Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

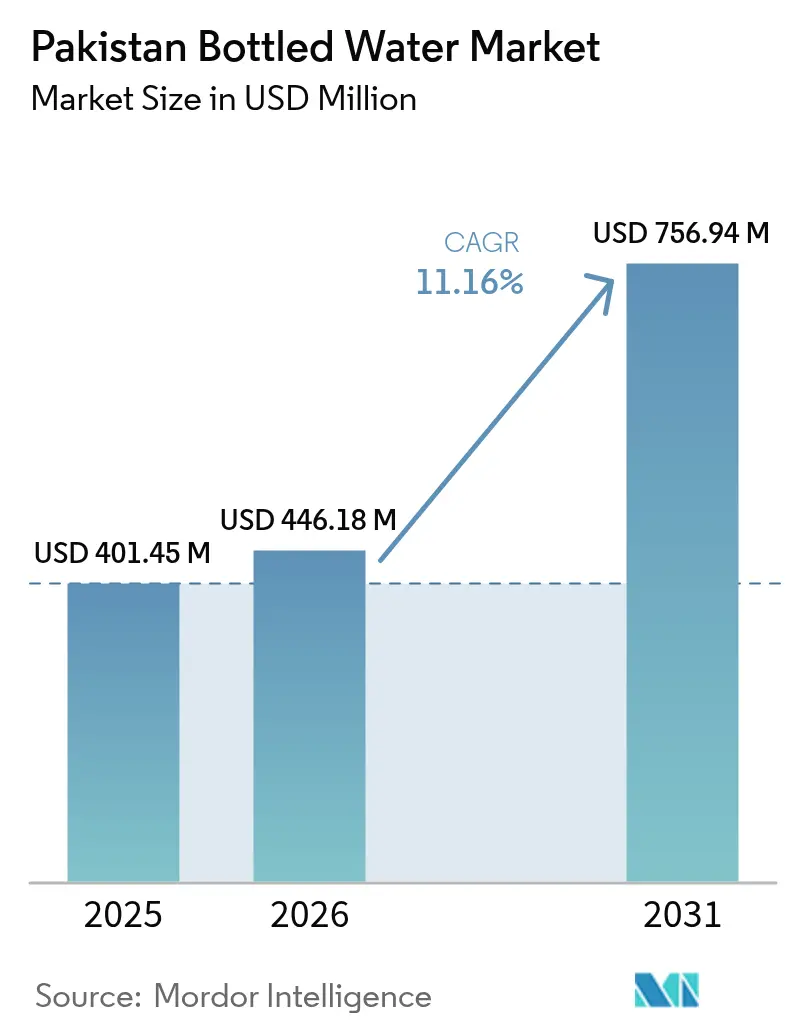

| Base Year Market Size (2025) | USD 401.45 Million |

| Market Size (2026) | USD 446.18 Million |

| Market Size (2031) | USD 756.94 Million |

| Growth Rate (2026 - 2031) | 11.16% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pakistan Bottled Water Market Analysis by Mordor Intelligence

Pakistan bottled water market size in 2026 is estimated at USD 446.18 million, growing from 2025 value of USD 401.45 million with 2031 projections showing USD 756.94 million, growing at 11.16% CAGR over 2026-2031. This expansion reflects mounting health concerns linked to tap-water contamination, rapid urbanization that increases on-the-go consumption, and widening retail access that brings packaged drinking water within reach of ever-larger consumer segments. Multinational and domestic brands now compete head-to-head on quality, price, and sustainability credentials, while regulatory crackdowns on non-compliant producers accelerate market consolidation. Heightened climate volatility, reflected in prolonged droughts and erratic rainfall, further undermines municipal supply reliability and sustains demand for packaged alternatives, particularly in Punjab, Sindh, and the Islamabad Capital Territory. Against this backdrop, premium, sparkling, and functional offerings are carving out fast-growing niches as middle-class buyers trade up for perceived purity, taste, and lifestyle alignment.

Key Report Takeaways

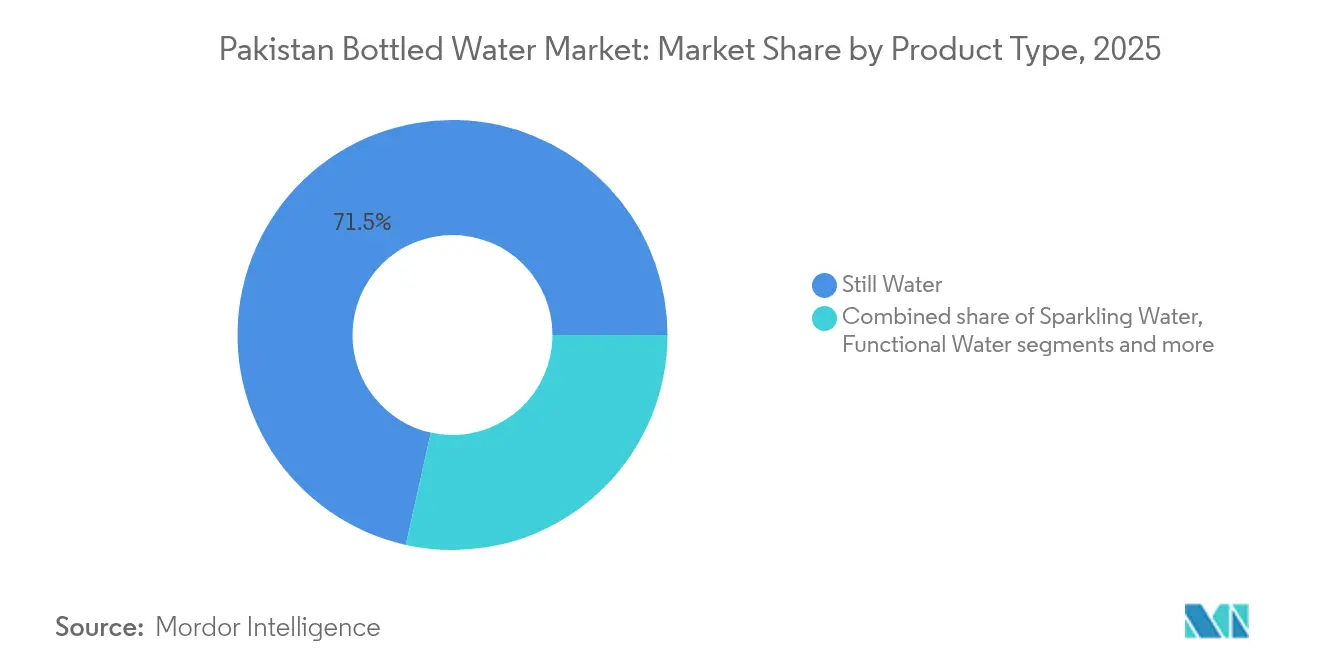

- By product type, still water commanded 71.52% of Pakistan bottled water market share in 2025, while sparkling water is advancing at a 13.62% CAGR through 2031.

- By price point, the mass segment accounted for 83.67% of the Pakistan bottled water market size in 2025; premium products are expected to expand at a 12.98% CAGR out to 2031.

- By packaging, PET bottles held 63.12% of Pakistan bottled water market share in 2025, whereas glass packaging is projected to grow at a 11.96% CAGR during the forecast period.

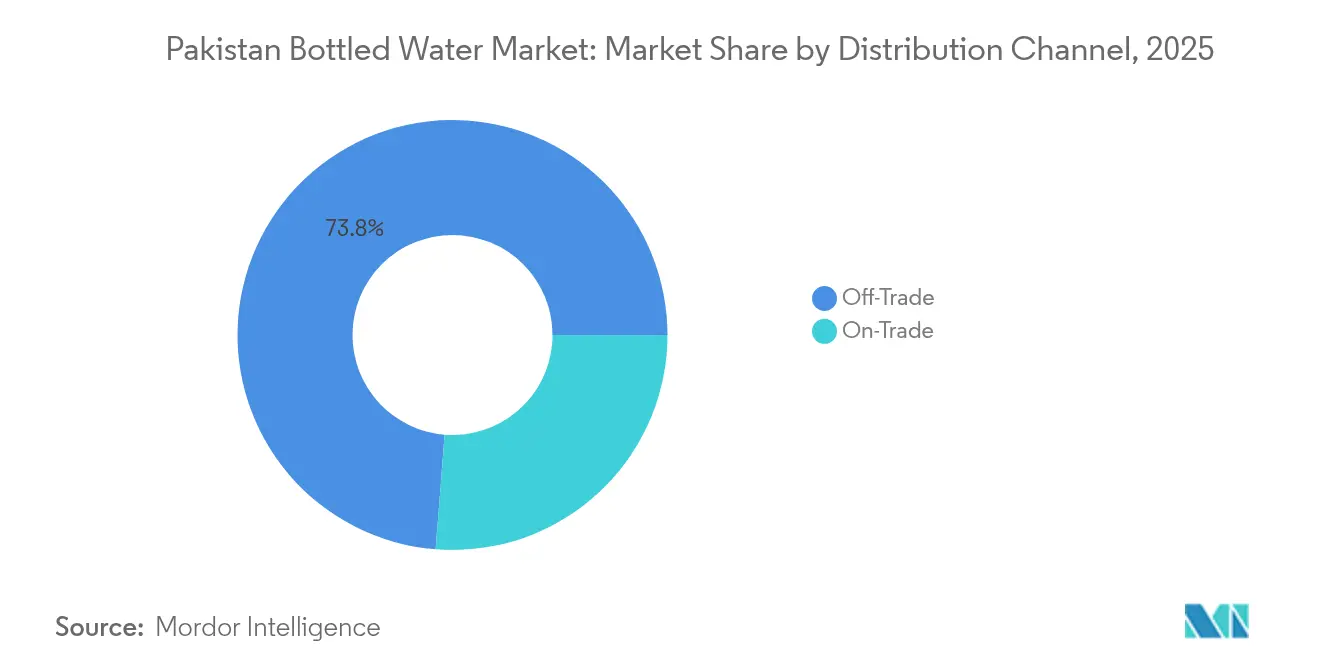

- By distribution, off-trade channels captured 73.75% of Pakistan bottled water market size in 2025, while on-trade recorded a 13.21% CAGR outlook to 2031.

- By geography, Punjab led with 39.88% Pakistan bottled water market share in 2025; Islamabad Capital Territory is forecast to post a 14.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and contamination concerns | +2.8% | National, with acute impact in Punjab and Sindh urban centers | Medium term (2-4 years) |

| Urbanisation-driven on-the-go consumption | +2.1% | Punjab, Sindh, Islamabad Capital Territory | Long term (≥ 4 years) |

| Climate-induced tap-water unreliability | +1.9% | National, with severe impact in Balochistan and Southern Punjab | Short term (≤ 2 years) |

| Expanding retail channels | +1.6% | Punjab, Sindh, Islamabad Capital Territory | Medium term (2-4 years) |

| Concerns over tap water quality | +1.4% | National, particularly urban areas | Short term (≤ 2 years) |

| Government sanitation initiatives | +1.2% | National, with priority focus on rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health and contamination concerns

Health and contamination concerns are on the rise, significantly driving the growth of the Pakistan bottled water market. Increasing awareness about waterborne diseases and the adverse effects of consuming contaminated water has led to a surge in demand for safe and hygienic drinking water. Consumers are increasingly opting for bottled water as a reliable and convenient solution to address these concerns. Additionally, the lack of access to clean and safe drinking water in several regions of Pakistan further amplifies the need for bottled water, making it a critical factor in the market's expansion. The Pakistan Council of Research in Water Resources (PCRWR) recently labeled 28 bottled brands as unsafe due to quality concerns, an action that eliminated fringe players from the market [1]Source: Associated Press of Pakistan, "28 bottle water brands unsafe for consumption: PCRWR's Report", app.com.pk. This regulatory intervention has funneled demand toward certified and trusted labels, as consumers increasingly prioritize safety and quality assurance. Consequently, established players with certified products have gained a competitive edge, further solidifying their position in the market.

Urbanisation-driven on-the-go consumption

Pakistan's urban population is projected to reach 99.4 million by 2030, creating unprecedented demand for portable hydration solutions[2]Source: Asian Development Bank, “PAKISTAN NATIONAL URBAN ASSESSMENT PIVOTING TOWARD SUSTAINABLE URBANIZATION”, adb.org. This urbanization trend significantly drives the bottled water market in Pakistan by increasing the need for convenient, on-the-go consumption options. Urban consumers, who lead increasingly fast-paced lifestyles, actively seek bottled water as a practical and hygienic solution to meet their hydration needs while on the move. USDA's Pakistan Exporter Guide highlights the expansion of modern retail infrastructure, which ensures bottled water is readily available in supermarkets, convenience stores, and on growing e-commerce platforms. The rise of e-commerce platforms, in particular, has made it easier for urban consumers to access bottled water, further supporting the market's growth. Urban consumers actively invest in premium and functional water segments, showing a higher willingness to pay for superior hydration experiences that align with their evolving preferences. This shift toward packaged consumption reflects broader lifestyle changes in Pakistan's rapidly modernizing urban centers, where convenience, quality, and health-conscious choices are becoming increasingly important.

Climate-induced tap-water unreliability

Climate-induced factors are making tap water increasingly unreliable in Pakistan, driving the growth of the country's bottled water market. Changes in weather patterns, such as prolonged droughts and erratic rainfall, have taken a toll on both the availability and quality of water in Pakistan. In 2023, the International Water Management Institute (IWMI) reported that mild drought conditions impacted over 80% of the nation [3]Source: International Water Management Institute, “Pakistan looks beyond drought with innovation turning crisis into hope”, iwmi.org. These droughts further strained Pakistan's already fragile water infrastructure, causing frequent disruptions in the tap water supply. Compounding the issue, rising temperatures and melting glaciers have intensified water scarcity, rendering tap water less dependable for daily needs. The combination of these factors has led to a growing perception among consumers that tap water is unsafe and unreliable. Consequently, consumers are turning to bottled water as a safer, more reliable alternative for drinking and other essential uses, such as cooking and hygiene. This shift in consumer behavior is significantly contributing to the expansion of the bottled water market in the country.

Government sanitation initiatives

Government-led sanitation initiatives play a crucial role in driving the growth of the Pakistan bottled water market. These programs aim to improve access to clean drinking water and promote public health by addressing water contamination issues. As part of these initiatives, the government has been actively investing in infrastructure development, such as water treatment plants and distribution networks, to ensure the availability of safe drinking water. Additionally, the National Drinking Water Policy earmarks infrastructure upgrades and rural filtration plants, gradually expanding awareness of potable standards across demographics. Complementary campaigns by provincial food authorities further drive household education, reinforcing bottled water as the immediate solution pending public-pipeline remediation. Awareness campaigns highlighting the importance of clean water and hygiene have also encouraged consumers to opt for bottled water as a reliable and convenient solution. These efforts not only enhance consumer trust in bottled water but also create opportunities for market players to expand their reach and cater to the growing demand for safe drinking water in Pakistan.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating packaging/raw material costs | -1.8% | National, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Environmental concerns about plastic waste | -1.5% | National, with regulatory pressure in Punjab and Sindh | Medium term (2-4 years) |

| Quality consistency challenges | -1.2% | National, particularly affecting smaller producers | Short term (≤ 2 years) |

| Intense brand competition hindering market growth | -0.9% | Punjab, Sindh, Islamabad Capital Territory | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating packaging/raw material costs

Rising and falling costs of packaging and raw materials significantly impact the Pakistan Bottled Water Market. These fluctuations create challenges for manufacturers in maintaining consistent production costs and pricing strategies. The volatility in raw material prices, such as plastic resins used for bottle manufacturing, directly affects the overall cost structure. Additionally, packaging materials, which are crucial for product safety and branding, often experience price variations due to changes in supply chain dynamics, import duties, and global market trends. Such unpredictability can hinder profit margins and force companies to either absorb the costs or pass them on to consumers, potentially affecting demand. Furthermore, the dependency on imported raw materials exposes the market to currency exchange rate fluctuations, further exacerbating cost instability. Manufacturers also face challenges in securing a steady supply of high-quality materials, as disruptions in the global supply chain can lead to shortages and increased prices. These factors collectively create a complex environment for bottled water producers, making it difficult to maintain competitive pricing while ensuring profitability.

Environmental concerns about plastic waste

Plastic waste has become a significant environmental restraint in the market. The increasing accumulation of plastic waste, primarily from single-use plastic bottles, poses severe challenges to waste management systems. Improper disposal and lack of recycling infrastructure exacerbate the issue, leading to pollution of land and water bodies. Additionally, growing awareness among consumers about the environmental impact of plastic waste has led to a shift in preferences toward sustainable and eco-friendly alternatives. This trend is pressuring bottled water manufacturers to adopt sustainable packaging solutions, which may increase production costs and impact profit margins. The regulatory environment is also tightening, with governments and environmental organizations advocating for stricter policies to reduce plastic waste, further challenging the market's growth potential. Moreover, the long-term environmental consequences of plastic waste, such as its contribution to microplastic pollution and harm to marine ecosystems, are intensifying public scrutiny. These factors collectively create a complex scenario for the bottled water market in Pakistan, where balancing consumer demand, environmental responsibility, and regulatory compliance remains a critical challenge for industry players. The need for innovative solutions, such as biodegradable packaging and improved recycling mechanisms, is becoming increasingly urgent to address these environmental concerns effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Water Dominance Faces Sparkling Disruption

In 2025, still water dominates the Pakistan bottled water market, commanding a substantial 71.52% share. This large market presence highlights the strong preference of Pakistani consumers for basic hydration solutions. The widespread concerns over tap water contamination have significantly boosted reliance on still bottled water as a safer and more accessible alternative. Consumers prioritize purity and safety, which reinforces the demand for still water across urban and rural regions alike. Additionally, the affordability and availability of still water further contribute to its leading position in the market. Overall, still water remains the most trusted option for hydration amidst ongoing public health awareness.

On the other hand, sparkling water represents the fastest-growing segment in the Pakistan bottled water market, projected to achieve a robust 13.62% compound annual growth rate (CAGR) through 2031. This rapid growth is largely driven by increasing urbanization, which exposes consumers to modern lifestyles and new beverage choices. Younger demographics, in particular, are gravitating toward sparkling water due to its refreshing taste and perceived lifestyle appeal. The rising influence of health-conscious trends and premiumization also fuels the demand for sparkling water. Moreover, improvements in distribution channels and marketing efforts are helping this segment gain traction. As a result, sparkling water is poised to become a significant player in Pakistan’s evolving bottled water landscape over the coming years.

By Price Point: Mass Market Foundation Enables Premium Growth

In 2025, the mass price segment holds a commanding 83.67% share of the Pakistan bottled water market, underscoring the price sensitivity of Pakistani consumers. Affordability remains a critical factor driving purchasing decisions, especially given the economic challenges faced by many households. This segment’s dominance reflects the widespread demand for budget-friendly hydration options accessible to a large portion of the population. Consumers in this category prioritize cost-effectiveness without compromising basic quality and safety standards. Availability of mass-priced bottled water in various retail outlets further supports its extensive market penetration. Overall, the mass price segment serves as the backbone of the bottled water industry in Pakistan, catering to the essential hydration needs of the majority.

Conversely, the premium segment is the fastest-growing sector in the Pakistan bottled water market, projected to grow at a robust 12.98% CAGR through 2031. This growth signals a shifting consumer landscape where a notable segment of the population is increasingly willing to invest in higher quality products. Factors such as superior water purity, aesthetically appealing packaging, and trusted brand reputation drive the appeal of premium bottled water. Rising disposable incomes and greater health awareness among urban consumers contribute to this upward trend. Additionally, marketing efforts highlighting the benefits of premium water reinforce consumer confidence and desire for elevated experiences. As a result, the premium segment is set to gain significant momentum alongside evolving consumer preferences in the coming years.

By Packaging Type: PET Dominance Challenged by Sustainability Concerns

In 2025, PET bottles hold a dominant position in the Pakistan bottled water market, capturing a significant 63.12% market share. This widespread adoption is largely due to the cost efficiency of PET packaging, making it a preferred choice for manufacturers aiming to offer affordable products. Its lightweight nature enhances convenience for both producers and consumers, facilitating easier transportation and handling. Additionally, the well-established supply chains supporting PET bottle production contribute to their extensive availability across the country. The durability and versatility of PET bottles further reinforce their market leadership. Overall, PET bottles remain the preferred packaging format in Pakistan, successfully balancing affordability with practical benefits.

In contrast, glass bottles represent the fastest-growing packaging segment in the Pakistan bottled water market, expected to achieve a 11.96% CAGR through 2031. This growth is driven by a rising consumer demand for premium and environmentally sustainable packaging options. Glass bottles are perceived as a more upscale choice, often associated with higher quality and a better drinking experience, which appeals to a niche but expanding audience. Increasing environmental awareness among consumers encourages preference for recyclable and reusable materials like glass. Furthermore, improvements in packaging design and branding efforts enhance the attractiveness of glass bottles. As a result, glass packaging is poised to gain significant traction in Pakistan’s bottled water market, reflecting shifting consumer values and sustainability trends.

By Distribution Channel: Off-Trade Dominance Meets On-Trade Acceleration

In 2025, off-trade channels dominate the Pakistan bottled water market with a substantial 73.75% market share. This segment collectively provide wide-ranging and convenient access to bottled water across urban and semi-urban areas. The extensive presence of these retail outlets ensures that consumers can easily purchase bottled water as part of their everyday shopping habits. The convenience, variety, and competitive pricing offered by off-trade channels appeal to a broad base of customers. Moreover, the growth of e-commerce platforms in Pakistan further strengthens the distribution and accessibility of bottled water through off-trade channels. As a result, this segment remains the backbone of bottled water sales in the country, catering to diverse consumer needs with unparalleled reach and availability.

In contrast, on-trade segments are the fastest-growing channel in the Pakistan bottled water market, expected to achieve a robust 13.21% CAGR through 2031. This rapid expansion is fueled by the growth of the hospitality, corporate, and food service sectors, all of which emphasize the importance of safe and reliable bottled water supplies for their customers and operations. Increasing consumer expectations for hygiene and quality in restaurants, hotels, and offices have heightened demand within on-trade channels. Additionally, the rise in corporate events, conferences, and institutional catering further contributes to this upward trajectory. Enhanced focus on operational continuity and customer safety drives investment in dependable water sourcing under on-trade distribution. Consequently, the on-trade segment is projected to gain significant momentum in the coming years, reflecting broader economic and lifestyle developments in Pakistan.

Geography Analysis

In 2025, Punjab commands a 39.88% market share, a testament to its dense population and pressing water quality issues. Major urban centers in Punjab grapple with drinking water samples frequently surpassing contamination thresholds. Punjab's blend of a robust industrial base and an agricultural economy fuels varied consumption patterns, catering to both urban households and rural agricultural workers. Recent enforcement actions by the Punjab Food Authority against prominent brands such as Aquafina, Kinley, and Springley have shifted the competitive landscape, paving the way for both local and international brands that adhere to regulations.

Sindh, home to Pakistan's commercial epicenter in Karachi, grapples with significant municipal water quality challenges. These issues have spurred a widespread shift towards bottled water across various income brackets. Sindh boasts well-established distribution networks and a consumer base with purchasing power. However, infrastructure limitations hinder consistent access to reliable tap water. Meanwhile, Khyber Pakhtunkhwa, despite having relatively better natural water resources, faces mounting urbanization pressures. As cities like Peshawar grow, they present burgeoning market opportunities.

Islamabad Capital Territory is on track for a 14.01% CAGR growth through 2031, driven by factors like high per capita income and a significant government sector employment. The territory's small size and wealthy population make it a prime spot for premium brand placements and cutting-edge distribution strategies. As Pakistan's political nucleus, Islamabad sets consumption trends that ripple across the national market. The city's international diplomatic community and corporate headquarters bolster the on-trade segment, while residential zones facing dwindling groundwater supplies maintain a steady demand for household consumption.

Regulatory Landscape

Bottled water in Pakistan is regulated as a food product, with mandatory product standards set and enforced by the Pakistan Standards and Quality Control Authority (PSQCA) under the Ministry of Science and Technology. For bottled drinking water, PSQCA specifies physical, chemical, and microbiological limits under PS:4639-2018, including annual type testing requirements for heavy metals and other contaminants. Compliance with these parameters underpins licensing and ongoing market access.

Regulatory oversight is complemented by the Pakistan Council of Research in Water Resources (PCRWR), which conducts quarterly monitoring of bottled water brands across multiple cities and publicly discloses results, increasing the commercial risk of non-compliance. In May 2026, the Federal Board of Revenue (FBR) issued a sales-tax directive requiring bottled water manufacturers to install electronic production monitoring systems by June 15, 2026 (including scanners, sensors, industrial PCs, and IP cameras through FBR-authorized vendors), tightening tax compliance and increasing formalization pressure on smaller producers.

Value Chain Analysis

The value chain starts with water sourcing (groundwater and other approved sources), followed by treatment (filtration, reverse osmosis, UV/ozonation), and then in-house and third-party testing aligned to PSQCA requirements (PS:4639 for bottled drinking water and PS:2102 for natural mineral water). After testing, producers move to bottling and secondary packaging. Key inputs include PET resin and preforms, caps, labels, cartons, and shrink films, while cost volatility is amplified by reliance on imported materials and currency movements, which tends to pressure pricing for mass-priced SKUs that account for the majority of volume.

Downstream, producers depend on national FMCG distribution, modern trade and convenience retail, e-commerce, and Home and Office Delivery (HOD) for larger formats. HOD economics add reverse-logistics costs (returnable jars, route density, and last-mile delivery), which makes localized production and depot networks more important to limit transport expenses. The sector also operates alongside neighborhood filtration plants as a parallel hydration option, while rising scrutiny of groundwater extraction in water-stressed areas, notably Punjab and Sindh, increases the importance of water stewardship practices and transparent quality controls.

Competitive Landscape

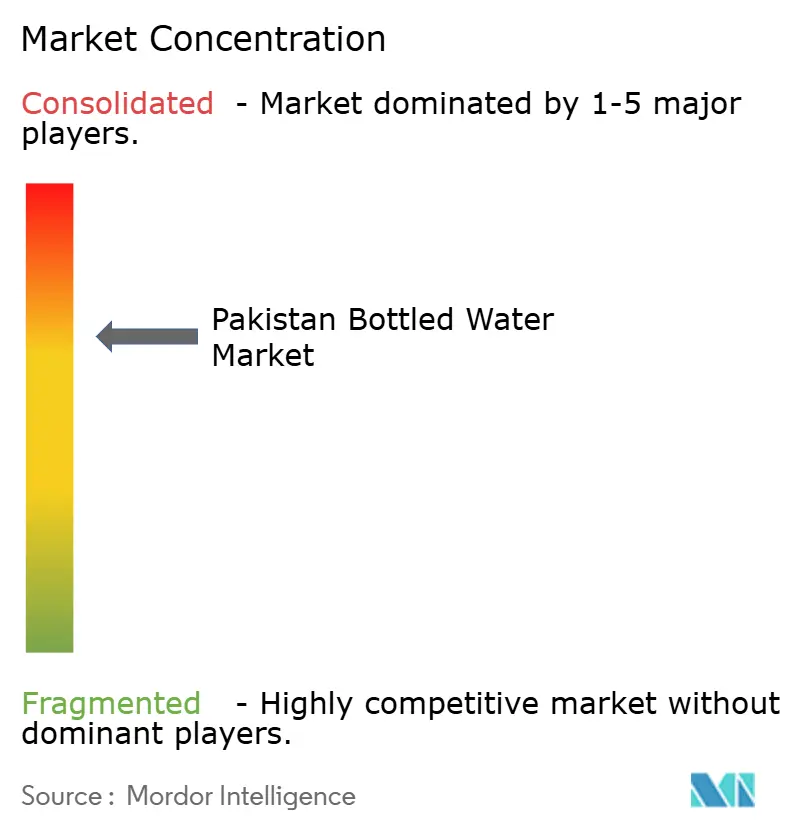

The competitive landscape of Pakistan's bottled water market is consolidated, indicating intense rivalry. Established international brands compete directly with emerging local players, who are leveraging shifting consumer preferences to gain traction. The market dynamics have undergone significant changes, particularly following the impact of the BDS movement on international brands. This shift has created strategic opportunities for domestic manufacturers to capture market share that was previously dominated by global giants, thereby intensifying competition further.

Technology adoption has emerged as a critical factor for maintaining a competitive edge in this market. Leading players are heavily investing in advanced water treatment technologies, automated bottling lines, and digital distribution platforms. These investments are aimed at ensuring consistent product quality and enhancing operational efficiency, which are essential for sustaining market positions in a highly competitive environment. The focus on technological advancements highlights the industry's drive toward innovation and efficiency to meet evolving consumer demands.

Nestlé's investment in water plants exemplifies how established players are utilizing technology and capital to strengthen their market presence. Such investments not only demonstrate the importance of technological integration but also underline the financial commitment required to maintain a competitive advantage. As the market continues to evolve, both international and domestic players are expected to intensify their efforts to capture a larger share, making the competitive landscape increasingly dynamic.

Pakistan Bottled Water Industry Leaders

-

The Coca-Cola Company

-

Masafi LLC

-

Qarshi Industries (Pvt.) Ltd.

-

PepsiCo, Inc

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public disclosure of quality outcomes through PCRWR quarterly monitoring, combined with PSQCA mandatory standards, creates room for brands that can demonstrate repeatable compliance through stronger lab capability, digital QA records, and more consistent plant governance. Provincial enforcement further differentiates market access, including Punjab Food Authority (PFA) laboratory testing and Certificate of Product Registration (CPR) requirements for food items, which can favor organized players with established regulatory affairs and traceable supplier documentation.

Technology-led water management and compliance infrastructure is also becoming more visible across the wider water ecosystem, with direct relevance to bottled water operational upgrades. A recent example is the October 2025 Cyclon Tech MoU (about RMB 5 billion) with Shaanxi Water Development and Construction Group to develop smart water management and infrastructure projects in Pakistan, supporting a pipeline of automation and monitoring solutions that can be adapted for plant controls and resource efficiency. On the packaging side, environmental pressure around single-use plastics creates pull for refill-led models (HOD) and more recyclable formats, while the FBR production monitoring requirement encourages investment in line-level data capture that can improve traceability and inventory discipline across off-trade and on-trade channels.

Recent Industry Developments

- May 2026: Pakistan's Federal Board of Revenue (FBR) directed bottled water manufacturers to install electronic production monitoring systems by June 15, 2026, enabling real-time oversight of production for sales-tax compliance. The required setup includes industrial barcode scanners, counting sensors, industrial PCs, and IP cameras through FBR-authorized vendors. This change increases compliance capex and strengthens formal-sector enforcement, raising the operating bar for smaller and informal producers.

- March 2026: Nestle Waters & Premium Beverages reported that Nestle Pakistan achieved 100% Alliance for Water Stewardship (AWS) certification across its bottling sites, including Sheikhupura, Islamabad, Karachi, and the Kabirwala factory. The milestone supports a higher standard of site-level water governance and stewardship practices. For the bottled water category, it elevates competitive benchmarks around audited sustainability claims in water-stressed regions.

- March 2024: The Coca-Cola Company launched watershed stewardship initiatives in Pakistan's Ravi River basin with WWF-Pakistan, including rainwater harvesting, recharge wells, and floating treatment wetlands. The program targeted water-scarcity and quality issues affecting communities around Lahore. It reinforced water stewardship as a strategic plank for beverage companies operating amid rising scrutiny of water use and local resource stress.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Pakistan bottled water market covers packaged drinking water sold in bottles in Pakistan, across still and other bottled formats, and measured in value terms in USD.

Scope exclusions: Bulk water supplied through tankers, tap or municipal water services, and in-home filtration devices are excluded from this market.

Segmentation Overview

-

By Product Type

- Still Water

- Sparkling Water

- Functional Water

- Flavoured Water

-

By Price Point

- Mass

- Premium

-

By Packaging Type

- PET Bottles

- Glass Bottles

- Others

-

By Distribution Channel

- On Trade

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Home and Office Delivery (HOD)

- Other Distribution Channels

-

By Geography

- Punjab

- Sindh

- Khyber Pakhtunkhwa

- Balochistan

- Islamabad Capital Territory

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the full packaged drinking water chain in Pakistan, from bottling and packaging inputs through retail and foodservice sale points. We use public sources such as Pakistan Bureau of Statistics releases, Pakistan Customs trade statistics, State Bank of Pakistan publications, and food safety and standards notifications (including provincial regulators) to understand formal activity, pricing signals, and compliance changes.

To make the inputs usable for sizing, company annual reports, press releases, and investor presentations are reviewed for capacity additions, plant footprints, and channel focus. We also refer to a paid subscription for company financials and intelligence, plus a shipment level import-export database when trade flows help explain packaging resin, caps, or other material movement linked to bottled water output. The desk sources mentioned here are illustrative, and we checked additional public documents to fill gaps, validate assumptions, and clarify unclear points.

Primary Interviews and Surveys

Primary work focuses on verifying what drives value in Pakistan bottled water, where pricing moves fastest, and how sales mix shifts across off-trade, on-trade, and home and office delivery. We speak with bottlers, packaging and distribution partners, modern trade contacts, and industry practitioners across major provinces so secondary data can be adjusted for local route-to-market realities and informal spillovers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 19% | APAC: 41% |

| Mid tier: 53% | Functional/Unit leaders: 21% | EMEA: 33% |

| Smaller Players: 20% | Managers: 60% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where packaged drinking water demand is reconstructed from consumption cues and channel throughput, and then filtered through pack mix and price points to land at value. In practice, the model is tied to variables such as urban population and household purchasing patterns, retail and foodservice channel expansion, the share of sales moving through home and office delivery, typical pack sizes, and observed price ladders between mass and premium products.

To keep the totals realistic, we cross-check the output with selective bottom-up approximations, such as sampling average selling prices by pack type and multiplying them by plausible volume bands, followed by supplier and distributor checks on where volumes concentrate. Where direct inputs are thin, gaps are handled using peer city comparisons inside Pakistan and conservative smoothing across adjacent years, and then re-tested with interview feedback.

Forecasts are produced using scenario analysis anchored on expected inflation and income pressure, likely regulation and enforcement intensity, and how quickly modern trade and delivery routes scale. The assumptions are reviewed with primary respondents so the final growth path does not depend on a single indicator.

Data Validation & Update Cycle

Validation is done in steps so that a single data point does not over-influence the result. Analysts compare the modeled totals against independent signals, such as observed retail price bands, packaging mix movement, and reported capacity additions, and then investigate any large variance before numbers are finalized.

A second analyst review is used to stress test calculations, and follow-up outreach is triggered when a key assumption changes or when a province-level trend looks inconsistent with channel feedback. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest view available at the time of release.

Mordor Intelligence's Pakistan Bottled Water Market Sizing Compared With Other Published Estimates

It is common to see different market values for Pakistan bottled water because sources do not always count the same products, the same channels, or the same price basis for conversion to USD. Differences also come from whether the study leans more on formal reporting, or whether it tries to include informal distribution with broader assumptions.

Bulk tanker water and refill jar delivery are outside Mordor Intelligence's scope, which removes a large adjacent spend bucket that some publishers roll into bottled water when they use a wider packaged water definition.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 401.45 M (2025) | |

| Global Consultancy A | USD 1.82 B (2024) | Uses a broader packaged water framing and a different base year, which can pull in refill and bulk-like spending and inflate value when converted at a single-year USD rate. |

| Industry Publisher B | USD 327.61 M (2025) | Appears to rely more on narrower formal channel capture and a smaller demand pool, which can understate home and office delivery and premium price tiers if these are lightly sampled. |

The spread across published numbers is mainly explained by what is counted as bottled water and how channel mix is treated in the value build. By keeping inputs tied to pack types, price points, and channel split checks that can be repeated, the estimate stays transparent and easier to update when market conditions change.

Key Questions Answered in the Report

What is the current value of Pakistan’s bottled water market?

The Pakistan bottled water market size is USD 446.18 million in 2026.

How fast is the market expected to grow?

The sector is projected to post an 11.16% CAGR, lifting value to USD 756.94 million by 2031.

Which region shows the strongest growth momentum?

Islamabad Capital Territory leads with a forecast 14.01% CAGR through 2031.

How significant are premium products?

Premium water still represents a minority share but is forecast to grow at 12.98% CAGR, outpacing mass-priced offerings.

What packaging trends are emerging?

Glass bottles are gaining popularity at a 11.96% CAGR as consumers and regulators push for eco-friendly formats.

Page last updated on: