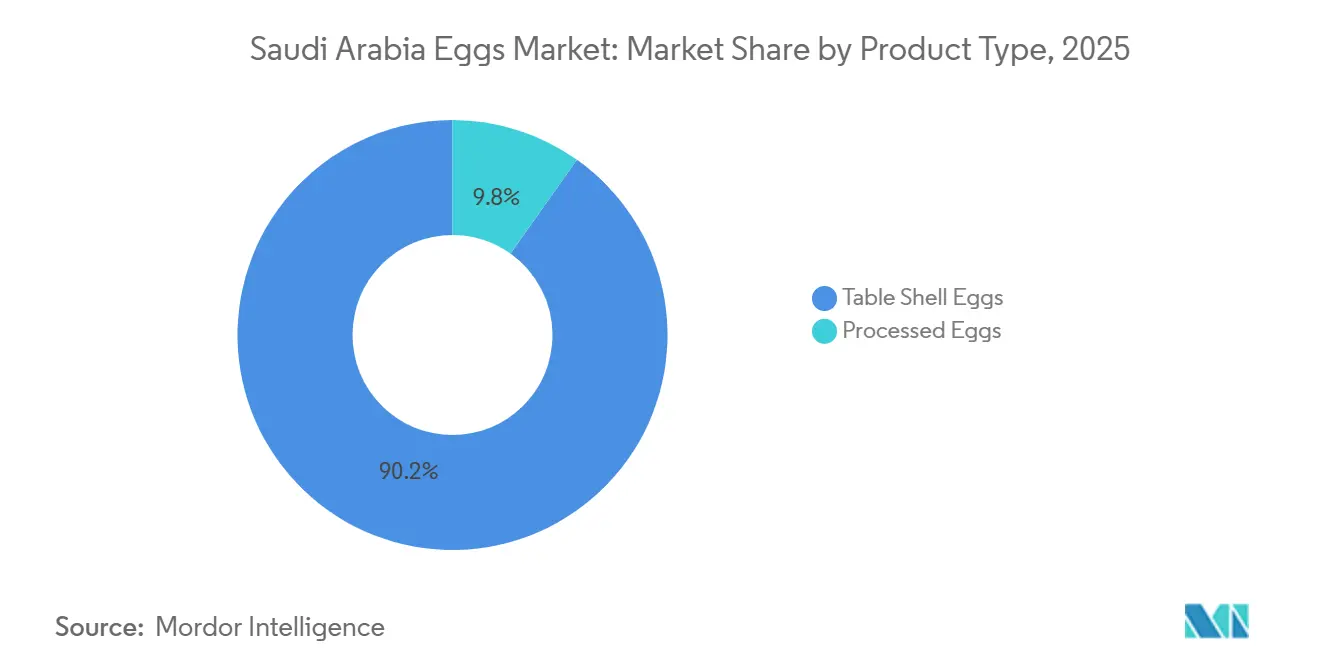

- By product type, table shell eggs captured 90.17% of Saudi Arabia eggs market share in 2025, while processed formats are advancing at a 6.95% CAGR for 2026-2031.

- By nature, conventional output held 95.09% share in 2025; organic eggs are projected to expand at a 7.96% CAGR over 2026-2031.

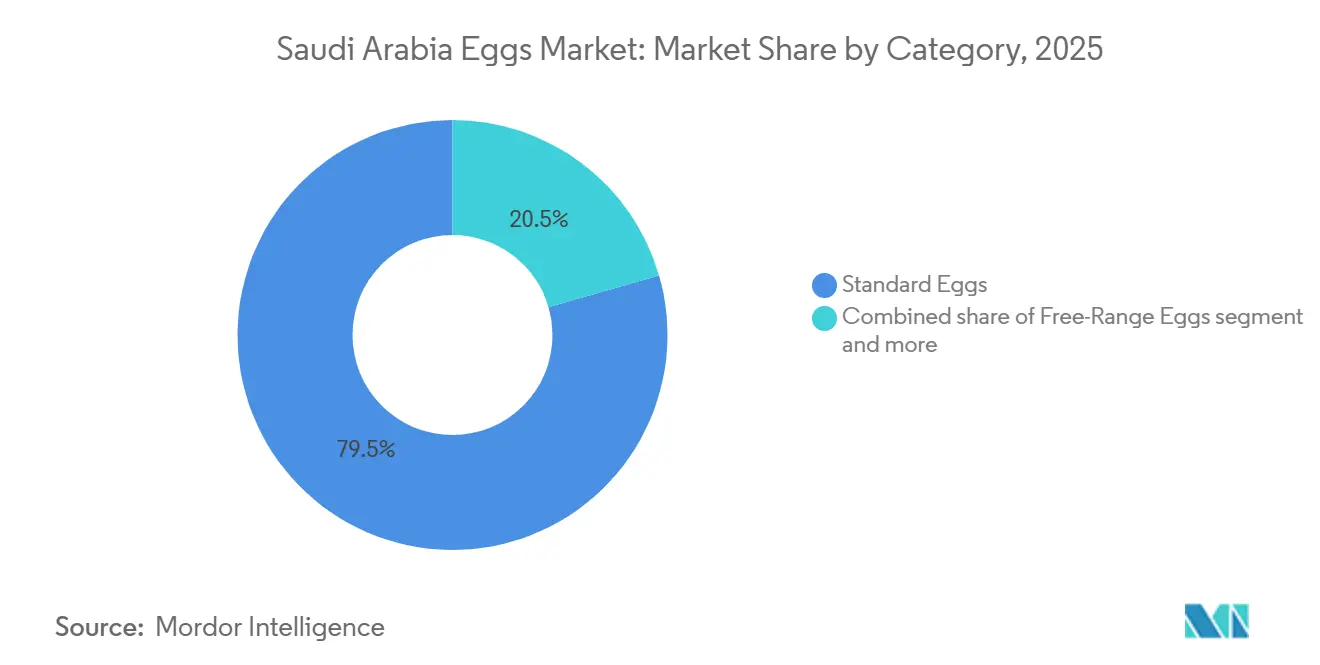

- By category, standard eggs accounted for 79.47% of 2025 volume, whereas free-range alternatives are rising at a 7.23% CAGR to 2031.

- By end-user, retail channels owned 56.18% share in 2025 and lead growth at a 6.85% CAGR through 2031, underscored by hyermarket and e-commerce proliferation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Eggs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of local poultry production | +1.2% | National, with concentration in Riyadh (38% of layer capacity), Qassim (18%), and Eastern Province (16%) | Medium term (2-4 years) |

| Government policies and food security initiatives | +0.9% | National, aligned with Vision 2030 targets and Agricultural Development Fund disbursements | Long term (≥ 4 years) |

| Rising demand for convenience food products | +0.8% | National, with urban centers (Riyadh, Jeddah, Dammam) leading bakery and processed-food consumption | Medium term (2-4 years) |

| Growth of tourism and food-service sectors | +0.7% | National, with early gains in Makkah, Madinah, and Riyadh due to Hajj, Umrah, and business tourism | Short term (≤ 2 years) |

| Diversification into premium/specialty eggs | +0.6% | National, with higher adoption in affluent urban districts and expatriate communities | Medium term (2-4 years) |

| Integration of advanced packaging | +0.4% | National, driven by SFDA traceability mandates and modern retail requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of local poultry production

The growth of domestic poultry production remains a key factor driving the Saudi Arabia eggs market. In 2024, table egg production exceeded 8.4 billion eggs, marking a 6.4% increase compared to 2023 and demonstrating the sector's consistent expansion. The Riyadh Region accounted for the highest production with approximately 3.2 billion eggs, followed by the Makkah Region with 1.5 billion eggs and the Eastern Region with 1.1 billion eggs, emphasizing the presence of major production hubs [1]Source: General Authority for Statistics, "GASTAT": Broiler chicken production in Saudi Arabia reaches 1.3 million tons in 2024", stats.gov.sa. These regions benefit from advanced farming techniques, favorable infrastructure, and government support, which collectively contribute to their high production capacities. This growth contributes to market stability by ensuring a steady supply of fresh eggs to meet increasing consumer demand across retail, food-service, and industrial sectors. Enhanced local production reduces reliance on imports, strengthens supply chain resilience, and facilitates improved product standardization and quality control. Additionally, the focus on modernizing poultry farms includes the adoption of automated systems, better feed management, and disease control measures, which further enhance productivity and efficiency. As poultry farms in key regions continue to modernize and expand, the Saudi eggs market is well-positioned for sustained growth, driven by increased production volumes and enhanced operational efficiency.

Government policies and food security initiatives

Government policies and strategic food security initiatives play a significant role in driving the Saudi Arabia eggs market. The Saudi government has emphasized enhancing domestic food production to achieve self-sufficiency, stabilize supply chains, and reduce dependency on imports. This focus has created a supportive environment for the poultry and egg industry. Investment incentives, updated regulatory frameworks, and infrastructure development have enabled poultry producers to increase capacity, enhance operational efficiency, and meet the rising domestic demand. Additionally, these measures have encouraged the adoption of advanced farming techniques and biosecurity measures, further strengthening the sector's resilience and productivity. Vision 2030 has reinforced this commitment through a wide range of initiatives, with 1,502 active programs launched since its inception. Of these, 674 have been completed, and 596 are progressing as planned[2]Source: Vision 2030, "Vision 2030 Annual Report 2024", vision2030.gov.sa. These initiatives encompass agricultural development, technology integration, and sustainability efforts, all of which contribute to boosting local egg production, improving quality standards, and ensuring a steady supply to both retail and food-service sectors. Furthermore, the focus on sustainability includes efforts to optimize resource utilization, reduce environmental impact, and promote renewable energy use within the agricultural sector, aligning with broader national goals.

Rising demand for convenience food products

Urbanization, changing consumer habits, and institutional consumption are driving increased demand for processed and convenience foods in Saudi Arabia. According to the World Bank, 85% of Saudi Arabia's population is expected to reside in urban centers by 2024, making time-saving food options increasingly essential. Saudi Arabia's food manufacturing industry is among the most dynamic in the region, supported by approximately 1,300 food processing plants operated by the Saudi Authority for Industrial Cities and Technology Zones (Modon). This industrial activity has created a growing demand for scalable, safe, and efficient ingredients, which powdered eggs and table eggs effectively fulfill. Additionally, the expanding confectionery and baked goods market, driven by strong consumer demand, plays a significant role in shaping the country's food industry sector. For example, the Capital Market Authority reports that total consumer expenditure on sugar and confectionery in Saudi Arabia reached approximately SAR 17.7 billion in 2024, highlighting the importance of this segment. This spending supports robust industrial production of packaged cakes, cookies, pastries, sweet sauces and fillings, dessert mixes, and ready-to-eat sweets. Eggs are a critical ingredient in these products, providing consistent aeration and binding in sponge cakes and meringues, stable emulsification in custards and fillings, and extended shelf life for export-grade confectionery items.

Growth of tourism and food‑service sectors

The growth of the tourism and food-service sectors in Saudi Arabia is a significant driver for the country's eggs market. In 2024, inbound tourism reached 29.7 million visitors, exceeding pre-pandemic levels, while domestic tourism rose to 86.2 million [3]Source: Ministry of Tourism, "Inbound and Domestic Tourism Indicators", mt.gov.sa. This surge in tourist activity has led to increased demand for food and beverages, particularly in hotels, restaurants, cafes, and catering services, where eggs are a fundamental ingredient in a wide range of dishes. Eggs are extensively used in traditional Saudi recipes, such as shakshuka and desserts, as well as in international cuisines served across the country. Additionally, the expansion of the hospitality industry has driven higher production of prepared foods, bakery products, and processed egg-based items, such as liquid eggs and powdered egg products, which cater to both commercial and retail consumers. With initiatives like Saudi Vision 2030 positioning Saudi Arabia as a global tourism hub, the combined growth of food-service outlets and tourist arrivals is expected to sustain strong demand for eggs in both fresh and value-added forms, supporting the market's long-term growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High feed-cost exposure due to global import reliance | -0.8% | National, with acute impact on producers lacking vertical integration or hedging strategies | Short term (≤ 2 years) |

| Recurrent avian-influenza outbreaks | -0.5% | National, with spillover risk from GCC neighbors (Kuwait, Oman, UAE) and migratory bird routes | Medium term (2-4 years) |

| Rising SFDA accreditation costs for specialty labels | -0.3% | National, disproportionately affecting small and mid-tier producers entering organic or free-range segments | Long term (≥ 4 years) |

| Supply chain vulnerability | -0.4% | National, concentrated in cold-chain gaps for processed eggs and last-mile distribution to rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High feed‑cost exposure due to global import reliance

A significant challenge for the Saudi Arabia eggs market is its heavy dependence on imported feed ingredients, such as corn, soybean meal, and other protein sources. Variations in global commodity prices, currency fluctuations, and supply chain disruptions directly affect poultry farmers' production costs, leading to higher egg prices for consumers. These fluctuations can be driven by factors such as geopolitical tensions, adverse weather conditions affecting crop yields, and changes in international trade policies. This reliance on imported feed not only heightens operational risks but also narrows profit margins for producers, particularly small and medium-scale farms. Elevated feed costs can hinder expansion efforts, limit investments in production capacity, and slow market growth, especially during periods of global price instability. For instance, smaller farms often struggle to absorb sudden cost increases, which can force them to scale back operations or exit the market entirely. As a result, managing feed costs remains a critical issue for ensuring both the affordability and competitiveness of eggs in the domestic market.

Recurrent avian-influenza outbreaks

The Saudi Arabia eggs market continues to face challenges due to recurrent avian influenza (AI) outbreaks, which disrupt production, reduce flock sizes, and affect both supply and pricing. These outbreaks often lead to significant economic losses for poultry farms, as infected or exposed birds must be culled to prevent further spread of the disease. This results in immediate production shortages, increased biosecurity costs, and financial strain on producers who must invest in preventive measures and recovery efforts. These outbreaks also create uncertainty for retailers and food-service providers, potentially impacting consumer confidence and demand for eggs. Consumers may become hesitant to purchase eggs due to concerns about safety and quality, further complicating market dynamics. Additionally, government-mandated containment measures, such as farm quarantines, movement restrictions, and enhanced surveillance, can temporarily limit operations and increase operational costs. These measures, while necessary to control the spread of the disease, can disrupt the supply chain and delay market recovery. Consequently, the market's growth remains vulnerable to disease outbreaks, emphasizing the importance of biosecurity management and preventive strategies to maintain production stability and ensure a consistent supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Processed Formats Gain Traction in Industrial Channels

Table shell eggs retained 90.17% of the 2025 value share, driven by sustained consumer preference for whole-shell formats in retail. Processed eggs are expected to grow at a compound annual growth rate (CAGR) of 6.95% through 2031, surpassing the market's overall growth rate of 5.96%. This divergence highlights structural changes in end-use applications. Bakeries and foodservice operators are increasingly adopting liquid eggs for improved labor efficiency and portion control. A single 1-liter carton of liquid eggs can replace approximately 20 shell eggs, eliminating tasks such as cracking, separation, and disposal, which typically incur labor costs of USD 0.10-0.15 per dozen. Additionally, liquid eggs offer extended shelf life and ease of storage, making them a practical choice for large-scale operations.

White eggs dominate the table-shell segment due to their lower production costs and strong consumer familiarity. The strategic implication of this trend is a bifurcation in the market: while table shell eggs will continue to lead in volume, processed egg formats are poised to capture a larger share of value growth. This shift is driven by producers' vertical integration efforts and industrial buyers' preference for consistency over cost considerations. Furthermore, the growing demand for processed eggs is supported by their versatility in various food applications, including ready-to-eat meals, bakery products, and confectionery, which require standardized and reliable ingredients.

By Nature: Organic Segment Accelerates Despite Feed-Sourcing Constraints

Conventional egg production is projected to account for 95.09% of the market share in 2025, supported by established infrastructure, cost efficiency, and consumer price sensitivity in the mass market. This segment's dominance underscores the Kingdom's emphasis on ensuring food security through affordable protein sources rather than focusing on premium offerings. Meanwhile, organic eggs are expected to be the fastest-growing segment, with a compound annual growth rate (CAGR) of 7.96% through 2031. This growth is driven by rising health awareness and higher disposable incomes among urban consumers, despite challenges including higher production costs and limited awareness in secondary markets.

The growth of the organic segment aligns with global wellness trends and the Kingdom's economic diversification objectives under Vision 2030. Premium retailers in metropolitan areas are expanding their organic product portfolios, while e-commerce platforms are enhancing access to specialty products for health-conscious consumers. Conventional producers are also exploring certification pathways to capitalize on premium pricing opportunities. However, this transition requires substantial investment in facility upgrades and operational adjustments. The Saudi Food and Drug Authority's organic food regulations provide a clear compliance framework, fostering market development while maintaining quality standards.

By Category: Free-Range Variants Capture Premium Tier as Standard Eggs Anchor Volume

Standard eggs retained 79.47% of the value share in 2025, primarily due to their affordability and widespread availability through mass-market distribution channels. Meanwhile, free-range eggs are expected to grow at a compound annual growth rate (CAGR) of 7.23% through 2031, driven by increasing consumer awareness of animal welfare and the perception that cage-free production enhances taste and nutritional value. Standard eggs benefit from economies of scale, automated grading processes, and established retail partnerships. However, the segment's CAGR of 5.96%, which aligns with the market average, indicates limited opportunities for differentiation beyond price-based competition.

Enriched eggs, which require specialized feed formulations containing ingredients such as flaxseed, fish oil, or algae, face challenges related to feed sourcing, similar to those encountered by organic egg producers. For instance, Saudi Arabia imports 4.9 million metric tons of corn annually but lacks domestic production of functional feed ingredients. Enriched eggs, fortified with omega-3 fatty acids, vitamins, or probiotics, present a parallel growth opportunity. Global trends indicate that functional egg formats can command price premiums of 20-30%, appealing to health-conscious consumers.

By End-User: Retail Channels Lead Growth as E-Commerce and HORECA Expand

Retail channels are expected to account for 56.18% of the end-user share by 2025 and are projected to grow at a CAGR of 6.85% through 2031. This growth is driven by the expansion of hypermarkets, with chains such as Panda, Othaim, Tamimi, LuLu, and Danube collectively controlling over 80% of modern retail. Additionally, the relatively low penetration of e-commerce, which reached USD 334 million in food sales in 2024, presents further growth potential. Industrial users, including bakeries, confectioneries, sauces and dressings manufacturers, meat processors, and dairy analogue producers, prefer liquid and powder egg formats due to their consistency and labor efficiency. This preference creates favorable conditions for processed-egg producers capable of meeting SFDA traceability requirements.

Abdullah Al Othaim Markets, with 256 branches and a market capitalization of SAR 11.052 billion, exemplifies the modern retail infrastructure supporting egg distribution in the Kingdom. The company's Iktissab Loyalty Program, which engages 3.9 million customers, highlights the scale of organized retail penetration. Industrial end-users, such as bakeries and food processors, provide stable demand volumes but operate with thinner margins, necessitating efficient supply chain management and bulk handling capabilities. The shift toward organized retail offers opportunities for branded producers while posing challenges to traditional distribution networks dominated by small-scale wholesalers.

Geography Analysis

The northern and central regions dominate agricultural production, leveraging their proximity to Riyadh, a major consumption center, and the established agricultural infrastructure in the Qassim province. These regions produce over 1.22 million tons of agricultural products annually, including significant poultry output supported by favorable climate conditions and groundwater access. The presence of government institutions and corporate headquarters ensures stable demand for premium egg products, while logistical advantages reduce distribution costs to major population centers. Additionally, Al-Ahsa governorate in the Eastern Province has emerged as a cost-efficient production hub, where operational efficiency, scale, and feed optimization drive competitive advantages.

The western region is the fastest-growing area, driven by industrial development initiatives and port infrastructure that support both domestic distribution and export activities. Its strategic location along Red Sea shipping routes facilitates export opportunities to African and European markets. Modern retail development in metropolitan areas such as Jeddah and Mecca creates opportunities for premium markets, while religious tourism generates consistent demand from the hospitality sector.

The eastern and southern regions hold smaller market shares but present distinct growth opportunities through specialized production and evolving consumption patterns. The Eastern Province benefits from employment in the petrochemical industry and higher disposable incomes, which support demand for premium products. In the Southern region, the mountainous terrain and higher rainfall provide natural advantages for free-range and organic production methods, aligning with the growth of specialty segments. For example, Wadi Bin Hashbal farm in the Asir region demonstrates sustainable production capabilities through treated water irrigation, highlighting the potential for environmentally conscious operations. However, cross-regional supply chain optimization remains a challenge due to transportation distances and infrastructure limitations, creating opportunities for regional specialization strategies.

Competitive Landscape

The Saudi Arabia egg market is moderately fragmented, characterized by the presence of several major players alongside numerous smaller regional producers. Key companies operating in the market include Al Gharbia Farms, Tanmiah Food Company, Al Ain Farms (Arabian Farms), Al Watania for Industries, and Fakieh Group, among others. This market structure presents opportunities for consolidation, as regulatory compliance requirements and economies of scale tend to favor larger, professionally managed operations.

Strategic mergers and acquisitions activity is gaining momentum in the market. A notable example is Al Watania Poultry, which has attracted acquisition bids from Almarai, Tanmiah Food Group, and international company JBS, with potential transaction values estimated at approximately SAR 2 billion. Technology adoption is becoming a critical competitive factor, with leading players investing in IoT systems, automated feeding, and climate control technologies to enhance operational efficiency and animal welfare standards.

The Saudi Food and Drug Authority's mandatory halal certification and quality standards provide compliance advantages for established producers while creating barriers for new entrants. Opportunities are emerging in specialty segments, particularly in organic and enriched egg varieties. These segments offer potential for higher margins through consumer education and premium positioning. Additionally, the NEOM biomanufacturing initiative introduces the possibility of disruption through alternative protein technologies, although the commercial viability of these technologies is still under evaluation.

Saudi Arabia Eggs Industry Leaders

-

Al Gharbia Farms

-

Al Ain Farms (Arabian Farms)

-

Al Watania for Industries

-

Fakieh Group

-

Al Kadi for Agriculture and Poultry Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Naqi Water Company has committed SAR 12.31 million (approximately USD 3.28 million) to a significant poultry expansion project designed to substantially increase egg production capacity in Saudi Arabia. Executed in partnership with Belad Al Sham Contracting Company, the project is expected to enhance the poultry segment’s capacity by up to 450%, enabling the production of approximately 165 million eggs annually upon completion.

- October 2024: Almarai and Algharbia Farms have signed a Memorandum of Understanding (MoU) with Saudi Arabia’s Ministry of Environment, Water, and Agriculture (MEWA) to localize egg powder production within the Kingdom. This initiative aims to enhance food security, reduce dependence on imports, and promote local value-added food manufacturing by establishing a domestic egg powder production facility.

- May 2024: Almarai has entered into five strategic agreements worth over SAR 500 million with leading global poultry companies as part of its investment strategy to expand poultry production and increase market share. Announced at the Middle East Poultry Exhibition in Riyadh, these agreements aim to raise annual production capacity from over 250 million birds to more than 450 million birds by 2027. These deals are aligned with Almarai’s five-year, SAR 7 billion investment plan to boost domestic poultry production, enhance local self-sufficiency, and support the national economy.

Saudi Arabia Eggs Market Report Scope

An egg is defined as the hard-shelled reproductive body produced by a bird, especially by the common domestic chicken, and is considered food. The Saudi Arabia egg market is segmented by type, such as table eggs and hatching eggs. By nature, it is divided into organic, conventional. By specialty, it is divided into free-range and enriched eggs. By end user, it is divided into retail channels, hotels/foodservice, and industrial. By region, it is divided into northern and central regions, the western region, the eastern region, and the southern region. The market forecasts are provided in terms of value (USD) and volume (tons).

| Table Shell Eggs | White Eggs |

| Brown Eggs | |

| Processed Eggs | Liquid Eggs |

| Dry Eggs | |

| Frozen Eggs |

| Organic |

| Conventional |

| Standard Eggs |

| Free-Range Eggs |

| Enriched Eggs |

| Retail Channels | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| Horeca/Foodservice | |

| Industrial | Bakeries and Confectioneries |

| Sauces, Dressings, and Mayonnaise | |

| Meat and Seafood Processing | |

| Dairy and Dessert Analogues | |

| Others |

| By Product Type | Table Shell Eggs | White Eggs |

| Brown Eggs | ||

| Processed Eggs | Liquid Eggs | |

| Dry Eggs | ||

| Frozen Eggs | ||

| By Nature | Organic | |

| Conventional | ||

| By Category | Standard Eggs | |

| Free-Range Eggs | ||

| Enriched Eggs | ||

| By End-User | Retail Channels | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| Horeca/Foodservice | ||

| Industrial | Bakeries and Confectioneries | |

| Sauces, Dressings, and Mayonnaise | ||

| Meat and Seafood Processing | ||

| Dairy and Dessert Analogues | ||

| Others | ||

Key Questions Answered in the Report

How fast is demand growing for processed egg formats in the Saudi Arabia eggs market?

Processed eggs, liquid, powder, frozen, are expanding at 6.95% CAGR through 2031, outpacing shell-egg growth thanks to bakery, food-service, and tourism demand.

What share do retail outlets command in national egg distribution?

Retail channels accounted for 56.18% of 2025 sales and are growing 6.85% CAGR on the strength of hypermarket expansion and rising e-commerce penetration.

How are feed costs affecting producer profitability?

Imports of 4.9 million tons of corn and 4.0 million tons of barley expose farmers to global price swings that can cut margins by up to 20% in a single quarter.

What is the outlook for organic eggs?

Organic eggs volumes grow at 7.96% CAGR but remain niche because certification costs and imported non-GMO feed restrict participation to well-capitalized integrators.

Page last updated on: