Egg Processing Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 34.64 Billion |

| Market Size (2031) | USD 42.46 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

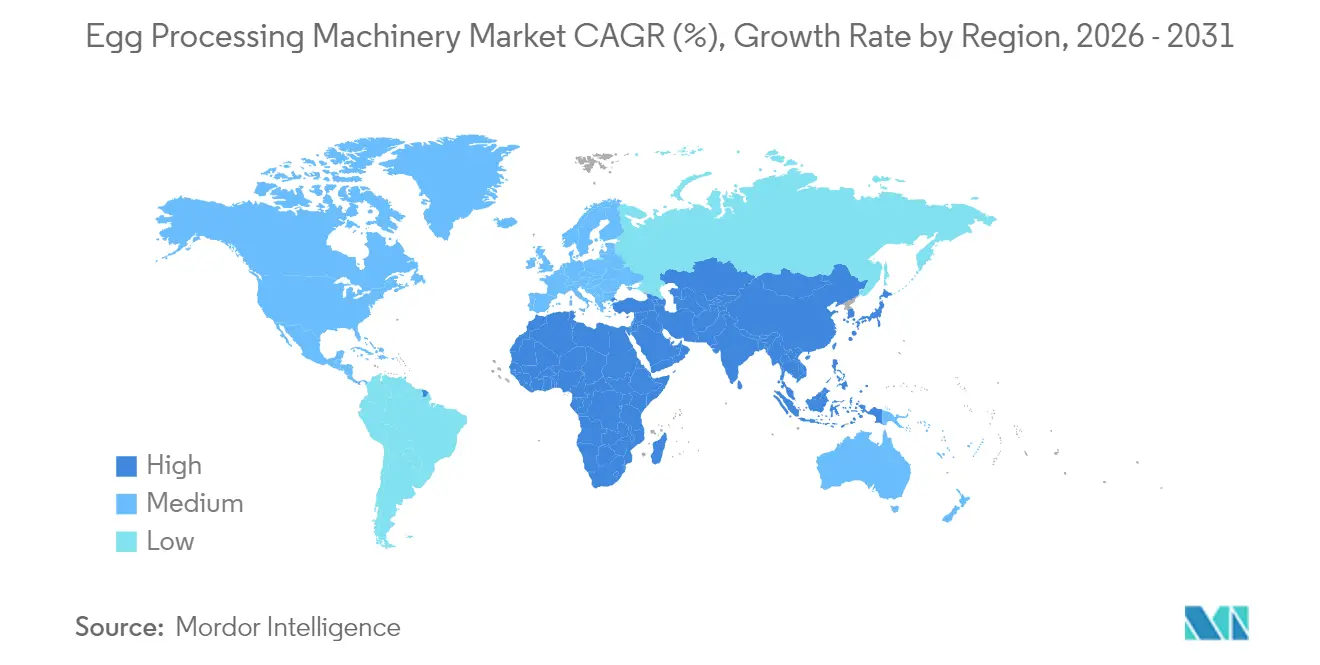

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

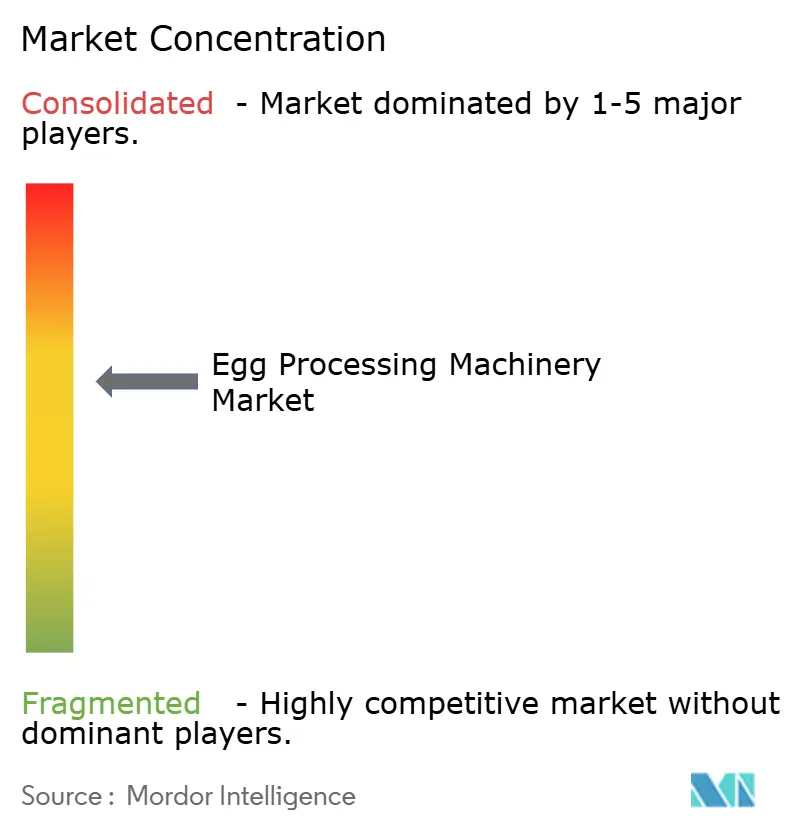

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egg Processing Machinery Market Analysis by Mordor Intelligence

The egg processing equipment market size is expected to grow from USD 33.26 billion in 2025 to USD 34.64 billion in 2026 and is forecast to reach USD 42.46 billion by 2031 at 4.17% CAGR over 2026-2031. This growth is fueled by advancements in automation technologies, stringent food-safety regulations, and the increasing diversification of protein consumption patterns. Regulatory changes in the United States and Europe are driving the adoption of advanced machinery equipped with continuous monitoring systems, robust cybersecurity measures, and AI-based safety features, which are also contributing to shorter replacement cycles. In North America, processors are heavily investing in flexible production lines to counteract supply-chain disruptions, such as those caused by Highly Pathogenic Avian Influenza outbreaks. Concurrently, operators in the Asia-Pacific region are rapidly integrating smart technologies to meet the surging demand in urban markets, driven by population growth and changing dietary preferences. The competitive landscape is evolving towards integrated, solution-oriented offerings that combine state-of-the-art hardware with advanced data analytics. These solutions empower processors to monitor key performance indicators, such as yields, energy efficiency, and regulatory compliance, in real time, thereby enhancing operational efficiency, reducing costs, and ensuring adherence to food safety standards.

Key Report Takeaways

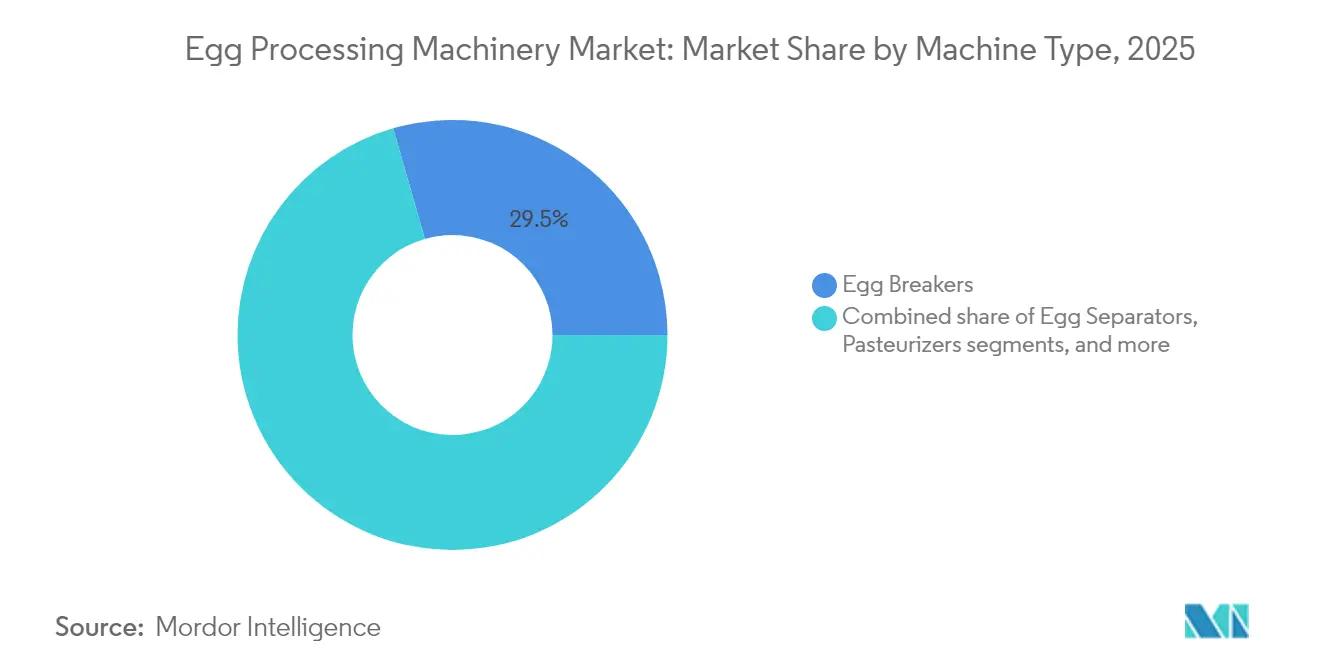

- By machine type, egg breakers held 29.45% of the egg processing equipment market share in 2025, while homogenizers are projected to post the fastest 6.18% CAGR through 2031.

- By end product, liquid eggs commanded 45.98% share of the egg processing equipment market size in 2025 and are forecast to expand at 6.92% CAGR to 2031.

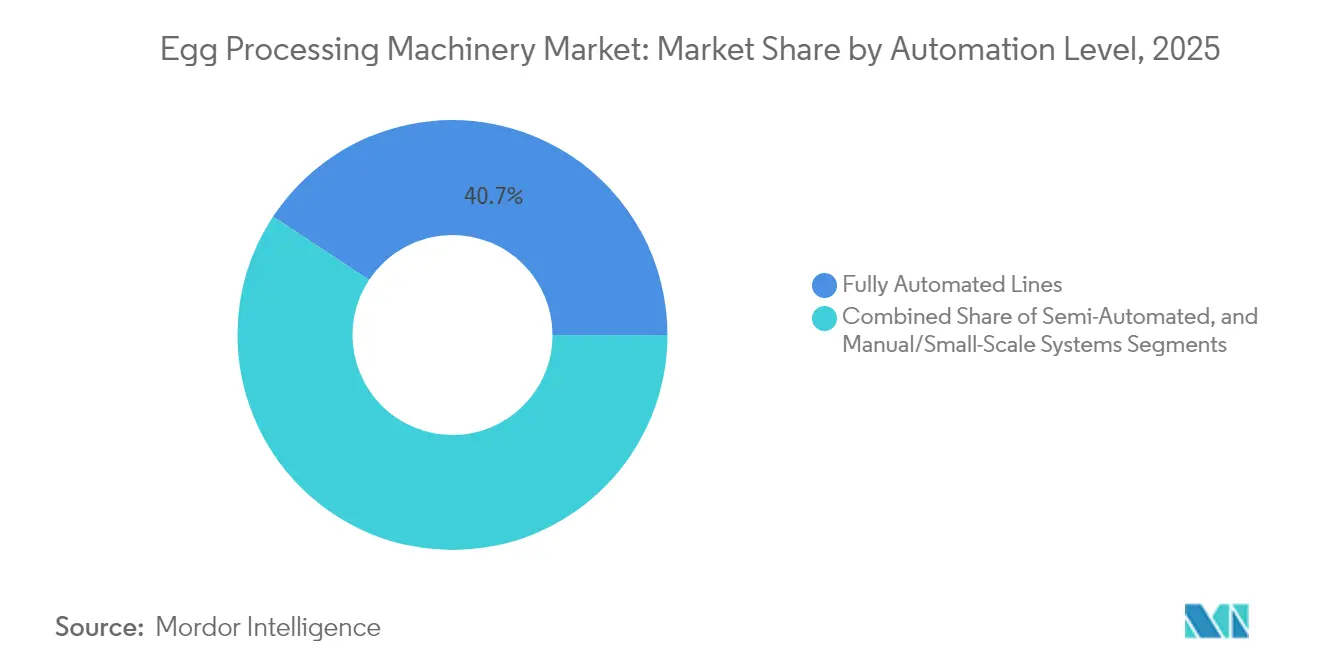

- By automation level, fully automated lines captured 40.72% of the egg processing equipment market in 2025 and are expected to lead growth at 8.74% CAGR through 2031.

- By end user, egg product manufacturers accounted for 38.02% of the egg processing equipment market, whereas bakery and confectionery processors are set to grow the quickest at 5.25% CAGR.

- By geography, North America retained 30.88% market share in 2025; Asia-Pacific is anticipated to register the highest 7.22% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Egg Processing Machinery Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience egg products | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Increasing focus on food safety and hygiene standards | +0.8% | Global, driven by regulatory mandates | Short term (≤ 2 years) |

| Adoption of automation and smart processing technologies | +1.0% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Rising popularity of protein-rich diets and functional foods | +0.7% | Global, early gains in urban markets | Medium term (2-4 years) |

| Technological advancements in egg processing machinery | +0.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Emergence of on-farm modular pasteurization systems for cage-free egg production | +0.3% | North America & EU regulatory zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for processed and convenience egg products

Shifting consumer preferences toward ready-to-eat and shelf-stable protein sources are driving sustained demand for advanced processing technologies that surpass traditional liquid egg applications. The acquisition of Echo Lake Foods by Cal-Maine for USD 258 million in 2025 highlights the strategic importance of value-added egg products, which offer higher profit margins but require advanced and specialized processing equipment. This trend is accelerating the replacement cycles for processing equipment, as manufacturers seek systems capable of producing innovative products such as egg bites, pre-cooked omelets, and protein-enriched convenience foods. These products demand precise temperature control and robust contamination prevention measures, making advanced equipment essential. The homogenizer and spray dryer segments are particularly benefiting from this shift, as these technologies are critical for achieving the texture modifications and extended shelf life required by convenience food applications. To remain competitive, equipment manufacturers must now design systems that can handle multiple product formats on a single production line. This requirement is increasing both the complexity and capital intensity of production systems, setting a higher standard compared to traditional single-product equipment. The evolving market dynamics underscore the need for innovation and adaptability in processing technologies to meet the growing demand for diverse, high-quality convenience food products.

Increasing focus on food safety and hygiene standards

Regulatory enforcement is evolving from periodic inspections to continuous monitoring, creating a profound impact on equipment design specifications and operational protocols. The FDA's updated Egg Regulatory Program Standards (ERPS) establish robust frameworks for state-federal collaboration, leading to more frequent inspections and stricter data reporting mandates. This shift is driving the adoption of advanced equipment featuring embedded monitoring systems, automated cleaning technologies, and real-time data capture capabilities, which ensure compliance with minimal manual intervention. Additionally, the USDA's development of Radio Frequency (RF) pasteurization technology, which achieves a 99.999% reduction in Salmonella in just 24 minutes—significantly faster than the traditional 57-minute process—demonstrates how regulatory requirements are accelerating technological advancements. Suppliers that can seamlessly integrate these innovative safety technologies while maintaining operational efficiency are positioned to gain a competitive edge. In markets where regulatory compliance costs increasingly influence profitability, such advancements are becoming critical for sustaining market leadership and meeting evolving safety standards.

Adoption of automation and smart processing technologies

As regions face demographic transitions, the convergence of manufacturing labor shortages and the growing need for consistent quality is driving automation to become an operational imperative rather than a strategic option. India's SAMARTH Udyog Bharat 4.0 initiative exemplifies this shift by establishing Industry 4.0 experiential centers and providing technical support to promote manufacturing automation. This initiative reflects the government's recognition that modernizing processing equipment is critical for maintaining competitiveness in the global market. The integration of IoT sensors and AI-driven process control systems allows manufacturers to optimize critical parameters such as temperature, humidity, and flow rates in real-time. This not only minimizes waste but also enhances yield consistency, ensuring higher efficiency. For instance, ABB's implementation of variable frequency drives at MPS Egg Farms resulted in significant energy savings of 400,000 kW annually, showcasing measurable returns on automation investments. Furthermore, this adoption cycle generates network effects, where early adopters gain cost advantages, compelling competitors to follow suit. This dynamic accelerates the transformation of the market, fostering widespread technological advancement and operational efficiency.

Rising popularity of protein-rich diets and functional foods

Increasing nutritional awareness is driving the demand for advanced egg processing equipment designed to produce protein isolates, functional ingredients, and nutraceutical products. These applications require precise molecular preservation during processing to maintain the desired quality and functionality. In response to this demand, the industry has developed spray drying technologies specifically optimized for egg white proteins. These technologies ensure the retention of gelation properties while achieving submicron particle sizes, addressing the growing requirements of the nutraceutical market. Manufacturers are heavily investing in innovative technologies that can efficiently separate and concentrate specific protein fractions while preserving their bioactivity. The rising trend toward functional foods further emphasizes the need for processing equipment capable of integrating additional ingredients, controlling particle size distribution, and safeguarding nutritional integrity throughout production cycles. This shift is driving the development of sophisticated control systems and specialized processing modules. These advancements enable the handling of diverse product formulations within integrated production lines, ensuring efficiency and consistency in meeting evolving consumer demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment in processing equipment | -0.6% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Limited adoption in small- and medium-sized enterprises | -0.4% | APAC & MEA, rural processing centers | Medium term (2-4 years) |

| Environmental concerns over egg processing waste | -0.3% | EU & North America regulatory zones | Long term (≥ 4 years) |

| Competition from plant-based egg substitutes | -0.2% | North America & EU urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial capital investment in processing equipment

Technological advancements in equipment financing are increasingly benefiting large processors, while smaller operations face growing challenges to modernization. These challenges are particularly pronounced in emerging markets, where access to financing remains constrained. Fully automated egg processing lines, which require significant capital investment exceeding USD 10 million for comprehensive installations, highlight the financial barriers smaller players encounter. To address such constraints, the Indian government has allocated USD 144 million in 2025 under its Production Linked Incentive Scheme for food processing, signaling the need for policy-driven interventions. The financing gap has also opened opportunities for alternative solutions, such as equipment-as-a-service models and modular systems, which enable incremental deployment. However, these approaches often fall short in delivering the operational efficiency of fully integrated installations. Consequently, processors with limited capital frequently delay equipment upgrades, exposing themselves to heightened risks of regulatory non-compliance and competitive disadvantages. Over time, these vulnerabilities can escalate, leading to potential market share erosion and further segmentation within the market.

Limited adoption in small- and medium-sized enterprises

Economies of scale in egg processing equipment create significant adoption barriers for SMEs, as these enterprises often fail to achieve the utilization rates required to justify investments in advanced automation. This limitation perpetuates efficiency gaps, threatening their long-term viability in an increasingly competitive market. To address these challenges, the National Livestock Mission has introduced a policy offering 50% capital subsidies, up to USD 60,000 in 2025, for livestock processing facilities[1]Source: Ministry of Fisheries, Animal Husbandry & Dairying, " National Livestock Mission", www.pib.gov.in. This initiative underscores the recognition of the critical need for targeted support to sustain SMEs and enhance their competitiveness. However, financial constraints are not the sole obstacle. SMEs frequently lack the technical expertise required to operate advanced processing equipment, which further complicates adoption. This knowledge gap highlights the need for equipment manufacturers to innovate by designing user-friendly interfaces and offering robust remote support solutions. Without such measures, the adoption gap widens, leading to increased market concentration risks. Larger processors, with greater access to advanced technology, gain significant competitive advantages, potentially reducing supplier diversity. This concentration also amplifies supply chain vulnerabilities, particularly during crises such as HPAI outbreaks, where disruptions can severely impact the availability and stability of supply chains. Addressing these challenges is essential to ensure a more resilient and inclusive market environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Breakers Dominate, Homogenizers Accelerate

In 2025, egg breakers captured a significant 29.45% share of the market, solidifying their role as the cornerstone of downstream processing operations. This dominance stems from the essential function of converting shell eggs into liquid form, a critical step before any value-added processing can take place. As a result, egg breakers are fundamental to the industry's infrastructure. The segment benefits from steady replacement demand, driven by equipment wear and compliance with stringent sanitary design regulations. Manufacturers have responded by developing advanced breaking systems that incorporate automated shell separation and quality inspection features. These innovations not only minimize contamination risks but also enhance yield efficiency, ensuring consistent performance. The sustained market leadership of egg breakers highlights the industry's reliance on mechanical processing solutions, even as other equipment categories experience technological advancements.

Homogenizers are positioned as the fastest-growing machine category, with a projected CAGR of 6.18% through 2031. This growth is propelled by increasing demand for uniform product consistency and extended shelf life in liquid egg applications. A notable example of innovation in this segment is Moba's cavitation homogenizing technology, which enables gentler homogenization processes. This technology extends pasteurizer run times and reduces operational costs compared to traditional high-pressure systems, offering significant efficiency gains. The rapid growth of this segment reflects the industry's recognition of the critical role homogenization quality plays in determining the performance of final products, particularly in bakery and food service applications. Modern homogenizers now integrate seamlessly with pasteurization systems, optimizing thermal treatments while preserving product integrity. This technological convergence enhances overall processing efficiency and positions homogenizers as indispensable components in contemporary egg processing lines, where maintaining product quality and operational efficiency is key to achieving a competitive advantage.

By End Product: Liquid Eggs Lead Both Size and Growth

In 2025, liquid eggs captured a significant 45.98% share of the market, with a projected CAGR of 6.92% through 2031. This growth highlights their versatility across food services, bakeries, and industrial applications, where consistent quality and ease of handling are critical. The segment's dominance is driven by its ability to meet the needs of multiple end-user categories while offering processors operational efficiencies, such as simplified storage, transportation, and inventory management compared to shell eggs. Technological advancements, such as engineered water nanostructures (EWNS) achieving a 97.6% E. coli inactivation rate for eggshell decontamination, have further enhanced the safety and quality of liquid eggs while preserving their natural protective properties. Additionally, advanced processing systems now integrate real-time quality monitoring and automated contamination detection, ensuring consistent product specifications. This market leadership reflects the food industry's growing preference for standardized ingredients that enable predictable and efficient manufacturing processes.

Liquid eggs are also expanding into emerging applications, including convenience foods, protein supplements, and functional food ingredients, leveraging their processing advantages. The USDA's development of Radio Frequency pasteurization technology, which reduces Salmonella by 99.999% in just 24 minutes compared to the traditional 57-minute process, has opened new opportunities for liquid egg applications by improving safety and reducing processing time. Equipment manufacturers supporting this segment are experiencing sustained demand growth but face increasing pressure to develop systems capable of handling specialized formulations and meeting extended shelf-life requirements. With a strong growth trajectory, liquid eggs are expected to continue their market expansion, driven by ongoing technological innovations and diversification into new applications.

By Automation Level: Full Automation Dominates and Accelerates

In 2025, fully automated lines captured a 40.72% share of the market and are projected to grow at a 8.74% CAGR through 2031. This growth highlights the increasing preference for automation among processors aiming to enhance operational efficiency and meet regulatory requirements. Automation systems have gained prominence due to their ability to deliver measurable benefits, including reduced labor costs, improved safety compliance, and consistent product quality—advantages that manual operations fail to provide. For instance, the integration of AI-driven monitoring systems in poultry management, achieving a 93.1% precision rate in operational monitoring, illustrates how automation technologies are evolving beyond traditional processing equipment to encompass comprehensive production management systems. Modern automated lines now feature advanced capabilities such as predictive maintenance and real-time quality control, which significantly reduce downtime while ensuring consistent output quality. The dominance of this segment reflects the growing competitive pressures that are driving widespread adoption of automation, even among processors facing initial capital constraints.

Furthermore, the accelerated growth of automation is fueled by the convergence of labor shortages, stringent regulatory requirements, and the demand for consistent quality, making automation an operational necessity rather than a strategic option. A notable example is ABB's implementation of variable frequency drives at MPS Egg Farms, which resulted in annual energy savings of 400,000 kW, demonstrating the tangible returns on automation investments that justify the associated capital expenditures. To address the challenges faced by processors transitioning from manual to fully automated operations, equipment suppliers are developing modular automation solutions that allow for incremental upgrades. The strong growth trajectory of full automation underscores the role of technological advancements and competitive pressures in shaping market conditions, positioning automated systems as indispensable for long-term sustainability and success.

By End User: Manufacturers Lead, Bakeries Drive Growth

In 2025, egg product manufacturers commanded a 38.02% share of the market, underscoring their pivotal role in transforming shell eggs into diverse products for various industries. This dominant position arises from their intermediary role, bridging the gap between egg producers and end-users. To cater to a wide array of customer needs, these manufacturers employ advanced processing techniques. Their facilities, often equipped with large-scale continuous processing systems, prioritize efficiency while upholding the stringent quality standards demanded by both food service and industrial clients. Benefiting from stable demand and enduring customer ties, these manufacturers enjoy consistent revenue streams, a boon for their equipment suppliers. The market's structure favors these specialized processing facilities, allowing them to serve multiple end-users more adeptly than if individual companies operated their own equipment.

Bakery and confectionery processors are poised to be the fastest-growing end-user segment, with a projected CAGR of 5.25% through 2031. This growth is fueled by a rising appetite for convenience foods and artisanal baking, both of which lean on specialized egg processing. A testament to this trend is Rembrandt Foods' acquisition of Artisan Kitchens, signaling a strategic move into the precooked egg sector. Such expansions highlight processors' shift towards high-value applications, often necessitating specialized equipment. The segment's growth mirrors a broader premiumization trend in the food market, where processors are gravitating towards higher-margin applications, justifying their investments in advanced equipment. In bakery applications, the demand is for equipment that ensures specialized textures, precise ingredient ratios, and consistent performance, all vital for predictable baking results. Given the growth trajectory, it's evident that bakery and confectionery applications will spearhead equipment innovation and market growth, as processors chase premium pricing."

Geography Analysis

In 2025, North America holds a 30.88% market share, supported by its advanced food processing infrastructure and stringent regulatory frameworks that drive continuous equipment modernization. The region benefits from widespread automation adoption and a strong preference for convenience foods. However, market maturity limits its growth potential compared to emerging regions. A notable example of supply chain disruptions creating opportunities is the U.S. decision to import 420 million eggs from Turkey in 2025 to address shortages caused by HPAI outbreaks. Turkey remains the only country from which the U.S. imports eggs, despite the U.S. producing over 7.5 billion eggs annually, as per the American Egg Board. This scenario highlights the increasing demand for adaptable processing systems capable of handling inputs from diverse sources with varying quality standards.

Asia-Pacific is positioned as the fastest-growing region, with a projected CAGR of 7.22% through 2031. This growth is driven by rapid urbanization, increasing protein consumption, and government-led initiatives aimed at modernizing food processing industries. India's food processing sector, which attracted USD 12.58 billion in FDI between April 2000 and March 2024, exemplifies the region's investment appeal and growth potential In China, agricultural trade dynamics, such as the rejection of 154 U.S. food shipments in early 2025, underscore the critical need for robust domestic processing capabilities and stringent quality control systems. The region's expansion creates significant opportunities for equipment suppliers who can adapt technologies to meet local preferences, regulatory requirements, and cost-efficiency demands.

Europe continues to exhibit steady demand, driven by strict regulatory compliance and sustainability mandates. In contrast, South America and the Middle East & Africa present emerging opportunities, albeit with growth constrained by infrastructure deficits and limited capital availability. These geographic disparities reflect varying stages of economic development and food processing industry maturity. They also highlight opportunities for equipment suppliers to implement region-specific strategies and offer financing solutions tailored to local market needs.

Regulatory Landscape

Egg processing machinery demand is shaped by food safety and hygiene rules that require sanitary design, pasteurization control, and audit-ready documentation. In the United States, shell egg production and on-farm controls fall under FDA requirements (21 CFR Part 118) for Salmonella Enteritidis prevention, while egg products produced in official plants fall under USDA FSIS inspection (9 CFR Part 590) with HACCP and Sanitation SOP expectations. This encourages processors to favor equipment with validated thermal controls, automated monitoring, and traceable data logging.

In the European Union, the Hygiene Package (Regulation (EC) No 852/2004 and 853/2004) requires HACCP-based procedures for food business operators, affecting equipment cleanability, CIP design, and cross-contamination controls. The EU also updated egg-related hygiene requirements via Delegated Regulation (EU) 2024/1141 amending annexes to Regulation (EC) No 853/2004, reinforcing the need for processors and OEMs to align line design, sanitation access, and verification records with evolving compliance expectations across member states.

Value Chain Analysis

The value chain links upstream shell-egg supply and hatchery or production systems to downstream processing plants that convert eggs into liquid, powdered, frozen, and ingredient formats for foodservice, bakery, and industrial users. Core machinery OEM activities cover design and engineering, fabrication, automation and controls, installation and commissioning, and validation support that ties into HACCP documentation, along with recurring aftermarket services such as CIP retrofits, spares, and performance optimization. Processors increasingly favor integrated lines over stand-alone machines, shifting buyer expectations toward turnkey delivery and sustained compliance support.

Capacity and trade-enablement moves show how the chain is changing. EggSolutions Vanderpol broke ground on a 65,000 sq ft egg processing facility in Abbotsford, British Columbia, incorporating spray drying technology and microbiology research capability, which is expected to expand local downstream demand for breakers, pasteurizers, dryers, and QA systems. On the demand-pull side, the American Egg Board increased export development activity in Asia through trade missions and outreach (including Japan and Indonesia in 2026), which raises requirements for consistent specification, traceability, and packaging performance, and increases the value of service networks and digital monitoring to reduce waste and manage egg product perishability.

Competitive Landscape

The global egg processing equipment market is moderately consolidated, with a few dominant players holding significant market shares while regional and niche manufacturers actively contribute to the competitive landscape. Leading companies such as Sanovo Technology Group, Ovobel Foods Limited, Moba Group, and Big Dutchman AG have established robust market positions by offering extensive machinery portfolios and customized automation solutions. These solutions enable them to efficiently serve large-scale egg processors. Their competitive advantage is further reinforced by continuous technological advancements, expansive global distribution networks, and strategic collaborations. At the same time, smaller firms catering to localized or low-scale processing needs ensure sustained competition, fostering a dynamic environment that balances innovation-driven scalability with cost-effective regional adaptability.

Competition within the market is intensifying, particularly in the area of technology integration. Traditional equipment manufacturers face mounting pressure from digitally-native entrants introducing IoT-enabled systems equipped with features like predictive maintenance and remote monitoring. Additionally, the industry's response to regulatory changes, such as the EU's Machinery Regulation 2023/1230, which mandates compliance with cybersecurity and AI safety standards, is becoming a critical differentiator. Companies capable of delivering compliant solutions ahead of the January 2027 deadline are well-positioned to gain a competitive edge and capture market share.

Opportunities are emerging in the development of modular systems designed to handle variable production volumes and accommodate multiple product formats. These systems address the growing need for flexibility driven by supply chain disruptions and shifting consumer preferences. Furthermore, new entrants are focusing on integrating advanced automation and data analytics capabilities, enabling egg processors to optimize operations in real-time while maintaining adherence to regulatory requirements. This focus on innovation and adaptability is expected to drive growth and transformation within the market.

Egg Processing Machinery Industry Leaders

-

Sanovo Technology Group

-

Moba Group

-

Ovobel Foods Limited

-

OVO-TECH Sp. z o.o.

-

Big Dutchman AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on compliance-oriented upgrades that combine hygienic design with automated verification. The May 2026 USDA FSIS availability notice for a revised Food Safety Guideline for Egg Products highlights processor focus on pasteurization, cooling or freezing, and related control points, supporting demand for equipment that embeds temperature control, automated recording, and sanitation verification as standard features rather than add-ons.

A second opportunity is the move beyond pure throughput toward data-driven quality and lower total cost of ownership, reflected in launches focused on closed-loop CIP, recipe-based operation, and vision-based inspection. Moba Group introduced the Proxima breaker series (January 2026) with closed-loop CIP and optional automated egg inspection. SANOVO expanded high-capacity grading and inspection with the GraderPro 400-800 series (March 2026) and VisionAI Detector for contactless, vision-based weighing (May 2026). These releases create room for OEMs and integrators to retrofit legacy lines with CIP optimization, Industry 4.0 connectivity for traceability, and non-contact inspection to reduce mechanical wear, calibration downtime, and water use across both mature and fast-expanding processing regions.

Recent Industry Developments

- July 2026: Moba Group published its Q2 2026 quarterly press update, highlighting continued development across its egg grading and breaking portfolio. Regular cadence updates from a leading OEM keep competitive pressure focused on faster product iteration and service-led differentiation in integrated processing lines.

- June 2026: SANOVO Technology Group announced a partnership with Canadian Egg Technologies and MatrixSpec Solutions to commercialize a hyperspectral imaging-based in-ovo sexing system capable of non-destructive sex determination at day four of incubation. The collaboration expands SANOVO’s technology scope adjacent to egg handling and inspection, strengthening its automation and imaging platform positioning across the egg value chain.

- January 2024: Ovoconcept launched the Ovopal 1000 robotic case palletizer for egg operations, designed to handle multiple case formats and raise automation in end-of-line packaging. The introduction supports labor reduction and higher line efficiency in packing environments, and increases demand for robotics-compatible case handling and palletizing integration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers machines and systems used to convert shell eggs into processed egg products in industrial settings, from breaking and separation through pasteurization, filtration, drying, and related handling steps. The market size is measured in value terms.

Scope exclusions: It does not count the value of processed egg products themselves, farm level egg production, or general food plant utilities that are not purpose-built for egg processing lines.

Segmentation Overview

-

By Machine Type

- Egg Breakers

- Egg Separators

- Pasteurizers

- Homogenizers

- Spray Dryers

- Centrifuges and Filters

- Other Machine Type (Boiling/Cooling/Peeling Lines)

-

By End Product

- Liquid Eggs

- Powdered Eggs

- Frozen Eggs

-

By Automation Level

- Manual/Small-Scale Systems

- Semi-Automated

- Fully Automated

-

By End User

- Egg Product Manufacturers

- Bakery and Confectionery Processors

- Nutraceutical and Protein Ingredient Firms

- Other End Users

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping the industrial processing flow and the core equipment steps, so the market boundary stays practical for buyers. Public sources were used to anchor demand signals and operating context, such as USDA and national agriculture statistics, FAO production datasets, UN Comtrade trade data for relevant machinery categories, and food safety and inspection references from agencies such as the FDA and the European Commission.

We also reviewed company annual reports, investor presentations, product brochures, and reputable press coverage to understand typical line configurations, replacement cycles, and where automation upgrades are being adopted. To avoid over-relying on any single public series, paid subscriptions that track company financials and news were used selectively, along with patent databases and shipment-level trade datasets, to cross-check timelines and confirm which equipment types are being commercialized. The desk sources listed here are illustrative only, and additional public documents and references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with equipment manufacturers, system integrators, plant engineering teams, and processed egg producers across major consuming and exporting regions. The discussions were used to confirm typical price bands by machine type, utilization patterns, and replacement behavior. We also checked whether operators usually expand processing lines or upgrade existing assets, which helped correct assumptions that public sources alone did not fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 35% | EMEA: 36% |

| Smaller Players: 16% | Managers: 52% | Americas: 23% |

Market-Sizing & Forecasting

The core sizing logic was built top-down, where processed egg output and trade flows were translated into required processing capacity, and then converted into equipment demand using typical line layouts and replacement timing. Once that demand pool was formed, we ran selective bottom-up checks, such as sampling average selling prices for key machines and multiplying by estimated unit volumes. We then compared the results with channel feedback from integrators to adjust any obvious mismatches.

Key inputs used in the model included industrial egg processing volumes (liquid, dried, and frozen), capacity additions announced by processors, average line throughput and shift patterns, typical refurbishment and replacement cycles for breakers and pasteurizers, and mix shifts toward spray drying and automation in larger plants. Forecasts were developed using scenario analysis, with variables such as processed egg consumption growth, export intensity, and capex appetite stress-tested with expert feedback, then consolidated into one base case outlook. Where bottom-up visibility was weaker for smaller installations, the gap was handled by applying penetration rates linked to processor size bands and validating the resulting totals with primary responses.

Data Validation & Update Cycle

Outputs were validated by comparing model totals against independent signals such as processed egg production trends, machinery trade direction, and the pace of new plant and line announcements, then reviewing variances step by step. If a region or machine category showed an unusual spike, the underlying assumptions were revisited and follow-up calls were triggered to confirm whether it was a one-time project effect or a sustained demand change.

Before sign-off, the work is reviewed across analysts so the calculations, scope boundaries, and unit conversions remain consistent across regions. Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity expansions, major regulatory shifts, or sharp currency moves. Right before delivery, a final pass is performed so clients get the most current view possible, using inputs that can be traced to their original sources.

Mordor Intelligence's Egg Processing Machinery Market Size Compared Against Other Published Estimates

Published market sizes for egg processing machinery can look far apart even when the topic label is similar, mostly because companies count different equipment, use different base years, and sometimes mix product value with machinery value. Differences also come from how price inflation is treated, how quickly capacity additions are assumed to translate into equipment orders, and how often the model is refreshed.

The gap is usually driven by scope handling, where some estimates blend egg processing machinery with broader poultry or food processing equipment, and by how demand is reconstructed, such as using shipment proxies versus using processed egg output and line capacity needs. Currency timing and whether list prices or realized transaction prices are used can move totals as well, especially when imported machinery share changes year to year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 34.64 B (2026) | |

| Industry Research House A | USD 1.40 B (2024) | Uses an earlier base year and appears to apply a narrower equipment value view, which can exclude complete line systems and larger-scale industrial installations that are counted in broader machinery scopes. |

| Industry Research House B | USD 31.29 B (2024) | Uses a different base year and a longer forecast window, and the sizing may rely more on historical progression of market value without the same level of capacity-to-equipment conversion checks by machine type. |

The table shows a wide spread, and in Mordor Intelligence's model the market is counted as the value of dedicated egg processing machinery across core steps like breaking, separation, pasteurization, filtration, homogenizing, centrifuging, and spray drying, which is then tied back to processed egg output and capacity needs. When the scope is kept consistent and the demand pool is rebuilt from repeatable operating variables, the final number becomes easier to reconcile and to update as new capacity and pricing signals emerge.

Key Questions Answered in the Report

What is the current size of the egg processing equipment market?

The market is valued at USD 34.64 billion in 2026 and is projected to reach USD 42.46 billion by 2031.

Which machine category is growing the fastest?

Homogenizers are expected to register a 6.18% CAGR through 2031 as processors seek better product consistency and shelf life.

Why are liquid eggs the dominant end product?

Liquid eggs hold 45.98% share due to their versatility in food service and industrial baking, and they lead growth at a 6.92% CAGR.

How significant is full automation in the sector?

Fully automated lines already account for 40.72% of revenue and are expanding at 8.74% CAGR as labor shortages and compliance needs intensify.

Page last updated on: