Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.14 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 9.26% CAGR |

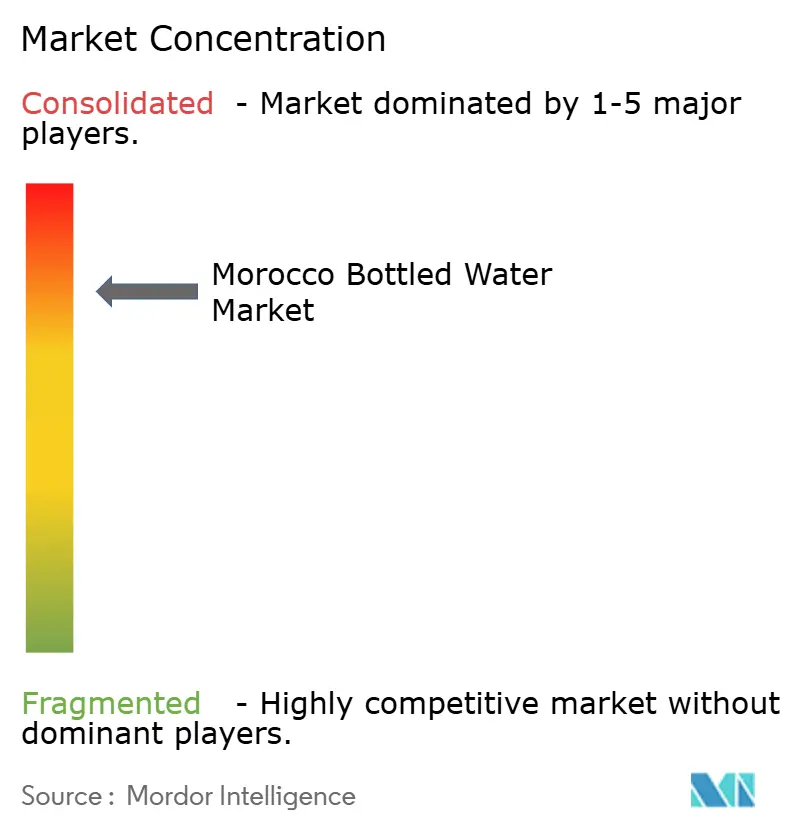

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Morocco Bottled Water Market Analysis by Mordor Intelligence

The Morocco bottled water market size is expected to grow from USD 1.14 billion in 2025 to USD 1.25 billion in 2026 and is forecast to reach USD 1.95 billion by 2031 at 9.26% CAGR over 2026-2031. Consumers in Morocco are increasingly aware of water scarcity, urbanization is advancing rapidly, and tourism is recovering at an accelerated pace, all of which are driving strong demand for packaged hydration solutions. Still water continues to dominate the market; however, sparkling and functional water variants are steadily capturing market share as consumers actively seek products that offer both refreshment and perceived health benefits. In major cities, brands are driving premiumization by highlighting factors such as mineral provenance, sustainable packaging, and strong branding to justify higher price points. Organized retail channels and the expanding e-commerce ecosystem are actively broadening distribution networks, increasing brand visibility, and enhancing consumer convenience.

Key Report Takeaways

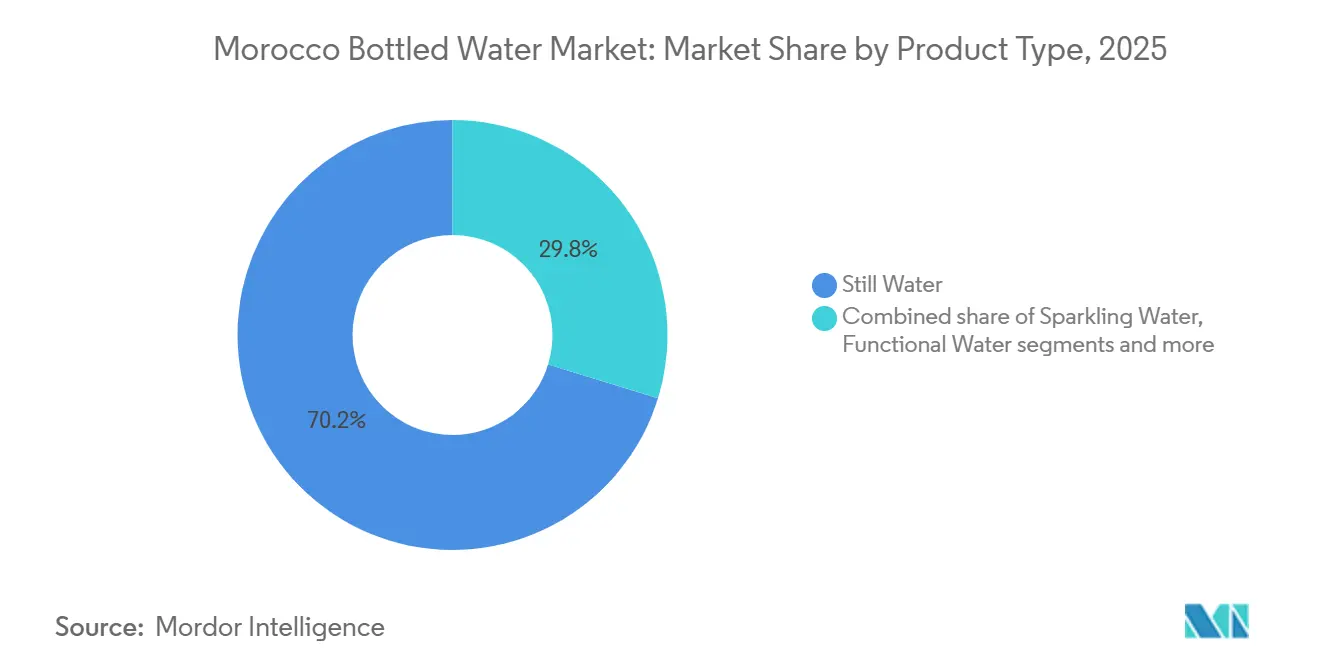

- By product type, still water led with 70.24% revenue share in 2025, while sparkling water is advancing at a 9.88% CAGR through 2031.

- By price point, the mass segment accounted for 82.52% of the Morocco bottled water market share in 2025; premium products are forecast to expand at a 10.59% CAGR to 2031.

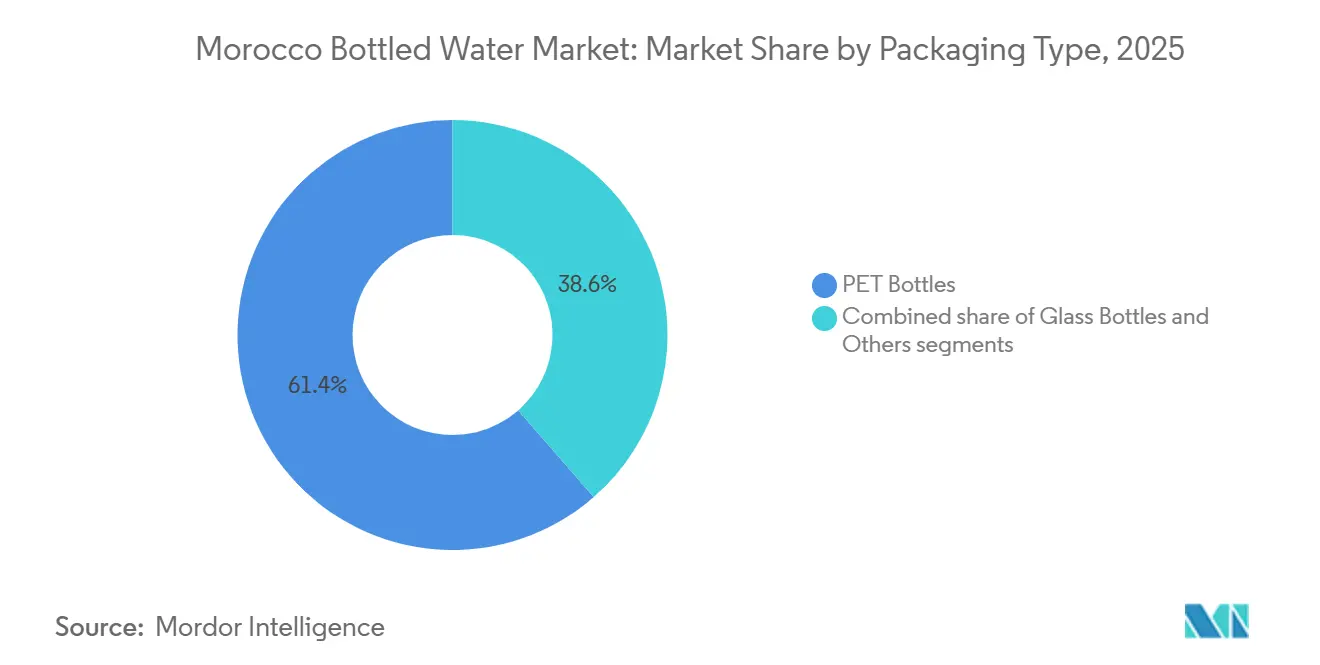

- By packaging, PET formats captured 61.41% of the Morocco bottled water market size in 2025, whereas glass bottles are growing fastest at 10.26% CAGR.

- By distribution, off-trade channels held 73.83% share in 2025, and on-trade venues are projected to rise at a 10.75% CAGR during the outlook window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer awareness of water scarcity issues | +1.8% | National, with acute impact in Casablanca, Rabat, Marrakech, Fès | Medium term (2-4 years) |

| Growing urbanisation supporting demand for convenient, on-the-go consumption | +1.5% | Urban centres: Casablanca, Rabat, Tangier, Marrakech | Long term (≥ 4 years) |

| Rising tourist arrivals increasing demand for portable hydration solutions | +1.2% | Coastal and heritage destinations: Marrakech, Agadir, Casablanca, Tangier | Short term (≤ 2 years) |

| Expansion of organised retail formats and e-commerce distribution infrastructure | +1.4% | Urban agglomerations with modern retail penetration | Medium term (2-4 years) |

| Rising concerns regarding the safety and quality of tap water | +2.1% | National, concentrated in Rabat-Salé-Kenitra, coastal aquifers, and drought-affected regions | Short term (≤ 2 years) |

| Increasing environmental awareness encouraging sustainable consumption preferences | +0.9% | Urban middle-income and premium segments; hospitality sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer awareness of water scarcity issues

Increasing consumer awareness of water scarcity issues is a key driver of the Morocco bottled water market, as limited water availability is reshaping consumption patterns across the country. Reservoirs reached critically low levels in 2024, with an average filling rate of just 23.17%, marking a significant decline of nearly 8%, or over 1.3 billion cubic meters of water, compared to the same period the previous year[1]Source: General Directorate of Water, "Morocco's Looming Thirst Crisis", carnegieendowment.org. This shortage has heightened public concern about access to safe and reliable drinking water, prompting consumers to rely more heavily on bottled water for daily hydration. Awareness campaigns, media coverage, and government advisories have further reinforced the importance of safe drinking water. Urban populations, particularly in areas experiencing higher demand and lower supply, are increasingly prioritizing bottled water for convenience and reliability. The trend is also reflected in rural regions, where access to treated water is inconsistent, driving consistent bottled water consumption.

Growing urbanisation supporting demand for convenient, on-the-go consumption

Growing urbanization is a major driver of the Morocco bottled water market, as it supports increasing demand for convenient, on-the-go consumption. Urban lifestyles, characterized by longer work hours, commuting, and active social engagement, have heightened the need for portable hydration solutions. According to the World Bank, Morocco’s urbanization rate reached 66% in 2024, reflecting a steadily expanding urban population[2]Source: World Bank, "Urban population (% of total population) - Morocco", data.worldbank.org. This demographic shift has led to higher adoption of bottled water in offices, public transport, retail outlets, and recreational spaces. The convenience and ready availability of bottled water cater directly to busy city consumers who prioritize safety, hygiene, and accessibility. Retail expansion, including supermarkets, convenience stores, and e-commerce channels in urban areas, further facilitates consumption. Consequently, urbanization continues to reinforce the market’s growth, positioning bottled water as a key everyday product for Morocco’s increasingly urban population.

Rising tourist arrivals increasing demand for portable hydration solutions

Rising tourist arrivals are driving increased demand for portable hydration solutions, making it a key growth driver for the Morocco bottled water market. Tourists, particularly those visiting urban centers and popular destinations, rely heavily on convenient and safe drinking water during travel, sightseeing, and outdoor activities. Morocco recorded a record 19.8 million tourist arrivals in 2025, marking a 14 % increase over 2024, according to the Ministry of Tourism, highlighting the growing influx of visitors[3]Source: Ministry of Tourism, “Morocco Tourist Arrivals Hit Record 19.8 Million in 2025”, mtaess.gov.ma.This surge in tourism amplifies consumption of bottled water in hotels, restaurants, cafes, and retail outlets catering to travelers. Portable and single-serve bottled water meets the needs of on-the-go tourists seeking hygiene, convenience, and reliability. Seasonal peaks and tourism-driven demand also support sustained sales growth, especially in coastal and cultural hotspots. As a result, the expanding tourism sector continues to reinforce market opportunities for bottled water manufacturers in Morocco.

Expansion of organised retail formats and e-commerce distribution infrastructure

Morocco's bottled water market is experiencing significant growth, largely fueled by the rise of organized retail and e-commerce logistics networks. The expansion of organized retail chains spanning supermarkets, hypermarkets, and convenience stores has broadened the accessibility of bottled water to a wider consumer audience. These outlets not only offer a diverse range of bottled water options, catering to varied consumer tastes, but also boost overall sales. Concurrently, the swift evolution of e-commerce platforms has optimized the distribution process, allowing consumers the convenience of online bottled water purchases. Features like doorstep delivery, subscription models, and enticing discounts on e-commerce platforms have further nudged consumers towards online buying. These logistical advancements have bolstered supply chain efficiency, shortened delivery times, and ensured steady product availability, all contributing to the market's expansion. Moreover, the adoption of cutting-edge technologies, including real-time tracking and sophisticated inventory management systems, has significantly boosted the operational efficiency of both organized retail and e-commerce logistics networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity among rural populations and lower-income consumers | -1.3% | Rural areas and peri-urban low-income households nationwide | Medium term (2-4 years) |

| Growing environmental concerns related to plastic packaging waste | -0.8% | Urban centres with higher environmental awareness; hospitality sector | Long term (≥ 4 years) |

| Difficulties in maintaining consistent product quality standards | -0.5% | National, with heightened risk in regions with groundwater contamination | Short term (≤ 2 years) |

| Intense competition from tap water and household filtration alternatives | -0.7% | Urban areas with improved municipal supply; middle-income households | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High price sensitivity among rural populations and lower-income consumers

Morocco's rural population, while diminishing in proportion, remains sizable and is notably price-sensitive, complicating market penetration efforts. Rural households allocate a large chunk of their income to essentials like food, housing, and utilities, leaving scant disposable income for non-essentials such as bottled water. Consequently, bottled water is often viewed as a luxury, especially during economic downturns or agricultural slumps. Thanks to government-led initiatives like improved road connectivity and electrification, access to remote areas has surged, allowing bottled water companies to broaden their marketing horizons. Yet, these efforts fall short of bridging the income gaps in rural locales, which still curtail the affordability and uptake of bottled water. Moreover, the seasonal ebb and flow of agricultural income in these regions results in pronounced purchasing power fluctuations. This cyclical income variability translates to erratic demand, posing challenges for distribution planning and inventory management for bottled water companies, which must navigate these inconsistencies to ensure smooth operations.

Growing environmental concerns related to plastic packaging waste

In Morocco, urban and educated segments are increasingly scrutinizing packaging sustainability, reflecting a heightened awareness of environmental issues. This shift in consciousness is fueling a demand for eco-friendly packaging, with consumers favoring products that resonate with sustainable practices. The tourism sector, shaped by international visitor expectations and global certification standards, faces mounting pressure to embrace sustainable packaging. Yet, these eco-friendly solutions often come at a premium, potentially squeezing profit margins or limiting product availability, posing challenges for businesses. On the regulatory front, the Moroccan government is taking decisive steps to tackle environmental challenges. With reforms in waste management and the formation of environmental police forces, the government is hinting at stricter regulations, especially against single-use plastics. Such measures could upend conventional packaging practices, compelling businesses to pivot and invest in greener alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Variants Disrupt Still Dominance

Still water accounted for a dominant 70.24% market share in Morocco in 2025, reflecting long-established hydration habits and price-conscious consumption patterns among Moroccan consumers. Its widespread acceptance is largely driven by its familiarity as the primary everyday beverage for hydration across different income groups. The segment benefits from affordability and broad availability through supermarkets, convenience stores, and rural retail outlets, making it accessible to a wide consumer base. Consumer preference for still water also aligns with cultural and dietary practices that emphasize natural and minimally processed beverages, strengthening trust and regular consumption. In addition, well-developed distribution networks ensure consistent product availability, particularly in less urbanized regions where alternative bottled water options may be limited by pricing or accessibility.

In contrast, sparkling water, while holding a smaller share of the market, represents the fastest-growing segment, projected to expand at a CAGR of 9.88% through 2031. Growth in this category is driven by changing consumer lifestyles and increasing urbanization, which are influencing evolving beverage preferences. Greater exposure to global consumption trends through tourism, media, and social influences has contributed to rising acceptance of sparkling water, particularly among younger and higher-income consumers. The segment also benefits from growing health awareness, as consumers increasingly seek alternatives to sugary soft drinks and conventional beverages. Its novelty, premium positioning, and availability in diverse flavors further enhance consumer interest.

By Price Point: Premium Gains as Mass Holds Volume

In 2025, the Mass segment accounted for a commanding 82.52% of the market value, highlighting the stronghold of economy-priced formats. This dominance comes as no surprise, given that the average monthly net salary hovers around MAD 4,451.32 (roughly USD 410) and rural households in Morocco lean towards essential staples over luxury purchases. On the other hand, premium formats are set to chart a robust growth trajectory, with a projected CAGR of 10.59% through 2031. This surge is fueled by urbanization, a booming tourism sector, and the rising perception of glass-bottled mineral waters as luxury items. Sidi Ali is capitalizing on this trend, offering 750-millilitre and 500-millilitre glass bottles at premium prices in on-trade channels. Meanwhile, Aïn Saïss has rolled out a uniquely designed glass bottle, inspired by Moroccan tiles, targeting both heritage-conscious consumers and hospitality operators. The Moroccan market is also seeing a presence of imported premium brands like Acqua Panna, Vichy Catalan, and Mondariz, which are strategically catering to expatriates, upscale restaurants, and luxury hotels in key cities like Marrakech, Casablanca, and Tangier.

The swift rise of the Premium segment underscores a significant shift among urban middle-income households. These households are increasingly viewing bottled water not just as a beverage, but as a symbol of wellness, quality sourcing, and sustainability. Les Eaux Minérales d'Oulmès, a key player in the market, reported a notable revenue of MAD 1,002.9 million in Q3 2025, marking a 10.3% increase from the previous year. Their Vitalya functional water range stands as a testament to their strategy: focusing on innovation for higher margins rather than chasing volume. Yet, despite the Premium segment's growth, the Mass segment is poised to maintain its dominance. This is largely due to the price-sensitive nature of rural and peri-urban households, which make up about 40% of Morocco's population, and their limited exposure to premium branding. Producers eyeing the Premium segment are channeling investments into glass packaging, storytelling rooted in heritage, and distribution in on-trade venues.

By Packaging Type: Glass Accelerates as PET Dominates

The PET bottle segment holds a commanding 61.41% share of the packaging market in 2025 within Morocco’s bottled water industry, driven by multiple practical and economic factors. Its dominance is closely tied to the material’s cost efficiency, which makes it an ideal choice for mass production and distribution across urban and rural areas alike. PET bottles offer significant logistical advantages they are lightweight, minimizing transportation costs and emissions, and shatterproof, enhancing product safety during handling and transport. Additionally, Moroccan consumers are familiar and comfortable with PET packaging, which supports convenience, particularly in fast-paced, mobile consumption settings such as on-the-go drinking. The prevalent use of PET aligns well with the realities of Morocco’s distribution infrastructure, which requires packaging that can withstand varying transport conditions while remaining affordable and accessible.

In contrast, the glass bottle segment represents the fastest-growing packaging category, expanding at a robust CAGR of 10.26% through 2031. This growth is largely fueled by increasing awareness and concern around environmental sustainability, as glass is recognized for its recyclability and premium, eco-friendly attributes. Moroccan consumers, especially in urban and tourist-centric areas, are gravitating towards glass bottled water for its perceived higher quality, purity, and alignment with a more sustainable lifestyle. The tourism sector notably favors glass bottles, often associating them with luxury and exclusivity traits that appeal to international and affluent consumers. Manufacturers leverage this perception by positioning glass bottles as premium packaging, offering opportunities for differentiation in a crowded market. Additionally, government regulations and industry initiatives promoting environmental responsibility encourage the adoption of sustainable packaging, giving further impetus to glass bottle growth.

By Distribution Channel: On-Trade Surges as Off-Trade Holds Base

In 2025, off-trade distribution channels dominated Morocco's bottled water market, capturing a notable 73.83% share. This significant share highlights Morocco's evolving retail landscape, where consumers are leaning towards bulk purchases and home consumption rather than immediate consumption on-the-go. Off-trade channels span a variety of retail formats, from traditional souks and modern supermarkets to hypermarkets and the swiftly expanding e-commerce platforms. These channels adeptly cater to both urban and rural consumers, ensuring widespread accessibility and convenience. The variety within off-trade channels allows consumers to select bottled water in pack sizes that best suit their household needs. Furthermore, as retail formats across Morocco expand and modernize, these channels play a pivotal role in bolstering bottled water sales and penetrating areas that were previously underserved.

On the other hand, on-trade distribution channels, which encompass hotels, restaurants, cafes, and other hospitality venues, are witnessing the fastest growth. Expanding at a robust CAGR of 10.75% through 2031, this surge is largely attributed to the post-pandemic rebound of the tourism sector and ongoing urbanization, both fueling the demand for bottled water outside the home. With Morocco enhancing its hospitality and leisure infrastructure—especially in prime tourist spots like Marrakech, Casablanca, and Agadir—the uptick in bottled water consumption at these venues is evident. Both tourists and urban professionals gravitate towards bottled water for its convenience and perceived health safety, amplifying the significance of this distribution channel. Moreover, on-trade venues are seizing the opportunity to offer premium options, such as flavored or sparkling bottled water, enriching their service experience and propelling the segment's growth.

Geography Analysis

The market is geographically influenced by variations in urbanization levels, climate conditions, and access to potable water infrastructure across regions. Major urban centers such as Casablanca, Rabat, and Marrakech account for a significant share of bottled water consumption due to higher population density, rising disposable incomes, and strong retail penetration. Increasing urban lifestyles and on-the-go consumption patterns continue to support steady demand in metropolitan areas. In addition, concerns regarding tap water quality in certain locations encourage consumers to rely on packaged drinking water for daily hydration. Coastal and tourism-driven regions also contribute meaningfully to sales, supported by hospitality and foodservice sector demand. Strong distribution networks enable manufacturers to maintain product availability across both modern retail and traditional trade channels.

Rural and semi-urban areas present a different consumption dynamic, where affordability and accessibility strongly influence purchasing behavior. Still water dominates these regions due to its lower price point and suitability for everyday consumption among price-sensitive consumers. Distribution through small retail outlets and local supply chains plays a crucial role in expanding market reach beyond major cities. Seasonal demand fluctuations are also evident, with higher consumption during warmer months due to Morocco’s hot climate and increasing hydration needs.

Government initiatives aimed at improving water infrastructure may gradually influence consumption patterns, although bottled water remains a trusted alternative in many areas. Furthermore, growing awareness of health and hygiene is encouraging gradual market expansion across smaller towns. Overall, geographic diversity in consumer preferences and infrastructure continues to shape bottled water demand across the country.

Competitive Landscape

.The market is consolidated, with international players dominating the competitive landscape. Companies like Nestlé Waters Maroc, Danone's Aïn Saïss, and Coca-Cola's Ciel and BonAqua actively leverage their global expertise, extensive distribution networks, and well-established brand equity to maintain their leadership. However, quality controversies recently associated with Nestlé's European operations have raised concerns about potential reputational damage. This situation creates opportunities for local competitors to capitalize on the uncertainty and strengthen their market positions.

Local brands in Morocco actively differentiate themselves by emphasizing their natural sourcing and cultural authenticity. They appeal to consumers who prioritize tradition and local identity. In contrast, international players focus on delivering consistent quality, driving product innovation, and positioning their offerings as premium choices. These contrasting strategies highlight the diverse approaches market participants use to secure consumer loyalty. Additionally, the fragmented nature of the market allows niche players to emerge. These smaller players target specific consumer segments by employing tailored distribution strategies and localized marketing efforts that align with regional preferences, enabling them to carve out a competitive space.

Although technology adoption in the market remains limited, companies are gradually integrating digital marketing and e-commerce into their strategies to gain a competitive edge. These advancements are particularly effective among younger urban consumers, who show higher levels of brand experimentation and digital engagement. By actively utilizing digital platforms, companies can expand their reach and appeal to this tech-savvy demographic, further intensifying competition. As competitive dynamics continue to evolve, market players must adapt to shifting consumer behaviors and leverage emerging technologies to secure a sustainable competitive advantage.

Morocco Bottled Water Industry Leaders

-

Les Eaux Minérales d’Oulmès SA

-

Nestlé S.A.

-

The Coca-Cola Company

-

PepsiCo, Inc.

-

Danone SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Equatorial Coca‑Cola Bottling Company (ECCBC) inaugurated two new production lines at its Nouaceur (Casablanca) plant following a MAD715 million investment. These new lines are dedicated to producing both carbonated soft drinks and bottled water, and the expansion is expected to increase the factory’s annual production capacity by approximately 40%.

- May 2025: ACCIONA, along with Green of Africa (holding a 45% stake) and AfriquiaGaz (holding 5%), has initiated the financing and construction of the Casablanca desalination plant located in Sidi Rahal, near Casablanca, Morocco. This project aims to establish Africa's largest desalination facility, which will also become the first in the world to operate entirely on renewable energy. The plant will utilize wind power generated by the 360MW Bir Anzarane wind farm. Upon completion, the facility will produce 300 million cubic meters of drinking water annually.

- May 2025: Morocco and the UAE have signed a USD 14 billion investment agreement, which represents the largest private investment in Morocco's history. This landmark deal focuses on developing water and energy infrastructure, including seawater desalination plants capable of producing a combined 900 million cubic meters of water annually. The agreement underscores the commitment of both nations to address water scarcity and enhance energy infrastructure in the region.

Morocco Bottled Water Market Report Scope

Bottled water is water that is packaged in bottles or other containers for human consumption. The Morocco bottled water market is segmented by product type, price point, paclaging size and distribution channel. Based on product type, the market is segmented into still water, sparkling water, functional water and flavored water. Based on price point, the market is segmented into mass and premium. Based on packaging type, the market is segmented into PET Bottles, Glass Bottles and Others. Based on distribution channels, the market is segmented into off-trade and on-trade. Off-trade is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores and other distribution channels. The market sizing has been done in value terms in USD for all the above mentioned segments.

By Product Type

| Still Water |

| Sparkling Water |

| Functional Water |

| Flavored Water |

By Price Point

| Mass |

| Premium |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Others |

By Distribution Channel

| On Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Home and Office Delivery (HOD) | |

| Other Distribution Channels |

| By Product Type | Still Water | |

| Sparkling Water | ||

| Functional Water | ||

| Flavored Water | ||

| By Price Point | Mass | |

| Premium | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Others | ||

| By Distribution Channel | On Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Home and Office Delivery (HOD) | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the current value of the Morocco bottled water market?

The Morocco bottled water market size stands at USD 1.25 billion in 2026.

How large will Morocco’s bottled-water sales be by 2031?

Forecasts point to USD 1.95 billion, reflecting a 9.26% CAGR over 2026-2031.

Which segment is expanding fastest within Moroccan bottled water?

Sparkling water leads, advancing at a projected 9.88% CAGR through 2031 on the back of hospitality demand.

Will desalination projects curb bottled-water use?

Large coastal plants may trim at-home consumption after 2027 in Casablanca and Rabat, but tourism and on-the-go trends continue to lift overall demand.

Why is glass packaging gaining traction?

Urban consumers and premium hotels favor glass for sustainability and heritage cues, driving a 10.26% CAGR for glass bottles to 2031.

Page last updated on: