Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

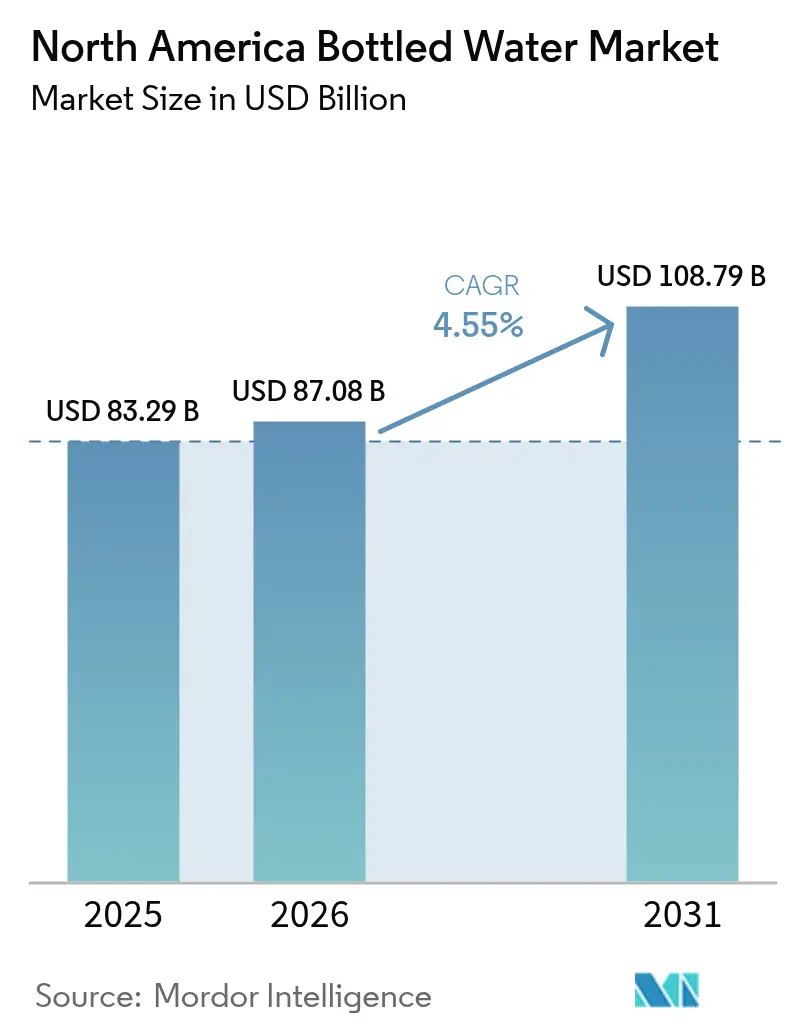

| Base Year Market Size (2025) | USD 83.29 Billion |

| Market Size (2026) | USD 87.08 Billion |

| Market Size (2031) | USD 108.79 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Bottled Water Market Analysis by Mordor Intelligence

The North American bottled water market size is expected to grow from USD 83.29 billion in 2025 to USD 87.08 billion in 2026 and is forecast to reach USD 108.79 billion by 2031 at 4.55% CAGR over 2026-2031. Market growth is driven by increased health consciousness, persistent water quality issues, and a recovery in the tourism and hospitality sectors. While still water remains the primary sales segment, functional and flavored water variants are experiencing increased demand as consumers prioritize health and performance benefits. Manufacturers are implementing packaging innovations, including recycled PET materials and lightweight cans, to meet sustainability requirements while maintaining profitability. The market expansion is further supported by population growth and the convenience of portable bottled water. Functional water, enhanced with vitamins, has gained consumer acceptance due to its convenience, health benefits, and improved taste compared to tap water.

Key Report Takeaways

- By product type, still water led with 74.12% of the market share in 2025, while functional and flavored water are projected to rise at a 5.22% CAGR through 2031.

- By packaging format, PET bottles accounted for 78.05% share of the market in 2025, whereas cans are expected to grow at a 5.61% CAGR through 2031.

- By category, the mass segment held 69.10% share in 2025, and premium offerings are set to expand at a 6.02% CAGR between 2026 and 2031.

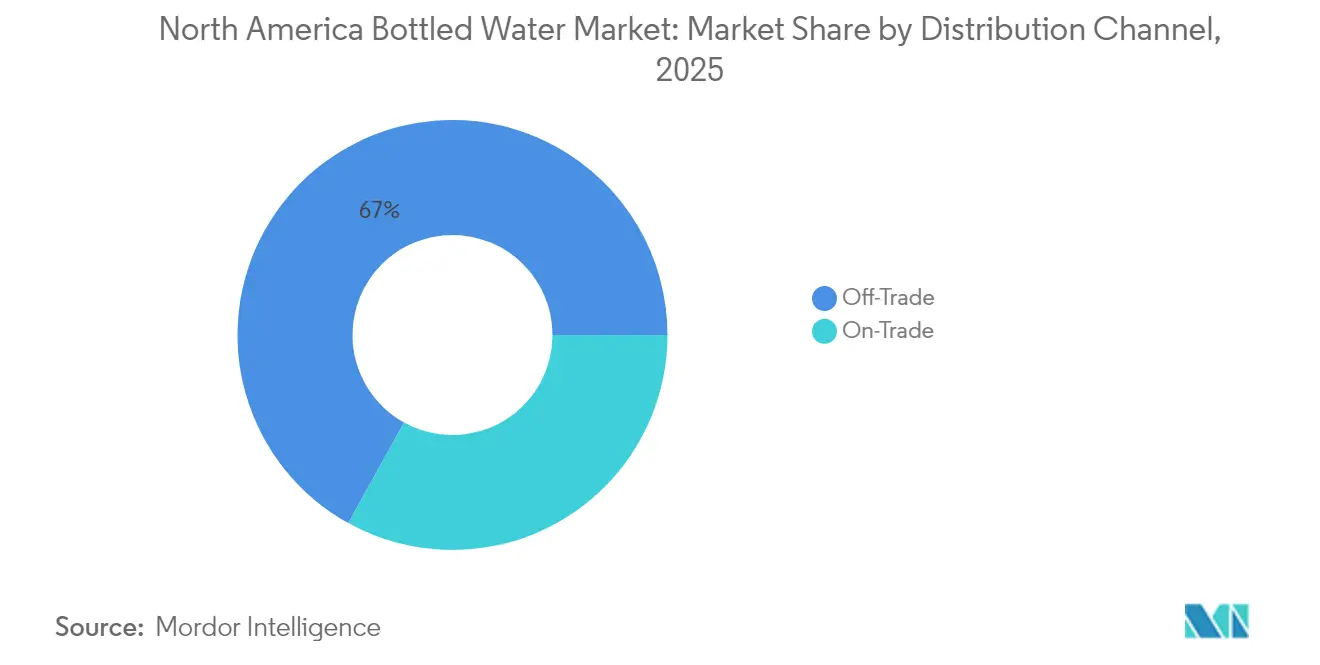

- By distribution channel, off-trade outlets captured 66.95% share in 2025, while on-trade venues are forecast to register a 4.78% CAGR through 2031.

- By geography, the United States commanded 82.10% of the market share in 2025, whereas Mexico is poised for the fastest growth at a 6.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional water from fitness enthusiasts | +1.2% | United States and Canada, urban centers | Medium term (2-4 years) |

| Advertisements and promotional campaigns | +0.8% | North America, digital and traditional media | Short term (≤ 2 years) |

| Growing tourism and hospitality sector | +0.9% | United States, Mexico, Canada tourist destinations | Medium term (2-4 years) |

| Expansion of food service establishments | +0.7% | Urban North America, franchise corridors | Long term (≥ 4 years) |

| Water quality and safety concerns | +1.1% | Global, rural and urban areas | Long term (≥ 4 years) |

| Increased awareness of waterborne diseases | +0.6% | Mexico, rural United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Functional Water From Fitness Enthusiasts

The growing emphasis on health and wellness has transformed consumer perception of hydration from a basic need to a performance enhancement tool. This shift has increased demand for water products enhanced with electrolytes and vitamins. Consumers now associate functional beverages with healthy lifestyles and proactive health management. The fitness community particularly seeks products with natural electrolytes, adaptogens, and minerals for recovery and performance benefits, as these components directly support their athletic pursuits and training goals. According to the U.S. Census Bureau data[1]Source: U.S. Census Bureau, "Percentage of the population engaged in sports, exercise, and recreation per day in the United States", www.bls.gov. from 2023, 21.1% of Americans participated in daily sports, exercise, and recreational activities, indicating a substantial market for functional hydration products. This increased fitness participation has created a robust consumer base seeking specialized hydration solutions. The younger demographic's preference for functional benefits over traditional beverages has reshaped market dynamics significantly. This shift in consumer behavior, combined with growing health awareness, has driven demand for premium functional water products.

Advertisements and Promotional Campaigns

Digital marketing strategies target health-conscious consumers through social media platforms and influencer collaborations to increase brand visibility and educate consumers about hydration benefits. Companies use data analytics to create personalized messages that position bottled water as essential for health-focused consumers. Marketing campaigns focus on brand differentiation through source purity, mineral content, and sustainability credentials to support premium pricing. The emphasis on digital channels allows companies to reach specific consumer segments with tailored messaging about product benefits and environmental commitments. In the premium segment, brand reputation and quality perception significantly influence consumer purchase decisions. The growth of direct-to-consumer channels enables targeted marketing campaigns that reduce retail markups, allowing companies to allocate more resources to consumer education and loyalty programs. These direct channels provide companies with valuable consumer data and feedback, enhancing their ability to refine marketing strategies. Companies leverage this information to develop more effective promotional campaigns and strengthen customer relationships across digital platforms.

Growing Tourism and Hospitality Sector

Tourism in the region is increasing, due to which the demand for bottled water products is increasing. According to the U.S. Bureau of Economic Analysis data[2]Source: U.S. Bureau of Economic Analysis, "Travel and Tourism", www.bea.gov. from 2023, travel and tourism output in the United States increased by 7% in 2023. Hospitality operators increasingly view bottled water as both a revenue generator and a guest satisfaction tool, particularly in regions with questionable tap water quality or taste. The sector's growth creates predictable demand patterns that support long-term supply contracts and distribution partnerships. Hotels implementing sustainability initiatives, such as Marriott's 15% water intensity reduction goals, create opportunities for eco-friendly packaging and refillable bottle programs, according to Marriott International data from 2024. Tourism's seasonal nature requires flexible supply chain management, favoring suppliers with robust distribution networks and inventory management capabilities.

Expansion of Food Service Establishments

The growth of restaurants and quick-service establishments generates consistent demand for bottled water through direct sales and operational requirements, especially in areas with urban development and population growth. Food service operators choose bottled water for their beverage programs due to quality consistency, brand recognition, and higher profit margins compared to tap water. The expansion of franchise networks across North America has standardized bottled water procurement, enabling national supply agreements and volume-based discounts. The standardization of procurement processes has led to improved supply chain efficiency and cost management for food service operators. Additionally, the consistent quality and brand recognition of bottled water products help maintain service standards across multiple locations. Food service establishments are incorporating premium bottled water options to enhance dining experiences and increase average transaction values. The introduction of premium water options has enabled restaurants to differentiate their beverage offerings and capture higher-margin sales. The trend towards healthier beverage choices has further strengthened bottled water's position in food service establishments' beverage programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and plastic waste | -1.4% | North America, environmentally conscious regions | Long term (≥ 4 years) |

| Strong competition from water purifier appliances | -0.9% | United States and Canada, urban households | Medium term (2-4 years) |

| Consumer shift towards sustainability | -0.8% | North America, millennial and Gen Z demographics | Long term (≥ 4 years) |

| High cost associated with functional water | -0.5% | Price-sensitive segments, rural areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Plastic Waste

Environmental awareness has increased consumer resistance to single-use plastic bottles, leading to regulatory measures and corporate sustainability commitments that raise operational costs. Companies are investing in recycling infrastructure and alternative packaging materials, which increases production costs and supply chain complexity. Plastic bottle bans in airports and public venues require companies to use aluminum and glass alternatives. These alternatives have resulted in higher transportation costs across the supply chain. The shift in consumer preferences has also led to increased scrutiny of packaging materials and their environmental impact. The environmental factors continue to drive innovation in packaging design and biodegradable materials development. Companies are implementing comprehensive recycling systems to address sustainability concerns. These initiatives require significant capital investments that affect industry profit margins. The industry is also experiencing pressure to develop more sustainable solutions while maintaining product quality. The balance between environmental responsibility and operational efficiency remains a key challenge for companies in the sector.

Strong Competition From Water Purifier Appliances

Water purification systems for homes and offices provide economical alternatives to bottled water, attracting environmentally conscious consumers and budget-focused households. The adoption of these systems continues to grow as consumers recognize the long-term cost benefits and environmental impact reduction. Installation of purification systems eliminates the need for regular bottled water purchases and storage. These systems also reduce plastic waste associated with bottled water consumption. The convenience of having purified water on demand further enhances their appeal to households and businesses. Water purifiers with IoT features and automated filter replacement notifications simplify maintenance, addressing the convenience advantage of bottled water. The integration of smart technology enables users to monitor water quality and system performance in real-time. In urban areas where tap water meets quality standards, competition increases as bottled water companies focus on convenience, portability, and taste advantages instead of safety benefits. The market dynamics have shifted towards emphasizing user experience and technological innovation. Manufacturers continue to develop advanced features to maintain competitive advantages in the water purification segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Water Dominance Faces Functional Disruption

Still bottled water maintains commanding market leadership with 74.12% share in 2025, reflecting consumer preference for pure, unflavored hydration solutions across diverse consumption occasions. However, functional and flavored bottled water segments demonstrate superior growth momentum at 5.22% CAGR through 2031, driven by health-conscious consumers seeking enhanced benefits beyond basic hydration. This growth differential suggests a gradual market evolution where traditional still water consumption stabilizes while innovation concentrates in value-added segments. Sparkling bottled water occupies a smaller but stable niche, appealing to consumers seeking carbonation without artificial additives or sweeteners.

The functional water segment benefits from technological advances in mineral infusion, electrolyte balancing, and vitamin fortification that maintain product stability and taste profiles. Companies increasingly position functional variants as lifestyle products rather than mere beverages, targeting fitness enthusiasts, health-conscious professionals, and wellness-focused demographics willing to pay premium prices. In March 2024, Essentia Water launched its first-ever range of flavored and functional water products. The products are available in lemon lime, peach-mango, and raspberry pomegranate flavors. The segment's growth trajectory aligns with broader consumer trends toward preventive health measures and performance optimization, creating sustained demand that justifies higher production costs and marketing investments

By Packaging Format: PET Bottles Dominate Despite Sustainability Pressure

PET bottles command 78.05% market share in 2025, benefiting from lightweight properties, cost efficiency, and an established supply chain infrastructure that supports mass market distribution. The format's dominance reflects practical considerations, including transportation costs, breakage resistance, and consumer convenience preferences across diverse retail channels. However, cans experience accelerated growth at 5.61% CAGR through 2031, driven by premium positioning, sustainability perceptions, and enhanced product differentiation capabilities.

Sustainability initiatives increasingly influence packaging decisions, with companies investing in recycled content, lightweighting technologies, and alternative materials to address environmental concerns while maintaining cost competitiveness. The National Association for Packaging Innovation focuses on recyclability improvements, barrier properties for extended shelf life, and design elements that enhance brand differentiation in competitive retail environments. In October 2023, A US-based mountain spring mineral water introduced 100% recycled polyethylene terephthalate (rPET) for its water bottles. The bottles feature CleanFlake label technology, which enhances the recovery of high-quality PET during recycling.

By Category: Premium Segment Outpaces Mass Market Growth

The mass market segment holds 69.10% share in 2025, serving price-conscious consumers who prioritize value and availability over premium features or brand prestige. This segment benefits from economies of scale, efficient distribution networks, and broad retail presence that ensures consistent market access. Conversely, the premium segment accelerates at 6.02% CAGR through 2031, reflecting consumer willingness to pay higher prices for perceived quality, unique sourcing, enhanced packaging, or functional benefits. The premium segment's growth trajectory indicates market maturation where differentiation becomes increasingly important for margin preservation and brand loyalty.

Premium positioning strategies emphasize source authenticity, mineral content, sustainability credentials, or functional enhancements that justify price premiums over mass market alternatives. Companies leverage premium segments to improve overall profitability while using mass market volumes to maintain manufacturing efficiency and distribution leverage.

By Distribution Channel: Off-Trade Dominance Challenged by On-Trade Recovery

Off-trade channels hold a 66.95% market share in 2025, with distribution through supermarkets, hypermarkets, convenience stores, and online retail platforms. This dominance stems from household consumption patterns and bulk purchasing preferences. The channel's strength reflects established consumer shopping habits, effective promotional activities, and efficient inventory management that ensures consistent product availability. On-trade channels are projected to grow at a 4.78% CAGR through 2031. This growth is attributed to tourism recovery, restaurant expansion, and overall hospitality sector development. The channel benefits from higher per-unit pricing and premium product positioning, contributing to increased profitability.

Online retail within off-trade channels shows significant growth due to improved delivery logistics and subscription-based services. Convenience stores and grocery outlets maintain strong performance through strategic location placement and effective promotional programs. The Organisation for Economic Co-operation and Development's tourism recovery forecasts from 2024 indicate positive growth for on-trade channels as international travel returns to normal levels and hospitality venues expand their beverage offerings. Distribution strategies now emphasize the integration of multiple channels, utilizing data analytics and focusing on customer experience optimization across various purchasing points.

Geography Analysis

The United States holds 82.10% of the North American bottled water market in 2025, supported by established consumption patterns, comprehensive distribution networks, and consumer purchasing power across mass market and premium segments. United States consumption reached 16.2 billion gallons in 2024, showing a 2% increase that indicates market maturity while maintaining growth, according to the International Bottled Water Association. The market's strength stems from clear regulations, established quality standards, and widespread consumer trust in bottled water safety. Recent FDA testing confirming the absence of PFAS in bottled water samples has further strengthened consumer confidence and demonstrated regulatory compliance.

Mexico projects the highest regional growth rate at 6.38% CAGR through 2031, driven by infrastructure limitations, water quality issues, and the world's highest per-capita bottled water consumption. In 2023, the Mexican government allocated USD 1.386 billion through SDG Bonds for clean water and sanitation projects, benefiting over 18.7 million people. However, according to the Ministry of Finance and Public Credit, persistent infrastructure gaps continue to drive bottled water demand.

Canada maintains a stable market position with moderate growth, distinguished by strict water quality standards, environmental awareness, and consumer preference for premium products. Statistics Canada's 2024 Biennial Industrial Water Survey offers detailed water use data that guides market strategies and regulatory compliance. The Canadian market leverages its proximity to U.S. distribution systems, aligned consumer preferences, and harmonized regulations to facilitate trade and optimize supply chains.

The Rest of North America, including Caribbean territories, represents a small portion of the market but presents growth potential through tourism expansion and infrastructure development.

Competitive Landscape

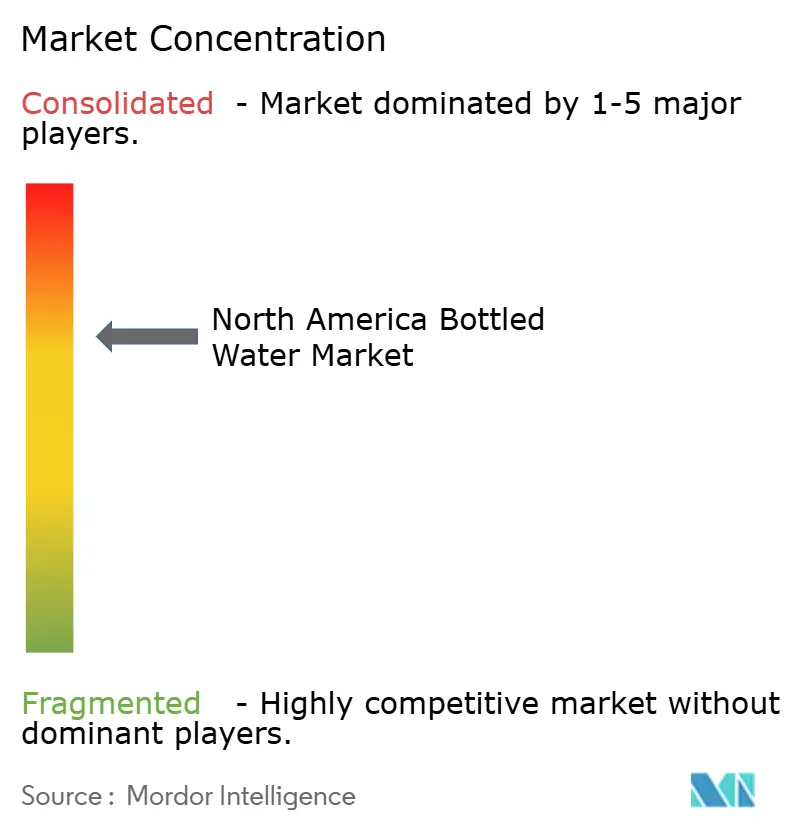

The North American bottled water market is moderately consolidated. Major players in the market include Primo Brands Corporation, The Coca-Cola Company, PepsiCo, Inc., Danone S.A., andNestlé S.A. The market structure continues to evolve through strategic mergers and acquisitions, creating new competitive landscapes. Companies increasingly focus on building comprehensive portfolios that address various consumer preferences and price points. The ongoing vertical integration and geographic expansion enable companies to achieve significant economies of scale while serving diverse market segments.

Companies are shifting their competitive focus beyond traditional factors like price and availability. The industry now emphasizes sustainability initiatives, functional product development, and distribution channel optimization as key differentiators. Technology adoption has become crucial across various operational aspects, including supply chain management and consumer engagement platforms. Companies invest heavily in smart packaging solutions and IoT-enabled distribution tracking systems. Advanced data analytics capabilities are being developed to improve demand forecasting and inventory management.

The market presents significant growth opportunities in functional water segments, which cater to health-conscious consumers. Sustainable packaging solutions continue to gain importance as environmental concerns influence purchasing decisions. Direct-to-consumer channels are emerging as viable alternatives to traditional retail distribution. These new channels enable companies to bypass conventional retail markup structures. The shift toward direct distribution also supports the implementation of premium pricing strategies while maintaining profit margins.

North America Bottled Water Industry Leaders

-

Primo Brands Corporation

-

The Coca-Cola Company

-

PepsiCo, Inc.

-

Danone S.A.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Win Win Water launched a bottled water product with 100% plant-based, fully biodegradable bottles. The bottles, labels, and lids are manufactured using Luminy PLA (Poly Lactic Acid), a sugarcane-derived material produced by TotalEnergies Corbion.

- August 2024: National Beverage Corp. launched a new LaCroix Sparkling Water flavor, Strawberry Peach, which combines strawberry and peach flavors. The beverage features a blend of strawberry and peach tastes.

- August 2024: Flow Beverage Corp introduced a mineral spring sparkling water line in 300 ml aluminum bottles containing 70% recycled aluminum. The product range includes unflavored water and three flavored variants: blackberry-hibiscus, lemon-ginger, and cucumber-mint.

- March 2024: PepsiCo Inc. introduced Bubly Burst, a sparkling water beverage featuring fruit flavors, bright colors, zero added sugar, and minimal calories. Bubly Burst is available in six flavors: Triple Berry, Peach Mango, Watermelon Lime, Pineapple Tangerine, Cherry Lemonade, and Tropical Punch.

North America Bottled Water Market Report Scope

Bottled water is packed drinking water that can be carbonated or not. North America's bottled water market is segmented by type, distribution channel, and geography. Based on type, the market is segmented into still water, sparkling water, and functional water. Based on distribution channels, the market is segmented into on-trade and off-trade distribution channels. The off-trade distribution channel is further sub-segmented into supermarkets/hypermarkets, convenience stores, home and office delivery (HOD), online retail stores, and other off-trade distribution channels. Based on geography, the market is segmented into the United States, Canada, Mexico, and the rest of North America. The report offers market size and forecasts in value (USD million) for the above segments.

By Product Type

| Still Bottled Water |

| Sparkling Bottled Water |

| Functional/Flavored Bottled Water |

By Packaging Format

| PET Bottles |

| Glass Bottles |

| Cans |

By Category

| Mass |

| Premium |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Others Distribution Channel |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Still Bottled Water | |

| Sparkling Bottled Water | ||

| Functional/Flavored Bottled Water | ||

| By Packaging Format | PET Bottles | |

| Glass Bottles | ||

| Cans | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current size of the North America bottled water market?

The market is valued at USD 87.08 billion in 2026 and is expected to reach USD 108.79 billion by 2031.

Who are the key players in North America Bottled Water Market?

Danone S.A., The Coca-Cola Company, Nestle SA, BlueTriton Brands, and Niagara Bottling LLC are the major companies operating in the North America Bottled Water Market.

Which segment is growing the fastest?

Functional and flavored water shows the strongest momentum with a 5.22% CAGR forecast for 2026-2031.

What is the future outlook for the bottled water market in North America?

The market is expected to continue growing at a 4.55% CAGR, driven by health trends, innovation in product offerings, and expansion into new retail channels like e-commerce and subscription services.

Page last updated on: