United States Bottled Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 67.20 Billion |

| Market Size (2026) | USD 74.13 Billion |

| Market Size (2031) | USD 94.02 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Bottled Water Market Analysis by Mordor Intelligence

The United States bottled water market is expected to increase from USD 67.2 billion in 2025 to USD 74.13 billion in 2026 and reach USD 94.02 billion by 2031, growing at a CAGR of 4.87% over 2026-2031. This market growth is driven by a significant shift in consumer beverage preferences, with individuals increasingly replacing sugary drinks with packaged water and prioritizing water quality assurance. Retail sales data indicate that bottled water has transitioned from being an occasional purchase to a staple in daily consumption. Additionally, the increasing awareness of health and wellness among consumers is further boosting the demand for bottled water, as it is perceived as a healthier alternative to other beverages. However, challenges such as rising packaging costs and the growing adoption of home filtration systems are exerting pressure on margins in certain channels. Despite these challenges, the market is expected to maintain a steady growth trajectory over the coming years, supported by innovations in packaging, sustainability initiatives, and the introduction of enhanced water products with added minerals and flavors.

Key Report Takeaways

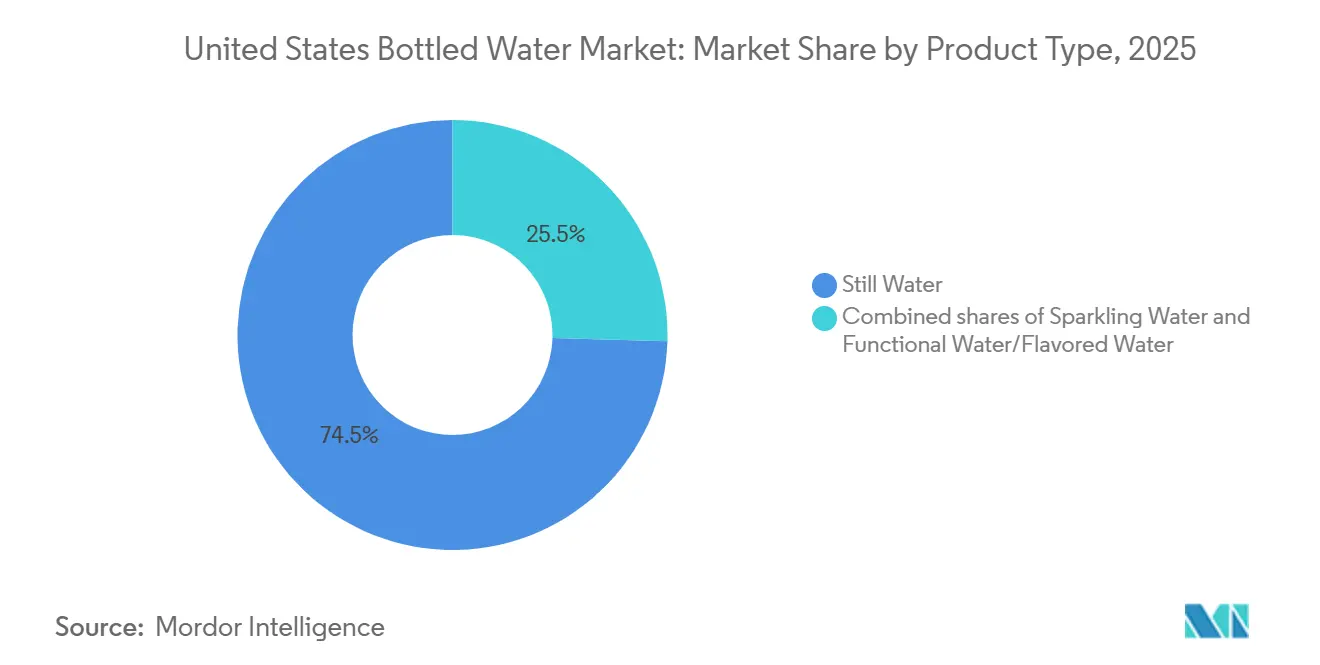

- By product type, still water held 74.5% of the United States bottled water market share in 2025, while functional water and flavored water are forecast to expand at a 5.7% CAGR through 2031.

- By packaging type, PET accounted for 77.9% of the 2025 value, while cans recorded the highest projected CAGR at 5.4% through 2031.

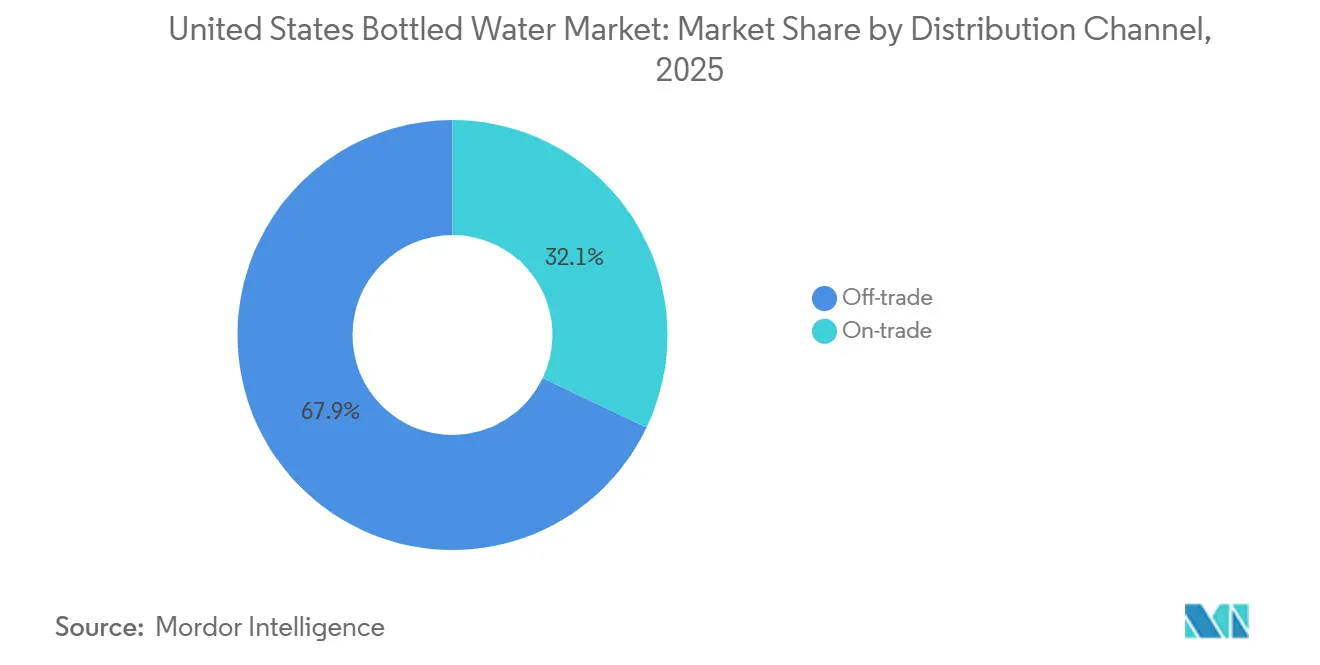

- By distribution channel, off-trade held 67.9% of the 2025 value, while on-trade is advancing at a 5.7% CAGR through 2031.

- By geography, the West held 28.3% of the United States bottled water market share in 2025 and also recorded the highest forecast CAGR at 4.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from sugary beverages to healthier hydration | +1.2% | National, concentrated in South and Midwest where soda consumption is highest | Long term (≥ 4 years) |

| Rising safety concerns around tap water quality | +0.9% | National, acute in Northeast and Midwest | Medium term (2-4 years) |

| Convenience, portability, and on-the-go consumption | +0.7% | National, strongest in urban cores and commuter markets in the West and Northeast | Medium term (2-4 years) |

| Premiumization in sparkling, functional, and imported water | +0.8% | West and Northeast, with spillover to South Sun Belt metros | Long term (≥ 4 years) |

| Climate-linked household preparedness buying | +0.5% | South, Southwest, and Mid-Atlantic | Short term (≤ 2 years) |

| Social media-led brand discovery among Gen Z and millennials | +0.4% | National, highest velocity in urban West and Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift from sugary beverages to healthier hydration

The shift from carbonated soft drinks to water appears to be a long-term trend rather than a temporary wellness phase. This change is further supported by medical and lifestyle factors. In 2026, Danone highlighted that the use of GLP-1 therapies is encouraging consumers in the United States to move away from caloric beverages and opt for water. GLP-1 therapies, which are often prescribed for weight management and diabetes, influence consumer preferences by promoting the adoption of healthier, low-calorie beverage options. This trend is particularly significant for enhanced hydration products, as individuals using GLP-1 therapies often prefer low-calorie drinks that provide additional benefits beyond basic hydration, such as added electrolytes or vitamins. Additionally, the United States Department of Agriculture (USDA) data indicates a decline in the consumption of added-sugar beverages, reinforcing the perspective that this demand shift is structural and likely to persist over the long term.

Rising Safety Concerns Around Tap Water Quality

Concern about municipal water quality continues to support a stable demand floor for the United States bottled water market. Analysis of Environmental Protection Act (EPA) monitoring data reported in 2025 found that more than 73 million Americans are exposed to Per- and Polyfluoroalkyl Substances (PFAS) levels in tap water that exceed EPA maximum contaminant limits. Food and Drug Administration (FDA) testing of 197 domestic and imported bottled water samples in 2024 detected PFAS in 10 samples, but none exceeded EPA standards for tap water, which helps reinforce bottled water’s quality positioning[1]Source: U.S. Environmental Protection Agency, “PFAS Standards and Tap Water Monitoring Framework Referenced in User Draft,” U.S. Environmental Protection Agency, epa.gov. Lead exposure concerns add to that pattern because a 2025 peer-reviewed study found that 84.7% of tested United States homes had at least trace levels of lead in their water, and 1.6% exceeded 10 parts per billion. The Northeast remains especially important in this discussion because older housing stock and older pipes keep water quality concerns visible in daily consumer decisions. As a result, the United States bottled water market continues to draw support from households that want sealed water for routine use as well as for risk mitigation.

Premiumization in sparkling, functional, and imported water

Value growth in the United States bottled water market is increasingly driven by premium price tiers, although mainstream formats continue to dominate total volume. This shift reflects changing consumer preferences, with a growing emphasis on quality, health benefits, and brand image. Primo Brands reported in Q1 2026 that Saratoga Spring Water and Mountain Valley achieved a 43% growth, gaining both dollar and volume share across mass, club, and away-from-home channels. This significant growth underscores the rising demand for premium bottled water options among consumers. Danone allocated over EUR 20 million (approximately USD 22 million) to modernize the Evian bottling facility over two years and expanded the brand’s presence in the hospitality sector in Las Vegas. This investment not only enhances production capabilities but also strengthens the brand’s positioning in high-end markets. These developments highlight the role of premium water as both a service offering and an image enhancer, appealing to consumers seeking exclusivity and quality.

Social Media-Led Brand Discovery Among Gen Z and Millennials

Social platforms are shortening the path from brand exposure to beverage trial in the United States bottled water market. This matters because category growth is no longer shaped only by shelf position and trade spend, but also by how well brands can fit digital habits and identity-led consumption cues. For example, Hint’s national "MMMMM Water" campaign, launched in May 2026 across streaming platforms, digital channels, social media, podcasts, out-of-home advertising, and retail activations, highlights the growing importance of social visibility in driving demand. The campaign’s multi-channel approach demonstrates how brands are leveraging diverse platforms to engage consumers and create a cohesive brand presence. Keurig Dr Pepper’s 2025 beverage trend report also found that 72% of Gen Z consumers try a new beverage each month, which suggests a high level of switching and experimentation[2]Source: Keurig Dr Pepper, “State of Beverages 2025 Trend Report Referenced in User Draft,” Keurig Dr Pepper, keurigdrpepper.com. This environment benefits brands that can quickly link visual identity, flavor positioning, and functional claims to prompt purchase decisions, emphasizing the need for agility and innovation in marketing strategies to capture consumer interest effectively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic waste scrutiny and packaging regulation pressure | -0.5% | California, Northeast, and national supply chains | Short term (≤ 2 years) |

| Mid-Market brand compression from private label and premium brands | -0.4% | National, most acute in value-oriented Midwest and South retail formats | Medium term (2-4 years) |

| Growth substitution from home filtration and refillable bottles | -0.6% | National, concentrated in urban West and Northeast | Long term (≥ 4 years) |

| Inflation sensitivity in single-serve and premium formats | -0.4% | National, with greater impact in lower-income Midwest and rural South markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plastic waste scrutiny and packaging regulation pressure

Packaging regulation is creating a near-term cost burden for PET-heavy players in the US bottled water market. California’s SB 54 took effect on May 1, 2026, and requires all single-use plastic packaging to be recyclable or compostable by 2032, along with a 25% reduction in single-use plastic and a 65% recycling rate. Full implementation begins on January 1, 2027, which means producers selling into California must register, submit packaging data, and carry out source reduction plans. These rules matter beyond one state because California is part of the West, which held 28.3% of the 2025 value in the United States bottled water market. The Western region's significant market share highlights the potential ripple effects of these regulations across the industry, influencing packaging strategies nationwide. Larger companies are better positioned to manage redesign efforts due to their resources and scale, while smaller regional brands face greater challenges balancing compliance costs, packaging changes, and retailer demands. This is accelerating the shift toward rPET, cans, and other alternatives, which were already gaining momentum for commercial reasons.

Growth substitution from home filtration and refillable bottles

Home filtration systems and refill behaviors are limiting certain household consumption occasions in the United States bottled water market. The primary impact is on routine at-home consumption, as filtration systems provide an alternative for daily drinking while maintaining the relevance of bottled water for travel, emergencies, hospitality, and premium use cases. Filtration systems allow consumers to access clean drinking water conveniently at home, reducing the need for frequent purchases of bottled water for everyday use. Consumers who adopt filtration systems often reduce their purchases of entry-level packs for pantry stocking but do not entirely exit the category. Instead, they continue to rely on bottled water for specific occasions where convenience, portability, or premium quality is prioritized. Consequently, brands are shifting their focus toward higher-margin packs, premium offerings, and occasion-based positioning to sustain revenue growth as unit growth becomes more challenging. This strategic shift highlights the importance of adapting to evolving consumer preferences while maintaining relevance in key consumption scenarios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Water Anchors Volume While Functional Formats Drive Value

Still water accounted for 74.5% of the US bottled water market size in 2025, which keeps it firmly positioned as the category’s core volume and value base. Its strength comes from broad affordability, wide availability, and suitability across daily hydration occasions from convenience purchases to bulk household stocking. The segment is also deeply embedded in large-format retail and home-and-office delivery, which makes it hard for premium or niche products to match at scale. Private-label still water remains important because large retail chains use it to maintain price access while protecting category traffic.

Functional water/flavored water is the fastest-growing product type in the United States bottled water market at a 5.7% CAGR from 2026 to 2031. Growth is being supported by consumers who want hydration with added benefits such as electrolytes, vitamins, antioxidants, and lower-calorie refreshment. Keurig Dr Pepper’s nationwide February 2026 rollout of Bai Barù Blood Orange shows that large beverage groups are already treating this part of the US bottled water industry as a priority area for product innovation.

By Packaging Type: PET Maintains Dominance Despite Sustainability Headwinds

PET represented 77.9% of the United States bottled water market size in 2025, which reflects its cost efficiency, light weight, and fit with high-volume retail logistics. PET remains the default format for mainstream single-serve and multipack products because it supports low unit costs and broad retail compatibility. That position is still strong, but it is facing more pressure from regulation and consumer concerns around single-use plastics. Glass keeps a smaller place in the category, mainly in premium dining and hospitality settings, where packaging appearance and perceived purity support higher pricing. Danone’s use of recycled PET for all Evian volumes sold in North America shows how large suppliers are trying to preserve PET’s role while adapting it to tighter sustainability standards.

Cans are the fastest-growing packaging format in the United States bottled water market at a 5.4% CAGR from 2026 to 2031. Their momentum comes from a mix of recyclability, premium visual identity, and growing acceptance beyond sparkling water. Hint’s May 2026 launch of 19.2-oz cans across its flavored still water range shows that can adoption is spreading into still and functional formats rather than staying limited to one subcategory.

By Distribution Channel: Off-Trade Scale Meets On-Trade Growth Premium

Off-trade accounted for 67.9% of the United States bottled water market size in 2025, making it the main channel for volume movement across the country. Supermarkets, club stores, convenience outlets, home-and-office delivery, and online platforms together give the US bottled water market its national reach and replenishment frequency. Primo Brands’ distribution footprint of more than 200,000 retail outlets shows how scale in store coverage can shape share and visibility in the mainstream tier. Home-and-office delivery remains valuable because it supports recurring demand in offices, households, and institutions where convenience and perceived purity outweigh price.

On-trade is the fastest-growing channel in the United States bottled water market at a 5.7% CAGR from 2026 to 2031. The channel benefits from higher per-unit pricing because restaurants, hotels, entertainment venues, and travel settings attach service and experience value to bottled water. Danone’s 2026 expansion of Evian placements across Las Vegas properties shows how premium water brands are using hospitality to build both pricing power and broader brand recognition.

Geography Analysis

The West accounted for 28.3% of the United States bottled water market size in 2025 and is also the fastest-growing region with a 4.9% CAGR through 2031. California remains the leading state inside this regional cluster because it combines high spending power, strong premium retail infrastructure, and early adoption of functional hydration formats. The state’s packaging rules are also pushing producers toward recyclable and aluminum-based options faster than in many other parts of the country. Oregon and Washington add to the region’s depth through growing urban populations that respond well to premium, flavored, and wellness-oriented water propositions. Taken together, these factors keep the West at the center of both value growth and format innovation in the United States bottled water market.

The South is the second-largest demand zone in the United States bottled water market. Population growth across Texas, Florida, Georgia, and the Carolinas continues to expand the addressable consumer base for everyday packaged hydration. Climate exposure adds another layer because households in hurricane-prone areas treat bottled water as a preparedness product as well as a daily beverage. International Bottled Water Association (IBWA) highlighted in 2025 that Federal Emergency Management Agency (FEMA) recommends at least 1 gallon of bottled water per person per day for emergency readiness, while National Oceanic and Atmospheric Administration (NOAA) expected an above-normal Atlantic hurricane season[3]International Bottled Water Association, “2025 Bottled Water Statistics and Market Facts,” International Bottled Water Association, bottledwater.org. Research published in the Journal of Agricultural and Applied Economics also found that households in the southeastern US can raise bottled water stockpiling to as much as 4 times weekly volume before hurricane events. These conditions give the South a structurally strong demand floor even when premiumization is less advanced than on the West Coast.

The Northeast remains the most strategically important region for premium, imported, and functional water in the United States bottled water market. Dense urban populations, strong on-trade networks, and high-income consumers support better value per unit than in more price-led regions. Water quality concerns also remain visible because older urban infrastructure and legacy pipe systems keep sealed packaged water attractive for risk-aware households. The Midwest is more price sensitive and depends more heavily on private-label packs, club stores, and practical household buying, which keeps growth steadier and more volume-led than premium-led.

Competitive Landscape

The United States bottled water market remains anchored by a small set of large platform companies, especially Primo Brands Corporation, The Coca-Cola Company, PepsiCo, and Danone, while premium and functional brands continue to create pockets of faster value growth. Primo Brands has a particularly strong position because the November 2024 merger of Primo Water and BlueTriton created a business with USD 6.5 billion in combined revenue, more than 80 spring sources, and distribution across over 200,000 retail outlets. That scale gives the company a broad reach in mainstream still water while still allowing targeted growth in premium sub-brands. Primo Brands also reported in Q1 2026 that Mountain Valley and Saratoga grew 43%, which shows that size does not prevent premium brand momentum when channel strategy is well managed. The large-company layer of the US bottled water market, therefore, combines supply chain depth, brand portfolios, and national retail leverage in ways that smaller players cannot easily match.

At the same time, competitive room still exists in segments where consumers pay more for format, function, or identity rather than simple hydration. Hint’s March 2026 brand refresh and May 2026 national campaign with canned expansion show how branded flavored water can compete through message, aesthetics, and format moves instead of broad price competition. Danone’s hospitality expansion for Evian in Las Vegas reflects another route to growth, where premium placements help shape perception and support price realization beyond the immediate venue. This means the United States bottled water market is not defined only by scale, but also by who can build the strongest link between product form, channel context, and consumer meaning.

Portfolio reshaping is also part of the current competitive picture. In March 2026 that Nestlé advanced the sale of a 50% stake in its European water business, including Perrier, San Pellegrino, and Acqua Panna, at a valuation of EUR 5 billion, or USD 5.75 billion, which could influence how premium imported water is managed in the United States. State packaging rules are also becoming a competitive filter because companies with stronger rPET or aluminum capabilities can adapt faster in markets with tighter compliance demands. The United States bottled water market therefore continues to reward scale, premium brand stewardship, and packaging flexibility at the same time. Strategic moves since late 2024 show that consolidation, premium channel expansion, and functional product development remain the main ways companies are competing for growth.

United States Bottled Water Industry Leaders

Primo Brands Corporation

The Coca-Cola Company

PepsiCo, Inc.

Nestlé SA

Danone SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hint, Inc. launched its "MMMMM Water" national brand campaign and introduced 19.2-oz cans for its unsweetened flavored still water range, its first major national marketing moment since 2024, spanning streaming, CTV, digital, social, podcasts, out-of-home, and retail activation.

- March 2026: Hint, Inc. unveiled a comprehensive brand refresh, repositioning the brand under the platform "Water for People with Tastebuds," with new visual identity, creative direction, and expanded product formats targeting the growing flavored still water opportunity in the United States.

- February 2026: Keurig Dr Pepper launched Bai Barù Blood Orange, an antioxidant-infused water beverage, targeting the functional water opportunity among citrus-forward and health-conscious consumers across the United States.

United States Bottled Water Market Report Scope

Bottled water refers to drinking water packaged in glass or plastic bottles. The United States bottled water market is segmented by product type, by packaging material, by distribution channel, and by geography. Based on product type, the market is segmented into still water, sparkling water, and functional/flavored water. Based on packaging type, the market is segmented into PET, glass, cans, and others. Based on distribution channel, the market is segmented into on-trade and off-trade distribution channels. The off-trade distribution channel is further sub-segmented into supermarkets/hypermarkets, convenience/grocery stores, home and office delivery (HOD), online retail stores, and other off-trade distribution channels. By geography, the market includes the Northeast, the Midwest, the South, and the West. For each segment, market sizing and forecasts have been conducted based on value (in USD).

| Still Water |

| Sparkling Water |

| Functional Water/Flavored Water |

| PET |

| Cans |

| Glass |

| Others |

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Home and Office Space | |

| Online Retail Stores | |

| Other Off-trade chanels |

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Still Water | |

| Sparkling Water | ||

| Functional Water/Flavored Water | ||

| By Packaging Type | PET | |

| Cans | ||

| Glass | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Home and Office Space | ||

| Online Retail Stores | ||

| Other Off-trade chanels | ||

| By Geography | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the current size of the United States bottled water market?

The United States bottled water market is valued at USD 74.1 billion in 2026 and is projected to reach USD 94 billion by 2031 at a 4.9% CAGR.

What is driving growth in bottled water demand in the United States?

The biggest drivers are substitution away from sugary drinks, persistent concern about tap water quality, premiumization, and faster brand discovery through digital channels.

Which product segment leads bottled water sales in the United States?

Still water led with 74.5% of 2025 value, supported by wide availability, low cost, and strong private-label presence.

Which packaging format is growing the fastest?

Cans are the fastest-growing packaging format with a 5.4% CAGR from 2026 to 2031, helped by recyclability and stronger premium positioning.

Page last updated on: