Food & Beverage

2nd MayMarket Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

The Bottled Water Market in Saudi Arabia is Segmented by Type (Still Water, Functional/Enhanced Water, and More), Packaging Type (PET Bottles and More), Nature (Organic and Conventional), Packaging Size (≤330 Ml, and More), Distribution Channel (Retail Channels, and More), and Region (Northern and Central Region, Western Region and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

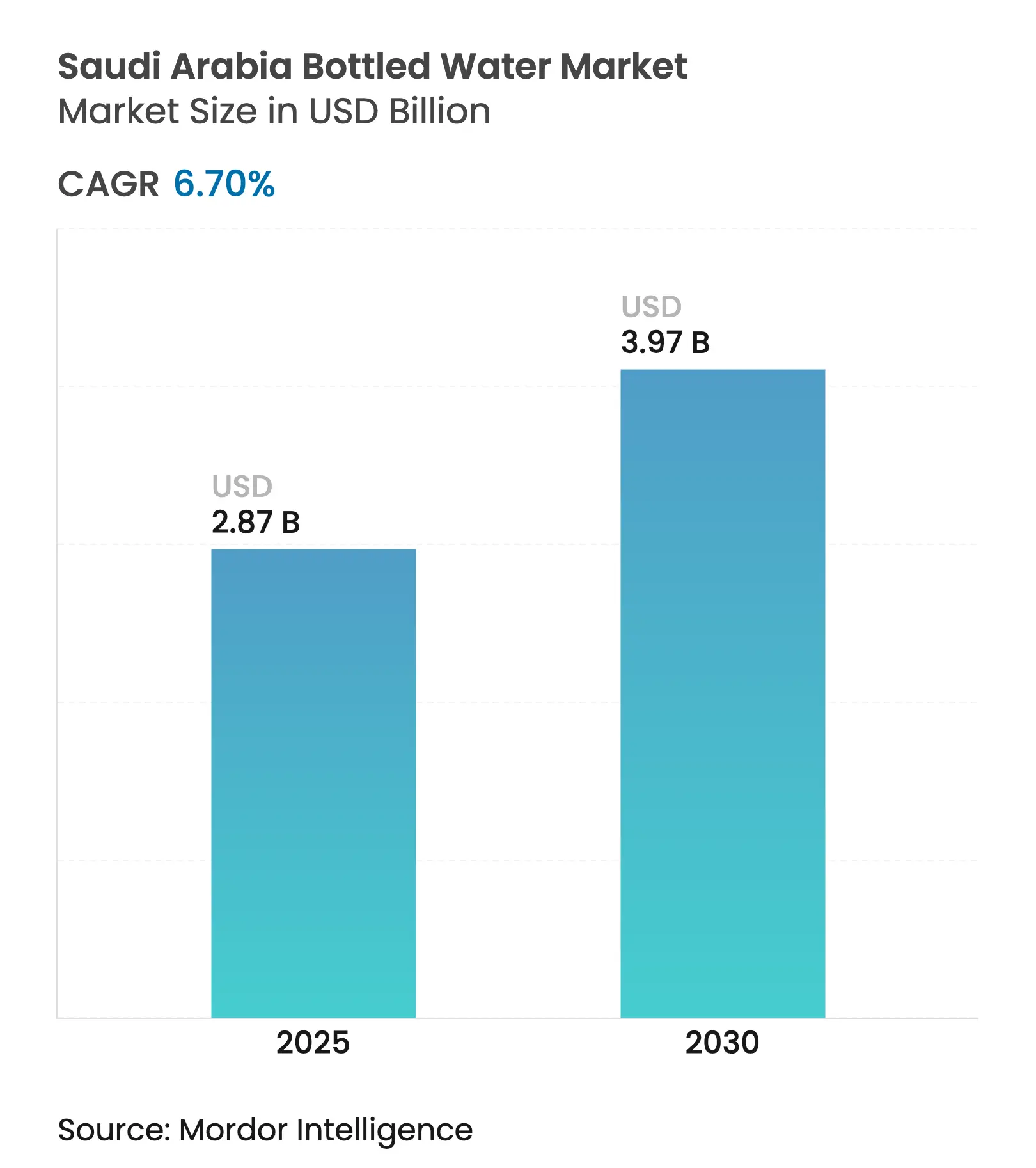

| Market Size (2025) | USD 2.87 Billion |

| Market Size (2030) | USD 3.97 Billion |

| Growth Rate (2025 - 2030) | 6.70 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Saudi Arabia Bottled Water Market size is estimated at USD 2.87 billion in 2025, and is expected to reach USD 3.97 billion by 2030, at a CAGR of 6.70% during the forecast period (2025-2030). This growth trajectory reflects the Kingdom's unique consumption dynamics driven by religious tourism, climate conditions, and evolving consumer health consciousness[1]Source: Saudi Vision, "Kingdom's unique consumption dynamics", my.gov.sa. Rising health awareness, religious tourism, and product innovation support steady growth, while climate-related water scarcity and Vision 2030 sustainability mandates shape supply-side strategies. The market's expansion aligns with Vision 2030's economic diversification goals while addressing water security challenges through sustainable production practices and regulatory compliance frameworks established by the Saudi Food and Drug Authority. Religious pilgrimage emerges as a distinctive demand catalyst, with Hajj and Umrah activities generating substantial seasonal consumption spikes that differentiate this market from conventional regional patterns. The General Presidency for the Affairs of the Prophet's Mosque distributes up to 400 tonnes of Zamzam water daily during Ramadan alone, while the broader pilgrimage economy supports year-round bottled water demand from millions of international visitors [2]Source: Saudi Press Agency, " 400 Tonnes of Zamzam Water Provided Daily for Visitors to the Prophet's Mosque during Ramadan", spa.gov.sa.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Introduction of enhanced and functional variants Introduction of enhanced and functional variants | +1.2% | National, with premium segments in Riyadh, Jeddah | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

National, with premium segments in Riyadh, Jeddah

|

Impact Timeline

:

Medium term (2-4 years)

|

Health Awareness and Preventive Consumption Trends Health Awareness and Preventive Consumption Trends | +1.5% | Urban centers, expanding to rural areas | Long term (≥ 4 years) | |||

Pilgrimage-Driven Demand and Infrastructure Expansion Pilgrimage-Driven Demand and Infrastructure Expansion | +1.8% | Western Region (Makkah, Madinah), national spill-over | Short term (≤ 2 years) | |||

Tap Water Quality Concerns and Consumer Shift Tap Water Quality Concerns and Consumer Shift | +0.9% | National, particularly in industrial areas | Medium term (2-4 years) | |||

Brand Competition and Marketing

Brand Competition and Marketing

| +0.7% | Major metropolitan areas, retail-focused regions | Short term (≤ 2 years) | |||

Retail & Distribution Expansion

Retail & Distribution Expansion

| +0.6% | National, with e-commerce growth in urban centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Introduction of enhanced and functional variants

Functional and enhanced water segments drive market premiumization as manufacturers introduce vitamin-enriched, mineral-fortified, and sports-oriented formulations targeting health-conscious consumers. Agthia Group's strategic decision to triple glass bottled water production capacity reflects growing demand for premium packaging alternatives, while local players like Kinza Drinks disrupt traditional carbonated water segments with innovative flavors under the Made in Saudi Program. The Red Sea Development Company's partnership with SOURCE Global demonstrates breakthrough atmospheric water generation technology that produces 2 million bottles annually using solar power, eliminating traditional sourcing constraints. Innovation extends beyond product formulation to sustainable packaging, where companies explore biodegradable materials and refillable systems to address environmental concerns while maintaining product integrity. Advanced reverse osmosis and Zero Liquid Discharge technologies enhance production efficiency, enabling manufacturers to meet growing demand while reducing environmental impact through brine waste conversion into valuable resources.

Health Awareness and Preventive Consumption Trends

Rising noncommunicable disease prevalence, accounting for 73.2% of deaths in Saudi Arabia, intensifies consumer focus on preventive health measures including hydration optimization and mineral intake management [3]Source: World Bank Group, "Noncommunicable Diseases in Saudi Arabia", worldbank.org. The Saudi Food and Drug Authority's implementation of nutritional labeling requirements and sugar taxation on beverages redirects consumer preferences toward bottled water as a healthier alternative to sugar-sweetened drinks. Quality monitoring studies demonstrate that local bottled water brands like Fayha and Hilwa outperform imported alternatives in meeting SASO safety standards, reinforcing consumer confidence in domestic products. Athletic populations show distinct consumption patterns, with 57.5% of college athletes using sports drinks and 42.5% consuming energy drinks, creating specialized market segments for performance-oriented hydration products. Government health initiatives emphasize dietary improvement and physical activity promotion, indirectly supporting bottled water consumption as part of lifestyle modification programs targeting diabetes and cardiovascular disease prevention.

Pilgrimage-Driven Demand and Infrastructure Expansion

Religious tourism generates unprecedented water demand spikes, with the Kingdom hosting millions of Hajj and Umrah pilgrims annually who require safe, accessible hydration throughout their spiritual journey. The King Abdullah Bottled Zamzam Water Project operates at industrial scale, producing 5,000 cubic meters daily and distributing 200,000 five-liter bottles to meet pilgrimage-specific requirements Ar. Vision 2030's target of accommodating 30 million pilgrims by 2030, compared to current levels, necessitates substantial infrastructure expansion and water supply capacity increases across holy sites. Quality assurance becomes critical during mass gatherings, with authorities implementing comprehensive testing protocols to ensure water safety for international visitors, as demonstrated by 2019 assessments of 55 water samples serving 9.6 million attendees. The National Water Company's SAR 3.1 billion investment in six major water projects specifically addresses pilgrimage-driven demand, including desalinated-water pipelines and expanded treatment facilities to support the projected 41 million cubic meters of water distribution during peak seasons.

Tap Water Quality Concerns and Consumer Shift

Municipal water quality variations and desalination process inconsistencies drive consumer preference for bottled alternatives, particularly in regions experiencing infrastructure transitions. The Saudi Water Authority's shift from thermal desalination to reverse osmosis technology, while improving energy efficiency, creates temporary quality fluctuations that require operational adjustments to maintain chloride levels and control boron and bromate concentrations. Jeddah residents demonstrate heightened quality consciousness, with 60% utilizing water filtration and purification systems, primarily reverse osmosis units, indicating persistent concerns about municipal supply adequacy. Regional water consumption disparities, ranging from 107 liters per capita in Najran to 368 liters in the Eastern Region, reflect varying infrastructure quality and consumer confidence levels in public water systems. Heavy metals and radioactivity monitoring studies reveal ongoing vigilance requirements for drinking water safety, with research emphasizing the need for stringent quality checks given the Kingdom's reliance on aquifer sources and bottled water alternatives.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Counterfeiting and Substandard Products

Counterfeiting and Substandard Products

| -0.8% | National, concentrated in border regions | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

National, concentrated in border regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

Seasonal Demand Volatility

Seasonal Demand Volatility

| -0.6% | Western Region pilgrimage areas, national tourism zones | Short term (≤ 2 years) | |||

Rise of Alternatives

Rise of Alternatives

| -0.4% | Urban areas with advanced filtration infrastructure | Medium term (2-4 years) | |||

Plastic Waste and Environmental Impact

Plastic Waste and Environmental Impact

| -1.1% | National, with stricter enforcement in major cities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Counterfeiting and Substandard Products

Product authenticity challenges persist across distribution channels, with concerns surrounding premium brands and religiously significant products like Zamzam water. The Ministry of Hajj's enforcement actions against Umrah firms supplying fake Zamzam bottles highlight systematic counterfeiting issues that undermine consumer confidence and brand integrity. The Saudi Intellectual Property Authority's aggressive enforcement approach, demonstrated through blocking 2,500 counterfeit product websites and seizing nearly 1 million fake items in 2023, establishes precedent for bottled water market protection with penalties reaching SRA 1 million and three-year imprisonment terms. Quality monitoring becomes increasingly critical as the Saudi Food and Drug Authority implements enhanced surveillance protocols, with studies revealing that 55% of honey products marketed as health enhancers contained undisclosed adulterants, indicating broader food safety challenges that extend to beverage categories. The new Trade Name Law, effective January 2025, strengthens intellectual property protection through mandatory registration requirements and enhanced enforcement mechanisms, potentially reducing counterfeiting incidents while imposing compliance costs on legitimate manufacturers.

Plastic Waste and Environmental Impact

Environmental regulations targeting single-use plastics create compliance pressures and operational costs for bottled water manufacturers, while consumer awareness of sustainability issues influences purchasing decisions. The Saudi Investment Recycling Company's mandate to achieve 81% recycling rates by 2035 requires substantial infrastructure investments and supply chain modifications that may increase production costs. Plastic packaging regulations introduced in 2017 mandate oxo-biodegradable materials for import compliance, though implementation delays and working group formations indicate ongoing policy uncertainty that complicates long-term planning. The Kingdom's position in UN plastic treaty negotiations, advocating waste management solutions over production limits, suggests regulatory approaches that favor recycling and circular economy initiatives rather than consumption restrictions. Companies like DGrade's expansion into Saudi Arabia, processing 150,000 plastic bottles per hour into clothing, demonstrates emerging waste-to-value opportunities that could offset environmental concerns while creating new revenue streams for packaging waste management.

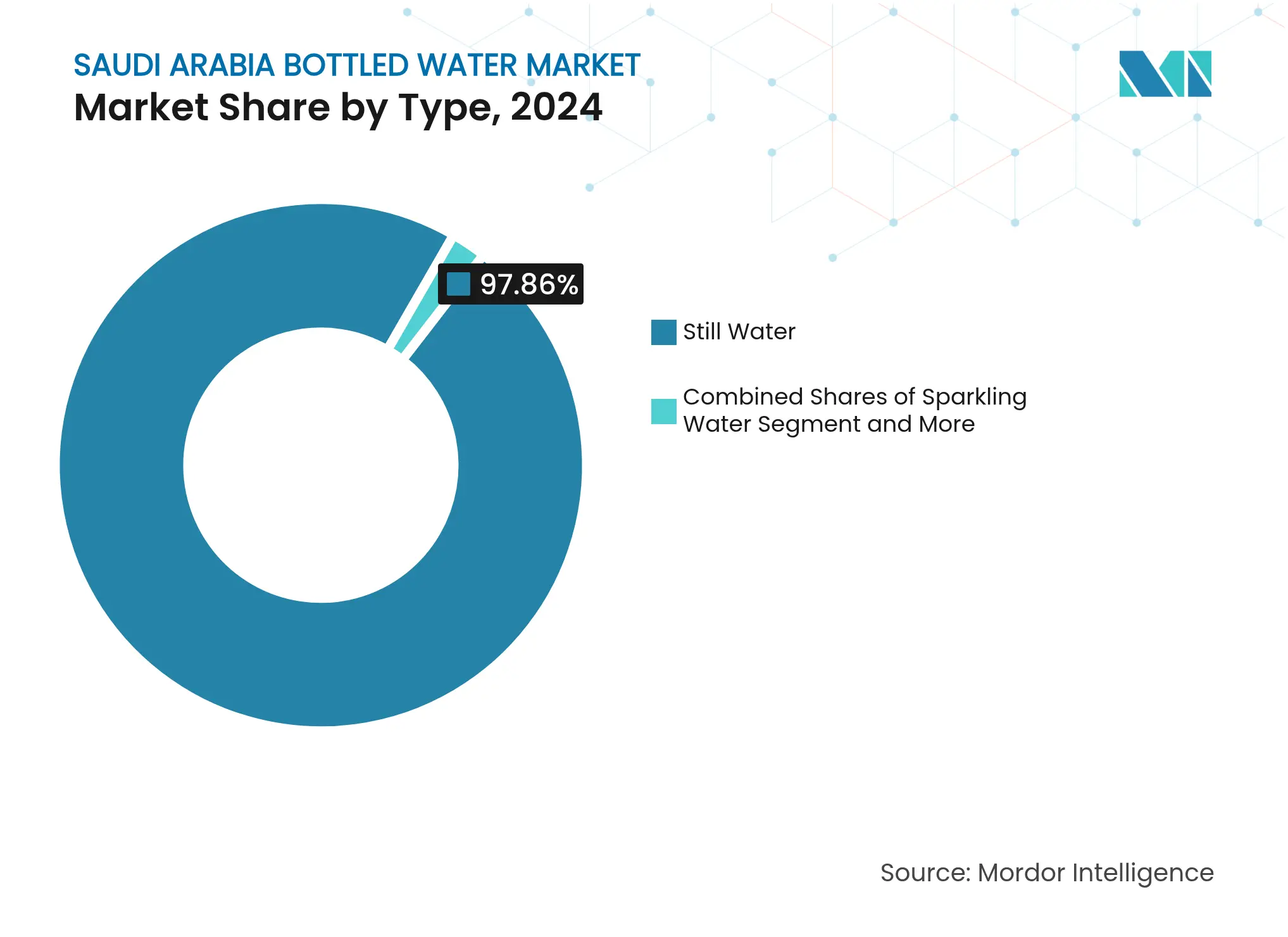

By Type: Still Water Dominance Amid Sparkling Growth

Still water commands 97.86% market share in 2024, reflecting traditional consumption preferences and broad accessibility across all consumer segments, while sparkling water emerges as the fastest-growing category at 8.67% CAGR through 2030. This growth differential indicates premiumization trends where consumers increasingly seek differentiated products beyond basic hydration needs, supported by urbanization and rising disposable incomes in major metropolitan areas. Functional and enhanced water segments gain traction through vitamin fortification, mineral supplementation, and sports-oriented formulations that target health-conscious demographics and athletic populations.

The sparkling water acceleration aligns with international beverage trends and restaurant industry expansion, where carbonated water serves as a premium alternative to traditional soft drinks amid health awareness campaigns. Local manufacturers like Kinza Drinks introduce innovative carbonated water flavors under the Made in Saudi Program, challenging multinational dominance through localized product development and competitive pricing strategies. Enhanced water products benefit from regulatory support through the Saudi Food and Drug Authority's nutritional labeling requirements, which enable clear health benefit communication to consumers seeking functional hydration solutions.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: PET Bottle Leadership Despite Sustainability Pressures

PET bottles maintain 81.26% market share in 2024 while simultaneously recording the highest growth rate at 7.55% CAGR, demonstrating the format's continued dominance despite environmental concerns and regulatory pressures. This apparent contradiction reflects cost advantages, supply chain efficiency, and consumer convenience factors that outweigh sustainability considerations in current market dynamics. Glass bottles experience renewed interest from premium segments, with Agthia Group planning to triple production capacity in response to consumer demand for environmentally conscious packaging alternatives.

Alternative packaging formats including jars and tetra packs serve niche applications but face scalability challenges in mass-market distribution. The Saudi Standards, Metrology and Quality Organization's oversight ensures packaging safety standards compliance across all formats, while environmental regulations mandate oxo-biodegradable materials for certain applications. Innovation in sustainable packaging accelerates through initiatives like The Red Sea Development Company's atmospheric water generation project, which eliminates single-use plastics entirely through on-site production and refillable distribution systems.

By Nature: Conventional Products Lead While Organic Segment Accelerates

Conventional bottled water holds 85.67% market share in 2024, reflecting established production infrastructure and cost-competitive positioning across mass-market segments. Organic water alternatives capture growing consumer interest with 7.72% CAGR growth through 2030, driven by health consciousness and premium positioning strategies that command higher margins for manufacturers. This segmentation reflects broader food industry trends where organic certifications provide differentiation opportunities in increasingly competitive markets.

The organic segment benefits from Vision 2030's emphasis on sustainable agriculture and environmental stewardship, creating policy alignment that supports premium product development. Consumer education initiatives by the Saudi Food and Drug Authority enhance organic product awareness through nutritional labeling requirements and health benefit communication. Local preference trends, with 30% of consumers favoring domestic bottled water brands, create opportunities for organic product positioning that emphasizes local sourcing and environmental responsibility. Quality monitoring studies demonstrate that local brands often exceed international standards, providing credibility foundations for organic product claims and premium pricing strategies.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

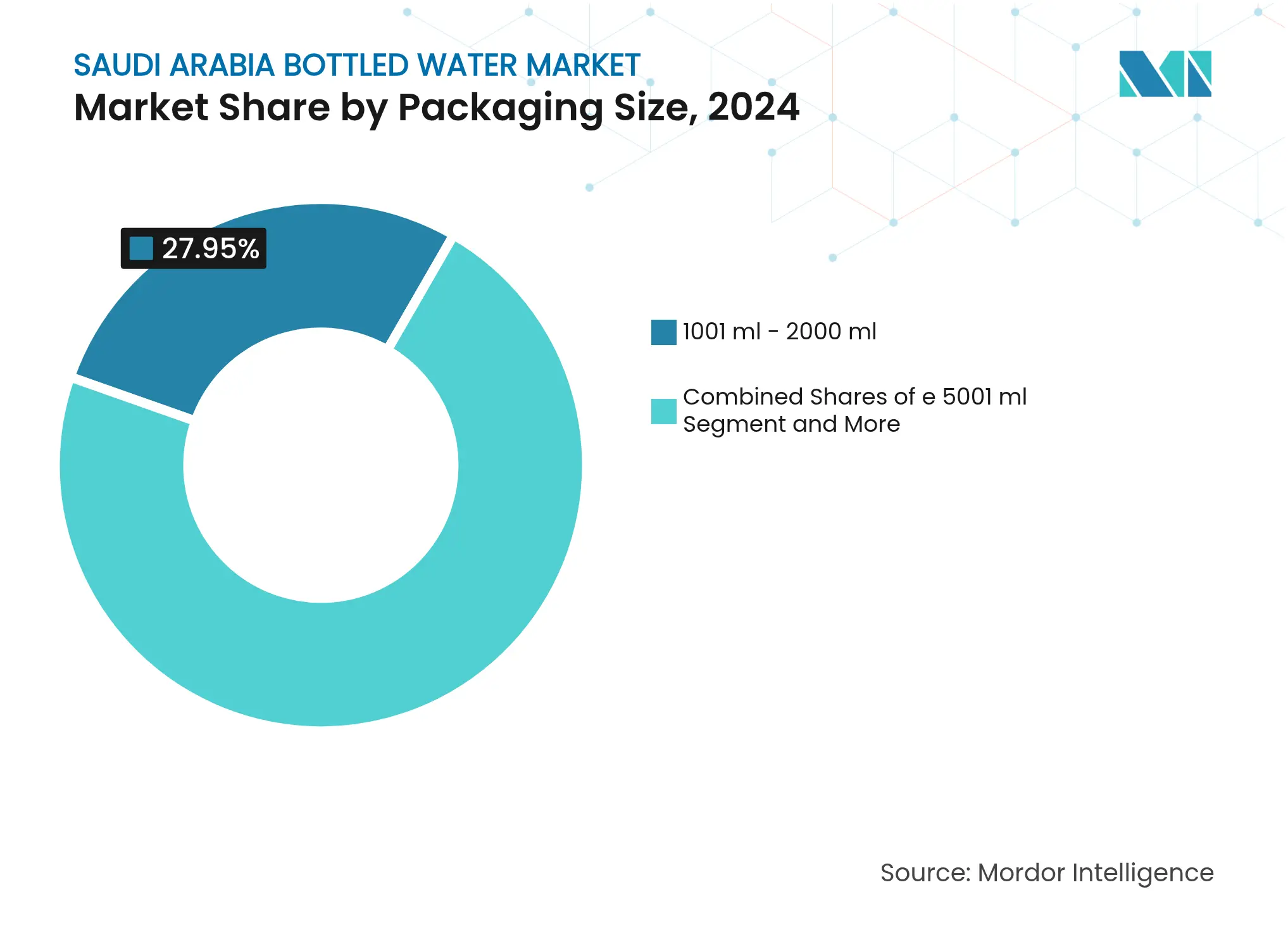

By Packaging Size: Large Formats Drive Growth Amid Diverse Needs

The 1001-2000 ml packaging size leads with 27.95% market share in 2024, optimizing convenience and value propositions for household and office consumption patterns. Large formats (≥5001 ml) post the highest growth rate at 8.05% CAGR, indicating institutional purchasing trends and bulk consumption preferences that reduce per-unit costs for commercial customers. Smaller formats (≤330 ml) serve on-the-go consumption and premium positioning, while mid-range sizes (331-1000 ml) address individual and family usage scenarios across diverse demographic segments.

Institutional demand drives large format growth through foodservice expansion, hospitality sector development, and corporate office consumption that prioritizes cost efficiency and reduced packaging waste. The 2001-5000 ml segment serves family and small business needs, bridging individual and institutional consumption patterns through versatile sizing options. Religious tourism creates unique packaging requirements, with specialized formats for pilgrimage activities and extended travel scenarios that require portable yet substantial hydration solutions. Packaging size optimization reflects supply chain efficiency considerations, where manufacturers balance transportation costs, storage requirements, and consumer preferences to maximize market penetration across diverse usage occasions.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Retail Dominance with Foodservice Momentum

Retail channels command 75.84% market share in 2024, encompassing supermarkets, hypermarkets, convenience stores, and online platforms that provide broad consumer access across urban and rural markets. Foodservice segments accelerate at 8.55% CAGR through 2030, reflecting hospitality industry expansion, restaurant growth, and institutional catering development aligned with tourism and economic diversification objectives. Home and office delivery services gain traction through e-commerce platform integration and direct-to-consumer business models that enhance convenience and bulk purchasing options.

The retail landscape benefits from major players like Panda Retail Co, Abdullah Al Othaim Markets, and Carrefour Saudi Arabia expanding bottled water shelf space allocation and promotional activities. Online retail growth accelerates through digital transformation initiatives and changing consumer shopping behaviors, particularly in urban centers where delivery infrastructure supports convenient access to bottled water products. Foodservice acceleration reflects Vision 2030's tourism development goals, where hotel, restaurant, and catering expansion creates substantial institutional demand for reliable, high-quality bottled water supplies. Convenience and grocery stores maintain significant market presence despite modern format growth, serving neighborhood-level distribution needs and impulse purchasing occasions that complement larger retail channels.

The Northern and Central Region dominates with 43.73% market share in 2024, leveraging Riyadh's population concentration, economic activity, and government sector presence that drives consistent demand across residential and commercial segments. The Western Region posts the highest growth rate at 8.31% CAGR through 2030, benefiting from Makkah and Jeddah's religious tourism, commercial port activities, and pilgrimage-driven consumption that creates seasonal demand spikes and year-round growth momentum.

Eastern and Southern regions contribute smaller but stable market shares, serving industrial, agricultural, and residential needs through established distribution networks. Religious tourism fundamentally shapes Western Region dynamics, where Hajj and Umrah activities generate millions of international visitors requiring safe, accessible hydration throughout their spiritual journey. The General Presidency for the Affairs of the Prophet's Mosque distributes up to 400 tonnes of Zamzam water daily during peak seasons, while broader pilgrimage infrastructure supports commercial bottled water demand.

Vision 2030 mega-projects including NEOM and The Red Sea Development Company concentrate in the Western Region, creating construction workforce demand and future tourism infrastructure that supports sustained market growth. Regional water consumption patterns vary significantly, from 107 liters per capita in Najran to 368 liters in the Eastern Region, reflecting infrastructure quality, economic development levels, and consumer behavior differences that influence bottled water market penetration.

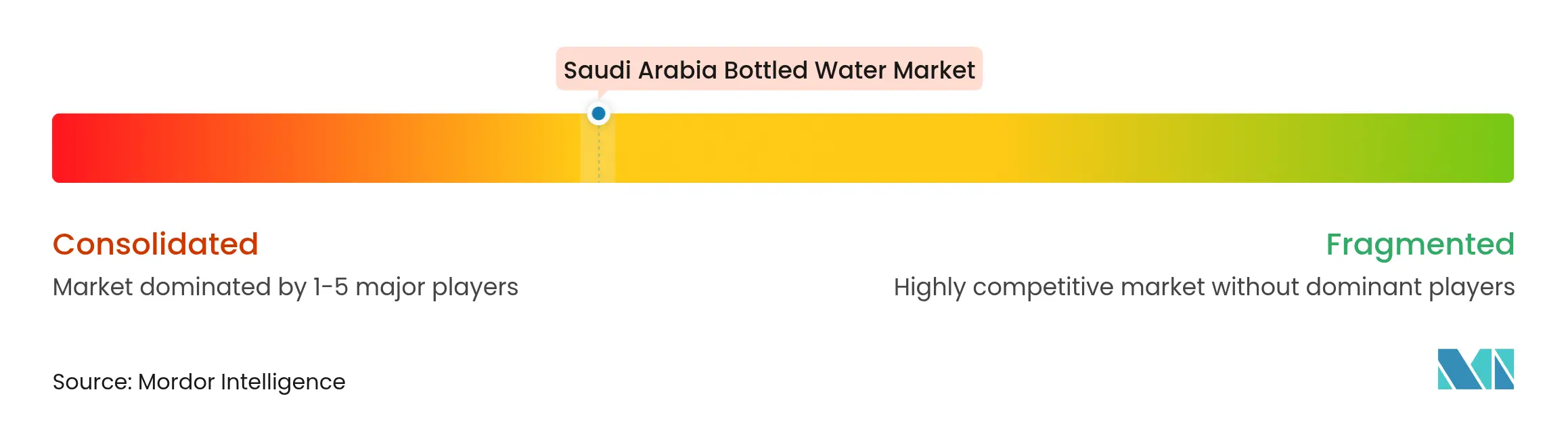

Market Concentration

The Saudi Arabia bottled water market exhibits moderate concentration, where established domestic players compete alongside international brands through integrated business models combining manufacturing capabilities with extensive distribution networks. Large companies collectively hold majority market share despite over 200 licensed producers operating in the market, indicating significant scale advantages and brand recognition barriers that limit smaller player market penetration.

Strategic consolidation accelerates through major acquisitions, exemplified by Almarai's SR1.04 billion purchase of Pure Beverages Industry Company and Hassana Investment Company's 40% stake acquisition in Berain Company, demonstrating how financial investors recognize long-term value creation opportunities in the sector. Innovation-driven differentiation emerges as a key competitive strategy, where companies leverage sustainable packaging, functional formulations, and premium positioning to capture market share beyond traditional price competition. Agthia Group's decision to triple glass bottled water production capacity reflects premiumization trends, while The Red Sea Development Company's atmospheric water generation partnership with SOURCE Global demonstrates how technology integration creates competitive advantages through environmental sustainability and operational efficiency.

Local brand preference, reaching a significant share of consumers for bottled water, creates opportunities for domestic manufacturers to compete effectively against multinational corporations through value positioning, quality assurance, and cultural alignment with Saudi consumer preferences. The Saudi Food and Drug Authority's regulatory framework ensures quality standards compliance across all market participants, while the new Trade Name Law effective January 2025 strengthens intellectual property protection and reduces counterfeiting risks that previously disadvantaged legitimate brand investments.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE and VOLUME)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Bottled water is drinking water packaged in plastic or glass water bottles.

Saudi Arabia's bottled water market is segmented by type, distribution channel, and packaging size. By type, the market is segmented into still water and sparkling water. By distribution channel, the market is segmented into retail channels, home and office delivery, and food service. By packaging size, the market is segmented into less than 330 ml, 331 ml-500 ml, 501 ml-1,000 ml, 1,001 ml-2,000 ml, 2,001 ml-5,000 ml, and more than 5,001 ml. For each segment, the market sizing and forecasts are based on value (USD million).

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.