Liquid Egg Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.22 Billion |

| Market Size (2031) | USD 4.16 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

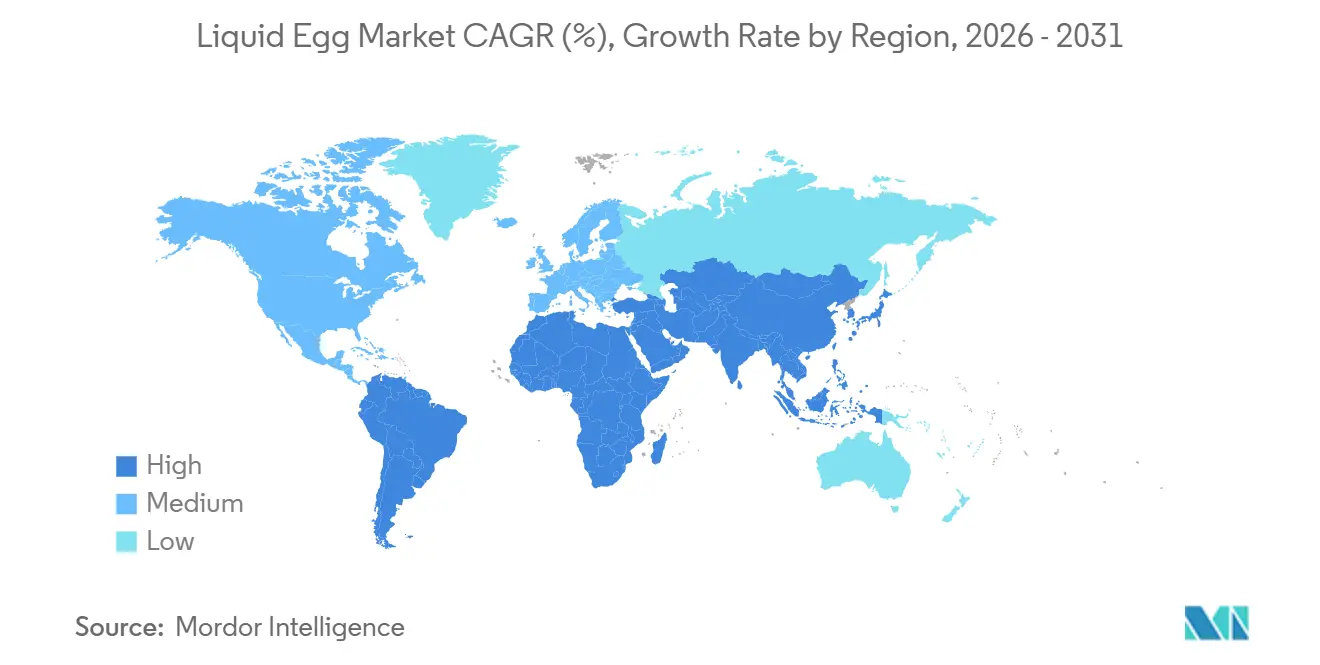

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

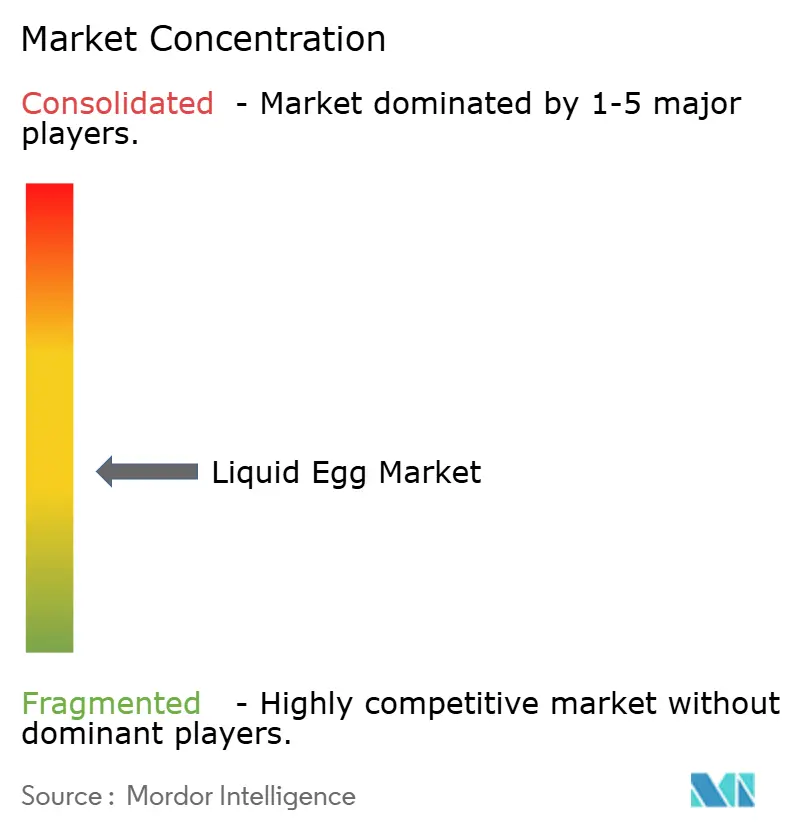

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Egg Market Analysis by Mordor Intelligence

The global liquid egg market size is expected to grow from USD 3.22 billion in 2026 to USD 4.16 billion by 2031, at a compound annual growth rate (CAGR) of 5.45%. The market growth is driven by supply chain adaptations to meet increasing production demands and evolving consumer preferences for convenient protein options. Food manufacturers are increasingly incorporating liquid eggs into their product formulations due to their ease of handling, consistent quality, and extended shelf life. Additionally, stringent food safety regulations requiring pasteurization processes effectively eliminate Salmonella while maintaining the eggs' nutritional profile, including essential proteins, vitamins, and minerals[1]Source: Food and Drug Administration, “CFR Title 21 Part 160 – Egg Products,” fda.gov. The pasteurization requirement has led to increased investments in processing technology and quality control measures across the industry.

Key Report Takeaways

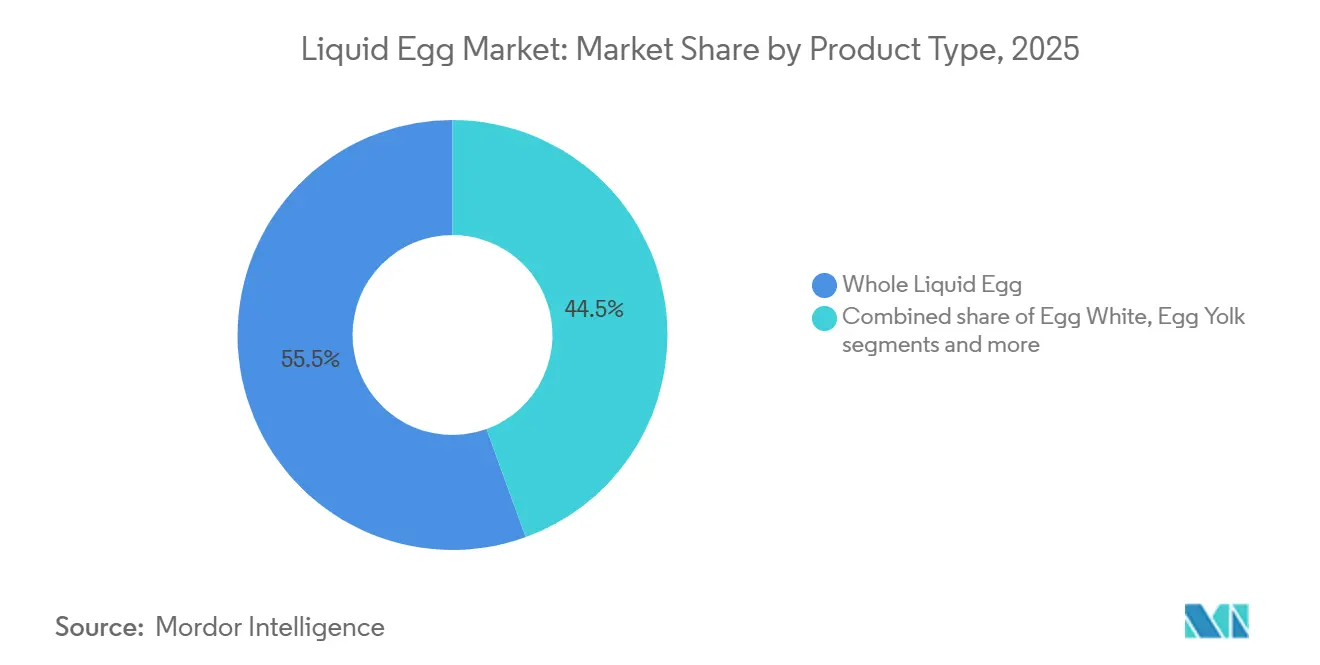

- By product type, whole liquid eggs led with 55.54% of 2024 revenue, while egg whites are projected to grow at a 6.78% CAGR through 2030.

- By form, refrigerated liquid captured a 47.64% share in 2024, while ambient/shelf-stable lines are expected to grow at a 7.04% CAGR to 2030.

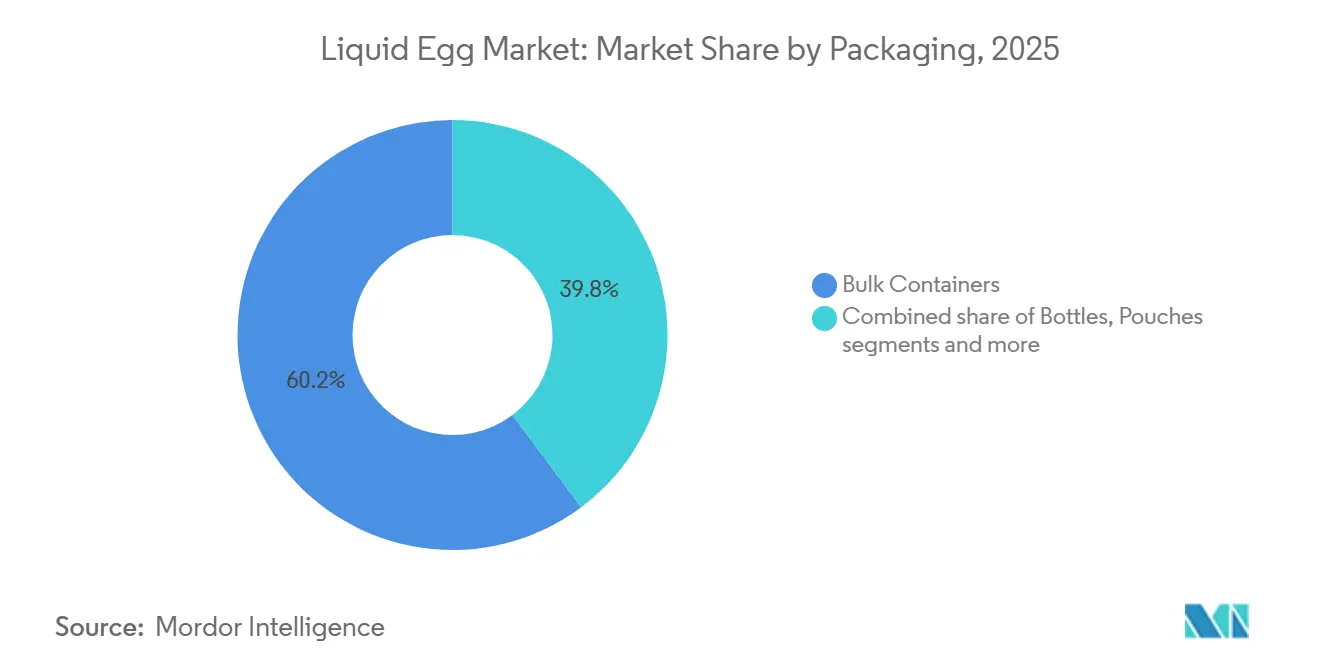

- By packaging, bulk containers accounted for 60.22% of 2024 sales, whereas pouches are expected to grow at a 6.52% CAGR over the forecast period.

- By distribution channel, industrial users held 50.16% of 2024 demand, and retail is set to expand at a 7.25% CAGR up to 2030.

- By geography, North America dominated with a 34.48% share in 2024, whereas Asia-Pacific is poised for a 7.43% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Egg Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-driven demand from food-service and industrial baking | +1.2% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Stricter food-safety regulations favor pasteurized liquid eggs | +0.9% | Global, with strongest impact in North America and EU | Long term (≥ 4 years) |

| High-protein diet adoption among fitness consumers | +0.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expansion of ready-to-cook and processed foods | +1.1% | Global, with Asia-Pacific showing highest growth | Medium term (2-4 years) |

| Ethical and cage-free sourcing | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Product and packaging innovation | +0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven demand from food-service and industrial baking

Food-service establishments increasingly prioritize liquid eggs to streamline operations and ensure consistent quality across high-volume applications. The shift eliminates labor-intensive shell cracking while reducing contamination risks and waste generation in commercial kitchens. Industrial baking operations particularly benefit from liquid eggs' standardized composition, which enables precise recipe formulation and automated processing systems. This trend accelerates as labor shortages in food service drive automation adoption, positioning liquid eggs as essential ingredients for operational efficiency. The convenience factor becomes particularly pronounced in quick-service restaurants and institutional catering, where speed and consistency determine competitive advantage.

Stricter food-safety regulations favour pasteurized liquid eggs

Regulatory authorities increasingly mandate pasteurization processes that eliminate pathogenic microorganisms while preserving nutritional value. The FDA's 21 CFR Part 160 requires liquid eggs to be treated to destroy all viable Salmonella microorganisms, creating a regulatory moat around pasteurized products. Recent FSIS declarations classifying Salmonella as an adulterant in poultry products signal intensifying regulatory scrutiny that favors processed alternatives over shell eggs[2]Source: Food Safety and Inspection Service, “Salmonella Framework for Raw Poultry Products,” fsis.usda.gov. The Canadian Food Inspection Agency's new export requirements for processed egg ingredients, effective September 2024, mandate detailed pasteurization documentation, demonstrating global regulatory alignment toward safety standards[3]Source: U.S. Department of Agriculture, “Food Price Outlook, 2025 and 2026,” ers.usda.gov. These regulations create competitive advantages for established processors with validated pasteurization systems while raising barriers for new entrants lacking compliance infrastructure.

High-protein diet adoption among fitness consumers

Consumer awareness of protein's role in muscle development and weight management drives demand for convenient, high-quality protein sources. Liquid egg whites particularly benefit from this trend, offering 26 grams of protein per cup with minimal fat content, appealing to fitness enthusiasts and health-conscious consumers. Rising consumer health consciousness and demand for nutritional additives position liquid eggs as premium ingredients in protein-focused applications. This demographic shift particularly impacts urban markets where convenience and health benefits converge, driving premium pricing for specialized liquid egg formulations targeting fitness and wellness segments.

Expansion of ready-to-cook and processed foods

Urbanization and changing lifestyles accelerate demand for convenient meal solutions that reduce preparation time without compromising nutritional value. Ready-to-cook products incorporating liquid eggs benefit from extended shelf life and consistent quality compared to shell egg alternatives. The global adoption of convenience foods reflects demographic shifts and expenditure patterns favoring time-saving solutions. Asia-Pacific markets demonstrate particularly strong growth in processed food consumption, driven by urbanizing middle-class populations with increasing disposable income. This trend creates opportunities for liquid egg processors to develop region-specific formulations that cater to local taste preferences while maintaining the convenience benefits that drive category adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-egg price volatility | -1.4% | Global, with strongest impact in North America | Short term (≤ 2 years) |

| Expansion of plant-based egg substitutes | -0.8% | North America, Europe | Medium term (2-4 years) |

| Cold-chain gaps causing spoilage in emerging markets | -0.6% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Consumer skepticism toward processed foods | -0.4% | Global, with stronger impact in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-egg price volatility

Highly pathogenic avian influenza outbreaks create severe supply disruptions that translate directly into liquid egg cost structures. The United States Department of Agriculture (USDA) forecasts egg prices to increase by 41.1% in 2025. Retail prices rose by 13.8% in January, primarily due to the impact of Highly Pathogenic Avian Influenza (HPAI) on commercial egg-laying operations[4]Source: Government of Canada, “Notice to industry – United States of America – Export requirements for edible food products containing processed egg ingredients,” inspection.canada.ca. Feed costs, representing 56% of production expenses, amplify volatility through commodity price fluctuations that impact both shell and liquid egg segments. This volatility constrains demand growth as food service operators and industrial users seek price stability for menu planning and contract negotiations. The cyclical nature of HPAI outbreaks creates unpredictable cost spikes that challenge liquid egg processors' ability to maintain consistent pricing strategies and customer relationships.

Expansion of plant-based egg substitutes

Alternative protein technologies increasingly replicate egg functionality in food applications, creating competitive pressure on traditional liquid egg products. The vegan egg market is experiencing rapid growth due to increasing health awareness, egg allergies, and ethical considerations among consumers. Companies like EVERY Company develop recombinant egg proteins through precision fermentation, producing egg white proteins without chickens while addressing environmental and ethical concerns. Plant-based alternatives using aquafaba, lentils, and soy proteins demonstrate functional properties that challenge liquid eggs in specific applications, particularly in vegan and allergen-free formulations. This competitive dynamic forces liquid egg producers to emphasize unique nutritional profiles and functional benefits that plant-based alternatives cannot fully replicate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whole Liquid Eggs Drive Volume, Whites Capture Premium Growth

Whole liquid eggs command 55.54% market share in 2024, reflecting their versatility across culinary applications from industrial baking to food service operations. The segment's dominance stems from cost efficiency and familiar functionality that requires minimal recipe modification for traditional egg-based products. Egg whites emerge as the fastest-growing segment at 6.78% CAGR through 2030, driven by fitness-conscious consumers seeking high-protein, low-fat alternatives. This growth trajectory reflects premiumization trends where consumers willingly pay higher prices for specialized nutritional profiles. Egg yolks maintain steady demand in specialized applications requiring emulsification properties, while blends and scrambled mixes cater to convenience-focused segments seeking ready-to-use formulations.

The University of Saskatchewan's development of engineered water nanostructures for pathogen inactivation represents a technological breakthrough that could reshape product type preferences by enabling safer processing of specialized formulations. This chemical- and heat-free method achieves 97.6% E. coli inactivation and 80.4% Salmonella reduction without damaging egg quality, potentially enabling premium product development across all segments. The technology's environmental benefits and quality preservation capabilities position it as a differentiating factor for processors targeting health-conscious and sustainability-focused market segments.

By Form: Refrigerated Dominance Faces Shelf-stable Innovation

Refrigerated liquid eggs maintain a 47.64% market share in 2024, supported by established cold-chain infrastructure in developed markets and consumer familiarity with temperature-controlled products. The segment benefits from shorter processing requirements and perceived freshness advantages that command premium pricing in retail channels. However, ambient/shelf-stable products demonstrate the strongest growth at 7.04% CAGR, driven by technological advances in ultra-pasteurization and aseptic packaging that extend shelf life without refrigeration. This growth reflects expanding distribution reach into markets with limited cold-chain infrastructure and convenience-focused applications requiring room-temperature storage. Frozen liquid eggs serve specialized industrial applications where long-term storage and batch processing requirements justify the additional handling complexity.

The FDA's recent revocation of M.G. Waldbaum Co.'s temporary permit for ultrapasteurized liquid eggs signals regulatory acceptance of advanced processing methods that enable shelf-stable formulations. This regulatory milestone removes barriers for shelf-stable product development while validating the safety and efficacy of ultra-pasteurization technologies. The decision creates opportunities for processors to develop ambient-stable products that expand market reach and reduce distribution costs.

By Packaging: Bulk Efficiency Meets Consumer Convenience Innovation

Bulk containers dominate with 60.22% market share in 2024, reflecting the industrial and food service segments' emphasis on cost efficiency and handling convenience for high-volume applications. These formats optimize transportation costs and reduce packaging waste per unit volume, appealing to sustainability-conscious commercial buyers. Pouches emerge as the fastest-growing packaging format at 6.52% CAGR, driven by consumer convenience trends and portion control benefits that reduce waste in retail applications. Advanced packaging technologies enable flexible formats that maintain product integrity while offering superior convenience and storage efficiency compared to rigid containers.

Cartons and bottles serve mid-volume applications where handling convenience and brand visibility requirements balance cost considerations. The shift toward flexible packaging reflects broader food industry trends emphasizing sustainability and consumer convenience. Pouches offer superior barrier properties and reduced material usage compared to rigid alternatives while enabling innovative dispensing mechanisms that enhance user experience.

By Distribution Channel: Industrial Foundation Supports Retail Expansion

Industrial channels command 50.16% market share in 2024, serving food manufacturers, bakeries, and processing facilities that require consistent quality and competitive pricing for large-volume applications. This segment benefits from established relationships and contract-based purchasing that provides revenue stability for liquid egg processors. Food service and institutional channels serve restaurants, cafeterias, and catering operations that prioritize convenience and food safety over cost considerations. Retail channels demonstrate the strongest growth at 7.25% CAGR, reflecting consumer adoption of convenient cooking solutions and increasing availability of consumer-friendly packaging formats.

The retail segment's growth trajectory reflects fundamental shifts in consumer behavior toward convenient, healthy protein sources that reduce meal preparation time. Rising consumer awareness of liquid eggs' safety advantages over shell eggs, combined with expanding product variety and improved packaging, drives retail adoption. This channel expansion creates opportunities for premium positioning and brand differentiation that can command higher margins compared to commodity-focused industrial sales.

Geography Analysis

North America holds 34.48% market share in 2024, driven by established food processing infrastructure, comprehensive regulatory frameworks, and high per-capita protein consumption. The region's advanced cold-chain logistics and consumer acceptance of processed foods support liquid egg adoption in retail and food service segments. While volume growth remains limited due to market maturity, opportunities exist in value-added products and premium positioning.

Asia-Pacific demonstrates the highest growth rate at 7.43% CAGR through 2030, fueled by urbanization, middle-class expansion, and increasing protein consumption. China's position as a major egg producer creates opportunities for liquid egg processing growth. While the region shows strong demand potential, cold-chain infrastructure limitations in emerging markets present spoilage risks. South Asia and Southeast Asia exhibit robust growth prospects through 2030, supported by economic development and evolving consumer preferences.

Europe maintains a stable market presence with strong regulations and consumer acceptance, despite competition from plant-based alternatives and market saturation. The region's focus on animal welfare creates demand for cage-free and ethically sourced liquid egg products at premium prices. Middle East, Africa, and South America offer growth potential through urbanization and food processing industry expansion, though infrastructure gaps and economic instability require strategic local partnerships for market development.

Competitive Landscape

The liquid egg market exhibits moderate fragmentation with a 4 out of 10 rating, indicating fragmented competition with opportunities for consolidation among regional and specialty players. Leading processors pursue vertical integration strategies that control supply chains from production through distribution, while smaller players focus on niche segments or regional markets where specialized products command premium pricing.

The adoption of advanced pasteurization methods, including high-temperature short-time processing and ultra-high temperature treatment, along with innovative packaging technologies such as aseptic packaging and modified atmosphere packaging, enables companies to gain market share by offering products with enhanced quality and longer shelf life. Companies are expanding their geographic presence and product portfolios through strategic acquisitions and consolidation, focusing on complementary businesses, distribution networks, and manufacturing capabilities to strengthen their market position.

The market presents significant growth opportunities in emerging regions where limited cold-chain infrastructure drives demand for shelf-stable products. In the premium segment, products such as organic, cage-free, and specialty nutritional offerings provide manufacturers with opportunities for higher profit margins. These premium categories attract health-conscious consumers willing to pay more for products that align with their dietary preferences and values. Manufacturers who invest in developing differentiated product lines in these segments can capitalize on the growing consumer demand for high-quality, specialized products.

Liquid Egg Industry Leaders

Igreca S.A.

Ovobest Eiprodukte GmbH & Co. KG

Cal-Maine Foods Inc.

Cargill Incorporated

Michael Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sa-Nguan Farm introduced pasteurized cage-free liquid whole eggs in January 2025 and plans to release pasteurized cage-free liquid egg white and yolk products in mid-2025.

- October 2024: Cooper Farms, based in Oakwood, Ohio, enhanced its egg processing operations through two major investments in its process line. The company, which supplies eggs and liquid egg products to private-label, food and beverage, and foodservice customers, installed storage silos at its Liquid Egg Processing facility in Fort Recovery, Ohio, and integrated a new egg breaker into its production line. These improvements increased the operation's efficiency, capacity, and sustainability.

Global Liquid Egg Market Report Scope

| Whole Liquid Egg |

| Egg White |

| Egg Yolk |

| Blends/Scrambled Mixes (with Milk, Salt, etc.) |

| Refrigerated Liquid |

| Frozen Liquid |

| Ambient/Shelf-stable |

| Cartons |

| Bottles |

| Pouches |

| Bulk Containers |

| Industrial |

| Foodservice and Institutional |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Whole Liquid Egg | |

| Egg White | ||

| Egg Yolk | ||

| Blends/Scrambled Mixes (with Milk, Salt, etc.) | ||

| By Form | Refrigerated Liquid | |

| Frozen Liquid | ||

| Ambient/Shelf-stable | ||

| By Packaging | Cartons | |

| Bottles | ||

| Pouches | ||

| Bulk Containers | ||

| By Distribution Channel | Industrial | |

| Foodservice and Institutional | ||

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the liquid egg market?

The liquid egg market is valued at USD 3.22 billion in 2026 and is expected to reach USD 4.16 billion by 2031.

Which region shows the fastest growth for processed liquid eggs?

Asia-Pacific leads with a projected 7.43% CAGR through 2031 owing to urbanization and a growing middle class.

Why are ambient/shelf-stable liquid eggs gaining attention?

Ultra-pasteurization and aseptic packaging extend shelf life to nine months, removing cold-chain dependence and lowering logistics costs.

Which packaging format is expanding quickest at retail?

Consumer-friendly pouches are growing at a 6.52% CAGR as they offer portion control and reduced plastic weight.

Page last updated on: