Rose Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

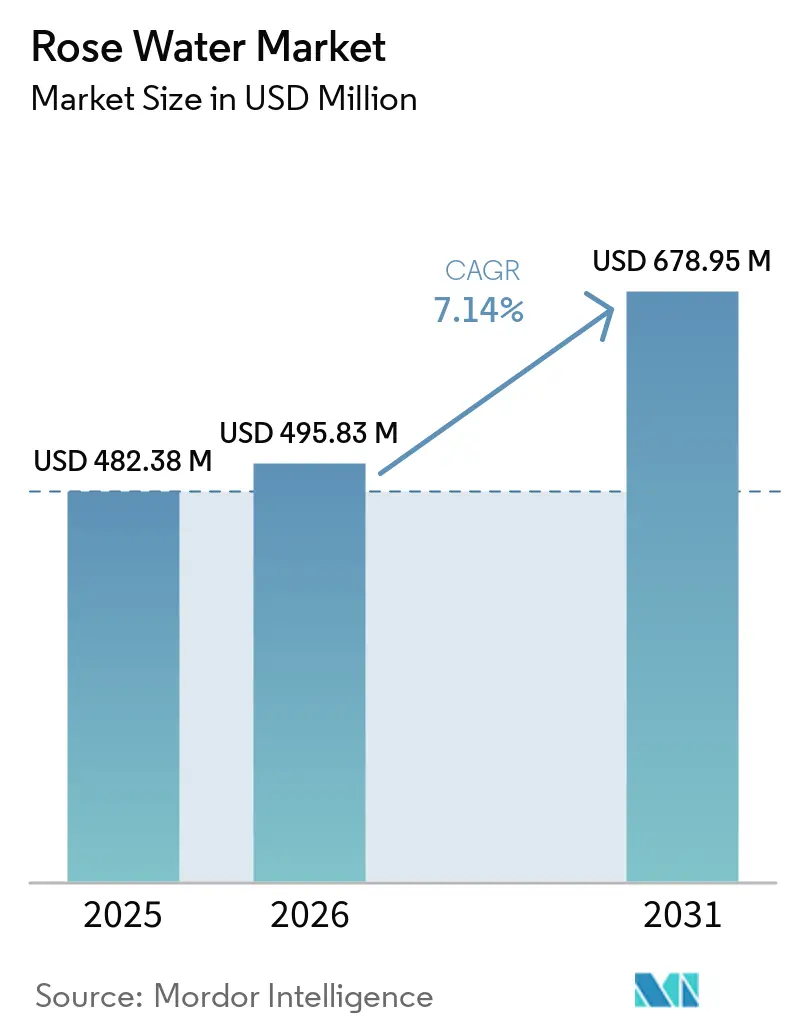

| Market Size (2026) | USD 495.83 Million |

| Market Size (2031) | USD 678.95 Million |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rose Water Market Analysis by Mordor Intelligence

The rose water market size is projected to expand from USD 482.38 million in 2025 and USD 495.83 million in 2026 to USD 678.95 million by 2031, registering a CAGR of 7.14% between 2026 and 2031. Growth is being supported by a wider move away from synthetic fragrance and preservative systems toward steam-distilled botanical hydrosols in personal care formulas. The ingredient is also gaining broader use in food and beverage products, where producers value both its flavor profile and its antimicrobial properties in premium applications. This broader use is changing procurement priorities because buyers increasingly need dependable origin, stable quality, and traceable supply at the same time. Premium feedstock pressure, especially in Bulgarian Damascena supply, is widening the gap between certified and non-certified product tiers and is supporting firmer pricing for traceable suppliers. Competition remains spread across regional distillers, Ayurvedic brands, European organic players, and digital-first labels, which leaves room for differentiated positioning in certification, sourcing, and channel strategy.

Key Report Takeaways

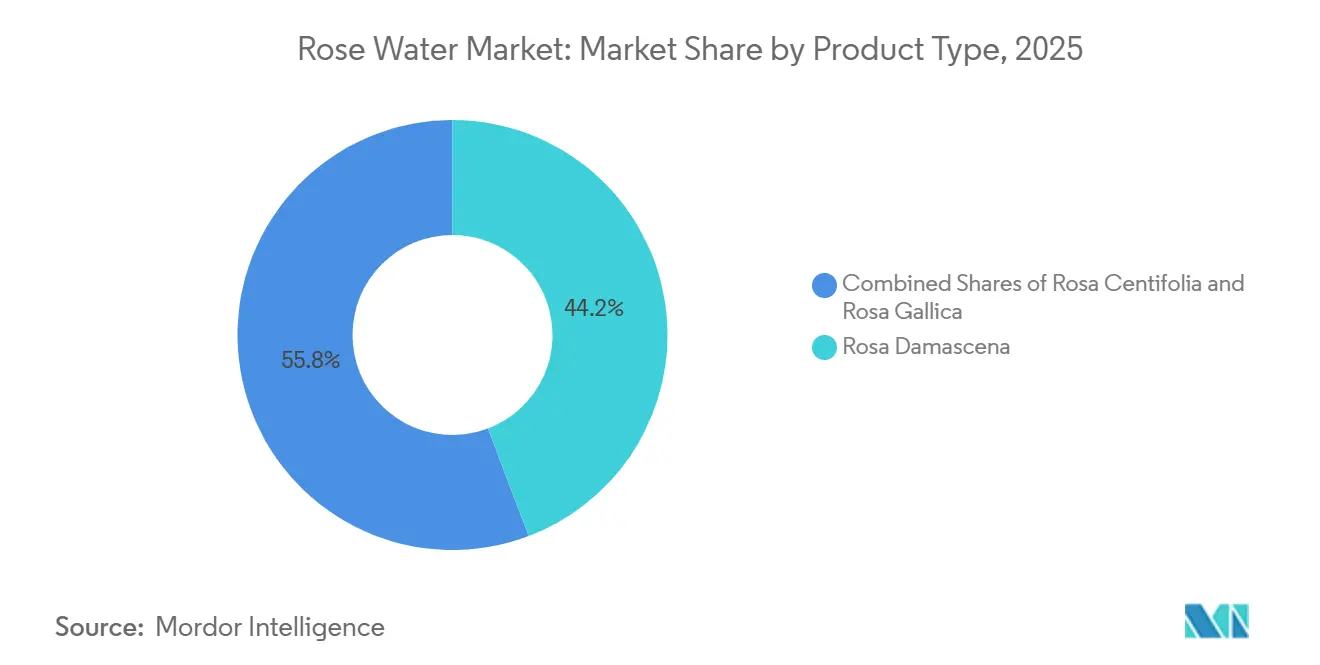

- By product type, Rosa Damascena led with a 44.23% share in 2025, while Rosa Gallica is forecast to expand at an 8.62% CAGR through 2031.

- By nature, conventional rose water held a 65.48% share in 2025, while organic rose water is projected to grow at an 8.55% CAGR through 2031.

- By end use, cosmetics and personal care accounted for a 54.78% share in 2025, while food and beverages are advancing at an 8.32% CAGR through 2031.

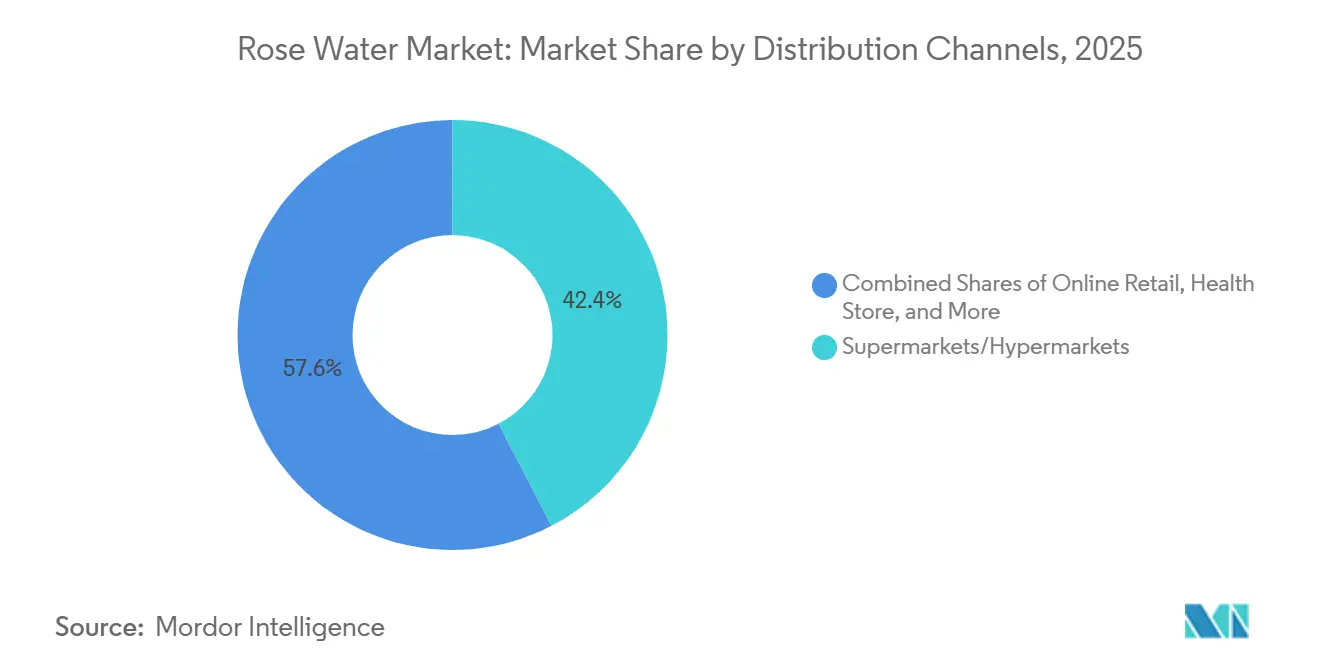

- By distribution channel, supermarkets and hypermarkets held a 42.38% share in 2025, while online retail is forecast to grow at a 9.02% CAGR through 2031.

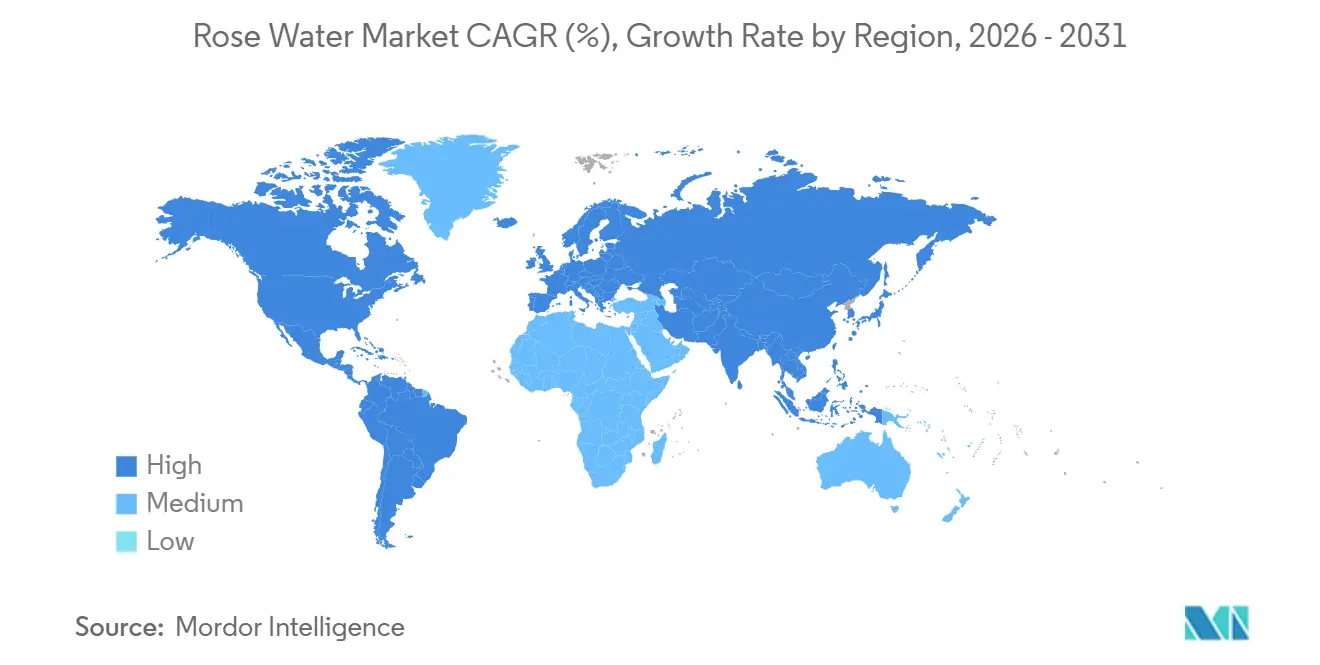

- By geography, Europe accounted for a 34.28% share in 2025, while Asia-Pacific is projected to expand at an 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rose Water Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural and Organic Skincare Products | +1.8% | Global, concentrated in North America, Europe, and APAC core | Medium term (2-4 years) |

| Growth of the Clean Beauty Movement | +1.2% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Expanding Personal Care and Cosmetics Industry | +1.5% | Global, APAC core with early gains in China, India, Vietnam | Long term (≥ 4 years) |

| Increasing Popularity of Ayurveda and Herbal Wellness Products | +0.8% | APAC core, especially India, with spill-over to MEA and North America | Medium term (2-4 years) |

| Rising Consumer Awareness of Skin-Soothing Benefits | +0.6% | Global, strongest in Europe and APAC | Short term (≤ 2 years) |

| Product Innovation and Multifunctional Applications | +0.9% | Global, with early-adoption gains in South Korea and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural and Organic Skincare Products

Natural ingredient preference has moved well beyond a niche and now shapes mainstream skincare assortment decisions across the rose water market. Rose water fits this shift because it is widely used in toners, facial mists, and cleansing waters without the synthetic positioning many shoppers now avoid. The premium end of the category is also becoming more selective about origin documentation and third-party organic status, especially in Europe and coastal North America. In Europe, tighter product compliance expectations reinforce deeper scrutiny of ingredient records and finished formula responsibility[1]Source: European Commission, “EU Cosmetics Regulation (EC) No 1223/2009,” European Commission, europa.eu. That screening narrows the pool of eligible suppliers and makes certified production more valuable in retailer and brand negotiations. As a result, the rose water market is seeing a clearer divide between bulk commodity supply and premium supply that can support trust-based claims.

Growth of the Clean Beauty Movement

The clean beauty shift is increasing the value of ingredients that support simple formulas and clear labeling in the rose water market. Pure steam-distilled rose hydrosol fits that requirement because it can combine fragrance, toning, and soothing performance in a single input[2]Source: Liu et al., “Phytochemicals and Bioactive Functional Ingredients from Rosa Damascena: From Extraction to Application in the Food and Healthcare Sectors,” National Library of Medicine, ncbi.nlm.nih.gov. Brands reformulating away from alcohol-heavy toners and synthetic fragrance systems are using rose water as a direct substitute in many mid-premium skincare lines. This is more visible where ingredient review standards and compliance expectations are stricter, because compliant botanical inputs have a clearer route to shelf placement. The substitution effect also reduces the room for synthetic alternatives in products that depend on transparent labeling. The result is a stronger demand for distilled material with documented purity rather than reconstituted blends that cannot support the same positioning.

Expanding Personal Care and Cosmetics Industry

The expanding personal care base in Asia-Pacific is giving the rose water market a broader volume platform across skincare, mist, cleansing, and hybrid formats. Growth is not uniform, because mass products often rely on lower-cost rose-scented blends while premium brands need certified distilled inputs to support natural and clean claims. That split is creating two procurement pools inside the same demand cycle, one led by cost and one led by provenance. Suppliers with certification and traceability systems are better placed to win higher-margin formulation contracts as consumer scrutiny deepens. The difference matters because brands are now expected to defend ingredient credibility as clearly as they defend product performance. This pattern supports steady volume growth, but it also raises the commercial value of quality assurance across the rose water market.

Product Innovation and Multifunctional Applications

Product development is widening the functional role of rose water beyond its traditional use as a toner or fragrance carrier. Research on Rosa damascena identified more than 200 bioactive compounds, while citronellol and geraniol make up large parts of the aromatic fraction. The same research reported antioxidant activity and antimicrobial effectiveness against food-borne pathogens, which supports use in both skincare and food applications. Encapsulation systems such as nanoliposomes, lignin nanoparticles, and whey-protein-pectin complexes are also improving stability and supporting integration into serum-toner hybrids. This changes the role of rose water from a sensory ingredient to a more functional formulation input. That shift is expanding the addressable use base for the rose water market in higher-value products where performance claims carry stronger pricing support.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Quality Rose Raw Materials | -1.2% | Bulgaria, Turkey, and the global premium supply chain | Short term (≤ 2 years) |

| Competition from Synthetic Floral Waters and Fragrances | -0.9% | Global, most acute in APAC economy tier and South America | Medium term (2-4 years) |

| Quality Variability Across Manufacturers | -0.6% | Global, most acute in emerging-market supply bases | Medium term (2-4 years) |

| Regulatory and Certification Challenges | -0.5% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Quality Rose Raw Materials

Premium rose raw material availability has tightened and is now a direct constraint on the rose water market. Bulgaria's Rose Valley recorded its weakest harvest in more than 30 years in 2025, with output falling by 50% and 30% to 40% of established plantations abandoned under climate pressure and weak economics. That matters because Bulgarian Damascena hydrosol still carries one of the strongest heritage and quality associations in premium beauty procurement. When that supply base contracts, input costs rise and certified buyers have fewer options that match their origin requirements. The practical response is wider sourcing interest in Turkey, Iran, and India, but those origins do not carry the same heritage premium in every contract. This keeps supply diversification active, yet it does not fully remove the pressure on premium pricing within the rose water market.

Competition from Synthetic Floral Waters and Fragrances

Synthetic odorants and reconstituted floral waters continue to pressure pricing in the mass end of the rose water market. These alternatives allow brands to sell rose-scented products at price points that pure hydrosol producers cannot easily match without margin loss. Retail labeling also does not always separate genuine steam-distilled rose water from water-based blends with added fragrance, which weakens product differentiation at the point of purchase. Adulteration and authenticity concerns have remained visible across rose-derived inputs, reinforcing the need for stronger verification and category clarity[3]Source: American Botanical Council, “Rose Oil Adulteration Bulletin,” HerbalGram, herbalgram.org. This quality-signal gap increases the education burden for premium brands that depend on provenance and purity. Until clearer labeling and more consistent certification enforcement spread further, synthetic substitutes will continue to cap upside in price-sensitive channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rosa Damascena Leads Volume While Rosa Gallica Gains Strategic Relevance

Rosa Damascena held 44.23% of the rose water market share in 2025, which gave it the leading position within the product type mix. Its lead rests on a well-recognized aromatic and bioactive profile, along with the heritage premium attached to Bulgarian and Turkish distillation traditions. That combination makes Damascena the reference product for premium formulations across the rose water market, especially where the ingredient story matters to brand positioning. It also remains the most familiar variety for buyers who want broad acceptance across cosmetics, personal care, and culinary applications. This established position gives Damascena a strong base, but it also ties a large part of premium supply to a narrower group of producing regions.

That concentration is why Rosa Gallica is forecast to expand at an 8.62% CAGR through 2031, making it the fastest-growing product type in the rose water market size outlook. It's better cold-hardiness improves its strategic value as climate shifts change cultivation patterns in Europe and other temperate areas. The rose water market is therefore beginning to treat Gallica not only as an alternative botanical source, but also as a practical hedge against future feedstock instability. Jurlique's 2025 introduction of the Intense Rose, a proprietary Rosa Gallica hybrid grown on its biodynamic farm in South Australia's Adelaide Hills, shows how brands are using cultivar development to create differentiation rather than relying only on Damascena origin claims. Rosa Centifolia still holds an important premium niche in fragrance and personal care, so the rose water market is likely to keep a three-layer structure with volume in Damascena, growth in Gallica, and selective high-end demand in Centifolia.

By Nature: Conventional Supply Holds Scale While Organic Gains Premium Momentum

Conventional rose water held 65.48% of the market in 2025, supported by cost advantages in food use and economy personal care lines. That scale means conventional supply still anchors the daily volume needs of the rose water market across price-sensitive channels. Culinary applications and mass skincare continue to absorb large volumes because certification is less critical in these formats than in premium beauty retail. For many mainstream buyers, stable price and acceptable aroma remain more important than formal organic status. The conventional side of the rose water industry is therefore likely to keep its volume base even as premium demand continues to move in a different direction.

Organic rose water is projected to grow at 8.55% CAGR through 2031, making it the fastest-growing nature segment in the rose water market size profile. The driver is not only consumer preference but also retailer listing standards that increasingly reward documented clean-chain provenance. This is raising the commercial value of traceability, smaller batch control, and certification readiness across the rose water market. It also creates stronger entry barriers for suppliers that cannot document origin, processing, and compliance with the same consistency. The result is a split where the conventional product keeps broader reach, while organic supply captures a larger share of premium account growth in the rose water industry.

By End Use: Cosmetics Anchors Demand While Food and Beverages Broadens Use Cases

Cosmetics and personal care accounted for 54.78% of the rose water market share in 2025, making it the largest end-use segment. That lead comes from steady use in toners, facial mists, cleansing waters, and newer serum-mist hybrids. The segment remains the core demand anchor in the rose water market because it absorbs most certified hydrosol output. It also gives producers a path to higher margins when functional efficacy and ingredient origin both matter to formulation claims. As clean-label beauty expands, this category is likely to remain the main setting where rose water is expected to perform as both a sensory and active ingredient.

Food and beverages are forecast to expand at 8.32% CAGR through 2031, placing it as the fastest-growing end-use area in the rose water market size outlook. The case for expansion is getting stronger as research supports antimicrobial performance and broader use in bakery, seafood, meat, and active packaging applications. This gives the rose water market a second growth engine that is less tied to beauty cycles and more connected to premium flavor and preservation value. It also helps the ingredient reach consumers through everyday eating and drinking formats, which can reinforce familiarity across categories. The smaller others segment, which includes medicinal, spa, and aromatherapy uses, continues to add steady niche demand where therapeutic botanical positioning remains relevant.

By Distribution Channel: Physical Retail Keeps Scale While Online Retail Accelerates Reach

Supermarkets and hypermarkets held a 42.38% share in 2025, which kept them as the largest distribution route for the rose water market. Their strength comes from broad household reach and the ability to carry both mass and mid-premium products in the same aisle. This channel still matters because it supports scale, repeat purchase, and cross-category visibility for established brands. It also gives price-sensitive shoppers easy access to entry-level products, which helps maintain category breadth. Health and beauty stores remain important where premium organic portfolios need staff explanation, ingredient storytelling, and curated shelf placement.

Online retail is expected to grow at 9.02% CAGR through 2031, making it the fastest-growing channel in the rose water market size by distribution. Digital commerce shortens the path between small-batch distillers and end users, which helps newer brands gain visibility without matching physical shelf investment. The rose water market also benefits from simple ingredient communication online because single-ingredient and low-ingredient products are easier to explain in search and social formats. Heritage Store's April 2026 launch of new 12 oz. Rosewater and Rosewater & Glycerin facial mists across its own website, Amazon, and TikTok Shop shows how established brands are directing incremental growth through digital-first routes. As online discovery expands, the rose water industry is likely to see stronger competition in search, social commerce, and direct-to-consumer repeat sales.

Geography Analysis

Europe held 34.28% of the rose water market in 2025, which made it the largest regional base. The region's position rests on deep demand in Germany, France, the UK, and the Benelux, where buyers place high value on certified botanical ingredients. Compliance expectations under the EU Cosmetics Regulation continue to support stricter ingredient documentation and traceability across the regional rose water market. That environment helps maintain stronger pricing for certified hydrosols than is typical in less regulated markets. It also encourages personal care manufacturers to narrow supplier lists toward pre-validated sources with stronger dossier support.

Asia-Pacific is projected to grow at 8.78% CAGR through 2031, making it the fastest-expanding regional segment in the rose water market. India combines established cultural use in Ayurvedic practice, religious rituals, and household skincare with a growing domestic production base that supports wider commercial use. China is adding demand through premium skincare imports and rising consumer familiarity with botanical ingredients in functional beauty formats. Japan and South Korea strengthen the regional premium mix because minimalist multi-benefit routines fit well with rose water in essence, mist, and sheet mask applications.

North America, South America, and the Middle East and Africa round out the global footprint with distinct demand profiles in the rose water market. North America shows strong potential for clean-label and digital commerce positioning, especially where ingredient simplicity supports direct-to-consumer communication. The Middle East retains a natural demand base through culinary traditions and is also developing premium personal care demand for alcohol-free and traceable formulations. South America remains smaller and earlier in development, but urban e-commerce growth is widening access to natural beauty products and related wellness formats.

Competitive Landscape

The competitive structure of the rose water market remains fragmented, with participation spread across regional distillers, Ayurvedic heritage brands, European organic houses, and digital-first skincare labels. No single company sets the pace globally, so differentiation depends more on sourcing credibility, product purity, distribution reach, and brand trust than on scale alone. This keeps entry possible for focused specialists, but it also makes consistent raw material access a critical advantage. Suppliers that can control cultivation, distillation, and documentation tend to be better placed in premium contracts across the rose water market. At the same time, companies that rely mainly on scent-led positioning face tighter competition from lower-cost reconstituted alternatives.

Jurlique provides one clear example of strategic differentiation through proprietary input development in the rose water market. The 2025 introduction of the Intense Rose, a Rosa Gallica hybrid developed with breeder George Thomson and grown on the brand's biodynamic farm in South Australia's Adelaide Hills, shows how cultivar exclusivity can support brand separation. Heritage Store offers a second example, with its April 2026 launch of larger-format Rosewater and Rosewater & Glycerin facial mists across owned digital channels and large online marketplaces. That move reflects a channel strategy built around repeat use, visibility, and faster consumer acquisition in online formats. Product and channel choices therefore remain as important as raw material quality in shaping competitive outcomes across the rose water market.

Competition in Europe also depends heavily on origin and certification narratives, especially where brands sell into premium natural beauty accounts. Bulgarian supply pressure adds another layer because reduced harvests can strengthen pricing power for verified producers while increasing procurement risk for buyers. This leaves room in the rose water market for suppliers that can offer halal-certified, pharmaceutical-grade, or tightly documented organic product without depending on a single origin. Over the forecast period, the strongest positions are likely to remain with companies that combine trusted sourcing, product clarity, and flexible channel execution.

Rose Water Industry Leaders

Dabur India Ltd.

ALTEYA ORGANICS

Poppy Austin Limited

The Estée Lauder Companies

Patanjali Ayurved Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Heritage Store launched a new 12 oz. Rosewater and Rosewater & Glycerin facial mists are available simultaneously across its own website, Amazon, and TikTok Shop. The expanded format, featuring an upgraded micro-mister sprayer, targets high-frequency daily-use consumers and represents the brand's first deliberate multi-platform social commerce integration for its flagship rose water line.

- February 2026: Jurlique launched a limited-edition Rose Iconic Duo gift set comprising the Rosewater Balancing Mist and a hand cream in Japan, timed for the Valentine's Day retail window. The Japan launch reflects a deliberate pivot toward high-value gifting occasions in Asia-Pacific's premium skincare segment and was supported by exclusive retail partnerships.

- June 2025: Sharjah unveiled its first successful locally produced rose water, extracted from Mohammadi and Taifi roses cultivated within the emirate. The product was showcased at the Sharjah Products Exhibition held at Al Dhaid University and reflects the region’s growing focus on agricultural innovation, food security, and value-added local production.

Global Rose Water Market Report Scope

| Rosa Gallica |

| Rosa Centifolia |

| Rosa Damascene |

| Organic |

| Conventional |

| Food and Beverages |

| Cosmetics and Personal Care |

| Others (medicinal use, spa and aromatherapy) |

| Supermarkets/Hypermarkets |

| Health & Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| Type | Rosa Gallica | |

| Rosa Centifolia | ||

| Rosa Damascene | ||

| Nature | Organic | |

| Conventional | ||

| End Use | Food and Beverages | |

| Cosmetics and Personal Care | ||

| Others (medicinal use, spa and aromatherapy) | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Health & Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the rose water market by 2031?

The rose water market is forecast to reach USD 678.95 million by 2031, rising from USD 495.83 million in 2026 at a 7.14% CAGR.

Which product type leads global demand for rose water?

Rosa Damascena led demand with a 44.23% share in 2025 because of its recognized aroma profile and its association with established producing regions.

Which end-use area is growing fastest for rose water?

Food and beverages is the fastest-growing end-use segment, with an 8.32% CAGR through 2031, supported by flavor and antimicrobial use cases.

Why does Europe lead rose water consumption?

Europe held a 34.28% share in 2025 because demand is supported by strong preference for certified botanical ingredients and stricter traceability expectations.

Page last updated on: